Sample Category Title

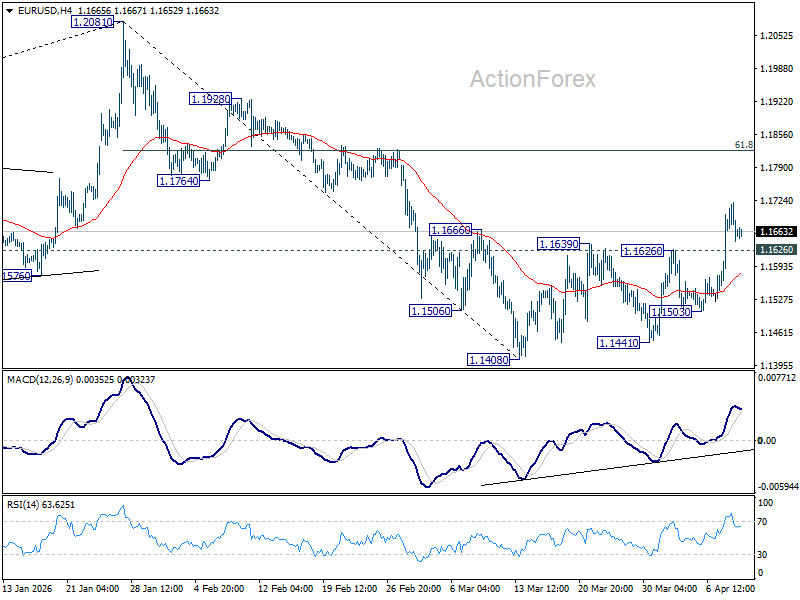

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1593; (P) 1.1658; (R1) 1.1727; More….

Intraday bias in EUR/USD stays mildly on the upside at this point. Fall from 1.2081 could have completed as a correction at 1.1408. Further rise should be seen to 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Firm break there will pave the way to retest 1.2081 high. On the downside, below 1.1626 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1505). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

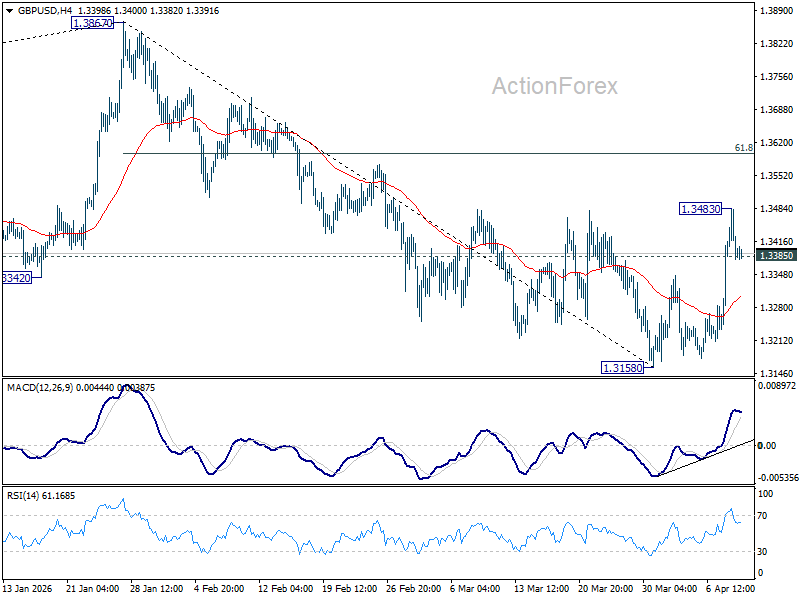

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3293; (P) 1.3389; (R1) 1.3492; More...

Intraday bias in GBP/USD is turned neutral first with current retreat. Fall from 1.3867 could have completed as a correction at 1.3158 already. Above 1.3483 will target 61.8% retracement of 1.3867 to 1.3158 at 1.3596. Firm break there will bring retest of 1.3867 high. Nevertheless, sustained break of 55 4H EMA (now at 1.3304) will dampen this bullish view and bring retest of 1.3158 instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

