Sample Category Title

Today OPEC+ May Announce New Oil Production Cuts

According to WSJ, the reduction could be 1 million barrels per day. Saudi Arabia is in favour of cuts, but the idea causes disagreements among other members of the organisation.

In anticipation of news about the OPEC+ decision, the price of oil is rising - this indicates that market participants assess the possibility of new production cuts as quite real, even if we are not talking about 1 million barrels per day. The price is approaching its maximum for November.

The Brent oil price chart shows that:

→ the level of 80 dollars per barrel acts as support. In the twenties, the price dropped to the level more than once, but each time the bulls found the strength to recover;

→ rising lows A-B-C indicate the predominance of demand around the mentioned psychological level;

→ the price has been within the descending channel (shown in red) for more than a month, but is trying to consolidate above the median line. This is another sign of the bulls' persistence.

However, it should be recognized that the current bullish sentiment could easily change if OPEC+ fails to reach a consensus on significant restrictions on oil production aimed at supporting commodity prices.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

BTC/USD Analysis: New High for the Year Shows Bulls Are Indecisive

During November, the price of bitcoin increased by approximately 10% in anticipation of the launch of a bitcoin ETF. But the positive sentiment of crypto investors is seriously overshadowed by news regarding Binance:

→ Changpeng Zhao resigned as head of Binance.US, pleading guilty to money laundering charges. He also agreed to pay $50 million in a lawsuit from the US Department of Justice, and his company will have to pay $4.3 billion. This fine to Binance was one of the largest in the history of punishment of corporations. In addition, Zhao faces up to 10 years in prison. The judges banned him from leaving the United States until the proceedings are completed.

→ Cristiano Ronaldo was sued for $1 billion for advertising Binance. This was done by people who claim they suffered losses by buying unregistered securities that the sports star was promoting.

Meanwhile, the BTC/USD chart shows signs that demand forces are losing confidence, although the price is moving within an ascending channel (shown in blue).

Notice that the November 29 top was only a few dollars higher than the previous November 24 top. This short-term excess suggests that there is no sustainable predominance of demand over supply in the market around the level of $38 thousand per Bitcoin, and the top on November 29 is nothing more than a bull trap.

In such conditions, perhaps more attention should be paid to the idea of testing the lower boundary of the current channel.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

EUR/USD Drops Ahead of Eurozone CPI

- Eurozone inflation expected to decline to 2.7%

- ECB’s Lagarde delivers remarks later today

The euro is in negative territory in Thursday trade. In the European session, EUR/USD is trading at 1.0940, down 0.27%.

Eurozone inflation expected to ease to 2.7%

Germany’s inflation rate declined sharply in November and the eurozone is up next, with the November inflation report later today. German inflation dropped to 3.2% y/y in November, down from 3.8% in October and below expectations. This was the lowest inflation rate since June 2021 and was driven by lower food and energy inflation.

Will eurozone inflation follow suit? The markets are expecting a modest decline for November. Headline inflation is expected to fall to 2.7%, down from 2.9% in October, and the core is expected to ease to 3.9%, down from 4.2% in October. If inflation falls modestly as expected, it is unlikely to cause the ECB to reconsider its rate policy. The markets have priced in a rate cut in May 2024 and a softer-than-expected print would likely result in the odds of a rate cut being brought forward.

The ECB has signalled a ‘higher for longer policy’, as have the Federal Reserve and other major central banks. Even though inflation has been dropping, it remains considerably higher than the ECB’s 2% target and the central bank hasn’t given any indications of a rate cut. Investors will be looking for hints about rate policy from ECB President Christine Lagarde, who will speak today at an ECB forum in Frankfurt after the eurozone inflation release.

In the US, second-estimate GDP for the third quarter was revised to 5.2%, up from the initial estimate of 4.9%. The strong reading should ease fears of a recession but also provides the Fed with little reason to trim rates while inflation remains well above the 2% target. The Fed has signalled a ‘higher for longer’ stance on rates but the markets are more dovish and have priced in a rate hike in March 2024 at 45%, according to the CME’s FedWatch tool.

