Sample Category Title

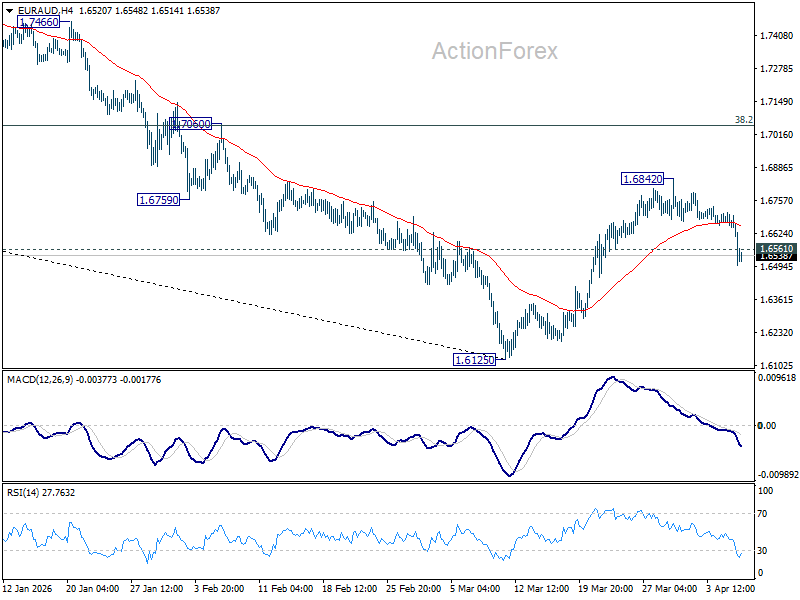

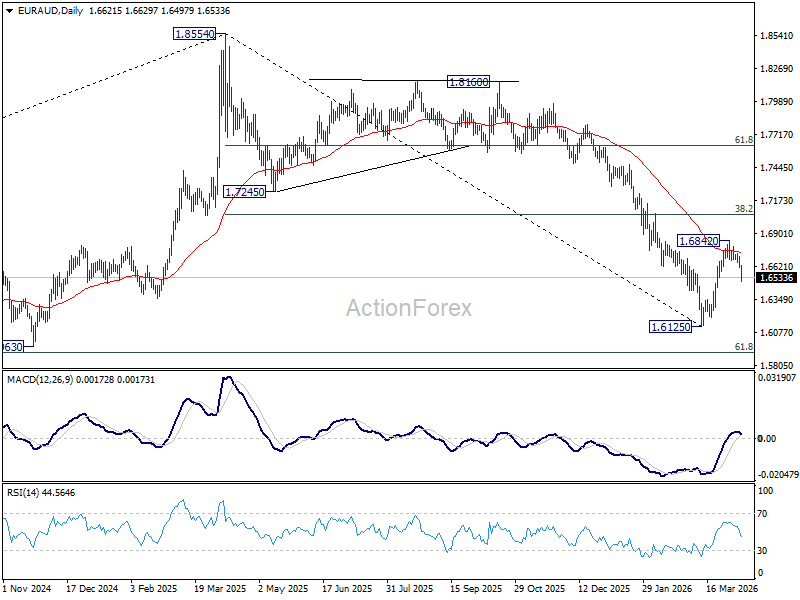

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6592; (P) 1.6653; (R1) 1.6686; More...

EUR/AUD's break of 1.6561 minor support suggests that corrective rebound from 1.6125 has already completed at 1.6842, after rejection by 55 D EMA (now at 1.6733)/ Intraday bias is back on the downside for retesting 1.6125. Firm break there will resume larger down trend. On the upside, though, break of 1.6842 will resume the rebound to 38.2% retracement of 1.8554 to 1.6125 at 1.7053.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281. For now, risk will stay on the downside as long as 55 W EMA (now at 1.7207) holds, even in case of strong rebound.

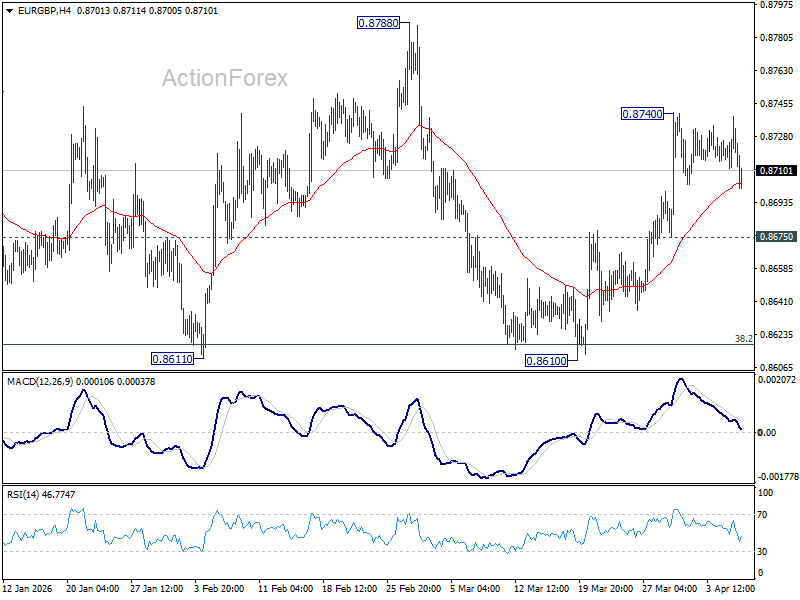

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8708; (P) 0.8725; (R1) 0.8739; More…

