Sample Category Title

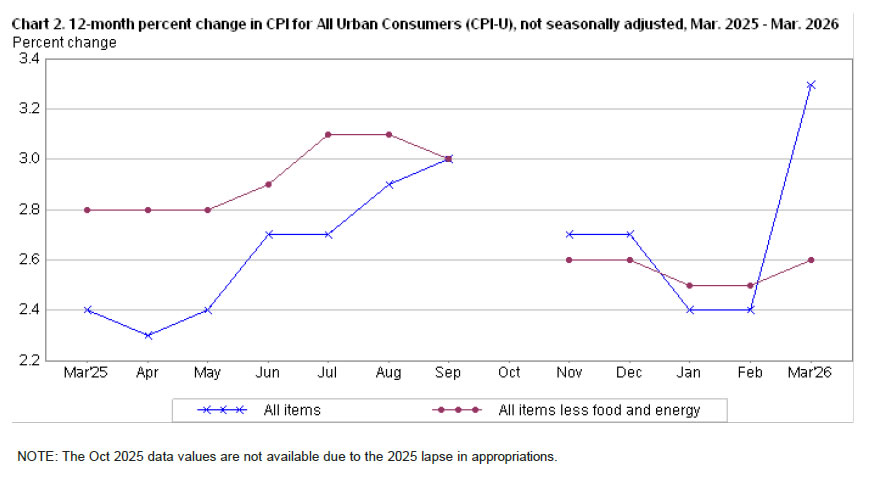

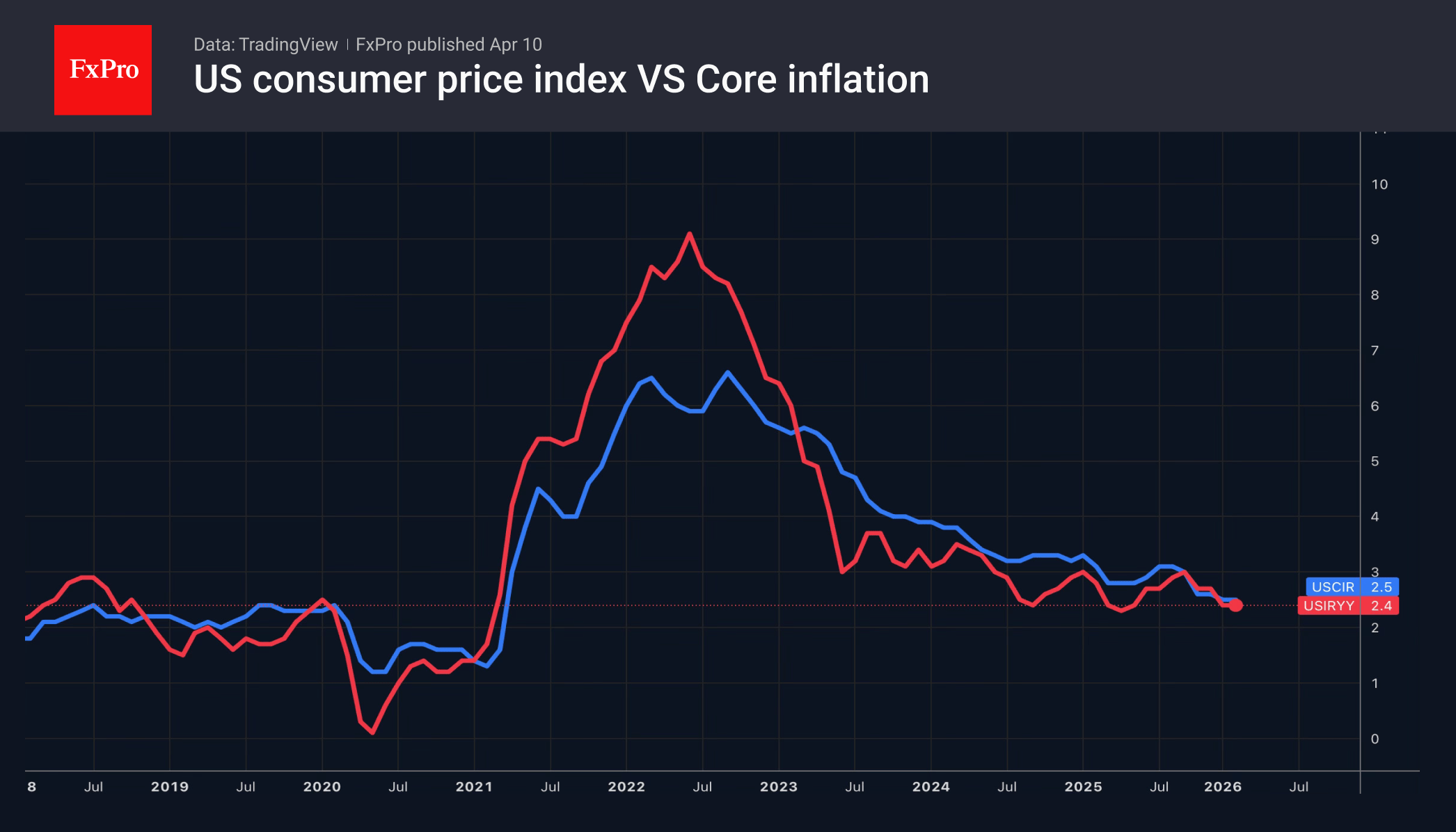

US: Inflation Jumps to a Near Two-Year High in March

The Consumer Price Index (CPI) shot higher by 0.9% month-on-month (m/m) in March, meeting the Bloomberg consensus forecast. On a twelve-month basis, CPI jumped to a near two-year high of 3.3% (from 2.4% in February).