EUR/USD Technical

- EUR/USD is putting pressure on support at 1.0920. Below, there is support at 1.0873

- 1.0986 and 1.1033 are the next resistance lines

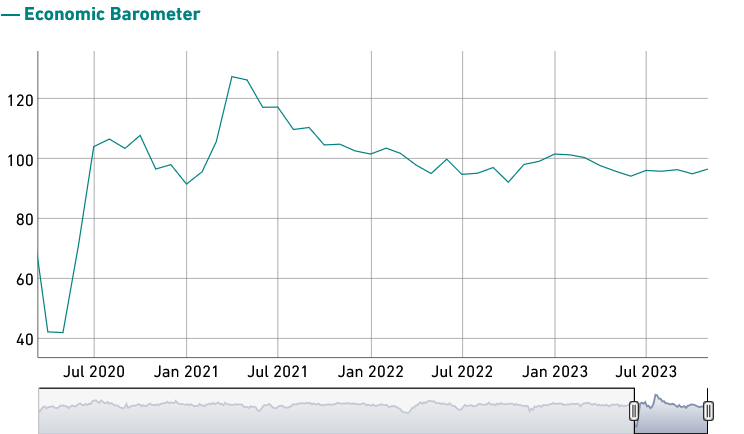

Swiss KOF rose to 96.7, moderate economic outlook

Swiss KOF Economic Barometer, a key indicator for forecasting the economy's direction, has shown a slight improvement in November, rising from 95.1 to 96.7. This rise slightly exceeded market expectations, which were set at 96.2.

According to KOF Swiss Economic Institute, since mid-2023, the barometer has stabilized, though it remains at a level below the historical average. This stabilization indicates moderate outlook for the Swiss economy in the near future.

The increase in the KOF Barometer can primarily be attributed to positive developments in manufacturing sector and other services sector.

However, not all sectors are signaling positive trends. Indicators for hospitality industry and finance and insurance sector are showing slightly negative signals.