EUR/GBP is still bounded in consolidations below 0.8740 and intraday bias remains neutral. On the upside, above 0.8740 will resume the rebound from 0.8610 short term bottom to 0.8788 resistance next. However, break of 0.8675 will bring retest of 0.8610 low instead.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be resume to resume through 0.8863. Nevertheless, sustained trading below 0.8618 should confirm reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

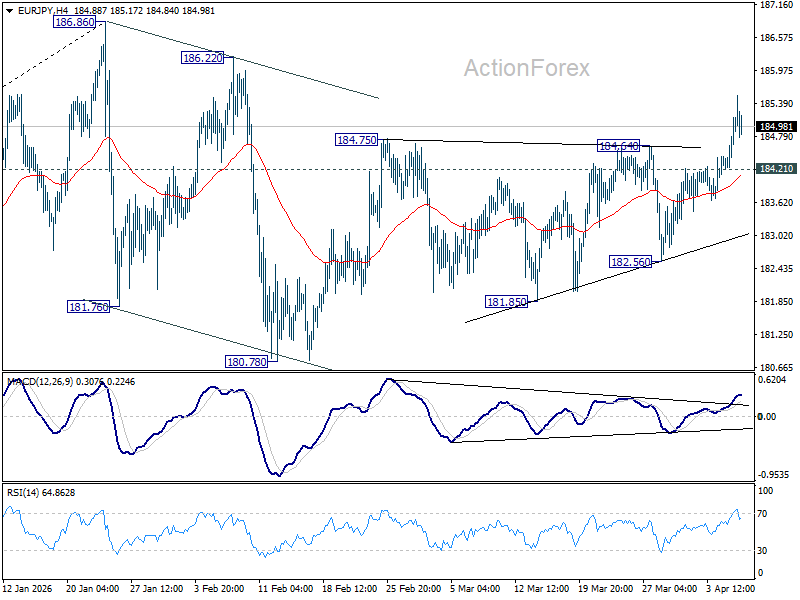

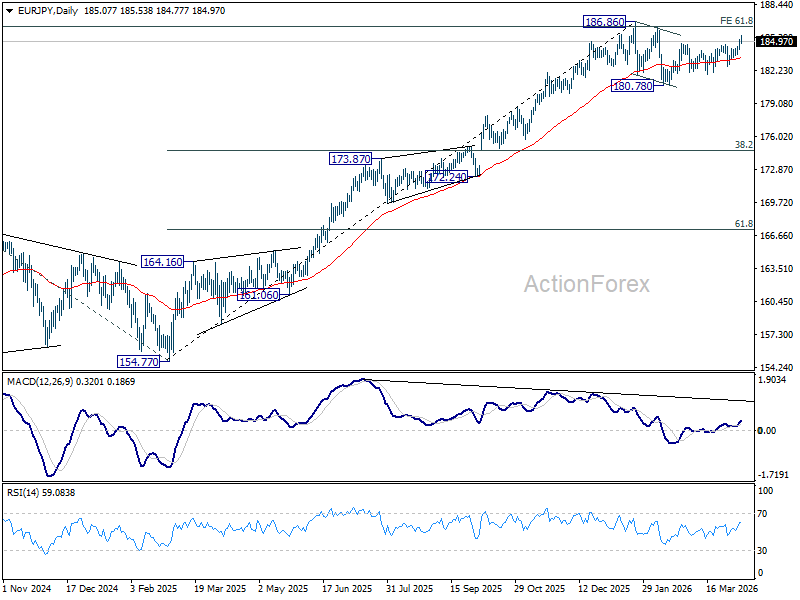

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.48; (P) 184.83; (R1) 185.44; More...

EUR/JPY's rise from 180.78 resumed by breaking through 184.75 resistance and intraday bias is back on the upside. Further rally should be seen to retest 186.86 high. On the downside, below 184.21 minor support will turn intraday bias neutral first. Further break of 182.56 will extend the corrective pattern from 186.86 with another falling leg.

In the bigger picture, a medium term top could be in place at 186.86 and some more consolidations would be seen. Nevertheless, as long as 55 W EMA (now at 176.21) holds, the larger up trend from 114.42 (2020 low) remains intact. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next.

