Sample Category Title

RBNZ’s Hawkesby highlights inflation pressure from record migration

RBNZ Deputy Governor Christian Hawkesby provided insights into the central bank's current monetary policy and the economic outlook in an interview today. He discussed timing of rate cuts, and impact of rising immigration.

RBNZ's revised forecast does not foresee rate cuts until mid-2025. Explaining the rationale behind the delayed rate cuts, Hawkesby emphasized the need for RBNZ to ensure that inflation expectations are securely re-anchored. He also pointed out that the New Zealand economy had experienced overheating and now requires a period of cooling, marked by a negative output gap.

The interview also highlighted the impact of recent demographic shifts on the The RBNZ had initially perceived rising immigration as a mitigating factor for inflation risk, considering its potential to alleviate labor shortages and reduce wage pressure. However, Hawkesby revealed that the immigration surge has been more significant than anticipated, now contributing to increased demand in the economy.

Hawkesby remarked, "Net migration has peaked at higher levels, so that's news in itself, important news." He further explained that the "demand-side impacts" of this trend are becoming more evident. He added, "The fact you have got to house a bigger population and the impact that that has, particularly on rental inflation and things like that."

New Zealand's population witnessed a substantial increase of 2.7% in the year through September, the largest in over three decades, with net annual immigration reaching a record high of 118,835.

Cliff Notes: Constructive Policy Developments

Key insights from the week that was.

In Australia, the Monthly CPI Indicator fell 0.3% in October, pulling the annual rate of inflation down from 5.6%yr to 4.9%yr; encouragingly for policy, there were no convincing upside surprises within the detail. Indeed, goods prices – which constitute the bulk of the new information at this point in the quarter – reportedly fell 0.1% in the month, with weakness across household contents (–1.6%mth) and certain footwear/garment prices that are measured quarterly. The main driver of the headline result was a decline in services inflation (–0.7%mth); note though, a partial reversal could be seen next month when a larger portion of the services basket is surveyed.

Other consumer data received this week was also on the softer side. Nominal retail sales declined by 0.2% in October after September’s 0.9% gain. Abstracting from inflation and population growth, real per capita retail spending is experiencing a sharp decline in the realm of –4.5%yr to –5.0%yr. Another ‘noisy’ month for dwelling approvals did little to shift the underlying narrative: approvals are holding at weak levels and signs of a sustainable recovery are limited, suggesting that housing availability and affordability will continue to have a significant bearing on prices and rents. For a comprehensive update on the current state of Australia’s housing market and its prospects, see the latest edition of Westpac’s Housing Pulse.

As discussed by Chief Economist Luci Ellis, the data flow since the RBA’s November meeting has not provided any further material upside surprises. But, over the last few weeks, RBA Governor Bullock has devoted much effort to explaining the nuances around Australia’s inflation outlook. The take-away message is that if inflation threatens to take any longer to return to target than currently expected, the RBA Board would respond by tightening policy further. Such risks will certainly be front-of-mind early next year, though we still believe inflation will most likely decelerate through year-end and 2024, removing the need for further increases in the cash rate. Once inflation is convincingly heading towards target, there will be room to begin easing policy, most likely from Q3 2024. Over this period and into the medium-term, labour and capital’s cost and productivity will remain critical for policy.

In the lead-up to the Q3 GDP report, this week the ABS also released two partial indicators of investment.

It was revealed that construction activity lifted by 1.3% in the quarter, spot on Westpac’s forecast. The detail continues to highlight a growing contribution from public works (+4.2%qtr), centred on infrastructure projects; while private construction is tracking a flattening trend at an elevated level (–0.7%qtr). Housing activity continues to experience mixed fortunes, with new dwelling construction still 0.7% below its pre-COVID level while renovation activity is 16.1% higher.

The Q3 CAPEX survey subsequently delivered an upside surprise relative to our expectations, with a 0.6% lift in current activity. The 0.5% gain in aggregate equipment spending was constructive, though the mining and non-mining sector performances were distinct (+5.9% vs. –0.5%). On spending intentions, the fourth estimate for 2023/24 CAPEX plans remained optimistic, up 10% compared to the fourth estimate a year ago. In our view, that implies a 9% rise in nominal CAPEX spending over the financial year. However, momentum is likely to fade as the impetus from tax incentives wanes and the drag from softer demand becomes increasingly evident.