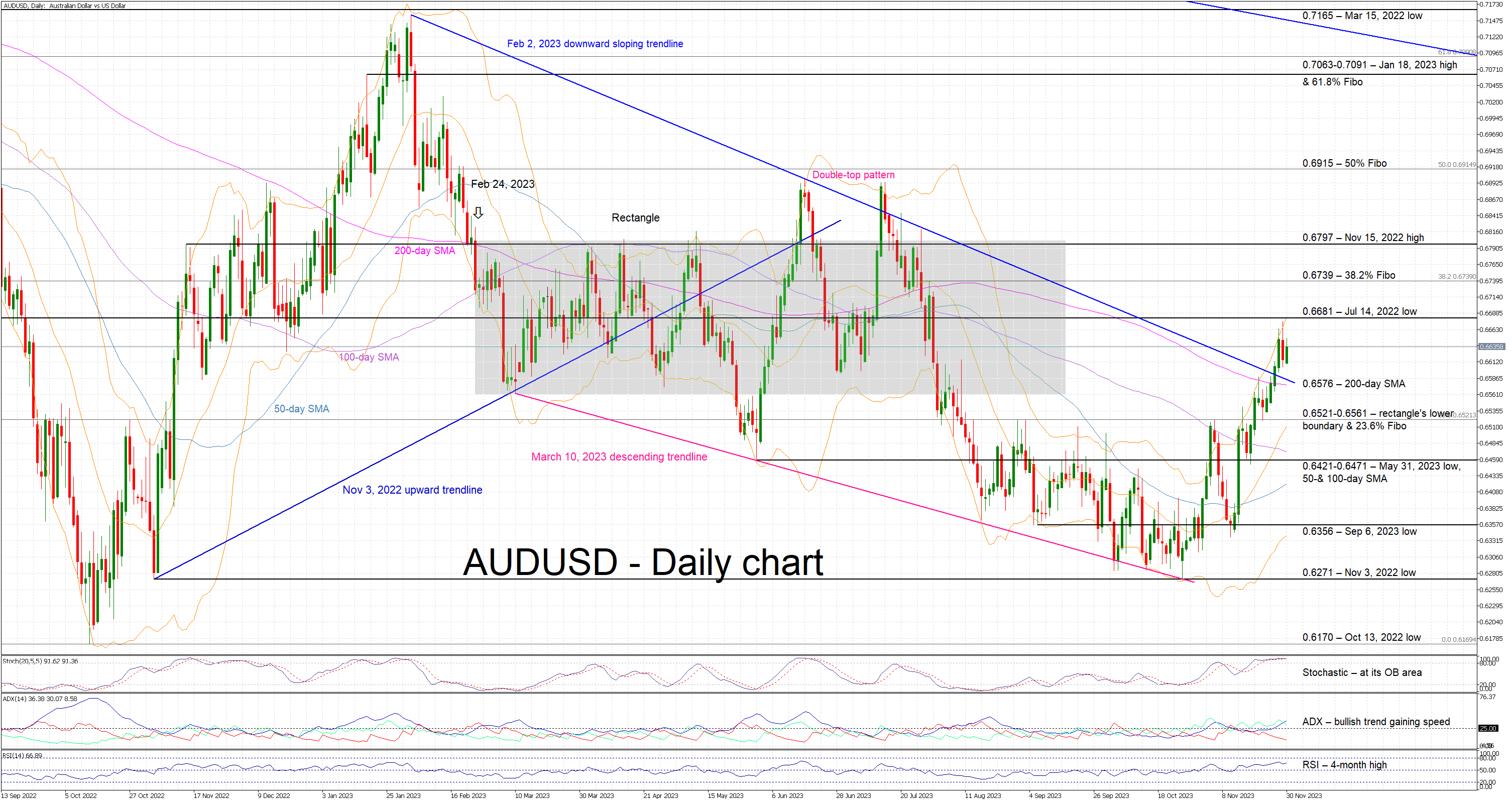

AUDUSD Bulls React to Yesterday’s Red Candle

- AUDUSD in the green again today, close to its 4-month high

- Aggressive move higher from the October lows

- Momentum indicators potentially ready to signal a reversal

AUDUSD is trying to register a strong green candle as it continues to trade above the key February 2, 2023 descending trendline. It has been an aggressive rally from the 2023 low of 0.6269 recorded in October, with AUDUSD currently hovering close to its 4-month high. All eyes are now on the momentum indicators for any clues on the continuation of the current upleg.

In more detail, the Average Directional Movement Index (ADX) is trading above its 25-threshold, thus signaling a decent bullish trend in the market. Similarly, the RSI continues to hover comfortably above its 50-midpoint, close to a 4-month high, but it appears unable to make a higher high. More interestingly, the stochastic oscillator is stuck at the upper end of its overbought area. While it can stay there for a while, the current movement could be seen as an early reversal signal.

Should the bulls remain confident, they could try to stage a move towards the July 14, 2022 low at 0.6681. Higher, the 38.2% Fibonacci retracement level of the April 5, 2022 – October 13, 2022 downtrend and the November 15, 2022 high at 0.6739 and 0.6797 respectively will probably test the bulls’ determination. If successful, the next key resistance area appears to be at the 50% Fibonacci retracement level of 0.6915.

On the flip side, the bears are probably keen to put a stop at the current bullish move. They could try to push AUDUSD back below the February 2, 2023 downward sloping trendline and the 200-day simple moving average (SMA) at 0.6576. They could then test the support set by the rectangle’s lower boundary and the 23.6% Fibonacci retracement at the 0.6521-0.6561 range. If successful, they could stage a move towards the 0.6421-0.6471 range.

To sum up, AUDUSD bulls could have the chance for a higher high if they manage to withstand the expected bearish pressure and keep AUDUSD above the February 2, 2023 trendline.

