Sample Category Title

US Manufacturing ISM Taking Center Stage

Markets

Poor French growth and inflation data published at the start of European dealings caused European interest rate markets to try a new leg on recent bull run. Yields across the European/German curve touched new cycle correction lows. The EMU flash CPI estimate at -0.5% M/M and 2.4% Y/Y (headline) and 3.6% Y/Y (core) beat consensus estimates by a big margin. However, this was no real surprise given earlier releases of national data. For sure, the subsequent price action, especially in European interest rate markets, didn’t look like a genuine exhaustion move yet. Especially yields at the short-end continue to price an ever growing chance of an early ECB rate cut next year (25 bps in April fully discounted). Still, yields tentatively started looking for a bottom. German yields at the end of the day changed between -2 bps (2-y) and +1.5 bps (10-y). In the US, the highly awaited October PCE deflators (headline 0% M/M and 3% Y/Y, core 0.2% M/M and 3.5% Y/Y) and the weekly jobless claims (218k) were too close to expectations to trigger further bond gains. The MNI Chicago PMI even delivered a big upside surprise (55.8 from 44.0) with solid details. The market reaction was limited, but it helped US yields to maintain intraday gains. US yields closed between 3.5 bps (2-y) and 7.2 bps (10-y) higher. Divergence both in data and in interest rates between EMU and the US, triggered hefty profit taking on the recent EUR/USD rally. The pair closed at 1.0888 (compared to a 1.0967 close on Wednesday). The move mirrored both euro weakness and USD resilience. DXY closed at 103.5 (open 102.79). USD/JPY regained the 148 big figure (close 148.2). Sterling showed some erratic swings intraday. The BoE Chief Financial Officers survey showed UK business leaders expect inflation to hold above 3% over the next three years. UK gilts underperformed. Sterling continued outperforming the euro with EU/GBP close at 0.8625, nearing the October correction low.

Asian equities mostly trade slightly in the red this morning. US treasuries are going nowhere. The dollar eases slightly after yesterday’s rally. After mostly disappointing data of late, the China Caixin Manufacturing PMI unexpectedly returned into positive growth territory (50.7 from 49.5). Later today, there are no important data in Europe. In the US, the Manufacturing ISM is taking center stage. A slight improvement from 46.7 to 47.8 is expected. Of late, markets were mostly driven by (perceived) soft/negative data release. After yesterday’s surprise jump in the Chicago PMI, maybe we now should look at the market reaction function in case of an unexpected strong figure. Will better than expected data finally help a bottoming out process in yields? If so, it might also support the downside in the dollar. In this respect, EUR/USD dropped out of an ST upward trend channel starting begin November. Next support is coming in at 1.0825/26 (Mid November correction low/38% retracement ST). Comments by Fed Chair Powell at Spelman College are a wildcard. It’s unclear if he’ll touch on monetary policy at the final occasion ahead of the blackout period in the run-up to the December 13 policy meeting.

News & Views

The OPEC+ meeting, originally scheduled for Nov 26 in Vienna but delayed because of diverging views and replaced by online discussions, ended yesterday with a commitment by Saudi Arabia to extend its voluntary production cuts of 1 mn barrels/day through the first quarter. Additionally, member states including Russia, the UAE, Kuwait and Iraq pledged voluntary cuts as well in Q1 2024 totaling a combined 1.2 mn barrels/day. Oil prices rallied in the run-up to the decision and fell back afterwards, from $84.5/b to $80.5/b. Apart from the anticipation effect, the vague wording and non-unanimous commitment in the OPEC statement created doubt and uncertainty on actual output levels in coming months.

Hungarian Cabinet Minister Gulyas yesterday announced an extension of interest rate caps on household mortgages and on corporate loans for SME’s. They were first introduced early October in a reaction to the high MNB policy rate. Gulyas said that MNB rates are coming down but are still very high (11.5%). The interest rate cap on new loans for households at 8.5% will be extended until July 1. The cap on new loans for businesses at 12% will be prolonged until April 1.