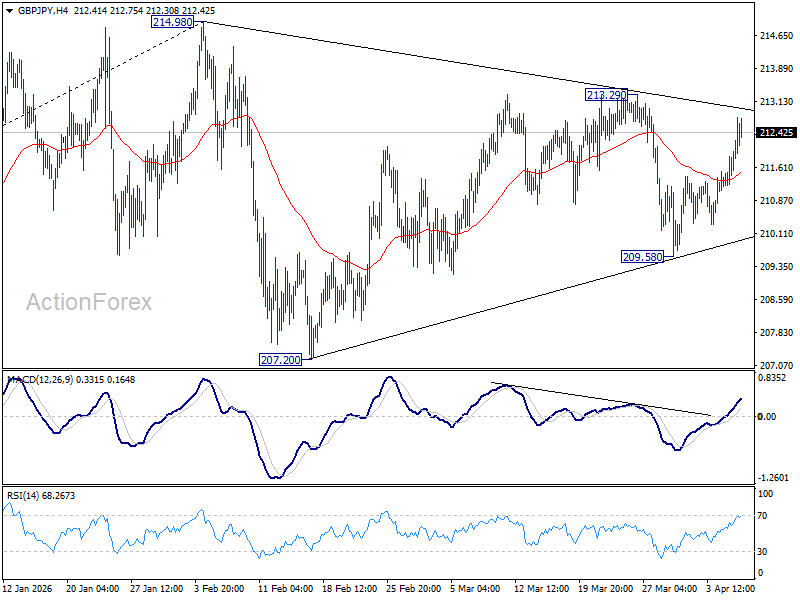

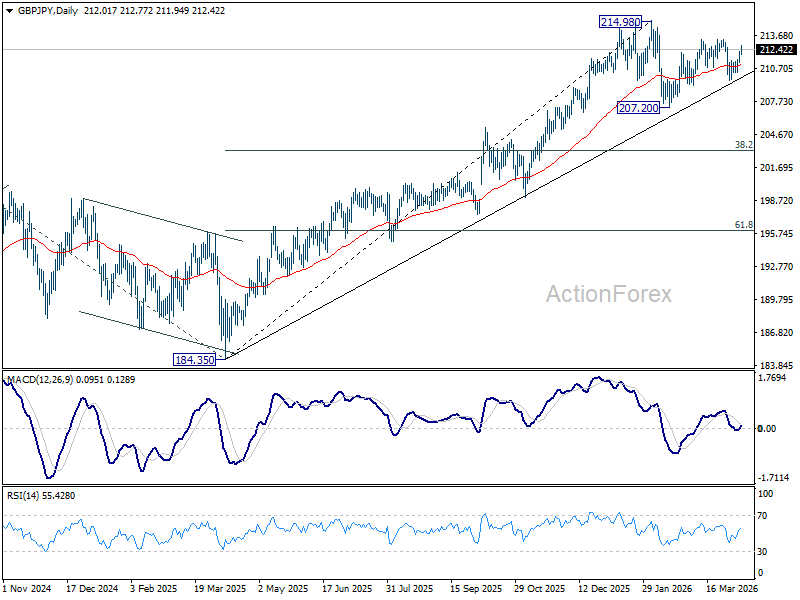

GBP/JPY Daily Outlook

Daily Pivots: (S1) 211.52; (P) 211.92; (R1) 212.60; More...

GBP/JPY is staying below 213.29 resistance despite current strong rebound. Intraday bias remains neutral first. On the upside, firm break of 213.29 will resume the rise from 207.20 and target a retest on 214.98 high. On the downside, below 209.58 will bring deeper fall to 207.20 to extend the corrective pattern from 214.98.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 203.13) holds, even in case of another deep pullback.

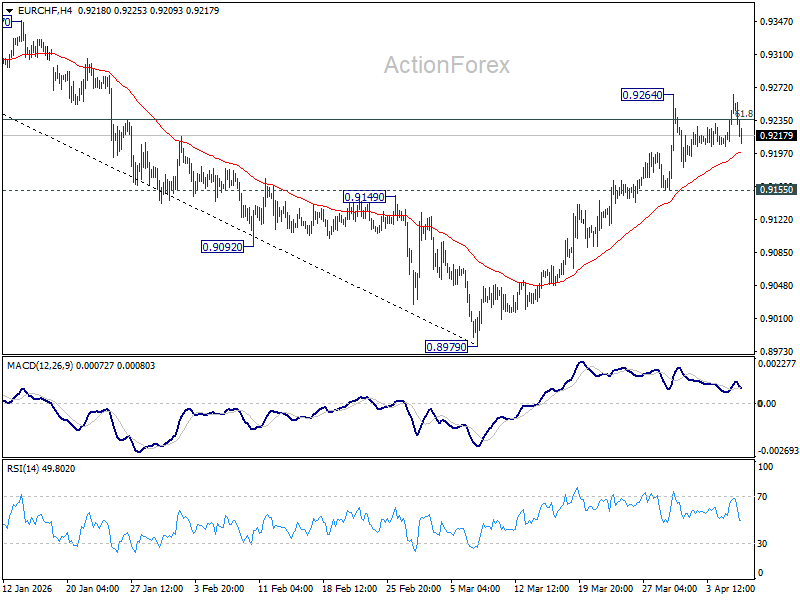

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9216; (P) 0.9241; (R1) 0.9277; More....

EUR/CHF is staying in range trading and intraday bias remains neutral. On the upside, sustained trading above 61.8% retracement of 0.9394 to 0.8979 at 0.9235 will pave the way to 0.9394 key resistance next. However, break of 0.9155 support will turn bias back to the downside for 0.8979 low.

In the bigger picture, as long as 55 W EMA (now at 0.9281) holds, the larger down trend from 0.9928 (2024 high) is still expected to continue through 0.8979 at a later stage. However, sustained break of 55 W EMA should confirm medium term bottoming, and bring stronger rise through 0.9394 resistance, even as a corrective move.

