Sample Category Title

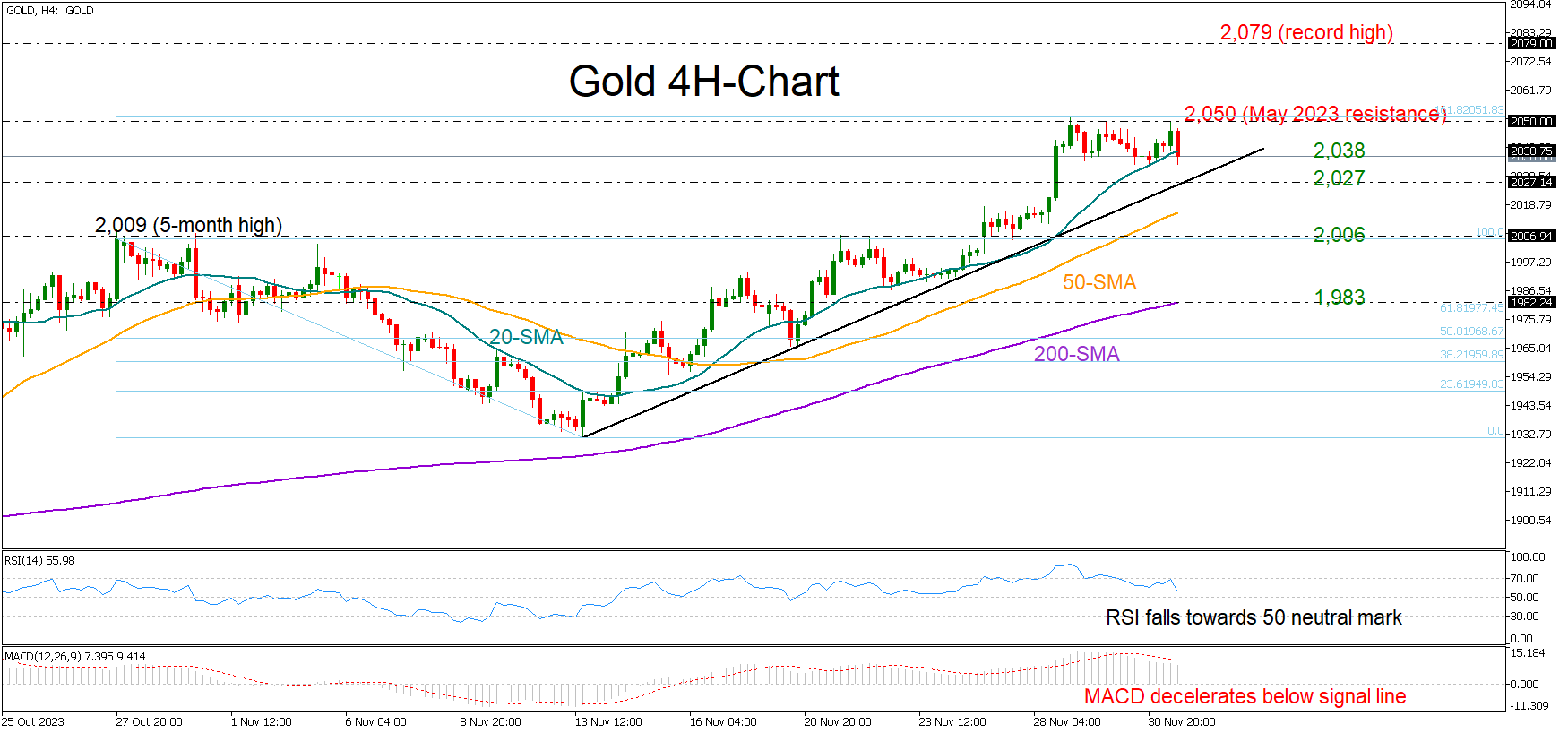

Gold Remains Trapped Below 2,050

- Gold flatlines near former resistance

- Short-term bias leans to the downside

- Key support levels hold intact

Gold shifted to the sidelines following the advance towards its May 2023 resistance of 2,051 on Wednesday.

The 20-period simple moving average (SMA), which has been cooling downside pressures recently, seems to be cracking at 2,038, but the support trendline drawn from November’s lows could still come to the rescue at 2,027 despite the negative trajectory in the RSI and the MACD. Then, the resistance-turned-support region of 2,006 might prevent an outlook deterioration ahead of the 200-period SMA at 1,983.

Alternatively, should the bulls set another strong footing around the 20-period SMA, they may push for a close above the 2,050 ceiling. A successful penetration higher could initially stall near the resistance line from September 2023 at 2,065 before heading for the 2023 record high of 2,079. If buying interest persists, the uptrend could gain new legs in the uncharted territory, likely bringing the 261.8% Fibonacci extension of the latest downleg at 2,126 under the limelight.