Interesting to See Whether EUR/USD Can Regain 1.10 Barrier

Markets

Yesterday, first November EMU inflation data from Germany and Spain come out in line with market momentum. Spain HICP inflation declined 0.6% M/M easing the Y/Y measure from 3.5% to 3.2% (3.7% expected). Core inflation also declined substantially (4.5% from 5.2%). Similar story in Germany as HICP inflation printed at -0.7% M/M and 2.3% Y/Y (from 3.0%). Technical factors and ‘erratic’ base effects due to support measures implemented last year create some noise and might cause countermoves in coming months. Whatever, softer than expected is softer than expected. German yields again declined between 8.2 bps (2-y) and 4.6 bps (30-y). Admittedly, major part of the move already occurred before the publication of the data. US markets more or less copied the trend in Europe, easing between 8.9 bps (2-y) and 6.5 bps (10-y). Comments from Fed Waller on Tuesday that the Fed is well positioned to slow the economy in a way that also might bring inflation back to 2.0% supported the case for bond bulls. Waller’s wait-and-see assessment yesterday was joined by Fed Mester and Barkin even as they didn’t formally rule out a further rate hike. US equities tried the extend the interest rate-driven rally, but gains could not be sustained. US indices closed little changed (S&P -0.09%). Soft EMU inflation data annex lower EMU yields prevented EUR/USD to hold north of 1.10 (close 1.097). At the same time, broader USD selling also eased (DXY close 102.76 from opening levels near 102.58). Sterling again outperformed the euro, maybe partially on recent comments from BoE members warning markets on early rate cut bets (EUR/GBP close 0.8640).

Asian equity markets this morning mostly show modest gains. China November PMI’s again disappointed (composite 50.4 from 50.7) raising market hope for additional policy support. US yields are ‘rebounding’ 1-2,5 bps across the curve, but don’t help the dollar (DXY 102.75, EUR/USD 1.0980, USD/JPY 146.95). Later today, the Flash EMU November CPI will be published. After yesterday’s releases, the risk obviously is for a below consensus (-0.2% M/M and 3.9% Y/Y headline, 2.7% Y/Y core) outcome. Interesting to see whether there is still additional reaction on interest rate markets or whether some consolidation can start going into the December 14 ECB policy meeting. In the US the October PCE deflators (core expected 0.2% M/M and 3.5%Y/Y), but also jobless claims and Chicago PMI will be released. US markets might still be more sensitive to weaker data. This especially might be the case for the dollar. Interesting to see whether EUR/USD can regain the 1.10 barrier. USD/JPY also looks vulnerable sub 147.

News & Views

The Bank of Korea unanimously decided to keep its policy rate unchanged at the 15-yr high reached in January (3.5%). The number of board member seeing a possible need to lift rates further, dropped from six to four. A slight alteration to the policy statement creates more leeway for the central bank going forward. The commitment to keep policy rates restrictive for “a considerable time” made way for guidance that it would remain restrictive for a sufficiently long period of time to ensure inflation converged to its goal. The BoK nevertheless raised this year’s inflation forecast slightly to 3.6% and from 2.4% to 2.6% for next year following an unexpected inflation acceleration in October. Governor Rhee still indicated that inflation will converge to the 2% target by end 2024 or early 2025. One board member contemplating last month the possibility of a rate cut if geopolitics affected the economy, no longer holds that view. The Korean central bank kept this year’s growth forecast unchanged at 1.4% while slightly downgrading the one for next year to 2.1%. The Korean won this morning holds near the strongest level against a weak USD since early August (USD/KRW 1291 area).

The Bank of Mexico released its latest quarterly inflation report. They expect a return to the 3% midpoint of the inflation target (+-1 ppt tolerance band) by early 2025, but inflation can prove slightly more sticky in the short term (core CPI: 5.3% from 5.1% for Q4 2023 and 3.3% from 3.1% for Q4 2024). Banxico also raised GDP forecast from 3% to 3.3% for this year and from 2.1% to 3% in 2024. It sees 2025 growth at 1.5%. Governor Rodriguez Ceja at the press conference afterwards she saw a possibility for the start of discussions on a rate cut at the meetings next year. The central bank still has a 11.25% policy rate in place since May, making real rates very positive. In November, they prepared a pivot by changing forward guidance from stable rates for an extended period to stable rates for some time. MXN loses ground this morning with USD/MXN rising from 17.14 to 17.28...

