Sample Category Title

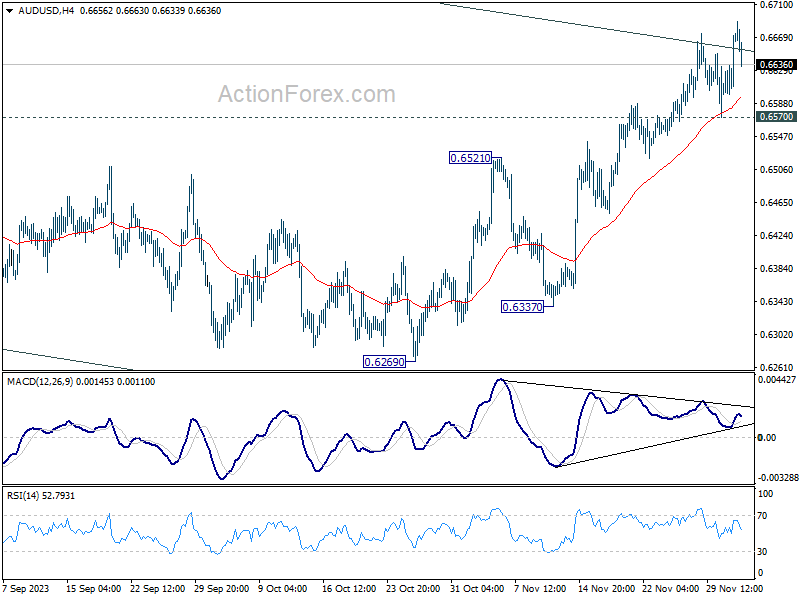

AUD/USD Daily Report

Daily Pivots: (S1) 0.6625; (P) 0.6650; (R1) 0.6701; More...

Further rally is expected in AUD/USD as long as 0.6570 support holds. Sustained break of channel resistance (now at 0.6652) will argue that whole decline from 0.7156 has completed with three waves down to 0.6269. Further rally should then be seen to 0.6894 resistance for confirmation. However, break of 0.6570 support will indicate rejection by the channel and turn bias back to the downside.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. price actions from 0.6169 (2022 low) could be just a medium term corrective pattern, with rise from 0.6269 as the third leg. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

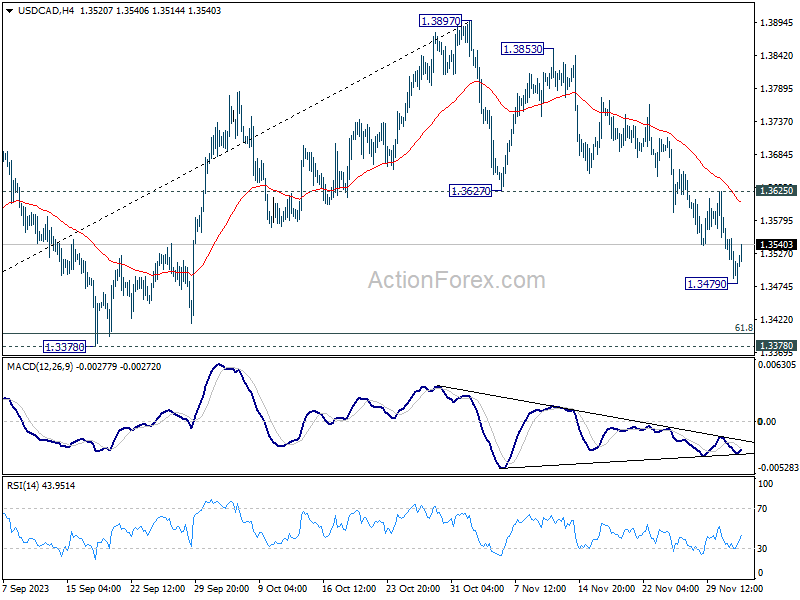

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3463; (P) 1.3521; (R1) 1.3555; More...

Intraday bias in USD/CAD is turned neutral first with current recovery, and some consolidations could be seen above 1.3479 temporary low. Still, further decline is expected as long as 1.3625 resistance holds. Below 1.3479 will resume the fall from 1.3897 to 1.3378 support next, which is close to 61.8% retracement of 1.3091 to 1.3897 at 1.3399. Strong support could be seen there to bring rebound.

In the bigger picture, rise from 1.3091 is seen as the fifth leg of the whole rise from 1.2005 (2021 low). Further rally is expected as long as 1.3378 support holds, to 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. However, decisive break of 1.3378 will dampen this view and bring deeper fall back to 1.3091 instead.

