Sample Category Title

Brent Oil Stalls at $100 Ahead of Islamabad Talks, $80 or $110+ Next?

Global markets have shifted from ceasefire euphoria to cautious consolidation, with Brent oil recovering from initial selloff and stabilizing at around $100, as traders await clarity from high-stakes talks in Islamabad. The initial relief rally in stocks has also stalled quickly, highlighting skepticism that the current truce can deliver a lasting de-escalation.

At the center of the current setup is a clear binary outcome. The Islamabad talks mark the first real transition from a “handshake ceasefire” to a potential “verified accord”, and markets are now waiting for concrete terms rather than political signaling.

If negotiations deliver a credible framework—particularly unconditional reopening of the Strait of Hormuz and a defined timeline for clearing maritime mines—the war premium embedded in oil prices could unwind rapidly. In that scenario, Brent could slide back toward the $80 region as supply normalization becomes credible.

On the other hand, if the U.S. delegation (led by JD Vance) and the Iranian delegation fail to agree on the "Red Line"—which the White House has defined as the total end of uranium enrichment—the ceasefire will be viewed as a 14-day window for Iran to refortify the Strait. In this case, Brent will likely slingshot back to $110+ immediately.

For now, the market is treating the ceasefire as "fragile by design", and underlying developments suggest that caution is warranted.. Continued Israeli strikes in Lebanon and reports of Iran reasserting control over Hormuz transit highlight how quickly tensions can resurface, even within the ceasefire window.

Operational realities in the Strait of Hormuz remain a major constraint. Despite reopening narratives, transit is far from normalized. Additionally, the IRGC intermediaries are demanding lump-sum "transit fees" of up to $2 million per passage, often settled in yuan or tether (USDT), for passage through the Strait effectively bakes a permanent cost increase into every barrel of Middle Eastern crude.

Meanwhile, regional oil facilities remain under threat, with Iran striking sites in nearby countries after the ceasefire, including the East-West Pipeline in Saudi Arabia that has been used to bypass the blockaded Strait of Hormuz. Supply disruptions could still persist regardless of diplomatic progress.

Against this backdrop, traders are reluctant to take directional bets. With talks scheduled for Friday, positioning has turned defensive, as market participants reduce exposure to avoid being caught on the wrong side of a potential weekend gap.

For now, oil remains anchored near $100 as markets await confirmation. Islamabad is the immediate catalyst, but the broader question is whether the ceasefire evolves into a durable framework—or simply marks a brief pause before the next escalation.

In the currency markets, selling pressure has shifted to Yen today, as markets react to the lack of any signal from Kazuo Ueda on the possibility of a rate hike this month. Beyond that, trading remains largely range-bound as participants stay cautious ahead of the geopolitical catalyst.

For the week so far, Dollar remains the worst performer, followed by Yen and Loonie. Kiwi leads gains, with Aussie and Sterling also firm, while Euro and Swiss Franc continue to trade in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.41%. DAX is down -1.39%. CAC is down -0.71%. UK 10-year yield is up 0.101 at 4.752. Germany 10-year yield is up 0.06 at 3.011. Earlier in Asia, Nikkei fell -0.73%. Hong Kong HSI fell -0.54%. China Shanghai SSE fell -0.72%. Singapore Strait Times fell -0.38%. Japan 10-year JGB yield rose 0.025 to 2.397.

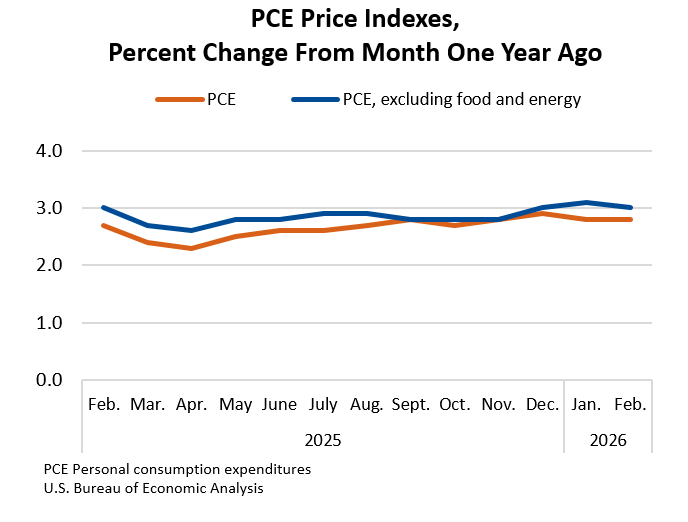

US Core PCE Inflation Eases Slightly to 3% in February

US February data showed a clear split: income declined, but consumer spending remained strong. At the same time, core PCE inflation eased only slightly, highlighting that underlying price pressures are still sticky. Read More.

