Sample Category Title

Week Ahead – US PPI Data and ECB Meeting Minutes on Tap

- Fed rate cut bets return after ceasefire in Iran war.

- US PPI figures to test whether the Fed could resume rate reductions.

- ECB meeting minutes and UK data to test ECB and BoE expectations.

- Aussie traders await AU employment report and China’s GDP.

Dollar pulls back amid ceasefire in the Middle East

The US dollar started the week on the back foot on hopes that the US and Iran could work things out and end their conflict, and accelerated its tumble on Wednesday after headlines hit the wires that the two nations agreed to a two-week ceasefire, including the reopening of the Strait of Hormuz, through which one-fifth of global oil shipment passes. The White House confirmed that Israel was also on board for the ceasefire.

WTI crude oil dropped as much as 16% on the news and stocks skyrocketed as the news come just a day after US President Trump threatened massive attacks on civilian infrastructure, specifically warning that “a whole civilization will die tonight” if his demands were not met.

The ceasefire and the tumble of oil prices eased inflation fears, prompting investors to start speculating that the Fed may need to resume cutting interest rates following the truce. According to Fed fund futures, there is a nearly 30% chance of a quarter-point cut by the end of the year.

And that’s even after the minutes from the latest FOMC decision showed that a growing group of Fed officials believed that rate hikes may be needed to prevent inflation from spiraling out of control. Perhaps, with the ceasefire now in place, investors were convinced that the surge in oil prices will prove to be temporary as Fed Chair Powell highlighted in his remarks last week.

Focus turns to US PPI inflation data

Next week appears relatively light compared to the previous ones, with the only US releases worth mentioning being the PPI figures for March, due out on Tuesday, as well as the industrial and manufacturing production rates, scheduled to be released on Thursday.

A strong rally in the PPI figures could revive worries that the inflation problem may be more serious than initially thought as higher producer prices now could translate into stickier consumer prices in the following months. Thus, anything suggesting that prices could remain elevated for a while longer may convince investors to scale back their rate cut bets.

Having said that though, conditional upon the truce in the Middle East remaining in effect, this is unlikely to revive rate hike bets and thus, the dollar is unlikely to stage a meaningful recovery.

After all, although rate paths were lowered elsewhere as well, most major central banks are still expected to proceed with rate hikes, which marks a divergence between them and the Fed. The ECB is still expected to press the hike button twice this year, while 30bps worth of rate increases are penciled in for the BoE. The probability of a BoJ rate hike later this month remains a coin toss and there is a strong 60% chance for the RBA to proceed with the third consecutive quarter-point rate increase at its upcoming meeting in May.

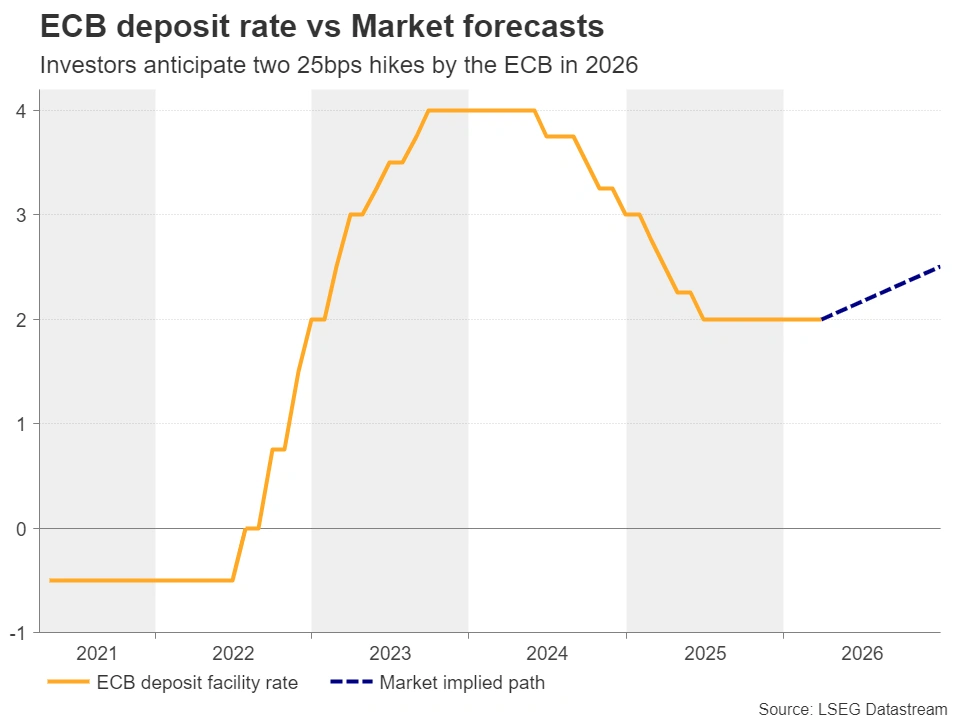

ECB minutes to reveal how willing officials are to hike rates

Speaking about the ECB, the minutes of its latest monetary policy decision, held on March 19, will be released on Thursday. At that meeting, policymakers kept interest rate unchanged but signaled they were closely monitoring growth and inflation risks from surging energy prices amid the war in Iran, adding that they were ready to adjust their strategy if deemed necessary.

