Sample Category Title

Crypto: Sentiment Recovering, Bitcoin Finds Support at Ever-Higher Levels

Market Overview

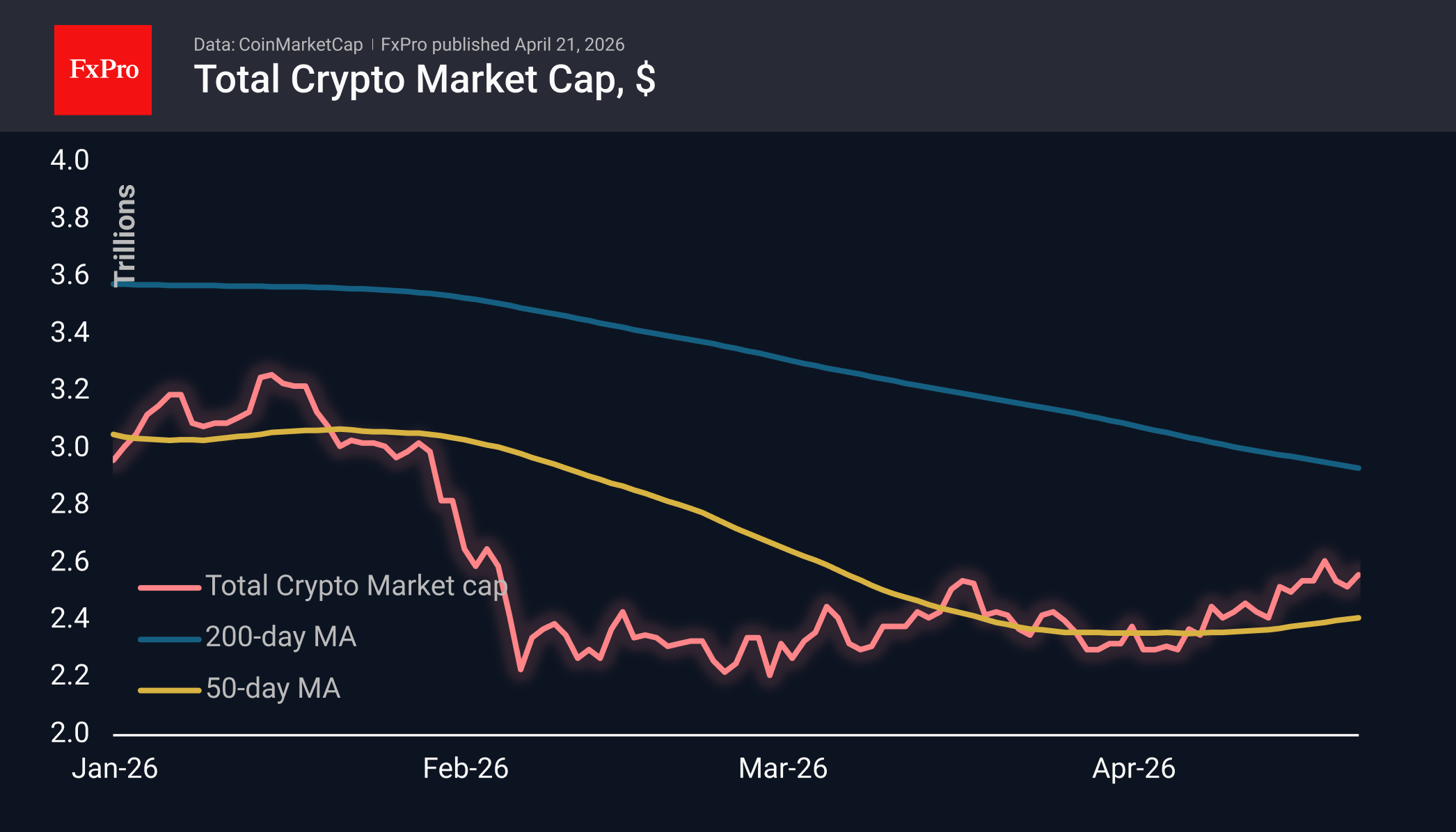

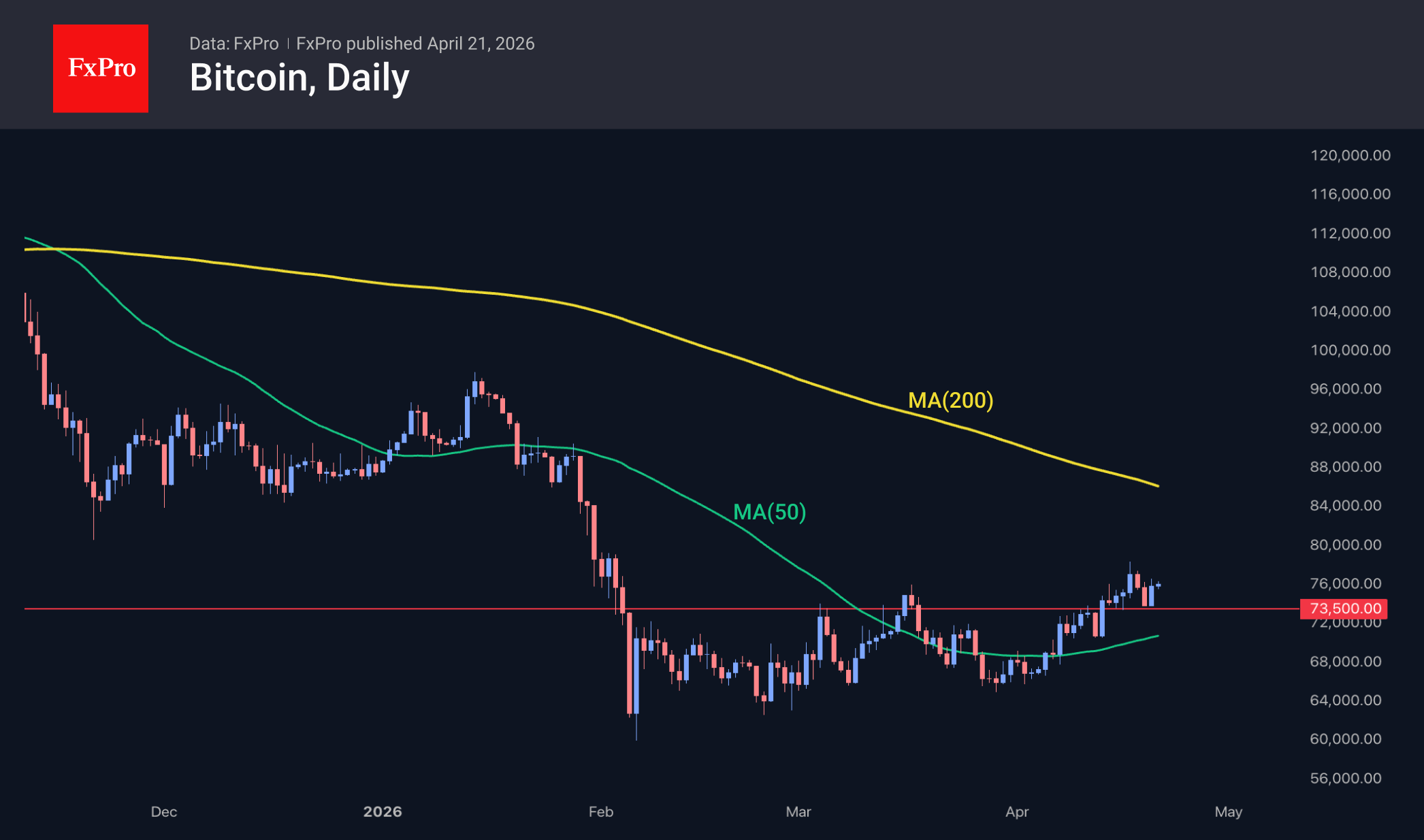

The crypto market cap rose by 2.52% over the past 24 hours to $2.56 trillion. Among the most liquid coins, the top gainers are Basic Attention Token (+7.7%), Immutable (+7.6%) and Toncoin (+5.9%). Lagging are Tron (−0.74%), Uniswap (−0.68%) and Algorand (+0.2%).

The sentiment index is continuing its recovery, rising to 33, its highest level since 19 January. This remains in fear territory but is now close to neutral levels.

Bitcoin is trading at $76K, having found support at March’s highs during yesterday’s intraday pullback. This classic transformation of resistance into support points to further positive momentum in the coming days towards $86K, where the 200-day moving average and the support zone from late last year are concentrated.

News Background

According to CoinShares, global investments in crypto funds rose by $1.401 billion last week, hitting their highest level since mid-January. Investments in Bitcoin increased by $1.116 billion, in Ethereum by $328 million, in Chainlink by $5 million, and in Sui by $2 million. Investments in XRP fell by $56 million, and in Solana by $2 million.

Bitcoin has consolidated above the realised price of short-term holders at around $69,400, notes analyst Darkfost. This helps restore confidence among traders who have recently entered the market and reduces the likelihood of their rapid capitulation.