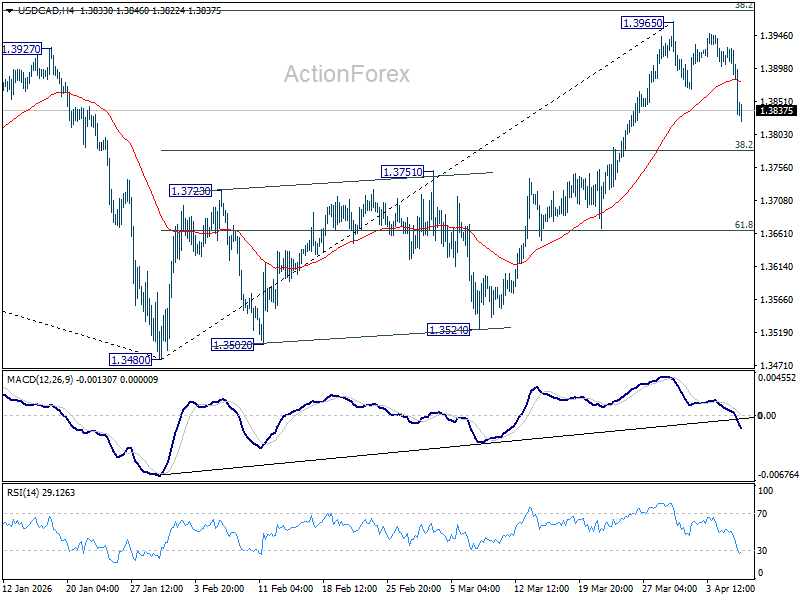

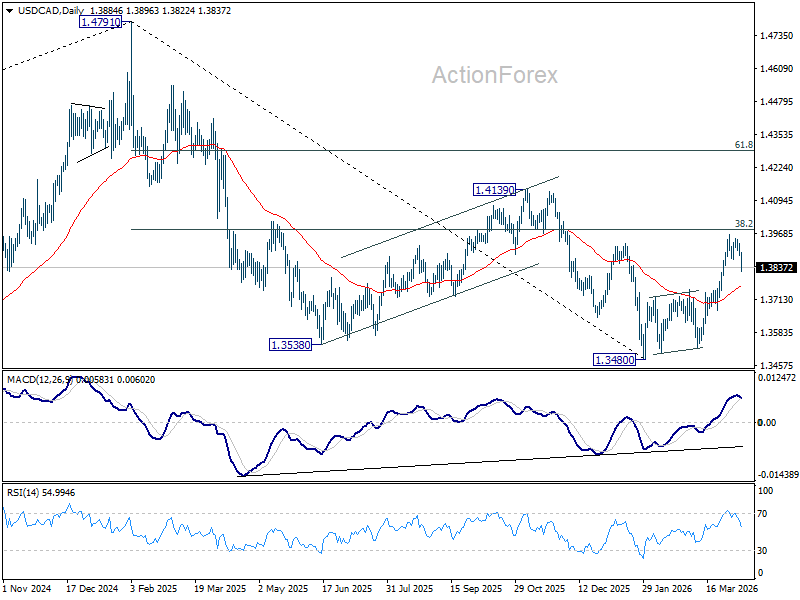

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3869; (P) 1.3900; (R1) 1.3917; More...

USD/CAD's fall from 1.3965 extended lower last week and focus is now on 38.2% retracement of 1.3840 to 1.3965 at 1.3780. Decisive break there will argue that whole rebound from 1.3840 has completed, and bring deeper decline to 61.8% retracement at 1.3665 and below. Nevertheless, strong rebound from 1.3780 will retain near term bullishness for another rise through 1.3965 at a later stage.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