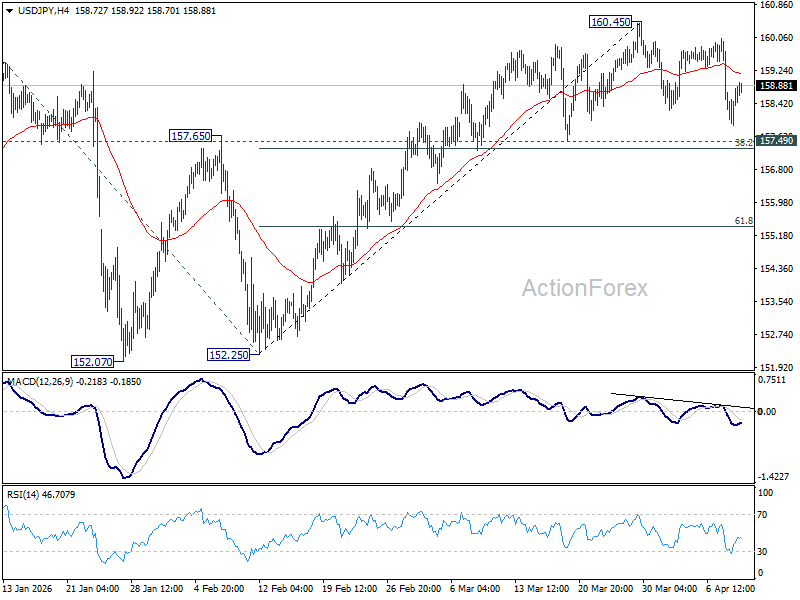

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.72; (P) 158.73; (R1) 159.59; More...

USD/JPY is still extending the consolidation pattern from 160.45 and intraday bias remains neutral. Further rise is expected as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. Firm break of 160.45 will resume the rise from 152.25 to retest 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.97) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

Middle East Truce Lifts Markets, But Tensions Persist

In focus today

Focus remains on energy markets, as tensions in the Middle East continue to weigh on oil supply disruptions and market sentiment.

From the US, February PCE data and final Q4 GDP are due for release in the afternoon. While the PCE is the Fed's preferred measure of inflation, the pre-war data will likely gather less attention than usual.

The Bank of Poland (NBP) is widely expected to keep the key rate unchanged at 3.75% at today's meeting. Although Governor Glapinski has previously hinted that there might be the odd cut left in store for NBP, the Board has been unanimous over the last month in communicating that for the time being, a wait-and-see approach is to be preferred. And the recent ceasefire deal between the US and Iran is unlikely to have changed that, given the remaining uncertainties and its likely brittle status.

Economic and market news

What happened yesterday

Global markets breathed a sigh of relief as Brent crude fell 14% to USD 95/bbl and equities surged to one-month highs following President Trump's announcement of a two-week ceasefire late Tuesday. However, the truce has failed to completely halt fighting across the region. Israel launched heavy strikes on Lebanon, while Hezbollah retaliated with rocket fire into northern Israel. Iran targeted Gulf neighbours' critical oil and power infrastructure, adding to the volatility. Confusion over the terms of the ceasefire has emerged, with Iran believing it included Lebanon, while the US and Israel maintain it does not. The oil market has reacted with relative calm, suggesting that reported damages may be manageable for now. That said, Asian markets turned more cautious on Thursday, with Japan's Nikkei flat and South Korea's Kospi down 0.4% after sharp gains the previous day. Brent futures also edged up slightly to USD 97/bbl. The Strait of Hormuz remains blocked, though Iran has indicated it could reopen later this week subject to further agreements. Markets are closely watching for signs of increased traffic through the strait in the coming days.

In the US, FOMC minutes from the March meeting revealed a growing openness among policymakers to potential rate hikes, as concerns about persistently high inflation, driven by the war-related oil shock, outweighed earlier expectations. While the Fed held rates steady at 3.50-3.75%, several officials cited the risk of prolonged above-target inflation and its impact on core price trends. Despite this, most participants still viewed rate cuts as the baseline scenario, anticipating that the economic fallout from the Middle East conflict could weaken growth and labour markets.

Equities: Global equities rallied sharply yesterday in the wake of the Iran ceasefire headlines, leaving global benchmarks just ~2% below all-time highs and back in positive territory year-to-date. Unsurprisingly, the move was characterized by a strong cyclical rotation, while energy stood out as the clear underperformer. At the same time, minimum volatility significantly lagged; in fact, min vol is now the worst-performing factor since our latest strategy report in early March, standing in stark contrast to the heavy flow of geopolitical risk over the past month.