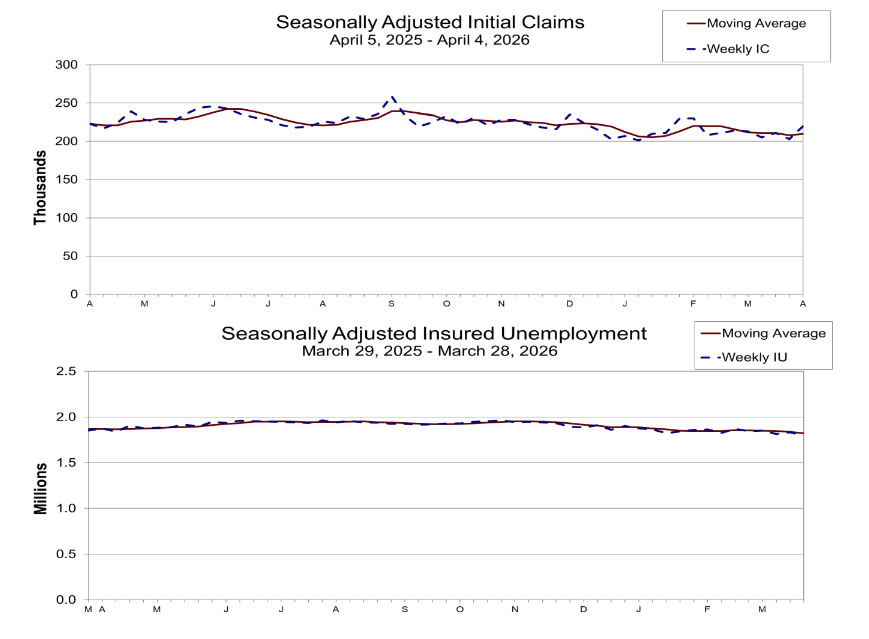

US Initial Jobless Claims Rise but Continuing Claims Signal Labor Market Resilience

US jobless claims data sent mixed signals. Initial claims rose above expectations, hinting at a gradual cooling in labor demand. But continuing claims dropped to their lowest levels since mid-2024, showing that unemployed workers are still finding jobs quickly. Read More.

BoJ’s Ueda: Negative Real Rates Sustain Investment, Warns of Fiscal Crowding-Out Risks

BoJ’s Ueda highlights negative real rates supporting investment but warns rising fiscal spending could lift yields and risk crowding out private sector activity. Read More.

RBNZ’s Breman: Ready to Act Decisively with Rate Hikes if Inflation Jumps

RBNZ Governor Anna Breman delivered a clear hawkish signal: if inflation starts rising again, the central bank is ready to act decisively with rate hikes. With risks now tilted to the upside, easing is off the table as policymakers focus on preventing a renewed inflation surge. Geopolitical tensions and supply disruptions are adding uncertainty, but the policy bias is clear—RBNZ is prepared to tighten again if price pressures build. Read More.