DAX Will Open Elliott Wave Bullish Sequence Soon

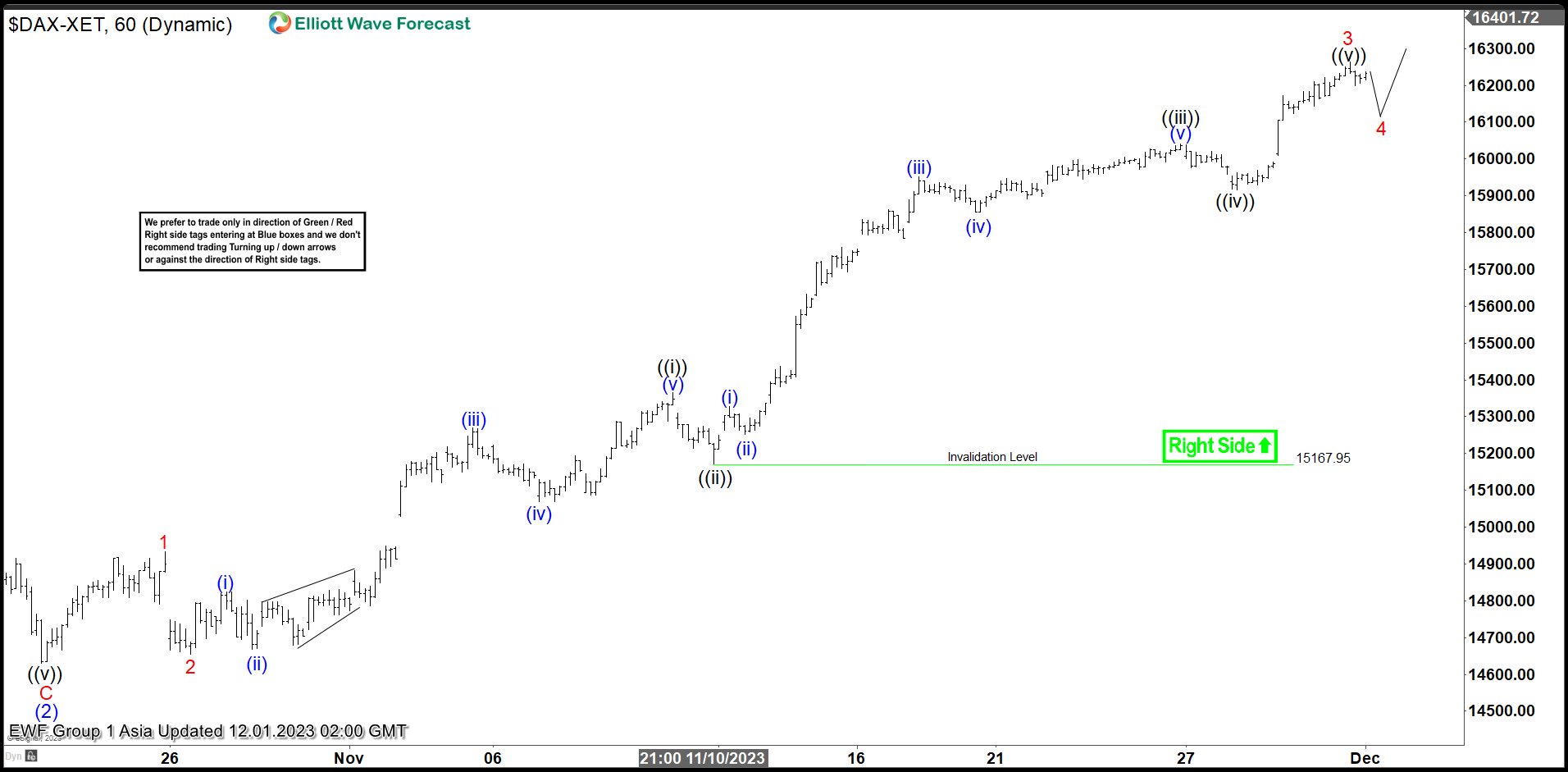

$DAX cycle from 9.29.2022 low is in progress as a 5 waves impulse Elliott Wave structure. Up from 9.29.2022 low, wave (1) ended at 16528.97 and dips in wave (2) ended at 14630.21. The Index extends higher again in wave (3). It still needs to break above wave (1) at 16528.97 to validate this view and opens up a bullish sequence.

The 1 hour chart below shows the wave (2) pullback at 14630 and the subsequent rally higher. Up from wave (2), wave 1 ended at 14933.69 and dips in wave 2 ended at 14655.08. The Index is then nesting to the upside in wave 3. Up from wave 2, wave ((i)) ended at 15364.49 and pullback in wave ((ii)) ended at 15171.58. Index then extended higher in wave ((iii)) towards 16041.17 and wave ((iv)) pullback ended at 15915.4. Expect the Index to extend higher in wave ((v)) to complete wave 3. It then should pullback in wave 4 and extends higher again afterwards in wave 5. Near term, as far as pivot at 15167.95 low stays intact, expect the Index to extend higher. Once wave 5 is done, it should complete wave (3) in higher degree.

DAX 1 Hour Elliott Wave Chart

DAX Elliott Wave Video

https://www.youtube.com/watch?v=k128NTtrFRw

WTI Oil Technical: Positive Elements Intact Ex-post OPEC+

- Earlier rally in WTI crude oil fizzled out ex-post OPEC+ meeting due to uncertainty over 2024 oil supply cut commitments from members.