In summary, gold is preserving an upward trajectory in the short-term timeframe. While the falling technical indicators are reflecting some discomfort among traders, only a pullback below 2,006 would officially violate the positive structure.

Sunset Market Commentary

Markets:

Today’s waiting game ahead of the November US manufacturing ISM and Powell’s final public appearance ahead of the blackout period before the December 13 FOMC meeting freed up time to take a look at some of the key asset classes’ November performance. It’s stating the obvious that bonds after three years of mainly gloom turned out big winners. US Treasuries clearly outperformed German Bunds which in their turn performed better than UK Gilts. US Treasury yields lost 40 bps (2-yr) to 60 bps (10-yr & 30-yr) on a monthly basis. Investors embraced softer payrolls growth, the ongoing disinflationary process and Fed comments as evidence of the goldilocks safe landing scenario. At the end of October, they still pondered the possibility of a final rate hike early next year (50% probability at the January meeting) with an end of 2024 policy rate expected around 4.5%-4.75%. One month later, we’re talking about a fully discounted first rate cut at the May meeting with a prognosed EoY policy rate of 4%-4.25%. German Bunds followed US Treasuries with monthly changes varying between -20 bps (2-yr) and -40 bps (30-yr). A first 25 bps ECB rate cut is now discounted by the April 2024 meeting from the June meeting one month ago. Investors see the ECB policy rate now clearly below 3% by the end of next year compared to a level of 3.25% at the end of October. UK gilt yields lost 17.5 bps (2-yr) to 34 bps (10-yr) with Bank of England members being the most vocal in pushing back against market pricing of a rapid central bank pivot. Overall, we don’t believe that the big central bankers will have the scope for policy rate cuts before H2 2024 with the Fed in pole position to be a frontrunner in the cycle. Monthly yield differentials and the positive risk climate in help explaining sterling’s outperformance against the euro and the dollar. EUR/GBP ended the month at 0.8625 from 0.8707. Cable (GBP/USD) rallied from 1.2153 to 1.2624. EUR/USD went from 1.0575 to 1.0888 with a small stay above 1.10 (first time since mid-August) in between. The trade-weighted dollar (DXY) faced losses of 3%. The S&P 500 rallied by almost 9% with the Nasdaq adding 10.70%. Both tested the 2023 top. The EuroStoxx50 added nearly 8% over the reference period.

News & Views:

Q3 growth in the Czech Republic surprised again on the downside. After marginal growth of 0.1% Q/Q in Q1 and Q2, activity contracted by a bigger than expected 0.5% Q/Q in the July-September quarter. Activity was 0.7% below the level in the same period last year. Household consumption declined by 0.3% Q/Q, but financial consumption expenditure overall (+0.7 Q/Q) was supported by strong demand from the public sector (1.2%). Gross capital formation declined by 1.8% Q/Q. Both fixed investment (-0.3%) and especially changes in inventories contributed negatively as was the case for external demand. Also today, the Czech manufacturing PMI at 42.0 (from 41.7) indicates an ongoing contraction in the sector in Q4. This keeps the Czech economy on the brink of a potential recession in the second half of this year. Poor activity data and sluggish (foreign & domestic demand) might support the case for the Czech National Bank to start (CNB) its easing cycle already at the December 21 meeting. Even so, a rate cut, if any, will probably be limited (25 bps) as the CNB wants to be sure that price setting at the start of the new year won’t support an upward price spiral.

The November Canada labour market report was mixed to slightly stronger than expected. The economy added 24.9k jobs (net), slightly more than the 14k expected. Growth was due to a substantial rise in full time jobs (+ 59.6k). Part time employment declined. Employment increased in manufacturing (+28k) and construction (+16k), but declined in the services sector (-13.4k). Still the unemployment rate rose slightly from 5.7% to 5.8% on a further increase of the labour force. Total hours worked declined 0.7% M/M but were still 1.3% higher on a Y/Y-basis. The hourly wage growth rate for permanent employees was unchanged at 5%. Even as the BoC still has a tightening bias due to persistent core inflation, today’s report will allow it to keep a wait-and-see approach at next week’s policy meeting. The loonie gains marginally after the release of the report (USD/CAD 1.3525), extending its recent gradual rebound against the dollar.

