Sample Category Title

EUR/GBP Weekly Outlook

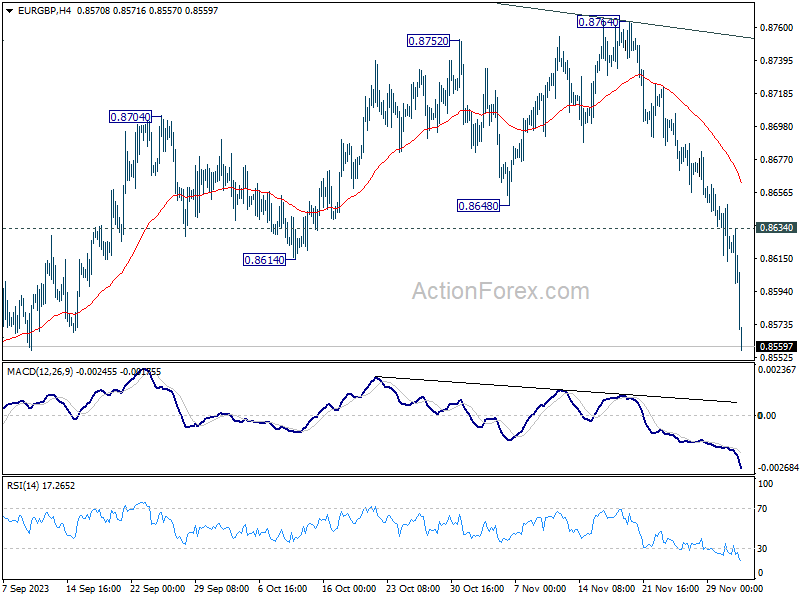

EUR/GBP's fall from 0.8764 accelerated to as low as 0.8557 last week. The development suggests that rebound from 0.8491 has completed as a corrective move at 0.8764. Initial bias stays on the downside this week for retesting 0.8491 low first. Firm break there will resume larger down trend. On the upside, touching 0.8634 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, current development suggests that down trend from 0.9267 (2022 high) is still in progress. This decline is now seen as the third leg of the pattern from 0.9499 (2020 high). Break of 0.8201 will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969. In any case, outlook will stay bearish as long as 0.8764 resistance holds.

In the long term picture, long term range pattern from 0.9799 (2008 high) is extending, and is set to continue until further development.

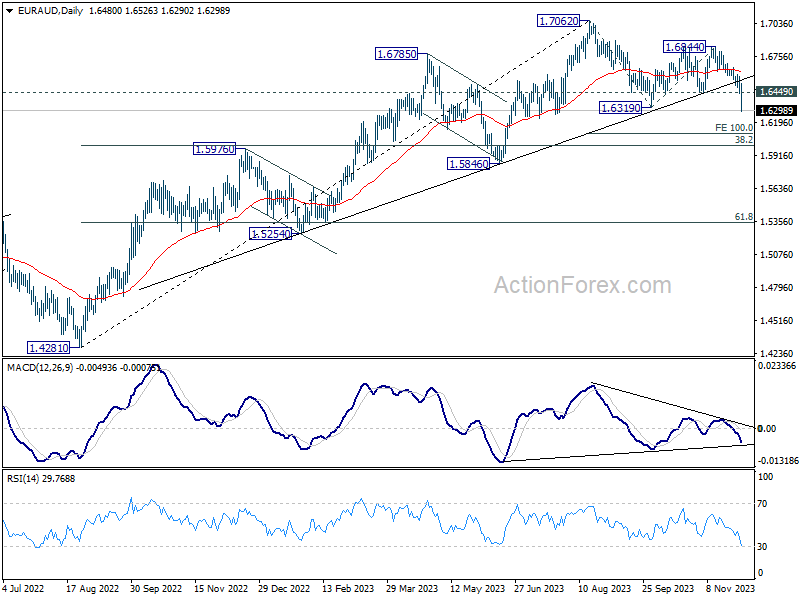

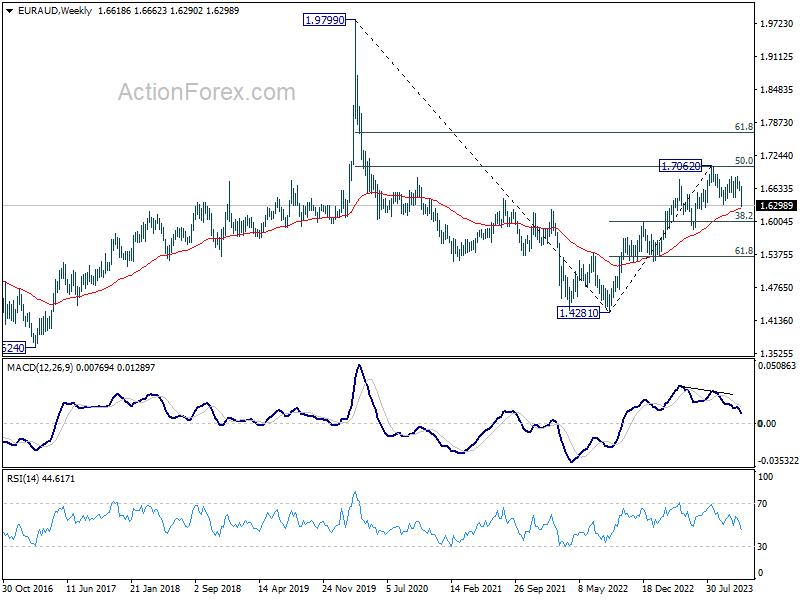

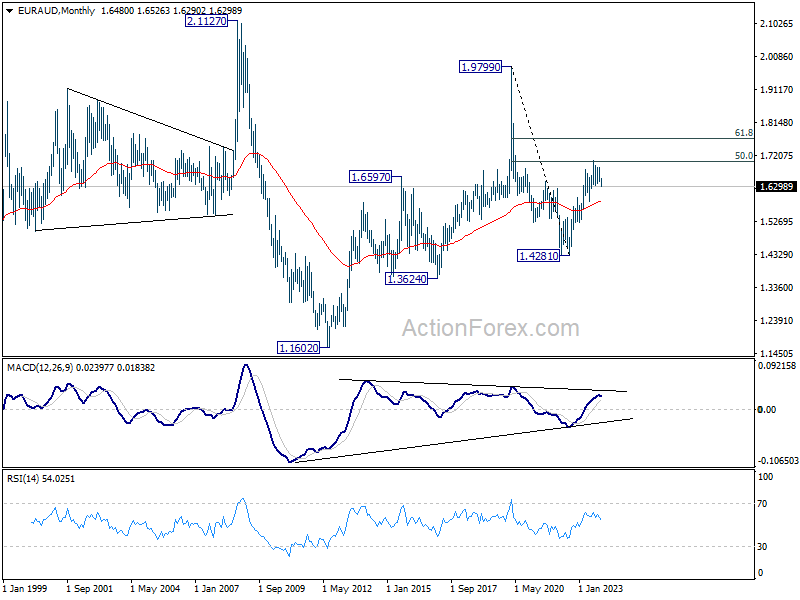

EUR/AUD Weekly Outlook

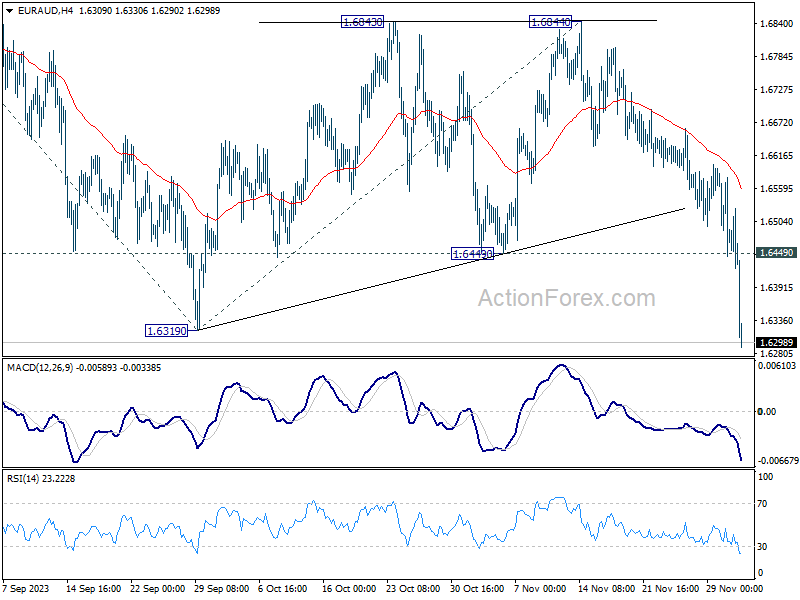

EUR/AUD's decline from 1.7062 resumed by diving through 1.6319 support last week. Initial bias stays on the downside this week for 100% projection of 1.7062 to 1.6319 from 1.6844 at 1.6106 next. On the upside, above 1.6649 resistance will turn intraday bias and bring consolidations first, before staging another decline.

