Sample Category Title

Gold Technical: A Potential Minor Corrective Pull-back in Play as FOMC Looms

- Gold (XAU/USD) has traded in a tight range of 2% in the past two weeks after it printed a fresh all-time high of US$2,195 on 8 March.

- The biggest risk event for today will be the latest Fed FOMC’s dot plot projection on the trajectory of its Fed funds rate; a reduction to two cuts from three cuts for 2024 cannot be ruled out.

- Technical analysis suggests potential short-term weakness in Gold (XAU/USD).

- Watch the key short-term resistance at US$2,180 on Gold (XAU/USD).

The price actions of Gold (XAU/USD) have staged the expected bullish breakout and rallied by +7.4% to print a new fresh all-time high of US$2,195 on 8 March.

In the past two weeks, the price actions of Gold (XAU/USD) have started to consolidate ahead of today’s major risk event, the US central bank, FOMC monetary policy decision outcome, latest “dot plot projections”, and Fed Chair Powell press conference.

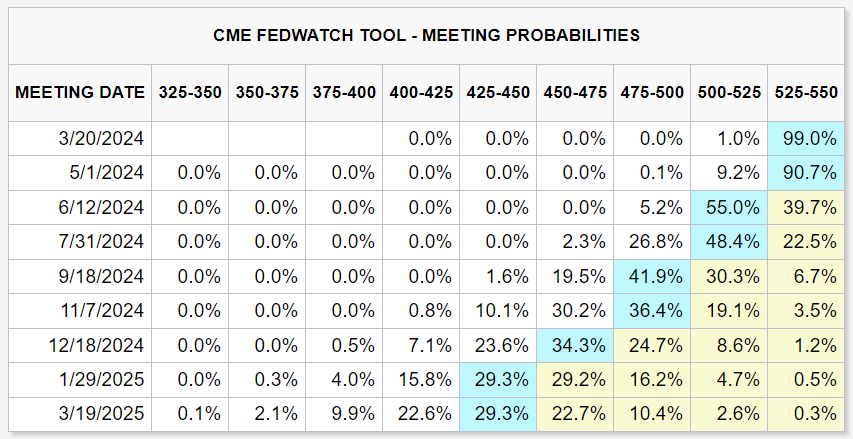

The US monetary policy outcome will likely be a non-event as market participants have been “guided” by the latest slew of Fed Speak as well as a not-so-soft inflationary trend (February’s CPI and PCE data) in the US to price in a no-change to the Fed funds rate at 5.25%-5.50% for the 6th consecutive meeting as indicated by the CME FedWatch tool with a 99% probability of such an outcome.

Fed funds rate futures is still pricing a total of three cuts for 2024

Fig 1: Fed FOMC meeting probabilities as of 20 Mar 2024 (Source: CME FedWatch Tool, click to enlarge chart)

The biggest risk will be a change to the dot-plot projection of the forecasted trajectory of Fed funds rate for 2024; in the previous dot-plot released during the December 2023 FOMC meeting, three cuts have been pencilled in which is now in line with market participants’ expectations as priced by the CME FedWatch Tool. It now reflects only three interest rate cuts by the Fed before 2024 ends, down from six cuts at the start of 2024.

If the latest Fed officials’ median projection on the trajectory of the Fed funds rate for 2024 indicates a reduction to two cuts from three (below market expectations) which in turn may trigger a further potential rebound in the US 10-year Treasury yield to surpass the 4.3% level.

This scenario is likely to be detrimental for Gold at least in the short-term because the opportunity costs for holding Gold increase as it is “a zero-yielding asset”.

A minor corrective pull-back may be in play for Gold

Fig 2: Gold (XAU/USD) major trend as of 20 Mar 2024 (Source: TradingView, click to enlarge chart)

Fig 3: Gold (XAU/USD) short-term trend as of 20 Mar 2024 (Source: TradingView, click to enlarge chart)

Technically speaking, the price actions of Gold (XAU/USD) are still evolving within a major uptrend phase in place since the 28 September 2022 low of US$1,615 supported by an upward trajectory of the Gold/Copper ratio (see Fig 2).

In the lens of technical analysis, price actions of highly liquid tradable instruments do not move vertically up or down but oscillate within a trending phase.