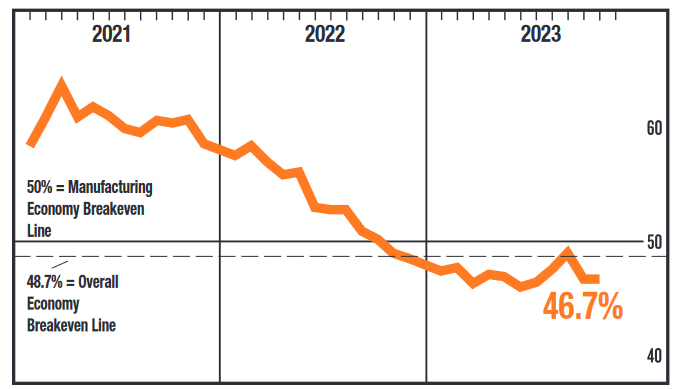

US ISM manufacturing unchanged at 46.7, corresponds to -0.7% annualized GDP contraction

US ISM Manufacturing PMI was unchanged at 46.7 in November, missed expectation of 47.7. Looking at some details, new orders rose from 45.5 to 48.3. Production fell from 50.4 to 48.5. Employment fell from 46.8 to 45.8. Prices rose from 45.1 to 49.9.

ISM said: "The past relationship between the Manufacturing PMI and the overall economy indicates that the November reading (46.7 percent) corresponds to a change of minus-0.7 percent in real gross domestic product (GDP) on an annualized basis."

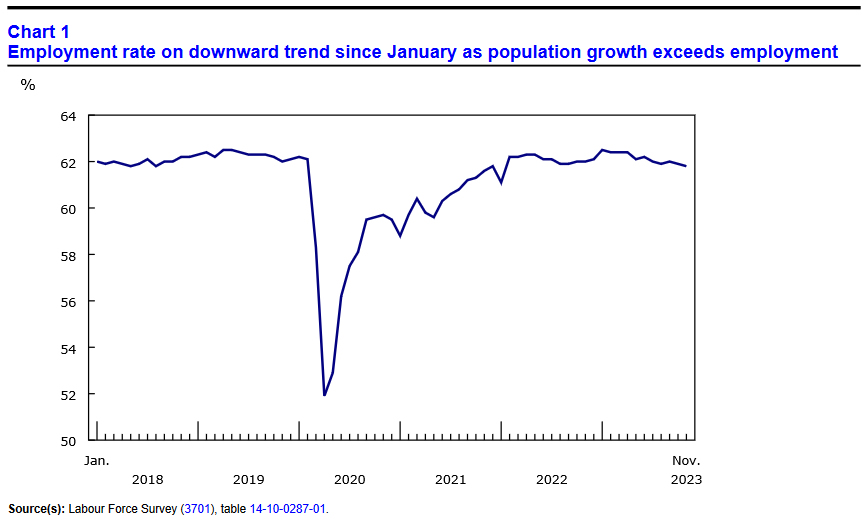

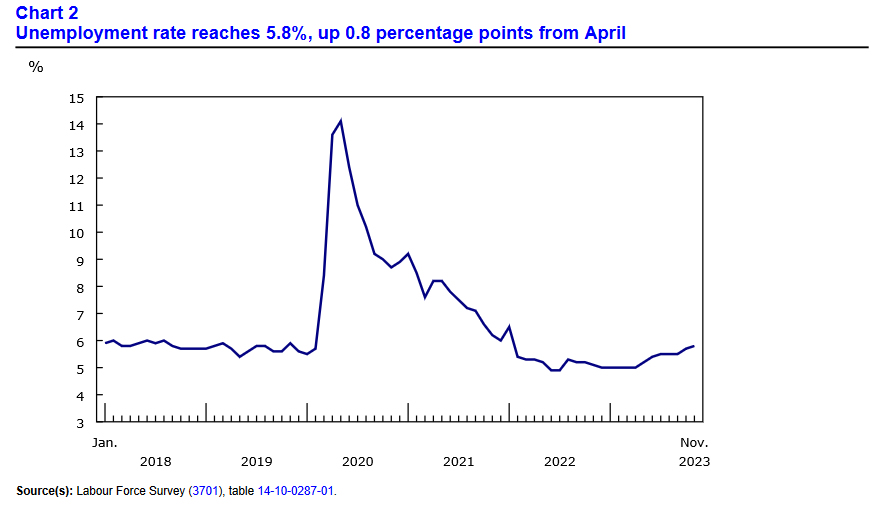

Canada’s Labour Market Posts Decent Gain in November

The Canadian labour market added 24.9k positions in November, with full-time employment up 59.6k and part-time employment down 34.7k.

The unemployment rate rose 0.1 percentage point to 5.8% and the participation rate was unchanged at 65.6%.

Employment by sector showed gains in manufacturing (+28k) and construction (+16k), while losses were seen in wholesale/retail trade (-27k) and finance, insurance, real estate, rental and leasing (-18k).

Lastly, total hours worked fell 0.7% month-on-month and wages were up 4.8% year-on-year (flat versus October).

Key Implications

Today's job gain was quite healthy with full-time jobs in the cyclically sensitive private sector driving the increase. But still, the 25k increase in the net number of Canadians finding jobs again failed to keep up with the 78k increase in population and the 36k boost to the labour force. The number of unemployed Canadian workers continues to grow (197k increase over 2023), forcing the unemployment rate higher again. As we have been talking about for some time, there are factors in the Canadian economy that will provide a buffer for the job market (see construction hiring), which is keeping the soft-landing scenario on track.

