Sample Category Title

US Inflation Data Provides First ‘Hard’ Evidence on Economic Fall-out from the Conflict

Markets

Markets yesterday were looking for a new short-term equilibrium/new starting point as a next phase in the Middle East conflict had started. Earlier this week markets were pushed back and forth by consecutive U-turns as the war between the US and Iran unfolded. The ceasefire announced Wednesday morning avoided an outright escalation and triggered an impressive relieve short-squeeze. However, markets soon realized that reaching a sustained military & political solution faces multiple high hurdles. With Iran only allowing minimal, highly selective and strictly controlled passage through the Strait of Hormuz any relieve to supply disruptions (and price pressure) is probably hard to imagine. Israel agreeing to hold talks with Lebanon intraday eased overall market ‘hesitation’ to some extent. After Wednesday’s sharp decline, Brent oil yesterday rebounded to the $97 p/b area. This also triggered a partial reversal of Wednesday’s easing on interest rate markets. German yields rose between 2.8 bps (2-y) and 5.9 bps (30-y) with similar moves visible in the UK as markets try get further insight in the ECB’s and the BoE’s reaction function. Moves in US yields again were more modest with yields easing between 2.6 bps (5-y) and -0.2 bps (30-y). With policy still slightly above neutral, the US central bank still has some more room to maneuver with the March inflation data to be published today a first post-war reality check. A $22 bln US 30-y Treasury Bond sale tailed slightly and only met mediocre investor interest even as the yield (4.876%) was the highest monthly result since July. Equities took a breather after Wednesday’s aggressive squeeze higher (EuroStoxx 50 -0.29%; S&P 500 +0.62%). The dollar stayed on the backfoot. DXY closed at 98.8 from an open near 99.15. EUR/USD closed near 1.17. The yen still underperforms (USD/JPY close just below 159).

Asian equities this morning mostly hold a constructive bias looking forward to the US-Iran negotiations scheduled to take place in Islamabad staring tomorrow. Oil at the same time shows no clear bias (Brent $96.75). The dollar also shows no clear direction (DXY 98.9, EUR/USD 1.169, the yen still underperforms (159.3)). Aside from headlines on developments/negotiations regarding the conflict in the Middle East, US inflation data to be published today provides a first ‘hard’ evidence on the economic fall-out from the conflict. We expect US headline inflation to jump to 3.3% Y/Y (from 2.4%). The rise in core inflation for now is expected to be ‘limited‘ to 2.6% Y/Y (from 2.5%). It will be interesting to see the reaction of US markets especially in case of a higher than expected outcome. Inflation expectations measures from the U. of Michigan consumer confidence survey also deserve more than average attention.

News & Views

The Bank of Korea left its policy rate unchanged at 2.5%. The central bank kept a balanced assessment on the impact of the war in the Middle East which poses both downside growth and upside inflation risks. CPI inflation for the year is expected to considerably exceed the February forecast of 2.2%, while core inflation is also likely to be somewhat higher than the previous forecast of 2.1%. If the current shocks (energy, other commodities, supply chain disruptions) are prolonged, leading to a broadening of inflationary pressures and heightened inflation expectations, a monetary policy response is required. Departing BoK governor Rhee compared the current situation with the aftermath of the Russian invasion in Ukraine. While the economy is currently in a moderate recovery instead of facing pent-up demand, it is more vulnerable to rising inflation (expectations) because of the weaker currency and the potential for faster pass-through in prices. South Korean money markets currently discount two to three rate hikes by the BoK for this year.

The OECD’s new chief economist, Scarpetta, warned that governments that cut fuel taxes after the start of the Iran war must swiftly phase out those costly subsidies. Scarpetta said that such initiatives helped fuel inflation, store up fiscal problems and blunt incentives to cut dependence on fossil fuels. Any measures should be targeted at low-income households and energy-intensive businesses. Earlier this week, also the EC warned against turning the current energy crunch into a fiscal crisis.