65% of Japanese institutional investors use Bitcoin to diversify their portfolios, according to a survey by Japanese financial holding company Nomura. 31% of respondents view the market outlook positively. Most investors plan to allocate between 2% and 5% of their capital to crypto assets over the next three years.

Strategy has made its largest Bitcoin purchase since November 2024, acquiring 34,164 BTC for $2.54 billion at an average price of $74,395 per coin. Strategy now holds 815,061 BTC, purchased for $61.6 billion at an average price of $75,527 per Bitcoin.

Over the past week, BitMine has increased its purchases to 101,627 ETH. The company’s reserves have exceeded 4.97 million ETH, representing 4.12% of the Ethereum supply. ETH is showing resilience amid geopolitical instability and is in demand in AI and asset tokenisation, noted BitMine CEO Tom Lee.

Investors withdrew over $13 billion from DeFi protocols in two days following Saturday’s $292 million hack of the Kelp, liquid restaking protocol.

Pound Declines Amid Geopolitics and Political Risks

GBP/USD traded at 1.3515 on Tuesday as the US dollar strengthened. Pressure on the pound intensified at the start of the week following a sharp escalation of the US-Iran conflict, with markets fearing the breakdown of the truce and rotating into safe-haven assets.

The trigger was heightened tensions around the Strait of Hormuz. The US reported the detention of an Iranian vessel, while Tehran refused to participate in further negotiations. This development supported higher oil prices and boosted demand for the dollar.