Today's report alongside yesterday's negative GDP print will be enough for the Bank of Canada (BoC) to hold its policy rate steady when it meets next week. While we aren't expecting the BoC to signal victory, the Bank will be able to project greater confidence that the process is working. This rhetoric will likely continue over the coming months, before it switches gears and starts to signal the beginning of rate cuts in the spring.

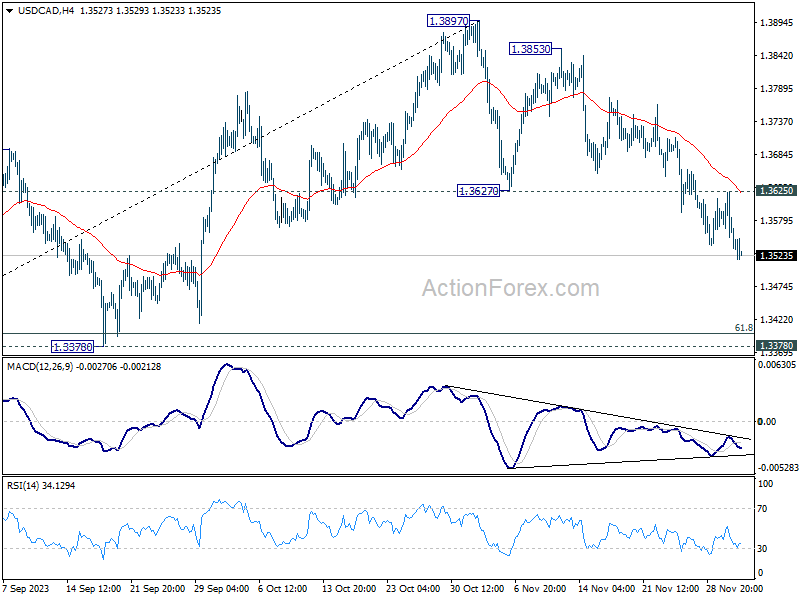

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3532; (P) 1.3579; (R1) 1.3606; More...

Intraday bias in USD/CAD remains on the downside at this point. Current fall from 1.3897 is in progress, and should target 1.3378 support next. On the upside, though, above 1.3625 minor resistance will turn intraday bias neutral again first.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

Canadian Dollar Rises on Jobs Data, Dollar Soft, Euro Worse

Canadian Dollar is firming slightly up in early US session, bolstered by stronger-than-expected Canadian job growth data. Despite the weakness in oil prices following disappointment over OPEC's production cut decisions, Loonie is displaying resilience. However, in the weekly performance chart, while Canadian Dollar is outshining Australian Dollar, it still lags behind the New Zealand Dollar (Kiwi).

In contrast, Euro is on track to be the week's weakest performer, with fresh selling pressure emerging. There is a potential for extending the selloff in the near term, particularly as EUR/GBP and EUR/AUD break through key near-term support levels. A critical point of focus in the currency markets is whether EUR/USD will manage to defend 1.0851 support level.

Turning to Dollar, it remains the second worst performer of the week. The market is anticipating Fed Chair Jerome Powell's final speech before Fed's blackout period. But it is unlikely that he will deliver any significant new information. From this point forward, the Dollar's trajectory is expected to be heavily data-dependent, leading up to FOMC rate decision on December 23. Key data releases that will likely influence Dollar's movement include today's ISM manufacturing data, next week's ISM services and non-farm payroll reports, and CPI data in the following week.

In Europe, at the time of writing, FTSE is up 0.64%. DAX is up 0.71%. CAC is up 0.25%. Germany 10-year yield is down -0.0115 at 2.437. Earlier in Asia, Nikkei fell -0.17%. Hong Kong HSI fell -1.25%. China Shanghai SSE rose 0.06%. Singapore Strait Times rose 0.56%. Japan 10-year JGB yield rose 0.0256 to 0.700.

Canada's employment rises 24.9k in Nov, unemployment rate ticks up to 5.8%

Canada's employment grew 24.9k in November, better than expectation of 14.2k.

Unemployment rate rose from 5.7% to 5.8%, matched expectations, and continuing an upward trend observed since April.

Total hours worked fell -0.7% mom and were up 1.3% on a year-over-year basis.

On a year-over-year basis, average hourly wages rose 4.8%, similar to the increase recorded in October.

UK PMI manufacturing finalized at 47.2, recovery remains elusive

UK PMI Manufacturing was finalized at 47.2 in November, up notably from October's 44.8. This marks the third consecutive month of rising PMI figures and the highest level since May.