More recently, ECB policymaker Dimitar Radev noted that Eurozone inflation expectations were at risk of rising more quickly and that the Bank should be ready to raise rates swiftly. This, combined with the flash CPI data revealing a jump in headline inflation to 2.5% y/y in March from 1.9%, allowed investors to maintain bets of around 50bps worth of rate hikes by the end of the year.

Therefore, euro traders will dig into the minutes to see how willing other policymakers were to shift to rate increases if the situation warrants so. Although the information could be deemed outdated, as the meeting took place amid an escalating war, an intense hawkish flavor could corroborate the notion that the ECB could consider raising interest rates even after the ceasefire, allowing the euro to continue gaining against its US counterpart.

Weak UK data could weigh on BoE hike bets

In the UK, the monthly GDP, the industrial and manufacturing production figures, as well as the trade data, all for the month of February will be released. Weak growth-related numbers even before the war in the Middle East erupted could prompt investors to question whether it will be wise for the BoE to proceed with rate hikes, especially amid a ceasefire.

Thus, receding rate cut bets could weigh on the pound, but with an even weaker US dollar, any pound losses may be more prominent on the euro/pound pair.

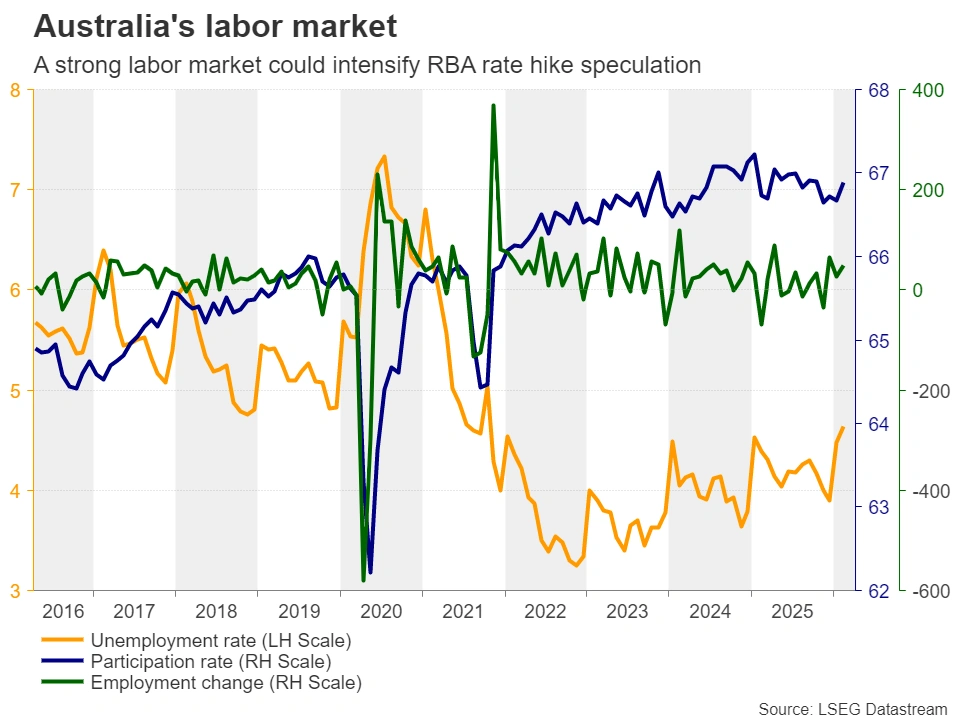

Australian jobs report and Chinese GDP to move the Aussie

The risk-linked aussie was among the currencies that benefited the most amid the truce announcement, surging as much as 1.75% on Wednesday. The increase in risk appetite and the still hawkish RBA rate expectations are very supportive variables for the currency. A strong employment report for March on Thursday could allow investors to take the probability of third straight 25bps hike by the RBA higher and thereby allow further advances in the commodity currency.

Aussie traders are likely to pay attention to Chinese data as well, as China is Australia’s main trading partner. During the Asian session on Wednesday, the world’s second largest economy will release its trade data for March. The GDP for Q1 is due to be released on Thursday, alongside the industrial production, retail sales, fixed asset investment and the unemployment rate, all for March.

Although trade tensions between the US and China have eased, the conflict in the Middle East and the spike in oil prices during the month of March may have left their mark on the Chinese economy, which is the world’s biggest oil importer. If the data suggest that China was able to withstand the pressure, the aussie may strengthen even more.

Oil Just Doesn’t Want to Correct With Persistent Ceasefire Uncertainty – WTI Technical Analysis

- Oil attempted to correct after the latest US-Iran ceasefire announcement

- However, the truce is very fragile and with headlines going back and forth, commodity traders are stuck in the mud

- Exploring an in-depth Technical Analysis of WTI Crude Oil

Traders were just celebrating the latest 2-week US–Iran ceasefire news, but it now seems that Markets got ahead of themselves.