In the short term, Gold (XAU/USD) has started to turn “soft” after a rapid rally from 23 February to 8 March, and price actions have been capped by a minor descending trendline in the past week.

In addition, the hourly RSI momentum indicator has just staged a bearish momentum breakdown from its parallel ascending support at the 43 level which translates to further potential weakness in price action (see Fig 3).

Watch the US$2,180 short-term pivotal resistance for Gold (XAU/USD), a break below the US$2,146 near-term support may see further weakness to expose the next intermediate supports at US$2,125 and US$2,110 (also the upward-sloping 20-day moving average).

On the flip side, a clearance above US$2,180 invalidates the corrective pull-back scenario to kickstart another bullish impulsive sequence for the next intermediate resistance to come in at US$2,200/210 in the first step.

UK Inflation Sets Up a Marathon for BoE

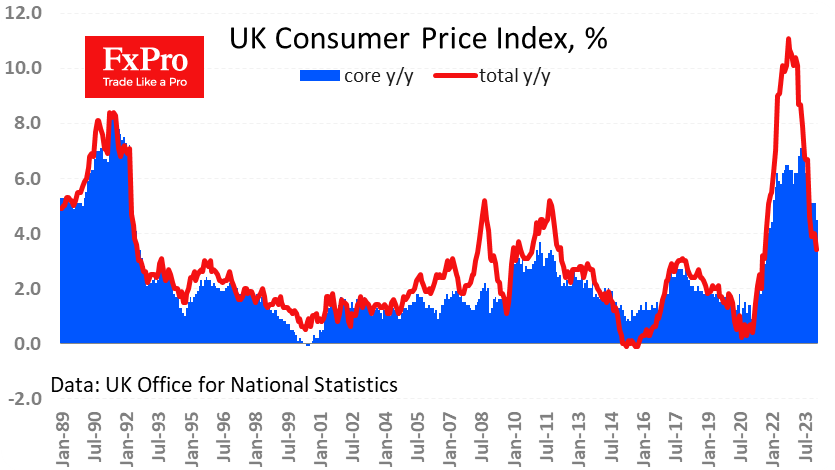

UK inflation has come in slightly weaker than expected, but this does not significantly bring the rate cut date any nearer.

The CPI rose by 0.6% in February after a similar fall in January. Annual inflation slowed to 3.4% from 4.0%, vs expected 3.5%. Core CPI slowed its rise to 4.5% y/y in February after three months of stabilising at 5.1%.

Rising prices for services are driving core inflation. This is a very sluggish component, making it a marathon rather than a sprint for the Bank of England.

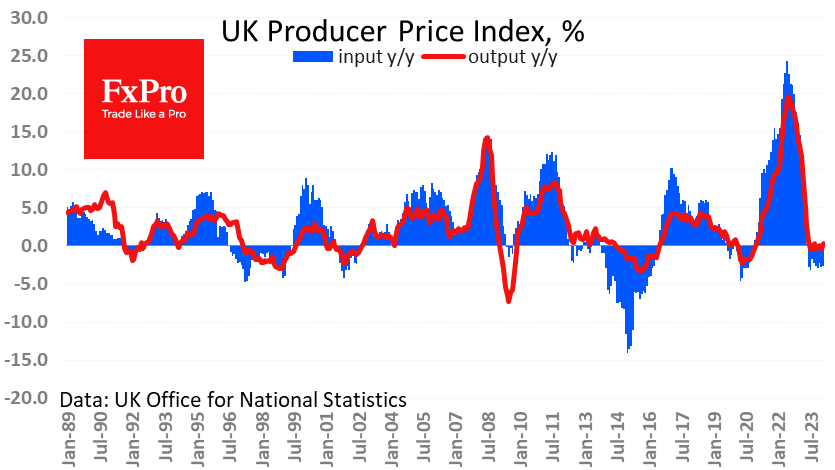

Input Producer prices fell 0.4% in February and are down 2.7% y/y. The index has retreated to May 2022 levels thanks to lower prices for energy, metals, and a range of agricultural products.

Output PPI have not shown much momentum over the past three quarters. Rising wage costs have offset the fall in input prices. The generally strong labour market is allowing manufacturers to regain profitability.

This is not bad news for the economy as it indicates business confidence, which is often self-sustaining.