In the bigger picture, the break of medium term trend line support now suggests fall from 1.7062 correcting the whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound on first attempt. But risk will stay on the downside as long as 1.6844 resistance holds. Sustained break of 1.6000 would bring further fall to 61.8% retracement at 1.5343.

In the longer term picture, fall from 1.9799 (2020 high) is seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5846) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

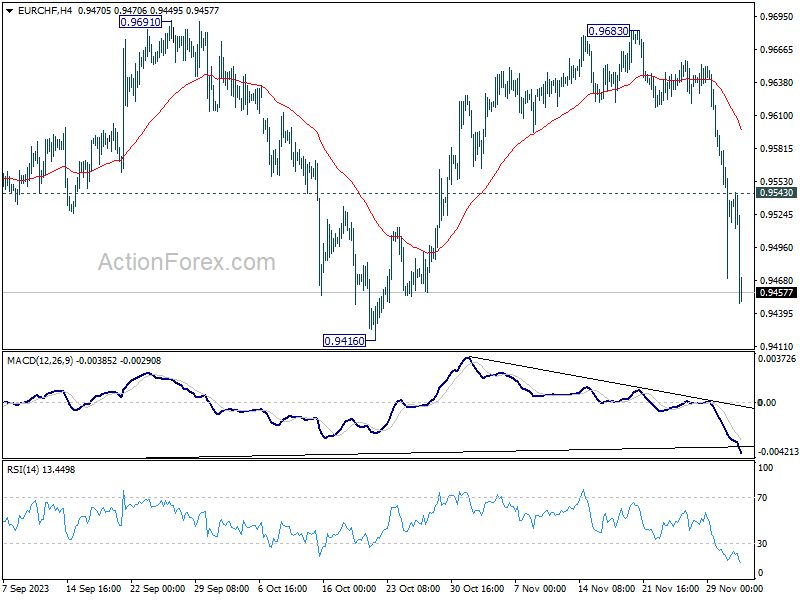

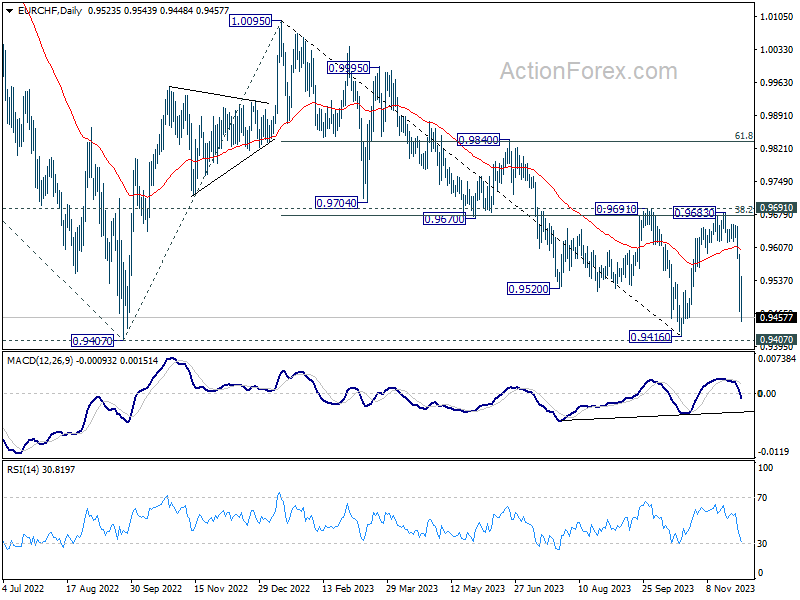

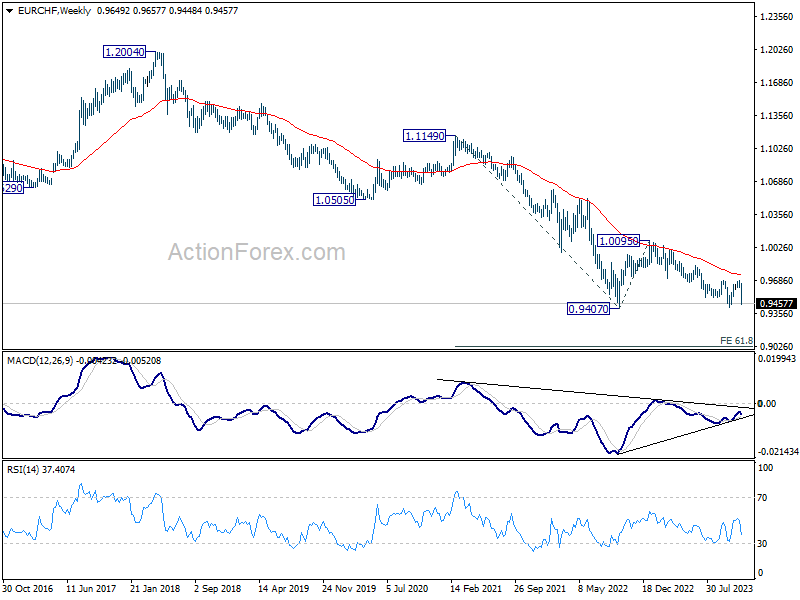

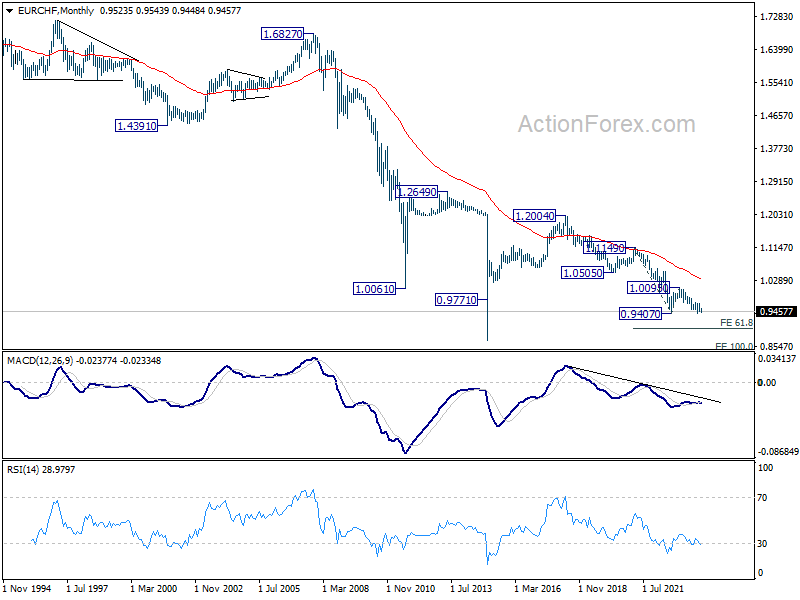

EUR/CHF Weekly Outlook

EUR/CHF's steep decline last week indicates that rebound from 0.9416 has completed at 0.9683 already, after rejection by 0.9691 cluster resistance. Initial bias stays on the downside this week for retesting 0.9407/16 support zone. Decisive break there will resume larger down trend. On the upside, touching 0.9543 minor resistance will delay the bearish case and turn intraday bias neutral first.

In the bigger picture, rejection by 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) maintains medium term bearishness in EUR/CHF. Firm break of 0.9047 support (2022 low) will resume long term down trend. Next target will be 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, outlook will be neutral at best as long as 0.9683 holds.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0306). Larger down trend from 1.2004 (2018 high) is in progress to break through 0.9407 low.

Summary 12/4 – 12/8

Monday, Dec 4, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q3 | -2.10% | 0.40% |

| 23:50 | JPY | Monetary Base Y/Y Nov | 9.50% | 9.00% |

| 00:00 | AUD | TD Securities Inflation M/M Nov | -0.10% | |

| 07:00 | EUR | Germany Trade Balance (EUR) Oct | 17.0B | 16.5B |

| 07:30 | CHF | CPI M/M Nov | -0.10% | 0.10% |

| 07:30 | CHF | CPI Y/Y Nov | 1.60% | 1.70% |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | -16 | -18.6 |

| 15:00 | USD | Factory Orders M/M Oct | -2.50% | 2.80% |

| 23:30 | JPY | Tokyo CPI Y/Y Nov | 3.30% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Nov | 2.40% | 2.70% |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Nov | 3.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q3 | |

| Forecast: -2.10% | Previous: 0.40% | ||

| 23:50 | JPY | Monetary Base Y/Y Nov | |

| Forecast: 9.50% | Previous: 9.00% | ||

| 00:00 | AUD | TD Securities Inflation M/M Nov | |

| Forecast: | Previous: -0.10% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Oct | |

| Forecast: 17.0B | Previous: 16.5B | ||

| 07:30 | CHF | CPI M/M Nov | |

| Forecast: -0.10% | Previous: 0.10% | ||

| 07:30 | CHF | CPI Y/Y Nov | |

| Forecast: 1.60% | Previous: 1.70% | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | |

| Forecast: -16 | Previous: -18.6 | ||

| 15:00 | USD | Factory Orders M/M Oct | |

| Forecast: -2.50% | Previous: 2.80% | ||

| 23:30 | JPY | Tokyo CPI Y/Y Nov | |

| Forecast: | Previous: 3.30% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Nov | |

| Forecast: 2.40% | Previous: 2.70% | ||

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Nov | |

| Forecast: | Previous: 3.80% | ||

Tuesday, Dec 5, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Current Account (AUD) Q3 | 3.5B | 7.7B |

| 01:45 | CNY | Caixin Services PMI Nov | 50.8 | 50.4 |

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% |

| 07:45 | EUR | France Industrial Output M/M Oct | -0.20% | -0.50% |

| 08:45 | EUR | Italy Services PMI Nov | 48.2 | 47.7 |

| 08:50 | EUR | France Services PMI Nov F | 45.3 | 45.3 |

| 08:55 | EUR | Germany Services PMI Nov F | 48.7 | 48.7 |

| 09:00 | EUR | Eurozone Services PMI Nov F | 48.2 | 48.2 |

| 09:30 | GBP | Services PMI Nov F | 50.5 | 50.5 |

| 10:00 | EUR | Eurozone PPI M/M Oct | 0.20% | 0.50% |

| 10:00 | EUR | Eurozone PPI Y/Y Oct | -9.40% | -12.40% |

| 14:45 | USD | Services PMI Nov F | 50.8 | 50.8 |

| 15:00 | USD | ISM Services PMI Nov | 52.6 | 51.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Current Account (AUD) Q3 | |

| Forecast: 3.5B | Previous: 7.7B | ||

| 01:45 | CNY | Caixin Services PMI Nov | |

| Forecast: 50.8 | Previous: 50.4 | ||

| 03:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 4.35% | Previous: 4.35% | ||

| 07:45 | EUR | France Industrial Output M/M Oct | |

| Forecast: -0.20% | Previous: -0.50% | ||

| 08:45 | EUR | Italy Services PMI Nov | |

| Forecast: 48.2 | Previous: 47.7 | ||

| 08:50 | EUR | France Services PMI Nov F | |

| Forecast: 45.3 | Previous: 45.3 | ||

| 08:55 | EUR | Germany Services PMI Nov F | |

| Forecast: 48.7 | Previous: 48.7 | ||

| 09:00 | EUR | Eurozone Services PMI Nov F | |

| Forecast: 48.2 | Previous: 48.2 | ||

| 09:30 | GBP | Services PMI Nov F | |

| Forecast: 50.5 | Previous: 50.5 | ||

| 10:00 | EUR | Eurozone PPI M/M Oct | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Oct | |

| Forecast: -9.40% | Previous: -12.40% | ||

| 14:45 | USD | Services PMI Nov F | |

| Forecast: 50.8 | Previous: 50.8 | ||

| 15:00 | USD | ISM Services PMI Nov | |

| Forecast: 52.6 | Previous: 51.8 | ||

Wednesday, Dec 6, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | 0.40% | 0.40% |

| 07:00 | EUR | Germany Factory Orders M/M Oct | 0.50% | 0.20% |

| 09:30 | GBP | Construction PMI Nov | 47.1 | 45.6 |

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | 0.20% | -0.30% |

| 13:15 | USD | ADP Employment Change Nov | 120K | 113K |

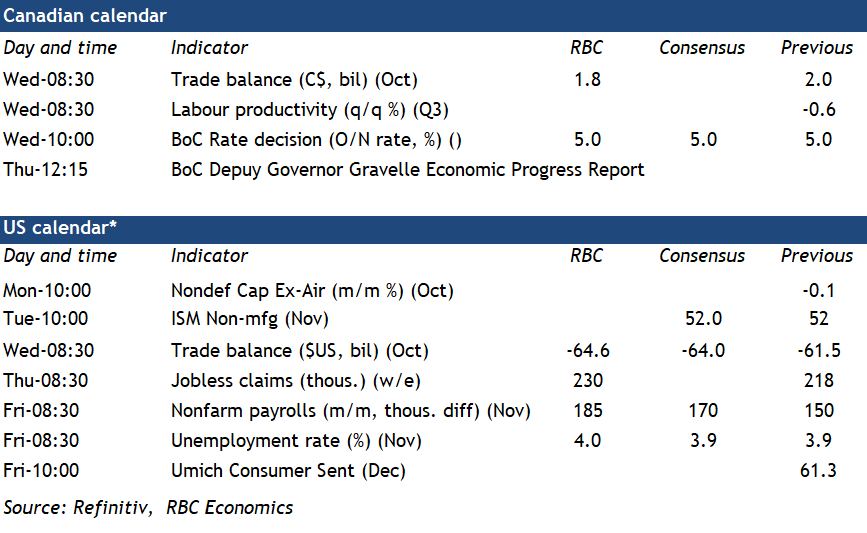

| 13:30 | CAD | Labor Productivity Q/Q Q3 | 0.20% | -0.60% |

| 13:30 | CAD | Trade Balance (CAD) Oct | 2.0B | |

| 13:30 | USD | Trade Balance (USD) Oct | -63.0B | -61.5B |

| 13:30 | USD | Nonfarm Productivity Q3 | 4.70% | 4.70% |

| 13:30 | USD | Unit Labor Costs Q3 | -0.80% | -0.80% |

| 15:00 | CAD | BoC Rate Decision | 5.00% | 5.00% |

| 15:00 | CAD | Ivey PMI Nov | 54.2 | 53.4 |

| 15:30 | USD | Crude Oil Inventories | 1.6M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 07:00 | EUR | Germany Factory Orders M/M Oct | |

| Forecast: 0.50% | Previous: 0.20% | ||

| 09:30 | GBP | Construction PMI Nov | |

| Forecast: 47.1 | Previous: 45.6 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 13:15 | USD | ADP Employment Change Nov | |

| Forecast: 120K | Previous: 113K | ||

| 13:30 | CAD | Labor Productivity Q/Q Q3 | |

| Forecast: 0.20% | Previous: -0.60% | ||

| 13:30 | CAD | Trade Balance (CAD) Oct | |

| Forecast: | Previous: 2.0B | ||

| 13:30 | USD | Trade Balance (USD) Oct | |

| Forecast: -63.0B | Previous: -61.5B | ||

| 13:30 | USD | Nonfarm Productivity Q3 | |

| Forecast: 4.70% | Previous: 4.70% | ||

| 13:30 | USD | Unit Labor Costs Q3 | |

| Forecast: -0.80% | Previous: -0.80% | ||

| 15:00 | CAD | BoC Rate Decision | |

| Forecast: 5.00% | Previous: 5.00% | ||

| 15:00 | CAD | Ivey PMI Nov | |

| Forecast: 54.2 | Previous: 53.4 | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 1.6M | ||

Thursday, Dec 7, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Oct | 7.45B | 6.79B |

| 03:00 | CNY | Trade Balance (USD) Nov | 48.6B | 56.5B |

| 05:00 | JPY | Leading Economic Index Oct P | 108.2 | |

| 07:00 | EUR | Germany Industrial Production M/M Oct | -0.20% | -1.40% |

| 07:45 | EUR | France Trade Balance (EUR) Oct | -8.5B | -8.9B |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Nov | 658B | |

| 09:00 | EUR | Italy Industrial Output M/M Oct | -0.60% | 0.00% |

| 10:00 | EUR | Italy Retail Sales M/M Oct | 0.10% | -0.30% |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 | -0.10% | -0.10% |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 F | 0.30% | 0.30% |

| 12:30 | USD | Challenger Job Cuts Nov | 8.80% | |

| 13:30 | USD | Initial Jobless Claims (Dec 1) | 226K | 218K |

| 13:30 | CAD | Building Permits M/M Oct | -6.50% | |

| 15:00 | USD | Wholesale Inventories Oct | -0.20% | -0.20% |

| 15:30 | USD | Natural Gas Storage | 10B | |

| 21:45 | NZD | Manufacturing Sales Q3 | 0.20% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | 1.00% | 1.20% |

| 23:30 | JPY | Overall Household Spending Y/Y Oct | -3.00% | -2.80% |

| 23:50 | JPY | Bank Lending Y/Y Nov | 2.80% | 2.80% |

| 23:50 | JPY | GDP Q/Q Q3 F | -0.50% | -0.50% |

| 23:50 | JPY | GDP Deflator Y/Y Q3 | 5.10% | 5.10% |

| 23:50 | JPY | Current Account (JPY) Oct | 1.85T | 2.01T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Oct | |