- The strongest commitment came from Saudi Arabia where it will extend its its voluntary 1 million barrels per day supply through Q1 2024 while Angola has decided to go against its newly reduced supply target.

- Technical analysis suggests several positive elements in WTI crude oil despite the uncertainty over the demand and supply dynamics of the oil market.

- Watch the key support zone at US$74.30/72.40 per barrel for the week ahead.

In the recent two weeks, oil prices have exhibited wild swings of 6% to 8% as the bulls and the bears grappled with the uncertainty over oil supply cuts from OPEC+ coupled with increasing inventory stockpiles from the US and a sticky weak external demand environment.

The earlier OPEC+ ministerial meeting scheduled last Sunday has been rescheduled to yesterday, 30 November due to disagreements among African nations with leading member, Saudi Arabia on the quantum of the extended supply cuts for 2024.

In the lead-up to the outcome of yesterday’s meeting, oil prices staged an initial rally of close to 3% where the West Texas oil (a proxy of WTI crude oil futures) cleared above the 200-day moving average to print an intraday high of US$79.79/barrel due to several media reports that there was a possibility of deeper cuts enacted for 2024 before its gains were wiped out to close at a daily loss of -2.70% ex-post OPEC+ meeting.

The oil market has faced the curse of the “buy the rumour, sell the fact” due to uncertainty over the anticipated extended oil supply cuts for 2024. The strongest commitment came from Saudi Arabia where it would extend its voluntary 1 million barrels per day supply through Q1 2024 but there was an absence of a comprehensive breakdown of supply cuts among all members with only a selected few detailing their respective supply reductions.

Also, these agreed supply cuts for 2024 are voluntary which means members may defy the committed output quotas, and Angola has “revolted” against its new supply target and stated it will continue pumping as usual, increasing the risk of other OPEC+ members may not follow through on the latest set of agreed commitments.

In the lens of technical analysis, there are still several positive elements intact to potentially stall the ongoing bearish onslaught in oil prices.

Weekly price actions have formed “long-legged Doji” candlesticks

Fig 1: West Texas Oil medium-term trend as of 1 Dec 2023 (Source: TradingView, click to enlarge chart)

In the prior two weeks, the price actions of West Texas Oil have formed two weekly consecutive “long-legged Doji” candlestick patterns that suggest the current bearish sentiment has started to exhibit a form of “hesitation and indecisiveness” to potentially push prices lower.

In addition, the daily RSI momentum indicator has continued to inch higher since 16 November 2023 after it drifted down to its oversold zone.

These observations have taken shape right above a key medium-term support of US$72.40 (also the ascending trendline from the 20 March 2023 low) which suggests that the downside momentum of the two-month corrective decline of -23% from its 28 September 2023 high of US$95.50/barrel to 16 November 2023 low of US$72.68/barrel has started to abate.

Impending minor bullish reversal “Inverse Head & Shoulders” sighted

Fig 2: West Texas Oil minor short-term trend as of 1 Dec 2023 (Source: TradingView, click to enlarge chart)

On its shorter-term hourly chart, the price actions of West Texas Oil have traced out a potential minor “Inverse Head & Shoulders” bullish reversal configuration.

Watch the key short-term pivotal support at US$74.30 and a clearance above US$79.80 (neckline resistance of the “Inverse Head & Shoulders” may trigger a bullish breakout to see the next intermediate resistance coming at US$83.20/84.05 (also the downward sloping 50-day moving average).

However, failure to hold at US$74.30 exposes the medium-term support of US$72.70/72.40.

Are Equity Bulls Too Tired to Continue Running?

Here we are, saying thanks and goodbye to the excellent month of November for both bond and equity markets. US bonds rallied, and the bond yields melted starting from the end of October remember, and the melting bond yields offered to the S&P500 one of its biggest gains for a month of November. The index rallied more than 9% in November, is up by more than 10% since the end of October and Nasdaq 100 gained nearly 12% last month and is up by 15% since its October dip. Note that yields are one – and an important - part of the valuation story because when the return for low-risk assets decline, the valuations of riskier assets automatically move up. But there is also a fundamental leg to the US equity story.

Hot off the press from the US Bureau of Economic Analysis pointed at a 3.3% growth in total corporate profits during Q3, reaching an annualized rate of almost $3.3 trillion. This figure falls just short of the previous all-time peak of $3.3 trillion recorded in Q3 of 2022. And the significance lies in the fact that this profit increase demonstrates the adaptability of US companies to the post-COVID operating landscape of elevated wages and increased borrowing costs.