Sterling rose by 0.1% against the general downtrend following the inflation release but very quickly returned to the general downtrend against the dollar.

Inflation is one of the variables that influences central bank decisions. Now, the markets are in a wait-and-see mode for the outcome of the FOMC meeting on Wednesday night and the Bank of England meeting on Thursday afternoon.

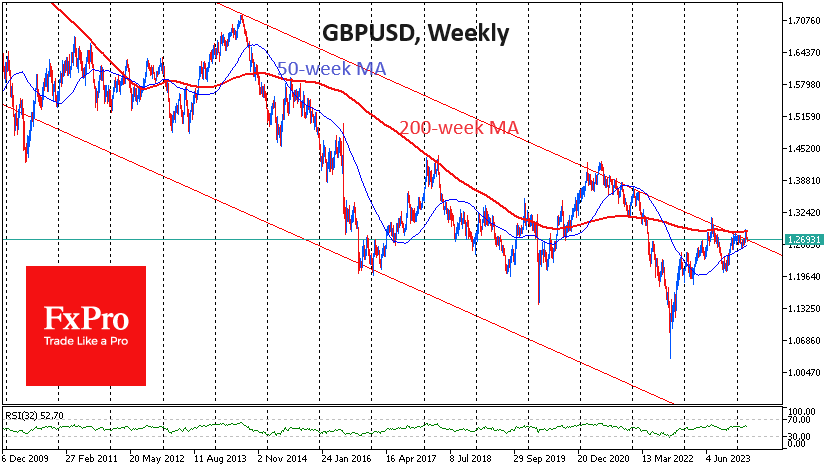

GBPUSD has lost ground over the past two weeks, failing to make gains after a long period of consolidation. Cable has now erased the recent gains and is back near 1.27.

In the weekly timeframe, GBPUSD is near the upper boundary of a descending corridor that has been in place since 2008. A break above would be a significant event, but the basic scenario in such cases is a reversal to the downside with a hold within the range. This week’s events have enough potential to put an end to this consolidation.

GBP/USD Dips as UK Inflation Lower Than Expected

The British pound has extended its losses on Wednesday. In the European session, GBP/USD is trading at 1.2695, down 0.21%. The pound has been on a slide and is down about 1.2% since March 13.

UK inflation falls by 3.4%

Households in the UK haven’t had much to smile about when it comes to the economy, but there was some good news today as UK inflation dropped to 3.4% y/y in February, down from 4% in January and just below the market estimate of 3.5%. This was the lowest rate since September 2021.

The driver of the drop in CPI was a slowdown in food inflation, while housing and fuel prices showed less of a decline in February than a month earlier, putting upward pressure on inflation. Monthly, CPI rose 0.6%, up from -0.6% in January but below the market estimate of 0.7%.

Core CPI eased to 4.5% y/y, compared to 5.1% in January and below the market estimate of 4.6%. Monthly, core CPI rose 0.6%, up from -0.9% but below the market estimate of 0.7%.

The Bank of England will no doubt be encouraged by the inflation data, which showed a significant drop in February and was lower than expected. The BoE meets on Thursday and is widely expected to maintain the cash rate at 5.25% for a sixth straight time.

The Bank has not yet bought into rate cuts and we can expect a cautious message from Governor Bailey acknowledging that inflation is on a downtrend but that the battle ain’t over yet. There is a concern among BoE policy makers that lowering rates too soon could lead to inflation rebounding, which would force the central bank to zigzag and raise rates.

GBP/USD Technical

- GBP/USD is testing support at 12708. Below, there is support at 1.2681

- There is resistance at 1.2747 and 1.2774

Dollar Index: Bulls Hold Grip on Expectations that Fed Will Keep Hawkish Stance

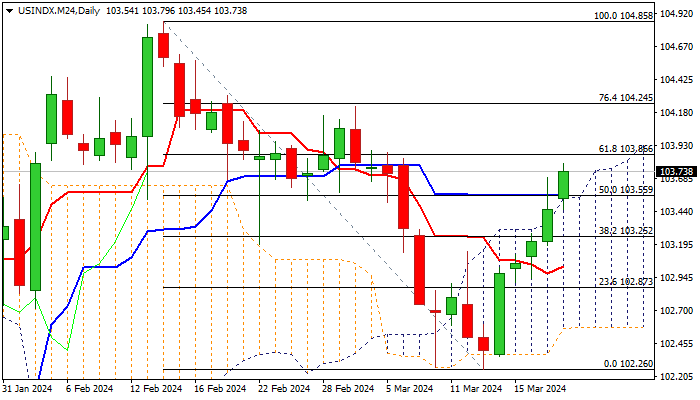

The dollar index continues to trend higher and hit two-week high on Wednesday, benefiting from the hawkish outlook from the Fed, as the central bank will deliver its monetary policy decision later today.