Notably, the rebound dynamics show a clear reversal pattern: the strongest moves were seen in Asia and Europe, and at industry level, semiconductors outperformed energy by ~15% yesterday alone. While US moves were more muted, it is worth noting that yesterday marked the sixth consecutive positive session for the S&P 500.

This morning, with uncertainties around how the ceasefire will evolve, Asian equities are giving back some of the gains. European and US futures are also modestly lower.

FI and FX: EUR/USD initially rallied on the ceasefire, but with stirring doubts regarding the longevity of the deal we saw the greenback slowly crawl back, as well as equities softening a tad and risky assets in general retrace some of the earlier moves. The SEK had a stellar first half of the session, with EUR/SEK briefly printing 10.75, before turning 10 figures higher in the latter half, currently sitting close to 10.90. Also, US treasuries saw partial reversals of the initial ceasefire rally, with a modest bear-flattening of the curve, supported a slight hawkish lean to the March FOMC minutes. The NOK failed to capitalize on the rallying risk sentiment, weighed down by the decline in energy prices, highlighting the tug-of-war that is likely to dominate the NOK over the coming weeks.

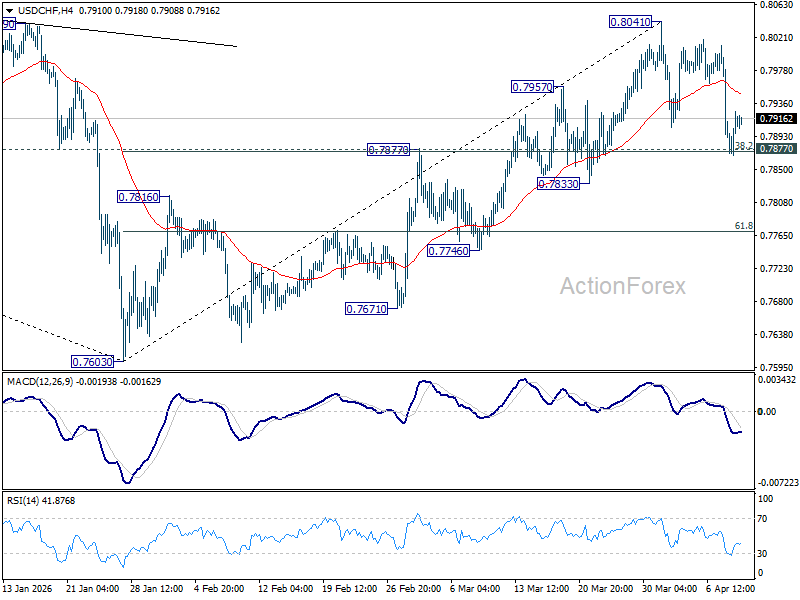

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7855; (P) 0.7927; (R1) 0.7985; More….

USD/CHF recovered after drawing support from 0.7877 cluster support (38.2% retracement of 0.7603 to 0.8041 at 0.7874). Intraday bias stays neutral first with price actions from 0.8041 seen as a consolidation pattern. With 0.7874/7 intact, rally from 0.7603 is expected to resume through 0.8041 later. However, decisive break of 0.7874/7 will argue that the rise has completed, and bring deeper fall to 61.8% retracement at 0.7770 and below.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. rejection by 55 W EMA (now at 0.8081) will affirm this case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

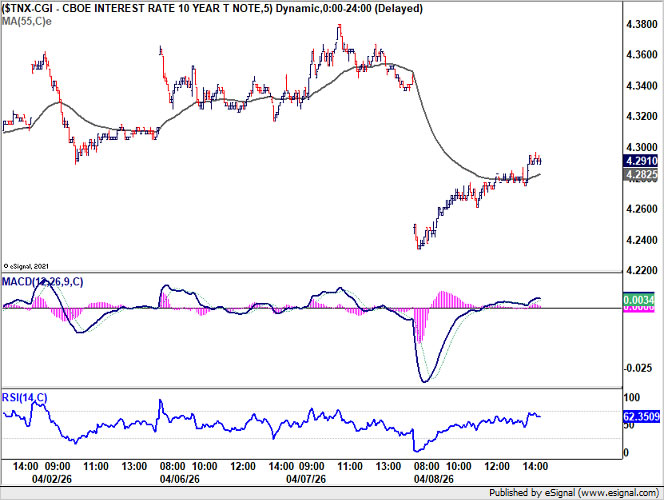

US 10-Year Yield “V” Shaped Rebound Signals Rejection of Iran Ceasefire Optimism

The market reaction to the two-week US-Iran ceasefire is already turning, with signs of rejection of ceasefire optimism emerging across key asset classes. What initially appeared as a decisive de-escalation could be reassessed as a fragile truce, not peace, with markets are pricing risk re-entry as early doubts take hold. The most telling signal lies in the rates market. The US 10-year yield "V-shaped" reversal—from an initial drop to 4.234 overnight, and then back to close 4.291—highlights a sharp shift in sentiment. It should be highlighted that 4.300 was nearly reclaimed.