- A surge in energy costs accounted for more than three-quarters of the monthly gain in headline, led by a 21.2% m/m surge in gasoline prices. Food prices were flat on the month, as a pullback in grocery costs (-0.2% m/m) was offset by a similar gain in "food away from home".

Excluding food and energy, core inflation rose 0.2% m/m, a tick weaker than consensus, but matching February's gain. On a twelve-month basis, core prices were up 2.6% (from 2.5% in February).

Services inflation was up 0.2% m/m, following a gain of 0.3% m/m the month prior. Primary shelter costs heated up at touch, though this was offset by some cooling in non-housing services, which were up just 0.1% m/m – its slowest monthly gain since May 2025.

Core goods prices rose 0.1% m/m, as gains in apparel, recreational goods, household furnishings, and new vehicles were partially offset by a steep pullback in medical goods and another decline in used vehicle prices.

Key Implications

It goes without saying that higher energy prices were going to be a focal point of this morning's release – accounting for most of the gain in headline inflation. While core prices came in a bit softer than expected, it feels a bit backward looking as the surge in energy costs are likely to pressure prices for other goods and services higher in the months ahead. This will be happening alongside the continued passthrough of higher tariff costs, suggesting inflation's near-term direction of travel is likely to be higher.

With the labor market appearing to be on a firmer footing, the bar for further rate cuts is set higher. Policymakers can afford to remain patient and sit tight for the time being. Fed futures were largely unchanged following this morning's release and are currently pricing in just 8 basis points of rate cuts by year-end.

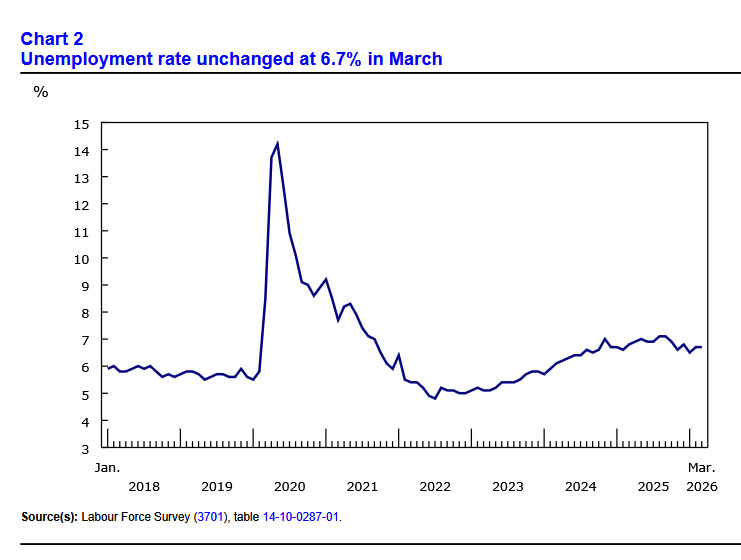

Canada’s Unemployment Rate Holds Steady Amid Weak Hiring

Canada’s economy added 14k jobs in March (+0.1% m/m), more-or-less in line consensus expectations for a 15k gain. Employment was essentially flat across job types, with full-time employment edging down slightly (-1k) while private-sector employment rose by 15k on the month.

The unemployment rate was unchanged at 6.7% after February’s increase. The labour force grew by 15k in March, while the participation rate was unchanged at 64.9%. Importantly, the layoff rate is in line with pre-pandemic values, while 15.2% of February's unemployed found work in March, in line with the rate in 2025 (14.7%), but below the 19.1% recorded in the same months in 2017-2019. The data suggest that the high unemployment rate is "mostly driven by slower hiring, rather than by increased layoffs."

Job gains were concentrated in “other services” (+15k) and natural resources (+10k), while finance, insurance, real estate, rental and leasing posted the largest decline (-11k).

Wage growth firmed further, with average hourly wages up 4.7% year-on-year (y/y) in March, accelerating from 3.9% in February. However, wages were lifted by the changing composition of the workforce. Holding the composition of employment fixed, average hourly wages were up 3.6% y/y, in line with January and February 2025.

Key Implications

The labour report came in as expected, showcasing the lack of dynamism in the Canadian labour market. The unemployment rate remains elevated, with the lack of hiring showcasing the general apprehension in the economy. With the economy continuing to progress in fits and starts, and uncertainty sky-high, the outlook is for subdued job growth and a steady unemployment rate.

The outlook remains fraught, with the energy shock beginning to be felt in the economy, and no clarity on the direction of the conflict. How long the conflict lasts and energy supplies remain disrupted, will determine the size of the inflation shock. For now, weak demand conditions should provide some offset to inflationary pass-through, allowing the Bank of Canada to stay on the sidelines and wait to see how things play out.