The central bank is not expected to make any changes to the policy, with high interest rates to be kept for extended period and further contribute to positive environment for the greenback.

Recent solid economic data from the US signal that the economy is resilient and can stand higher borrowing cost for some time, while inflation remains sticky and likely to produce increased headwinds to the pace of expected rate cuts this year, which will boost positive outlook for the dollar from the fundamental side.

Technical picture on daily chart is also improving, as the recovery leg from 102.26 (Mar 13 low) extends into the fifth straight day and generated bullish signal from Tuesday’s close above the top of thickening daily Ichimoku cloud.

Today’s fresh extension higher broke above 200DMA (103.47) and 50% retracement of 104.85/102.26 (103.55) with sustained break above these levels to further strengthen near-term structure and open way for probes above next pivotal barrier at 103.86 (Fibo 61.8%).

However, caution is still required as 14-d momentum stays in the negative territory and stochastic is overbought, but near-term bulls are expected to hold grip while the price stays above daily cloud top/200DMA.

Res: 103.86; 104.25; 104.85; 105.47.

Sup: 103.47; 103.38; 103.25; 102.96.

ECB’s Lagarde sets conditions for June rate cut

ECB President Christine Lagarde provided clarity in a speech on the conditions that would lead to a rate cut in June, highlighting reliance on "two important pieces of evidence" as pivotal to the central bank's confidence on dialing back monetary restrictions. .

Firstly, ECB anticipates receiving data on negotiated wage growth for Q1 by the end of May. Secondly, by June, ECB will have access to a new set of economic projections, enabling it to verify the validity of the inflation path forecasted in its March projection.

After the first move, Lagarde emphasized to "confirm on an ongoing basis" that incoming data aligns with its inflation outlook. This approach underscores a commitment to data-driven policy decisions, maintaining a "meeting-by-meeting" stance that eschews any pre-commitment to a fixed rate path.

Furthermore, Lagarde noted the enduring significance of ECB's policy framework in processing incoming data and determining the appropriate policy stance. However, she also mentioned that the relative importance of the three criteria guiding these decisions would require regular reassessment.