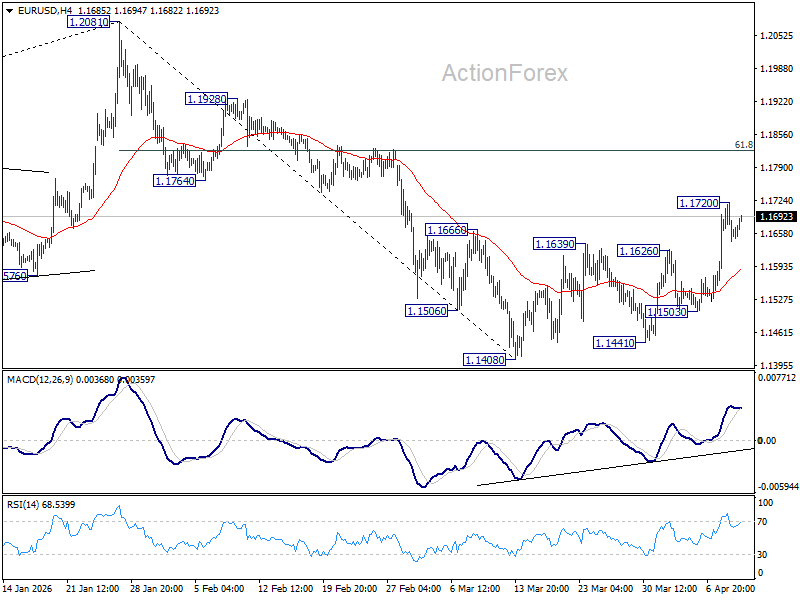

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1593; (P) 1.1658; (R1) 1.1727; More….

Intraday bias in EUR/USD is turned neutral first with current retreat. Some consolidations could be seen but further rise is expected as long as 55 4H EMA (now at 1.1584) holds. Fall from 1.2081 could have completed as a correction at 1.1408. Above 1.1720 will resume the rise from 1.1408 to 1.8% retracement of 1.2081 to 1.1408 at 1.1824. However, sustained break of 55 4H EMA will suggest that the rebound has completed, and bring retest of 1.1408 low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1505). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

US Core PCE Inflation Eases Slightly to 3% in February

In February, US personal income fell -0.1% mom, or USD 18.2B, undershooting expectations of 0.3% growth. In contrast, personal spending rose 0.5% mom, or USD 103.2B, in line with forecasts, pointing to continued consumption strength despite weaker income dynamics.

On the inflation side, PCE price index rose 0.4% mom, while core PCE also increased 0.4% mom, both matching expectations.

Annually, headline PCE held steady at 2.8% yoy, while core PCE edged down from 3.1% yoy to 3.0% yoy, indicating only a modest easing in underlying price pressures.

US Initial Jobless Claims Rise but Continuing Claims Signal Labor Market Resilience

US initial jobless claims rose from 203k to 219k in the week ending April 3, coming in above expectations of 210k and pointing to a modest pickup in layoffs. The four-week moving average also edged higher by 1.5k to 209.5k, suggesting some softening at the margin in labor market conditions.

However, the broader picture remains more resilient. Continuing claims fell by -38k to 1,794k in the week ending March 28, marking the lowest level since May 2024. The four-week average also declined by -13.25k to 1,823.25k, the lowest since June 2024, indicating that unemployed workers are finding jobs relatively quickly.

The divergence between rising initial claims and falling continuing claims highlights a labor market that is cooling but still firm. For policymakers, this mix supports a wait-and-see approach, as the data does not yet point to a meaningful deterioration that would force a shift in the policy outlook.

Gold Outlook: Firm Break of Cracked Key Barrier at $4,759 to Signal Bullish Continuation

Gold keeps firmer tone but trading within a narrow range and under key barrier on Thursday, as traders remain cautiously optimistic about still fragile ceasefire in the Middle East.

Wednesday’s immediate reaction on announcement of a ceasefire between the US and Iran was strong (gold price spiked to $4857, the highest since March 19) but short-lived, as the price subsequently dropped and closed at $4719, leaving Doji daily candle with long upper shadow that indicates indecision but also building offers.

Near-term price action continues to trade between two key boundaries at $4603 (broken Fibo 38.2% of $5419/$4099, acting as support) and $4759 (50% retracement, marking strong resistance) but remains in the upper side of the range and above 100DMA ($4671) that keeps near-term bias bullishly aligned.

Daily studies also provide slight optimism, as the price holds above 100DMA for the sixth consecutive session, converging 10/100DMA are about to form a bull-cross and 14-d momentum has returned to positive territory, while gradually ascending RSI is in neutrality zone).

Bulls need to register a clear break of $4759 Fibo barrier to generate signal of continuation of bull-leg from $4099 (March 23 spike low) that will expose targets at $4915/36 (Fibo 61.8% / daily cloud base) and $5000 (psychological) in extension.

On the flip side, 100DMA offers solid support, ahead of $4600 zone, loss of which would sideline bulls.

However, geopolitical situation is likely to make the biggest contribution to the near-term price direction, with further weakness of the dollar to continue to underpin the yellow metal’s price.

Res: 4759; 4800; 4857; 4915.

Sup: 4700; 4671; 4603; 4553.

Gold Risks Repeating the 1980s Demise

- High interest rates could force central banks to sell gold.