| Forecast: 7.45B | Previous: 6.79B | ||

| 03:00 | CNY | Trade Balance (USD) Nov | |

| Forecast: 48.6B | Previous: 56.5B | ||

| 05:00 | JPY | Leading Economic Index Oct P | |

| Forecast: | Previous: 108.2 | ||

| 07:00 | EUR | Germany Industrial Production M/M Oct | |

| Forecast: -0.20% | Previous: -1.40% | ||

| 07:45 | EUR | France Trade Balance (EUR) Oct | |

| Forecast: -8.5B | Previous: -8.9B | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Nov | |

| Forecast: | Previous: 658B | ||

| 09:00 | EUR | Italy Industrial Output M/M Oct | |

| Forecast: -0.60% | Previous: 0.00% | ||

| 10:00 | EUR | Italy Retail Sales M/M Oct | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 F | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | USD | Challenger Job Cuts Nov | |

| Forecast: | Previous: 8.80% | ||

| 13:30 | USD | Initial Jobless Claims (Dec 1) | |

| Forecast: 226K | Previous: 218K | ||

| 13:30 | CAD | Building Permits M/M Oct | |

| Forecast: | Previous: -6.50% | ||

| 15:00 | USD | Wholesale Inventories Oct | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 10B | ||

| 21:45 | NZD | Manufacturing Sales Q3 | |

| Forecast: | Previous: 0.20% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | |

| Forecast: 1.00% | Previous: 1.20% | ||

| 23:30 | JPY | Overall Household Spending Y/Y Oct | |

| Forecast: -3.00% | Previous: -2.80% | ||

| 23:50 | JPY | Bank Lending Y/Y Nov | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 23:50 | JPY | GDP Q/Q Q3 F | |

| Forecast: -0.50% | Previous: -0.50% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q3 | |

| Forecast: 5.10% | Previous: 5.10% | ||

| 23:50 | JPY | Current Account (JPY) Oct | |

| Forecast: 1.85T | Previous: 2.01T | ||

Friday, Dec 8, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Eco Watchers Survey: Current Nov | 49.2 | 49.5 |

| 07:00 | EUR | Germany CPI Y/Y Nov F | 3.20% | 3.20% |

| 07:00 | EUR | Germany CPI M/M Nov F | -0.40% | -0.40% |

| 09:30 | GBP | Consumer Inflation Expectations | 3.60% | |

| 13:30 | CAD | Capacity Utilization Q3 | 81.40% | |

| 13:30 | USD | Nonfarm Payrolls Nov | 190K | 150K |

| 13:30 | USD | Unemployment Rate Nov | 3.90% | 3.90% |

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.30% | 0.20% |

| 15:00 | USD | Michigan Consumer Sentiment Index Dec P | 61.7 | 61.3 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Eco Watchers Survey: Current Nov | |

| Forecast: 49.2 | Previous: 49.5 | ||

| 07:00 | EUR | Germany CPI Y/Y Nov F | |

| Forecast: 3.20% | Previous: 3.20% | ||

| 07:00 | EUR | Germany CPI M/M Nov F | |

| Forecast: -0.40% | Previous: -0.40% | ||

| 09:30 | GBP | Consumer Inflation Expectations | |

| Forecast: | Previous: 3.60% | ||

| 13:30 | CAD | Capacity Utilization Q3 | |

| Forecast: | Previous: 81.40% | ||

| 13:30 | USD | Nonfarm Payrolls Nov | |

| Forecast: 190K | Previous: 150K | ||

| 13:30 | USD | Unemployment Rate Nov | |

| Forecast: 3.90% | Previous: 3.90% | ||

| 13:30 | USD | Average Hourly Earnings M/M Nov | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Dec P | |

| Forecast: 61.7 | Previous: 61.3 | ||

The Weekly Bottom Line: Moving Toward Target

U.S. Highlights

- A second reading on U.S. GDP showed that the economy expanded by an even more impressive 5.2% (annualized) last quarter, a 0.3 percentage point upgrade from the initial reading. Government spending and business investment were revised up, but consumer spending was revised down slightly.

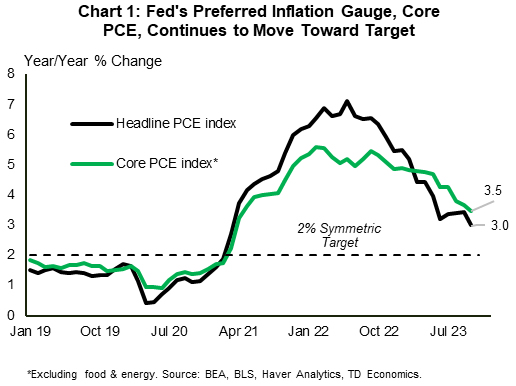

- October’s real consumer spending data showed that growth eased at the start of the fourth quarter. Core PCE inflation, the Fed’s preferred measure, also cooled to 3.5% year-on-year from 3.7% in September.

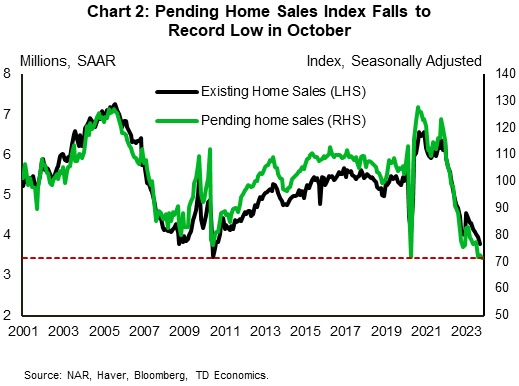

- The National Association of Realtors pending home sales index fell to a record low in October.

Canadian Highlights

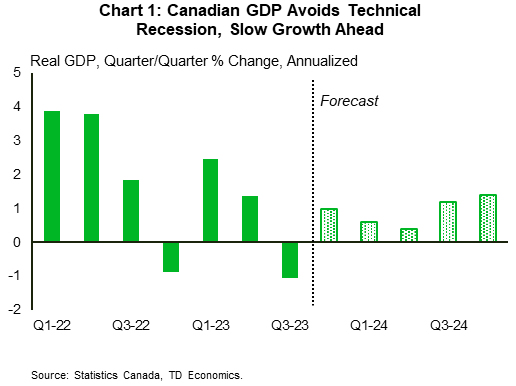

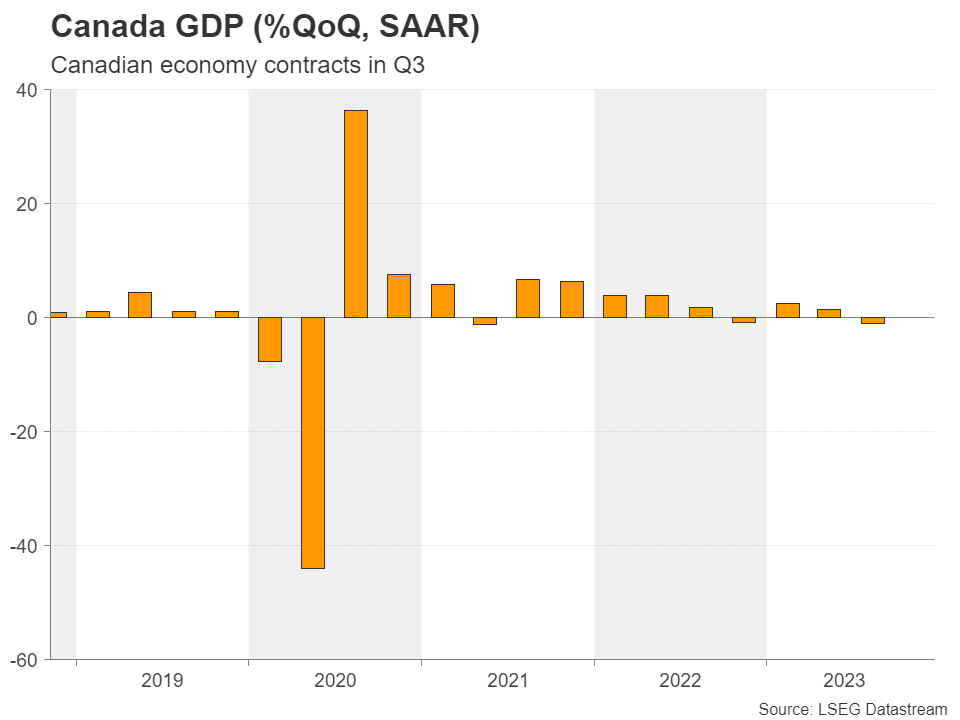

- Canada has avoided a technical recession. The contraction in Q3 GDP growth was offset by large upward revisions to the quarter prior that brought output back into positive territory.