Despite these gains, it is important to note that the PMI has remained below the neutral 50 mark for 16 consecutive months, indicating a prolonged period of contraction in the manufacturing sector.

Rob Dobson, Director at S&P Global Market Intelligence, commented, "Although the downturn in production eased sharply in November, the latest PMI report brings little festive cheer when the finer details are considered."

Dobson pointed out that despite improvement in production, the sector faces ongoing challenges. These include sharp declines in new order inflows and exports, along with clients destocking, which collectively suggest that a robust and sustained revival in meaningful growth is not yet on the horizon.

Dobson also noted, "Manufacturers are preparing for tough times ahead, with their continued caution leading to cutbacks in staffing, inventories, and purchasing."

Eurozone PMI manufacturing finalized at 44.2, continuing contraction, but slower

Eurozone's PMI Manufacturing was finalized at 44.2 in November, up from October's 43.1, reaching a six-month high. The report highlights reduction in the rate of decline for new orders, stocks, and purchasing activity, yet underscores a concerning trend of increasing employment cuts.

Breaking down the performance across Eurozone member states, Greece emerged as the only country in expansion, with PMI of 50.9. Ireland remained stable at 50.0. In contrast, other major economies like Spain (46.3), the Netherlands (44.9), Italy (44.4), France (42.9), Germany (42.6), and Austria (42.2) all registered figures indicative of ongoing contraction in their manufacturing sectors.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, said, "November has not been the prettiest." He noted the continuous decline in output and the trend of workforce reductions extending for six months. While acknowledging slight improvements in various sub-indices, de la Rubia pointed out that these are insufficient to signal a robust upward trend, describing them as "timid" and lacking the necessary dynamism.

De la Rubia also highlighted the divergent conditions within the top four Eurozone economies, with Germany uniquely showing a softening in output decline. In contrast, the situation appears to be worsening in other major economies.

He emphasized, "A crucial barometer for the recovery's onset will likely be a more synchronized upward movement in the economies PMI indexes, leading to a self-reinforcing reciprocal push among countries."

Swiss GDP rises 0.3% qoq in Q3, services provides support

Swiss GDP grew 0.3% qoq in Q3, above expectation of 0.1% qoq. SECO said: "The international environment remains challenging, with value added in industry stagnating accordingly. However, the service sector was once again able to provide a support."

China's Caixin PMI manufacturing rises to 50.7, back to growth amidst challenges

China's Caixin PMI Manufacturing index climbed from 49.5 to 50.7 in November, surpassing the expected 49.3. According to Caixin's release, this improvement is attributed to sustained rise in total new work, which helped push production back into growth territory. Additionally, there was softer reduction in employment and uptick in business confidence, reaching a four-month high.

Wang Zhe, Senior Economist at Caixin Insight Group, noted, "Overall, the manufacturing sector improved in November." He cited several factors contributing to this improvement: expansion in supply and demand, stable prices, improved logistics, increased purchasing quantities, and a more optimistic outlook among manufacturers. However, he also pointed out some ongoing challenges, such as sluggish external demand, weak employment, and cautious inventory management by manufacturers.

Wang also commented on the broader macroeconomic context, stating, "The macro economy has been recovering." He observed improvements in household consumption, industrial production, and market expectations. Despite these positive signs, he cautioned that both domestic and foreign demand remain insufficient, employment pressures are high, and the economic recovery is still searching for a solid footing.

Japan's PMI manufacturing finalized at 48.3, contraction continues yet optimistic

November saw Japan's Manufacturing PMI finalized at 48.3, a slight decline from October's 48.7. This figure, reported by S&P Global, indicates a continued contraction in the manufacturing sector, with more pronounced decreases in output and new order inflows. The PMI reaching its lowest since February signals a challenging phase for the sector, primarily due to weakened demand both domestically and internationally.

Usamah Bhatti of S&P Global Market Intelligence commented on the sector's performance, noting, "The headline PMI slipped deeper into contraction territory, largely due to quicker deteriorations in output and new order inflows." He identified weak customer demand across both domestic and international markets as key factors behind this downturn.

On the inflation front, although inflationary pressures remained high, there was a noticeable easing. Input cost inflation slowed down to a three-month low, and selling price inflation reduced to its softest since July 2021. This easing in inflation suggests some relief in cost pressures for manufacturers.

Despite the current contraction, Japanese manufacturers are holding onto a sense of optimism for the future. Bhatti emphasized this positive outlook, stating, "Manufacturers remained optimistic that muted demand and production conditions would lift over the coming year." This confidence is underpinned by expectations of a boost in demand, spurred by new product launches, particularly in the semiconductor sector.

RBNZ's Hawkesby highlights inflation pressure from record migration

RBNZ Deputy Governor Christian Hawkesby provided insights into the central bank's current monetary policy and the economic outlook in an interview today. He discussed timing of rate cuts, and impact of rising immigration.