The initial reaction was one of a classic risk unwind – WTI Crude Oil gapped sharply lower from around $118 to $92 as risk premium evaporated almost instantly on the announcement. For a brief moment, it looked like the geopolitical overhang that had fueled oil’s explosive rally was finally unwinding.

But that relief didn’t last.

Since the gap lower, prices have been grinding steadily higher again, now hovering back near the key $100 level — a sign that traders are reassessing just how fragile this truce really is.

Headlines over the past 24 hours have painted a highly uncertain picture:

Iranian officials have stressed that any meaningful peace agreement must extend beyond bilateral talks, explicitly mentioning broader regional considerations, including Lebanon, and warning that the coming hours are “critical.”

At the same time, conflicting narratives between US and Iranian sources have only confirmed that the two sides are still far from trusting each other. What is sure is that traffic in the Strait of Hormuz remains more than muted, if inexistent.

A recent Reuters report indicated 6 crossings in the last 24 hours compared to the usual 140 in the same timespan – That's not the type of progress that Markets want to see.

Odds for a proper US-Iran peace deal – Source: Polymarket. April 9, 2026

This kind of environment is particularly difficult for commodity pricing – Oil thrives on clarity of supply expectations, but current conditions offer anything but that. Instead, participants are stuck in a feedback loop of headline-driven volatility, where each new comment shifts sentiment without establishing a durable trend.

The result is a market caught in limbo — no longer pricing worst-case escalation, but far from confident in a sustained de-escalation.

As WTI breaks the $100 threshold yet again, the next directional move will likely depend less on technicals and more on whether diplomacy can turn from words into verifiable action. Until then, expect volatility to remain elevated and conviction to stay thin.

As the situation looks to be more clear in the coming days, let's dive into a multi-timeframe analysis of WTI (US) Oil to determine levels of interest and put the odds in the trader's favor to capitalize on the issue.

US Oil Multi-Timeframe Analysis

WTI 4H Chart and Technical Levels

WTI Oil 4H Chart – April 9, 2026. Source: TradingView

WTI has seesawed after yesterday's large drop to $92.70 , having already rallied by 11% since.

After touching the oversold RSI border and the bottom of the Pivotal War support (~$93), bulls have raged back into the commodity as uncertainty still looms – A very important test is now coming closer with the 4H 50-period MA ($104.62)

- Breaching back above would put the bullish panic-thesis fully back into action

- Rejecting it however would allow a more rangebound action ahead ($98 to $104 until Markets get more clarity)

- Breaking $98 again hints at a lower range ($92.70 to $98)

WTI Technical Levels:

Resistance Levels

- 4H 50-period MA / 1H 200-MA (~$104.20)

- $106 to $108 June 2022 Resistance

- $110 psychological level

- 2022 and War highs $117 to $120

Support Levels

- $98 to $100 Major Pivot

- War Support Pivotal $93.00 to $95

- $87 to $90 mini-Support (4H 200-period MA)

- 2025 Highs Key Support $78 to $80

- Pre-War Support $63.80 to $64

1H Chart and action levels

WTI Oil 1H Chart – April 9, 2026. Source: TradingView

Looking closer, WTI is once again stuck in uncertain back and forth action.

The 200-Hour MA ($104.18) will be acting as a major barometer for traders.

On the immediate action, the rebound in WTI is stalling as the 1H RSI is back to overbought.

- Traders will surely await for further news before moving on to the next trades

- Keep an eye on a potential rangebound formation from $98 to $104 as Markets await for further clarity.

Keep a close eye on the latest headlines!

Safe Trades!

Sunset Market Commentary

Markets

Correction on a correction? A reality check on an overly optimistic short-squeeze yesterday? Or markets just re-entering low-visibility no-man’s land? Whatever the labeling of the today’s market price action, investors clearly don’t see a good enough reason to build on yesterday’s euphoria triggered by the ceasefire in the war between the US (& Isreal) against Iran. Reportedly, the ceasefire is holding up fairly well except for the Israel’s campaign against Hezbollah which at the same time remains one of many high profile points of discussion between the US and Iran as they prepare for talks in Islamabad this weekend. (Free) passage of shipping through the Strait of Hormuz also faces a huge ‘interpretation gap’ between the parties involved as Iran holds to its point that any passage will be subject to ‘necessary arrangements with the Iranian authorities to securely pass’. This suggests that any normalization of supply from the Persian Gulf probably won’t occur anytime soon. Oil, still one of the better barometers to measure supply obstructions, rebounded from levels just north of $90 p/b yesterday (Brent) to $98 currently. The easing in the TTF Dutch gas reference for now proves to be a bit more resilient (€46 MWh). The Eurostoxx 50, after an outsized 5% gain yesterday, returns 0.7%. US indices open modestly lower (S&P 500 -0.15 %). On yield markets, ECB officials don’t give much of a specific assessment on most recent developments yet. German yields after yesterday’s sharp easing are rebounding between 7 bps (2-y) and +5 bps (30-y). A sideways intraday pattern after a higher open maybe also illustrates some market agnosticism on what to expect both on the geopolitical process as well as on stagflationary risks going forward. US yields in a daily perspective change less than 1 bp across the curve. Data these days, especially if they refer to the pre-war era mostly have little market impact. February US PCE deflators (headline 0.4% M/M and 2.8% Y/Y, core 0.4% M/M and 3% Y/Y) anyway came in as expected, but are holding well above the 2% level going into Iran crisis. Personal income (-0.1%) disappointed. US weekly jobless claims rose a higher than expected 219k , but longer term averages still suggest no major deterioration. As indicated, these data don’t capture much of the post-Iran economic dynamics. In this respect, tomorrow’s US March CPI release is one of the first hard data with potential market relevance.