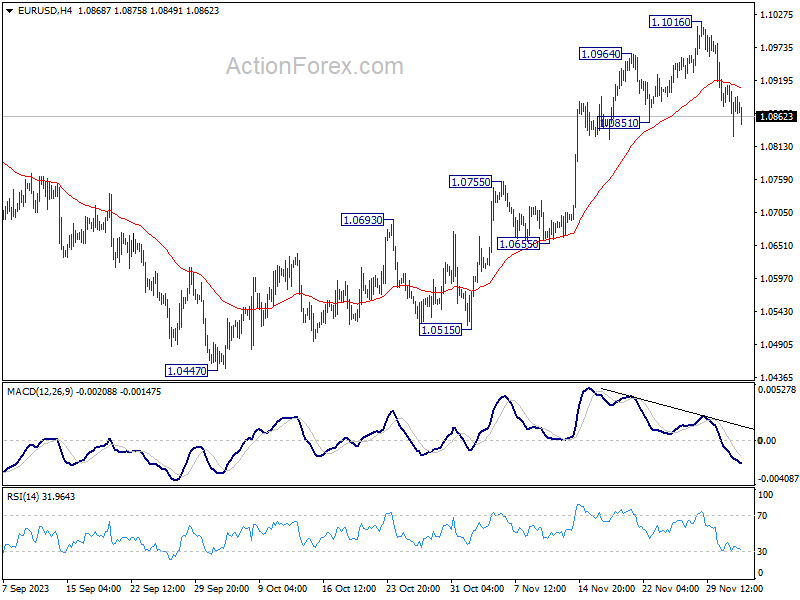

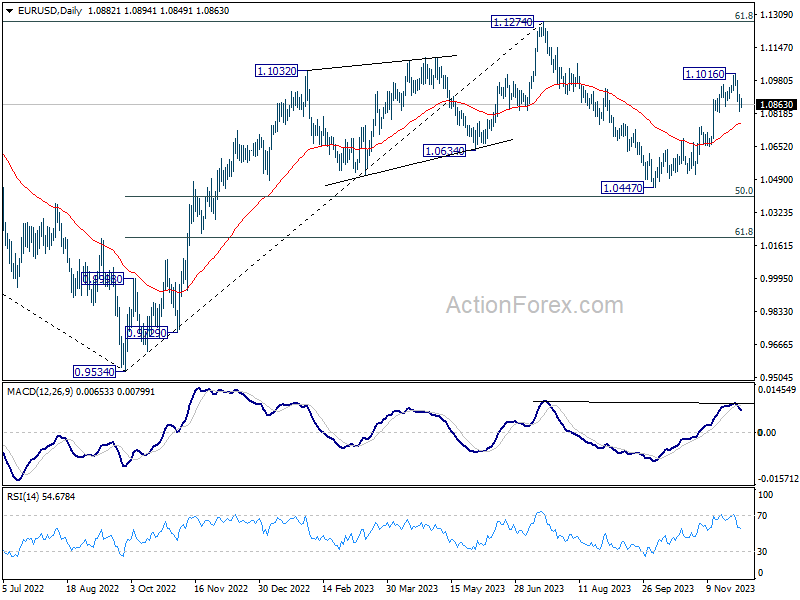

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0838; (P) 1.0875; (R1) 1.0922; More...

Intraday bias in EUR/USD remains mildly on the downside at this point. Fall from 1.1016 short term top should extend to 55 D EMA (now at 1.0769). On the upside, however, break of 1.1016 will resume the rise from 1.0447 to retest 1.1274 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