RBNZ's revised forecast does not foresee rate cuts until mid-2025. Explaining the rationale behind the delayed rate cuts, Hawkesby emphasized the need for RBNZ to ensure that inflation expectations are securely re-anchored. He also pointed out that the New Zealand economy had experienced overheating and now requires a period of cooling, marked by a negative output gap.

The interview also highlighted the impact of recent demographic shifts on the The RBNZ had initially perceived rising immigration as a mitigating factor for inflation risk, considering its potential to alleviate labor shortages and reduce wage pressure. However, Hawkesby revealed that the immigration surge has been more significant than anticipated, now contributing to increased demand in the economy.

Hawkesby remarked, "Net migration has peaked at higher levels, so that's news in itself, important news." He further explained that the "demand-side impacts" of this trend are becoming more evident. He added, "The fact you have got to house a bigger population and the impact that that has, particularly on rental inflation and things like that."

New Zealand's population witnessed a substantial increase of 2.7% in the year through September, the largest in over three decades, with net annual immigration reaching a record high of 118,835.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3532; (P) 1.3579; (R1) 1.3606; More...

Intraday bias in USD/CAD remains on the downside at this point. Current fall from 1.3897 is in progress, and should target 1.3378 support next. On the upside, though, above 1.3625 minor resistance will turn intraday bias neutral again first.

In the bigger picture, corrective pattern from 1.3976 (2022 high) should have completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will remain the favored case as long as 1.3378 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Oct | 2.50% | 2.60% | 2.60% | |

| 23:50 | JPY | Capital Spending Q3 | 3.40% | 3.40% | 4.50% | |

| 00:30 | JPY | Manufacturing PMI Nov F | 48.3 | 48.1 | 48.1 | |

| 01:45 | CNY | Caixin Manufacturing PMI Nov | 50.7 | 49.3 | 49.5 | |

| 08:00 | CHF | GDP Q/Q Q3 | 0.30% | 0.10% | 0.00% | -0.10% |

| 08:30 | CHF | Manufacturing PMI Nov | 42.1 | 42 | 40.6 | |

| 08:45 | EUR | Italy Manufacturing PMI Nov | 44.4 | 45.5 | 44.9 | |

| 08:50 | EUR | France Manufacturing PMI Nov F | 42.9 | 42.6 | 42.6 | |

| 08:55 | EUR | Germany Manufacturing PMI Nov F | 42.6 | 42.3 | 42.3 | |

| 09:00 | EUR | Manufacturing PMI Nov F | 44.2 | 43.8 | 43.8 | |

| 09:30 | GBP | Manufacturing PMI Nov F | 47.2 | 46.7 | 46.7 | |

| 13:30 | CAD | Net Change in Employment Nov | 24.9K | 14.2K | 17.5K | |

| 13:30 | CAD | Unemployment Rate Nov | 5.80% | 5.80% | 5.70% | |

| 14:30 | CAD | Manufacturing PMI Nov | 48.6 | |||

| 14:45 | USD | Manufacturing PMI Nov F | 49.4 | 49.4 | ||

| 15:00 | USD | ISM Manufacturing PMI Nov | 47.7 | 46.7 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Nov | 46.2 | 45.1 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Nov | 46.8 | |||

| 15:00 | USD | Construction Spending M/M Oct | 0.40% | 0.40% |

Canada’s employment rises 24.9k in Nov, unemployment rate ticks up to 5.8%

Canada's employment grew 24.9k in November, better than expectation of 14.2k.

Unemployment rate rose from 5.7% to 5.8%, matched expectations, and continuing an upward trend observed since April.

Total hours worked fell -0.7% mom and were up 1.3% on a year-over-year basis.

On a year-over-year basis, average hourly wages rose 4.8%, similar to the increase recorded in October.

EURCAD Technical Analysis – Price Action Forecast and Important Levels to Watch

This article goes over different tools and indicators covering EURCAD, in some cases, cross-pairs can provide trade setups of a different nature as the US Dollar is partially taken out of the equation. Trading in financial markets requires an overview of different types of tools and the same applies to forex trading.

Talking points

- Inflation Rate Overview – European Union and Canada

- Daily Chart Technical analysis

- Sentiment Indicators: Commitment of Traders report, and OANDA’s order book.

- Relative Rotation Graph

Inflation Rate Overview – European Union and Canada

Source: Bloomberg Terminal

Inflation Rates globally are declining faster than expected and as global Central banks continue to tread carefully, traders continue to speculate on Central banks’ moves and are sometimes overwhelmed by conflicting central bankers’ comments or analyst’s opinions. Many Market participants are convinced that the recent decline in inflation suggests that Central banks should consider rate cuts, but Central banks still have concerns about inflation returning in any form.