Despite lingering global uncertainty, the dollar again shows a rather hesitant pattern. DXY eases from 99.05 to 98.90. EUR/USD is holding yesterday’s gain quite easily (EUR/USD 1.169). The yen underperforms with USD/JPY rising from 158.6 to 159.05. Sterling also slightly underperforms the single currency with EUR/GBP returning north of the 0.87 mark.

News & Views

The European Commissioner for Economy Dombrovskis told Members of the European Parliament that nothing prevents EU countries seeking to introduce a windfall tax on energy companies similar to what was done in the wake of the Russian invasion. The raised amount could be used to cushion the blow from the price spike. Dombrovskis said they are looking into a coordinated approach on a European level. He added that other measures are being prepared too, including making sure that electricity is taxed less than fossil fuels. The Commissioner ruled out more radical options such as Italy’s called-for activation of the general escape clause that would temporarily lift the 3% budget deficit rules. “A condition for activating the general escape clause is to have a severe economic downturn in the euro area or European Union. We are currently not in this scenario.”

The Polish central bank kept the policy rate at an unchanged 3.75%. The unusually short policy statement barely touched on domestic developments. Inflation rose to 3% in March, mainly due to a strong surge in fuel prices resulting from the Middle East conflict. The outlook for prices, which next to fiscal policy, fuel price regulations, wage and economic growth is currently strongly influenced by external geopolitical developments, will shape the central bank’s future decisions. The Polish zloty unsurprisingly shrugged at the expected outcome with EUR/PLN hovering around 4.25. Polish swap yields add between 3 and 4.5 bps, joining the broader trend in core euro areas.