Following the stronger result on equipment spending, we have lifted our Q3 GDP forecast slightly to 0.4% (1.8%yr).

In the US, anecdotes from the 12 Federal Reserve districts were captured in the latest Beige Book. On activity, goods demand was perceived to have weakened, but services held up. Scaling the turn in aggregate momentum, “two [Districts indicated] conditions were flat to slightly down, and six [noted] slight declines in activity” compared to only “four Districts reporting modest growth”. Signs of labour market cooling were also evident with applicants more readily available and firms comfortable letting go of weak performers. Businesses also sought fewer loans while consumer credit remained robust; that said, delinquencies among consumers ticked up according to some banks. In this context, FOMC members' comments through the week indicated optimism that a soft landing was being achieved and that present policy settings were sufficient to rein in inflation.

Adding weight to this view was October’s PCE deflator which came in flat month-on-month, 3%yr. The components were in line with the recent CPI outcome and suggest that inflation’s next leg down will need to come from the shelter component. Personal income and spending both rose 0.2%mth; but over the year, income growth has outpaced spending, highlighting consumer restraint. The pace of real income growth will be critical in determining the degree to which consumption and GDP fall below trend in 2024 and the likely recovery thereafter. Significant job shedding, which the Beige Book hints is a risk, would destabilise income growth and lead to much weaker GDP outcomes. Financial and credit conditions are also critical.

Over in Europe, the flash CPI slowed to 2.4%yr in November from 2.9%yr, the core measure also improving materially to 3.6%yr from 4.2%yr. The deceleration was driven by a surprisingly large slowdown in services inflation from 4.6%yr to 4.0%yr. While on the surface the result supports the case for a near-term pivot to rate cuts, the European Central Bank's Nagel made clear that risks remain “skewed to the upside” and would not rule out further hikes if inflation accelerated once more.

In Asia, China's NBS PMIs were broadly unchanged in November. Manufacturing input prices declined 1.9pts, reflecting the impact of excess capacity in the economy alongside easing global supply pressures. Output prices improved, but the index remained below 50. Further downward pressure on prices will support global goods deflation; it is important to recognise that this trend stems as much from increased capacity, productivity and efficiency as it does soft demand. The non-manufacturing PMI meanwhile held just above 50. Helpfully, employment and new orders look to be stabilising, albeit at a weak level.