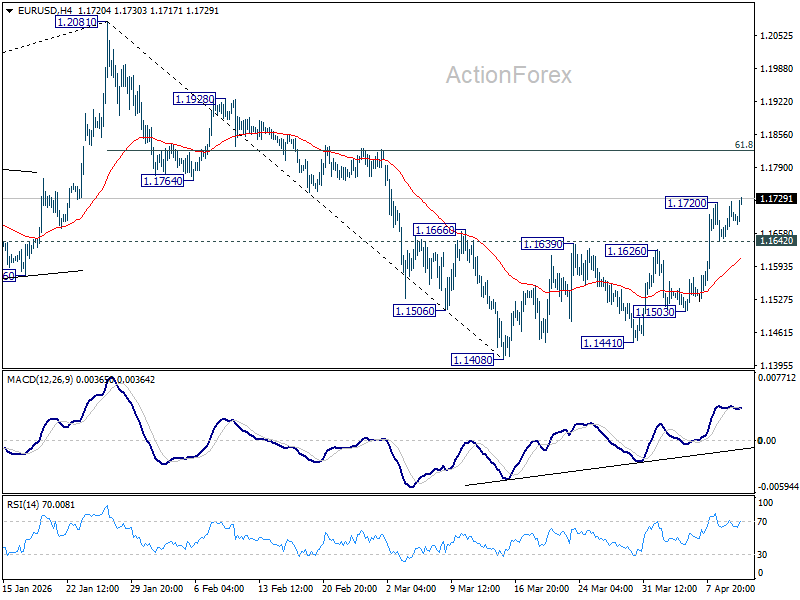

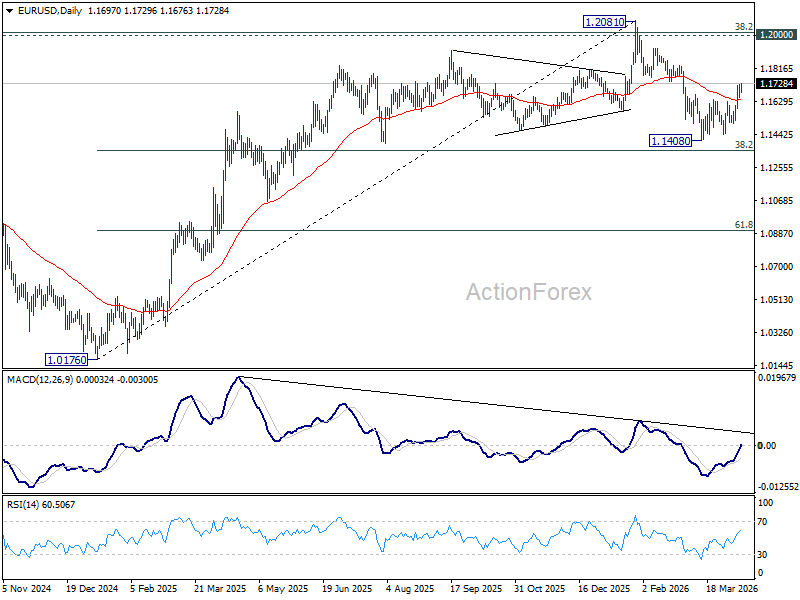

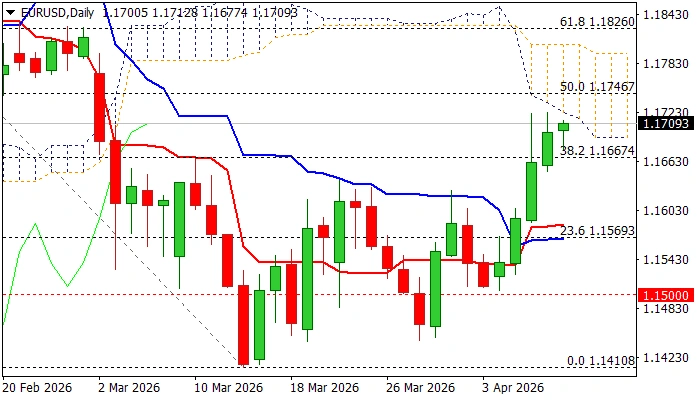

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1658; (P) 1.1692; (R1) 1.1733; More….

Intraday bias in EUR/USD is back on the upside with break of 1.1720 temporary top. Rise from 1.1408 is resuming and should target 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Decisive break there will pave the way to retest 1.2081 high. On the downside, below 1.1642 minor support will turn intraday bias neutral again first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1505). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Dollar Slips as CPI Fails to Rattle Fed’s Transitory View, Islamabad Talks Awaited

Dollar is back under mild pressure as US trading gets underway, with markets reacting to a softer-than-feared inflation report from the US. While headline CPI surged in March, the print missed expectations, easing fears of a more aggressive inflation shock. The key relief came from the core reading. Despite the sharp rise in headline inflation driven by energy, underlying price pressures remained contained. This has reassured markets that the inflation spike is not yet broadening into the wider economy.

As a result, the Fed is unlikely to shift its stance. Policymakers have long emphasized their willingness to look through energy-driven inflation shocks, and the latest data does little to challenge that framework. There is no immediate pressure for the Fed to pivot back toward tightening. Market pricing reflects this view. Futures are assigning around a 35% probability of a rate cut before year-end, slightly higher than earlier in the week, suggesting expectations for policy easing remain delayed but not abandoned.

However, the inflation outlook remains tightly linked to geopolitics. The Strait of Hormuz remains shut, and tensions persist despite the two-week ceasefire, with both the US and Iran accusing each other of violations. These developments underscore the fragility of the current truce. Ongoing exchanges involving Israel and Hezbollah, alongside continued disruptions to oil flows, highlight that the situation remains far from resolved. Attention now turns to the upcoming US-Iran talks in Islamabad, which represent a critical inflection point. Markets are waiting to see whether the ceasefire can evolve into a more durable agreement or unravel further.