An additional factor weighing on sterling is domestic UK politics. Prime Minister Keir Starmer has come under pressure following the scandal surrounding the appointment of Peter Mandelson as ambassador to the US. The market is watching his parliamentary address and assessing the risks of political instability.

Despite the current decline, the pound remains close to two-month highs and is up approximately 2% for the month. It had previously been supported by expectations of de-escalation in the Middle East. If political pressure on the government intensifies further, the pound could give back some of its recent gains.

Technical Analysis

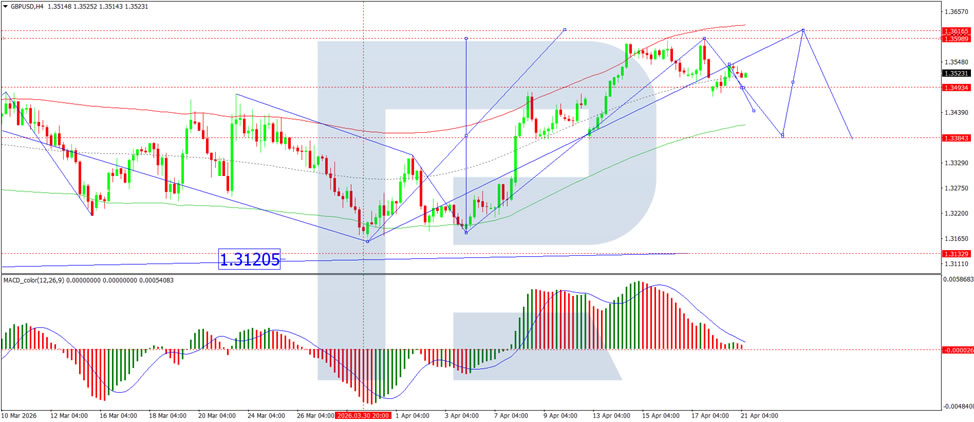

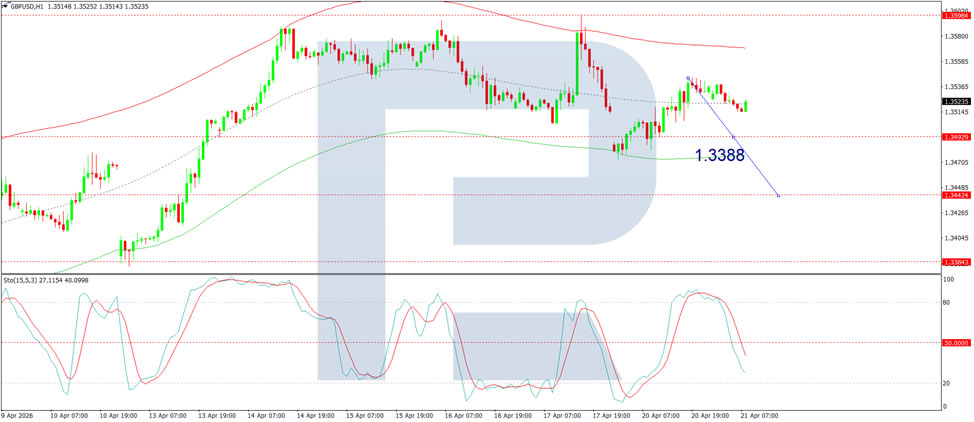

On the H4 GBP/USD chart, the market is forming a wide consolidation range above 1.3494, currently extending up to 1.3545. A move lower towards 1.3333 is likely in the near term. Following this correction, a new consolidation range is likely to form. An upside breakout would open potential for a continuation wave to 1.3611, while a downside breakout would suggest further movement to 1.3120. Technically, this scenario is confirmed by the MACD indicator, with its signal line above the zero level and pointing firmly downwards.

On the H1 chart, the market has formed a compact consolidation range around the 1.3515 level. A downside breakout could lead to a move towards 1.3444, followed by a possible rise to 1.3495. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line below the 20 level and pointing firmly downwards.

Conclusion

The pound has come under pressure as renewed US-Iran tensions around the Strait of Hormuz drive safe-haven demand for the dollar. At the same time, domestic political uncertainty adds an extra layer of risk. The detention of an Iranian vessel and Tehran's refusal to negotiate have revived energy supply concerns and pushed oil prices higher. Meanwhile, the scandal surrounding the UK ambassador appointment has put Prime Minister Starmer in a difficult position, with markets assessing the potential for political instability. Despite the current pullback, sterling remains near two-month highs, having gained 2% this month. However, technical indicators suggest further near-term downside, and the pound could give back more of its recent gains if geopolitical or political pressures intensify.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 214.36; (P) 214.73; (R1) 215.34; More...