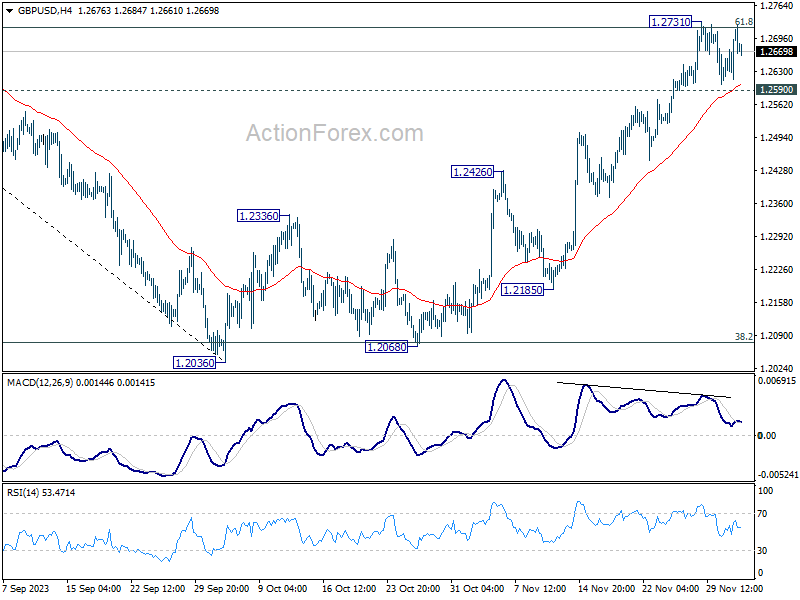

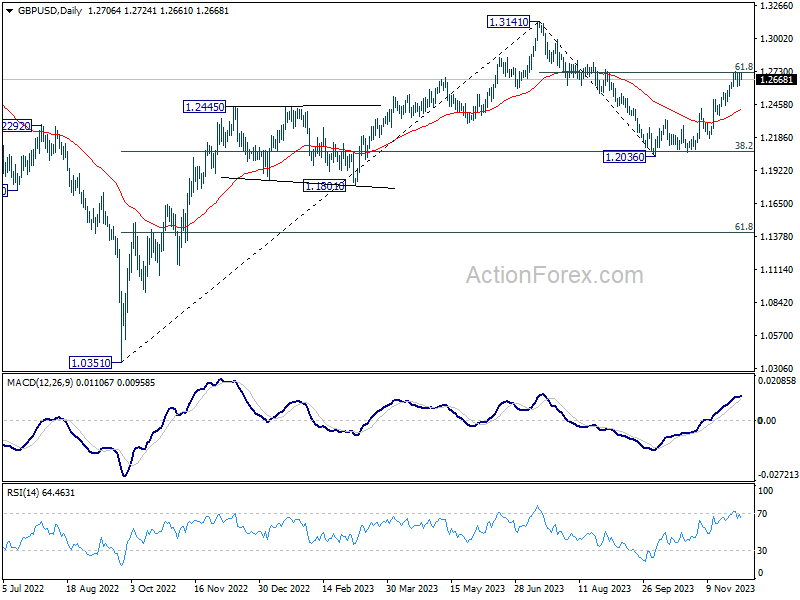

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2645; (P) 1.2680; (R1) 1.2747; More...

Intraday bias in GBP/USD remains neutral and consolidation from 1.2731 could extend further. But further rally is expected as long as 1.2590 minor support holds. On the upside, decisive break of 1.2731 will resume the rally from 1.2036 for retesting 1.3141 high next.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

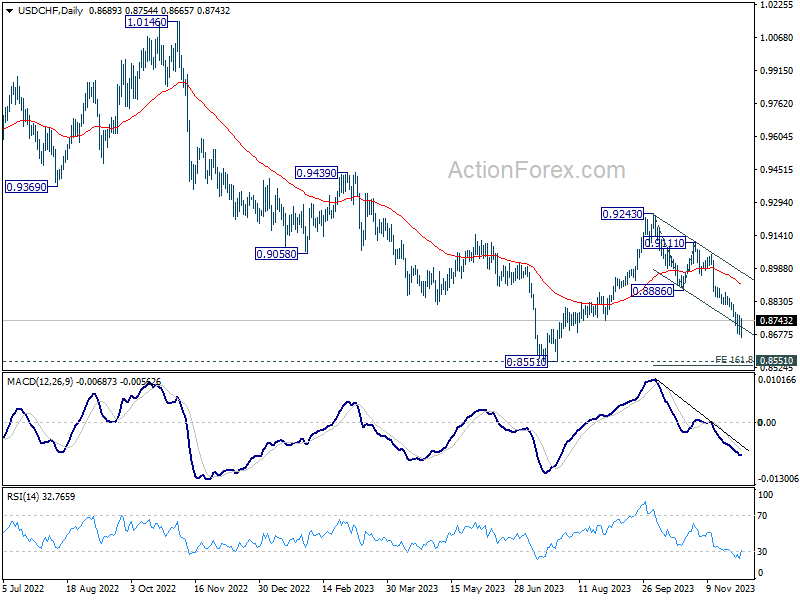

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8657; (P) 0.8713; (R1) 0.8746; More....