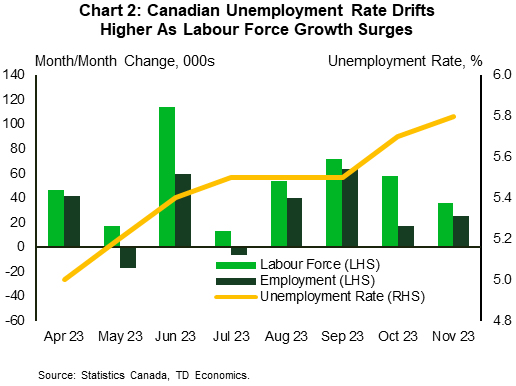

- Canada’s labour market continued to add jobs in November, but robust labour force growth lifted the unemployment rate higher.

- It is still too early for the Bank of Canada (BoC) to hint at interest rate cuts at its rate decision next week, but it’s becoming increasingly evident that further rate hikes are not necessary.

U.S. – Moving Toward Target

The U.S. economy grew at an even better pace than initially reported in the third quarter. But, a moderation in consumer spending in October coupled with some progress on the inflation front, reinforced market expectations that the Fed has likely reached the end of its tightening cycle. That said, Fed speak out this week was somewhat mixed, with some suggesting that today’s policy rate is sufficiently restrictive while others still feel it’s too early to call it quits. In his speech on Friday, Chair Powell called talk of cutting rates ‘premature’.

The second reading on U.S. GDP showed that the economy grew by 5.2% (annualized) last quarter, an upgrade of 0.3 percentage points from the initial reading. The upward revision reflects improvements in government spending and fixed investment. One major category going against the grain was consumer spending, which was revised slightly lower to 3.6% from 4% previously. Stepping into the fourth quarter, the personal income and outlays report, added another layer of moderation for the consumer. Nominal spending rose 0.2% month-over-month (m/m) in October, a deceleration from 0.7% in September. The spending slowdown was less pronounced on an inflation-adjusted basis, with growth easing to 0.2% from 0.3% in the month prior.

Given a reduction in credit availability and the drawdown of pandemic era ‘excess savings’, the American consumer will have to rely more closely on income growth to fund its spending. As such, any softness on the labor market should filter through to weaker spending. Peeking into the labor market, continuing jobless claims rose to 1.93 million in mid-November. This is the highest level since late 2021 and an added sign that the labor market is gradually cooling. Overall, we expect consumer spending to remain buoyant over the holiday period, but the momentum is likely to fade, with consumption growth likely to slow to around 2% this quarter.

The monthly personal income and outlays report also carried some good news on the inflation front. The highlight was a continued deceleration in core PCE – the Fed’s preferred inflation gauge – which slowed to 3.5% year-on-year in October from 3.7% in the month prior (Chart 1). Interest rates have eased alongside this continued progress toward the Fed’s 2% target, and so have mortgage rates. The 30-year mortgage rate is currently hovering near 7.2% – some 80 basis points lower than the 8% peak in mid-October. This pullback appears to be providing some relief on housing, with mortgage purchase applications ticking higher for the fourth week in a row last week. But, the impact of interest rates tends to be felt with a lag, so this will take some time to be manifested in sales activity. To that end, pending home sales fell to an all-time low in October, indicating that things are likely to get worse before they get better (Chart 2).

All in all, higher interest rates are working as intended with inflation gradually easing toward target, but the Fed can’t let its guard down prematurely and is likely to maintain a hawkish tone until it is convinced that the inflation is decisively moving back towards 2%.

Canada – Revisions, Surprises, and a Sprinkle of Jobs

The banner news for the week is that Canada isn't in a recession. The potential for such a scenario was a growing narrative before updated real GDP figures extinguished that possibility. GDP for the third quarter did in fact surprise to the downside, contracting by an annualized 1.1%. But, strong upward revisions to the second quarter brought output back into positive territory keeping Canada out of a technical recession.

Although Canada isn't in a recession, it is showing weakness, and the risk to growth cannot be dismissed heading into next year. The decline in real GDP growth for the third quarter was primarily driven by external factors, as net exports and slow inventory accumulation accounted for most of the drag. Final domestic demand, a better measure of domestic economic health, continued to grow at a robust pace.

Monthly industry-based GDP provided a first reading on how the fourth quarter is shaping up. Guidance for October points to output advancing at a moderate pace, piggybacking off September's slight, but above-consensus gain. This puts early Q4 growth tracking positive, but still in below-trend territory. The next few months will hopefully provide cleaner readings of GDP now that the host of one-off shocks that created choppiness over the last six-months dissipates. For now, chatter around Canada already being in a recession should quiet, but we expect GDP growth to hum along at below trend-pace for the better part of 2024 (Chart 1).

The Canadian labour market is also slowing, but hasn't fully ceded its strength. Canada added another 25k jobs in November, pulling the three-month trend in job gains slightly downward. The unemployment rate, however, has moved up eight-tenths since April, as labour force gains continue outpace employment. The labour market is holding up relatively well at this point in the cycle, but the Bank of Canada (BoC) likely wants to see the market move further into balance. Notably, wage gains are still robust, potentially fanning future inflation fears and vacancies, while declining, remain at elevated levels.

Developments this week support our forecast that the Bank of Canada (BoC) is done with rate hikes. However, it is too early for the BoC to lean too dovish at next week's meeting and say anything about rate cuts or their timing. The Bank will likely need to see inflation, especially core measures, move durably lower before they move off their bias towards rate hikes. Markets have priced the possibility of a first rate cut to occur around April–in line with our own view. Rest assured, the BoC's most aggressive rate hike campaign in over 40 years is working. Consumers are reeling in their spending, labour markets are returning to balance, and growth is evolving in a manner consistent with inflation inching closer to the BoC's 2% target. Whether it's a hard, soft, or bumpy landing is still yet to be seen, but the Air-Canad(ian economy) plane is getting closer to the runway.

Weekly Economic & Financial Commentary: Inflation Takes Another Leg Lower

Summary

United States: Inflation Takes Another Leg Lower

- The U.S. data this week signaled that the economic expansion remains intact even as inflation continues to slow. The year-ago rates of headline and core PCE inflation were the lowest since March 2021 and April 2021, respectively.

Next week: ISM Services (Tue.), Employment (Fri.), Consumer Sentiment (Fri.)

International: Mixed News on the International Economic Front

- Eurozone inflation slowed more than expected in November, and Canada's Q3 GDP unexpectedly declined, while the Reserve Bank of New Zealand held interest rates steady but offered hawkish policy guidance. China's manufacturing and services PMIs both slipped in November, while India's Q3 GDP advanced at a solid pace.

- Next week: Australia Policy Rate (Tue.), Mexico CPI (Thu.), India Policy Rate (Fri.)

Credit Market Insights: Credit Check: Is It Time to Worry About Credit Card Debt?

- After paying off credit card debt during the COVID lockdown period, households have levered up at a pace seven times as fast as they did in the prior cycle. Credit card delinquencies are starting to tick higher as well amid the highest average annual percentage rate on credit card debt in data going back to the early 1980s. So, is it time to start worrying about credit card debt?

Topic of the Week: Something in the Beige Tells Me We're Almost Done

- The blistering pace of growth in the third quarter is on track to cool in the final months of the year. That is the takeaway from contacts across the 12 Federal Reserve Districts who noted slowing economic activity since early October in the final Beige Book of this year.

BoC to Deliver ‘Dovish Hold’ Next Week

Next week’s Bank of Canada interest rate decision itself is unlikely to be a surprise. The BoC is widely expected to hold the overnight rate steady at 5% for the third meeting in a row. But the statement will be watched closely for signs that a slowing economy and easing inflation pressures are shifting future interest rate cuts into focus.

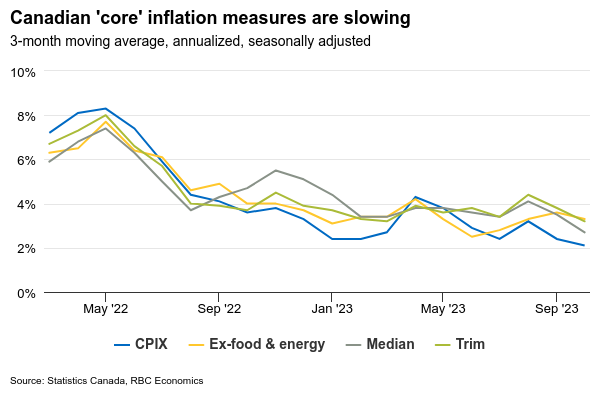

The BoC will remain mindful of inflationary risks and retain the option to move interest rate higher. But we don’t see that as likely to be necessary. Canadian inflation data has looked decidedly better . Headline CPI growth at 3.1% (year-over-year) in October was just a touch above the top end of BoC’s 1%-3% inflation target range. The Bank’s current preferred “core” inflation measures have also showed improvements – the ‘old’ CPIX core measure (which excludes mortgage interest costs along with 7 other volatile price components) has slowed to 2.8% year-over-year and an annualized 2.1% over the last three months. Moving forward, sluggish economic data should reinforce that slowing price pressures will persist. That includes a sizable downside surprise in Q3 GDP growth (-1.1% q/q annualized relative to -0.5% expected by RBC and +0.8% expected by the BoC) and softening labour market conditions with the unemployment rate rising to 5.8% in November from 5% earlier in spring.