EUR/USD Daily Outlook

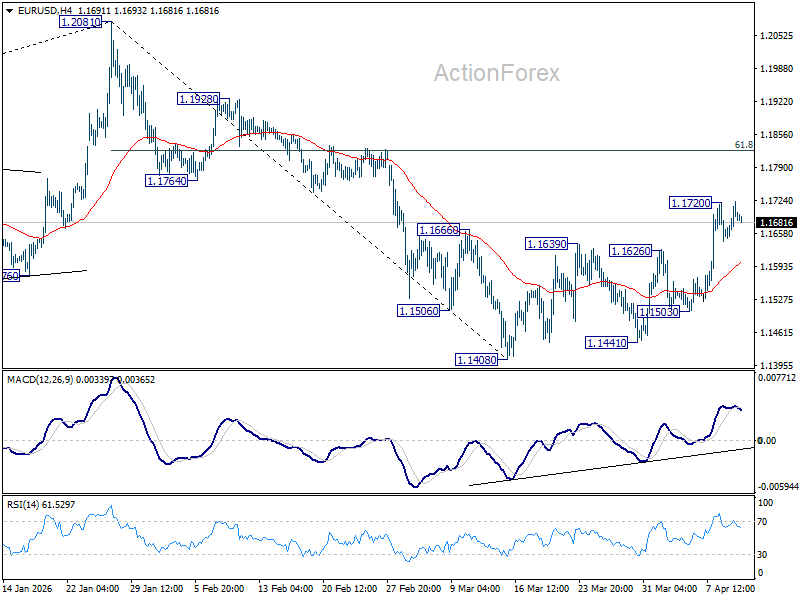

Daily Pivots: (S1) 1.1658; (P) 1.1692; (R1) 1.1733; More….

Intraday bias in EUR/USD stays neutral at this point. Further rise is expected as long as 55 4H EMA (now at 1.1596) holds. Fall from 1.2081 could have completed as a correction at 1.1408. Above 1.1720 will resume the rise from 1.1408 to 1.8% retracement of 1.2081 to 1.1408 at 1.1824. However, sustained break of 55 4H EMA will suggest that the rebound has completed, and bring retest of 1.1408 low instead.

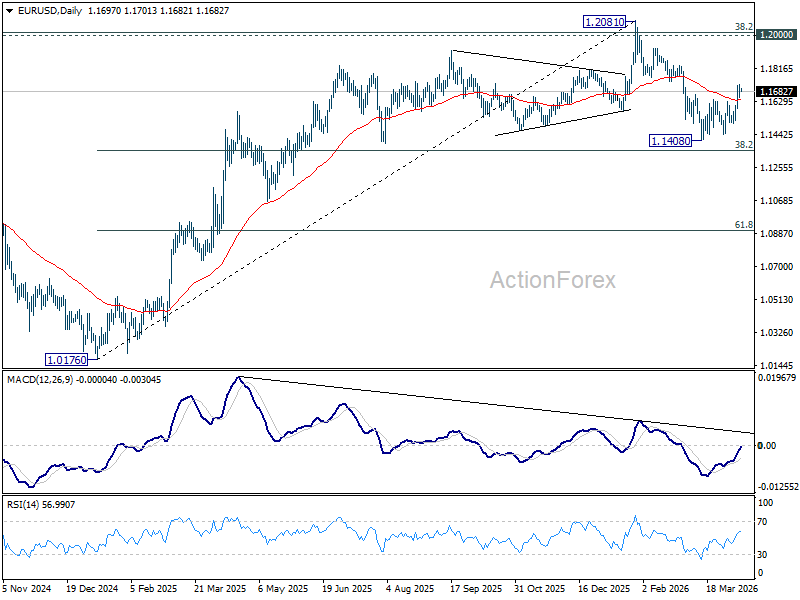

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1505). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

USD/JPY Daily Outlook

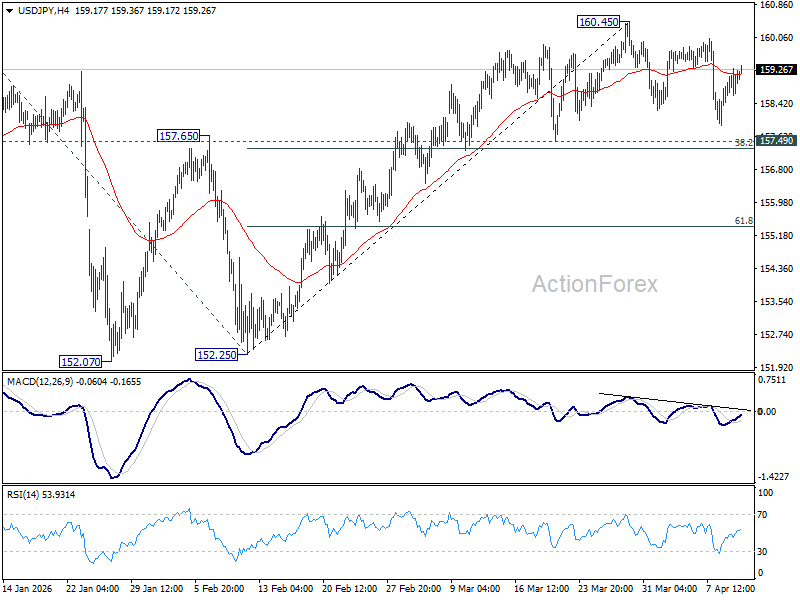

Daily Pivots: (S1) 158.54; (P) 158.92; (R1) 159.38; More...

