Sample Category Title

Sunset Market Commentary

Markets

Not to be the killjoy here, but so many questions remain following the dramatic U-turn in the Middle East conflict. The US and Iran have agreed on a two-week ceasefire, but no one knows when it actually starts. The US said the ceasefire is contingent on the complete, immediate and safe opening of the Strait of Hormuz chokepoint. Iran’s more guarded view suggests a limited reopening on the country’s terms (e.g. a tollbooth) and in coordination with its military. This turns something as economically so critical as the Strait into a political instrument. The longer-term implications of that could/should be a reason for concern. Another open question is Israel’s compliance. It supported the ceasefire but said it doesn’t apply to Lebanon and resumed strikes today. Iran’s 10-point plan that serves as a “workable basis” (for talks that start this Friday) however contains the explicit demand to end the war against “the axis of resistance”, a clear reference to Lebanon’s Hizbollah as well and Iraqi militias and Houthis in Yemen. There’s also huge uncertainty in terms of how quickly the stalled maritime traffic can and wants to resume. A ceasefire won’t resolve anything if shippers are not convinced the threat level has actually receded. It for sure doesn’t help that reports of attacks keep filtering in. While not unusual since ceasefire orders take some time to reach all parties involved, it underscores the fragility of the truce.

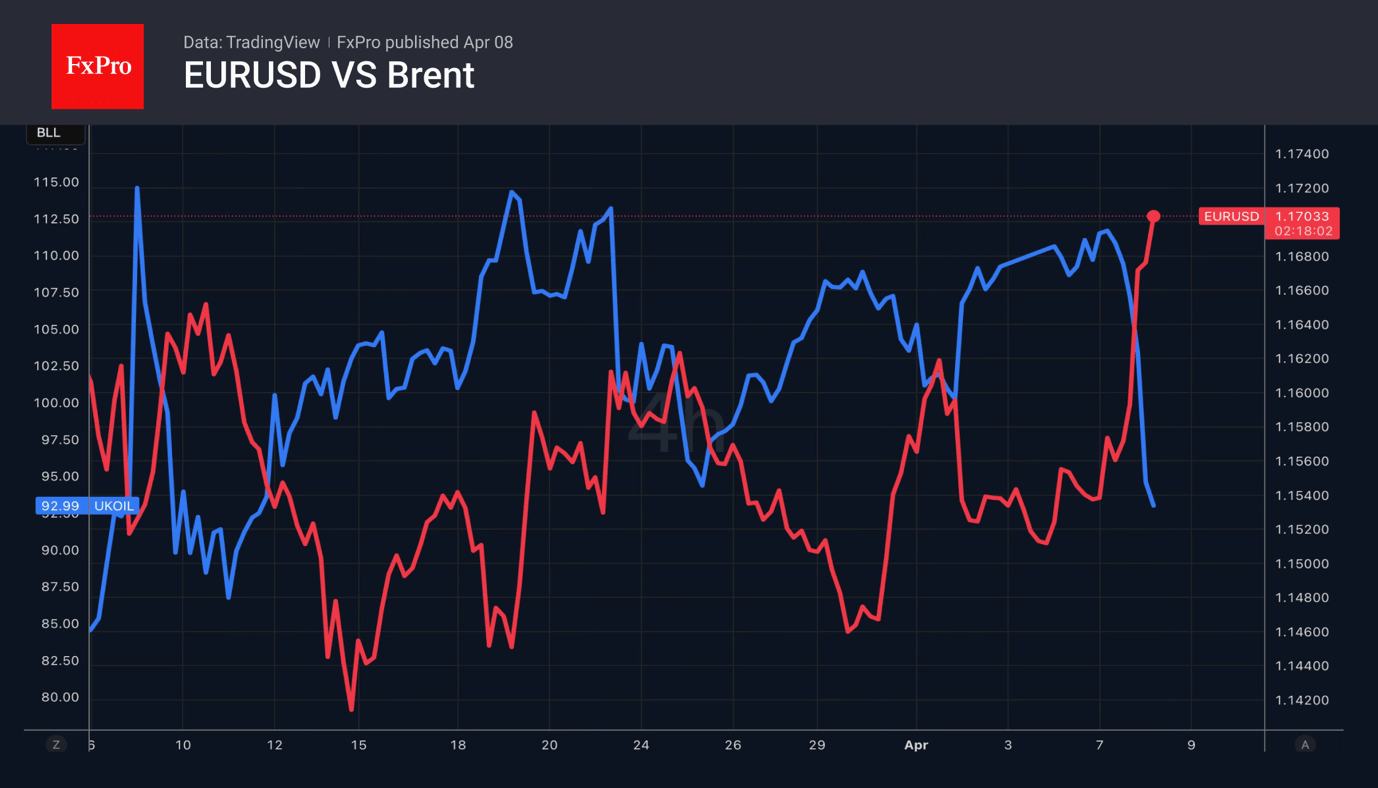

It’s a big disclaimer that markets couldn’t care less about. The sigh of relief overwhelmingly dominates the lingering risks & uncertainty. Weeks of rising tensions and a dramatic build-up to what would have been a major escalation also resulted in short covering, strengthening the rip higher. The basis lies in plummeting energy prices. A barrel of Brent oil was trading around $110 yesterday and around $92 today. Dutch natural gas prices collapsed by almost 20%. Risk assets are on a tear. Stocks in Europe surge more than 5% (EuroStoxx50) with American indices adding between 2.5% and 3.5%. Core bonds rally on easing rate hike bets, inflation risks and risk premia in general. Bunds hugely outperform Treasuries. The latter already anticipated something in late US dealings yesterday and another push today lowers yields by another 1.1-4.4 bps in bull steepening fashion. German rates are falling off a