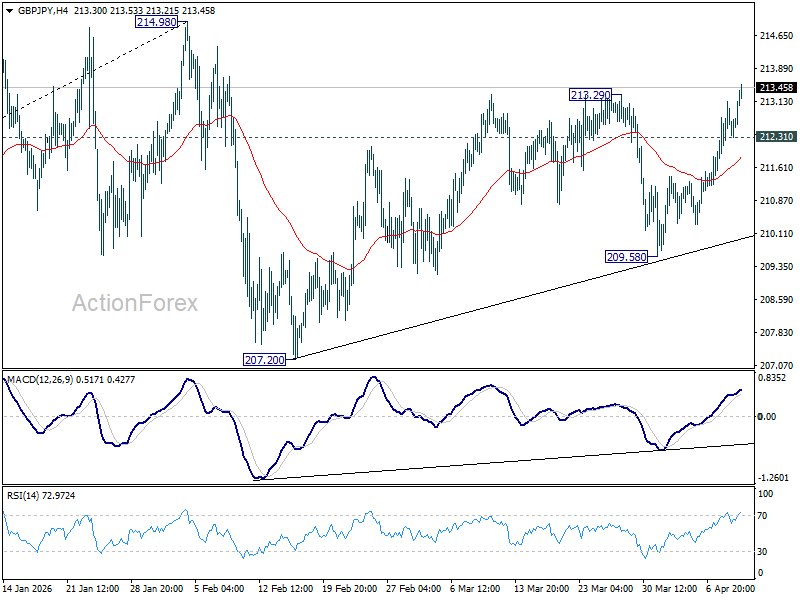

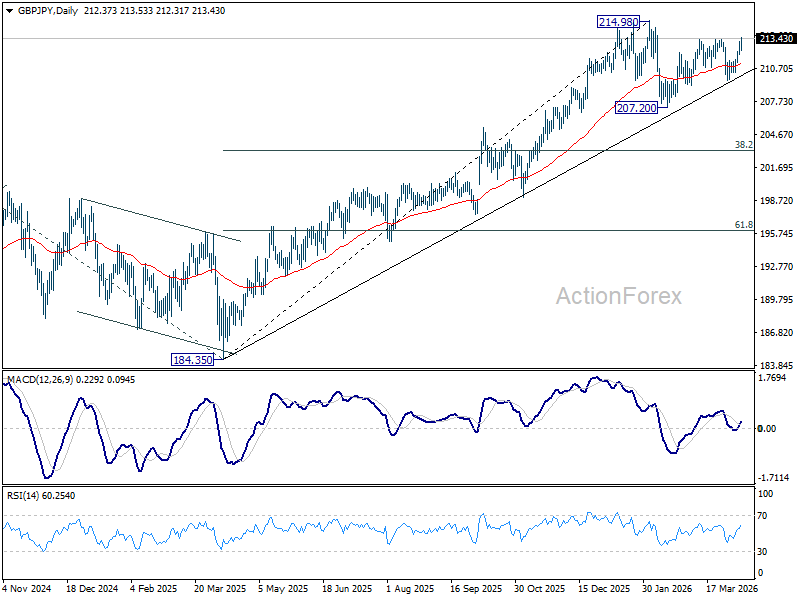

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 211.85; (P) 212.51; (R1) 213.07; More...

GBP/JPY's rise from 207.20 resumed by breaking 213.29 resistance and intraday bias is back on the upside. Further rise should be seen to retest 214.98 high. On the downside, below 212.31 minor support will turn bias neutral first. But risk will now remain on the upside as long as 209.58 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.13) holds, even in case of another deep pullback.

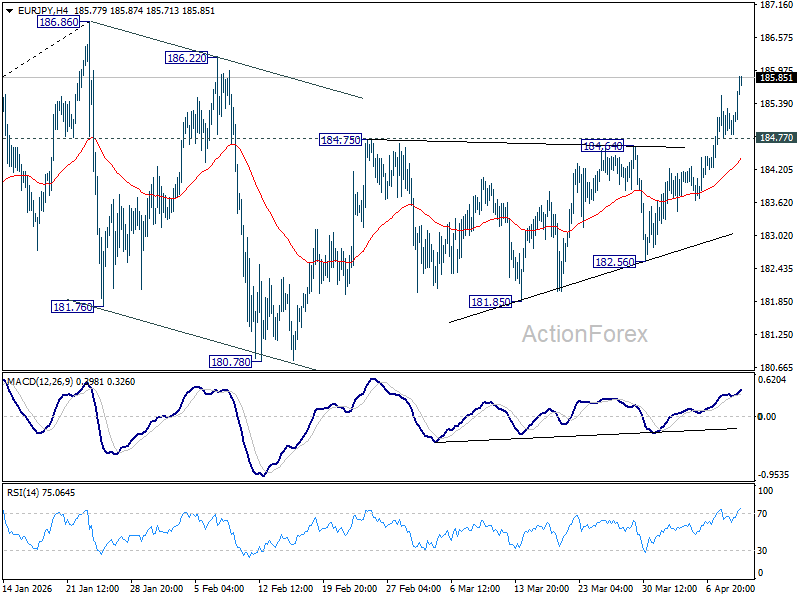

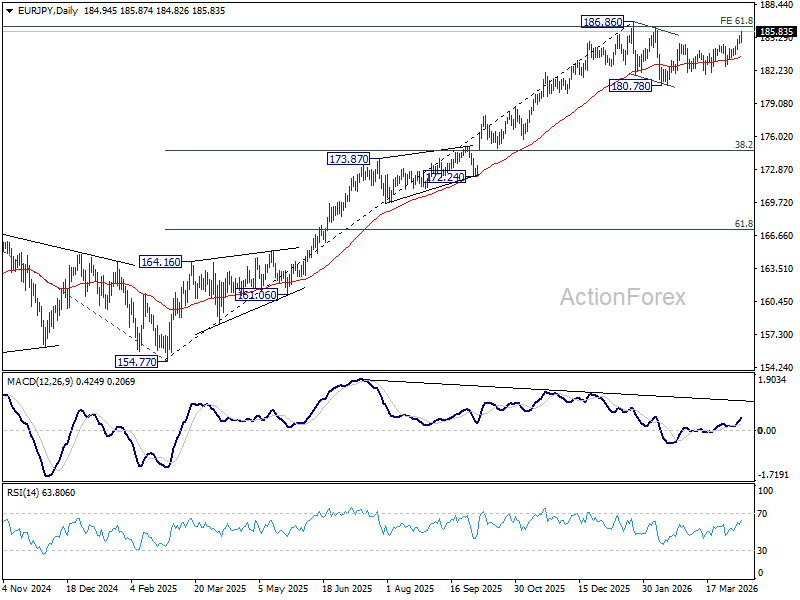

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 184.63; (P) 185.10; (R1) 185.38; More...