USD/JPY is still extending consolidations below 160.45 and intraday bias stays neutral. Further rise is expected as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. Firm break of 160.45 will resume the rise from 152.25 to retest 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

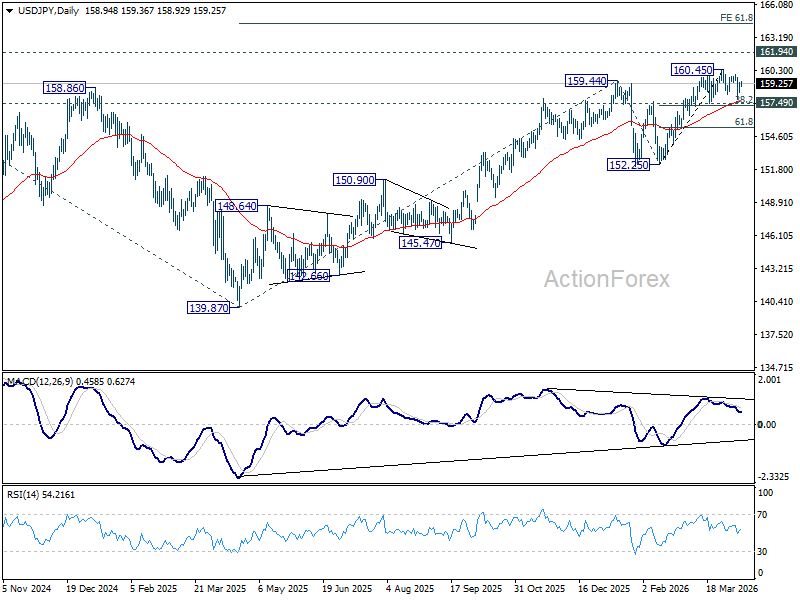

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.97) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

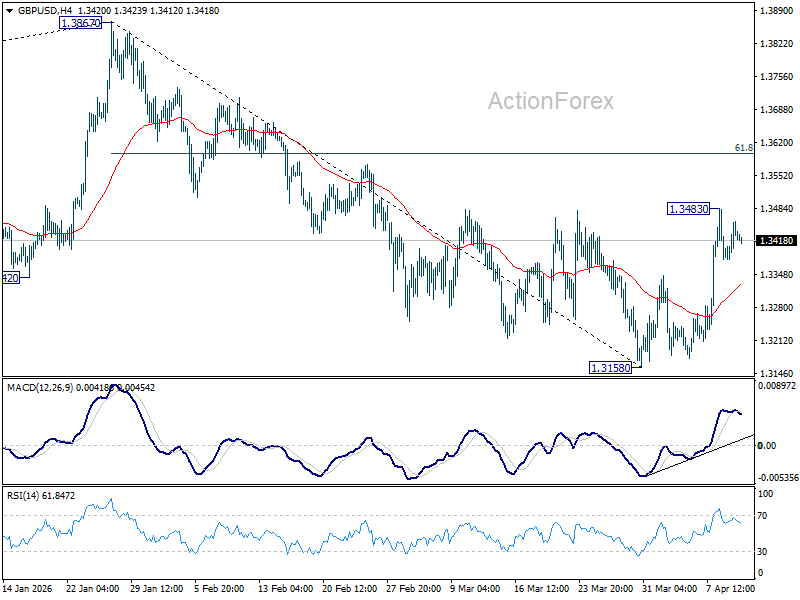

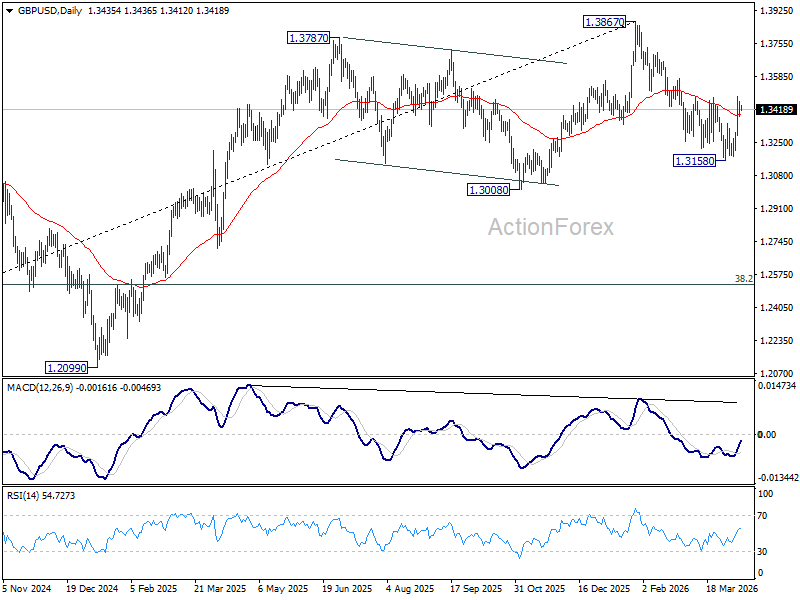

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3392; (P) 1.3425; (R1) 1.3470; More...