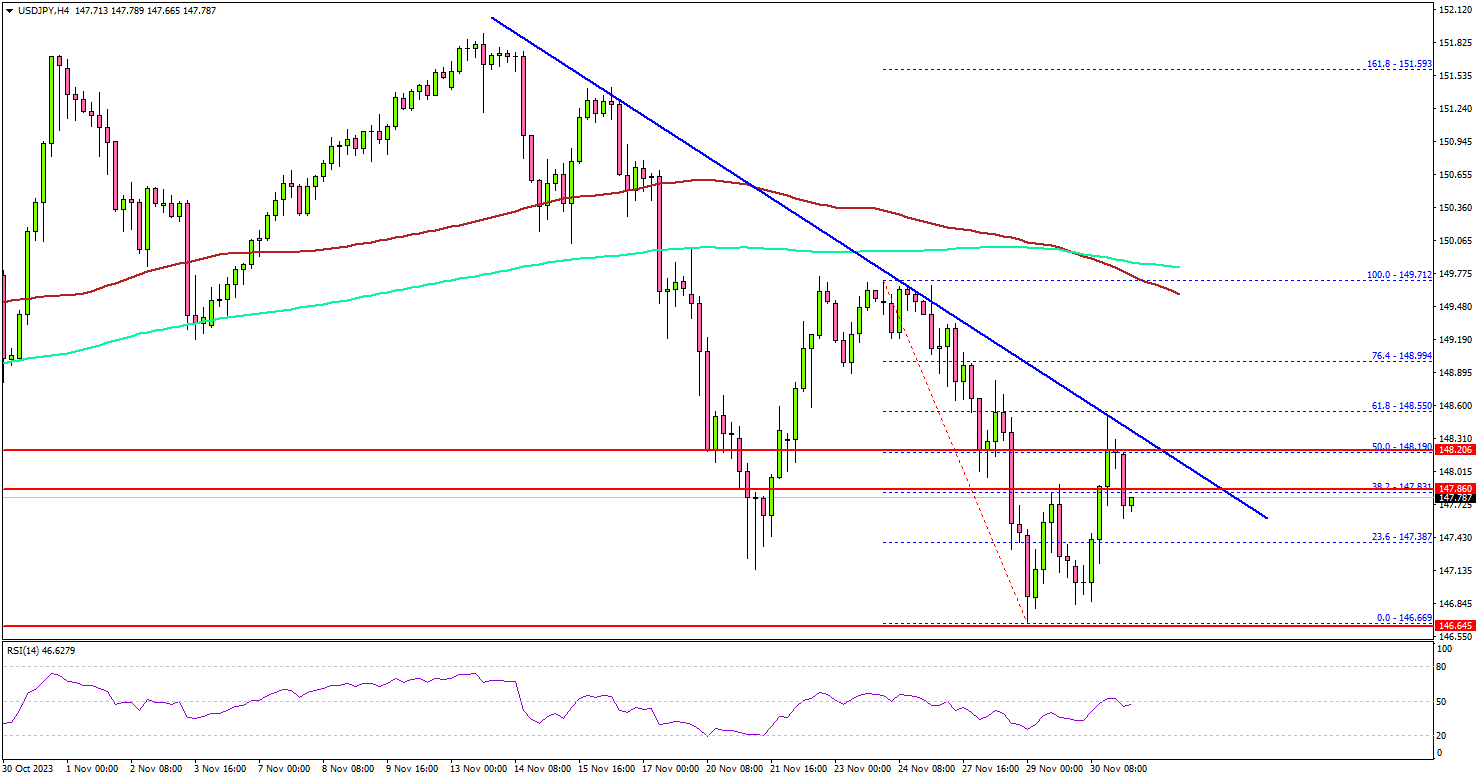

USD/JPY Faces Resistance While Oil Prices Recover

Key Highlights

- USD/JPY is facing many hurdles near 148.00.

- A major bearish trend line is forming with resistance near 148.10 on the 4-hour chart.

- Gold prices jumped toward $2,050 before it faced resistance.

- Crude oil prices are recovering losses and trading above $75.50.

USD/JPY Technical Analysis

The US Dollar saw a major decline from well above 149.50 against the Japanese Yen. USD/JPY declined below the 148.50 and 148.00 support levels to enter a bearish zone.

Looking at the 4-hour chart, the pair settled below the 148.00 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

It even spiked below the 147.00 level. A low was formed near 146.6 before the pair started an upside correction. There was a minor increase above the 147.20 level. The pair surpassed the 23.6% Fib retracement level of the downward move from the 149.71 swing high to the 146.66 low.

On the upside, immediate resistance is near the 148.00 level. The next key resistance is near the 148.20 level or the trend line. It coincides with the 50% Fib retracement level of the downward move from the 149.71 swing high to the 146.66 low.

A close above the 148.20 zone could open the doors for more upsides. The next stop for the bulls might be 148.80. If not, USD/JPY might resume its decline. Immediate support is near the 147.00 level.

The next key support sits at 146.65, below which the pair could test the 145.00 pivot level in the near term. Any more losses might call for a move toward 143.20.

Looking at Gold, there was a strong increase above the $2,025 resistance but the bears remained active near $2,050.

Economic Releases

- Germany Manufacturing PMI for Nov 2023 - Forecast 42.3, versus 42.3 previous.

- Euro Zone Manufacturing PMI for Nov 2023 – Forecast 43.8, versus 43.8 previous.

- UK Manufacturing PMI for Nov 2023 – Forecast 46.6, versus 46.7 previous.

- US Manufacturing PMI for Nov 2023 – Forecast 49.4, versus 49.4 previous.

- US ISM Manufacturing PMI for Nov 2023 – Forecast 47.6, versus 46.7 previous.