- The US dollar could rise thanks to the Fed’s passivity.

Amidst the turmoil in the Middle East, the US dollar almost missed an important event – the minutes of the FOMC meeting. Now, the Fed began managing expectations, formally maintaining its stance on cutting rates but kicking this idea down the road. In March, Fed officials acknowledged that the chances of inflation slowing down were diminishing, and not just because of the surge in oil prices. The impact of US tariffs on prices will be felt for a long time to come, and Americans’ growing habit of living with high price growth will result in heightened consumer inflation expectations. The Fed indicated that it is closely monitoring upside inflation risks, although it sees a greater threat from a slowdown in the labour market.

News of a ceasefire in the Middle East raised the chances of a policy easing by the end of the year from 12% to almost 50%, but the subsequent publication of the FOMC minutes pushed them back down to 25%. Investors realise that even a stabilisation of current petrol prices will keep prices higher in the coming months, forcing the Fed to keep rates on hold. It is too early to consider monetary policy easing, just as it is too early to count on a rally in EURUSD.

The surge in the main currency pair following news of the ceasefire is largely due to the mass liquidation of long US-dollar positions rather than a targeted bet on the euro’s rise. Until a peace agreement between Washington and Tehran is signed and while oil prices remain high, the eurozone economy remains vulnerable.

Gold was too quick to believe in an end to the conflict and a cut in Fed rates. The opposing sides remain far apart. Donald Trump has declared a total victory and is demanding a large payout from the supposedly defeated Iran. The latter continues to control the Strait of Hormuz.

If the negotiations fail, a situation similar to the late 1970s will arise, when the oil crisis sent US consumer prices soaring. In response, the Fed raised rates to 20%, and gold prices plummeted by 85% between 1980 and 1999. As a result, central banks began actively offloading their gold reserves. For instance, the Bank of England sold 395 tonnes of gold between 1999 and 2002. Some countries, such as Turkey, are beginning to follow suit. This will put a spanner in the works for gold bulls.

Reality Check Hits Markets as Ceasefire Fragility Weighs, US PCE Data in Focus

- Initial euphoria over the US-Iran ceasefire has been replaced by caution

- European equities are retreating, with the STOXX 600 sliding 0.6% and Germany’s DAX shedding 1.3%

- The "peace dividend" is being questioned as Brent crude claws back ground to trade around $97 a barrel

- The high price of oil suggests an inflationary surge is "baked into" upcoming data, leading traders to still price in two 25-basis-point hikes from the ECB before year-end.

The relief rally that swept through global markets on Wednesday has hit a significant roadblock this morning. As we move through the European session, the initial euphoria surrounding the US-Iran ceasefire is being replaced by a cold dose of reality.

Asian Session Recap: Cracks in the Ceasefire

Asian markets started the day on a cautious footing as reports emerged of potential breaches in the fragile two-week truce.

The MSCI Asia Pacific Index slid 0.9%, with Japan’s Nikkei struggling to maintain its footing after yesterday's monster 5.4% rally.The primary concern for the region remains the Strait of Hormuz. Despite the ceasefire agreement, Iran’s continued influence over the waterway and reports of "tolls" for safe passage have kept shipping markets on edge.

The RBNZ also caught some attention, holding rates steady as expected but maintaining a hawkish tilt, warning of further action if the recent energy-led inflation spike becomes entrenched.

European Session: Oil Rebounds, Equities Retreat

The initial euphoria has shifted to caution, with the STOXX 600 sliding 0.6% to 609.59.

The retreat is widespread across the continent:

- Germany’s DAX is leading the downside, shedding 1.3%.

- France’s CAC 40 has retreated 0.7%.

The "peace dividend" that saw oil prices collapse by nearly $20 yesterday is already being questioned. Brent crude has clawed back some ground, trading around $97 a barrel after Tehran warned that the terms of the deal were not being fully respected.

The sector rotation today tells the story of a market moving back into a defensive crouch:

- The Losers: Cyclical and growth sectors are feeling the heat. Industrials are down 1%, while Luxury stocks have plunged 2.3%. Travel, Banks, and Tech have all slipped into the red, surrendering a portion of yesterday's outsized gains.

- The Outperformer: Energy is the lone bright spot, gaining 0.9%. This comes as oil prices creep higher, reflecting the market's skepticism that the supply chokepoint in the Middle East will be resolved anytime soon.