Consolidations continue below 1.3483 temporary top and intraday bias in GBP/USD remains neutral. Fall from 1.3867 could have completed as a correction at 1.3158 already. Above 1.3483 will target 61.8% retracement of 1.3867 to 1.3158 at 1.3596. Firm break there will bring retest of 1.3867 high. Nevertheless, sustained break of 55 4H EMA (now at 1.3328) will dampen this bullish view and bring retest of 1.3158 instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

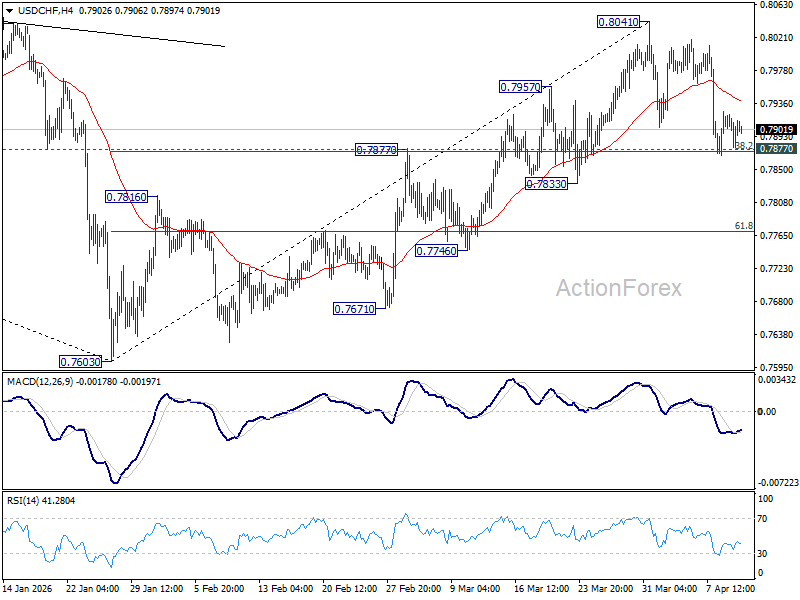

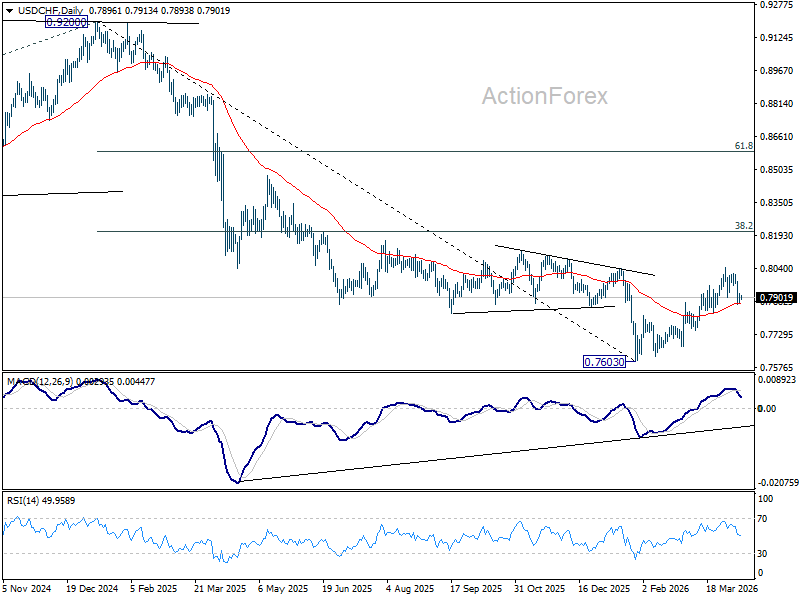

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7881; (P) 0.7903; (R1) 0.7927; More….

Intraday bias in USD/CHF remains neutral and outlook is unchanged. With 0.7877 cluster support (38.2% retracement of 0.7603 to 0.8041 at 0.7874) intact, rally from 0.7603 is expected to resume through 0.8041 later. However, decisive break of 0.7874/7 will argue that the rise has completed, and bring deeper fall to 61.8% retracement at 0.7770 and below.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. rejection by 55 W EMA (now at 0.8081) will affirm this case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

