Sample Category Title

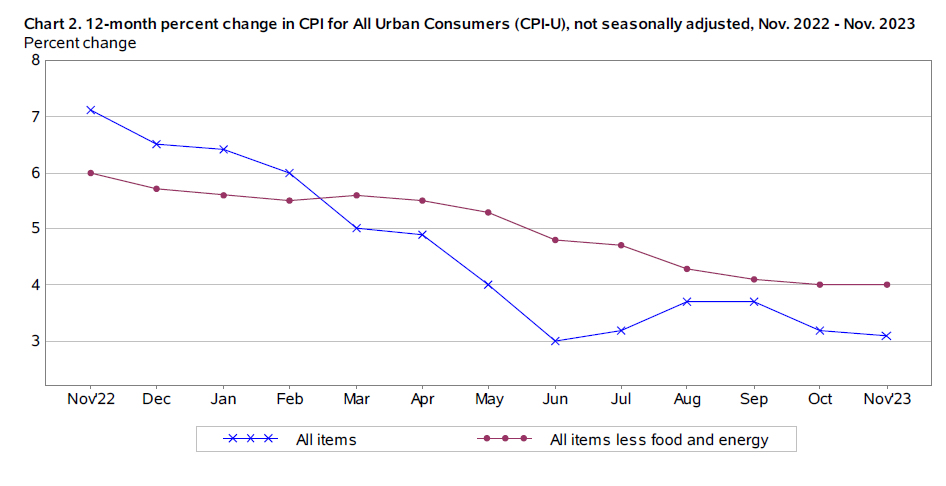

US CPI ticks down to 3.1% in Nov, core CPI unchanged at 4%

The latest CPI data for US in November aligns closely with market expectations. CPI rose 0.1% mom while CPI core ex food and energy) rose 0.3% mom. Energy index down -2.3% mom, food index rose 0.2% mom.

For the 12 months period, CPI slowed from 3.2% yoy to 3.1% yoy. Core CPI was unchanged at 4.0% yoy. Energy index was down -5.4% yoy while food index was up 2.9% yoy.

Is UK Labour Market Cool Enough for BoE?

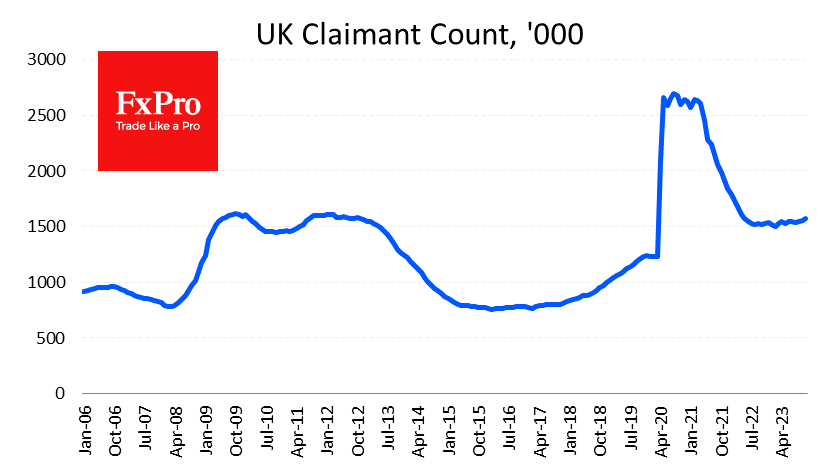

The UK labour market is cooling, showing an increase in claims from claimants. In addition, wage growth is slowing. The data provided further evidence that the UK economy has moved into a new phase of the economic cycle, although the inflation genie remains at large.

In November, the number of people receiving benefits rose by 16K to 1575K – the highest since April 2022. The UK labour market is cutting jobs more actively, a reversal after a plateau between September last year and February this year.