The debate now is, will such a strong month of November spoil our Santa rally, or the US stock markets will continue to extend gains in December? Looking at the aggregate company fundamentals, there is no reason for the rally to stop suddenly, unless shocker data pops up – like very bad jobs data or a very sharp decline in growth numbers to below-average levels. And even then, a part of the bad data would be tamed by soft Federal Reserve (Fed) expectations, right? And my past 10-year experience in the stock markets reminds me that valuations are never too high. Of course, over the past decade, the market was constantly navigating in the zero-rate regime and that’s changed since last year but it still feels like you are never thin enough, you are never rich enough, and the equities are never valued enough.

But looking at the technical indicators, US equities are now in overbought territory; they have been purchased too fast and in too short period of time and that a minor correction would be healthy in the next few sessions. But the latter doesn’t rule out a further rally when the overheated technical indicators cool down. A Santa rally is still on cards, if the Fed members continue not to mention to rapid fall in US yields to justify a more hawkish policy stance.

Good news is, inflation falls. Yesterday’s PCE data confirmed that the US PCE index fell from 3.4% to 3.0% in October, and core inflation eased from 3.7% to 3.5% - as expected. The fact that the data came in line with expectations gained little traction among bond buyers, as such we saw the US 2-year yield rebound past its 200-DMA and consolidate there this morning.

Better news is: inflation in Europe came in softer than expectations. Inflation in Eurozone fell to 2.4% in November from 2.9% printed a month earlier. It was also much better than a fall to 2.7% expected by analysts! Core inflation also eased more than expected to 3.6%. The EURUSD fell below 1.09 and losses could extend to 1.08/1.8020 region including the 200-DMA and the major 38.2% retracement on the October-November rebound.

Now, inflation can be a bit tricky and tends to make unexpected comebacks. Europe isn't completely out of the woods yet, as the jobs market remains robust, and the European Central Bank (ECB) remains cautious. However, one of the major drivers of inflation in Europe, the Russian gas nightmare, is gently over as the region has taken massive steps to prepare for this winter season: it reduced its dependence to Russian gas to only 12%. That’s a big drop from the 40% before the Ukraine war.

Moreover, OPEC seemed kind of overwhelmed with events this week, as the group announced an additional 1mbpd cut that will be shouldered by cartel members, on top of the 1mbpd cut that Saudi will extend to next year. But the latter was nowhere near appetizing to get the oil bulls running. The barrel of crude fell to $75pb and should continue finding sellers into the 200-DMA, near $78pb.

Disinflation Continues in Euro Area

Market movers today

The most important data release of the day will the November ISM Manufacturing index from the US. Consensus expects a modest rebound, as several other leading indicators for global manufacturing have shown signs of bottoming out lately, even if the US Flash PMI still ticked lower in November.

Manufacturing PMIs are due for release also for Sweden and Norway.

The Fed chair Powell will participate in a fireside chat at 17CET. The FOMC's blackout period begins tomorrow, so this will be a key opportunity to provide markets some final remarks ahead of the December meeting. We still think that the Fed is already done with hikes and will begin its cutting cycle in March.

The 60 second overview

Euro Area: The Euro area HICP inflation declined more as expected as also hinted by early country releases. The monthly decline of euro area HICP by 0.5 % m/m versus consensus of -0.2% m/m translated into a yearly growth rate of just 2.4% y/y, even below the market pricing of 2.5%. Core inflation ticked down to 3.6% y/y (cons: 3.9%, prior: 4.2%). Overall, the slowdown in inflation was broad-based and the momentum is slow which is important for the ECB. The previous base effects that have driven inflation down will fade now and therefore the low monthly price momentum is what will bring inflation to the target. Hence, this print is clearly positive for the ECB with ECB done on rate hikes, but the easy financial conditions opens for a discussion to ending full PEPP reinvestments at the upcoming December meeting, as Lagarde also hinted at earlier this week.

US: In the US the October PCE inflation was slightly below expectations (+0.0% m/m). The Fed's preferred Core Services PCE inflation continues to slow down in both m/m (+0.21%) and y/y (+4.6%) terms. We didn't find this to be major news for the markets here, albeit it is yet another signals that the Fed continues to make progress towards cooling underlying inflation.

Oil: OPEC disappointed the oil market yesterday with its decision to keep status quo and about roll over current output levels to next year. Amid deteriorating global demand, the decision not to tighten supply further was underwhelming. However, we were not surprised. We have downplayed the importance of OPEC which turned out right. Going forward, we expect the oil market to be in the hands of global growth and the dollar and look for Brent to average USD80-85/bbl.

China: Overnight, the Chinese Caixin manufacturing PMI unexpectedly rose to 50.7 from a below 50 reading last month.