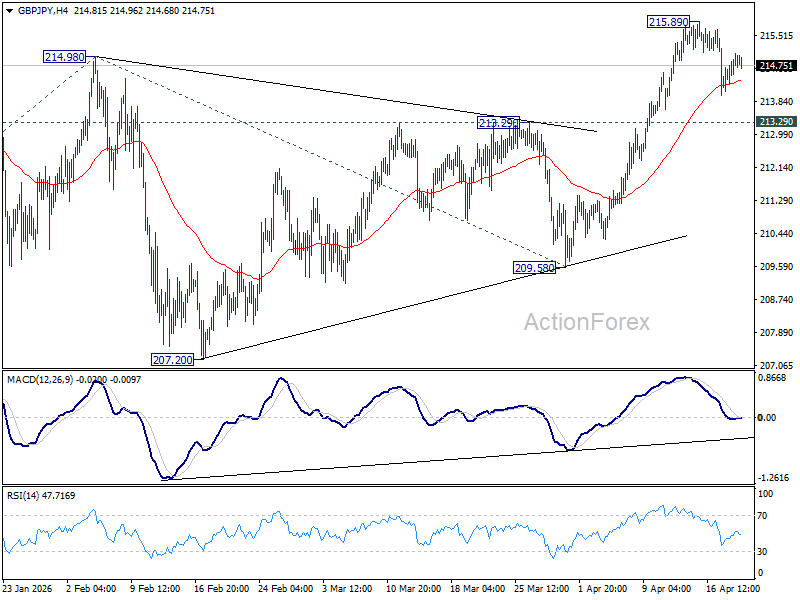

GBP/JPY is extending consolidations below 215.98 and intraday bias remains neutral. Further rise is expected as long as 213.29 resistance turned support holds. Firm break of 215.89 will resume larger up trend to 61.8% projection of 199.04 to 214.98 from 209.58 at 219.43.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 204.83) holds, even in case of another deep pullback.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 186.60; (P) 186.95; (R1) 187.57; More...

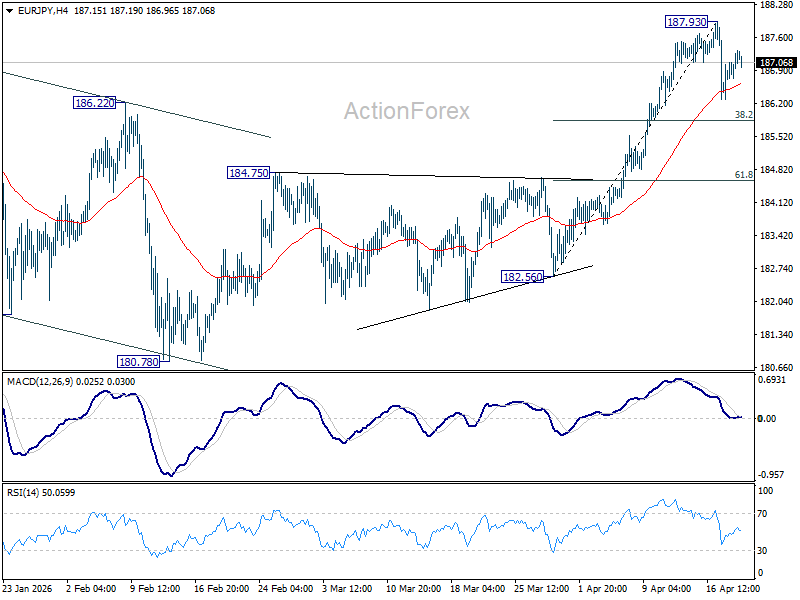

Intraday bias in EUR/JPY remains neutral and more consolidations could be seen below 187.93 short term top. Another fall might be seen to 38.2% retracement of 182.56 to 187.93 at 185.87. On the upside, though, break of 187.93 will resume larger up trend.

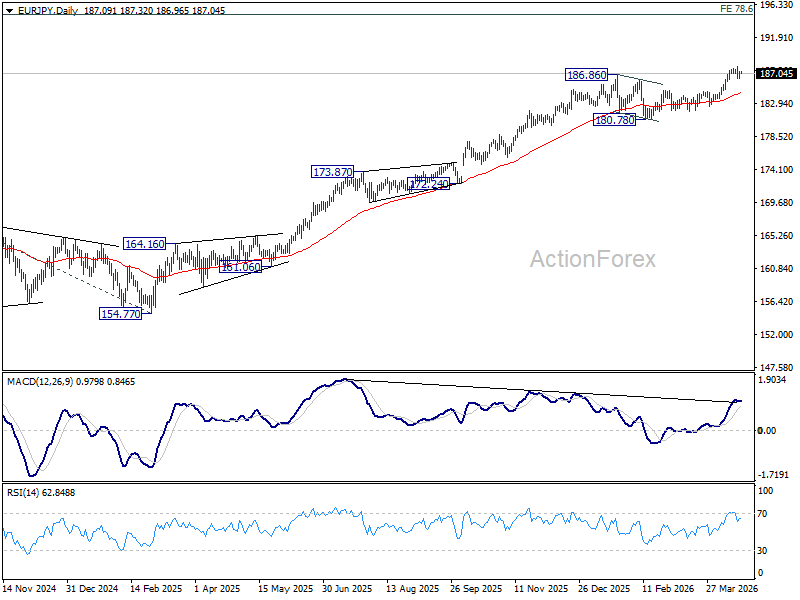

In the bigger picture, up trend from 114.42 (2020 low) is in progress Next target is 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. For now, medium term outlook will stay bullish as long as 180.78 support holds, even in case of deeper pullback.