This is not a stable repricing of lower risk, but a bond market rejecting the peace trade, with the yields rebound signals skepticism on de-escalation. This reversal carries broader implications. It suggests that the rates market are not pricing clean disinflation, as the initial assumption of easing energy pressures is being questioned.

Oil markets reinforce this narrative. Brent’s recovery from near $93 back to around $100 suggests that the war premium is creeping back. FX markets are adjusting in tandem. Dollar is stabilizing and recovering mildly, paring ceasefire-driven losses as euphoria fading. The move reflects a broader shift from optimism to caution.

What’s driving this rapid reversal is not just market positioning, but developments on the ground. The ceasefire is already facing compliance issues, with doubts emerging within the first 24 hours.

Iran’s Parliament Speaker Mohammad Bagher Ghalibaf accused the US of violating multiple clauses. At the center of the dispute is the "Lebanon Gap" as key fault line. While Iran and mediators claim the ceasefire should cover the Israel-Hezbollah front, Washington has rejected that interpretation, with strikes in Beirut continuing. This divergence is not a minor detail—it is a structural flaw in the agreement.

At the same time, the Strait of Hormuz remains a critical uncertainty. Despite reopening headlines, Hormuz still contested despite reopening claims, with Iranian naval threats requiring transit “permission” keeping shipping conditions fragile.

Taken together, these developments explain why negotiations risk collapsing before they begin. Institutional investors could already be pricing in a higher probability that upcoming talks will fail to produce a durable agreement.

Looking ahead, the Islamabad talks is next binary catalyst. A high-level US delegation led by Vice President JD Vance is expected to begin formal talks in Islamabad on Friday to attempt to solidify the "two-week pause" into something more durable. However, If the US insists on "complete denuclearization" and Iran insists on "lifting all sanctions" as prerequisites for a permanent deal, the ceasefire is merely a 14-day clock ticking toward a larger escalation.

In parallel, data like those from MarineTraffic over the next 12 hours will be the ultimate "truth-teller" regarding whether the Strait of Hormuz is actually open for commercial transit or if insurance premiums will remain at prohibitive, war-time levels. Until then, ceasefire is a 14-day clock, not a resolution, and markets are shifting from optimism to conditional skepticism.

In the currency markets, Dollar is the worst performer so far this week, followed by Yen and Loonie. Kiwi leads gains, with Aussie and Sterling also firm, while Euro and Swiss Franc trade in the middle of the pack.

In Asia, at the time of writing, Nikkei is down -0.65%. Hong Kong HSI is down -0.25%. China Shanghai SSE is down -0.73%. Singapore Strait Times is down -0.24%. Japan 10-year JGB yield is up 0.026 at 2.398. Overnight, DOW rose 2.85%. S&P 500 rose 2.51%. NASDAQ rose 2.80%. 10-year yield fell -0.052 to 4.291.

Fed Minutes: Rates Near Neutral, Cuts Still Seen but No Longer a Given

Federal Reserve minutes delivered a clear message: rate cuts are no longer on autopilot. With policy now near neutral, officials signaled that further easing will depend on a sustained decline in inflation—not just expectations. At the same time, Middle East tensions and oil price risks have created a rare two-sided policy dilemma, where both rate cuts and hikes remain possible. Read More.

RBNZ’s Breman: Ready to Act Decisively with Rate Hikes if Inflation Jumps

RBNZ Governor Anna Breman delivered a clear hawkish signal: if inflation starts rising again, the central bank is ready to act decisively with rate hikes. With risks now tilted to the upside, easing is off the table as policymakers focus on preventing a renewed inflation surge. Geopolitical tensions and supply disruptions are adding uncertainty, but the policy bias is clear—RBNZ is prepared to tighten again if price pressures build. Read More.