Top Three Trade Ideas for December 2023

Hey folks, it’s a wrap to yet another month in the 2023 calendar, and I’m guessing you know what that means - time for another episode in the “What To Trade” series. For December, I will be mapping out trade more cautiously as the market volatility often drops massively, causing the markets to slow down drastically. Having said that, these are my top three trade ideas for December, for the time being.

USDJPY - D1 Timeframe

USDJPY on the Daily timeframe can be seen reacting from the confluence of the 100-Day moving average and the drop-base-rally demand zone. This confluence in conjunction with the bullish array of the moving averages indicates a likely bullish outcome - which is my sentiment in this case.

Analyst’s Expectations:

- Direction: Bullish

- Target: 150.153

- Invalidation: 146.482

AUDJPY - D1 Timeframe

AUDJPY on the daily timeframe has already been rejected from the supply zone for a second time, this time also breaking minor structure on the H4 timeframe. In this case, my initial target is set at the intersection of the demand zone, 50-period moving average, and the trendline support.

Analyst’s Expectations:

- Direction: Bearish

- Target: 96.500

- Invalidation: 98.344

NZDJPY - D1 Timeframe

NZDJPY is currently trading within the supply zone on the weekly timeframe, and has already been rejected once from the zone. At the moment, there is also a resistance trendline intersecting the weekly supply, increasing the likelihood of a bearish momentum from the current supply zone.

Analyst’s Expectations:

- Direction: Bearish

- Target: 87.922

- Invalidation: 92.011

CONCLUSION

The trading of CFDs comes at a risk. To succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

Is Bitcoin Set to Drop?

Bitcoin's price remains stagnant despite the Fed's slightly less hawkish tone. In contrast, Bitcoin has outperformed other assets, doubling in price from $16K to nearly $38K this year. Improved fundamentals, including the resolution of Binance concerns and FTX's token performance, boost sentiment. Traders are eagerly awaiting the approval of BlackRock's ETF, a potential catalyst for Bitcoin surpassing $50,000 by year-end. Technically, Bitcoin is in an upward channel, suggesting bullish momentum unless it violates this pattern.

BTCUSD - D1 Timeframe (BEFORE & NOW)

In my article dated 10th of October, I detailed my reasons for expecting a decline in BTC prices, followed by a surge from a technical point-of-view. The chart above shows the outcome of that analysis, which confirms to a large extent the degree of accuracy in such articles as this. So, follow me closely as I expound on my expectations for BTCUSD in the coming days.

BTCUSD - W1 Timeframe

Currently, on the 4-hour timeframe, BTCUSD is trading within a bullish channel, and seems poised to break out of the trendline resistance. This already signifies the likelihood of a bullish outcome. From a larger perspective, we also see that a head-and-shoulder pattern appears to be in formation on the weekly timeframe chart, as attached. This being the case means that we may get to see BTCUSD prices soar all the way to the $45,000 mark. Do note, however, that this is my personal opinion on the matter and not financial advice.

Analyst’s Expectations:

- Direction: Bullish

- Target: $45,000

- Invalidation: $36,280

CONCLUSION

Trading CFDs comes at a risk. To succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