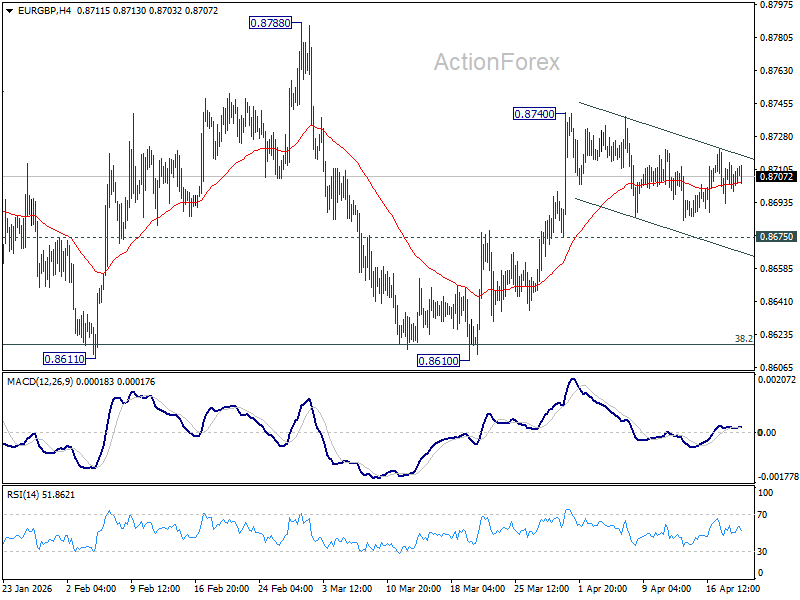

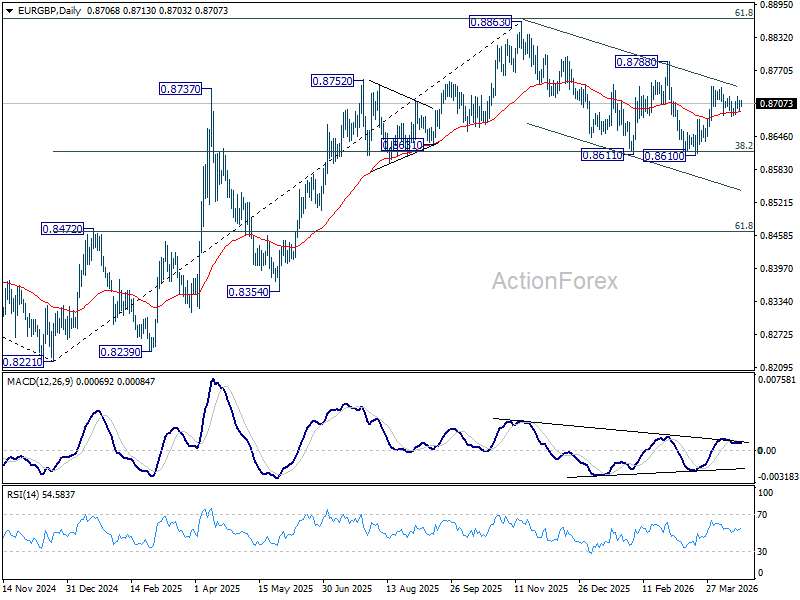

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8693; (P) 0.8710; (R1) 0.8719; More…

EUR/GBP is still extending the consolidation pattern form 0.8740 and intraday bias remains neutral. As long as 0.8675 support holds, further rise remains mildly in favor. On the upside, break of 0.8740 will resume the rally from 0.8610 to 0.8788 resistance. However, firm break of 0.8675 will turn bias back to the downside for retesting 0.8610 low instead.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be ready to resume through 0.8863 (2025 high). Nevertheless, sustained trading below 0.8618 should confirm bearish reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