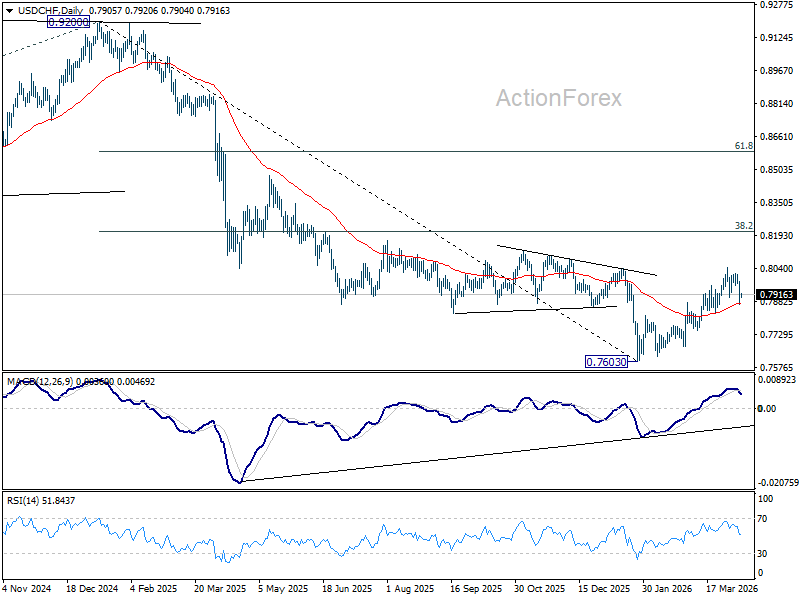

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7855; (P) 0.7927; (R1) 0.7985; More….

USD/CHF recovered after drawing support from 0.7877 cluster support (38.2% retracement of 0.7603 to 0.8041 at 0.7874). Intraday bias stays neutral first with price actions from 0.8041 seen as a consolidation pattern. With 0.7874/7 intact, rally from 0.7603 is expected to resume through 0.8041 later. However, decisive break of 0.7874/7 will argue that the rise has completed, and bring deeper fall to 61.8% retracement at 0.7770 and below.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. rejection by 55 W EMA (now at 0.8081) will affirm this case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