Beyond the US, the energy shock is once again feeding into global rates markets. Yields in Germany and the UK have surged following reports of potential jet fuel shortages within three weeks, based on the intrinsically linked "energy-inflation-interest rate" cycle. The development has taken EUR/JPY and GBP/JPY notably higher.

Overall for the week so far, Dollar is still the worst performer, followed by Yen, and then Loonie. Kiwi is the best, followed by Aussie and then Sterling. Euro and Swiss Franc are positioning in the middle.

In Europe, at the time of writing, FTSE is up 0.40%. DAX is up 0.80%. CAC is up 0.64%. UK 10-year yield is up 0.099 at 4.777. Germany 10-year yield is up 0.056 at 3.045. Earlier in Asia, Nikkei rose 1.84%. Hong Kong HSI rose 0.55%. China Shanghai SSE rose 0.51%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield rose 0.045 to 2.442.

US CPI at 3.3% Misses Expectations, Second-Round Effects Still Limited

US inflation surged in March, driven by a sharp jump in energy prices, particularly gasoline. But beneath the headline spike, core inflation remained subdued, showing little sign of broader price pressures. The lack of second-round effects suggests the shock may stay contained—for now. Read More.

Canada Employment Rebound 14.1k in March, Wage Growth Picks Up

Canada’s labor market showed signs of stabilization in March, with employment beating expectations after two months of sharp losses. At the same time, wage growth accelerated to its strongest pace since late 2024, adding another layer to the outlook as policymakers weigh growth risks against inflation pressures. Read More.

BoJ’s Himino Sees No Stagflation Yet, Warns of Oil-Driven Policy Dilemma

BoJ Deputy Governor Ryozo Himino said Japan is not facing stagflation for now, with inflation near target and growth still holding up. But he warned that a prolonged Middle East conflict could change that dynamic—pushing inflation higher while dragging on growth and creating a difficult policy trade-off. Read More.

Japan PPI Accelerates to 2.6% in March as Import Costs Surge 7.9%

Japan’s producer prices picked up more than expected in March, driven by a sharp rise in import costs and higher energy and industrial input prices. The surge in import prices points to renewed upstream inflation pressure, raising the risk that cost increases could feed through more broadly into the economy. Read More.

China PPI Turns Positive for First Time Since 2022 as CPI Softens

China’s factory prices returned to growth for the first time since 2022, driven by rising energy and commodity costs. But consumer inflation is losing momentum, with CPI and core prices slowing sharply—highlighting a growing gap between upstream cost pressures and weak domestic demand. Read More.

NZ BNZ Manufacturing Falls to 53.2, Slower Expansion as War Concerns Weigh on Sentiment

New Zealand’s manufacturing sector is still expanding, but momentum is clearly slowing. PMI eased in March as production and new orders softened, while inventories rose—hinting at cooling demand. Read More.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1658; (P) 1.1692; (R1) 1.1733; More….

Intraday bias in EUR/USD is back on the upside with break of 1.1720 temporary top. Rise from 1.1408 is resuming and should target 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Decisive break there will pave the way to retest 1.2081 high. On the downside, below 1.1642 minor support will turn intraday bias neutral again first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1505). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Canada Employment Rebound 14.1k in March, Wage Growth Picks Up

Canada’s employment rose by 14.1k in March, slightly above expectations of 12.6k, offering a modest rebound after a cumulative decline of -109k over the first two months of the year. Despite the headline gain, both full-time and part-time employment showed little variation, suggesting underlying momentum remains limited.

Labor market conditions were broadly stable. The unemployment rate held at 6.7%, below expectations of 6.8%. Employment rate remained unchanged at 60.6%. Participation was also steady at 64.9%, indicating that the stability in unemployment partly reflects a lack of re-entry into the labor force rather than a strong pickup in hiring.

Wage growth, however, accelerated notably. Average hourly earnings rose 4.7% yoy, up from 3.9% in February and marking the fastest pace since October 2024. Adjusted for composition effects, wage growth was more moderate at 3.6% yoy. The combination of modest job gains and firmer wages presents a mixed picture, offering some relief after earlier weakness but not enough to signal a clear turnaround in Canada’s labor market.

US CPI at 3.3% Misses Expectations, Second-Round Effects Still Limited

US inflation surged in March, with CPI rising 0.9% mom and lifting the annual rate from 2.4% yoy to 3.3% yoy. While the jump was significant, both figures came in slightly below expectations of 1.0% mom and 3.4% yoy respectively, suggesting the energy-driven spike was largely anticipated.

The surge was overwhelmingly driven by energy costs. Energy prices jumped 10.9% mom, led by a 21.2% spike in gasoline, which accounted for nearly three quarters of the monthly increase in headline CPI.

In contrast, underlying inflation pressures remained more contained, with core CPI rising 0.2% mom and edging up from 2.5% yoy to 2.6% yoy, both below expectations of 0.3% mom and 2.7% yoy.

Other components painted a more stable picture. Shelter rose 0.3% mom, continuing its gradual climb, while food prices were unchanged on the month. Overall, the data reinforces the view that the inflation spike is largely energy-driven, with limited evidence so far of broad-based second-round effects.

EUR/USD: Bulls Face Headwinds on Approach to the Base of Falling and Thickening Daily Cloud

The Euro slowed on Friday, signaling that strong rally of past four days might be showing initial signs of fatigue on approach to next very significant barrier at 1.1722 (base of falling and thickening daily Ichimoku cloud).