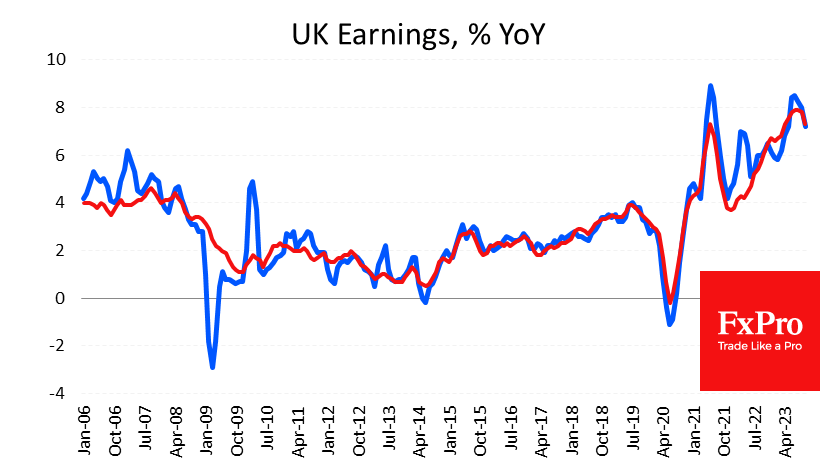

Meanwhile, wages continue to contribute to inflation, adding 7.2% in the August-October period to the same period a year earlier. The rate of wage growth is down 1.3 percentage points from a peak of 8.5% four months ago, although it remains notably above the consumer inflation rate of 4.6% y/y.

On the one hand, the Bank of England has seen slowing inflation and there are growing signs of a cooling labour market, supporting the sentiment that it will reach a plateau and that the next move after a prolonged pause will be lower.

On the other hand, both price and wage growth rates have been held at elevated levels for an extended period (3 years for wages and over two years for inflation), working to raise inflation expectations and making returning to the norm more difficult.

And this divergence creates intrigue ahead of the Bank of England’s looming meeting on Thursday. If the Bank of England acts based on hard data, it should remain in inflation-suppressing mode, warning it is ready to raise rates to bring inflation back on target more quickly.

However, major peers – the ECB and the Fed – are signalling that they are done with hikes and have moved into a ‘wait-and-see’ mode, and the Bank of England may announce the same shift in two days.