Equities: Equities were higher again yesterday. This was interesting as a new relationship came back into place: Equities went up together with yields. Reason being right data being strong (manufacturing) and the "right" areas weakening (jobless claims, inflation). Value cyclicals fared well, such as industrials or banks. Thereby huge dispersion between value indices like Dow jones up 1.5% vs Nasdaq down -0.2%, as investors found financing in big tech. S&P 500 0.4% and Stoxx 600 0.6%. US are unchanged this morning.

FI: European rates were volatile yesterday where initially a rally was observed across the maturities on the back of the low French, Dutch and European inflation data. However, what seemed like a buy the rumour, sell the fact reaction on the European inflation release the markets gradually sold off through the rest of the day amid US data release which was broadly in line with expectations during the afternoon (PCE core, jobless claims). Markets took 3bp out of the rate cut pricing for 2024, and now price ECB to cut 110bp through the end of 2024. The first full 25bp cut is priced for April 2024. The decline in yields in both the US and the EA has been driven by the front end, where both jurisdictions have added a full 25bp rate cut this week to its policy expectations for next year. We do not find data compelling enough, particularly on the euro side to validate this move, and hence we look to fade this rally.

FX: EUR/USD declined below the 1.09 mark on a day where the USD broadly strengthened across the G10, despite risk assets ending a strong November with another day in the green. USD/JPY is trading just above 148 - even though the cross trended up in yesterday's session, it seems that the JPY has increasingly been reacting to the notion of a peak in global yields recently. EUR/GBP declined to the lower end of the 0.86-0.87 range. The Scandies had a bad day, with both the SEK and NOK selling off. EUR/SEK rose to around 11.40, while EUR/NOK rose above 11.75.

Credit: Credit indices drifted wider yesterday where iTraxx Xover widened 6.5bp to 373.5bp and Main widened 1.2bp to 683bp. The slight cautious tone was also visible in the primary market where the activity was subdued.

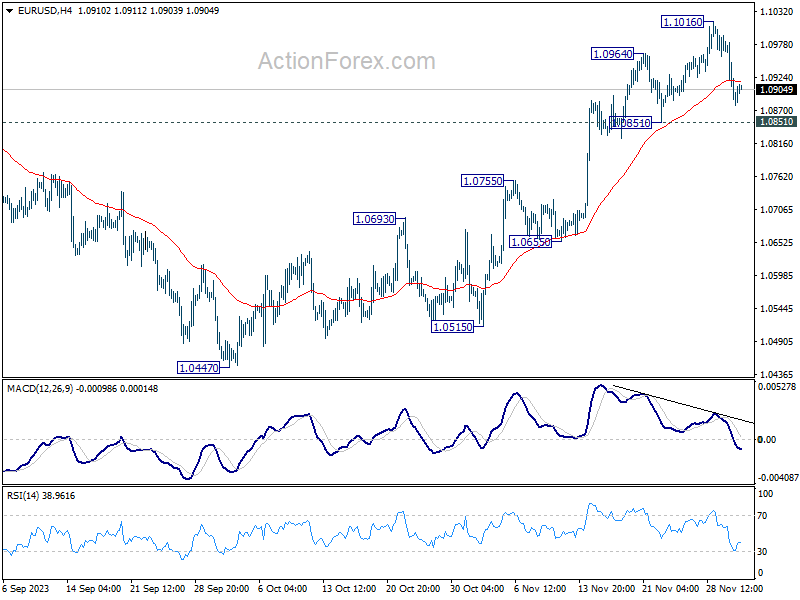

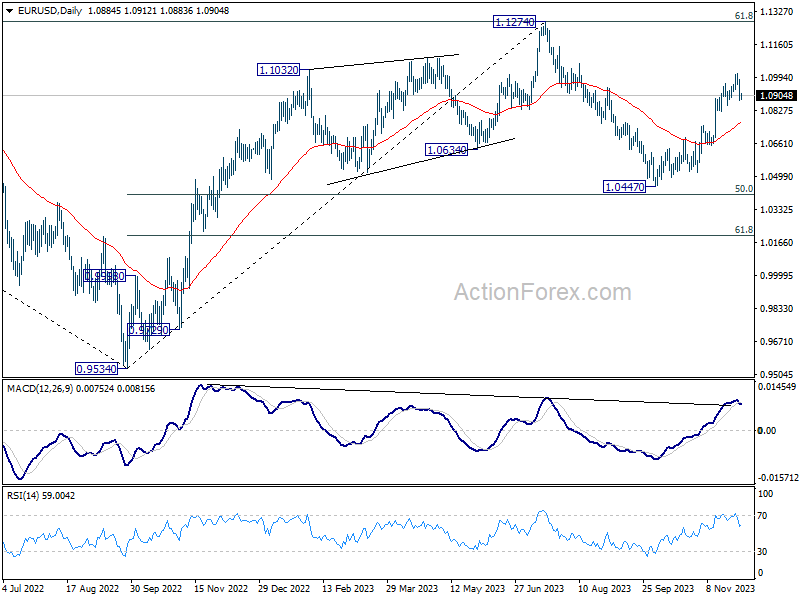

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0851; (P) 1.0917; (R1) 1.0956; More...