The latest CPI report from the EU shows inflation continues to decline reaching 2.4%, close to The European Central Bank (ECB) target of 2%. The current CPI may suggest that the ECB can hold interest rates at its current level but doesn’t warrant any rate cuts. ECB Nagel commented this morning that “Inflation risks are skewed to the upside”. The next CPI release is scheduled for December 19th, 2023, please check the economic calendar and your local time. In Canada, it’s a slightly different story, although the inflation rate is also declining the same as it is globally, it is declining at a slower pace than the EU. The inflation rate currently stands at 3.1%, down from its highs of 8.0% seen in June 2022.

Daily Chart Technical analysis

Source: Tradingview.com

- EURCAD price broke and closed below an intermediate trendline identified on the above daily timeframe chart, with no pullback to retest the broken level so far. The broken level was also a confluence of Support represented by 3 commonly used Moving average periods, EMA9, MA,9, MA21, and the monthly pivot point at 1.4800

- Applying the weekly Stochastic indicator onto the Daily timeframe to smooth the readings suggests that EURCAD may be overbought and shows that %K just crossed below %D along with the break below the intermediate trendline mentioned above.

- Applying Daily RSI with its default period of 14 shows that RSI is so far in line with price action, however, it is currently neutral near level 50.

- MACD line crossed below its signal line and the Histogram is also turning bearish.

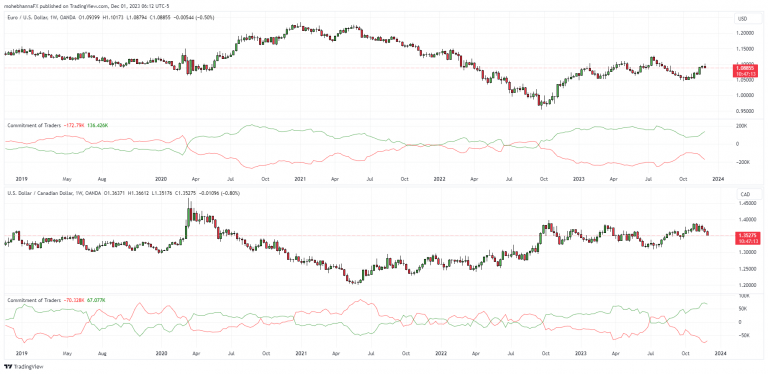

Sentiment Indicators: Commitment of Traders report, and OANDA’s order book.

COT Report

Source: Tradingview.com

The Commitment of Traders report offers insights about positioning changes in the futures market, although delayed, it still helps as a sentiment tool in a trader’s arsenal. Comparing Position levels on the latest COT report shows that Large Speculators on both currencies are favoring long positions, however, it also suggests that the Canadian Dollar is closer to its extreme than the Euro, thus a higher probability of Sentiment change. The above chart is for EURUSD and USDCAD side by side with the COT report applied to both. (COT for Canadian Dollar is inverted, CADUSD)

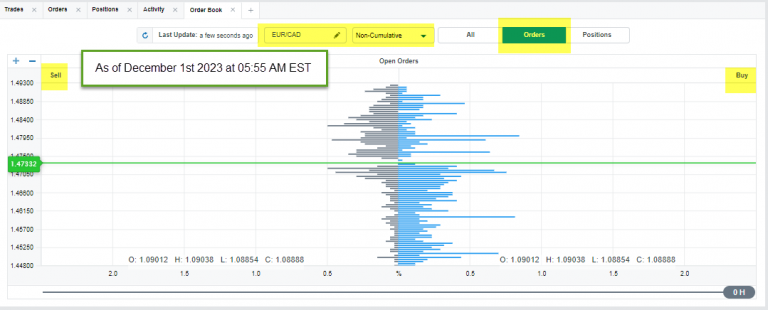

OANDA’s Orderbook Indicator

Source: OANDA.com

Another sentiment tool is the OANDA Orderbook Indicator, the above image reflects an aggregate view of pending entry orders on EURCAD for OANDA’s clients, the data falls under the Retail Traders category. The above image suggests that Retail traders are looking to buy as the price falls and sell as it rises, this is the typical retail trader sentiment and needs to be thought of carefully as Retail Traders can sometimes be in the opposite direction in trendy markets. The order book also reflects price levels that have the highest number of pending orders, these levels can be critical as the price continues to move regardless of direction. It is also important to note that the order book percentages include exit orders such as Stops and limits, we can continue to follow up on position percentage changes.