cliff with net daily changes varying between 9 and 25 bps. Front-end outperformance follows market implied probability for an April hike falling sharply from 70% yesterday to +/- 25% today. A cumulative 77 bps in hikes in 2026 as of April 7 gets reduced to 50 bps. Intra-European spreads narrow sharply, led by Italy and Greece. UK gilts join the rally. Yields slide 15-24 bps. The US dollar is the main laggard in FX space. The trade-weighted index fell from just south of 100 to 98.6. EUR/USD adds more than a percent to 1.1717, the highest since the Iran war erupted at the start of March. Sterling has the upper hand against USD (GBP/USD towards the March highs around 1.347) and the euro. EUR/GBP loses the 0.87 mark.

News & Views

Hungarian inflation accelerated to 0.4% M/M in March with annual inflation picking up from 1.4% to 1.8%. Both were below consensus estimates (0.8% M/M & 2.2% Y/Y). Electricity, gas and other fuel prices stagnated on a monthly basis but that’s because of the way a temporary utility allowance (Jan 2026) is accounted for. Household energy consumption data are available with a two-month delay so January consumption only enters domestic CPI statistics in March. Food prices declined by 0.1% M/M while services prices were up by 0.2%. Compared to March 2025, prices for electricity, gas and other fuels increased by 4.3%. Food prices stagnated while consumer durable prices were up by 2.7%. Services costs increased by 4.1% Y/Y. The Hungarian central bank (MNB) added that core inflation slowed from 2.1% to 1.9% Y/Y. Core inflation excluding indirect tax effects also decreased to 1.9%. Incoming inflation data was broadly in line with the projection in the March Inflation Report. The Hungarian forint already traded rather strong in the run-up to today’s extremely bullish risk session, eying this weekend’s elections. The forint adds to those gains with EUR/HUF testing the YTD low at 375.

Belgium’s Minister of Defense, Francken, today announced the establishment of a €2bn Defense Fund, a subsidiary of SFPIM International (Belgian public investment institution), to strengthen the country’s defense and security industry. The fund will support companies in scaling up production, strengthen strategic industrial capacity, and help keep jobs and expertise anchored in Belgium.

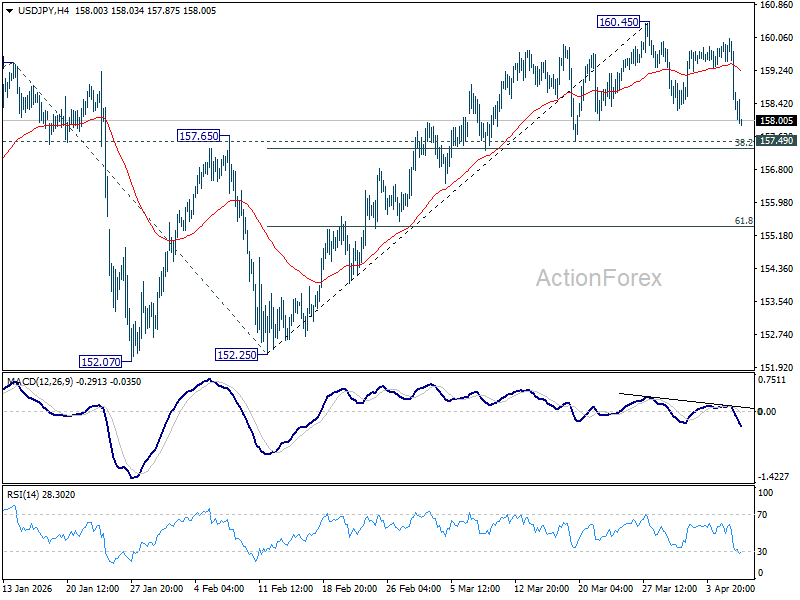

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.39; (P) 159.71; (R1) 159.94; More...