Intraday bias in EUR/USD remains neutral as consolidation from 1.1016 is extending. As long as 1.0851 support holds, further rally is still expected. On the upside, firm break of 1.1016 will resume the rise from 1.0447 to 1.1274 resistance next. But strong resistance should be seen there to limit upside. However, sustained break of 1.0851 will confirm short term topping, and turn bias back to the downside for deeper fall.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

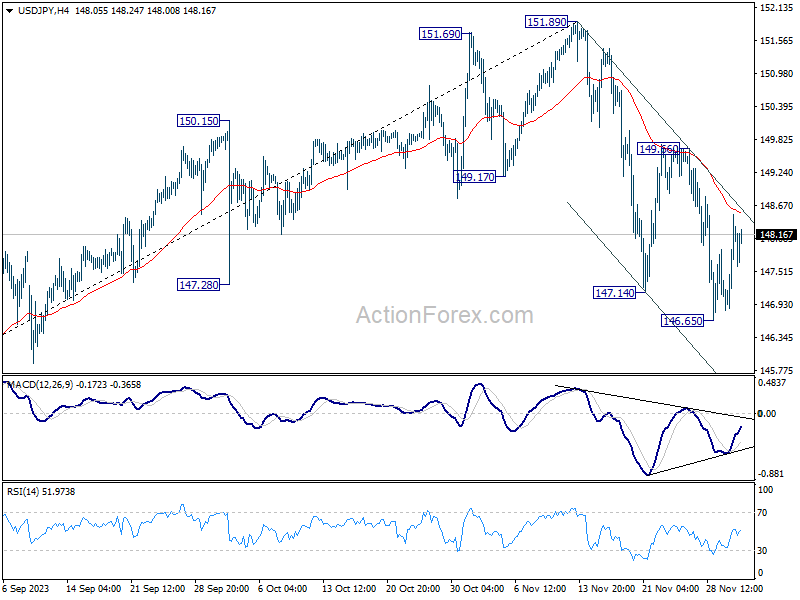

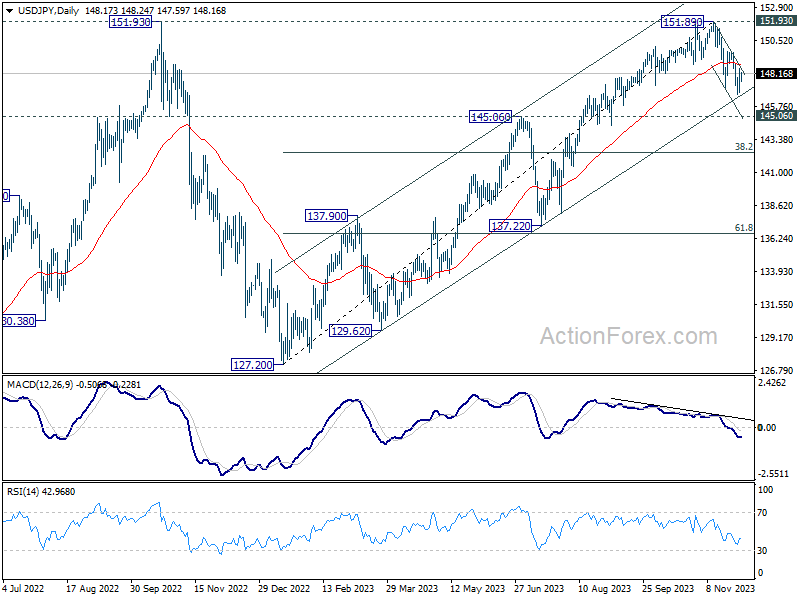

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.21; (P) 147.86; (R1) 148.88; More...