Intraday bias in USD/CHF is turned neutral first with current recovery. But another fall is in favor as long as 0.8769 minor resistance holds. Below 0.8665 will resume the decline from 0.9243 to 161.8% projection of 0.9243 to 0.8886 from 0.9111 at 0.8533, which is close to 0.8551 low. However, break of 0.8769 minor resistance should indicate short term bottoming, and turn bias back to the upside for stronger recovery.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. For now, this will remain the favored case as long as 0.8886 support turned resistance holds.

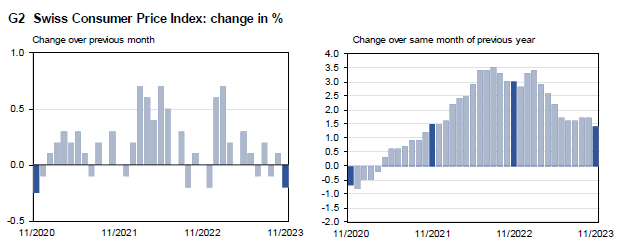

Swiss CPI slows to 1.4%, import prices turn negative

Swiss CPI fell -0.2 mom in November, below expectation of -0.1% mom. Core CPI (excluding fresh and seasonal products, energy and fuel), was flat at 0.0% mom. Domestic products prices was flat at 0.0% mom. Imported product prices fell -1.1% mom.

Annually, CPI slowed from 1.7% yoy to 1.4% yoy, below expectation of 1.6% yoy. Core CPI slowed from 1.5% yoy to 1.4% yoy. Domestic products prices slowed from 2.2% yoy to 2.1% yoy. Imported product prices turned negative from 0.4% yoy to -0.6% yoy.

Gold Advanced to 2072.22

Markets

The November yield correction found an easy way in at the start of the final month of the year through a disappointing US manufacturing ISM. The headline figure stabilized at 46.7 instead of improving to an expected 47.8. New orders fell though less rapidly (48.3 vs 45.5) while employment dropped to 45.8. Actual output fell sub 50 again after expanding for some months. Prices paid ticked higher to 49.9 though, potentially signaling that the strongest disinflationary pressures in the sector are easing. In Powell’s anticipated speech a bit later the Fed chair warned against speculating for rate cuts. But an otherwise balanced tone was not nearly enough to shift market thinking, especially after Waller’s comments earlier last week. Fed’s Goolsbee (“no evidence we stalled at 3% inflation”) and ECB’s Villeroy (“disinflation is even faster than expected”) all talked in the same direction. US yields hit a new correction low with daily changes varying between -10.6 (30-y) and -14.5 (5-y) bps. The 2-y (-14.2 bps) yield lost support at 4.60% (38.2% retracement on the 2023 yield rally). German yields followed their US peers lower with losses of 5.3 to 13.4 bps with similar outperformance of the front end. EUR/USD erased much of the earlier accumulated losses, rebounding from a low of 1.0829 to 1.0884 in the close. Stocks rallied. The EuroStoxx50 (4418) closed above resistance around 4400 and surpassed the 2021 recovery high. The only remaining reference standing in the way for a return to the pre-GFC high of 4572.82 is the current YtD high of 4491.51. US indices rallied 0.55-0.82%. The S&P500 came close to a test of the 2023 high (4607.07). Risk-on supported the likes of GBP. EUR/GBP tumbled to 0.8564 after testing support at the 76.4% GBP recovery on the H2 decline (0.85576). The hefty yield drop pushed the yen higher. USD/JPY closed at the lowest level since early September (146.82) while EUR/JPY lost the 160 mark. Gold advanced to 2072.22. The shiny metal hit a record high this morning by abruptly surging towards 2135.39 in a move that looks like stop-loss in a thin market. It pared gains to 2079.09, above the pandemic high of 2075.47 nonetheless. Today’s economic calendar is razor thin. ECB’s Lagarde appears at a conference today. She will touch on monetary policy in a last chance to do so before the blackout period kicks in later this week. We don’t expect her to turn the tide on markets. US yields recover a few bps this morning (5.5 bps at the front) but that’s merely stabilizing at the current levels. The dollar seeks to further capitalize on HICP-driven euro weakness by pushing the EUR/USD pair further south to 1.0868. Support at 1.0862 (50% retracement on the Oct-Nov rally) may soon break, introducing the next reference at 1.0764. The pound’s technical picture improved materially last week with the earlier mentioned resistance the only level standing in the way for a return to the YtD high (0.8492).