The Inflation "Hangover"

While Brent crude hasn't yet reclaimed the $100 level, a small silver lining for the bulls, it remains roughly 40% higher than pre-conflict levels. This is the "inflationary ghost" haunting the ECB and the Fed.

Even with the ceasefire, the lag in energy costs suggests an inflationary surge is already baked into upcoming data.

Eurozone bond yields are ticking higher today as traders realize that a two-week truce doesn't necessarily mean a dovish pivot. Markets are still pricing in two 25-basis-point hikes from the ECB before year-end.

Currency Markets: The flight-to-safety trade has moderated slightly, but the US Dollar remains resilient.

- EUR/USD is hovering near 1.1660, struggling to extend its recent recovery.

- GBP/USD is sitting around 1.3390, eyeing the 1.3400 handle but lacking the momentum to break through.

- USD/JPY is trading near 158.80, as the Yen remains the laggard in this high-volatility environment.

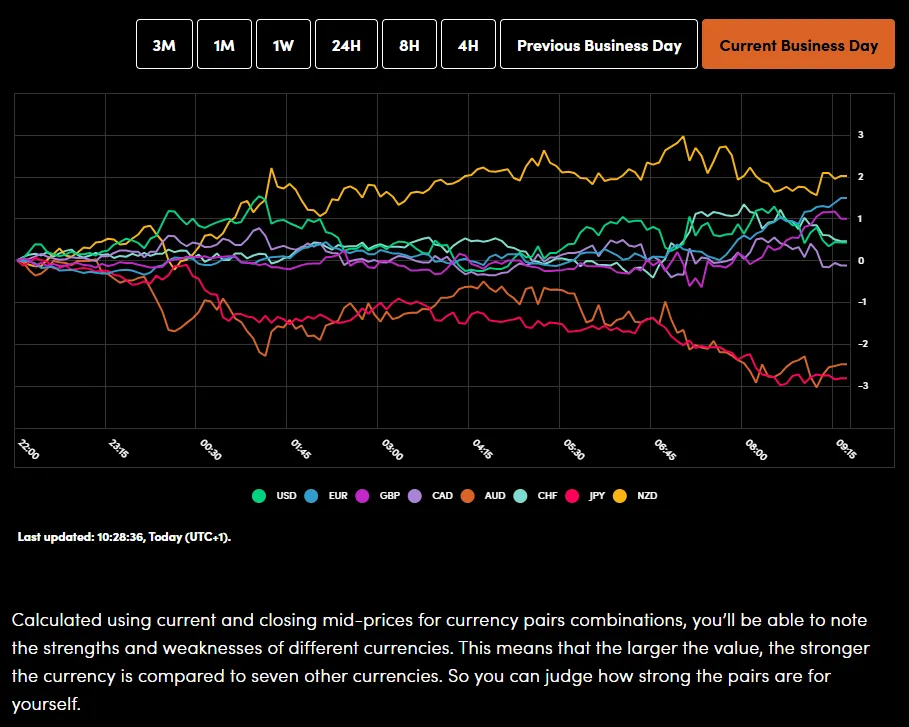

Currency Power Balance

Source: OANDA Labs

The Outlook: All Eyes on Washington and Islamabad

The rest of the day will likely be dominated by headlines regarding the upcoming Saturday morning talks in Islamabad. Markets are desperate for a permanent solution, but the "fragility" of this truce suggests we aren't out of the woods yet.

Key Levels to Watch:

- Brent Crude: $100 remains the psychological line in the sand. A move back above this could reignite stagflation fears.

- S&P 500 Futures: Currently down 0.2%, watch the 5200 level for support if the "reality check" intensifies.

US Core PCE (Due later): We are expecting a 0.4% rise. If this comes in hot, it will remind markets that even if peace holds, the inflationary "hangover" from the last five weeks of conflict is far from over.