Intraday bias in USD/JPY remains neutral for the moment. On the upside, sustained break of 55 4H EMA (now at 148.54) will argue that corrective fall from 151.89 has completed with three waves down to 146.65. Intraday bias would be back on the upside for 149.66 resistance for confirmation. Nevertheless, rejection by 55 4H EMA will resume the fall from 151.89 towards 145.06 key support level.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

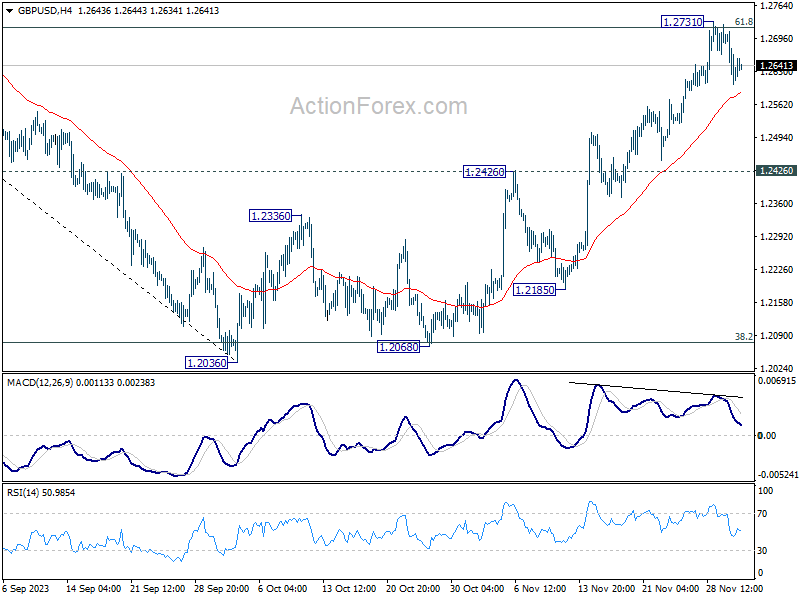

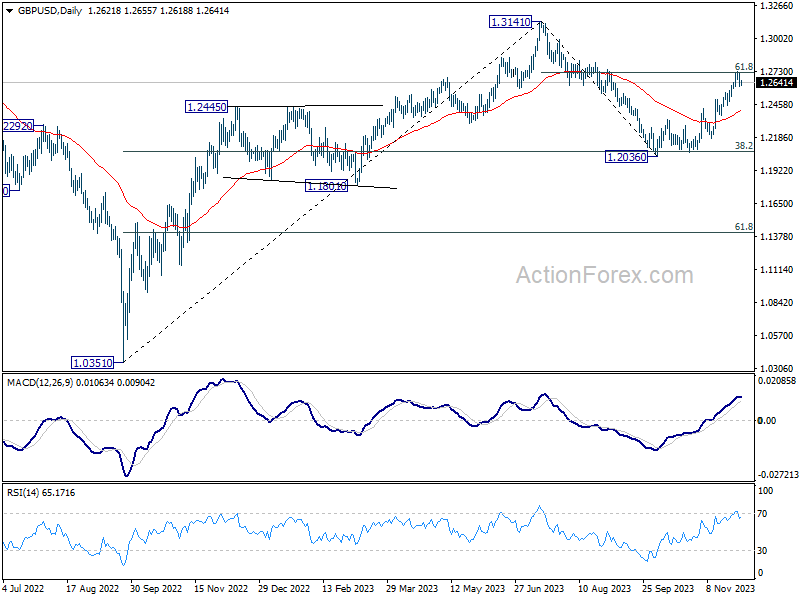

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2582; (P) 1.2646; (R1) 1.2689; More...

GBP/USD is staying in consolidation from 1.2731 and intraday bias remains neutral at this point. For now, further rally is in favor as long as 1.2426 resistance turned support holds. On the upside, sustained trading above 61.8% retracement of 1.3141 to 1.2036 at 1.2716 will pave the way to retest 1.3141 high.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

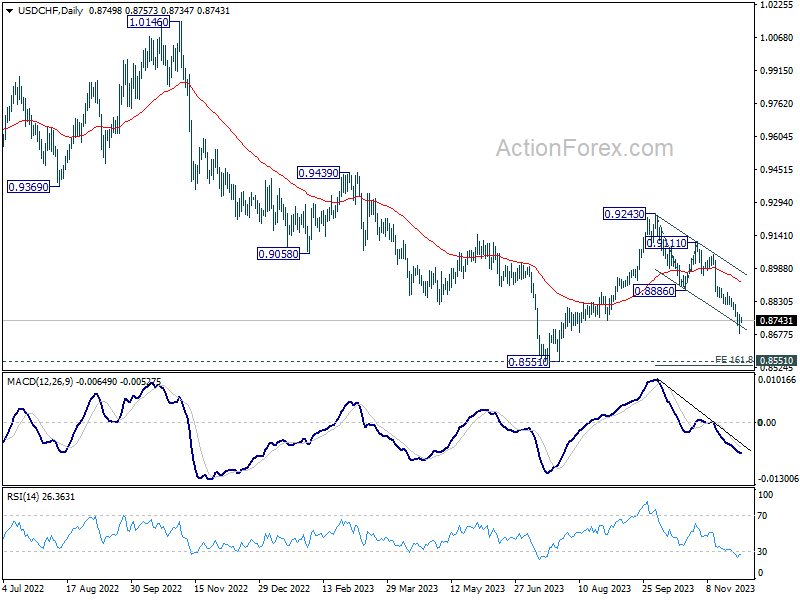

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8701; (P) 0.8736; (R1) 0.8787; More....

