Sample Category Title

NZD/USD Tests Major 0.57 Support Ahead of RBNZ Meeting – FX Technical Levels

NZD/USD has been thrashed since the start of the US-Iran war, amid heavy concerns about energy supply in the Land of the Kiwi.

At the beginning of 2026, the New Zealand Dollar was on a powerful run. Traders priced higher odds for rate hikes, while most other Central Banks were priced for pauses and cuts. Since then, pricing has dramatically shifted.

Numerous policymakers now hint at incoming rate hikes to diminish the inflationary impact of 60% rises in Oil prices.

Having lost some relative strength, the new Governor Anna Breman failed to forecast a significant hawkish turn that had been anticipated by Market participants earlier in the year – You can access her recent Speech right here.

Having missed its Q4 GDP data, released in mid-March, traders quickly began pricing out any signs of heating in the NZ economy.

Combine these factors with a gigantic rise in the Petrodollar since March, and traders got exactly what they needed to not only take profits on previous bullish views but also reverse them into a bearish trend – the major pair is down 4.75% since.

The upcoming meeting is strongly priced for a pause (about 90% odds).

However, traders have priced in 60 basis points of hikes for the rest of the year.

Given the turn in fundamentals and upcoming event, the drops in NZD/USD might just be over.

Traders will focus on New Zealand macro data and especially the Royal Bank's inflation outlook for the next meeting (May 27, 2026).

Combine high odds of more hawkish communications with daily bullish divergences (see below), and the NZD/USD could be poised for a decent upside reversal – The rest will be to see if it leads to a proper uptrend.

To prepare for the upcoming key RBNZ meeting this evening, it is appropriate to conduct a multi-timeframe analysis of NZD/USD and assess potential scenarios.

NZD/USD Multi-Timeframe Technical Analysis

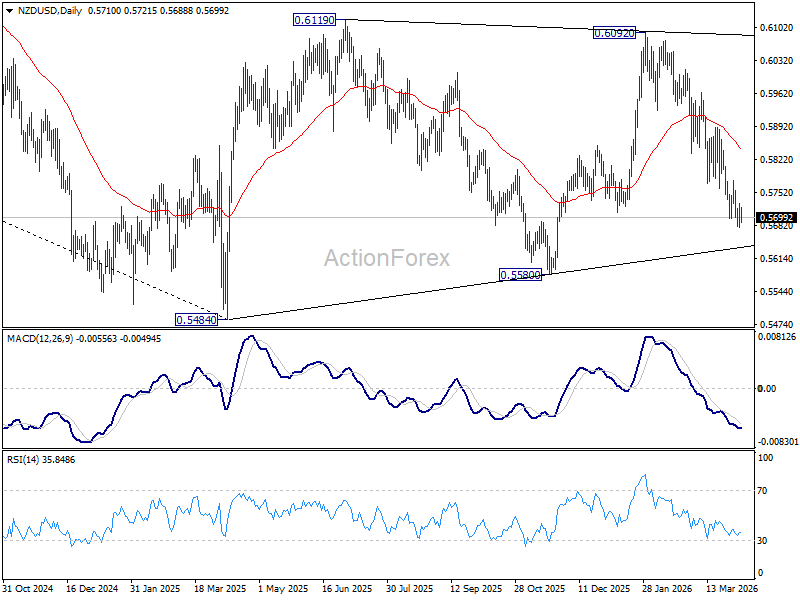

Daily Chart

NZD/USD Daily Chart – Source: TradingView. April 7, 2026

The Kiwi Dollar has entered a significant downtrend since beginning March, easing from 0.60 right below 0.57.

Subject to heavy profit taking from its mid-January gigantic rise, the selloff accelerated as concerns for antipodean crude delivery kept looming on the NZD buying power.

The conflict is nearing an important turning point; A de-escalation deadline is about to expire, so if the situation worsens, the outlook can be quite cloudy – To help yourself to spot a direction, it can be quite essential to look at the Dollar Index (DXY), remaining close to 100.00. Rejecting its highs will help NZD/USD to rebound.

If de-escalation occurs, NZD/USD is poised for a consequent reversal, particularly as the RBNZ is expected to tighten the screws for a potential future hike – Combine this with prices reaching the bottom of its main downward channel, and technicals are also corroborating this view.

Be careful as Monetary Policy meetings can be quite unpredictable, hence the largest traders will await for the decision to move their pawns.

Let's take a closer look to spot levels of interest for the ongoing correction.

4H Chart and Technical Levels

NZD/USD 4H Chart – Source: TradingView. April 7, 2026

The immediate action is still indecisive, as seen with the RSI hanging around the neutral zone.

To tilt the scales however, the recent dip below 0.57 could not hold, hence bulls could be getting the upper hand in coming times. This will need to be confirmed after the RBNZ meeting (tonight) and particularly after a break of the 4H 50-period MA (0.57275).