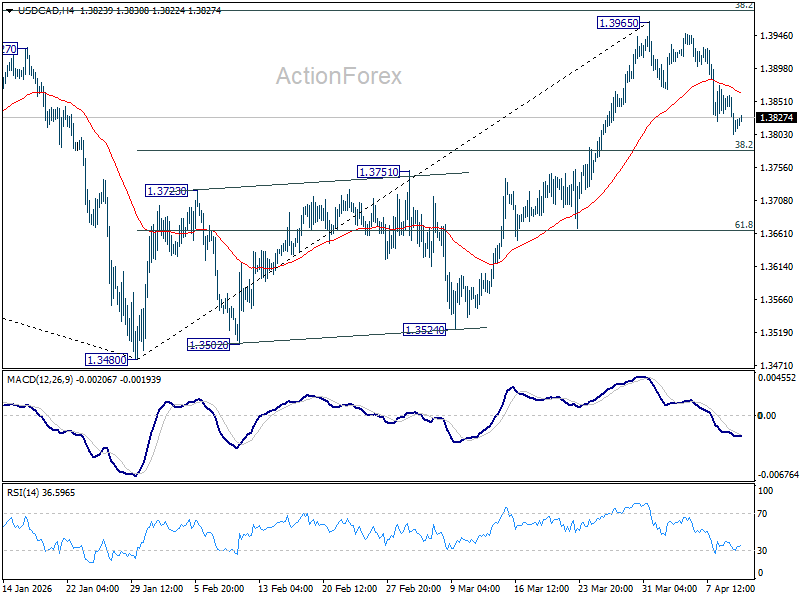

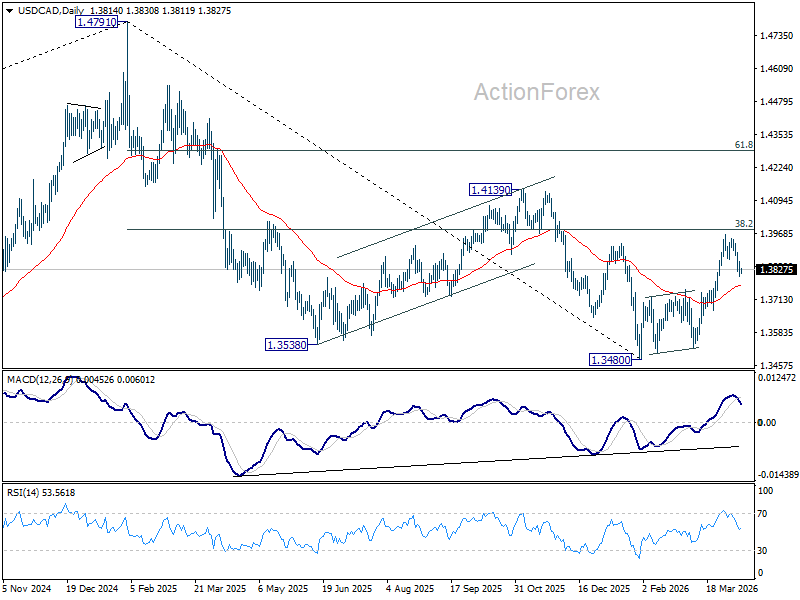

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3793; (P) 1.3827; (R1) 1.3849; More...

Intraday bias in USD/CAD stays neutral at this point. Consolidations from 1.3965 could extend. But as long as 38.2% retracement of 1.3840 to 1.3965 at 1.3780 holds, further rally is in favor. Break of 1.3965 will resume whole rise from 1.3480. However, sustained break of 1.3780 will argue that the rebound from 1.3840 has completed, and bring deeper decline to 61.8% retracement at 1.3665 and below.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

Middle East Tensions Weigh on Markets as Inflation Data Takes Focus

In focus today

The most important US data release of the week will be the March flash CPI this afternoon. We expect headline inflation to pick up to +0.9% m/m SA and 3.3% y/y (Feb: +0.3% m/m SA & 2.4% y/y) due to higher energy prices. We expect core inflation to remain much more steady at just +0.2% m/m SA and 2.6% y/y (Feb: +0.2% m/m SA & 2.5% y/y), anchored especially by the still low housing contribution.

In Norway, March inflation figures are released today. We expect that food prices will fall somewhat more than last year, because Easter sales have started earlier. On the other hand, prices of imported goods, other than food, fell more than usual last year, so we believe that annual growth here will pick up, despite the somewhat stronger exchange rate. We also believe that annual growth in service prices will pick up, because of base effects. Hence, we expect that core inflation will increase to 3.1% y/y in March

On Sunday, the election in Hungary will be pivotal for political developments in the European Union in the coming years. Prime Minister Viktor Orbán risks losing to Péter Magyar, whose Tisza party is polling at 48% compared with Orbán's Fidesz at 39%. Over the years, Orbán has become a contentious figure in Brussels, criticised for weakening the rule of law at home and for impeding EU efforts to sanction Russia after its invasion of Ukraine. He has also threatened to block the EU's next seven-year budget for 2028-2035, which affects the EU's funding outlook. Péter Magyar, a former Orbán ally, is campaigning on rebuilding trust with the EU and NATO, restoring the rule of law and joining the euro area by 2030. However, he does not signal a clear break from Orbán's approach, shares several core positions and is neither seeking an abrupt cut in ties with Russia nor advocating the provision of military aid to Ukraine.