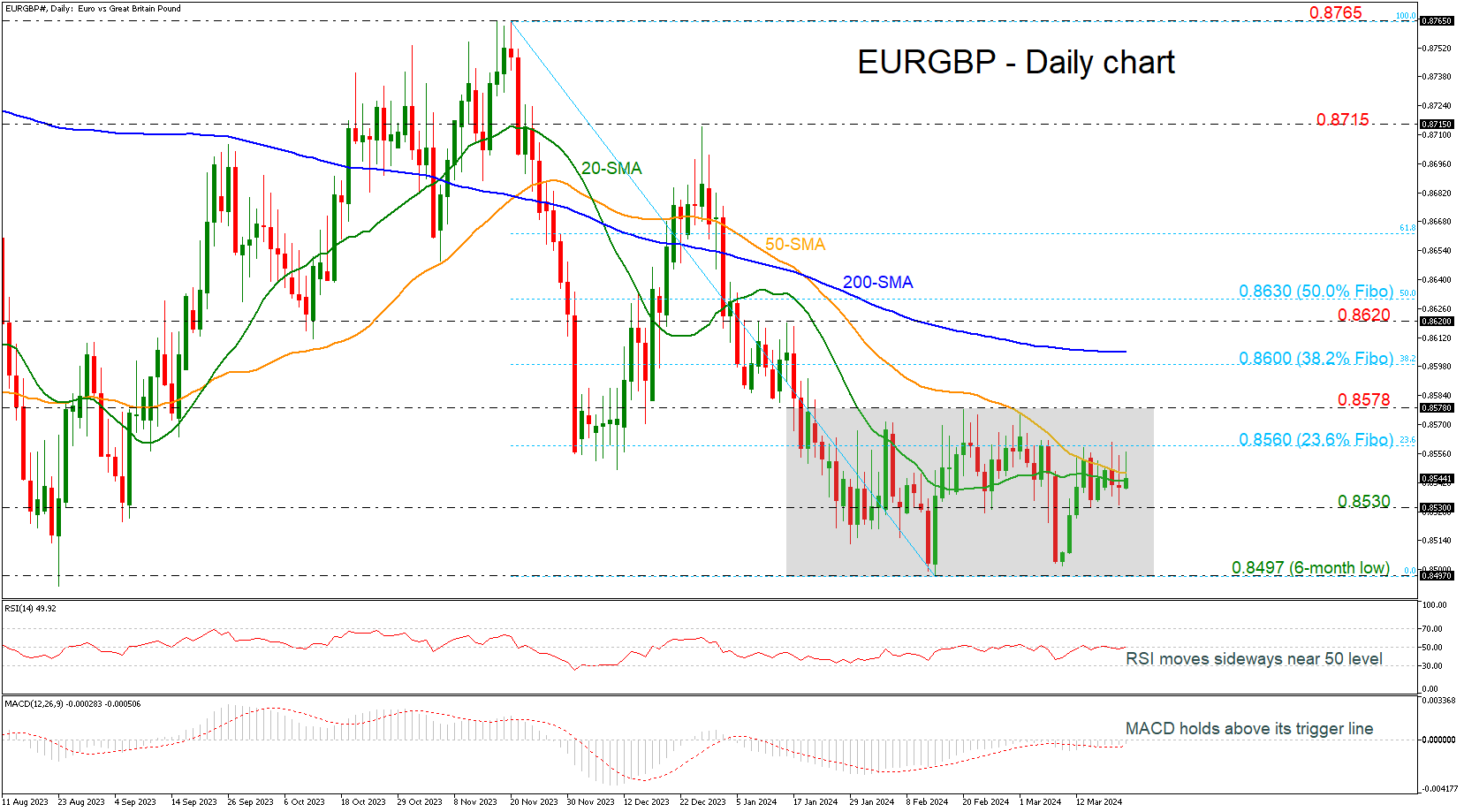

EURGBP Struggles to Surpass 23.6% Fibo

- EURGBP remains in sideways channel

- Technical oscillators lose steam

EURGBP is finding another strong obstacle to surpass within the medium-term trading range of 0.8497 to 0.8578. Specifically, the 23.6% Fibonacci retracement level of the down leg from 0.8765 to 0.8497 at 0.8560.

The pair is also flirting with the 20- and the 50-day simple moving averages (SMAs) and the technical oscillators are showing some weak signals. The RSI is flattening near the neutral threshold of 50, while the MACD is standing above its trigger line in the negative territory.

If the market slips beneath the mid-level of the range of 0.8530 then it may retest the lower boundary of 0.8497. Steeper decreases could open the way towards the 0.8400 handle, registered back in August, changing the outlook to a more bearish one.

On the flip side, a jump above the 23.6% Fibonacci of 0.8560 could lead the pair until the 0.8578 barricade. A climb towards the 38.2% Fibonacci of 0.8600 and the 200-day SMA at 0.8605 may switch the bias to bullish, meeting the 0.8620 resistance.

In a nutshell, EURGBP has been trading without clear direction since January 17. A closing session above or below the consolidation area could show the next path.