Trading Levels for NZD/USD:

Resistance Levels

- 4H 50-period MA (0.57275)

- 0.5770 to 0.5790 Major Momentum Pivot (channel highs)

- 0.5850 December High Pivotal Resistance

- 0.5885 to 0.59 Minor resistance

- September 2025 Pivot area 0.60 to 0.60150

Support Levels

- Main Support 0.57 (+/- 150 pips) – testing

- War lows 0.56825

- Minor Support 0.5650

- January 2025 Support 0.56

1H Chart

NZD/USD 1H Chart – Source: TradingView. April 7, 2026

Looking even closer to the 1H timeframe, the Major FX pair marks heavy indecision as traders await the key fundamental events to make their moves.

- Above 0.57275, bulls take the upper hand which would point to 0.58850 (Channel highs)

- Below 0.5690, bears retake control and point to further selling acceleration.

Safe Trades and good luck for the upcoming meeting!

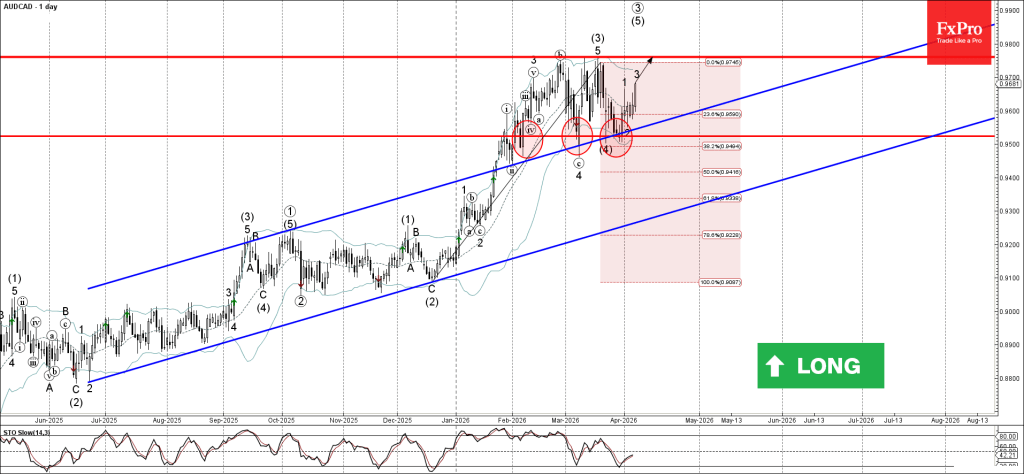

AUDCAD Wave Analysis

AUDCAD: ⬆️ Buy

- AUDCAD reversed from support level 0.9510

- Likely to rise to resistance level 0.9760

AUDCAD currency pair recently reversed up from the support level 0.9510 (which has been reversing the price from February).

The support level 0.9510 was strengthened by the lower daily Bollinger Band, upper trendline of the weekly up channel from June and the 38.2% Fibonacci correction of the upward impulse from December.

Given the long-term uptrend, AUDCAD can be expected rise to the next resistance level 0.9760 (which stopped earlier waves b and (3)).

Eco Data 4/8/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Feb | 3.30% | 2.70% | 3.00% | 2.50% |