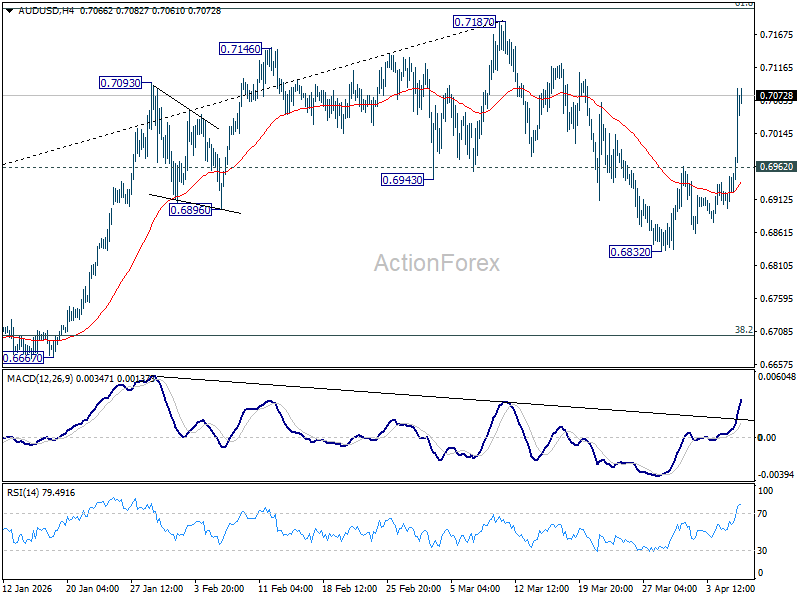

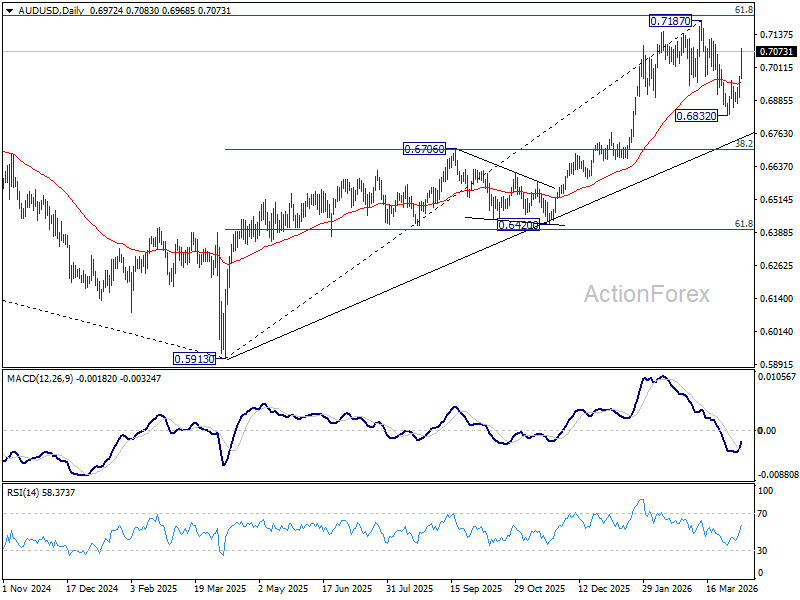

AUD/USD Daily Report

Daily Pivots: (S1) 0.6923; (P) 0.6951; (R1) 0.7004; More...

AUD/USD's strong rally today indicates that corrective fall from 0.7187 has already completed at 0.6832. Intraday bias is back on the upside for retesting 0.7187 high. Strong resistance could be seen there to bring another fall the extend the corrective pattern. On the downside, below 0.6962 resistance turned support will turn intraday bias neutral again first.

In the bigger picture, as long as 0.6706 cluster support holds, rise from 0.5913 (2024 low) should still be in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). However, firm break of 0.6706 will dampen this bullish case, and bring deeper fall back to 0.6420 support, and possibly below.

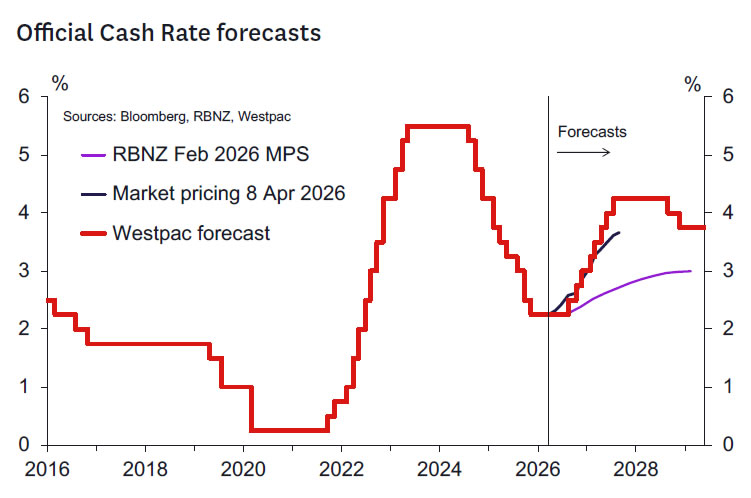

RBNZ to Tighten in September

- As widely expected, the RBNZ retained the OCR at 2.25%. There was no vote, with the decision reached by consensus.

- The commentary was hawkish as concerns of rising second-round inflation pressures were quite prominent.

- The MPC debated the options of an earlier vs later beginning to interest rate normalisation. Interest rate cuts were not discussed.

- An earlier start was described as May or July. A hike was discussed as an option today, but the Governor said that the MPC was not close to hiking at this meeting.

- The RBNZ’s short-term inflation forecast is now 4.2%y/y in June 2026 – higher than before, but close to our 4.1% forecast.

- We have pulled forward our forecast for the first OCR hike from the RBNZ to September (previously December).

- The balance of risks is towards an earlier start to hikes than September, should evidence of second-round inflation impacts accumulate.

OCR retained at 2.25% but coupled with a hawkish outlook.

The RBNZ kept the OCR unchanged at 2.25% as expected. There was no vote, with the decision reached by consensus. However, the Bank’s commentary adopted a more hawkish tone than expected. There was no discussion of needing to cut the OCR despite acknowledging that, at least in the short term, there would be greater excess capacity than previously thought. Rather, the debate was between:

- a “a pre-emptive response to medium-term inflation pressures could guard against the risk of inflation expectations becoming unanchored”; or

- a gradual increase in the OCR towards “more neutral levels” to reduce the risk of “reacting to higher nearterm inflation and accentuating weakness in the real economy and labour market”.

In the press conference the Governor noted that the MPC discussed the possibility of raising the OCR at this meeting, but there had been “no strong advocate” for doing so.

We interpret the more gradual path as being something akin to the late 2026 lift-off date that we have been forecasting, and that the RBNZ largely had in mind at the February meeting. A pre-emptive response likely implies something faster that begins by September but could come sooner than that, should evidence of secondround inflation impacts begin to accumulate. Indeed, the Governor indicated that the pre-emptive approach could have been a tightening in May or July. More dovish members were uncomfortable with the risks of that.