With evidence building that the economy is softening, focus has shifted from whether additional interest rate hikes will be needed to how long before the first cuts. While we’re expecting a dovish lean from the BoC relative to past interest rate decisions, and Governor Macklem himself has said that past rate hikes may have been enough to slow inflation to target, we don’t see the BoC rushing to cutting rates. Lower inflation prints over the late fall were welcome but followed a string of “sticky” core inflation readings. We expect the BoC will stay on hold through the first half of 2024 before moving to rate cuts in Q3 next year.

Week ahead data watch

November’s U.S. employment report likely revealed more softness in the labour market. We expect the unemployment rate to tick up again (+0.1%) in November to reach 4%. Employment likely grew by 185K, slightly higher than the 150K in the prior month but with return of workers from the UAW strike accounting for 30K workers of that gain. Broadly speaking, we expect labour demand will continue to slow, and for that to ease wage pressures further.

The Canadian trade surplus likely narrowed in October, given oil prices (-4.3%) were lower during that month, resulting a negative trade balance in the energy sector. September saw a large pullback in exports of metal and non-metallic mineral products, reversing part of the strength in that component in August.

Advance indicators showed the U.S. goods deficit likely widened by $3B in October, led by lower exports of consumer (-9.1%) and auto goods (-7.3%). Imports went up for capital goods (2.5%) during that month.

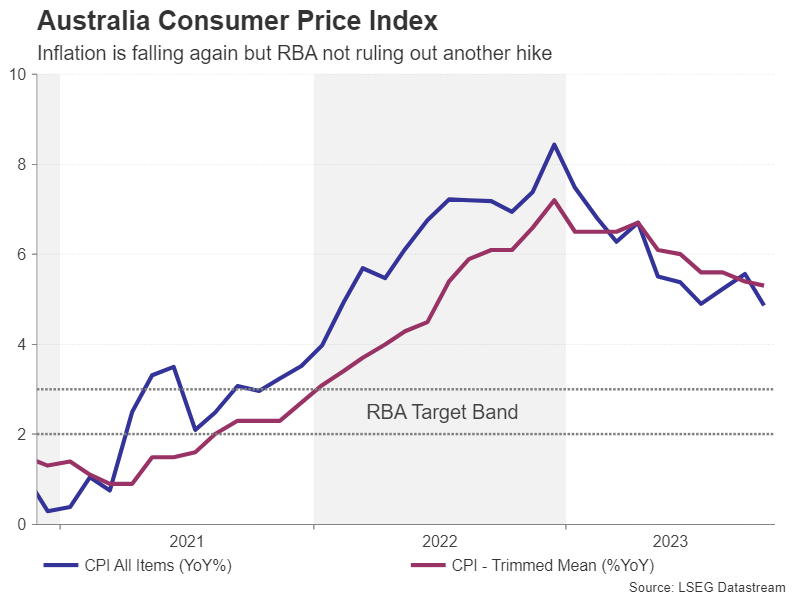

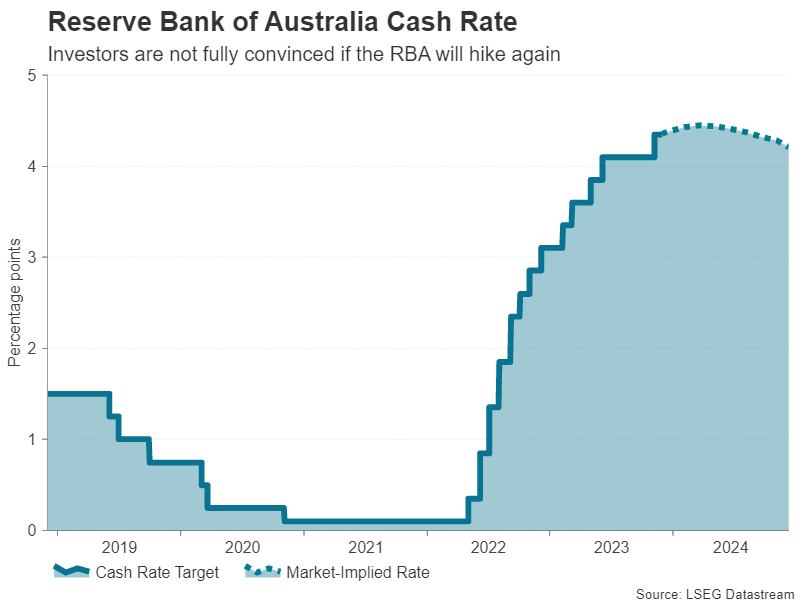

Will RBA Maintain Tightening Bias After CPI Miss?

- RBA is expected to hold rates in December after hiking last month

- But will it signal future hikes or will it turn more cautious?

- After soft CPI, RBA’s decision on Tuesday, 3:30 GMT, poses a risk for the aussie

New governor has been beating the hawkish drum

The Australian economy has been gradually losing steam all year and GDP data due on December 6 is likely to show that growth slowed further in the third quarter. Rising borrowing costs for households and businesses, combined with the patchy recovery in China, were a major factor why former RBA Governor Philip Lowe was more comfortable to stand pat than his successor Michele Bullock.

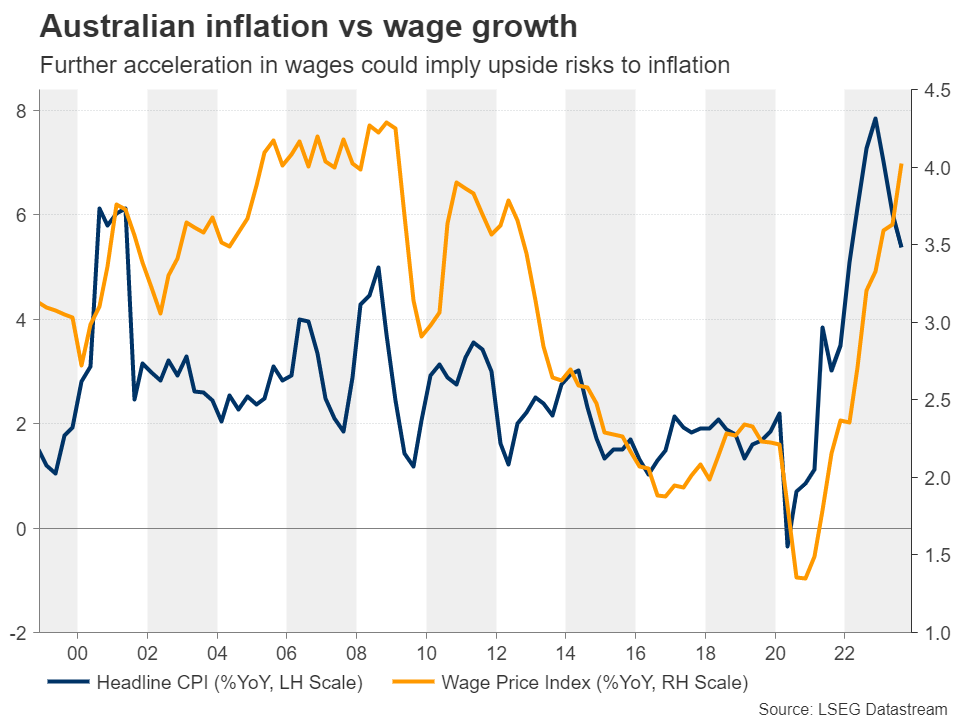

Under Bullock’s leadership, which began in mid-September, there’s been a very notable hawkish tilt in RBA policy even though the economic data has been mixed. It’s fair to say that the recent uptick in the consumer price index as well as the acceleration in wage growth have been at the forefront of policymakers’ minds.

Is the surprise drop in CPI a game-changer?

But inflation appears to be heading lower again. Monthly CPI edged down to 4.9% y/y in October after rising by 5.6% in September. The October picture isn’t entirely positive, however, as one of the core metrics – trimmed mean CPI – fell only modestly to 5.3%. In addition, the labour market remains very tight. The jobless rate has stayed below 4.0% since April 2022, while wages are rising at the fastest pace since 2009, hitting 4.0% y/y in the third quarter.

Until there is clearer evidence that inflation is resuming a downward course or that wage pressures are cooling, it’s unlikely that there will be much change in the language coming from the Reserve Bank of Australia on Tuesday. However, if the statement makes reference to the softer-than-anticipated CPI read, that would suggest an increased caution against further hikes.

Markets not fully convinced by RBA’s hawkish shift

Investors see a less than 5% probability of a rate increase in December, which rises to around 40% by March. But that’s sharply lower than the more than 60% probability priced in before the latest CPI numbers came out.