Intraday bias in USD/JPY stays neutral at this point as consolidations continue below 160.45. Further rise is expected as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. Firm break of 160.45 will resume the rise from 152.25 to retest 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.97) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

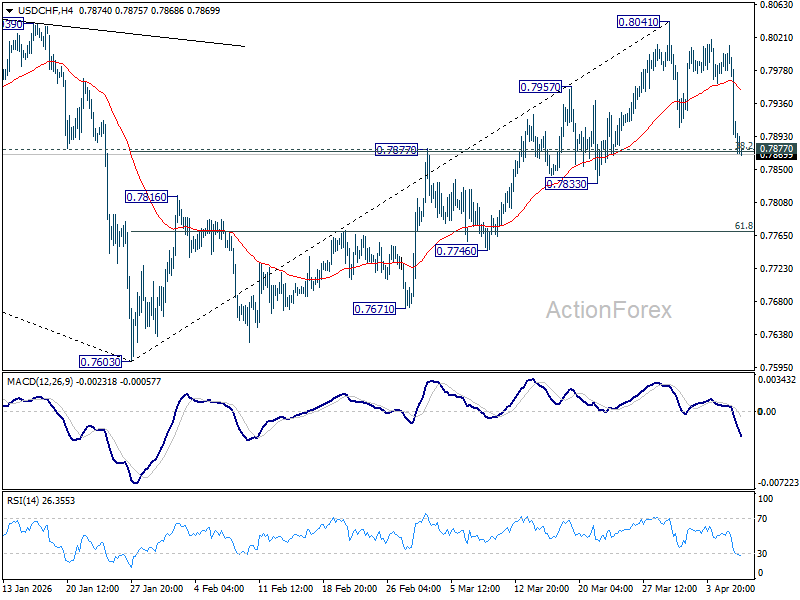

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7962; (P) 0.7987; (R1) 0.8002; More….

Focus remains on 0.7877 cluster support (38.2% retracement of 0.7603 to 0.8041 at 0.7874) in USD/CHF. Decisive break there will argue that whole rise from 0.7603 as completed, and bring deeper fall to 61.8% retracement at 0.77706 and below. Nevertheless, strong bounce from 0.7874/7 will retain near term bullishness for another rise through 0.8041 at a later stage.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. rejection by 55 W EMA (now at 0.8081) will affirm this case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