In Denmark, we expect inflation to have risen to 1.3% in March from 0.7%, primarily due to energy prices. A significant driver is that a sharp drop in electricity prices from March 2025 is no longer part of the inflation measure, although electricity market prices fell again in March 2026. Additionally, we will be watching closely to see if the downward trend in food inflation has persisted.

Economic and market news

What happened overnight

In China, March inflation data presents a mixed picture. PPI surprised to the topside and rose 0.5% y/y (cons: +0.4), driven by rising costs in energy-intensive industries. This is the first rise in factory-gate prices since September 2022. Conversely, CPI slowed to 1% y/y and fell 0.7% m/m, making China the only Asian economy with a m/m CPI decline in March. The figures spark worries that imported inflation could pressure corporate margins and complicate Beijing's growth and policy outlook, especially as external demand remains fragile. Furthermore, it underscores the challenge of balancing inflation risks with efforts to stabilise domestic demand.

What happened yesterday

In the Middle East, ship traffic through the Strait of Hormuz remains paralysed at less than 10% of normal levels, despite a US-Iran ceasefire. Iran is directing vessels to transit near Larak Island, citing mine risks, and reports suggest it may impose cryptocurrency transit tolls, an idea strongly opposed by Western leaders and the International Maritime Organization. Brent crude futures are priced at USD 96/bbl at the time of writing. On Thursday, President Trump criticised Iran for "doing a very poor job" of allowing oil shipments through the strait, stating this was not the agreement they had reached. Peace talks between the US and Iran, mediated by the Pakistani prime minister, are scheduled to begin on Saturday, but tensions remain high due to disagreements over the agenda. Iran insists on its ten-point plan, which White House Press Secretary Karoline Leavitt claims President Trump "literally threw in the garbage." Further complicating the situation are disputes over whether the ceasefire terms should extend to Lebanon, after Israel's deadly attacks there on Wednesday.

From the US, February PCE inflation picked up as expected, with the headline index rising 0.4% m/m and 2.8% y/y. Core PCE inflation, which excludes food and energy, increased 0.4% m/m and 3.0% y/y. The data reflects persistent inflation pressures, which are likely to intensify in March due to the war-driven surge in energy and food prices. Meanwhile, consumer spending rose 0.5% m/m, supported by tax refunds, though elevated gasoline prices may weigh on broader consumption ahead.

In Poland, The Bank of Poland (NBP) kept the key rate unchanged at 3.75% at yesterday's meeting, in line with consensus expectations. Governor Glapiński emphasised that interest rates are unlikely to change in the near future, with developments in the Middle East remaining a key factor for the bank's decisions.

Equities: Equities continued higher yesterday, led by the US, and the week is increasingly shaping up as a full reversal on the equity side. We have seen pronounced cyclical outperformance, while low-vol/defensive equities have been aggressively unwound.

With VIX now back below 20, this should serve as a yet another reminder of how markets behave in periods characterised by elevated geopolitical noise, a still-solid macro backdrop, and late-cycle exuberance. In such environments, the behavioural component becomes critical highlighting the risk of 'running after the market' when breaking news hits the screen continuously.

Despite the strong focus on Iran, an equally important theme is unfolding beneath the surface, both for equities and for broader asset allocation, including private equity and private credit. Namely, that 'tech is no longer just tech'. Software continues to lag meaningfully and yesterday was another clear example: software was the worst-performing segment, while semiconductors outperformed sharply, by ~4pp in the US and ~7pp in Europe on the day alone.

Zooming out, this is a continuation of a trend we highlighted months ago in our "When tech disrupts tech" editorial. Over the past nine months, hardware has been the best-performing industry in the US, while software has been the worst, leaving hardware outperforming software by ~125 percentage point (!) over the period.

This morning, Asian equities are trading higher, European futures are pointing up, while US futures are broadly flat.

FI and FX: Markets whipsawed yesterday as initial pessimism around the US-Iran ceasefire and upcoming peace talks reversed in the afternoon, as Israel opened up for talks with Lebanon. President Trump has said that he is "optimistic" about a deal with Iran but has also warned Iran against charging fees for passage through the Strait of Hormuz. The oil price (Brent) almost touched 100 USD/barrel yesterday before dropping sharply to below USD 95 on the Israel-Lebanon news. Subsequently, the price has however moved higher again to around 96-97 USD/barrel. Fixed income markets have largely followed the movements in oil, and looking at US yields, they are now basically unchanged compared to levels from yesterday morning. EUR/USD peaked just above 1.1720 yesterday but now trades just below 1.17. NOK FX was the clear outperformer in G10 space yesterday amid rising scepticism around the Iran ceasefire deal sending energy prices higher while risk appetite stayed decent.