Focus Turns to EA and US Inflation

Market movers today

Today we get the HICP inflation numbers for the euro area. After yesterday's lower-than-expected Spanish and German prints, consensus expects the euro area figure at 2.5% y/y.

At 14:30 FED's preferred inflation gauge is released. Consensus expects the PCE core to slow down to 0.2% m/m SA, mirroring a similar decline in the CPI measure released earlier.

OPEC+ convenes on Thursday after their last scheduled meeting was postponed.

The 60 second overview

Heavy data releases from the euro area showed declining inflation, below consensus estimates, and mixed consumer confidence. European rates markets reacted strongly to the inflation release sending yields lower from the front end as additional rate cuts were priced. 10y German yields declined to multi-month lows of 2.42%. The German and Spanish inflation print came in below expectations at -0.4% m/m in November (cons.: -0.1%, prior: 0.0%), and -0.4% m/m (cons.: 0.1%, prior: 0.3%), respectively. This combined with slowing inflation in Belgium and Ireland means that today's euro area flash inflation print is pointing to a 2.5% release. The EU Commission confidence indicator was mixed across sectors with improved confidence in the service sector and lower confidence in the industry. Yet, over the past months, confidence in the industry has stabilized from the large downward trend during the previous years in a signal of activity bottoming out like we have seen in the PMIs.

In the US, we had positive economic data, including an upwardly revised Q3 GDP growth of 5.2% annualised rate, which has strengthened the broad USD, yet the Beige Book has signalled a pre-November 18 economic slowdown.

Overnight, the Chinese PMI pointing to a slowdown in the manufacturing sector with a 49.4 print, while services pointed to a largely stagnating sector of 50.2, both indicators below consensus.

Yesterday, we published a piece on the EU fiscal rules and what to expect from the negotiations on a new set of rules. Currently there is no agreement on the new fiscal rules and the clock is ticking, as the old rules will otherwise come into force again from 1 January 2024. We expect that the EU Member States will most likely not sign a final legal set of rules before year-end, however, we expect that they will agree on a "landing zone" for the new rules at the ECOFIN meeting on 8 December. We expect that the "landing zone" will reinstate the old 3% deficit and 60% debt targets, but with greater flexibility to adapt country specific fiscal adjustment paths. The fiscal stance in the euro area becomes tighter in the coming years as sustainable public finances get renewed focus. See more in Euro Area Research: New fiscal rules in the EU - aligning theory and practice?, 29 November 2023.

Equities: Equities were mixed on Wednesday, with US a tad lower and Europe half a percent higher. The European outperformance partly underscored by benign inflation numbers, but also catchup from the prior session. Interesting that the fall in yields have not chalked up a new wave of equity risk taking. AAII bull/bear spread is back at July highs, so positioning is probably a piece to the puzzle. Cyclicals beat defensives though, with an odd mix of both banks and real estate among best sectors. US futures and Asian markets are a little higher this morning.

FI: The inflation releases from Spain and Germany sent yields lower through yesterday's trading session with 10y Bunds ending the day 6bp at multi-month lows of 2.42%. Intra-euro area spreads saw little change. Curves steepened from the front end as the markets added to rate cut expectations with adding another 10bp yesterday to the 2024 pricing. Compared to Monday' close, markets have added 22bp in total with a total of 111bp of cuts priced in through 2024.

FX: EUR/USD sustained consolidation slightly below the 1.10 mark amid a prevailing strengthening of the USD. USD/JPY has exhibited a downward trajectory and currently hovers just above 147. Meanwhile, EUR/GBP experienced a further decline, settling within the mid-0.86 range. EUR/SEK dipped below 11.40, and EUR/NOK is positioned around 11.70.

Credit: Yesterday, credit markets were again positive with iTraxx Main 1.5bp tighter to 66.8bp while Xover tightened by 10.2bp to 367.1bp. In addition, the primary markets continue to be wide open with several financial and corporate issuers active with deals across the Nordic area and five Eurobond transactions. The current market sentiment is showing constructive credit conditions most types of credit transactions, however some seasonal slowdown should soon be expected to influence the current high activity.