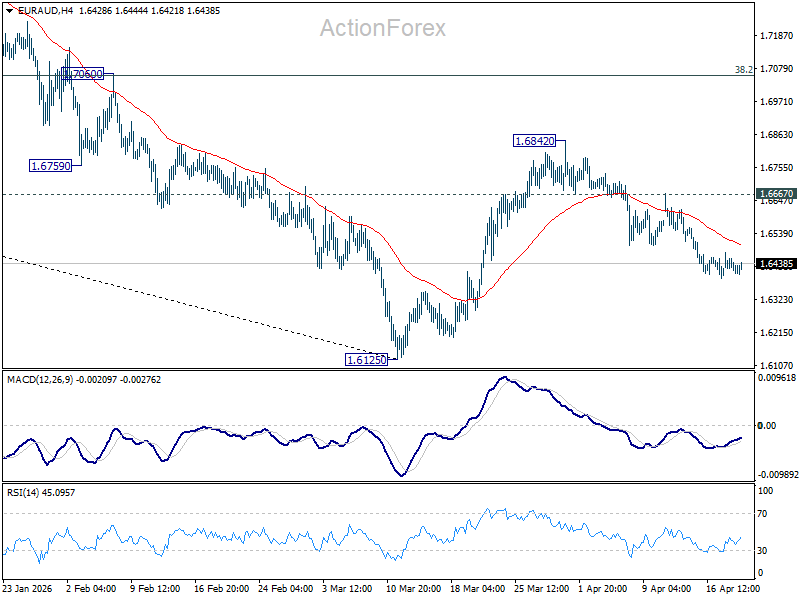

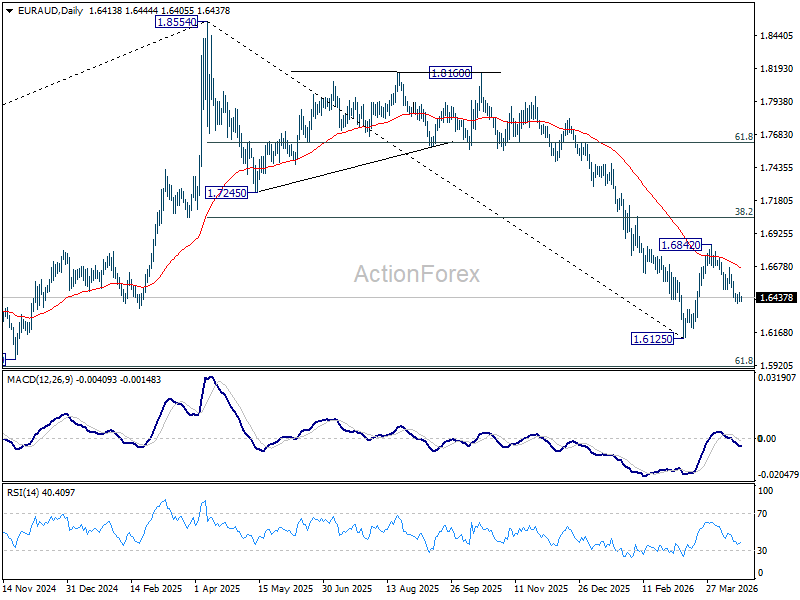

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6394; (P) 1.6440; (R1) 1.6467; More...

Despite loss of downward momentum, further fall is still expected in EUR/AUD with 1.6667 resistance intact. Decline from 1.6842 should target a retest on 1.6125 low. Firm break there will resume whole down trend from 1.8554 to 1.5913 fibonacci level next. However, break of 1.6667 will turn bias back to the upside for 1.6842 resistance instead.

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7131) holds, even in case of strong rebound.

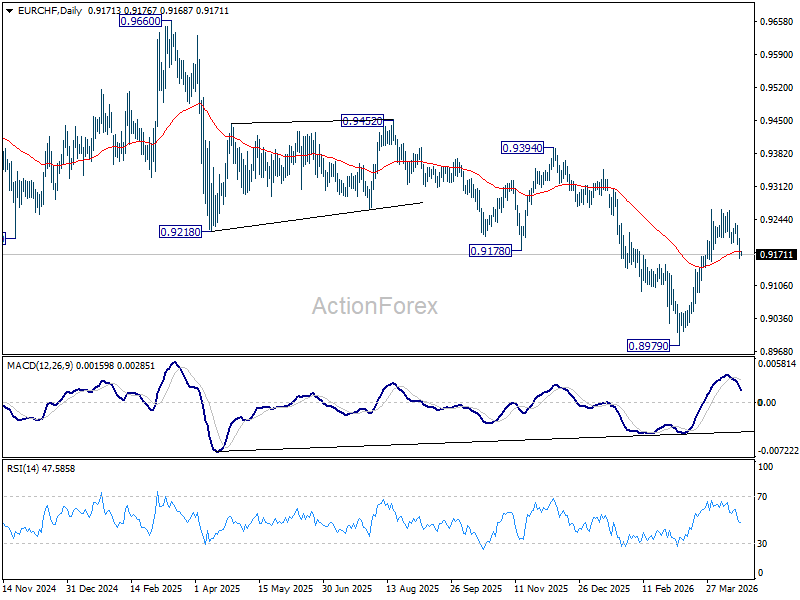

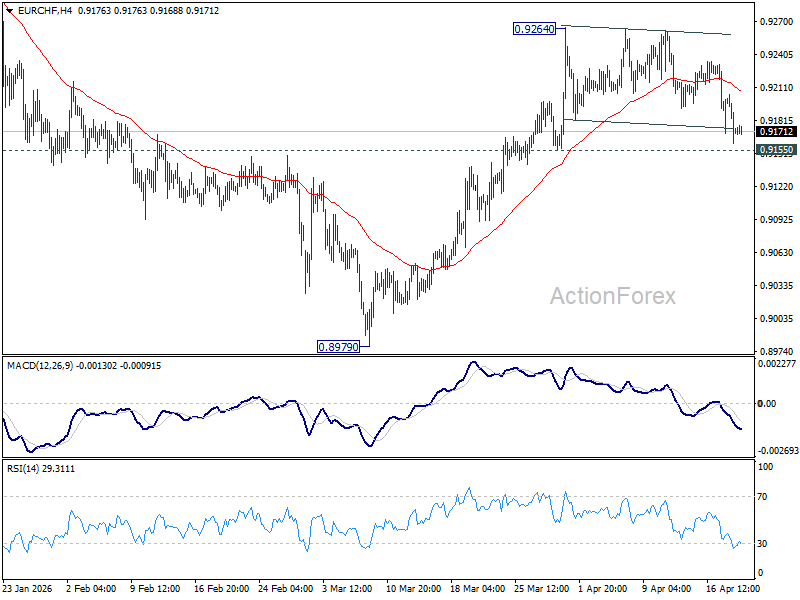

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9156; (P) 0.9183; (R1) 0.9202; More....