Bulls managed to crack strong resistance zone at 1.1667/97, consisting of Fibo 38.2% of 1.2082/1.1410 descend and converged 200/100/55DMAs, at the second attempt (after Wednesday’s attack was rejected and left bullish candle with long upper shadow).

Fading bullish momentum and overbought stochastic contribute to developing negative signals, though more action to the downside (return and close below MAs and broken Fibo 38.2%) will be needed to boost signal.

Meanwhile, near term action would keep bullish bias while holding above MAs (or at least not to drop below 1.1667 – Fibo / 200DMA) but increased headwinds from falling daily cloud should be anticipated.

We will closely watch reaction at this zone, with penetration of cloud and violation of 1.1746 (50% retracement) to sideline immediate downside risk and keep near term focus at the upside (initial signal of bullish continuation).

Traders will also focus on the developments on the peace talks between the US and Iran, as well as release of US March CPI data, as economists expect inflation to start rising, in reaction to crisis from the war in the Middle East.

Res: 1.1722; 1.1746; 1.1800; 1.1826.

Sup: 1.1688; 1.1667; 1.1640; 1.1585.

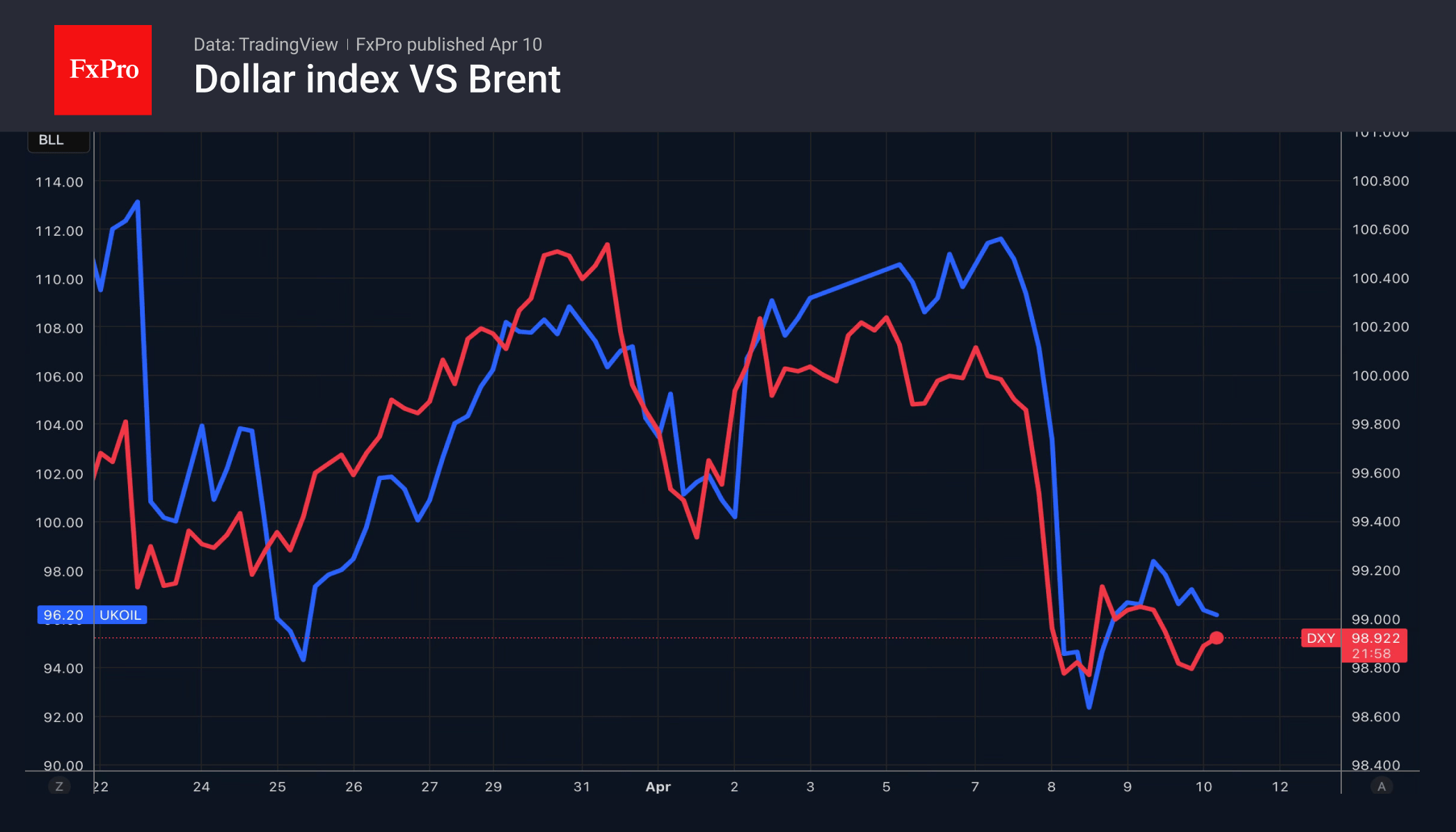

Dollar Seeking a Foothold

- Inflation data could boost the US dollar.

- Gold is rising as risk appetite recovers.

The US dollar is attempting to stabilise after its slump on 8 April, as oil prices find their footing following their worst rout since 2020. The truce between the US and Iran is fragile, having led only to a reduction in the ‘war premium’, but not its complete elimination. Donald Trump has called on Israel and Lebanon to engage in talks and stated that Tehran is struggling to manage the opening of the Strait of Hormuz. Indeed, according to Marine Traffic, only 8 tankers have passed through it in the last 24 hours, compared to 135 before the March conflict.