Key evidence that the RBNZ seeks seems to be in the form of anecdotal evidence on pricing and wage setting behaviour combined with higher frequency evidence on price setting, costs and inflation expectations coming from monthly surveys. We think it likely that at least some evidence along these lines will accumulate given the broad-based cost shock that the economy is facing. As a result, an earlier than December beginning to the tightening cycle looks much more likely now.

Hence, we are bringing forward our existing 25bp per meeting tightening profile to begin in September. The OCR will thus end 2026 at 3% and reach the previously expected 4.25% peak earlier, in September 2027. Easing is forecast to begin a year later in September 2028 with the neutral OCR reestablished in December 2028.

An earlier start than September should not be ruled out. And given it’s likely easier to explain the tightening profile in a Monetary Policy Statement meeting then the bias is likely for an earlier move to come in May versus July. The key question is: will sufficient evidence of second-round inflation impacts have accumulated by then? We think that’s still an open question at this point.

Key quotes from the press release and Record of Meeting were:

- “The Monetary Policy Committee is focused on ensuring that inflation returns to the 2-percent target midpoint over the medium term. This requires core inflation and wage growth to remain contained and medium- and long-term inflation expectations to remain around 2 percent. If these conditions are not met, decisive and timely increases in the OCR would be required.”

- “The outlook for medium-term inflation pressures depends on the size and persistence of the inflationary impulse stemming from higher oil prices and the extent to which it is offset by weaker demand in the economy.”

- “If the increase in near-term inflation is largely temporary, the Committee envisages gradually moving the OCR to more neutral levels as activity recovers and near-term inflationary pressures dissipate. However, any signs of significant secondround inflationary effects or increases in medium-term inflation expectations would require decisive and timely increases in the OCR to re-anchor inflation expectations.”

- “On the timing of any increase in the OCR, members discussed that a pre-emptive response to mediumterm inflation pressures could guard against the risk of inflation expectations becoming unanchored and reduce the extent of second round price increases.”

- “Conversely, the Committee noted the risk of reacting to higher near-term inflation and accentuating weakness in the real economy and labour market. Members noted that this could cause unnecessary volatility in output and employment if the conflict was resolved in the near term or if the economic outlook weakens by more than currently expected.”

The RBNZ’s initial thoughts on the near-term outlook.

The RBNZ provided updated inflation forecasts for the next two quarters. This is a change from their usual practice of not releasing updates to their forecasts at interim reviews and reflects that recent geopolitical developments have in the RBNZ’s words “materially altered the outlook and the balance of risks for inflation and economic growth”.

The RBNZ now expects inflation of 3% in the March quarter (previously 2.8%), rising to 4.2% in the June quarter (previously 2.7%). Those updated figures are close to our own forecasts. The RBNZ did not provide forecasts further ahead.

The RBNZ has noted that higher energy costs will push up other prices in the economy. However, longer term impacts on wage and price setting (aka. ‘second round impacts’) are expected to be constrained by weak demand at this stage. This is a key area of uncertainty and one where the RBNZ will be watching closely for signs that longer-term inflation pressures are increasing. Indeed, the RBNZ went on to note that “any signs of significant second-round inflationary effects or increases in medium-term inflation expectations would require decisive and timely increases in the OCR to re-anchor inflation expectations. The Committee is vigilant to these risks.”

While the RBNZ did not provide forecasts for other variables, they noted that the conflict and related increases in both operating costs and economic uncertainty will result in weaker activity in the near term. That’s very much in line with our own thoughts.

Things to watch ahead of the next meeting.

The RBNZ’s next policy review is on 27 May, when it will also publish a full Monetary Policy Statement (MPS) with refreshed forecasts (and probably some alternative scenarios too considering the current level of uncertainty). How the RBNZ’s stance evolves between now and then will depend on the path the Middle East conflict takes; what early indicators and anecdote suggest about the impact of the conflict on activity and inflation, both in New Zealand and abroad; and any developments in financial markets as a result of the conflict or other vulnerabilities triggered by the conflict.

As far as domestic economic indicators are concerned, we think the following are key ones to watch.

- Q1 CPI (21 April) and April Selected Prices (15 May): These pricing indicators will reveal the initial firstround direct and indirect impacts of the recent surge in fuel prices. They will provide some insight as to how high headline inflation might peak, but not about how long it will remain at elevated levels.

- Q1 QSBO (21 April) and April/May ANZ Business Outlook (30 April/27 May): Unfortunately, the data-rich QSBO survey was initially in the field very early in the conflict (it is unclear whether a breakdown of early and late responses will be released). Therefore, the ANZ surveys may provide a more up-to-date account of how businesses are responding to the conflict.

- March/April PMI and PSI surveys (mid-April/mid- May): These may provide some early insight regarding the likelihood of a contraction in GDP in Q2.

- Q1 labour market surveys (6 May): Employment and hours worked data from the HLFS and QES surveys will cast light on what momentum the economy had going into the conflict, while the LCI will cast light on underlying inflation pressures.

- Budget 2026 (28 May): While the formal unveiling of the Budget comes the day after the release of the MPS, ahead of the Budget the RBNZ’s MPC will receive a high-level briefing from the Treasury on what to expect at the macro level. Pre-Budget speeches and policy announcements may reveal more in the public sphere.