EUR/CHF is still holding inside range of 0.9155/9264. Intraday bias remains neutral and further rise is in favor. Firm break of 0.9264 will resume the rise from 0.8979 to 0.9394 resistance next. However, break of 0.9155 will turn bias back to the downside for deeper pullback.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9280) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

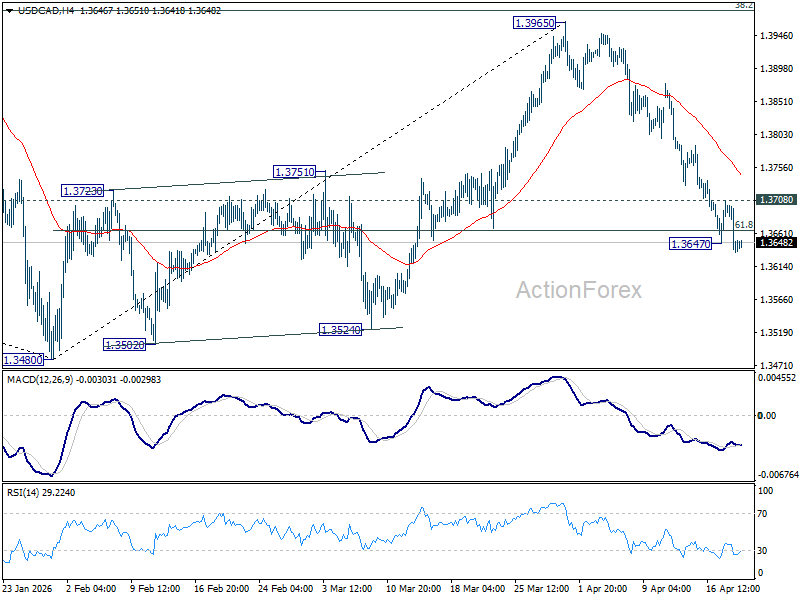

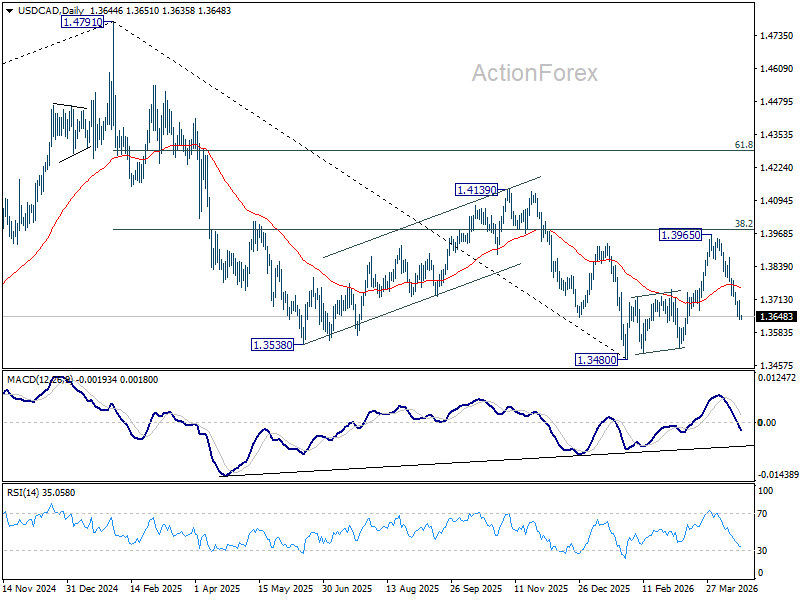

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3616; (P) 1.3664; (R1) 1.3693; More...

USD/CAD's fall from 1.3965 resumed after brief consolidations and intraday bias is back on the downside. Sustained trading below 61.8% retracement of 1.3480 to 1.3965 at 1.3665 will pave the way to retest 1.3480 low. On the upside, above 1.3708 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