EUR/JPY's rally continues today and intraday bias stays on the upside. Rise from 180.78 should target a retest on 186.86 high. Firm break there will confirm larger up trend resumption. On the downside, below 184.77 minor support will turn intraday bias neutral first. But rise will stay on the upside as long as 182.56 support holds, in case of retreat.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 176.21) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

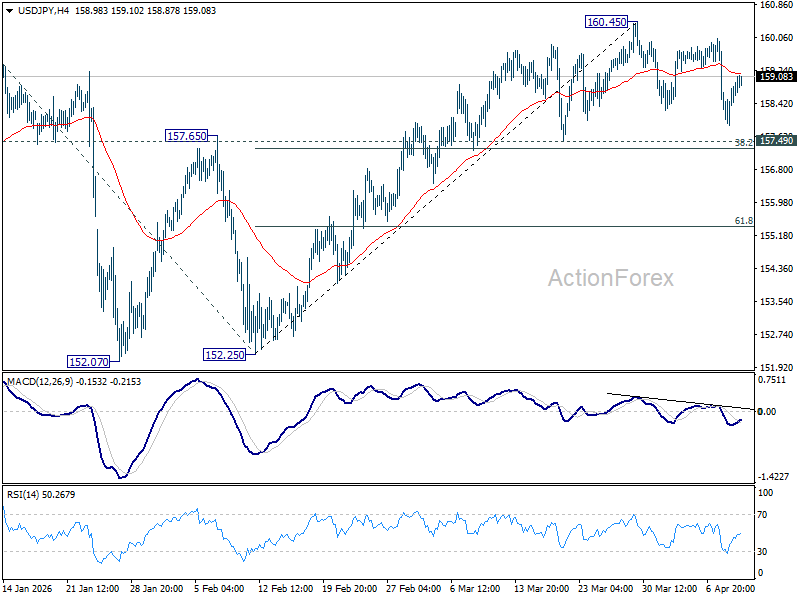

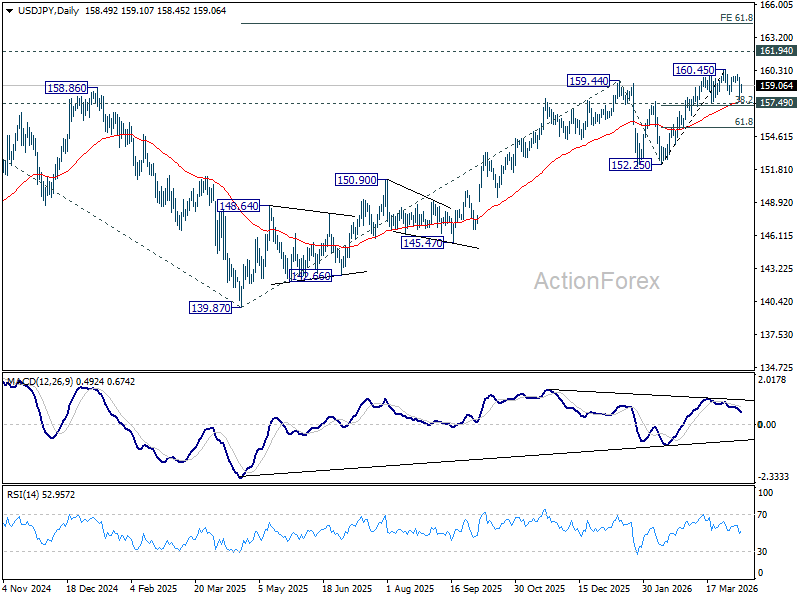

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.72; (P) 158.73; (R1) 159.59; More...

Intraday bias in USD/JPY remains neutral for the moment as consolidations from 160.45 is extending. Further rise is expected as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. Firm break of 160.45 will resume the rise from 152.25 to retest 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.97) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