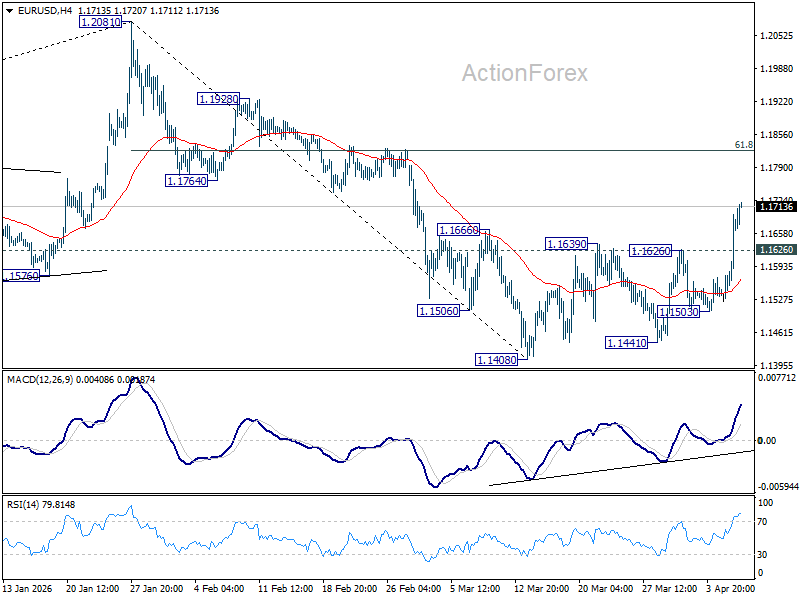

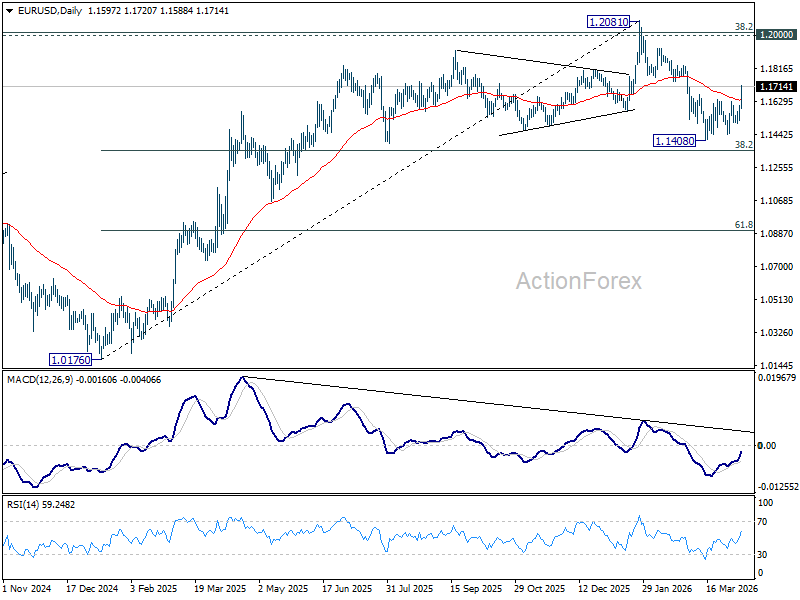

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1546; (P) 1.1575; (R1) 1.1627; More….

Intraday bias in EUR/USD remains on the upside for the moment. Fall from 1.2081 could have completed as a correction at 1.1408. Further rise should be seen to 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Firm break there will pave the way to retest 1.2081 high. On the downside, below 1.1626 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1505). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

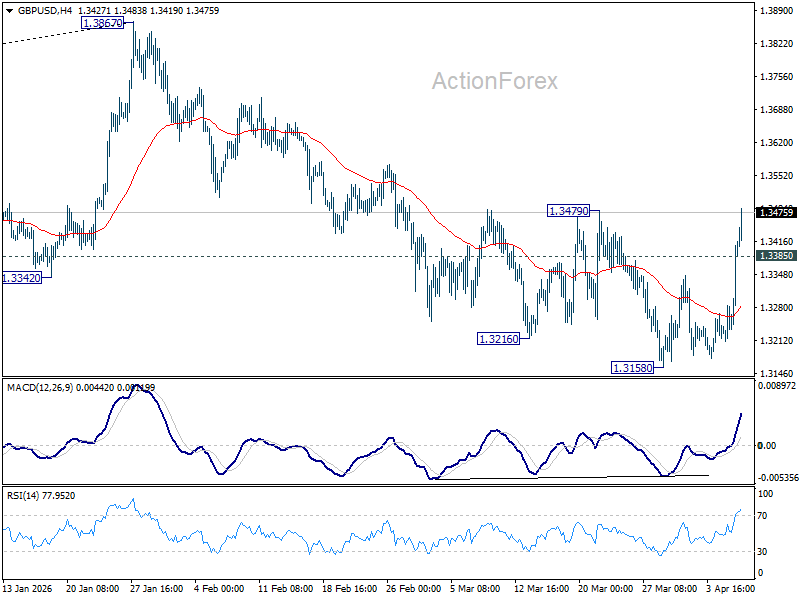

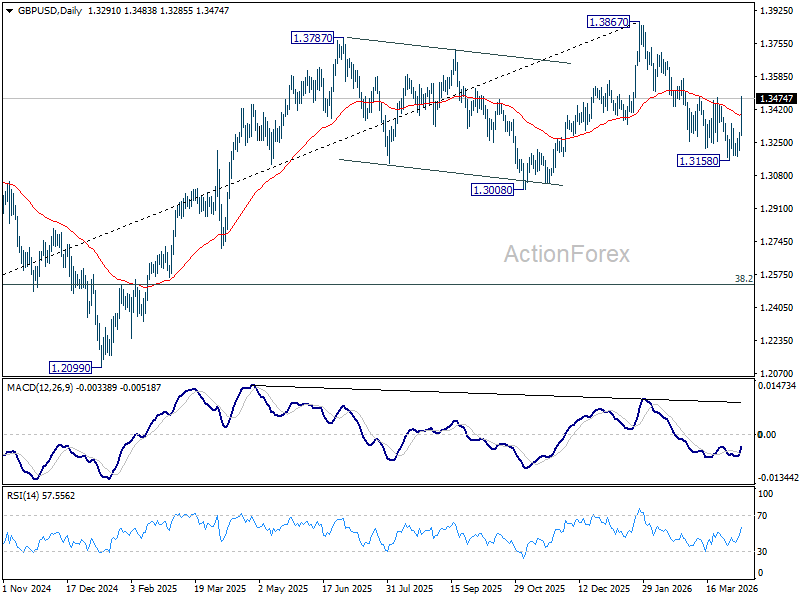

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3236; (P) 1.3268; (R1) 1.3327; More...