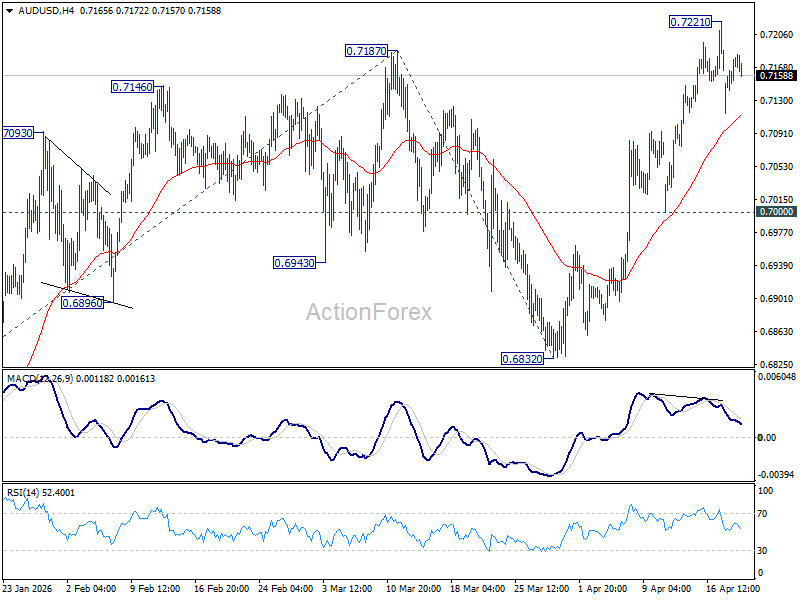

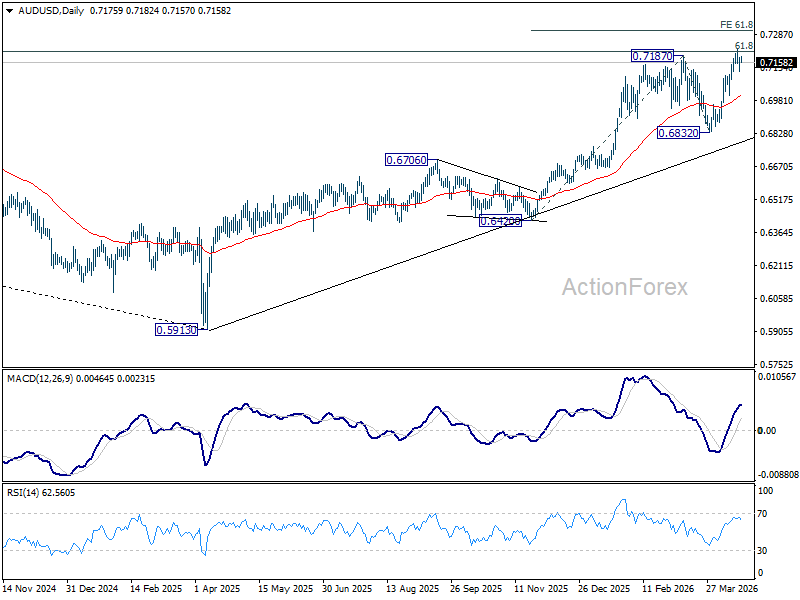

AUD/USD Daily Report

Daily Pivots: (S1) 0.7136; (P) 0.7159; (R1) 0.7200; More...

Intraday bias in AUD/USD remains neutral for consolidations below 0.7221. Downside should be contained above 0.7000 support. On the upside, above 0.7221 will extend the larger up trend to 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. However, break of 0.7000 will bring deeper fall back to 0.6832 support instead.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.

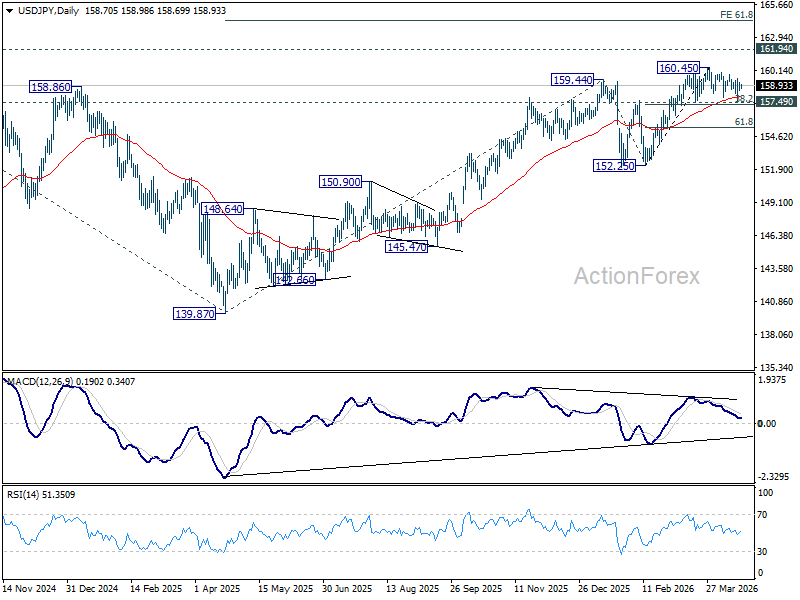

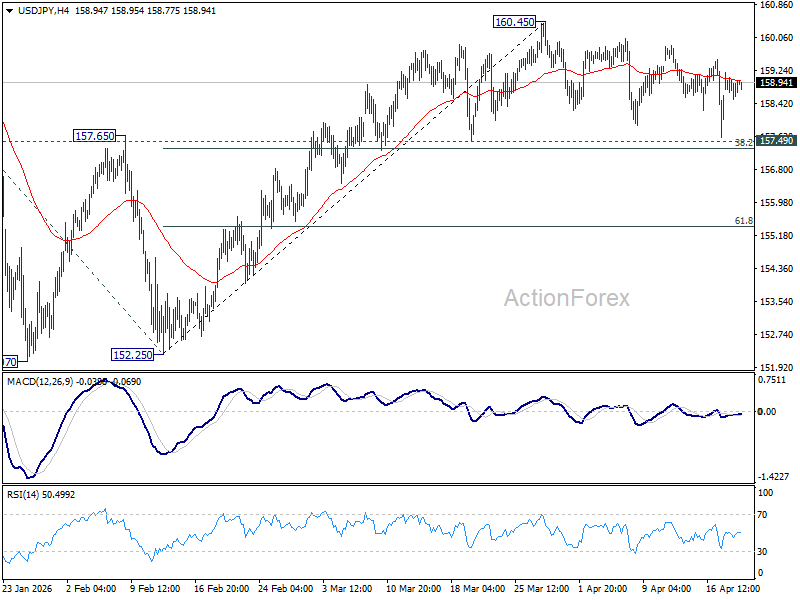

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.51; (P) 158.86; (R1) 159.16; More...

USD/JPY is extending consolidation pattern from 160.45 and intraday bias remains neutral. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.80) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.