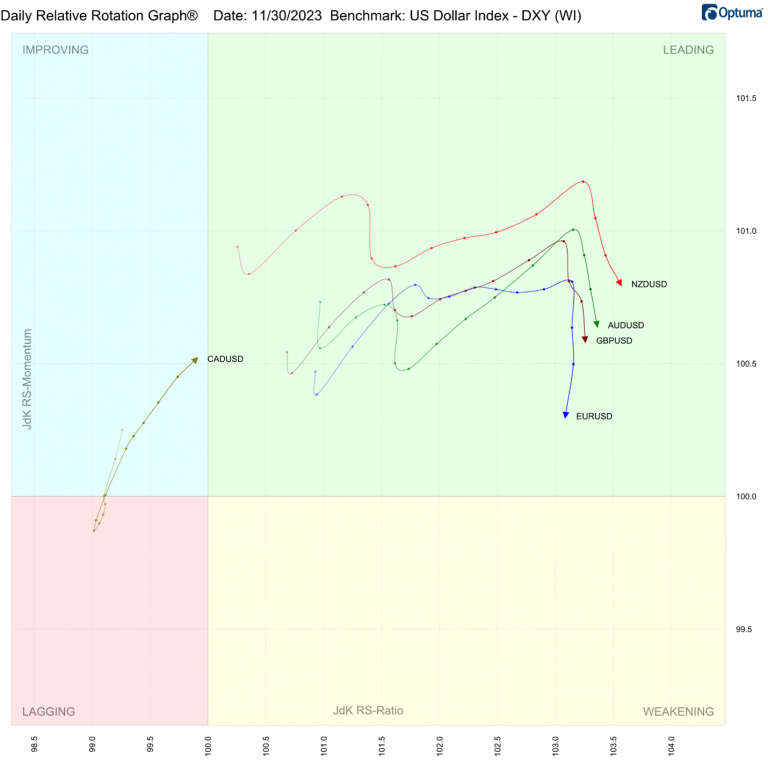

Relative Rotation Graph

Source: Optuma.com

The Relative Rotation graph RRG (A measurement for Momentum and Relative strength) on the daily time frame shows EURUSD, GBPUSD, AUDUSD, and NZDUSD are currently in the Leading Quadrant, with EURUSD leading the pack and CADUSD attempting to catch up from the Improving quadrant. The arrow direction for all pairs except CAD is so far pointing south towards the weakening quadrant.

Crude Oil Can Resume to 70-72 Support

On a daily chart, we see a drop in crude oil from 130 area as a five-wave move within wave A that bottomed at 62 - 57 support area. It was a strong drop and spike back in May, when energy bottomed, so we are tracking a higher degree correction from there; wave (B), which can be much higher than firstly thought; there can be room for 100. And the reason is a strong bullish trend back in September, which is looking impulsive, labeled as completed A, so be aware of more gains after current deep set-back in B is completed.

Looking at the 4h time frame (right) oil is coming down despite OPEC that can be trying to stabilize the prices after countries agrees to deepen voluntary oil output cuts down to 70-72 area as recent bounce to 79/80 resistance unfolded as subwave (4). If we are correct, then there can still be some itneresting bounce-back later this month.

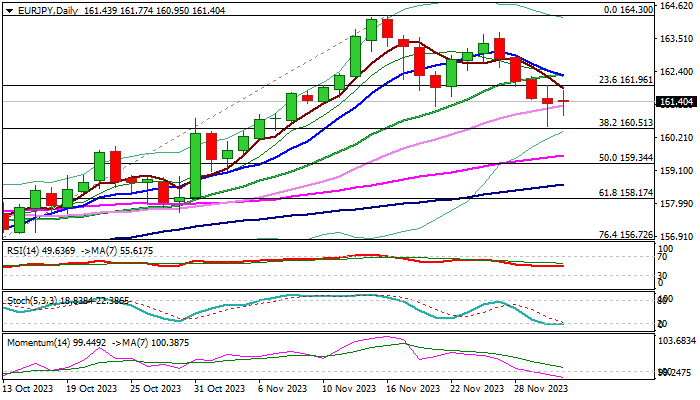

EUR/JPY: Completion of Failure Swing Pattern to Signal Deeper Pullback

EURJPY remains in red and holding near three-week low on Friday, on track for the first weekly loss in five week and the biggest drop since the second week of March.

Initial signal of larger rally stall was also generated by November’s monthly Doji with long upper shadow and overbought conditions on monthly chart.

Daily studies already turned bearish as 14-d momentum moved into negative territory and double bear-cross (5/20 and 10/20DMA) formed on daily chart.

However, fresh bears still look for confirmation of failure swing pattern on daily chart, as pullback faced headwinds on approach to pivotal Fibo support at 160.51 (38.2% of 154.38/164.30 bull-leg) which resulted in a second daily Doji candle, signaling indecision.

Firm break of 160.51 to confirm bearish near-term stance for extension through 160 (psychological) towards 159.34 (50% retracement of 154.38/164.30).

Daily Tenkan-sen (162.15) marks upper pivot and break higher would sideline near-term bears.

Res: 161.96; 162.15; 162.44; 162.88.

Sup: 161.00; 160.51; 160.00; 159.61.