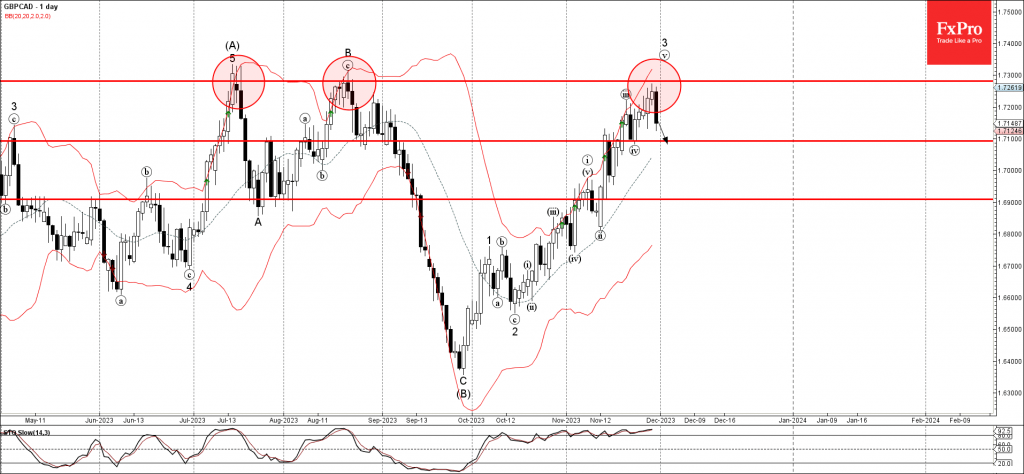

GBPCAD Wave Analysis

- GBPCAD reversed from resistance level 1.7280

- Likely to fall to support level 1.7100

GBPCAD currency pair recently reversed down from the long-term resistance level 1.7280 (strengthened by the upper daily Bollinger Band), which has been reversing the pair from the start of July, as can be seen below.

The pair is currently forming the daily Evening Star – strong sell signal for this currency pair.

Given the strength of the resistance level 1.7280, strongly overbought daily Stochastic, GBPCAD currency pair can be expected to fall further to the next support level 1.7100.

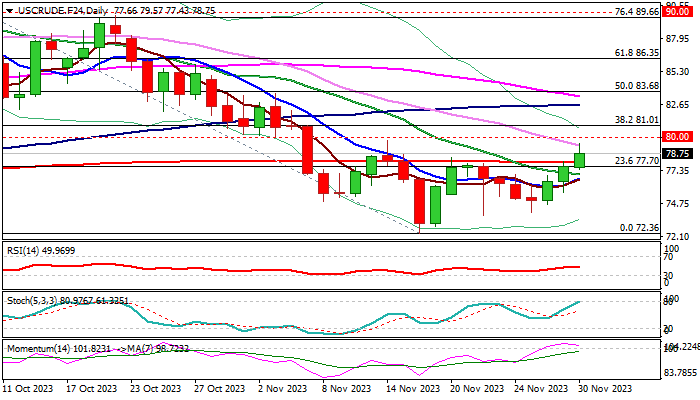

WTI Oil: Oil Price Extends Advance as OPEC+ Rolls Over Production Cuts

WTI oil price rose above $79 for the first time in two weeks on Thursday, as fresh bullish acceleration extends into third consecutive day.

The OPEC+ decided to extend its supply cuts in 2024, as the cartel met today, after meeting scheduled for Nov 26 was postponed, adding support to oil price.

The top world oil producers agreed preliminary cut of over 1 million barrels per day, including Saudi Arabia extending the voluntary cut since July, with smaller contribution from other members.

The OPEC+ members also discussed potential bigger cuts in 2024, with extension to 2 million barrels per day being on the table.

Tighter oil market will offer fresh support to oil and continue to underpin the price in coming months.

Today’s acceleration broke above significant barrier at $78.04 (200DMA) and cracked daily Kijun-sen ($79.12) increasing pressure on psychological $80 resistance.

Expect initial bullish signal on close above 200DMA, which reverted to solid support, with extension through $80 and $81 pivots (psychological / Fibo 38.2% of $95.00/$72.36) to further strengthen bullish structure and open way for further advance.

Improving daily technical studies add to positive near-term outlook, though bulls may face headwinds at $80 zone and enter consolidation before resuming.

Bullish bias expected to remain intact above 200DMA, while fall below converging 20/10DMA’s ($77.07/$76.78) would neutralize bulls.

Res: 79.57; 80.00; 81.00; 81.52

Sup: 78.07; 77.70; 76.78; 74.04

Sunset Market Commentary

Markets:

At the start of trading this morning, core (US) bonds showed tentative signs of taking a breather after their recent rally. However, French data again perfectly fit the recent bond friendly market momentum. French Q3 GDP growth was downwardly revised from +0.1% to -0.1%. October consumer spending fell off a cliff (-0.9% M/M) and, in line with evidence from other EMU member states, French HICP inflation printed well below expectations at -0.3% M/M and 3.8% Y/Y (from 4.5% and vs 4.1% expected). Yields across the Bund- and EMU swap curves, touched new correction low levels, with the short end taking the lead. Later, the flash estimate of EMU headline inflation printed at -0.5% M/M and 2.4% Y/Y (from 2.9%). Core inflation also eased substantially from 4.2% Y/Y to 3.6% Y/Y. This time there was no further market reaction. Too early to really call it a buy-the-rumour, sell-the fact reaction yet. Even so, especially long term yields tried to leave recent lows. German yields are changing between -1 bp (2-y) and +4 bps (30-y). In the US, the focus was on the October US income and spending data, and more in particular on the price deflators. Both spending & income (0.2% M/M) and the deflators (headline 3.0% vs 3.1% expected, core 3.5% from 3.7%) were very close to expectations. US jobless claims also brought no market moving news (218k from 211k, exactly as expected). US bonds are taking a breather from their recent rally with the 2-y rebounding 5.5 bps. The 10-y adds 9 bps (4.34%). The focus now turns the US manufacturing ISM, to be released tomorrow. The market expects a slight improvement (47.8) but still in contraction territory. Interesting to see how bond markets react in case of additional signs of a slowdown in activity. Despite some ‘hesitation’ over the previous days, especially in US indices, equities still feel supported by the hope for substantial monetary easing next year. The EuroStoxx 50 adds 0.30%, nearing the 4400 mark with the 2023 top at 4491 also coming on the radar. US indices open mixed (Dow +0.5%, Nasdaq -0.3%).

On FX markets, EUR/USD in the first place took a hit after the big miss in French data. At the same time, the dollar gradually also showed tentative signs of bottoming. At 1.09, the first attempt of the ) cross rate to regain the 1.10 probably is rejected for now. USD/JPY also tries to leave the recent lows behind (148.35). EUR/GBP in line with the broader early morning euro sell-off temporary dropped to the 0.862 area, but the move was fully reversed later (currently 0.8645). It’s a bit telling that sterling in the current environment fails to profit from broader euro weakness.

News & Views:

Saudi Arabia is rallying support behind a proposal of additional OPEC+ production supply cuts of 1 million barrels a day (1% of global supply) in an effort to prevent the oil market returning to a surplus next year. The Kingdom would simultaneously extend its own voluntary cutback of the same size which has been in place since July. OPEC+ has its ministerial meeting via online sessions after the physical event was delayed last week because of ongoing negotiations. One of the remaining stumbling blocks in negotiations are production for African members like Angola and Nigeria. Both countries have underproduced in recent years because of underinvestment and try to revive their output. Brent crude prices rallied from $83/b to $84.5/b on the news.

Canadian GDP unexpectedly shrank in the third quarter of the year (-0.3% Q/Q). An upward revision to the Q2 figure to 0.3% Q/Q implies that the technical recession is nevertheless avoided for now. Details showed a decrease in international exports (-1.3% Q/Q vs 0.2% decline in imports) and slower inventory accumulation being partially offset by increases in government spending and housing investment. Final domestic demand increased 0.3% Q/Q, following a similar increase in the second quarter. Business investment in non-residential structures fell by 2% Q/Q. Separate data showed compensation of employees rising by 1.3% on a nominal basis in Q3 of 2023. Canadian markets didn’t respond to the release with USD/CAD changing hands around 1.36.

Gold Breaks To New Highs. What Is Expected In December?

Gold prices, reaching the highest since May 5, are consolidating as traders await the US PCE Price Index, a key inflation indicator. The upcoming data could impact the Fed's policy, influencing the demand for the US Dollar and providing direction for gold. The Greenback sees some repositioning, recovering modestly ahead of the data risk. A positive tone in US equity futures acts as a headwind for gold, but the growing belief that the Fed might cut rates in March 2024 could limit significant dollar appreciation. Amid China's economic concerns, gold finds support in this nuanced market scenario.

XAUUSD - D1 Timeframe

As seen on the attached chart which shows the daily timeframe of XAUUSD (Gold), price seems to have created a head-and-shoulders pattern, with an initial rejection from the 88% of the Fibonacci retracement level. Based on this, I expect to see a pause in the bullish rally, at least, until price reaches the 50% Fibonacci level.

XAUUSD - H4 Timeframe

On the 4-Hour timeframe, a more cautious approach would be to wait for the break and retest of the trendline shown in the chart above, and then the bearish trend can be considered to be in motion.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1950.77

- Invalidation: 2053.42

CONCLUSION

The trading of CFDs comes at a risk. To succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.