GBP/USD's break of 1.3479 resistance argues that fall from 1.3867 has completed as a correction at 1.3158. Intraday bias is back on the upside. Further rally should be seen to retest 1.3867 high. On the downside, below 1.3385 will turn intraday bias neutral and bring consolidations first. But retreat should be contained well above 1.3158 low to bring another rally.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

Ceasefire Resets Fed Outlook, Markets Set to Look Through FOMC Minutes and Hot CPI

The ceasefire between the US and Iran has reset the Fed outlook, shifting market focus away from near-term inflation data toward the broader policy path. With oil prices falling and supply risks easing, the markets could be willing to look through both FOMC minutes today and a likely elevated March CPI reading on Friday.

The repricing has been swift. Odds of the Fed holding at 3.50–3.75% through year-end have dropped from around 80% to near 58%, with roughly 42% now pricing in at least one rate cut. More importantly, the possibility of a rate hike has been effectively erased. This marks a clear transition from a higher-for-longer mindset toward a more balanced outlook. Just days ago, markets were positioning for a prolonged inflation shock driven by surging energy prices. That narrative has now been disrupted.

As a result, this week’s key events are losing relevance. The March FOMC minutes, due today, will likely reflect a Fed grappling with a potential wartime shock, with oil prices approaching $120. Even if the tone appears hawkish, markets are expected to largely ignore it. The reason is straightforward. The primary driver behind that hawkish stance—the risk of sustained energy disruption—has been partially resolved. The ceasefire has effectively reset the clock, rendering the minutes outdated upon release.

The same logic applies to CPI. March inflation is almost certain to print high, capturing the peak of the energy shock. But with Brent already down sharply, markets are set to treat the data as rear-view mirror inflation, focusing instead on forward-looking indicators.

However, the disinflation path is not immediate. The reopening of the Strait of Hormuz is gradual, with shipping networks expected to take six to eight weeks to normalize. During this period, oil prices are likely to remain elevated, sustaining some inflation pressure in the near term.

This creates a transitional phase where inflation remains firm, even as the underlying drivers begin to fade. But importantly, many Fed officials are likely to view this as transitory. As long as inflation expectations remain anchored, policymakers can afford to look through short-term volatility. This supports a patient stance in the near term while keeping the door open for easing once the temporary effects dissipate.

By early second half, the data should begin to reflect a clearer disinflation trend if traffic through the Strait of Hormuz is fully normalized. As base effects from the energy shock roll off and supply conditions improve, the case for Fed's monetary policy normalization will strengthen. That makes a year-end rate cut a logical baseline scenario.

However, this repricing remains highly conditional. Vice President JD Vance described the ceasefire as a “fragile truce”, underscoring the risk that the current optimism may prove premature. Execution risk is particularly high around the Strait of Hormuz. Iranian Foreign Minister Abbas Araghchi noted that passage is currently managed “via coordination with Iran’s Armed Forces.” Any disruption or miscalculation could quickly reintroduce war premium.

For now, markets are effectively priced for perfection. Dollar has come under broad pressure, reflecting the shift in expectations, while risk currencies are benefiting from improved sentiment. Ultimately, the Fed itself has not changed—but the environment around it has. The path toward rate cuts is now visible, but it depends on sustained, tangible progress in the US-Iran negotiations. Until then, markets will continue to price easing cautiously, with one eye firmly on geopolitics.

In currency markets, Dollar is the clear underperformer today, with broad-based selling pressure. Loonie follows as the second weakest, weighed down by falling oil prices, while Yen also lags. On the other side, Kiwi leads gains, supported by RBNZ’s hawkish hold, followed by Sterling and Swiss Franc. Euro and Aussie are trading in the middle of the pack.

In Europe, at the time of writing, FTSE Is up 2.96%. DAX is up 5.14%. CAC is up 4.75%. UK 10-year yield is down -0.215 at 4.623. Germany 10-year yield is down -0.177 at 2.909. Earlier in Asia, Nikkei rose 5.29%. Hong Kong HSI rose 3.16%. China Shanghai SSE rose 2.03%. Singapore Strait Times rose 0.81%. Japan 10-year JGB yield fell -0.046 to 2.364.

Silver to Rally Toward 84 on Ceasefire Euphoria—Is “Day 10” a Trap?

Silver has broken out on ceasefire-driven Dollar weakness, with 84 now in focus. But the rally may be time-limited, as “Day 10” of the ceasefire window could bring back risk and trigger a reversal. Read More.

RBNZ Holds, Warns of “Decisive” Hikes if Inflation Expectations De-Anchor

RBNZ kept rates unchanged—but signaled it won’t hesitate to act. A warning of “decisive” hikes has put inflation expectations at the center of the policy outlook. Read More.