News & Views

After the S&P’s upgrade last month, rating agency Fitch on Friday also raised the credit long term foreign credit rating of Greece from BB+ to BBB- with a stable outlook. The agency sees the government debt to GDP ratio to ‘remain on a sharp downward trend, thanks to solid nominal growth, budget over-execution and a favourable debt servicing structure’. Fitch expects the country’s debt ratio to decline to 152.3% of GDP in 2024. The process is supported by ongoing solid growth expected at 2.9% next year after 2.4% this year. To support the fiscal consolidation process, the government also committed to further increase the primary budget surplus (balance excluding interest rate payments) from 1.1% this year to 2.1% next year.

The Hungarian debt agency AKK on Friday published its 2024 financing plan. The total net funding requirement for 2024 is HUF 2.515 billion, to be financed by a net issuance of HUF 2.643 billion. Contribution to the net issuance is expected to be HUF 1.528 billion in HUF retail securities and HUF 987 billion in FX financing. AKK plans a net negative institutional HUF bond issuance for 2024 with an average term-to-maturity of almost 7 years. On foreign currency financing, the 30% upper bound regarding the share of FX debt remains unchanged for 2024. AKK plans the issuance of an international USD bond with a volume of up to USD 2 billion and a benchmark sized green EUR bond in case of favourable market conditions in H1 2024. AKK also plans Samurai and Panda bond issuances in the second half of 2024 to further strengthen presence in Asian markets. FX project loans (e.g.: EIB, CEB, etc.) and other types of FX financing (e.g.: private placements, ECP) based on circumstances are also possible in 2024.

Gold Technical: Medium-Term Uptrend Remains Intact But Risk of Minor Pull-back

- Today’s early Asian session’s swift rally to a fresh all-time high is likely to be driven by a thin liquidity trading environment rather than the Israel-Hamas geopolitical war risk premium.

- Spot Gold’s portfolio hedging role may gain traction as global recession risk resurfaces.

- Medium-term uptrend phase remains intact but may shape a minor pull-back below US$2,152 key short-term pivotal resistance with immediate supports at US$2,032/2,018.

The price actions of Spot Gold (XAU/USD) have continued to push higher since our last analysis where it clear above the short-term resistance zone of US$2,028/2,037and rallied to retest its current all-time high level of US$2,075 (printed in August 2020) on last Friday, 1 December 2023.

In today’s (4 December) early Asian session before the opening of Tokyo trading hours, Spot Gold spurted upwards to hit a fresh intraday all-high of around US$2,148 before it almost gave up all its gains to trade at US$2,083 at this time of the writing.

Despite an uplift in geopolitical tensions in the Middle Eastern region after Israel resumed its offensive operations against Hamas in Gaza over the weekend, the geopolitical war risk premium is not being priced in the current price actions of oil where WTI crude remained soft ex-post OPEC+ meeting and it traded lower in today’s Asian session with an intraday loss of -1.10%.

Hence today’s intraday swift rally that lasted for around thirty minutes towards a fresh all-time high is likely to be driven by a thin liquidity environment at the start of the week rather than fundamental catalysts.