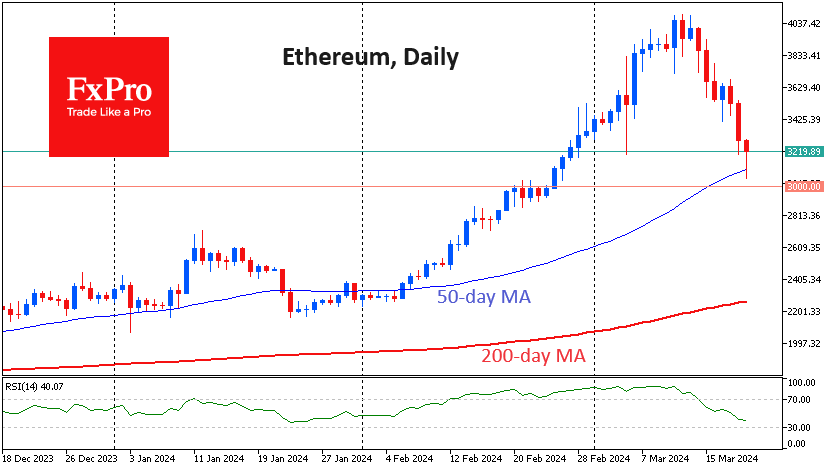

Bitcoin and Ethereum Seek Support

Market picture

The crypto market correction continues to deepen, although there have been some signs of stabilisation since the start of the day on Wednesday. The decline has continued for a whole week, reducing the market cap by almost 15%. The total cap was down to $2.28 trillion on Wednesday morning, rising to $2.35 trillion (-2.5% in 24 hours) by the start of active trading in Europe.

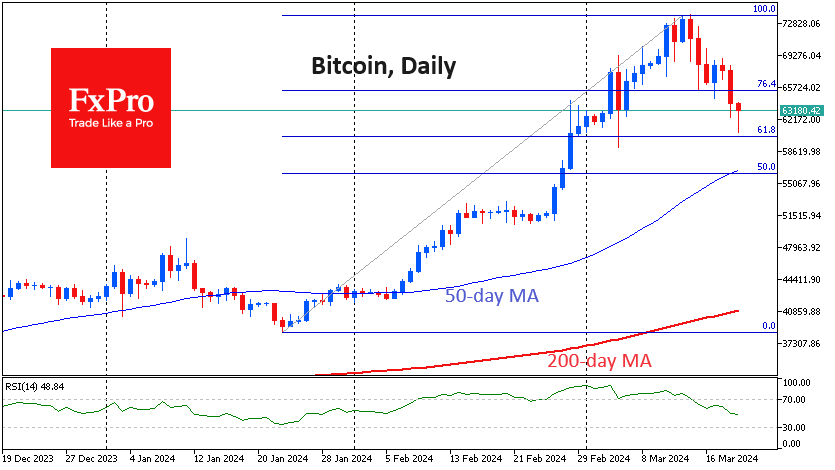

Bitcoin is down 13.6% in seven days, trading at $62.8K and dipping below $61.0K in the early session. Technically, it remains in a downtrend, with a series of lower lows and lower highs. We will pay attention to the first cryptocurrency’s dynamics at the following support levels: $60.3K (correction to 61.8% of the last rally), $56K area (50-day average and 50% level) and $51.5K (consolidation area in February).

Ethereum approached $3050, but a temporary break below the 50-day moving average spurred buyers. Some traders are seeing the situation as an opportunity to join the global bull market after profit-taking. However, crypto traders should now keep a close eye on the appetite for risk in the financial markets. Today, it will be heavily influenced by the FOMC and other major central bank meetings later in the week.

News background

Against the backdrop of the first cryptocurrency to rally above $70K, holders have turned to sellers to lock in profits, according to Glassnode. Bitcoin’s current correction offers an opportunity to “buy on the lows” ahead of the April halving, according to Bernstein.

Michael van de Poppe, founder of MN Trading, called the correction “sharp”. “But remember, you don’t want to buy altcoins when they’re going up. You want to buy them when they’re down 25-60 per cent. That’s when the real profits come in,” he added.

MicroStrategy bought 9,245 BTCs between 11 and 18 March at an average price of $67,382, according to founder Michael Saylor. MicroStrategy’s total cryptocurrency reserves reached 214,246 BTC, which is more than 1% of the total digital gold issued.

CryptoQuant founder and CEO Ki Yoon Ju expressed concern about the boom in the meme-token segment. In his opinion, such projects only harm the crypto industry. Yoon Ju compared the situation to the ICO boom in 2018, which resulted in most investors simply losing their invested funds.

Fidelity Investments has amended its proposal to launch a spot Ethereum ETF to include staking in its provision.

Total client assets on Binance have surpassed $100 billion, according to the exchange. According to DeFi Llama, $109 billion is held on the platform, with Bitcoin (32%), USDT (21%) and BNB (15%) making up the majority of assets.

Correction in Crypto Markets: BTC/USD Rate Drops to $60,000

On March 18, we wrote that bears became more active near the $70,000 level.