In addition to the above, we will be monitoring a range of other high-frequency indicators, such as monthly data on filled jobs, consumer spending, building consents, housing market activity and prices, job ads and consumer confidence. We will also be paying close attention to developments in prices for New Zealand’s key export commodities. The RBNZ looks to also be focused on anecdotal evidence of business pricing and wage setting behaviour – although that will be harder to track.

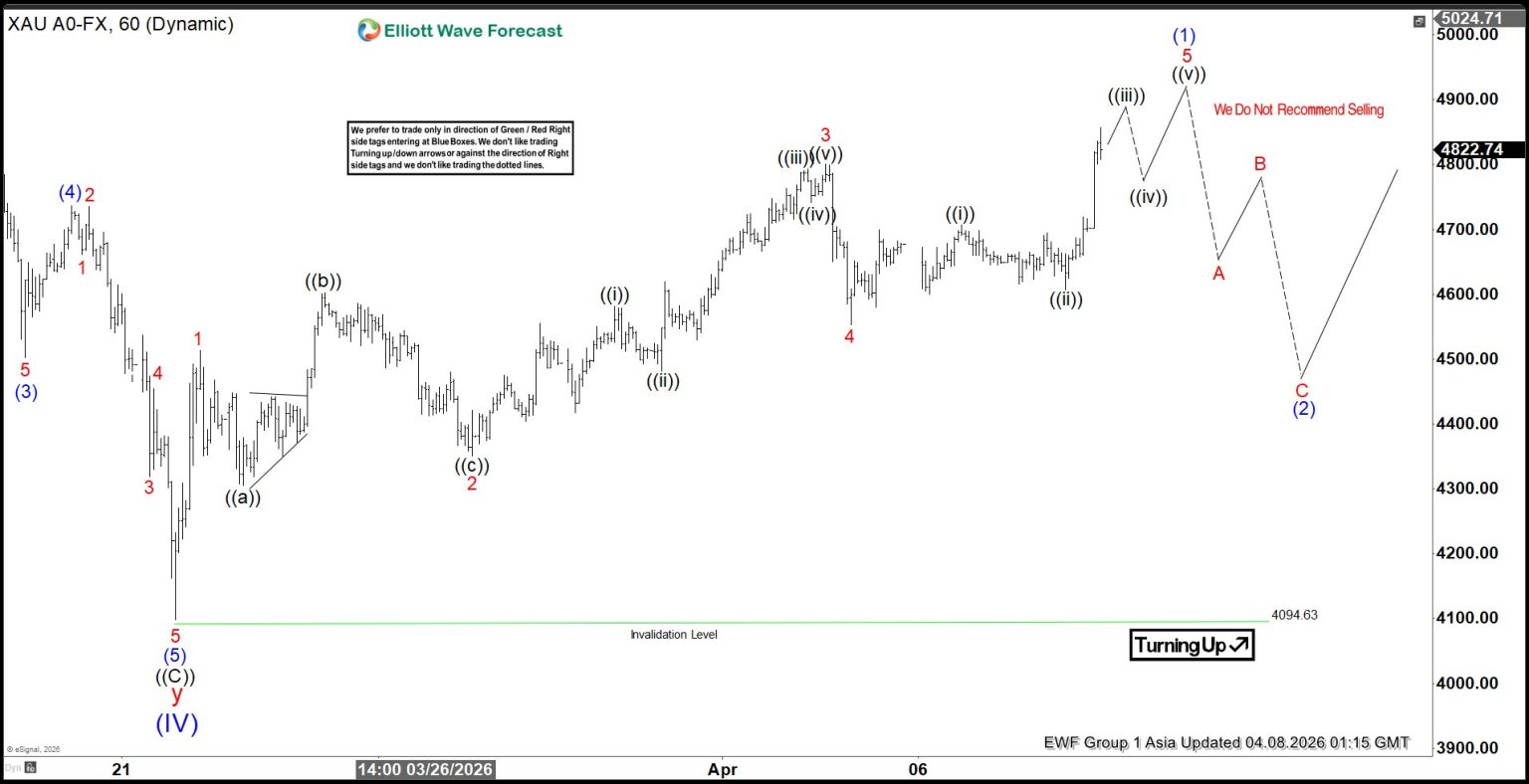

Elliott Wave: Gold (XAUUSD) Builds 5 Swings Higher, Favoring Upside

Gold (XAUUSD) reached an all-time high of $5598.75 on January 29 before undergoing a notable correction. This decline unfolded in a 3 Elliott waves zigzag structure, ultimately finding support at $4094.63. We have identified this corrective phase as wave (IV). Since then, the metal has resumed its upward trajectory, entering wave (V). To fully confirm the bullish outlook, however, gold must decisively break above the prior peak of $5598.75. Without such a move, the risk of a double correction remains present.

The short-term rally from the wave (IV) low has already displayed a five-swing structure. This pattern is characteristic of a motive sequence, which generally signals continuation rather than exhaustion. Consequently, the technical picture favors further upside momentum. From the wave (IV) base, wave 1 concluded at $4512.85, followed by wave 2 at $4350.52. Wave 3 extended higher to $4800.46, while the subsequent pullback in wave 4 ended at $4553.16. Current price action suggests that wave 5 is nearing completion. Once finalized, this will mark the end of wave (1) at a higher degree.