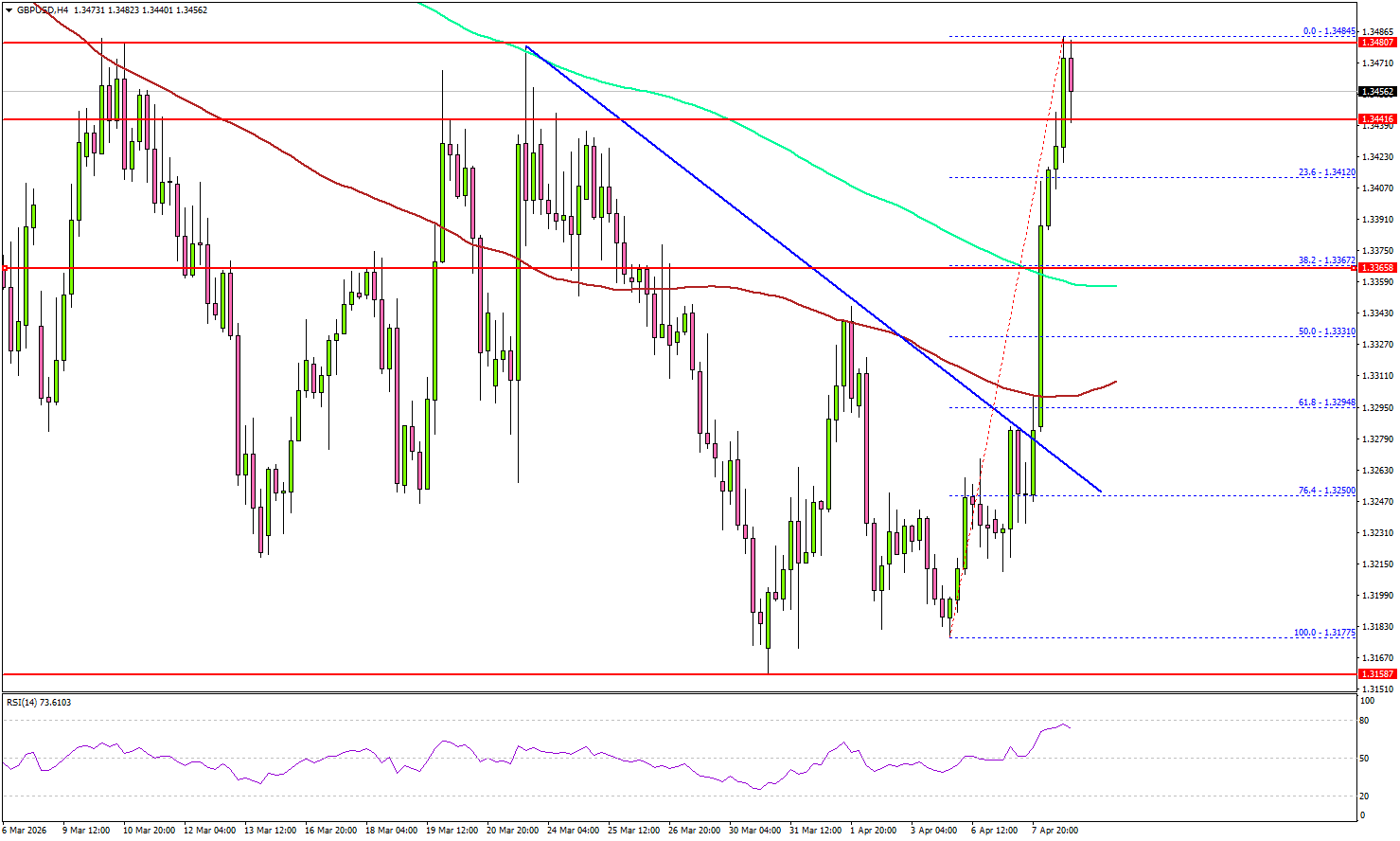

GBP/USD Picks Up Pace, Is a Breakout Now Imminent?

Key Highlights

- GBP/USD started a fresh surge above 1.3350 and 1.3440.

- It cleared a key bearish trend line with resistance at 1.3280 on the 4-hour chart.

- EUR/USD also climbed higher above the 1.1650 resistance.

- WTI Crude Oil prices trimmed most gains and traded below $95.

GBP/USD Technical Analysis

The British Pound found support at 1.3150 and started a fresh increase against the US Dollar. GBP/USD gained pace for a move above 1.3250 and 1.3350.

Looking at the 4-hour chart, the pair cleared a key bearish trend line with resistance at 1.3280 to enter a positive zone. The pair settled well above 1.3400, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The pair tested the 1.3485 resistance and started a consolidation phase. Immediate support is seen near 1.3410 and the 23.6% Fib retracement level of the upward move from the 1.3177 swing low to the 1.3485 high.

The first key support sits at 1.3365. The next key area of interest might be near 1.3300 or the 61.8% Fib retracement level of the upward move from the 1.3177 swing low to the 1.3485 high.

A close below 1.3300 might call for heavy losses. In the stated case, it could even revisit 1.3220. On the upside, the pair could face resistance near the 1.3500 zone. The first major resistance sits at 1.3550. The main resistance could be 1.3620. A close above 1.3620 could open the doors for gains above 1.3650. In the stated case, the bulls could aim for a move to 1.3750.

Looking at Oil, the price started a fresh decline amid peace talks, and the bears were able to push the price below $95.

Upcoming Key Economic Events:

- US Initial Jobless Claims - Forecast 210K, versus 202K previous.

- US Gross Domestic Product for Q4 2025 – Forecast 0.7% versus previous 0.7%.

RBNZ’s Breman: Ready to Act Decisively with Rate Hikes if Inflation Jumps

RBNZ Governor Anna Breman delivered a clear warning that inflation risks are shifting to the upside, reinforcing a tightening bias despite a softer growth outlook. Speaking to Bloomberg TV, Breman said “the balance of risks have shifted in terms of inflation,” signaling growing concern that price pressures could re-accelerate.

More importantly, Breman left little ambiguity about the policy response. She stressed that if medium-term inflation begins to rise, “we will act decisively and that means rate hikes.” This marks a firm signal that the RBNZ is prepared to tighten again if needed, rather than tolerate a renewed inflation cycle.

Geopolitical uncertainty remains a key wildcard. Breman highlighted supply-side disruptions stemming from the conflict, noting that both the duration and scale of the impact remain unclear. This uncertainty is keeping the RBNZ in a data-dependent stance, but with a clear bias: inflation risks are rising, and policy will lean restrictive if those risks materialize.