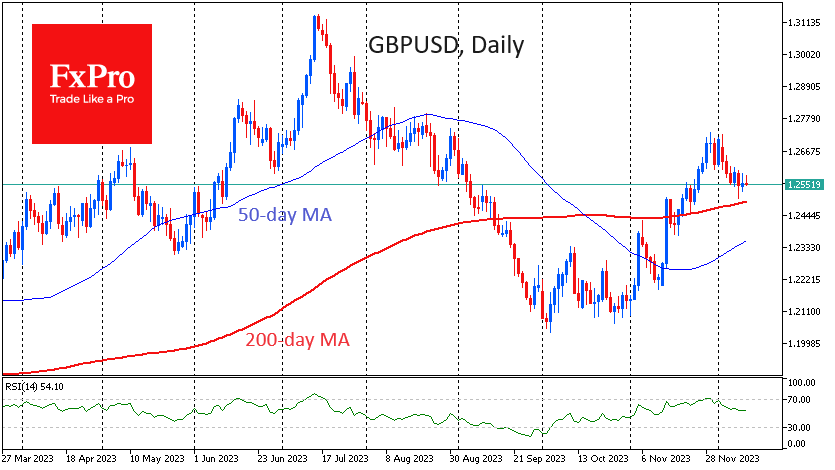

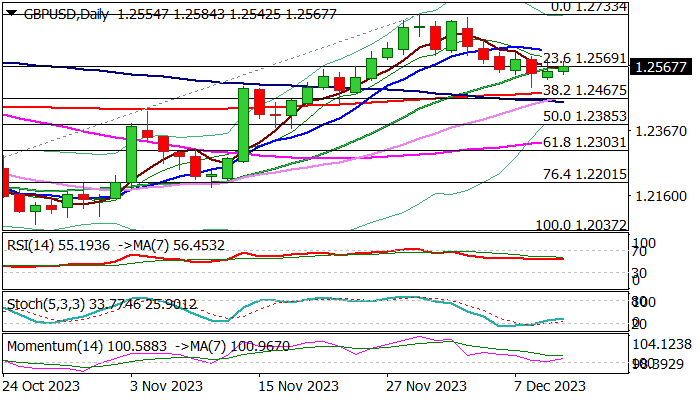

The GBP/USD pair retreated towards 1.25 at the end of last week, approaching its 200-day average from above. This week, the battle for the long-term trend has every chance of intensifying, and a bull or bear victory could signal a lasting signal of further Pound movement. A consolidation under 1.25 opens a quick path to 1.22 or even 1.2060. The ability to hold above due to a strong economy or a hawkish stance from the Central Bank will kick-start a growth momentum with a quick update to 1.27 and the potential to rise above 1.30 before the end of Q1.

USD/JPY, GBP/USD, EUR/USD Analysis: European Currencies in Consolidation Phase, Yen Declining

Better-than-expected US labour market data contributed to a sharp rise in the dollar against the yen and commodity currencies. At the same time, the euro and pound fell slightly, while managing to remain above strategic levels.

USD/JPY

The Japanese currency rose sharply last week as information emerged that the Bank of Japan may soon end its ultra-low rate policy and move on to tightening monetary policy. Investors exited long positions in the US dollar/yen pair, as a result of which the price tested the important range of 142.00-141.00. The latest US employment report for the year was published on Friday, showing an increase in average wages and an increase in new jobs. Indicators above the forecast contributed to the corrective growth of the pair to 146.00. Whether there will be a full resumption of the upward movement in the pair will most likely become clear in the coming trading sessions.

Today at 16:30 GMT+3, we are waiting for data on the consumer price index in the United States; a Federal Reserve meeting is scheduled for tomorrow.

On the daily USD/JPY chart, the price is below the alligator lines; sales may be a priority. With the appropriate foundation, a resistance test at 146.60-148.00 is possible.

GBP/USD

On the GBP/USD chart, the British currency is trading between 1.2500-1.2600. There is not enough news to resume the downward movement, and investors in the pound are not yet in a hurry to open new buy orders.

Today at 10:00 GMT+3, we are waiting for data on average wages and changes in employment in the UK for October. Tomorrow morning the UK GDP figure for the same period will be published.

On the daily timeframe, the pair is testing support at the alligator lines. The price behaviour at 1.2500-1.2450 will be important for the pair’s pricing.

EUR/USD

According to the EUR/USD technical analysis, the single European currency found support just above 1.0700. Sellers of the pair have been trying to break the range of 1.0740-1.0720 for several trading sessions, but so far without success.

Today at 12:00 GMT+3, we are waiting for data on the ZEW economic sentiment index in the eurozone for December. Tomorrow at 13:00 GMT+3, the eurozone industrial production volume for October will be published.

On the daily timeframe, the price is below the alligator lines. With appropriate fundamental data, the pair may test 1.0720-1.0650.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

US CPI Data: Dollar Down As Rate Uncertainty Sustains Volatility

As the clock ticks towards 13:30 GMT, financial markets are bracing for the release of the Consumer Price Index (CPI) data for November, a pivotal metric that provides a snapshot of the current state of the United States economy.

The CPI measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services, making it a crucial indicator for gauging inflationary pressures.

Against the backdrop of the recent dichotomy in US inflation trends, where rates have reduced from alarming figures in 2021 to a current 3.2%, the forthcoming CPI figures are anticipated to shed light on the continued trajectory. This reduction in inflation, although positive for economic stability, has occurred alongside a somewhat unconventional stance by the Federal Reserve.