Nordic macro

Riksbank Governor Bunge speaks about monetary policy and the latest decision. Recall the silent period has not yet passed, hence, she cannot say speak for herself, just on behalf of the Board's common decision.

Nothing Says ‘Let’s Save the Planet’ Like a Summit Led by a Big Oil CEO

The rally in US bonds continued at full speed yesterday and bonds are set to record their best month since the GFC this November. The US 2-year yield tumbled to almost 4.60% yesterday from nearly 5% at the start of the week. While the 10-year yield rebounded after hitting 4.25%. That makes an almost 40bp fall for the US 2-year yield and a 25bp fall for the US 10-year yield in three days only.

A faster fall in short-term yields means that that the market is busy pricing rate cuts (which we know it does), yet the amplitude of the move is relatively big.

Released yesterday, the US Q3 GDP was revised to an eye-popping 5.2% from an already high 4.9% printed earlier. The consumer spending component was revised slightly lower, and the price pressures seemed softer than previously announced. But we could easily say that the US economy’s Q3 performance made China jealous!

If you dig deeper: even though yesterday’s above-5% GDP print would’ve been an excellent trigger for a rebound in the US bond yields and the dollar – on belief that the US economy is strong enough to allow the Federal Reserve (Fed) to keep rates ‘high for long’ - it also surfaced the worries (or hope) that this incredible performance can’t last!

And guess what? The Atlanta Fed’s GDP Now forecast – which beautifully predicted last month’s above-average performance – is now pointing at a sharp decline in the US GDP growth in the current quarter to around 2%. Note that a 2% growth in the US is still above average and shouldn’t be enough to convince the Fed to start cutting the rates too early if the slowdown in inflation remains insufficient. But if inflation slows, nothing will stop the bond traders from continuing to rush in.

Today, all eyes on the US PCE index – the Fed’s favourite gauge of inflation. The headline PCE may have eased from 3.4% to 3.0% in October, and core PCE is seen down from 3.7% to 3.5%. A softer-than-expected figure could further fuel expectations of an early Fed cut, while a stronger-than-expected set of figures should, in theory, calm down the dovish enthusiasm and call for a rebound in the yields. Presently, activity on Fed funds futures gives almost 80% chance for a Fed rate cut in May, and the probability of a March cut is 50-50.

EUR/USD retreats despite soft Dollar

The rally in US bond markets, and the tumbling US yields weigh on the US dollar. The USDJPY extended its drop, and finds sellers above the 100-DMA, whereas the EURUSD couldn’t extend gains above the 1.10 mark as inflation data from some Eurozone countries came sufficiently soft yesterday. Spanish inflation fell more than expected to 3.2%, as German inflation fell more than expected to 2.3% in November. The Eurozone’s aggregate inflation will be released after the French and Italian figures this morning, and slowing inflation will certainly give cold feet to the euro bulls above the 1.10 level – even though it’s not impossible to see the pair surpass this level due to USD weakness.

Crude Oil rebounds before OPEC decision

OPEC is expected to announce an eagerly expected decision regarding its supply strategy today. The barrel of US crude is back to $78pb, and ready to jump above the 200-DMA if Saudi Arabia obtains a joint effort from other members in reducing supply.

Of course, OPEC will do its best to get the oil bulls on its side when it announced its decision today. But when expectations are high, they are harder to satisfy. Therefore, if a post-decision rally fails to send the price of a barrel above the $81pb level, the critical 38.2% Fibonacci support on September to November selloff that should distinguish between the actual bearish trend and bullish consolidation, it could be a better idea to sell the tops.

COP28

70’000 people flew to Dubai this week to talk about how to cut carbon emissions. 70’000 people. Staying where they were would certainly be a first step in gaining credibility on how to cut emissions. And that’s not all the absurd in this COP summit. The CEO of the Abu Dhabi National Oil Company will be leading this week’s summit. Yes, the CEO of a company that can survive only by keeping carbon emissions where they are. Additionally, the fossil fuel industry has been invited to participate more than any other COP since the gatherings began in 1995. You know, nothing says ‘let's save the planet’ like a summit led by a big oil CEO.