When looking at Bullock’s comments more closely, however, another rate hike cannot be ruled out, even after the bigger-than-expected drop in CPI. Although higher rates have started to bite for consumers and it’s too soon for Australian exporters to turn optimistic again on China, the slowdown in the economy hasn’t been as bad as initially feared and there’s also the strong housing market to consider.

Yet, most investors seem to be betting on inflation falling further by the time the RBA next meets in February 2024 and unless CPI were to turn higher again, fresh hawkish remarks by Bullock will likely do little in boosting rate hike odds.

Aussie propped up by soft US dollar

For the Australian dollar, however, the CPI-induced losses didn’t last long as the US dollar is under even more pressure from a weakening inflation landscape. Traders think a dovish pivot by the Fed is just around the corner and that looks set to keep a lid on any gains for the greenback.

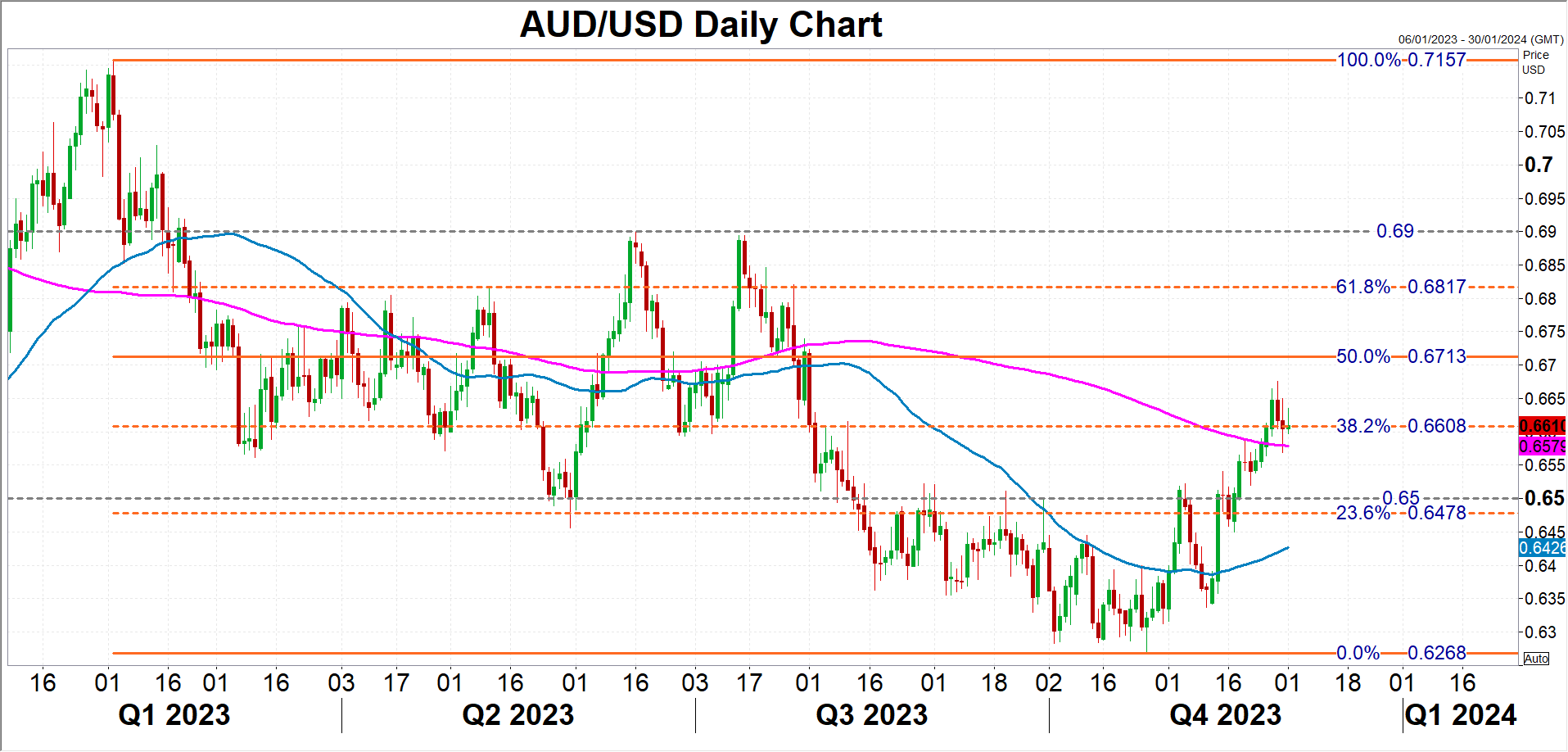

As things stand, the monetary policy divergence would still favour the aussie even if the RBA doesn’t have to raise rates again. The aussie has currently found support around the 38.2% Fibonacci retracement of the February-October downleg at just above the $0.6600 level. A renewed push upwards could see the 50% Fibonacci of 0.6713 being tested before making an attempt for the double top near $0.6900 from June and July.

But in the event that investors turn bearish on the aussie, the $0.6500 level will be a crucial support to watch before attention turns to the 50-day moving average at $0.6426.

Week Ahead – Nonfarm Payrolls Enter the Spotlight, RBA and BoC Decide on Policy

- Investors looking to US NFPs for confirmation of their Fed rate cut bets

- RBA could still signal that higher rates are possible

- But BoC may confirm that interest rates have peaked in Canada

- Japan’s Tokyo CPIs and employment numbers to impact BoJ speculation

Will the US jobs report change the dollar’s fate?

The US dollar has been suffering lately on increasing bets that the Fed will cut rates massively next year. The latest strong hit came from Fed Governor Waller earlier this week, who said that if the decline in inflation continues for several more months, they could start lowering the policy rate. This was the first time a Fed official, and particularly a hawkish one, discussed the possibility of a cut and that’s why market participants added to their rate cut bets, with a 25bps cut now being fully priced in for May and the total number of basis points of rate cuts expected for next year increased from 90 to around 115.

As they try to incorporate every new information into their forecasts, next week, investors are likely to turn their attention back to economic data as Fed officials enter the usual pre-meeting blackout period, and thus, there will be no more speeches. On Tuesday, the ISM non-manufacturing PMI for November and the JOLTS job openings for October are coming out, while on Wednesday, the ADP report for November may be scrutinized ahead of the highlight of the week, the official employment report for November.

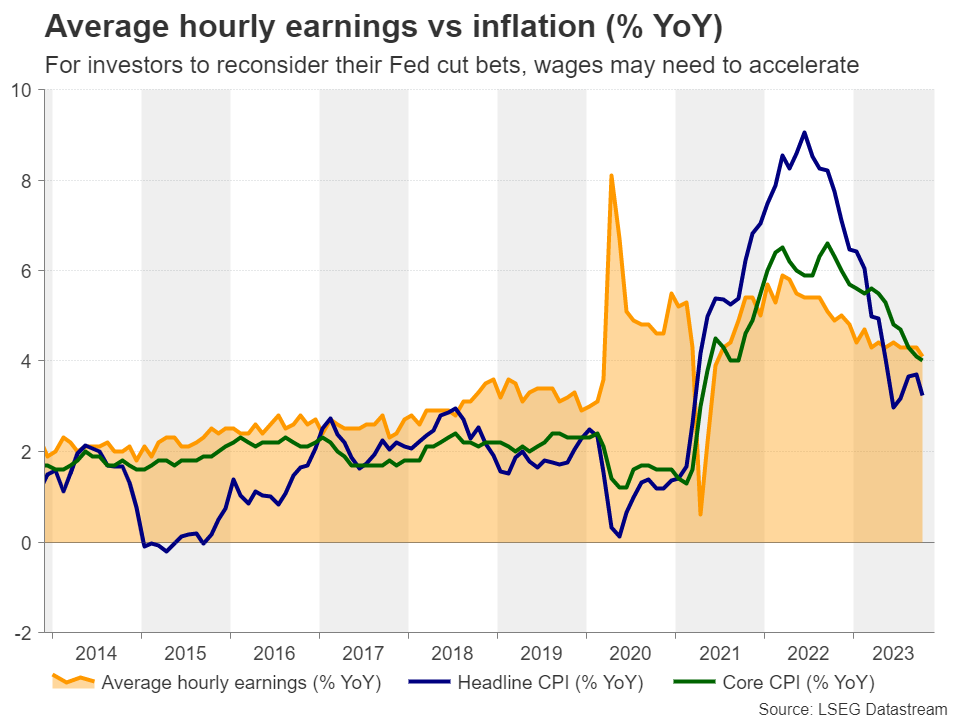

The report is expected to show that the unemployment rate held steady at 3.9% and that nonfarm payrolls increased by 175k in November from 150k in October. Currently, there is no forecast for average hourly earnings. A 3.9% jobless rate and a slight acceleration in the nonfarm payrolls are unlikely to shake much market expectations with regards to several rate reductions by the Fed next year. For that to happen, these numbers may need to be accompanied by a reacceleration in wages.