Potential global recession scenario is supporting a medium-term uptrend

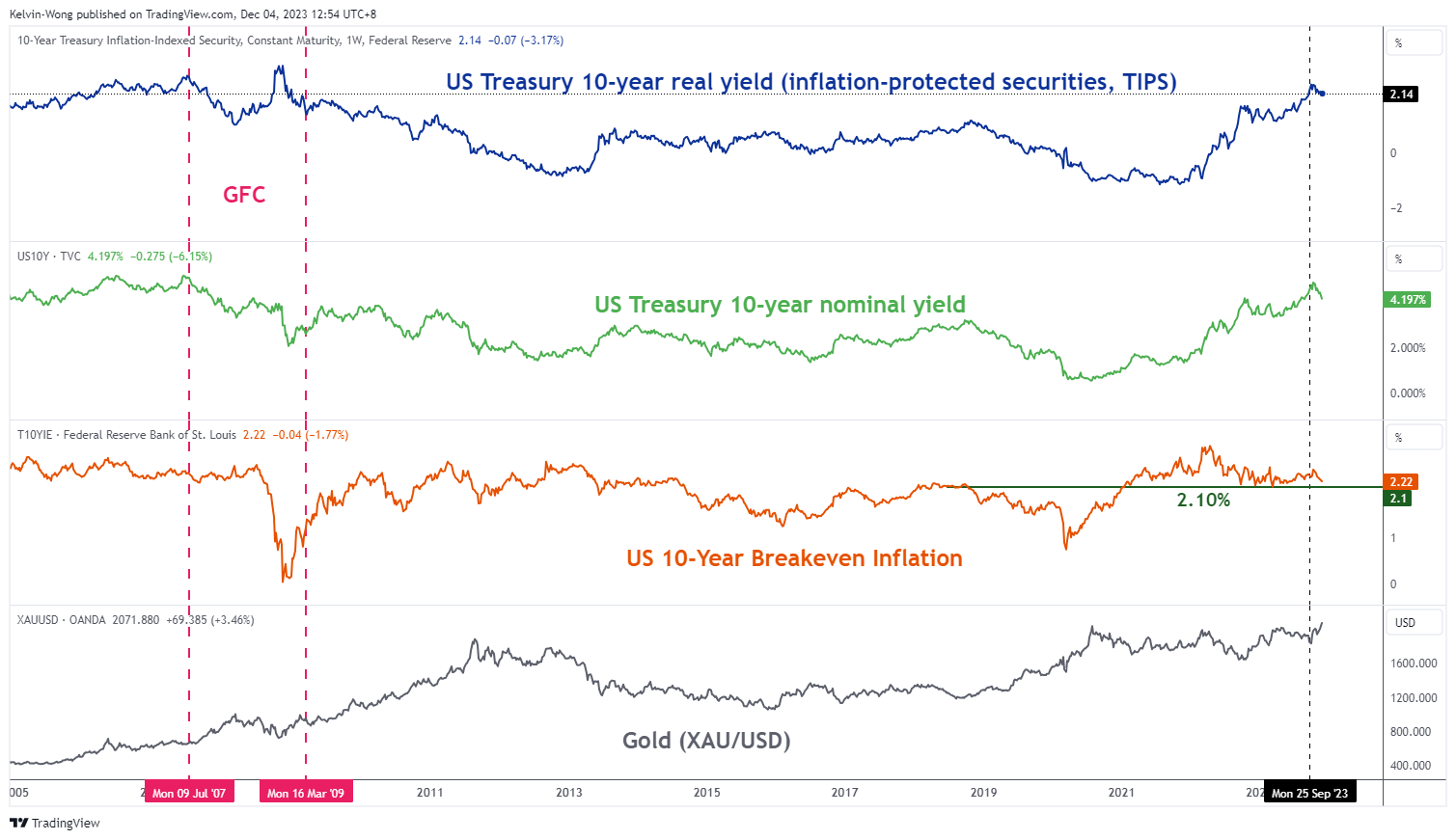

Fig 1: US 10-year Treasury real yield medium-term trend with breakeven inflation as of 4 Dec 2023 (Source: TradingView, click to enlarge chart)

Fig 2: S&P 500 – Spot Gold ratio as of 4 Dec 2023 (Source: TradingView, click to enlarge chart)

The next golden question will be is the current medium-term uptrend for Spot Gold sustainable after a rally of +18% from its 6 October 2023 low, and a third major retest on the US$2,075 high printed on 7 August 2020?

Using an intermarket analysis approach (see Fig 1 & 2), the medium-term uptrend phase low of 6 October 2023 seen in Spot Gold has coincided closely with the recent softness of the US 10-year Treasury real yield as it has declined by 47 basis points from 2.47% printed on 6 October 2023.

Also, the US 10-year breakeven rate (market-based implied US inflation rate 10 years from today) is looking vulnerable for a bearish breakdown below 2.10% suggesting that the US 10-year Treasury real yield still has room for further potential downside that in turn lowers the opportunity costs of holding gold.

Secondly, the long-term monthly ratio chart of the US S&P 500 against Spot Gold has continued to exhibit potential S&P 500 underperformance against Spot Gold as it has remained below a former major ascending support from August 2011 low with bearish momentum reading seen in the monthly RSI indicator of the S&P 500 – Spot Gold ratio; a sign of a potential imminent US recession.

Therefore, these two intermarket analyses suggest an increasing risk of a global recession which in turn may allow the current medium-term uptrend phase of Spot Gold to remain intact via its portfolio hedging role.

Overextended short-term rally in Spot Gold

Fig 3: Spot Gold (XAU/USD) medium-term trend as of 4 Dec 2023 (Source: TradingView, click to enlarge chart)

Fig 4: Spot Gold (XAU/USD) minor short-term trend as of 4 Dec 2023 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, price actions of highly liquid traded instruments and assets do not move in vertical up or down movements but rather oscillate within their trends as market participants react to the ebbs and flows of new catalysts.

Today’s swift rally has led Spot Gold (XAU/USD) to hit an extremely overbought level where the current daily RSI momentum is at 76.70, its highest level so far since the current medium-term uptrend started on 6 October 2023 low.