| 02:00 | NZD | RBNZ Interest Rate Decision | 2.25% | 2.25% | 2.25% | |

| 05:00 | JPY | Eco Watchers Survey: Current Mar | 42.2 | 47.9 | 48.9 | |

| 06:00 | EUR | Germany Factory Orders M/M Feb | 0.90% | 3.20% | -11.10% | |

| 07:00 | CHF | Unemployment Rate M/M Mar | 3.00% | 3.00% | 3.00% | |

| 08:30 | GBP | Construction PMI Mar | 45.6 | 43.6 | 44.5 | |

| 09:00 | EUR | Eurozone PPI M/M Feb | -0.70% | -0.70% | 0.70% | 0.80% |

| 09:00 | EUR | Eurozone PPI Y/Y Feb | -3.00% | -3.00% | -2.10% | -2.00% |

| 09:00 | EUR | Eurozone Retail Sales M/M Feb | -0.20% | -0.20% | -0.10% | |

| 14:30 | USD | Crude Oil Inventories (Apr 3) | 3.1M | -1.0M | 5.5M | |

| 18:00 | USD | FOMC Minutes |

| 23:30 | JPY |

| Labor Cash Earnings Y/Y Feb | |

| Actual | 3.30% |

| Consensus | 2.70% |

| Previous | 3.00% |

| Revised | 2.50% |

| 02:00 | NZD |

| RBNZ Interest Rate Decision | |

| Actual | 2.25% |

| Consensus | 2.25% |

| Previous | 2.25% |

| 05:00 | JPY |

| Eco Watchers Survey: Current Mar | |

| Actual | 42.2 |

| Consensus | 47.9 |

| Previous | 48.9 |

| 06:00 | EUR |

| Germany Factory Orders M/M Feb | |

| Actual | 0.90% |

| Consensus | 3.20% |

| Previous | -11.10% |

| 07:00 | CHF |

| Unemployment Rate M/M Mar | |

| Actual | 3.00% |

| Consensus | 3.00% |

| Previous | 3.00% |

| 08:30 | GBP |

| Construction PMI Mar | |

| Actual | 45.6 |

| Consensus | 43.6 |

| Previous | 44.5 |

| 09:00 | EUR |

| Eurozone PPI M/M Feb | |

| Actual | -0.70% |

| Consensus | -0.70% |

| Previous | 0.70% |

| Revised | 0.80% |

| 09:00 | EUR |

| Eurozone PPI Y/Y Feb | |

| Actual | -3.00% |

| Consensus | -3.00% |

| Previous | -2.10% |

| Revised | -2.00% |

| 09:00 | EUR |

| Eurozone Retail Sales M/M Feb | |

| Actual | -0.20% |

| Consensus | -0.20% |

| Previous | -0.10% |

| 14:30 | USD |

| Crude Oil Inventories (Apr 3) | |

| Actual | 3.1M |

| Consensus | -1.0M |

| Previous | 5.5M |

| 18:00 | USD |

| FOMC Minutes | |

| Actual | |

| Consensus | |

| Previous | |

RBNZ Preview: Hawkish Hold May Spark NZD/USD Bounce, Not Trend Reversal

The Reserve Bank of New Zealand is widely expected to leave the Official Cash Rate unchanged at 2.25% in the upcoming Asian session, with consensus firmly aligned around a hold. NZD/USD may see a relief bounce if the RBNZ delivers a hawkish hold, but the broader downtrend is unlikely to reverse as weak domestic demand and global risks continue to cap upside.

With the decision largely priced in, attention will turn to statement and the post meeting press conference, where tone—not action—will drive market reaction. The key issue is how the RBNZ interprets the current oil-driven inflation spike against a backdrop of softening domestic demand.

This puts the central bank in a familiar dilemma: oil-driven inflation versus fragile growth. Headline inflation is hovering above the top of the 1–3% target band at 3.1%, but policymakers may choose to “look through” the shock if it is deemed temporary. However, any concern about second-round effects, particularly on wages and expectations, would tilt the stance more hawkish.

At the same time, signs of economic fragility are building. GDP momentum has softened and unemployment is trending higher toward 5.4%. This leaves policymakers cautious about tightening prematurely, even as inflation pressures remain elevated.

The outcome is likely to hinge on forward guidance. A hawkish hold, emphasizing sticky core inflation and leaving the door open for future hikes, could trigger a relief bounce in NZD/USD. A dovish hold, focused on spare capacity and weak demand, would likely reinforce downside pressure.

Technically, NZD/USD, trading at around 0.5700, is still locked inside a year long consolidation pattern that started at 0.5484 (April 2025). It's plausible that the consolidation pattern has completed with three waves to 0.6092 (January 2026). But the momentum of the subsequent fall doesn't warrant range breakout yet.

For the near term, risk will stay on the downside as long as 55 D EMA (now at 0.5843) holds in case of recovery. Any downside acceleration ahead, and break of 0.5580 support will argue that the long term down trend is ready to resume through 0.5484.

On the other hand, firm break of 55 D EMA will suggest that the consolidation pattern is indeed a five-wave triangle, and another bounce would be seen towards 0.6092 resistance before the consolidation finally completes.