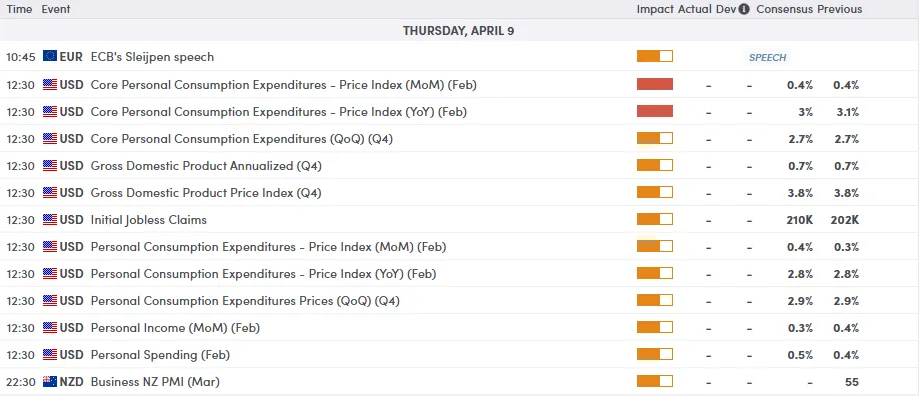

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day - WTI Oil

WTI crude (US Oil) is currently undergoing a "reality check" following the massive sell-off from the $115.00 peak. On the H4 chart, the price action has found immediate support around the $94.00 - $95.00 zone, but the recovery is struggling to clear the 100-period SMA (purple line) currently sitting at $98.89.

The RSI has bounced from oversold territory but remains capped below the 50-midline, suggesting the prevailing momentum is still skewed to the downside. While we are seeing a minor relief rally, the series of lower highs persists.

- Resistance: A break above $100.00 is essential to shift the intraday bias toward a retest of the $107.50 level.

- Support: Failure to hold $94.00 could see a swift slide toward the 200-period SMA (yellow line) near $88.83, which aligns with the key psychological and structural support at $90.00.

WTI Oil Four-Hour (H4) Chart, April 9, 2026

Source: TradingView.com (click to enlarge)

Note: Traders should be wary of "headline risk" today. We saw yesterday how quickly sentiment can pivot on a single announcement. Until we see actual tankers moving freely through the Strait without "tolls" or military escort, the risk remains skewed to the upside for commodities and downside for risk assets.

Stay nimble.

BoJ’s Ueda: Negative Real Rates Sustain Investment, Warns of Fiscal Crowding-Out Risks

Bank of Japan Governor Kazuo Ueda emphasized that monetary policy remains supportive, noting that real interest rates in Japan are still “clearly negative” and keeping financial conditions accommodative.

At the same time, Ueda flagged a potential headwind from fiscal policy. He warned that increased government spending could drive up market interest rates, raising the risk of "crowding out" private sector investment. This reflects concern that fiscal expansion, while supportive in the short term, could complicate the broader policy mix.

Despite these risks, Ueda struck a constructive tone on the outlook for investment. He highlighted that accommodative conditions are already feeding through to a “moderate uptrend” in capital expenditure, suggesting that negative real rates remain an effective transmission channel.

EUR/USD on the Plus Side: Middle East Truce Proves Fragile

EUR/USD rose to 1.1667 on Thursday. The US dollar partially recouped its losses from the previous session, as market sentiment remains cautious amid a fragile truce between the US and Iran.

The situation around the Strait of Hormuz remains tense. According to Iranian media, the passage of tankers is still restricted following new strikes in the region. Iranian representatives have alleged violations of several ceasefire conditions.

The dollar fell sharply the previous day following the announcement of a two-week truce, which led to a drop in oil prices and temporarily eased inflation fears.

An additional factor was the release of the Federal Reserve's meeting minutes. Some participants acknowledged the possibility of raising rates to contain inflation, though many still anticipate subsequent policy easing.

Investor attention is now focused on macroeconomic data, including consumer spending reports, the PCE index, and the upcoming CPI release, which will provide further insight into inflation. All of these could determine the near-term direction of markets.