On the hourly short-term chart, the price actions of XAU/USD have reacted off the upper boundary of the ascending channel from the 6 October 2023 low now acting as a near-term resistance of US$2,126.

In addition, the hourly RSI momentum indicator has just exited from its overbought region which increases the risk of a minor-pull back scenario within an ongoing medium-term uptrend phase.

Watch the US$2,152 key short-term pivotal resistance on XAU/USD and a break below US2,067 near-term support (former swing high areas of 4 May 2023/28 March 2023) exposes the next immediate support zone of US$2,032/2,018.

On the other hand, a clearance above US$2,152 sees a major resistance zone coming in at US$2,200/2,210.

Mixed Feelings

The Federal Reserve (Fed) President Jerome Powell pushed back against the rate cut bets at his speech given in Atlanta last Friday. He is of course playing the card of ‘high for long’ rates to tame inflation, yet he hinted that the Fed will probably not hike rates when it meets this month. He said that the US monetary policy is ‘well into restrictive territory’ and that the fell of effect of higher rates to combat inflation is working its way through economy. ‘We are getting what we wanted to get,’ said Powell. And indeed, inflation is cooling, people start to spend less, and the job market loosens. But in parallel, the financial conditions are loosening fast, as well. Hence the market optimism and stocks/bond gains become increasingly vulnerable to hawkish Fed comments, and/or strong economic data. The US jobs data will take the center stage this week. Investors expect further fall in US jobs openings, less than 200’000 job additions last month with slightly higher pay on month-on-month basis. The softer the data, the better the chances of keeping the Fed hawks away from the market.

Unsurprisingly, the part of Powell’s speech where he pushed back against rate cut expectations went fully unheard by investors on Friday. On the contrary, the Fed rate cut expectations went through the roof when it became clear that the Fed will stay pat again this month. The US 2-year fell to nearly 4.50% on Friday, the 10-year yield tipped a toe below the 4.20% mark. The S&P500 flirted with the summer peak, flirted with the 4600 level and closed the week a touch below this level, while the rate sensitive Nasdaq closed a few points below the 16000 and iShares core US REIT ETF jumped nearly 2.70% last Friday.

The SPDR’s energy ETF, on the other hand, barely closed above its 200-DMA, as last week’s OPEC decision to cut the production supply by another 1mbpd and to extend the Saudi cuts into next year barely impressed oil bulls – even less so given the apparent frictions at the heart of the group regarding this supply cut strategy when prices keep falling. The decline in oil prices continues this Monday. The barrel of US crude remained aggressively sold near the 200-DMA last week, and we are about to step into the $70/73pb region which should give some support to the market. With the clear deterioration of the positive trend, and the lack of any apparent boost to the oil market following last week’s OPEC meeting, there is a chance that we will see oil finish the year below the $70pb mark. An increasingly shaky OPEC unity, record US production, a slowing global economy, deteriorating global demand outlook and efforts to shift toward cleaner energy sources weigh heavier than the supply worries. As such, the $100pb level becomes an increasingly difficult target to reach. And even though the COP28 president Mr. Al Jaber said last weekend that there is ‘no science’ behind demands for phase-out of fossil fuels – yes 70’000 people flew to Dubai to hear that there is no evidence that fossil fuel is destroying climate – efforts to phase-out fossil fuel continues at full speed with solar panel installation surpassing the most optimistic estimates according to Climate Analytics.

In the FX, the US dollar’s positive attempt above the 200-DMA was halted by Powell’s speech on Friday – or more precisely by investors’ careful extraction of all the dovish elements in that Powell speech. Both the Reserve Bank of Australia (RBA) and the Bank of Canada (BoC) will likely keep their rates unchanged this week, but the RBA will certainly sound hawkish faced with worries of ‘home-grown’ inflation. The AUDUSD stepped into the bullish consolidation zone following a 6+% jump since the October dip and could gather further strength this week. The EURUSD, on the other hand, remains under growing selling pressure despite FX traders’ hesitancy regarding what to do with the US dollar. The pair sank to 1.0830 on Friday and is preparing to test the 200-DMA, which stands near 1.0820, to the downside. The easing Eurozone inflation, along with slowing European economies, boost the dovish ECB expectations. The final PMI data will confirm further contraction in the Eurozone last month, as the Eurozone GDP read will likely confirm a 0.1% contraction last quarter. Coming back to the EURUSD, the pair will likely see a solid support near 1.0800/1.0820, which includes the 200-DMA and the major 38.2% Fibonacci retracement on October – November rebound. And clearing this support should pave the way for an extended selloff toward 1.0730.