Sunset Market Commentary

Markets

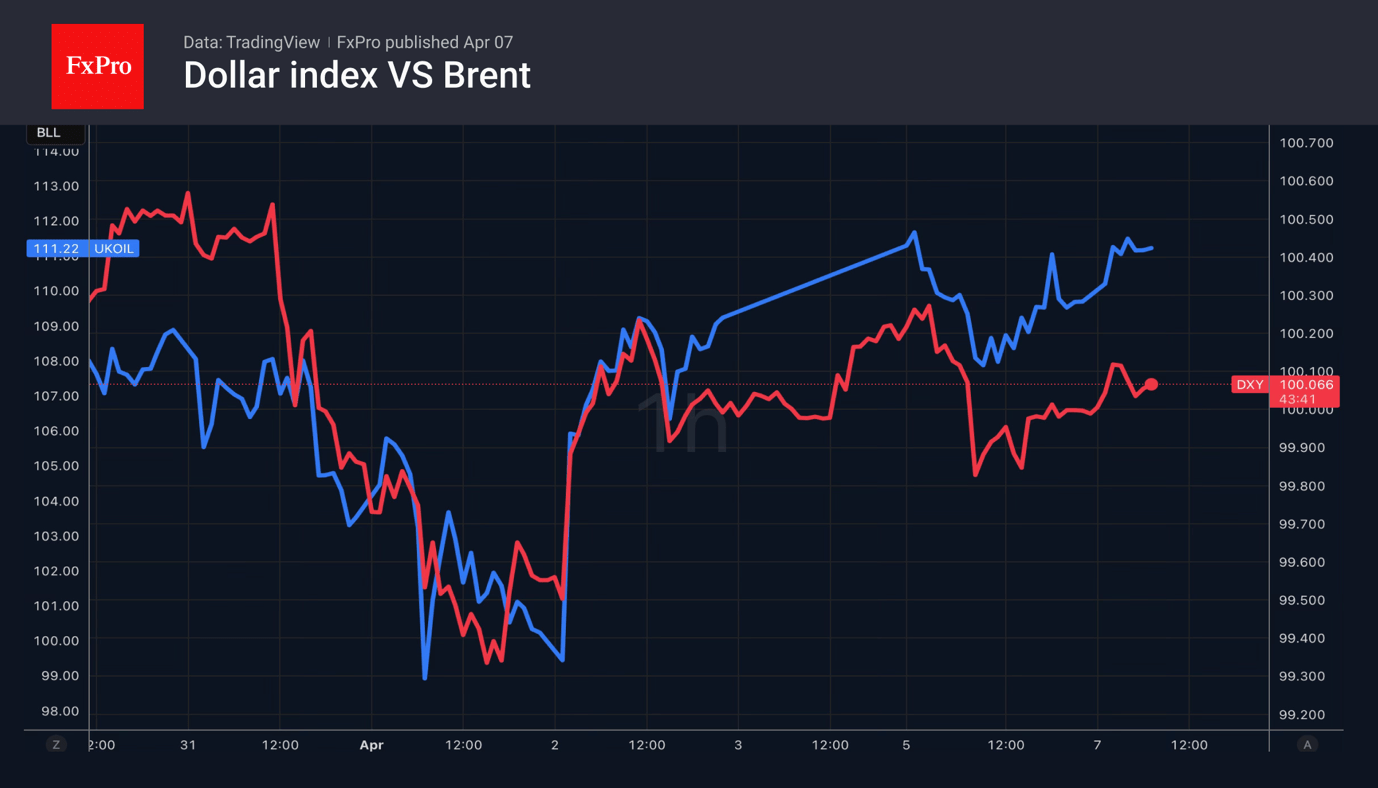

US President Trump this time seems to stand with his 8pm ET deadline to deliver a fatal blow against Iran (hitting energy facilities & infrastructure) unless the country cedes to his demands. On Truth Social he posted that “a whole civilization will die tonight, never to be brought back again. I don’t want that to happen, but it probably will”. Almost simultaneously, vice-president JD Vance at a press conference In Budapest suggested that “very shortly, this war will come to an end”. He hinted at two pathways to the end game, one of which is some sort of last-minute deal, the other being forceful military action. In the meantime, both the US and Israel stepped up pressure by striking more than 50 targets on Kharg Island, Iran’s oil export hub. Iran also rejected the temporary ceasefire offer put forward by intermediaries with threats to close the straight of Bab-El-Manbab (Red Sea) via proxies as well. Brent crude holds near the (June) contract high of $110/b. Several European and UK markets return from the long Easter break with interest rate markets doing so in bear flattening fashion. German yields add 2.5 bps (30-yr) to 7 bps (2-yr) with UK yields currently 5 bps higher at the front end of the curve. Central bank comments include ECB Wunsch in an interview with the WSJ. He doesn’t want to exclude an April rate hike: “We need to move at some point to control the indirect effects. So the focus will be on what’s our view over the medium term and it’s still an uncertain view.” He admitted that the ECB responded too slowly to the previous energy supply shock (2022) which is something to draw lessons from. That basically boils it down to April or June. He plotted two scenarios for the ECB. “Either this crisis ends quite soon and you know if we hike then we can probably undo that after a while. Or, this crisis is going to last and then the first hike will only be the first hike of probably a series.” Interestingly, he said that we need some demand destruction, although he linked that in first instance to avoiding fiscal stimulus to dampen the blow from rising energy prices. ECB Radev said that the likelihood of the more adverse scenario has increased, but doesn’t know if the ECB will have enough data by April to potentially pull the trigger on interest rates. During the Easter weekend, ECB Villeroy suggested that we’re closer to the adverse than to the baseline scenario. At the March ECB’s watcher conference, ECB President Lagarde hinted at some measured adjustment of policy if the energy shock gives rose to a large though not-too-persistent of overshoot of the inflation target. Agility is key so inaction isn’t interpreted as not willing to act. US Treasuries outperform today, but they ceded more ground especially just ahead of the Easter break (after strong payrolls). Today’s weekly ADP employment data continue to point at a strengthening labour market while (outdated) February core durable goods orders surprised positively (though after a January downward revision). The dollar (EUR/USD 1.1565) and stock markets (-0.5%) trade more stoic going into tonight’s deadline.