The IMF warns that it will soon lower its growth forecast for this year from 3.3%, as estimated in January. Even if the US and Iran agree on a lasting peace, the economic scars will remain, says Fund chief Georgieva. The OECD believes the impact on global GDP will depend on the damage to energy infrastructure. The worse the situation for the world, the worse it will be for the eurozone, which imports raw materials and energy, and its currency, the euro. In this context, a recovery in EURUSD appears premature. Traders bought into the rumours of negotiations, but the time will soon come to sell on the facts.

US inflation data for March could act as a short-term trigger for a decline in EURUSD. Consumer prices are forecast to rise by 0.9% month-on-month and 3.3% year-on-year. Such dynamics, along with the risks of core inflation accelerating from second-order effects, will force the Fed to keep rates high. Moreover, the resilience of the US economy may lead the futures market to anticipate a rise in borrowing costs. This will play into the dollar’s hands.

Meanwhile, USDJPY bulls are recovering after the sell-off triggered by news of the Washington-Tehran talks. The consolidation of oil prices at high levels makes Japan’s energy-import-dependent economy and the yen extremely vulnerable. At some point, the government’s verbal interventions will cease to work, and it will revert to currency interventions. Increased volatility in the pair is guaranteed.

Gold is gaining favour thanks to a resurgence in risk appetite and the long-term erosion of confidence in the US dollar as a reserve currency. In its time, the British pound lost this function due to the First World War, the abandonment of the gold standard, Bretton Woods and the Suez Crisis. Now, due to White House policy, the greenback may follow suit. For the first time in history, the value of assets denominated in it within the central bank’s reserves has fallen below the value of its precious metal reserves.