As the BTC/USD chart shows, today the price of Bitcoin is already close to the psychological level of USD 60k, while the price of Ethereum is close to USD 3,000.

According to MarketWatch, experts consider the decline to be a correction that is “long overdue” as part of an upward trend. According to Fundstrat, Monday saw net outflows from BTC ETFs for the first time since March 1, amounting to about $154.3 million.

What's next?

From a technical analysis point of view, the price of Bitcoin, given an increase of approximately 90% from point A (around USD 38.8k) to point B (around USD 73.4k), a normal correction of 50% indicates the prospect of a decline to the area of USD 56.1k.

Having constructed a channel (shown in blue), taking into account extrema A and B, as well as turning points (indicated by arrows), it is permissible to assume that the price of Bitcoin will drop to the lower boundary of the channel in the area of $57k, where it currently lies.

Thus, the USD 56-57k area can be seen as a target for the bears, who have seized the initiative after the upward momentum has exhausted itself (judging by the divergence on the RSI indicator).

In the event of a deeper correction, a test of the psychological mark of USD 50k per Bitcoin cannot be ruled out.

However, despite the significant decline (about 15% over the last 6 days), the Bitcoin market can be considered bullish:

→ the blue ascending channel has not yet been broken;

→ the approaching halving is seen as a growth driver;

→ according to the new Bitcoin price forecast from Standard Chartered, the target has been increased to USD 150k by the end of 2024 and USD 250k by the end of 2025.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*At FXOpen UK and FXOpen AU, Cryptocurrency CFDs are only available for trading by those clients categorised as Professional clients under FCA Rules and Professional clients under ASIC Rules respectively. They are not available for trading by Retail clients.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

NZDUSD in the Red Again Ahead of Fed

- NZD remains on the back foot against USD

- NZDUSD has finally broken below its one-year-long rectangle

- Momentum indicators acknowledge the current bearish move

NZDUSD is recording another red candle today and it is trading below the lower boundary of the one-year-old rectangle and the busy 0.6060-0.6092 area. It has actually registered a new 2024 low with the market now turning its focus to the critical Fed meeting, which could result in increased volatility in NZDUSD as made evident by the convergence of the 50- and 100-day simple moving averages (SMAs).

In the meantime, the momentum indicators are mostly on the bears’ side. More specifically, the RSI has dropped below its 50-midpoint and it is thus pointing to increasing bearish pressure. Similarly, the Average Directional Movement Index (ADX) is tentatively hovering above its 25-threshold and thus signalling the presence of a weak bearish trend in NZDUSD. More importantly, the stochastic oscillator has reached its oversold territory (OS) but maintains a good gap from its moving average.

If the bulls decide to retake the market reins, they could try to lead NZDUSD higher towards the 0.6060-0.6092 range, which is populated by the 38.2% Fibonacci retracement, the July 14, 2022 low and the 200-day simple moving average (SMA), and then back inside the aforementioned rectangle. Even higher, the 0.6120-0.6127 range defined by the 50- and 100-day SMAs appears to be a key resistance area.

On the flip side, the bears appear ready to take advantage of the current momentum and push NZDUSD lower. The 0.6000 level is probably the first key support level with the May 15, 2022 low at 0.5920 possibly being the next plausible target.

To sum up, NZDUSD bears have recorded a new 2024 low but market events could offer them the opportunity for an even stronger correction towards the November 2023 levels.