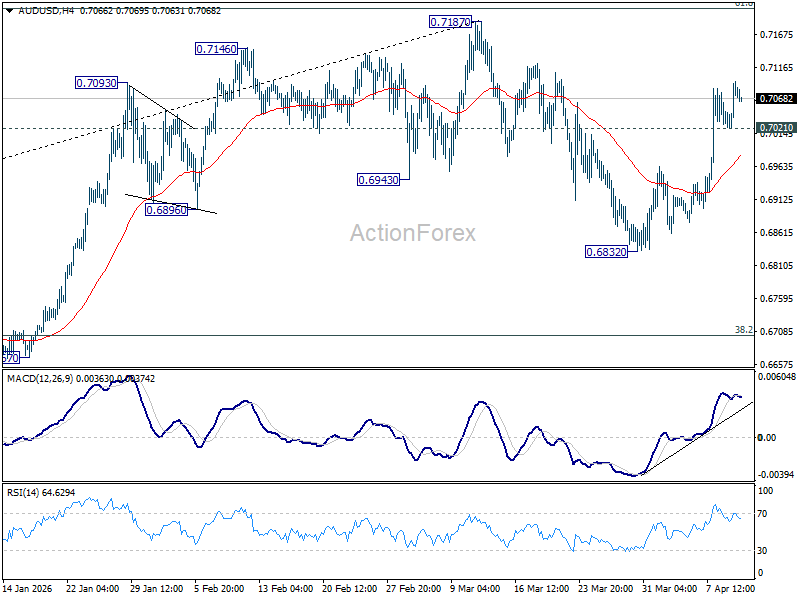

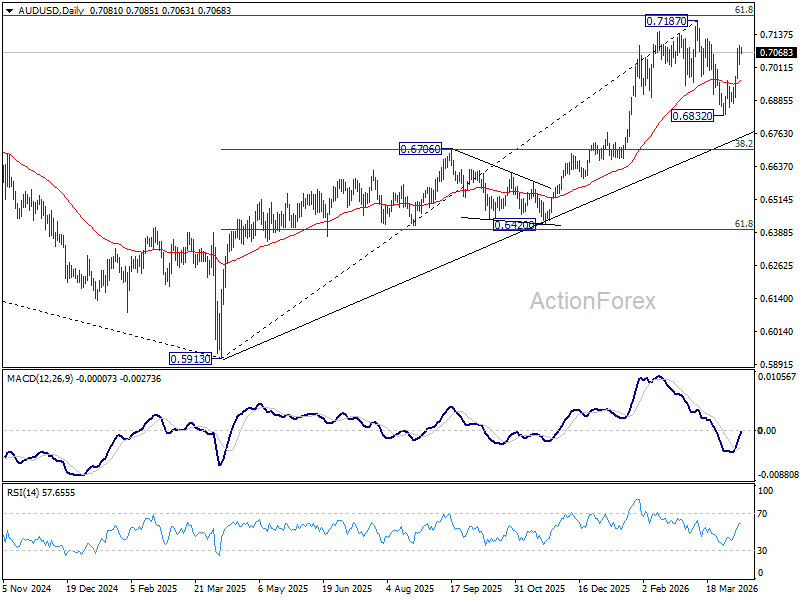

AUD/USD Daily Report

Daily Pivots: (S1) 0.7039; (P) 0.7068; (R1) 0.7113; More...

Intraday bias in AUD/USD remains mildly on the upside as rise from 0.6832 is in progress to retest 0.7187 high. Strong resistance could be seen there to bring another fall to extend the near term corrective pattern. On the downside, below 0.7021 minor support will turn intraday bias neutral again first.

In the bigger picture, as long as 0.6706 cluster support holds, rise from 0.5913 (2024 low) should still be in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). However, firm break of 0.6706 will dampen this bullish case, and bring deeper fall back to 0.6420 support, and possibly below.

US CPI Surge Expected, but Pass-Through Speed and Inflation Expectations Key for Fed

A sharp rise in US CPI is all but certain, with March inflation expected to accelerate from 2.4% yoy to 3.4% yoy on the back of a oil-driven energy shock. But markets are already looking beyond the headline number today. The key question is whether the surge spills into core inflation through second-round effects swiftly and pushes inflation expectations higher. That combination—not the CPI spike itself—will determine whether the Fed sticks to a “look-through” stance by delays its easing cycle further, not cancelling.

Headline inflation is expected to jump sharply, with a 1.0% mom increase largely driven by gasoline prices, which some estimates suggest surged nearly 20% during the month. Core CPI is also seen firming from 2.5% yoy to 2.7% yoy, with a 0.3% mom rise. While the headline spike will grab attention, it is widely understood to be energy-driven.

This distinction matters because the Fed has historically treated energy shocks as exogenous. Monetary policy cannot offset supply disruptions such as a closed Strait of Hormuz, and policymakers have often chosen to look through such volatility unless it feeds into broader inflation dynamics.

That is why the focus shifts immediately to second-round effects. The key issue is how quickly higher energy costs transmit into transportation services, including airfares and shipping, and into food prices. A faster and broader pass-through would signal that inflation is becoming more persistent.