Traditionally, central banks opt to raise interest rates to curb spending and counteract inflation. However, the US Federal Reserve has maintained a steadfast position in increasing interest rates for over a year, even as inflation trends abate. This seemingly contradictory approach has prompted speculation within financial circles, with analysts debating the motives behind the prolonged interest rate hikes.

The anticipated November CPI data is expected to show a 3.1% year-on-year increase, a slight dip from the 3.2% recorded in October. Additionally, annual Core CPI inflation is forecasted to remain steady at 4% for November. These figures will be closely scrutinised to discern any shifts or continuations in the recent trends.

Interestingly, the foreign exchange market has already signalled early sentiments ahead of the CPI release. The British pound exhibited strength against the US dollar in the early hours of the London session, reaching a value of 1.2580 at FXOpen. This movement is an intriguing indicator of market sentiment and may reflect expectations or reactions to the anticipated CPI figures.

As the financial community awaits the unveiling of the November CPI data, the juxtaposition of decreasing inflation and persistent interest rate hikes by the Federal Reserve adds an element of complexity to the economic narrative.

The numbers released will not only impact currency markets but will also influence broader economic outlooks and potentially shape future policy decisions.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

GBP/USD: Cable Remains Constructive Above 200DMA But More Action at the Upside Needed to Confirm

Cable edged lower on sub-forecast Uk November earnings which adds to talks about possible rate cuts, although the BoE signals that cuts are still not on the table, with hawkish hold expected on Thursday’s policy meeting.

Near-term structure remains positively aligned while the price stays above 200DMA (1.2491), but break above 10DMA (1.2608) is needed to generate positive signal and shift near-term mode from sideways to bullish.

Positive momentum on daily chart supports the notion, as larger uptrend from 1.2037 (Oct 4 low) is still intact.

Caution on loss of lower pivots at 1.2491 (200DMA) and 1.2467 (Fibo 38.2% of 1.2037/1.2733) which would open way for deeper correction.

Res: 1.2608; 1.2652; 1.2678; 1.2733.

Sup: 1.2502; 1.2491; 1.2467; 1.2428.

Japanese Yen Rebounds, US Inflation Looms

- Yen rebounds after two-day slide

- US inflation expected to drop to 3.0%

The Japanese yen has ended a two-day slide, in which it dropped 1.4% against the US dollar. In Tuesday’s European session, USD/JPY is trading at 145.21, down 0.66%.

Yen volatility continues

The yen has been showing sharp swings since last Thursday, when signals from the Bank of Japan of a possible tightening in policy sent the yen soaring over 2% on Thursday. The yen then reversed directions and gave up much of those gains but has bounced back on Tuesday.

The BoJ meets on December 18-19 in what has become a hotly anticipated event due to recent comments from Governor Kazuo Ueda and BoJ Deputy Governor Ryozo Himino. Ueda spoke of “an even more challenging situation” coming up for the BoJ and Himino mused about the consequences if rates were to rise into positive territory. On Monday, a report that Ueda was not referring to possible changes in rate policy sent the yen sharply lower. The takeaway is that the yen is very sensitive to talk about rate tightening and public comments from BoJ policy makers about rate policy ahead of the December meeting could have a strong impact on the yen’s movement.

US inflation expected to decline to 3.0%

The US releases November CPI later today, with a consensus estimate of 3.0% y/y, down from 3.2% in October. Monthly, CPI is expected to remain flat, unchanged from October. Core CPI, which has been running higher than the headline rate, is projected to remain unchanged at 4.0% y/y. Monthly, the core rate is expected to inch higher to 0.3%, up from 0.2% in October.

It’s a virtual certainty that the Fed will hold rates at a range of 5%-5.25% on Wednesday, but today’s inflation release could be a key factor as to what the Fed does in the upcoming months. There is a major disconnect between the markets, which have priced in four rate cuts in 2024, and the Fed, which is insisting that the door remains open to further hikes. A strong inflation report could temper market expectations for rate hikes next year, while a soft inflation release will provide support for the market stance and could force the Fed to reconsider its hawkish position.