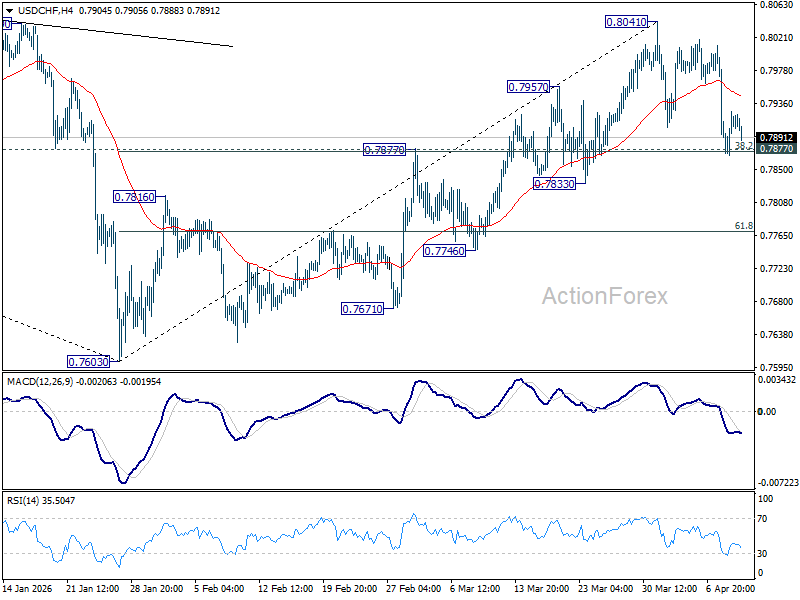

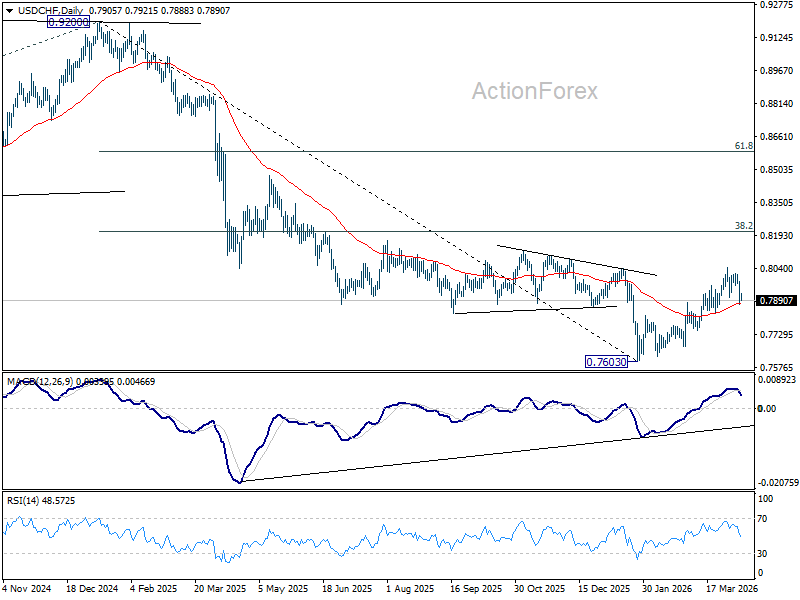

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7855; (P) 0.7927; (R1) 0.7985; More….

Intraday bias in USD/CHF stays neutral for the moment. With 0.7877 cluster support (38.2% retracement of 0.7603 to 0.8041 at 0.7874) intact, rally from 0.7603 is expected to resume through 0.8041 later. However, decisive break of 0.7874/7 will argue that the rise has completed, and bring deeper fall to 61.8% retracement at 0.7770 and below.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. rejection by 55 W EMA (now at 0.8081) will affirm this case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

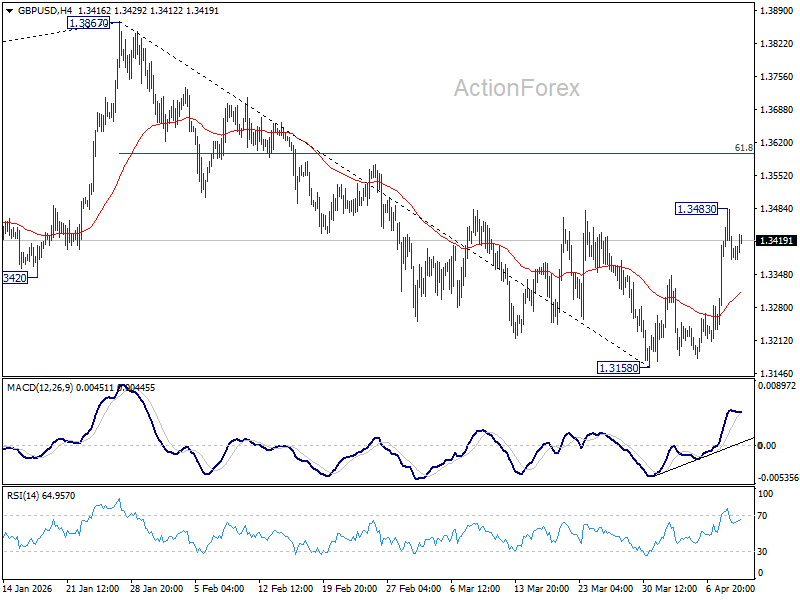

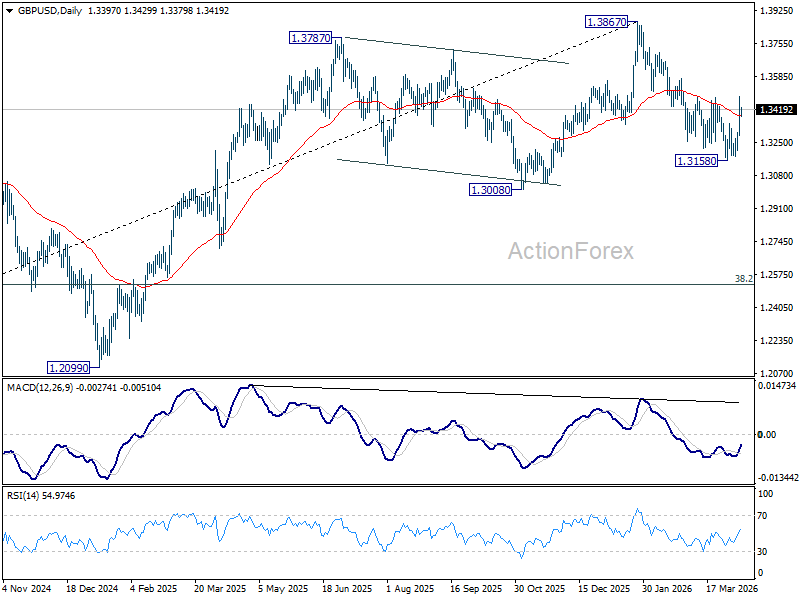

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3293; (P) 1.3389; (R1) 1.3492; More...