News & Views

Czech CPI inflation printed at 0.6%% M/M and 1.9% Y/Y in March (from -0.1% M/M and 1.4% in February). Energy prices rose 5.3% M/M reducing the decline compared to the previous year from -7.8% in February to -1.7% Y/Y. Services inflation rose 0.3% M/M and 4.7% Y/Y. Goods inflation accelerated to 0.8% M/M raising the yearly figure to 0.1% Y/Y from -0.7% previously. Headline inflation still holding below the CNB’s 2% target probably leaves the central bank time to assess how much the (energy) price shock from the conflict in the Middle East will filter though toward the rest of the economy. In the Minutes of the March meeting, the CNB analyzed that it was necessary to keep policy tight, not underestimate the cost of the current energy shock and that it remains prepared to respond in case of risks to a further rise in core inflation. At the same time, there was a consensus that the external shock occurred in a context of low inflation and relatively high interest rates. This provides a buffer for absorbing the shock and makes it premature to already consider raising rates. Despite the wait-and-see mode, markets currently still discount gradual rate hikes by the CNB (approximately 50 bps to near 4%) towards the turn of the year.

A survey of the German IFO institute showed that business climate in the German Automotive industry deteriorated somewhat in March. The indicator fell to minus 18.7 down from minus 15.7 points in February as companies assessed their current business situation as considerably worse. However, at the same time companies raised their expectations as they saw an improvement both for the backlog of orders and export orders. Companies also expect job cuts to slow down in coming months. IFO even assessed that “the decline in new jobs, which could be observed since 2022, seems to have come to a halt”.

Fed’s Williams Sees No Policy Shift Despite Oil-Driven Inflation Risks

New York Fed President John Williams signaled that the Fed could remain in a wait-and-see stance, even as higher energy prices from the Iran conflict are expected to push headline inflation higher. Speaking to Bloomberg TV, Williams said “the story hasn’t changed very much,” emphasizing that underlying inflation dynamics remain broadly stable despite the oil-driven headline surge.

Williams acknowledged that rising energy costs will lift headline inflation, but stressed the distinction between headline vs underlying inflation, suggesting policymakers are not yet concerned about second-round effects. He also downgraded his 2026 growth outlook modestly to 2.0–2.5% from 2.5–2.75%, while maintaining confidence in a stable labor market. “We’ve seen the labor market much more stable now,” he said, adding it is “definitely not… weakening.”

On policy, Williams made clear there is no urgency to adjust rates, stating that “monetary policy is exactly where it needs to be.” The Fed, in his view, is well positioned to monitor how the oil shock feeds through to the economy before responding.

Central Banks Risk Making a Mistake

- Raising interest rates during an oil crisis is a clear mistake.

- Stagflation is knocking at the door of the US economy.

The US dollar has been fluctuating within a 0.5% range since the end of last week amid conflicting signals regarding the situation in the Middle East. On the one hand, Iran has rejected mediators’ proposal for a 45-day ceasefire with the US, which marked a clear escalation and triggered a rise in Brent prices and a strengthening of the greenback. On the other hand, traffic through the Strait of Hormuz is at its highest since early March, as Tehran concludes more and more bilateral agreements on passage through the world’s main oil artery.

The gradual restoration of pre-war traffic through the Strait of Hormuz is key to stabilisation. Brent prices already factor in a risk premium for potential US strikes on Iran’s energy infrastructure. Another postponement of the ultimatum would cause Brent and the US dollar to retreat.

The conditions proposed by one side remain a red line for the other. So far, there has been no clear progress, and the parties are not genuinely moving closer to an agreement.

The problem is that geopolitical risks will not disappear even in the event of a truce, sustaining heightened demand for the US dollar as a safe-haven asset. This is all the more so given that the Fed’s rival central banks are poised to make a mistake by raising interest rates. The oil and gas shortage is a blow to spending, and a tightening of monetary policy will double the economic pain.

The fall in EUR/USD could have been more severe were it not for Donald Trump’s eccentricity, which is undermining investor confidence in the US dollar and bonds. At the same time, the market is realising that the US economy will also suffer. It is heading towards stagflation, as evidenced by the dynamics of leading indicators.