This could spark some fear that inflation could pick up steam in the months to come, thereby prompting the Fed to keep interest rates high for a longer period than currently anticipated. On the other hand, a further slowdown in wages could solidify investors’ belief and push the dollar lower. After all, lately, market moves suggest that investors are selling the dollar more aggressively when data or headlines corroborate their view, than buying it when there are indications supporting the opposing ‘higher for longer’ case.

Aussie awaits RBA decision, Australia’s GDP and Chinese data

At its November meeting, the RBA raised interest rates, citing more persistent inflationary pressures. Nonetheless, in the accompanying statement, there was an element of uncertainty about whether another rate hike may be needed. This resulted in a drop in the Aussie, as heading into the meeting there was confidence that another quarter-point hike may be in the works for the turn of the year.

That said, with the new Governor, Michele Bullock sounding hawkish thereafter, and the minutes of that meeting revealing concerns about high inflation, investors kept some rate hike bets on the table. Even after the monthly y/y CPI rate for October dropped by more than expected on Wednesday, investors continue to assign a decent 40% probability for another hike by March.

Perhaps that’s because the closely watched trimmed mean CPI only ticked down to 5.3% y/y from 5.4%, which is still well above the upper bound of the RBA’s 2-3% objective and/or because the monthly CPI data does not show all the components included in the quarterly CPI. In other words, the quarterly reading is a more reliable inflation metric. The q/q CPI rate for Q4 will be available on January 31. What’s more, the Wage Price Index for Q3 rose to 4.0% from 3.6%, which implies upside risks to inflation in the months to come.

With all that in mind, the RBA is more likely to stand pat on Tuesday, but it is unlikely to clearly signal that this hiking cycle is over. Officials are likely to maintain the view that interest rates could further rise if needed, which could allow the aussie to extend its recovery against the US dollar.

That said, the aussie may not be driven only by the RBA decision next week, as on Wednesday, Australia’s GDP for Q3 is scheduled to be released. The forecast is for a slowdown to 0.3% q/q from 0.4%, which could reignite some speculation that the RBA is done raising rates, even if just the previous day policymakers signal readiness to do more. On Thursday, Australia’s and China’s trade numbers will be released, while on Saturday, China publishes its CPI and PPI data. Given the close trade ties between Australia and China, more signs that the world’s second-largest economy is bottoming out could allow the aussie to continue marching north.

Will the BoC signal the end of this tightening crusade?

There is another central bank decision on next week’s agenda: The Bank of Canada on Wednesday. When they last met, policymakers of this Bank held interest rates steady, citing moderating spending and relieving price pressures. However, they remained prepared to raise the policy rate further if needed.

Since then, data have been coming out on the soft side with the unemployment rate rising to 5.7% from 5.5% in October, the employment change revealing that the economy added less jobs than forecast during the month, and inflation cooling more than expected. This combined with Thursday’s GDP data for Q3 pointing to a contracting economy has led investors to price in around 105bps worth of rate cuts by the end of 2024.

Although officials are unlikely to confirm the market’s view of so many bps worth of cuts, they could signal that they are done raising interest rates, which could hurt the loonie. Just last week, BoC Governor Macklem said that interest rates may be at their peak, given that excess demand has vanished, and weak growth is expected to persist for months.

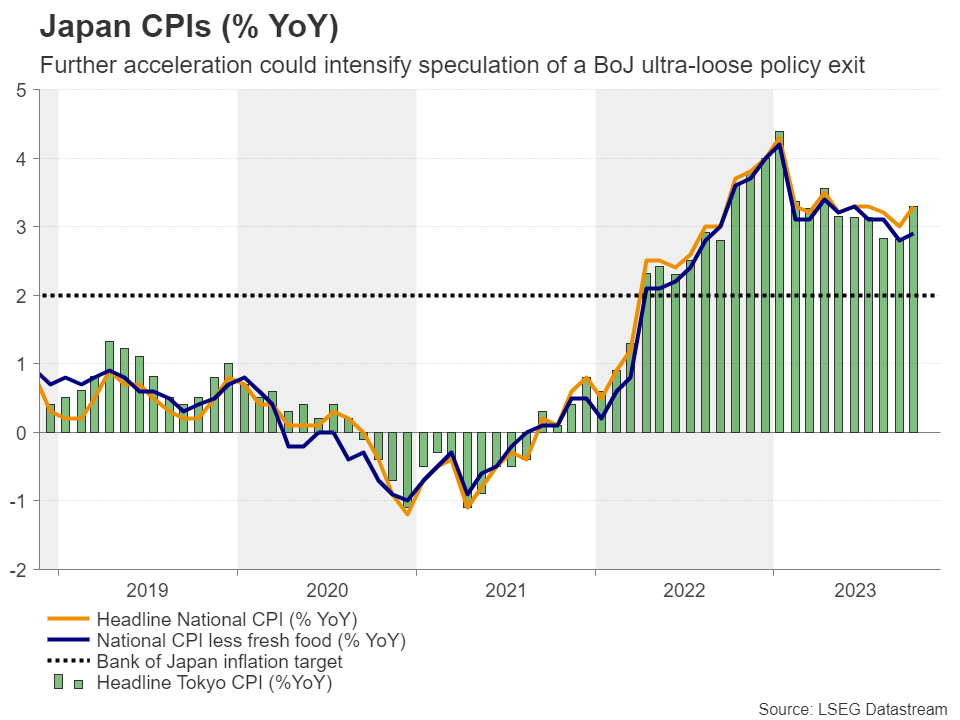

Japanese data could fuel speculation about a BoJ policy exit soon

It will be an interesting week for yen traders as well, as during the Asian session Tuesday, Japan’s Tokyo CPI figures are due to be released, while on Thursday, the final estimate of Q3 GDP and the employment report are coming out. The final estimate of GDP is forecast to confirm that the economy shrank 0.5% in Q3, but if the Tokyo CPIs, which are closely correlated with the National numbers, point to further acceleration in inflation, and the jobs data reveal another pick up in wages, then speculation that the BoJ could exit ultra-loose monetary policy conditions soon is likely to intensify, thereby adding more fuel to the yen’s engines.

Weekly Focus – Disinflation Continues

This week, inflation came in below expectations in the euro area and the US. In the euro area, headline inflation fell much more than expected to 2.4% y/y (consensus: 2.7% y/y) in November from 2.9% in October. The decline was broad-based as core inflation ticked down to 3.6% from 4.2%. Remarkably, the monthly change in core inflation was -0.15% m/m seasonally adjusted. This was a major surprise as the previously sticky service prices also fell in the month. Markets reacted quickly and priced in an extra full 25bp cut in the ECB deposit rate next year thus seeing it at 2.75% in December 2024. We think it is still too early to declare victory over inflation as wage growth is strong and expect just three 25bp cuts next year starting in June, which will bring the policy rate to 3.25%.

In the US, PCE inflation was slightly lower than expected in October at 3.0% y/y (consensus 3.1%, prior: 3.4%). Underlying inflation continued to ease as the Fed's preferred measure, core services PCE inflation, slowed down in both m/m (+0.21%) and y/y (+4.6%) terms. This signals that the Fed continues to make progress on cooling underlying inflation.

The Chinese PMIs sent mixed signals for activity in November. The official PMIs from NBS were weaker than expected while the private version from Caixin pointed to improvements in manufacturing. We lean more towards the Caixin index painting the right picture and expect further improvements in the manufacturing sector over the coming months. Regarding the service sector, it is a concern that the NBS continues to weaken if it reflects low private consumption. To support domestic demand, both the Chinese central bank and government agencies unveiled measures to support financing for the private sector this week and we expect more to come.

OPEC+ decided to keep status quo on production in a signal that we should not expect deeper cuts in production. Going forward, we expect the oil market to be in the hands of global growth and the dollar and look for Brent to average USD80-85/bbl.

The Reserve Bank of New Zealand (RBNZ) kept the policy rate unchanged at 5.50% as expected this week. The RBNZ communicated a hawkish stance by signalling a longer hold and slower rate cuts than previously. The RBZN now sees the first rate cut in Q2 2025.

Next week, focus will be on US data releases with both the November jobs report, ISM services, and the University of Michigan survey scheduled. We expect a further cooling in non-farm payrolls on Friday to +140k and see average hourly earnings growth stable at 0.2%. Markets will keep a close eye on the Michigan survey on Friday after two consecutive months of rising short-term inflation expectations. We also have several central bank meetings next week in Poland, Canada, and Australia. We expect unchanged policy rates from all three.

China and EU will have the first face-to-face summit in years which may attract some attention on Thursday and Friday. From China, we receive the November trade data on Thursday that will give clues as to whether global manufacturing recession is easing. On Tuesday, we closely follow the Caixin service PMIs after the weak NBS service PMIs.

On Tuesday, we publish new macroeconomic projections for the Nordic countries as well as the euro area, US, China, and UK in our Nordic Outlook publication.