Intraday bias in GBP/USD remains neutral and some more consolidations could be seen below 1.3483 temporary top. Fall from 1.3867 could have completed as a correction at 1.3158 already. Above 1.3483 will target 61.8% retracement of 1.3867 to 1.3158 at 1.3596. Firm break there will bring retest of 1.3867 high. Nevertheless, sustained break of 55 4H EMA (now at 1.3312) will dampen this bullish view and bring retest of 1.3158 instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

US: Consumer Spending Remained Soft in February

Personal income edged lower by 0.1% month-over-month (m/m) in February, coming in below market expectations for a 0.3% gain. Adjusting for taxes and transfers, disposable income also declined by 0.1%, following a strong gain in January that was due to the annual cost-of-living adjustment for social security benefits.

Consumer spending advanced by 0.5% m/m in nominal terms, slightly faster than January's 0.3% pace. However, as in the previous month, nearly all of the gain was attributed to higher prices. In inflation-adjusted terms, spending increased by just 0.1% m/m following no growth in January.

Spending on goods edged up by 0.2% m/m in real terms as purchases of cars and parts rebounded by 4.3% m/m. Outlays on other goods either declined or grew only slightly. Spending on services rose modestly (+0.1% m/m), with higher spending on transportation (+0.7%) and healthcare (+0.3%). However, spending on recreational services declined by 0.4% m/m and spending on accommodation and food edged up only slightly (+0.1% m/m).

The personal saving rate declined to 4.0% from 4.5% the previous month.

Inflation remains persistently above the Fed's 2% target. Core PCE— the Fed's preferred inflation gauge— rose by 0.4% in February, matching gains in the prior two months. In annual terms, core PCE inflation was up 3.0%, down slightly from the 3.1% pace seen in January.

Key Implications

Overall, it was a soft start to the year for U.S. consumers. Real spending remained subdued in February, likely restrained by weather-related factors. While spending on autos and parts rebounded, dining out and recreation remained weak, likely due to the weather. With the recent spike in gasoline prices, attention is now focused on the March report. Some rebound in spending is expected with improved weather, but the report will also be closely watched for signs of consumers pulling back on discretionary purchases amid high prices at the pump.

Headline inflation is expected to jump on higher prices in March, however, it's likely too soon for the second order price effects to show up in core inflation. This is where the uncertainty lies – the longer prices stay elevated – the larger the risks that firms outside of the airlines and transportation industries will begin to pass higher costs to consumers. The U.S. – Iran 10-day ceasefire already seems to be on shaky ground and the uncertainty about the conflict further muddies the water for policymakers. As such, the Fed is likely to remain until there's more clarity on the effects of the war on both the economic and inflation outlook.

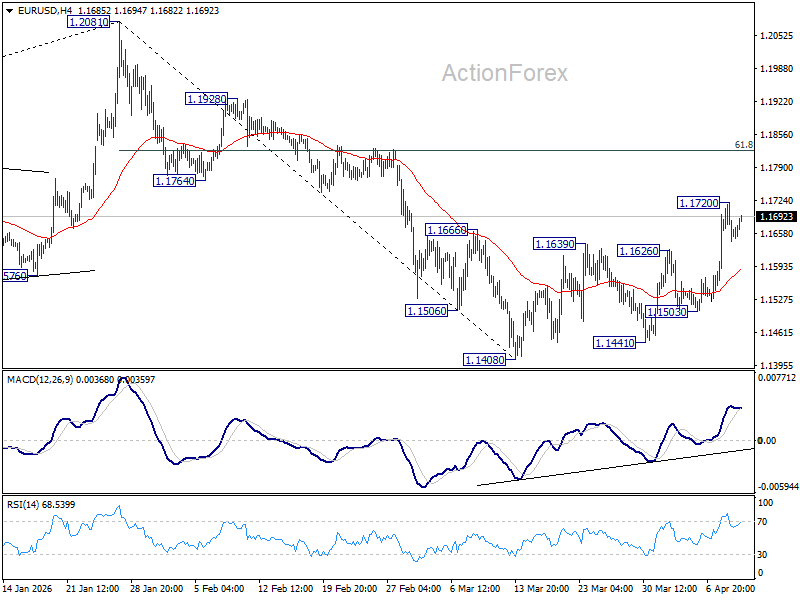

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1593; (P) 1.1658; (R1) 1.1727; More….

Intraday bias in EUR/USD is turned neutral first with current retreat. Some consolidations could be seen but further rise is expected as long as 55 4H EMA (now at 1.1584) holds. Fall from 1.2081 could have completed as a correction at 1.1408. Above 1.1720 will resume the rise from 1.1408 to 1.8% retracement of 1.2081 to 1.1408 at 1.1824. However, sustained break of 55 4H EMA will suggest that the rebound has completed, and bring retest of 1.1408 low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1505). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.