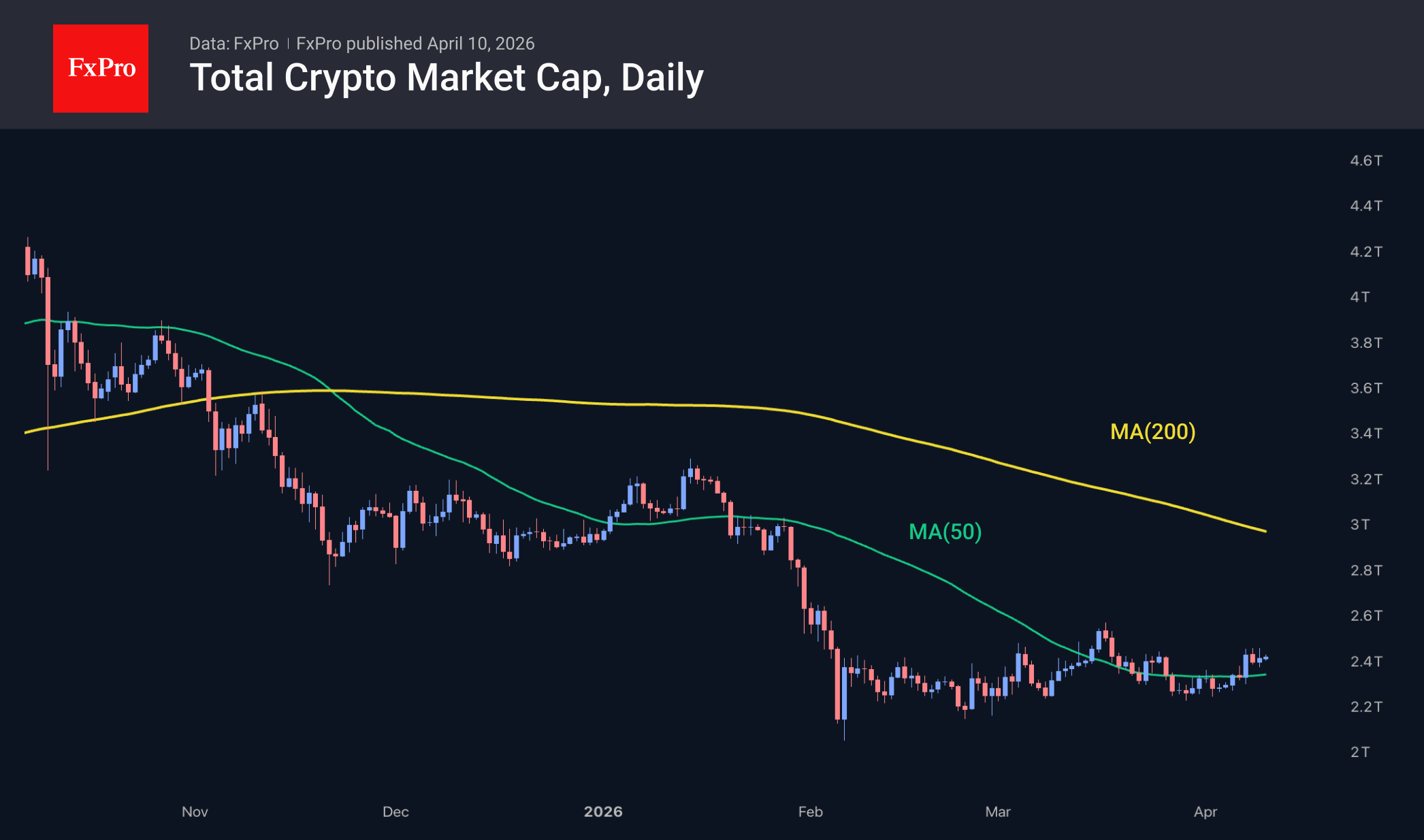

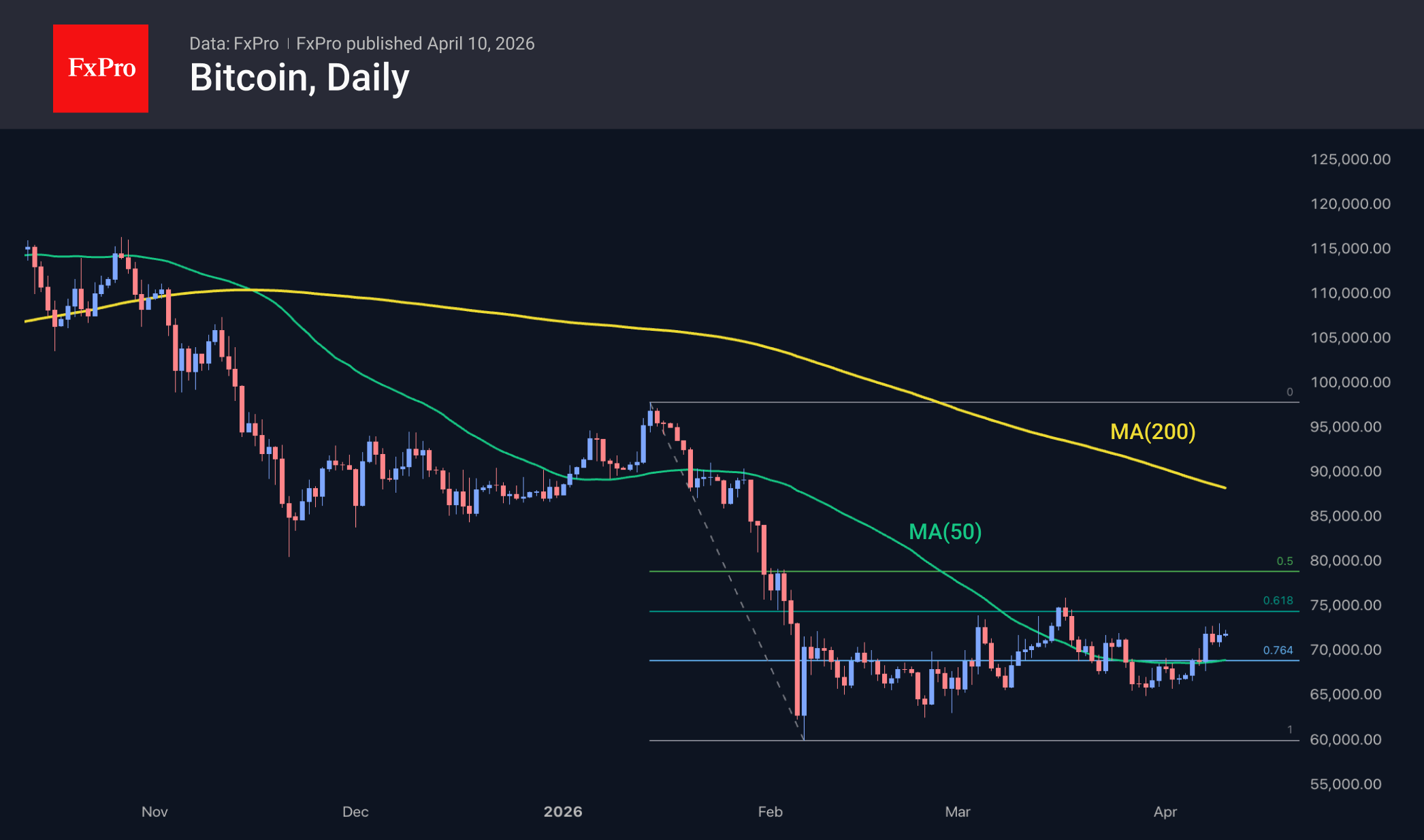

Bitcoin Steadily Reaching New Local Highs

Market Overview

The crypto market capitalisation has risen by 1.19% over the past 24 hours to $2.45 trillion. The crypto market has weathered a short-term consolidation phase following a growth surge quite successfully, consolidating above its 50-day MA, which is one of the first signs of a reversal in the medium-term trend towards a bullish tone. Today’s top performers include Dash (+17.4%), Zcash (+16.6%) and Theta Network (+11%). The underperformers were VeChain (−1.2%), Hedera (−1%) and OFFICIAL TRUMP (−0.9%).

Bitcoin is cautiously testing new local highs, briefly rising above $73K on Thursday, although it is currently trading just below $72K. These fluctuations around local highs and the cautious renewal of them appear to mark a new phase following a prolonged period of hovering near the bottom and a cautious upward trend since late March. However, the market still needs to pass an important test by breaking out of the 61.8% retracement of the decline seen at the start of the year. It cannot be ruled out that the bears are simply giving the market more room to move below their key levels near $75K.

News Background

Standard Chartered forecasts that Bitcoin could fall to $50K in the near term, then recover to $100K by the end of the year. In the long term, the bank’s target price is $500K by 2030.

According to Lookonchain, Bhutan is preparing to sell $22.7 million worth of Bitcoin. The country’s government has transferred 319.7 BTC to two different wallets. Publicly listed mining company Cango sold 2,000 Bitcoin for $143 million in March to repay debts.