Intraday bias in USD/CHF remains neutral for the moment, and some more consolidations could be seen above 0.8716. Risk will stay on the downside as long as 0.8886 support turned resistance holds. On the downside, break of 0.8716 temporary low will resume the fall from 0.9243 to 161.8% projection of 0.9243 to 0.8886 from 0.9111 at 0.8533, which is close to 0.8551 low.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. For now, this will remain the favored case as long as 0.8886 resistance holds.

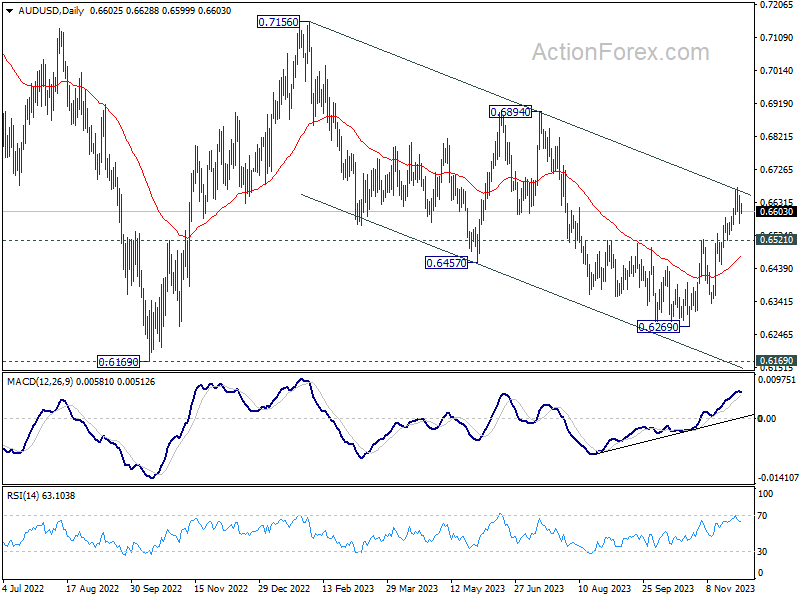

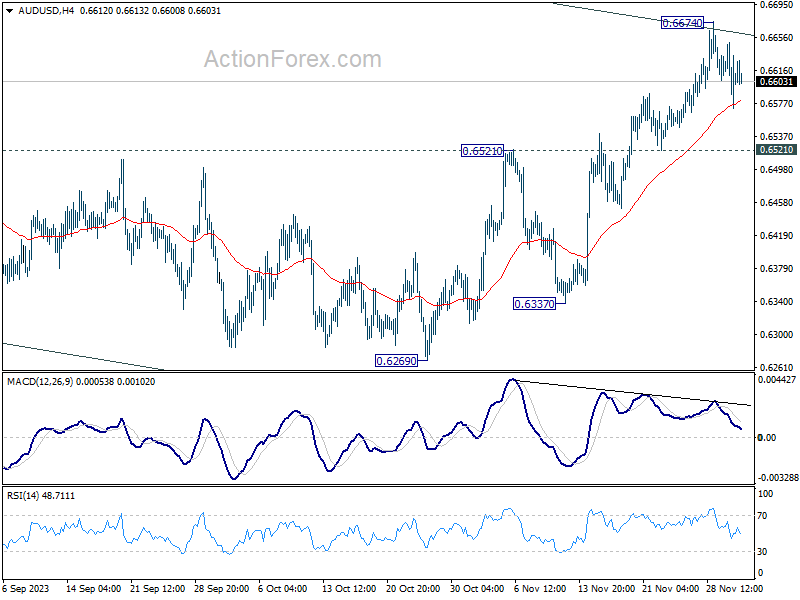

AUD/USD Daily Report

Daily Pivots: (S1) 0.6567; (P) 0.6609; (R1) 0.6647; More...

Intraday bias in AUD/USD remains neutral for the moment. Some more consolidations could be seen below 0.6674 first. But further rally is expected as long as 0.6521 resistance turned support holds. On the upside, sustained break break of channel resistance (now at 0.6661) will argue that whole decline from 0.7156 has completed with three waves down to 0.6269. Further rally should then be seen to 0.6894 resistance for confirmation.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. price actions from 0.6169 (2022 low) could be just a medium term corrective pattern, with rise from 0.6269 as the third leg. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.