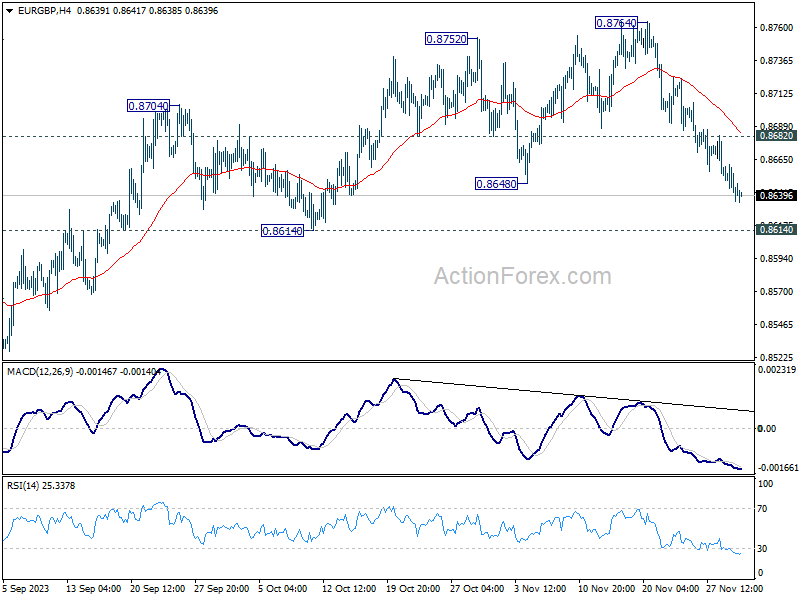

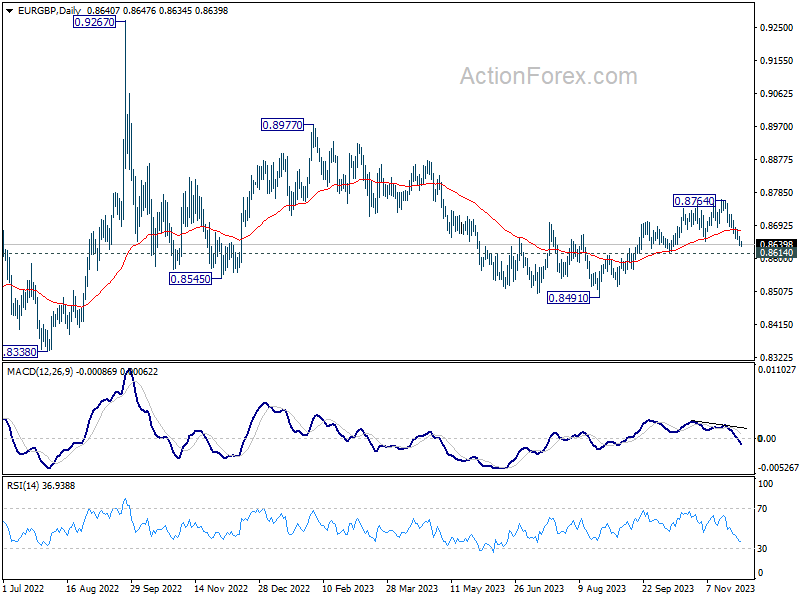

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8631; (P) 0.8647; (R1) 0.8657; More....

EUR/GBP's break of 0.8648 support argues that corrective rebound from 0.8491 has completed at 0.8764 already. Intraday bias is now on the downside for 0.8614 support first. Firm break there will target a retest on 0.8491 low. On the upside, above 0.8682 minor resistance will turn intraday bias neutral first.

In the bigger picture, outlook is mixed up by deeper than expected fall from 0.8764. On the downside, firm break of 0.8614 support will argue that down trend from 0.9267 (2022 high) is still in progress. Deeper fall would be seen through 0.8941 low. Nevertheless, break of 0.8764 will revive that case of medium term bullish reversal.