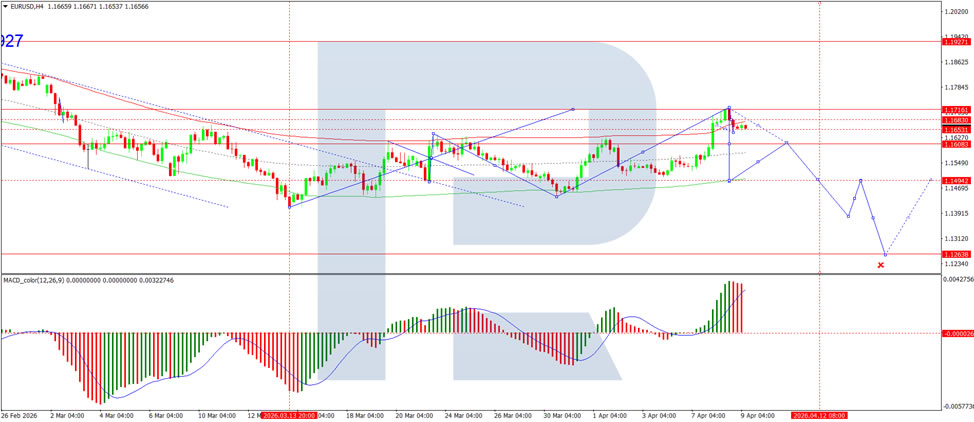

Technical Analysis

On the H4 chart of EUR/USD, the market is forming a consolidation range around 1.1683. A downward wave is expected, with a continuation to 1.1606 as a local target. Subsequently, a move higher back to 1.1683 is anticipated. Technically, this scenario is confirmed by the MACD indicator, with its signal line above zero but pointing firmly downwards, reflecting continued bearish momentum and the potential for the downtrend to persist.

On the H1 chart, the market is forming the structure of the next downward wave to the 1.1616 level. After reaching this level, an increase to 1.1666 is expected, followed by a further decline to 1.1494. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line below 50 and pointing firmly downwards towards 20.

Conclusion

EUR/USD remains on the front foot, though the dollar has managed to claw back some ground as the US-Iran truce shows signs of strain. Reports of continued restrictions on tanker movements through the Strait of Hormuz and alleged ceasefire violations have reintroduced caution into markets. The Fed minutes revealed a divided committee, with some members open to rate hikes while others lean towards eventual easing, adding to the uncertainty. With key US inflation and consumer data on the horizon, the pair's direction remains uncertain. Technically, near-term downside appears likely, but the broader trend will depend on whether the fragile truce holds or geopolitical tensions reignite.

Elliott Wave Outlook S&P 500 (SPX) Eyeing New All Time High

The S&P 500 (SPX) completed its cycle from the April 2025 low on February 2, 2026, when it reached 6991.92. This level is identified as wave (1). Since that peak, the Index has been correcting the entire cycle from April 2025 through a double‑three Elliott Wave structure. From the February high, wave W declined to 6652.56, followed by a recovery in wave X that ended at 6845.08. The Index then resumed lower in wave Y, which extended toward 6318.33. It has since turned higher in wave (3), although a break above the wave (1) high at 6991.92 is still required to fully invalidate the possibility of a second corrective sequence.

From the wave (2) low, wave (i) advanced to 6609.67, and the subsequent pullback in wave (ii) ended at 6474.94. The structure suggests that additional highs remain likely to complete waves (iii), (iv), and (v). This sequence should finish wave ((i)) and conclude the cycle that began from the March 31 low. A corrective pullback is expected afterward before the broader rally resumes. In the near term, the bullish outlook remains valid as long as the pivot at 6318.33 stays intact. Under this condition, any dips should continue to find support within a three‑, seven‑, or eleven‑swing sequence, reinforcing the potential for further upside as the larger trend progresses.

S&P 500 (SPX) 45-Minute Elliott Wave Chart

SPX Elliott Wave Video:

https://www.youtube.com/watch?v=MkTcqq9ty24

European Currencies Strengthen: Dollar Under Pressure Following Ceasefire News

European currencies posted solid gains, while the US dollar came under pressure amid easing geopolitical tensions following reports of a two-week ceasefire agreement between the United States and Iran. Reduced demand for so-called safe-haven assets acted as the primary driver, prompting a reallocation of capital flows towards risk-sensitive instruments and developed market currencies.

Additional pressure on the dollar came from a sharp decline in oil prices, driven by expectations of stabilised supply through the Strait of Hormuz. This has lowered inflation risks and reinforced expectations of a more accommodative stance from the Federal Reserve. At the same time, US Treasury yields declined, further supporting a reassessment of the Fed’s policy outlook. Against this backdrop, money markets are once again pricing in the probability of rate cuts before year-end, limiting the dollar’s recovery potential and reinforcing the current downward momentum.