US bank Morgan Stanley has launched its own spot Bitcoin ETF with reduced fees. Demand for digital gold from high-net-worth clients remains high, the bank notes.

According to CryptoQuant, trading volume on centralised crypto exchanges fell by 48% from its October 2025 peak to $4.3 trillion in March, reaching its lowest level in the last five months.

On 9 April, the Catchain 2.0 update was successfully activated on the TON network, increasing throughput tenfold. According to Pavel Durov, the blockchain now creates blocks six times faster, and transactions “take place instantly, in less than a second”.

USD/JPY: Yen Fared Better, but Energy Rally Not Over

USD/JPY traded at 159.16 on Friday. The yen is retreating slightly but appears less weak than previously, amid a two-week truce between the US and Iran. The decline in oil prices following the announcement of the truce has partially reduced stagflationary risks and provided some support to the Japanese currency.

Investor focus is on the upcoming talks in Islamabad, where Vice President JD Vance will lead the US delegation. Meetings with the Iranian side are expected to clarify the prospects for further de-escalation.

However, sentiment remains subdued. Continued strikes in the region and ongoing disruptions in the Strait of Hormuz continue to put the fragile truce at risk, driving ** market uncertainty.

The yen has remained under pressure since the conflict began, losing approximately 2%. Investors are factoring in rising energy prices, which add to inflationary pressures while dampening Japan's growth outlook.

The market is now awaiting signals from Bank of Japan Governor Kazuo Ueda ahead of the 28 April meeting, which could set the future direction of monetary policy.

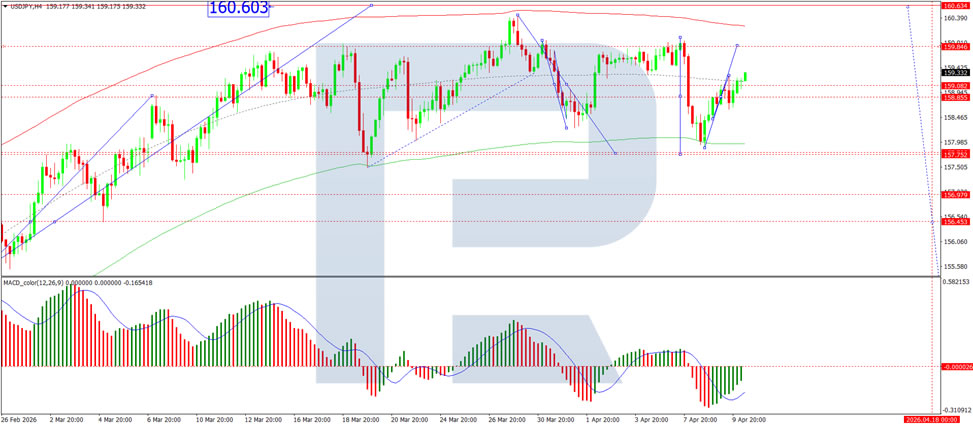

Technical Analysis

On the H4 USD/JPY chart, the market is forming a consolidation range around the 158.85 level, currently extending up to 159.30. A move higher towards 159.85 (testing from below) is expected today. Subsequently, a potential decline towards the 157.72 level will be considered. Technically, this scenario is confirmed by the MACD indicator, whose signal line is below zero and pointing upwards from low levels.

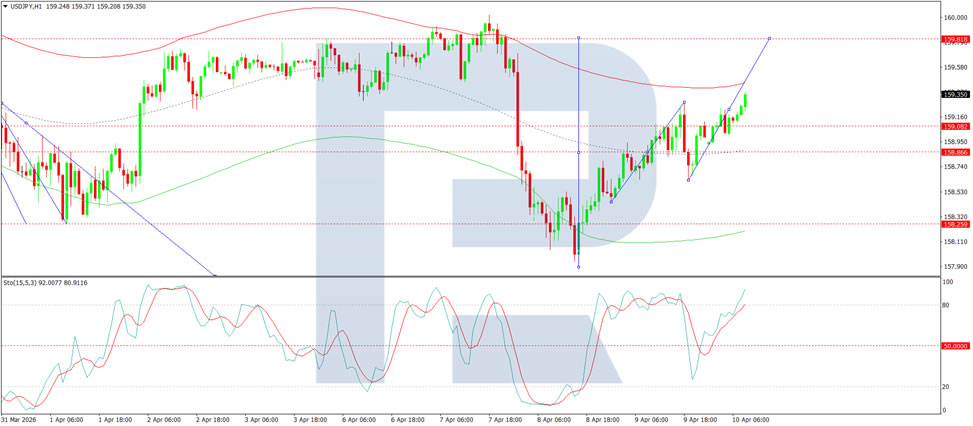

On the H1 chart, the market is forming a wave of growth towards the 159.82 level. A wave extension to the 160.00 level is possible. Thereafter, a downward wave to at least 158.85 is expected. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line below the 80 level and pointing strictly downwards.

Conclusion

USD/JPY has stabilised as the yen shows tentative signs of recovery, benefiting from the temporary truce between the US and Iran and the resulting pullback in oil prices. However, the fragility of the ceasefire – underscored by continued strikes and disruptions in the Strait of Hormuz – means that energy-driven risks remain very much alive. The yen has lost approximately 2% since the conflict began, and market attention now turns to upcoming diplomatic talks in Islamabad and BOJ Governor Ueda's signals ahead of the 28 April policy meeting. Technically, a short-term bounce in USD/JPY appears likely, but the broader trajectory will depend on whether de-escalation holds or tensions reignite.