USD/JPY Technical

- USD/JPY is putting pressure on support at 145.12. Below, there is support at 144.68

- There is resistance at 145.85 and 146.89

GBP/USD Drifting Ahead of US Inflation

- UK wage growth eases to 7.3%, lower than expected

- US inflation expected to fall to 3.0%

The British pound is drifting on Tuesday. In the European session, GBP/USD is trading at 1.2551, down 0.04%.

UK wage growth falls to 7.3%

Tuesday’s UK employment report was notable for the decline in wage growth. Earnings excluding bonuses rose 7.3% in the three months to October, down from 7.8% in the three months to September. This was lower than the consensus estimate of 7.4%.

Wage growth is an important driver of inflation and the decline is an encouraging sign for the Bank of England. Still, earnings are rising much faster than inflation, which suggests that the BoE won’t be cutting interest rates anytime soon. Inflation has fallen to 4.6%, but this is more than double the Bank’s target of 2%.

The BoE will announce its latest rate decision on Thursday and is widely expected to hold the cash rate at 5.25%. Governor Bailey has warned that rates could remain in restrictive territory for an extended period, but the markets are marching to a dovish tune and have priced in three rate cuts in 2024. Bailey has come out against expectations about rate cuts and we could see the BoE push back against rate cut speculation at the Thursday meeting.

US inflation expected to ease to 3.0%

The US releases November CPI later today, with a consensus estimate of 3.0% y/y, compared to 3.2% in October. Monthly, CPI is expected to remain flat, unchanged from October. Core CPI, which has been running higher than the headline rate, is projected to remain unchanged at 4.0% y/y. Monthly, the core rate is expected to inch higher to 0.3%, up from 0.2% in October.

The Fed is widely expected to hold rates at a range of 5%-5.25% at the Wednesday meeting, but the inflation release could be a key factor as to what the Fed does in the upcoming months. There is a major disconnect between the markets, which have priced in four rate cuts in 2024, and the Fed, which is insisting that the door remains open to further hikes. A strong inflation report could chill market expectations for rate hikes, while a soft inflation release will provide support for the market stance and could force the Fed to reconsider its hawkish position.

GBP/USD Technical

- GBP/USD is putting pressure on resistance at 1.25, followed by 1.2682

- 1.2484 and 1.2369 are the next support levels

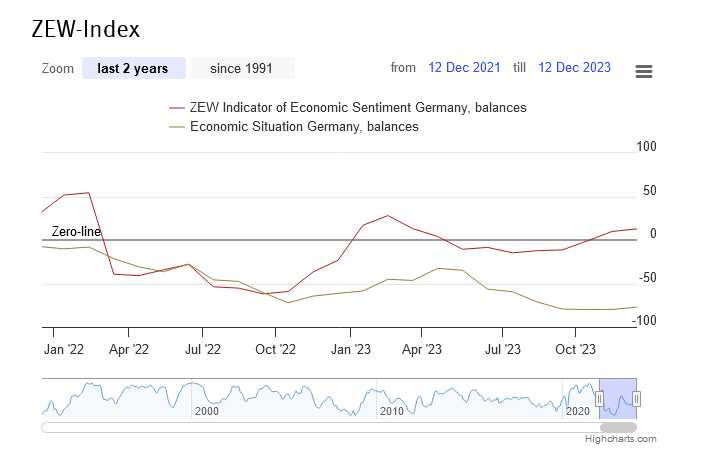

German ZEW rises to 12.8 on increasing expectation of ECB rate cut

German ZEW Economic Sentiment rose slightly from 9.8 to 12.8 in December, above expectation of 8.8. Current Situation Index rose from -79.8 to -77.1, but missed expectation of -75.5.