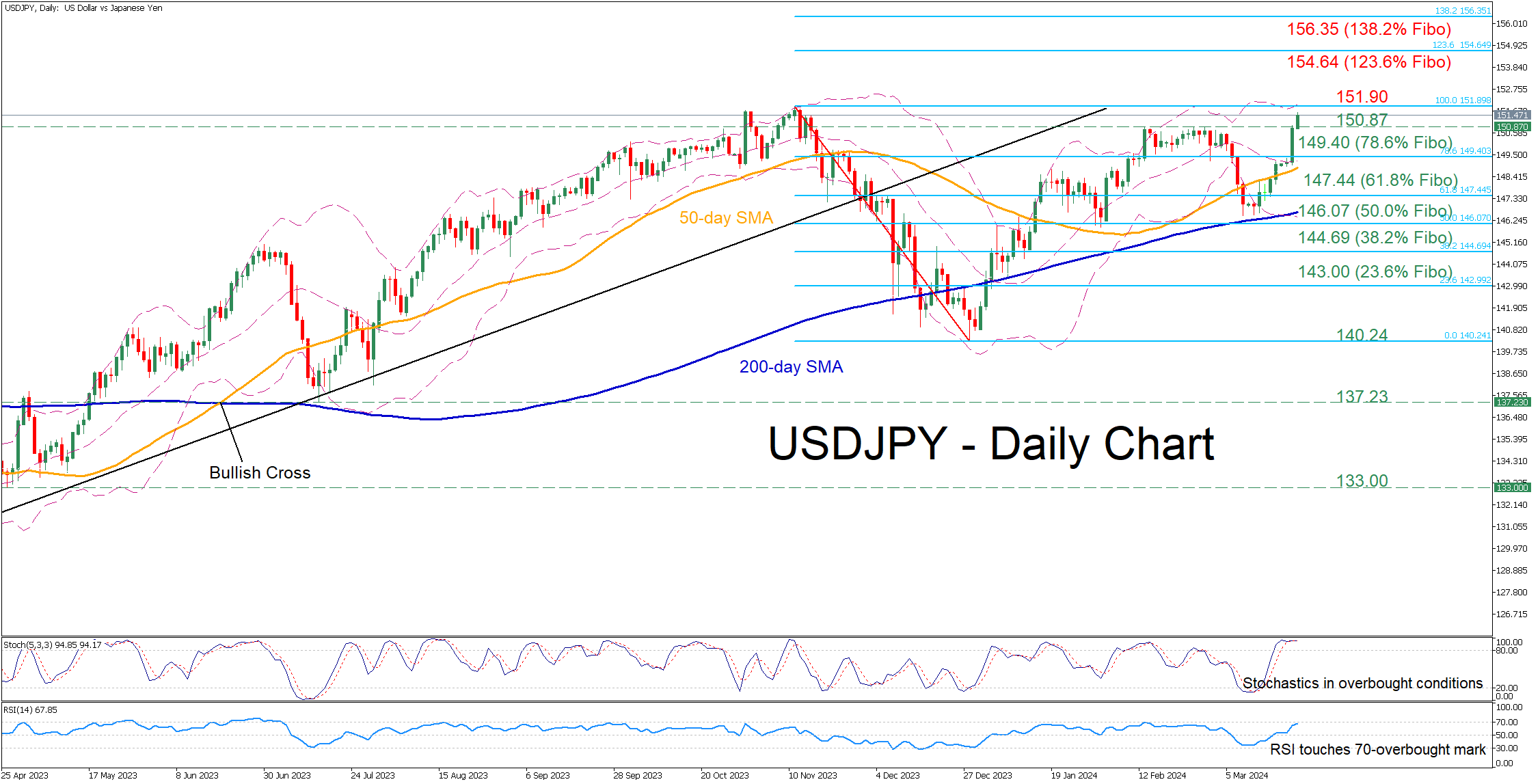

USDJPY Advances in BoJ Aftermath

- USDJPY storms to fresh 2024 high after BoJ’s rate hike

- The pair is within breathing distance from 33-year peak

- Momentum indicators point to overbought conditions

USDJPY has been in a steady uptrend after finding its feet a tad above the 200-day simple moving average (SMA) in early March. Meanwhile, the pair posted a fresh 2024 high following a dovish hike by the BoJ on Tuesday, while it has been extending its losses ahead of the FOMC meeting later today.

Should bullish pressures persist, the price might revisit the 2023 high of 151.90 ahead of the 33-year peak of 151.94 registered in 2022. Further advances could then cease at 154.64, which is the 123.6% Fibonacci extension of the 151.90-140.24 downleg. Conquering this barricade, the bulls could then attack the 138.2% Fibo of 156.35.

On the flipside, if the pair reverses lower, the 2024 resistance region of 150.87 could now serve as initial support. Even lower, the price could encounter strong support at the 78.6% Fibo of 149.40. A violation of that hurdle may set the stage for the 61.8% Fibo of 147.44.

Overall, USDJPY’s advance accelerated following the dovish hike by the BoJ, while the FOMC meeting later today could induce more upside pressures. Therefore, traders should be aware that there might be a battle around the 33-year high of 151.94 in the upcoming sessions.