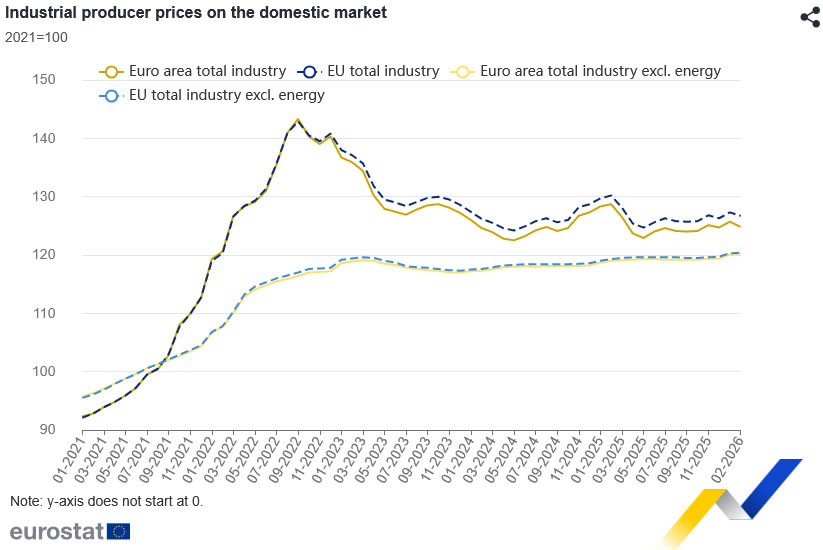

Eurozone Producer Inflation Falls -0.7% mom in February on Energy Drop

Eurozone PPI fell in February as energy prices dropped, signaling easing pipeline pressures. However, core components remained firm, suggesting underlying inflation is not fully fading. Read More.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3236; (P) 1.3268; (R1) 1.3327; More...

GBP/USD's break of 1.3479 resistance argues that fall from 1.3867 has completed as a correction at 1.3158. Intraday bias is back on the upside. Further rally should be seen to retest 1.3867 high. On the downside, below 1.3385 will turn intraday bias neutral and bring consolidations first. But retreat should be contained well above 1.3158 low to bring another rally.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

Euro Seized the Opportunity to Rise

- The US-Iran ceasefire sent EURUSD to 1.17.

- The dollar will be sensitive to developments in the Washington-Tehran talks.

The US dollar was hit by a wave of selling following reports of a two-week truce between Washington and Tehran. And although Middle Eastern countries continue to report attacks by Iran, and Israel has no intention of halting its strikes on Lebanon, EURUSD recorded its best rally since late January. Investors, driven by FOMO (fear of missing out), briefly pushed the euro above 1.17.

Markets shoot first and ask questions later. The war had led to a rise in oil prices and the US dollar, whilst the EURUSD and US stock indices were steadily falling. The ceasefire turned yesterday’s winners into losers and the underdogs into favourites. The greenback is losing ground as tensions ease. At the same time, the futures market has raised the odds of a Fed rate cut in 2026 from 12% to 44%.

It is unclear whether Donald Trump has resolved the conflict in the Middle East. The differences between the opposing sides have not gone away. Iran claims victory in the conflict, whilst the US says it has achieved and even exceeded its objectives. For now, the markets are trying to work out whose claims are more misleading and are awaiting signals from the direct talks on 10 April.

It is widely known how Donald Trump conducts negotiations. The tactic of threats has not gone away, which could be perceived as an escalation of the geopolitical conflict and could prompt the EURUSD to pull back. Nevertheless, Iran and the US have already taken the first step, and, coupled with falling oil prices, this offers hope that the euro will continue to rise.