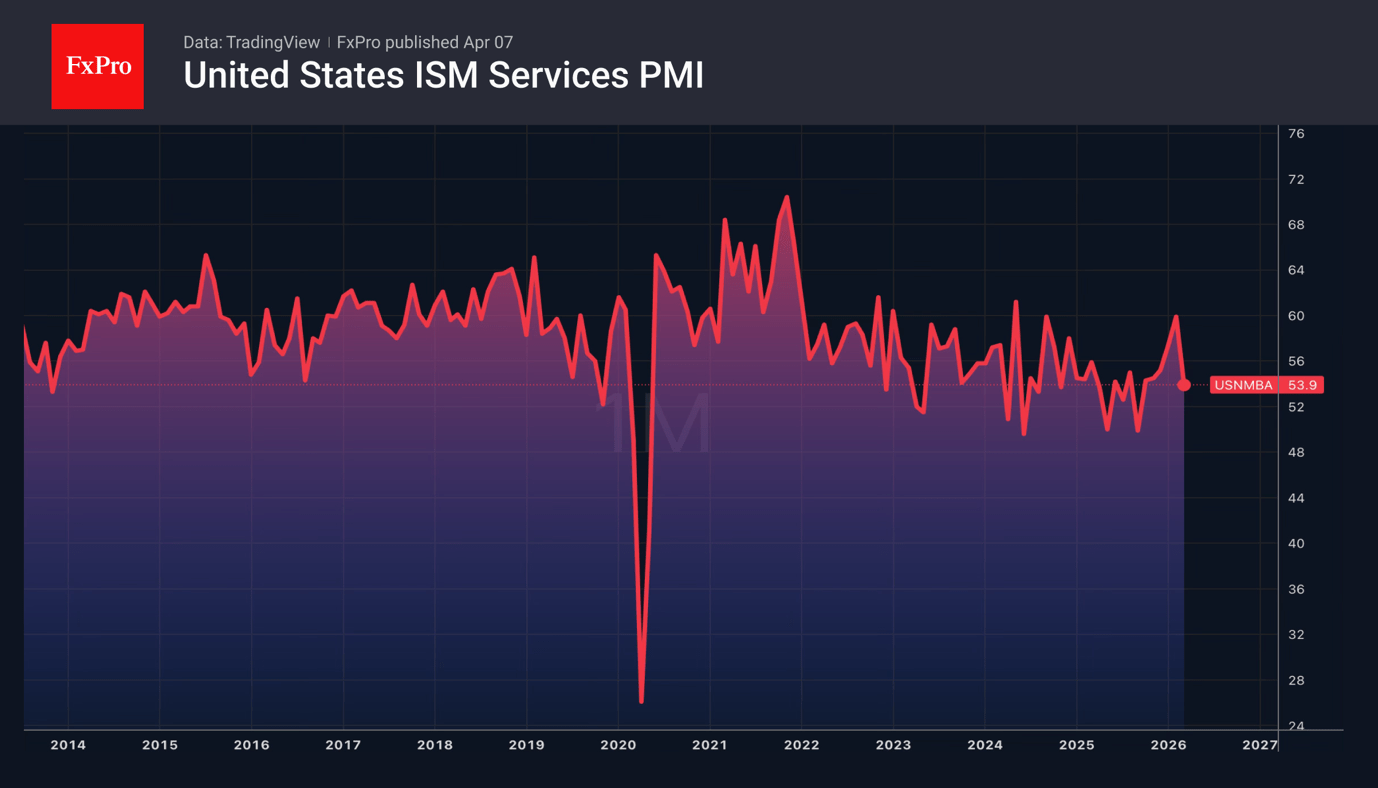

In March, the ISM Services PMI fell, with the employment component dropping to its lowest level since 2023. Meanwhile, the input prices component reached its highest level since October 2022, recording its largest monthly increase in the last 14 years. Stagflation is evident, which is weighing on the US dollar.