Eurozone ZEW Economic Sentiment rose sharply from 13.8 to 23.0, well above expectation of 11.2. Current Situation Index, however, fell marginally by -0.9 pts to -62.7.

ZEW President Achim Wambach noted the slight improvement in Germany's economic outlook could be attributed to doubled expectations of interest rate cuts by ECB in the medium term. In particular, significantly more optimistic expectations are observed in the construction industry.

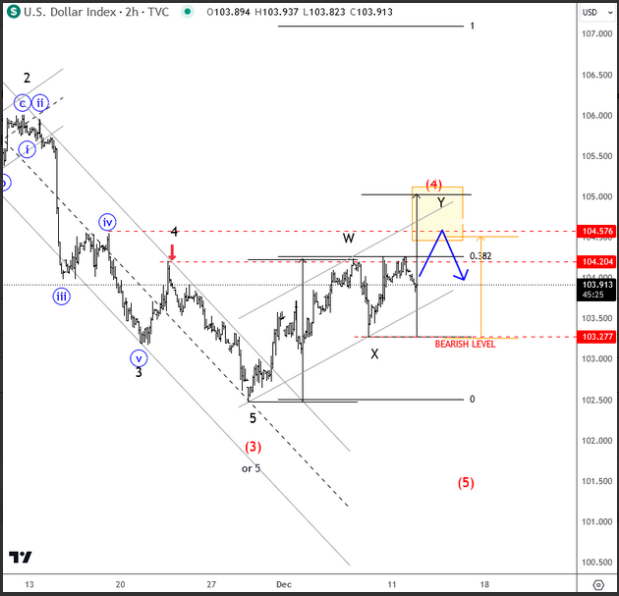

Dollar Index in a Corrective Wave (4) Rally – Technical Resistance at 104.50

It's an important day for the markets with the US CPI release and expectation of 3.1% down from 3.2%, so dollar and us yields can be volatile today on speculations regarding further policy rate decisions from the FED tomorrow. From an Elliott wave perspective, the DXY is still seen in a corrective phase so I think there can be some limited upside, ideally, near 104.50. If USD index comes down, I still think kiwi can do well; its been one of the strongest in recent weeks. If Dollar jumps after the release then watch out for more weakness on EURUSD pair.

Germany 30 Technical: A Potential Minor Corrective Decline Looms

- Short-term RSI momentum indicator has flashed out bullish exhaustion condition after 6 consecutive weekly positive closes.

- At the risk of minor corrective decline sequence below 16,910 key short-term resistance.

- Intermediate supports rest at 16,590 and 16,440.

The Germany 30 Index (a proxy for the DAX futures) has managed to soar towards the 16,780/850 resistance zone as highlighted in our last analysis and printed a fresh all-time high of 16,829 yesterday, 12 December.

Overall, the major uptrend phase from the October 2022 low of 11,795 remains intact with its major resistance zone at 17,780/18,170 (see Fig 1).

Fig 1: Germany 30 long-term secular trend as of 12 Dec 2023 (Source: TradingView, click to enlarge chart)

At risk of minor corrective decline after 6 consecutive weekly positive closes

Fig 2: Germany 30 minor short-term trend as of 12 Dec 2023 (Source: TradingView, click to enlarge chart)

In the shorter term, its medium-term uptrend phase in place since the 27 October 2023 low of 14,586 has reached overstretched conditions as it has recorded six consecutive weekly positive closes.

In addition, current price actions have almost reached the upper boundary of the medium-term ascending channel with a bearish divergence condition being flashed out by its hourly RSI momentum indicator at its overbought region yesterday, 11 December.

These observations suggest an increasing risk of an impending minor corrective decline sequence with 16,910 as a key short-term pivotal resistance and break down below 16,735 near-term support sees the next intermediate supports coming in at 16,590 and 16,440.

However, a clearance above 16,910 negates the bearish tone to expose the next intermediate resistance at 17,100.