Investor Confidence Grows Amid Dropping Yields

Market movers today

There are no market movers today in the calendar.

This week focus will be on US data releases with both the November jobs report, ISM services, and the University of Michigan survey scheduled. We expect a further cooling in non-farm payrolls on Friday to +140k and see average hourly earnings growth stable at 0.2%. Markets will keep a close eye on the Michigan survey on Friday after two consecutive months of rising short-term inflation expectations.

We have several central bank meetings this week in Poland, Canada, and Australia. We expect unchanged policy rates from all three.

The 60 second overview

Market focus and overnight: On Friday, both the S&P 500 and Nasdaq marked a fifth consecutive week of gains, underscoring sustained positive momentum in the market. US Treasury yields experienced a notable sell-off across the curve, triggered by cooler-than-expected inflation data and dovish remarks from the Federal Reserve. The 10-year yield saw a significant decline, reaching a three-month low. Notably, the market is currently pricing in the anticipation of over 100 basis points of Federal Reserve cuts in 2024, with the possibility of an initial move as early as March, aligning with our expectations of the first Fed cut in March. Federal Reserve Chair Jerome Powell tempered these expectations in a speech on Friday, suggesting it would be "premature" to speculate on the timing of any easing of monetary policy. Elsewhere, gold prices surged to record levels, achieving their highest close on record, reflecting a shift in investor preferences. EUR/USD is consolidating below the 1.09 mark. This morning, yields are somewhat rebounding while gold is declining from highs. Oil is trading lower as Brent fell below USD80/bbl. Asian markets are mixed together with European futures. US futures are a tad lower as we start the week.

US manufacturing ISM: The US November ISM manufacturing stayed at 46.7 (consensus: 47.8, prior: 46.7). The details were mixed. Prices paid rose to 49.9 from 45.1, the highest since April 2023. Additionally, new orders rose to 48.3 from 45.5. However, employment fell to 45.8 from 46.8.

Equities: Global equities rose on Friday, thereby securing a five-week winning streak. Last week was in some sense even more interesting than some of previous weeks where equities rose more than last. The reason is the underlying rotation where the soft-landing narrative is super visual. Thinking being: lower inflation, central bank losing is coming, lower yields, lower risk of recession, massive defaults in CRE avoided. Hence, REIT, small caps and banks (not least US regionals) performing very strongly although yields are moving lower. Again, the "inflation-normalization" trade has come a long way and we need to start seeing the "good data/bad data" differently as we move in 2024. To a large extent, this also means an end to the positive correlation for bonds and equities. Only caveat is inflation data where bonds and equities will still be positive-correlated at least in the beginning of 2024. US major indices on Friday: Dow +0.8%, S&P 500 +0.6%, Nasdaq +0.6%, Russell 2000 +3.0%. Asian markets are mixed this morning together with European futures. US futures are a tad lower as we start the week.

FI: Comments from Villeroy on Friday afternoon staged a massive rally led by the front end to end a week which was mostly a one-way trend for lower rates. With Villeroy saying that rate hikes are over and 'The question of a cut may arise when the time comes during 2024, but not now', 2y German yields dropped 10bp. 10y German yields are now trading at 2.36%. Markets added 13bp to the ECB rate cut expectations for 2024 and now points to 127bp. The awaited speech from Powell on Friday afternoon did not provide signals ahead of the blackout period that started this weekend.

FX: EUR and USD were the big losers on Friday, where in particular NOK, JPY and AUD saw strong gains. EUR/USD traded close to the 1.09 level. EUR/NOK fell to around 11.60 and EUR/SEK just below 11.30.

Credit: iTraxx Main traded again tighter on Friday and closed 13.2bp tighter than the week before at 65.9bp, while Xover tightened 57.3bp during the week to close at 363.8bp. The week was characterized by high activity in the primary market, sentiment remains constructive in credit and investor appetite for new deals continues to look solid.

Nordic macro

The Riksbank is publishing the minutes from the November monetary policy meeting today at CET 9:30. Interesting to see what the most hawkish members, Thedéen och Jansson, focused on in the latest decision. After the publication of the minutes Anna Breman will discuss 'the economic situation and current monetary policy' at CET 11:00. Governor Thedéen will follow up (on Tuesday) and the remaining three board members will speak on the same topic on Wednesday, Thursday and Friday, respectively.