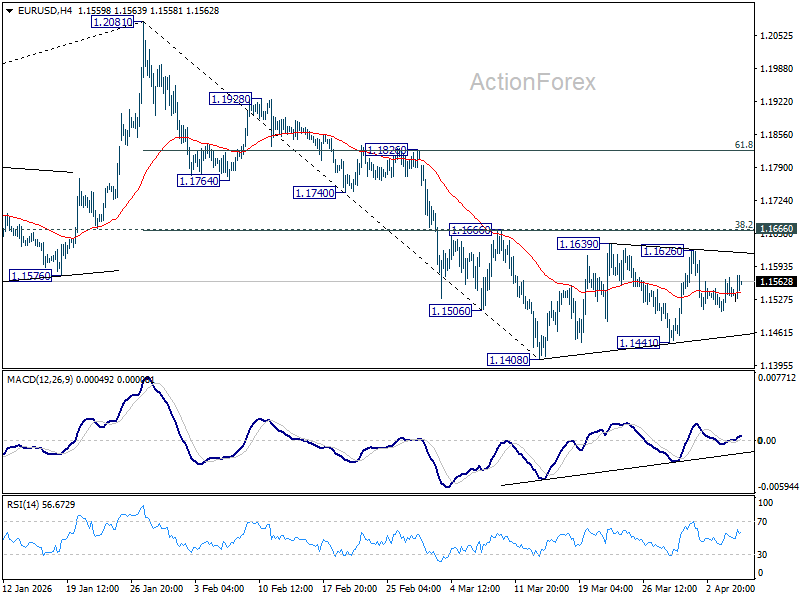

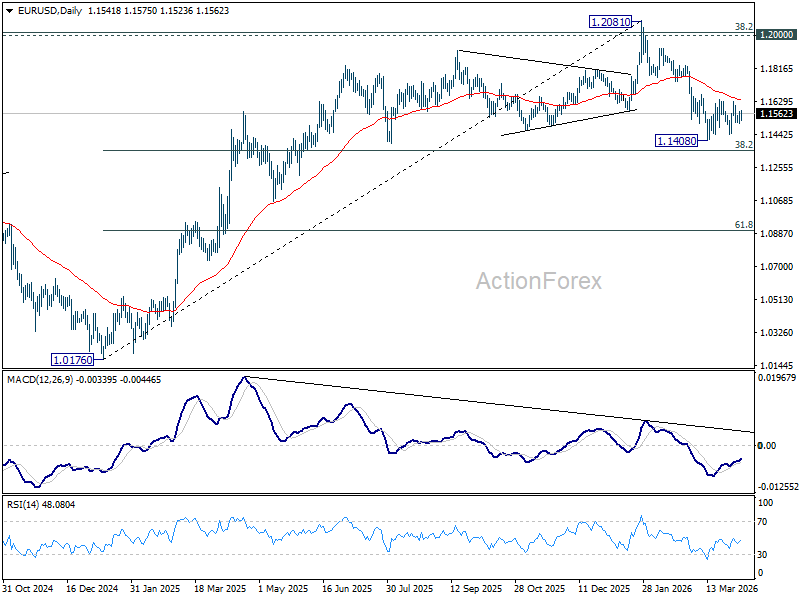

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1508; (P) 1.1540; (R1) 1.1575; More….

Intraday bias in EUR/USD remains neutral as consolidations from 1.1408 is still extending. With 1.1666 cluster resistance (38.2% retracement of 1.2081 to 1.1408 at 1.1665) intact, further decline is expected. On the downside, firm break of 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. However, decisive break of 1.1666 will argue that the fall from 1.2081 has completed, and turn bias back to the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824.

In the bigger picture, prior break of 55 W EMA (now at 1.5011) should confirm rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. Deeper fall is expected to long term channel support (now at 1.0535). Meanwhile, risk will stay on the downside as long as 1.2081 holds, even in case of strong rebound.