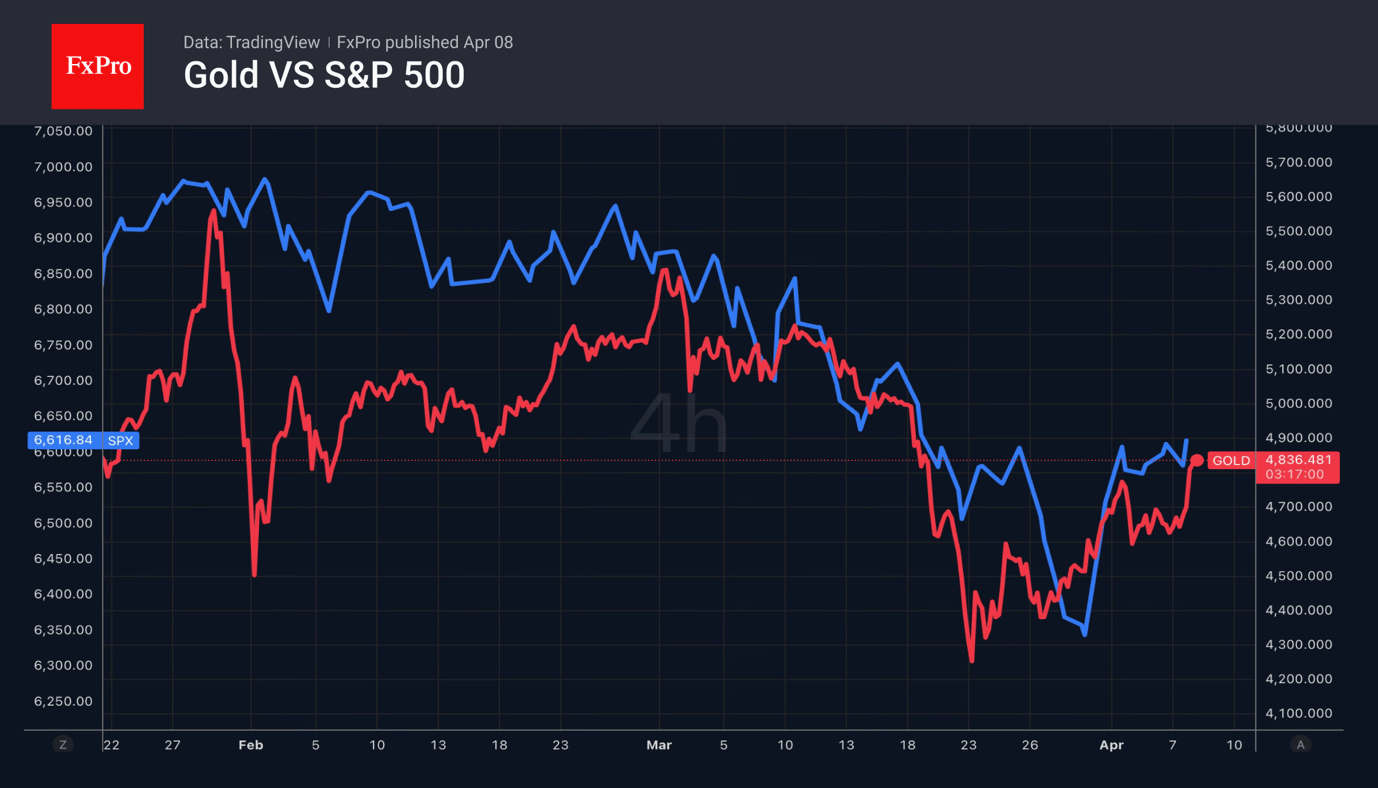

The fall in the dollar and US Treasury yields has allowed gold to recover. The precious metal has broken above $4,800 per ounce thanks to renewed hopes of a cut in the federal funds rate and the return of funds previously withdrawn to meet margin requirements on securities.

EUR/USD Soars on Middle East Pause

EUR/USD rose sharply midweek to 1.1675, reaching a four-week high. Pressure on the US dollar came after President Donald Trump postponed the threat of strikes on Iranian civilian infrastructure for two weeks. The politician described this as a "bilateral ceasefire" conditional upon the reopening of the Strait of Hormuz.

According to Trump, the US has received a 10-point proposal from Iran, which is being viewed as a working basis for negotiations. The two-week window could be used to reach a resolution. Iran has reportedly agreed to temporarily open the strait, provided that attacks cease. Israel has also supported the ceasefire.

At the same time, macroeconomic data point to rising inflation expectations in the US. In March, these increased, with transport costs in logistics rising markedly.

Investor attention is now focused on the release of March inflation data (CPI), which could clarify the degree of price pressure amid the ongoing conflict.

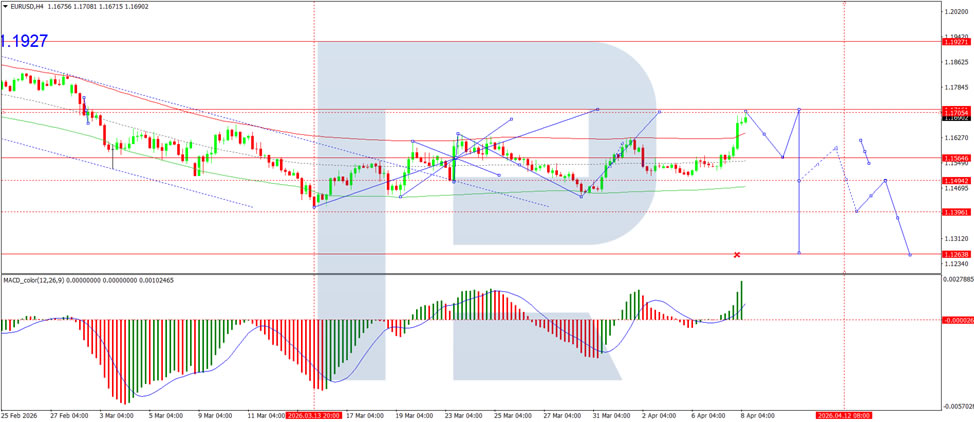

Technical Analysis

On the H4 chart of EUR/USD, the market is forming a consolidation range around the 1.1700 level. A downward wave to 1.1566 is expected as a local target. Subsequently, a move higher to 1.1717 is anticipated. Technically, this scenario is confirmed by the MACD indicator, with its signal line above zero and pointing firmly upwards, indicating continued bullish momentum and the potential for the uptrend to continue.