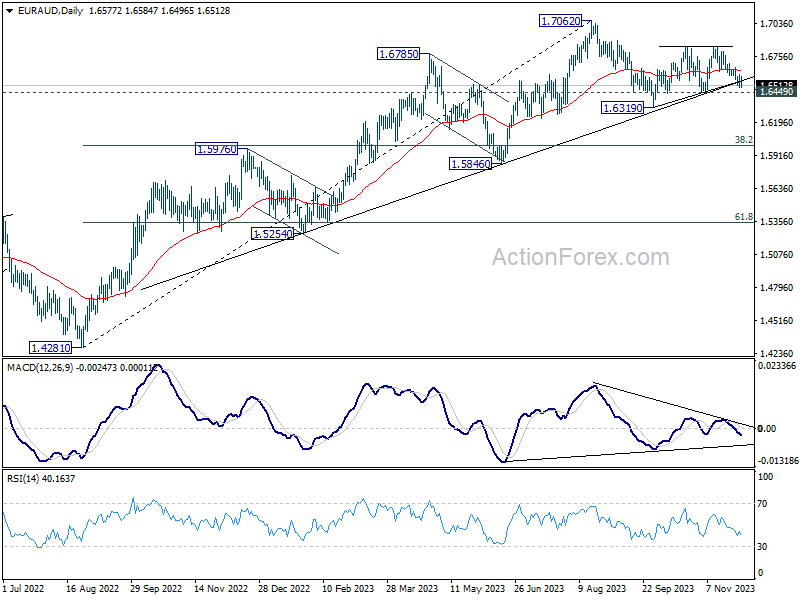

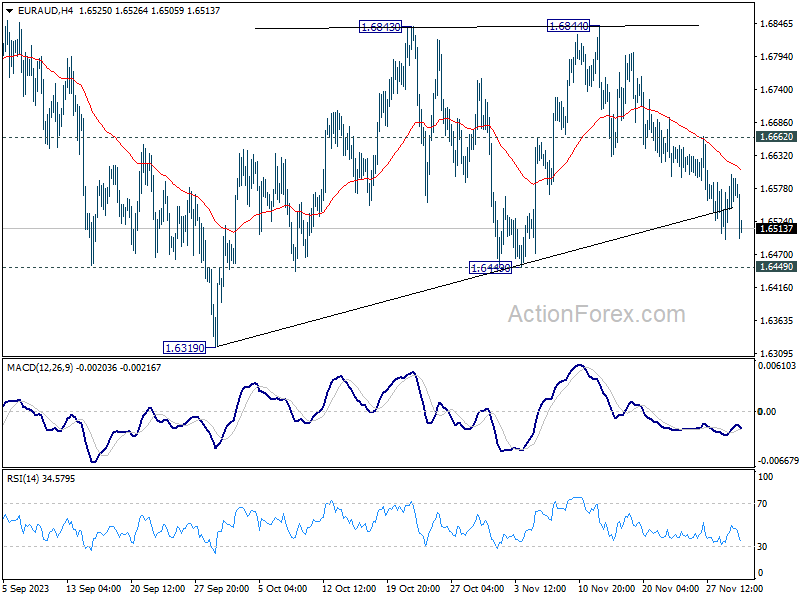

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6514; (P) 1.6560; (R1) 1.6621; More...

No change in EUR/AUD's outlook and further fall is expected with 1.6662 resistance intact. Firm break of 1.6449 support will argue that the pattern from 1.6319 has completed at 1.6844 as a corrective move, and fall from 1.7062 is ready to resume through 1.6319. On the upside, above 1.6662 minor resistance will turn bias back to the upside for 1.6844 resistance instead.

In the bigger picture, while 1.7062 is a medium term top, there is no clear sign of trend reversal as EUR/AUD continues to draw strong support from the medium term trend line. Break of 1.7062 will resume the larger up trend from 1.4281 (2022 low) to 1.7691 fibonacci level. Nevertheless, break of 1.6449 support will argue that deeper correction is underway to 38.2% retracement of 1.4281 to 1.7062 at 1.6000.