Core CPI is therefore the first test. If underlying inflation trends closer to 3%, it would suggest that second-round effects are already taking hold. That would challenge the Fed’s assumption that the current shock is temporary.

The second, and arguably more important, test comes from inflation expectations. The University of Michigan survey will provide a timely read on whether households see the current price surge as temporary or lasting.

In March, one-year inflation expectations already jumped from 3.4% to 3.8%, marking the largest increase in nearly a year. This rise reflected growing sensitivity to gasoline prices and near-term cost pressures. However, five-year inflation expectations edged down slightly to 3.2%, providing reassurance that long-term inflation credibility remained intact.

That balance could now be tested. A move in one-year expectations above 4%, coupled with a rise in five-year expectations toward 3.5%, would signal that inflation psychology is shifting more broadly. Such a development would likely unsettle the Fed.

For now, markets still lean toward the view that this inflation shock is temporary. If the US-Iran ceasefire holds and oil prices fall back toward $80, the Fed would have both the "economic and political cover" to treat March CPI as an outlier. Under that scenario, the broader disinflation trend would resume later in the year, and rate cuts would be delayed rather than cancelled. The policy path would shift in timing, not direction.

However, all of this ultimately hinges on geopolitics. Developments from the Islamabad talks will determine whether the energy shock fades or intensifies. In that sense, CPI may dominate today’s data calendar, but the real driver of inflation—and Fed policy—lies in whether the conflict moves toward resolution or escalation.

In the currency markets, Dollar remains the worst for the week so far, followed by Yen, and then Loonie. Kiwi is sitting on the top, followed by Aussie, and then Sterling. Euro and Swiss Franc are positioning in the middle.

In Asia, at the time of writing, Nikkei is up 1.95%. Hong Kong HSI is up 0.58%. China Shanghai SSE is up 0.63%. Singapore Strait Times is up 0.09%. Japan 10-year JGB yield is up 0.029 at 2.426. Overnight, DOW rose 0.58%. S&P 500 rose 0.62%. NASDAQ rose 0.83%. 10-year yield rose 0.002 to 4.293.

BoJ’s Himino Sees No Stagflation Yet, Warns of Oil-Driven Policy Dilemma

BoJ Deputy Governor Ryozo Himino said Japan is not facing stagflation for now, with inflation near target and growth still holding up. But he warned that a prolonged Middle East conflict could change that dynamic—pushing inflation higher while dragging on growth and creating a difficult policy trade-off. Read More.

Japan PPI Accelerates to 2.6% in March as Import Costs Surge 7.9%

Japan’s producer prices picked up more than expected in March, driven by a sharp rise in import costs and higher energy and industrial input prices. The surge in import prices points to renewed upstream inflation pressure, raising the risk that cost increases could feed through more broadly into the economy. Read More.

China PPI Turns Positive for First Time Since 2022 as CPI Softens

China’s factory prices returned to growth for the first time since 2022, driven by rising energy and commodity costs. But consumer inflation is losing momentum, with CPI and core prices slowing sharply—highlighting a growing gap between upstream cost pressures and weak domestic demand. Read More.

NZ BNZ Manufacturing Falls to 53.2, Slower Expansion as War Concerns Weigh on Sentiment

New Zealand’s manufacturing sector is still expanding, but momentum is clearly slowing. PMI eased in March as production and new orders softened, while inventories rose—hinting at cooling demand. Read More.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7039; (P) 0.7068; (R1) 0.7113; More...

Intraday bias in AUD/USD remains mildly on the upside as rise from 0.6832 is in progress to retest 0.7187 high. Strong resistance could be seen there to bring another fall to extend the near term corrective pattern. On the downside, below 0.7021 minor support will turn intraday bias neutral again first.

In the bigger picture, as long as 0.6706 cluster support holds, rise from 0.5913 (2024 low) should still be in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). However, firm break of 0.6706 will dampen this bullish case, and bring deeper fall back to 0.6420 support, and possibly below.

China PPI Turns Positive for First Time Since 2022 as CPI Softens

China’s producer prices rose from -0.9% yoy to 0.5% yoy in March, marking the first positive reading since September 2022 and ending a prolonged period of factory-gate deflation. The rebound was driven largely by energy-linked sectors, with non-ferrous metal mining surging 36.4% and smelting rising 22.4%, as higher oil prices pushed up input costs.

In contrast, consumer inflation softened. CPI slowed from 1.3% yoy to 1.0% yoy, below expectations of 1.2% yoy. Core CPI eased from 1.8% yoy to 1.1% yoy. On a monthly basis, CPI fell -0.7%, a sharper decline than the expected -0.2% and reversing February’s 1.0% increase.

While rising commodity prices are lifting producer costs, weak consumer demand and policy measures such as fuel price caps are limiting pass-through to households.