On the H1 chart, the market is forming the structure of the next downward wave to the 1.1566 level. After reaching this level, an increase to 1.1717 is expected, with the potential for the move higher to extend to 1.1730. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line below 80 and pointing firmly downwards towards 20.

Conclusion

EUR/USD has surged on news of a potential breakthrough in Middle East tensions, with Trump postponing strikes on Iranian infrastructure and a two-week "bilateral ceasefire" taking effect, conditional on the reopening of the Strait of Hormuz. Iran's reported 10-point proposal and agreement to temporarily open the strait have provided a significant boost to risk appetite, weighing on the safe-haven dollar. However, rising US inflation expectations and the upcoming CPI release remind markets that domestic price pressures remain a concern. While technical indicators suggest some near-term consolidation or pullback, the pair's direction will ultimately depend on whether diplomatic efforts hold and whether the ceasefire translates into a more lasting de-escalation.

Eurozone Producer Inflation Falls -0.7% mom in February on Energy Drop

Eurozone PPI fell -0.7% mom and -3.0% yoy in February, in line with expectations, with the decline largely driven by a sharp drop in energy inflation before the Iran War.

The breakdown highlights a mixed picture beneath the headline. Energy prices dropped -2.4% mom, offsetting gains in intermediate goods and capital goods, both up 0.3%, as well as a 0.2% rise in durable consumer goods. Non-durable consumer goods edged lower by -0.2%.

Across the EU, producer prices fell -0.5% mom and -2.7% yoy, with notable declines in (-3.1%), Ireland (-2.6%) and Portugal (-1.8%). The highest increases were observed in Croatia (+3.8%), Finland (+2.7%) and Lithuania (+1.8%).

AUD/USD And NZD/USD Turn Bullish, Is Rally Set to Extend?

AUD/USD started a fresh increase above 0.6970 and 0.7000. NZD/USD is also rising and might aim for more gains above 0.5850.

Important Takeaways for AUD USD and NZD USD Analysis Today

- The Aussie Dollar started a steady increase above 0.7000 against the US Dollar.

- There was a break above a rising channel with resistance at 0.6960 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is consolidating gains above the 0.5755 pivot zone.

- There was a break above a key contracting triangle with resistance at 0.5710 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair started a fresh increase from 0.6860. The Aussie Dollar was able to clear 0.6900 to move into a positive zone against the US Dollar.

There was a break above a rising channel with resistance at 0.6960. There was a close above 0.7000 and the 50-hour simple moving average. Finally, the pair tested 0.7080. A high was formed near 0.7084 and the pair recently started a consolidation phase. There was a minor decline below 0.7075.

On the downside, initial support is near the 23.6% Fib retracement level of the upward move from the 0.6859 swing low to the 0.7084 high. The next area of interest could be near 0.6970 and the 50% Fib retracement.

If there is a downside break below 0.6970, the pair could extend its decline toward the 0.6945 zone and the 50-hour simple moving average. Any more losses might signal a move toward 0.6895.

On the upside, the AUD/USD chart indicates that the pair is now facing resistance near 0.7085. The first major hurdle for the bulls might be 0.7120. An upside break above 0.7120 might send the pair further higher. The next stop is near 0.7200. Any more gains could clear the path for a move toward 0.7320.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair started a fresh increase from 0.5675. The New Zealand Dollar broke the 0.5720 barrier to start the recent rally against the US Dollar.

More importantly, there was a break above a key contracting triangle with resistance at 0.5710. The pair settled above 0.5755 and the 50-hour simple moving average.

It tested 0.5835 and is currently consolidating gains. There was a minor pullback below 0.5820. The NZD/USD chart suggests that the RSI is now just above 70. On the upside, the pair might struggle near 0.5835. The next major hurdle is near the 0.5880 pivot level.

A clear move above 0.5880 might even push the pair toward 0.6950. Any more gains might clear the path for a move toward the 0.7000 zone in the coming days.

On the downside, immediate support is near the 0.5795 level and the 23.6% Fib retracement level of the upward move from the 0.5678 swing low to the 0.5834 high.

The first key zone for the bulls sits at 0.5755 and the 50% Fib retracement. The next important level is 0.5720 and the 50-hour simple moving average. If there is a downside break below 0.5720, the pair might slide toward 0.5690. Any more losses could lead NZD/USD into a bearish zone to 0.5650.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.