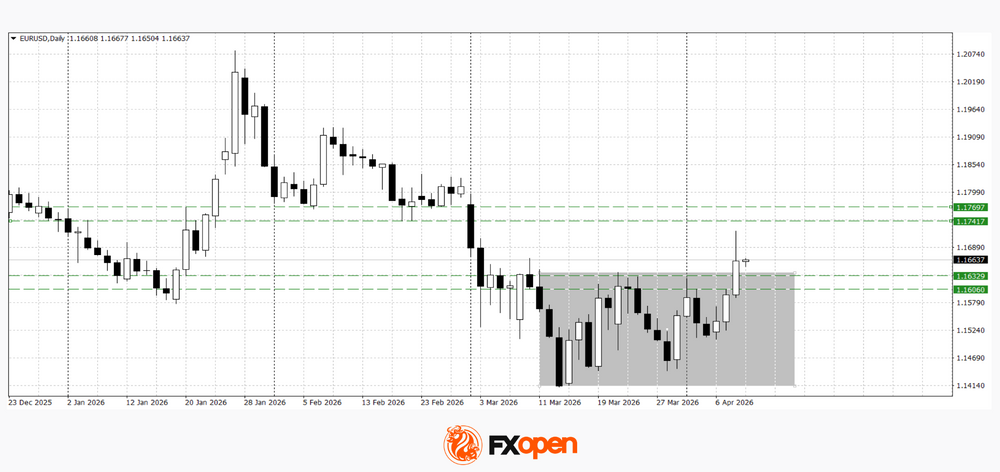

EUR/USD

The EUR/USD pair broke out of its recent range, moving higher in line with broad-based dollar weakness. The price could continue rising towards 1.1740–1.1770. However, a short-term corrective pullback towards former resistance at 1.1610–1.1630 could happen. A daily close below 1.1600 may signal a return to the previous consolidation range.

Key events for EUR/USD:

- Today at 09:00 (GMT+3): German industrial production

- Today at 15:30 (GMT+3): US Core PCE Price Index

- Today at 15:30 (GMT+3): US GDP

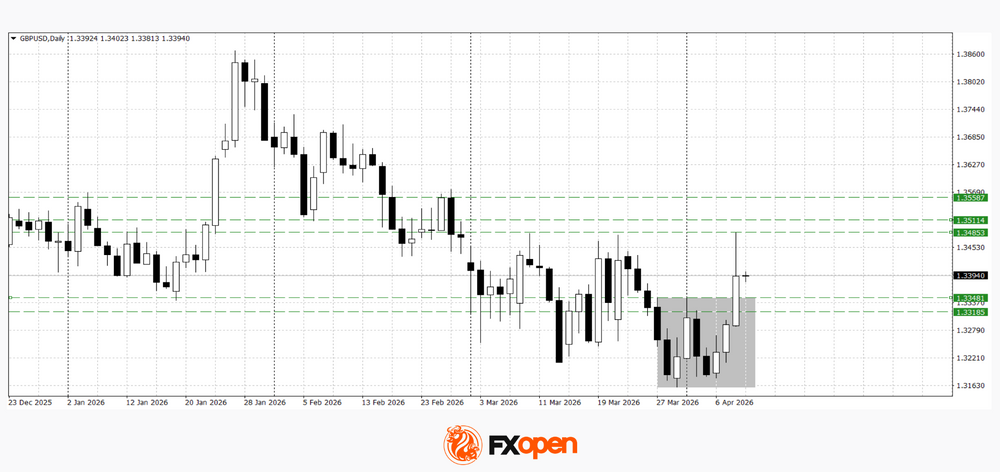

GBP/USD

The GBP/USD pair also broke out to the upside, following the broader trend of dollar weakness. After such a sharp move, a corrective pullback towards the recent highs at 1.3320–1.3350 might be possible. A sustained move above yesterday’s high could open the way for further gains towards 1.3510–1.3560.

Key events for GBP/USD:

- Today at 11:30 (GMT+3): Bank of England Credit Conditions Survey

- Today at 12:00 (GMT+3): UK mortgage rate data

- Today at 15:30 (GMT+3): US initial jobless claims

Summary

The appreciation of European currencies is being driven by a combination of easing geopolitical tensions, declining oil prices, and a reassessment of the Federal Reserve’s policy outlook. The upside breakouts in EUR/USD and GBP/USD reflect a shift in market balance towards risk assets. However, further direction will depend on confirmation from incoming US macroeconomic data. Should downward pressure on yields persist and rate cut expectations strengthen, the dollar may continue to weaken. Conversely, stronger-than-expected data could trigger short-term stabilisation and a return to consolidation.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.