Fed Minutes: Rates Near Neutral, Cuts Still Seen but No Longer a Given

The clearest signal from the March FOMC minutes is that policymakers collectively shifted away from any presumption of continued easing. With rates now judged to be “within a range of plausible estimates of its neutral level” following last year’s 75bps cuts, the bar for further policy easing has been materially raised.

The decision to hold at 3.50–3.75% was nearly unanimous, with only Stephen Miran dissenting in favor of a 25bps cut. The dominant driver behind the pause was “elevated” uncertainty tied to the Middle East conflict. Officials acknowledged that while economic activity remained solid, the external shock had introduced a level of unpredictability that warranted patience rather than pre-emptive action.

Crucially, the characterization of policy as near neutral marks a structural shift in the Fed’s reaction function. Earlier in the cycle, rate cuts were seen as necessary to avoid overtightening. That logic has now changed. With policy no longer clearly restrictive, easing is no longer automatic—it must be justified by incoming data. As the minutes suggest, any additional cuts would likely require inflation to “decline in line with their expectations.”

That conditionality is reinforced by a subtle but important shift in timing expectations. While many participants still anticipate that it “would likely become appropriate to lower” rates over time, “a couple” explicitly pushed back the expected timing of cuts due to recent inflation readings. This reflects growing discomfort with easing too early while price pressures remain sticky.

At the same time, the Fed is grappling with unusually pronounced two-sided risks. On one side, policymakers warned that a prolonged Middle East conflict could weaken labor markets, noting that higher oil prices may “reduce households’ purchasing power, tighten financial conditions, and reduce growth abroad,” potentially justifying rate cuts. On the other, “many participants” flagged the risk that persistent energy-driven inflation could “call for rate increases” to keep expectations anchored.

The result is a policy stance defined by balance rather than bias. As the minutes emphasized, policy is “not on a preset course” and will be determined “meeting by meeting.” This reinforces a reactive framework where both cuts and hikes remain on the table, depending on how inflation and growth evolve.

FOMC Members Highlight Inflation Risks in March

The Federal Reserve Open Market Committee (FOMC) held the federal funds rate at a target range of 3.50% to 3.75% in March.

The minutes showed that the committee is still concerned about inflation remaining above 2%. Some noted that "progress in reducing inflation had been absent in recent months" and that "the rate of increase in core goods prices remained well above the pace likely to be consistent with the sustainable achievement of the Committee's inflation objective". However, the expectation remains that inflation would gradually reach the "2 percent objective after the effect of increased tariffs and higher oil prices had faded." A prolonged conflict in the Middle East was cited as an upside risk where higher energy prices could raise input costs and these "would be more likely to pass through to core inflation." Partly due to the risks to the outlook, "the vast majority or participants" noted that progress to the inflation target "could be slower than previously expected" and that the risk of inflation staying above the target had increased.

With respect to the labor market, participants judged it to be roughly balanced. The rate of job creation was expected to stay in line with slower labor force growth, leaving the unemployment rate relatively unchanged. However, the risks to the labor market were judged to be skewed to the downside, with low net job creation, higher unemployment among prime age workers, and the concentration of job gains in the health-care sector being cited as reasons. "Many participants" also cited "business contacts and surveys suggesting that firms were likely to delay or reduce hiring in anticipation of AI adoption".

Importantly, "[m]any participants judged that, in time, it would likely become appropriate to lower the target range for the federal funds rate if inflation were to decline," as expected. However, the minutes noted that, "[s]ome participants judged that there was a strong case for a two-sided description" of future interest rate decisions, to better reflect that "upward adjustments to the target range" might be necessary if inflation were to stay above the target range. The minutes emphasized that policy decisions would be made on a "meeting-by-meeting" basis.

The risks to the outlook remained high and "the vast majority of participants judged that upside risks to inflation and downside risks to employment were elevated" and that they "had increased with developments in the Middle East".

Key Implications

Unsurprisingly, the risks around the inflation outlook were pronounced in the weeks after the onset of the conflict in the Middle East. The duration of the conflict is a key factor for inflation going forward and the participants reaffirmed that they would be making decisions on a meeting-by-meeting basis.

Despite today's news of a ceasefire, energy prices remain elevated, while the course of the conflict and any future disruptions remain highly uncertain. The inflation shock has started and will gradually disseminate through the economy. Nonetheless, our baseline view is that as the shock gradually fades, so too will inflation pressures. This may open the door for the Fed to normalize rates in the latter half of the year.