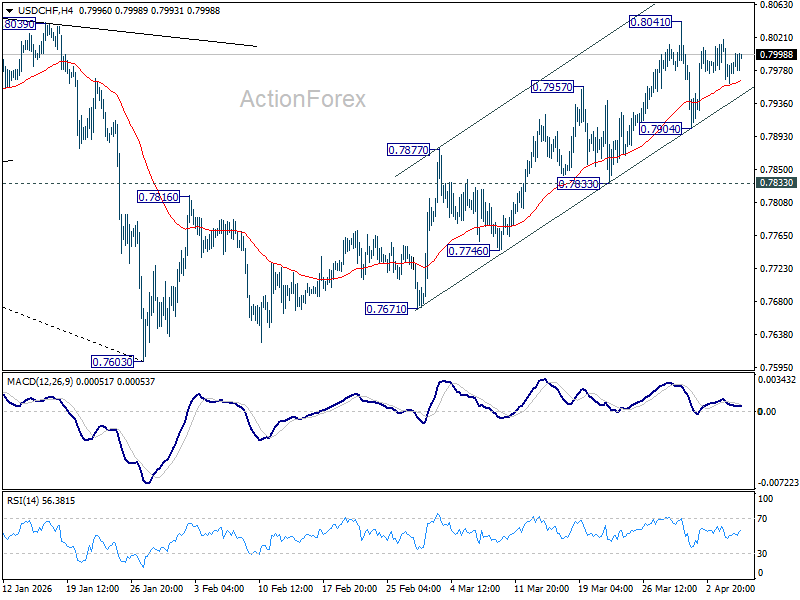

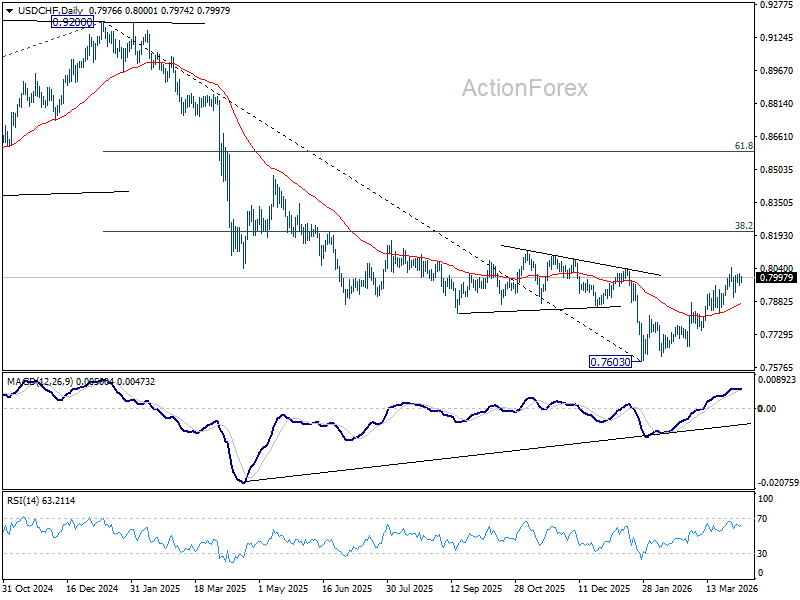

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7956; (P) 0.7988; (R1) 0.8015; More….

Intraday bias in USD/CHF stays neutral as consolidation from 0.8041 is still extending. Further rally is expected with 0.7833 support intact. On the upside, break of 0.8041 will resume the whole rally from 0.7603, and target 38.2% retracement of 0.9200 to 0.7603 at 0.8213. However, decisive break of 0.7833 support will argue that the rebound has completed, and turn bias back to the downside for deeper fall.

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8081) will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

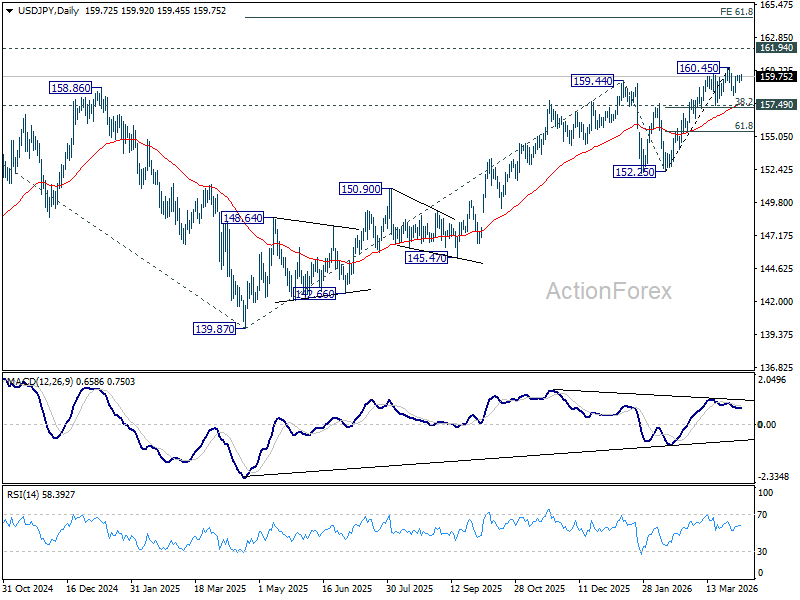

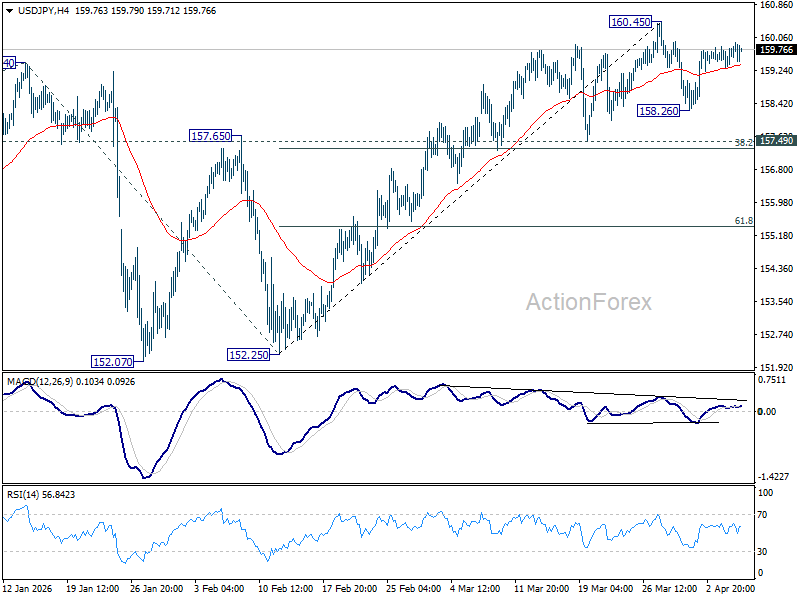

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.48; (P) 159.62; (R1) 159.81; More...

Intraday bias in USD/JPY stays neutral as consolidations from 160.45 is extending. Another fall could be seen, but overall outlook will remain bullish as long as 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) holds. Firm break of 160.45 will resume the rise from 152.25 to retest 161.94 high.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.97) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.