Afterward, gold is expected to retrace in wave (2). This corrective phase should address the cycle that began from the March 23 low. Such a pullback would be a natural development within the broader bullish structure, setting the stage for renewed strength. If the outlined progression holds, the metal could establish a sustainable advance beyond its previous record high.

Gold (XAUUSD) 60-Minute Elliott Wave Chart

XAUUSD Elliott Wave Video:

https://www.youtube.com/watch?v=PKRrBd3WawQ

Oil Tumbles Below USD 100/bbl on US-Iran Ceasefire Agreement

In focus today

All focus this morning is on the ceasefire in the Middle East and the impact on energy prices. Markets will closely monitor any information released on expectations for oil and gas flows.

Tonight, the minutes from FOMC March meeting are due for release. The minutes may get less attention than usual as the war in Iran was only in its early stages at the time of the meeting. That said, we will keep an eye out for any forward guidance on the balance sheet operations, which the Fed has lately provided mostly in the minutes.

Economic and market news

What happened overnight

In the US-Iran war, President Trump agreed to a two-week ceasefire with Iran just two hours before his deadline for Iran to reopen the Strait of Hormuz. Iran agreed to halt attacks and provide safe passage through the strait, while the US and Israel committed to the terms of the truce. Brent crude fell as low as USD92/bbl on the news, but the drop in prices is contingent on the pre-condition that traffic through the Strait of Hormuz resumes. For prices to stabilise at lower levels, oil and gas flows through the strait must pick up again, which remains uncertain. The deal looks fragile, particularly as Iran is allowed to charge fees on ships passing through. Stock markets surged, with S&P 500 futures rising over 2% and European futures up more than 5%, while the US dollar weakened on improved risk sentiment. The war is now in its sixth week, and scepticism remains about whether the ceasefire will hold, as many view it as a trust-building exercise. Significant uncertainties persist, and the oil market and broader markets are likely to stay volatile as they monitor activity from the Gulf.

In New Zealand, the Reserve Bank (RBNZ) kept its official cash rate unchanged at 2.25% during its April meeting, as expected. The central bank highlighted that rising oil and fuel prices driven by Middle East tensions are adding to near-term inflation pressures while weighing on economic growth. The RBNZ reiterated its focus on medium-term inflation, emphasising the importance of containing core inflation, wage growth, and inflation expectations.

What happened yesterday

In the euro area, the April Sentix investor confidence indicator declined to -19.2, its lowest level in a year, reflecting concerns over the war in Iran. The monthly drop is comparable to the sentiment deterioration seen in April last year following Trump's "Liberation Day" and is about two-thirds of the decline observed in March 2022 when the war in Ukraine began.

In Sweden, March inflation surprised on the downside, with CPI at 0.6% y/y (cons: 1.2%), CPIF at 1.6% y/y (cons: 2.2%), and CPIF-XE at 1.1% y/y (cons: 1.5%). Food prices declined -0.7% m/m, more than anticipated, while energy prices fell sharply by -5.3%, driven by milder weather lowering electricity costs after elevated levels in January and February. The data does not yet reflect any impact from the war in Iran, with the lower reading likely attributable to seasonality. Sweden's April services PMI rebounded strongly to 55.7 in March (prior: 48.3), supported by higher order intake and business volumes. Price pressures also rose, presenting a somewhat hawkish signal in contrast to the earlier low inflation print.

In Denmark, the Danish central bank did not sell EUR/DKK in FX intervention in March, where EUR/DKK hit 7.4728. This aligns with our expectation that it will allow the pair to rise to 7.4730-50 range before stepping into the market.

In the US, health insurers rallied after the government announced a 2.48% average increase in 2027 Medicare Advantage payment rates, exceeding the 0.09% proposed in January. The USD 13bn boost is expected to improve margins, with shares of UnitedHealth, CVS Health, and Humana rising in response.

Equities: The ceasefire agreed overnight between Iran, the US and Israel is clearly dominating market action this morning. What we are seeing is a classic "big war/cease fire reversal trade" across asset classes and equities.

In Asia, there is a pronounced cyclical rotation, led by tech, with the semiconductor space up around ~10% this morning. Defensives and low-vol stocks are underperforming, while energy is a clear laggard, down roughly 7%.

We will refrain from going into the details of the various statements from US and Iranian officials leading up to this, but once again this outcome is fully consistent with Trump's well-known negotiation tactics - maximum pressure followed by a "TACO"-style de-escalation. This remains the relevant framework for interpreting developments going forward, also as we approach the expiry of the two-week ceasefire. Importantly, this is only a ceasefire, and a lot can still go wrong, but it goes without saying that this is a step in the right direction. European equity futures are up around ~5% this morning, while US futures are higher by ~2-3%.

FI and FX: With Trump's deadline fast approaching, the US president announced a two-week ceasefire with Iran. This provided an imminent relief for markets, with oil prices collapsing below USD100/barrel, US yields falling by more than 10bp across the curve and EUR/USD rallying towards 1.17. The SEK, which weakened through yesterday's session on the back of lower-than-expected Swedish inflation, rallied sharply on the ceasefire announcement. As for the NOK, which is caught by opposing forces, EUR/NOK remains below 11.20. Although a lot of uncertainty still prevails, especially beyond the two-week ceasefire, risk sentiment seems to have turned and will likely act supportive for the time being.