Sample Category Title

RBA holds rates following sparse information since last meeting

RBA kept its cash rate target unchanged at 4.35%, aligning with market expectations. The central bank's latest statement indicates continued openness to further rate hikes, but emphasizes that any such decision "will depend upon the data and the evolving assessment of risks." This stance reflects a careful approach, as RBA awaits more comprehensive data, particularly the Q4 inflation figures due in January, before its next meeting in early February.

In its review of the "limited information" available since November meeting, RBA acknowledged that the data were "broadly in line with expectations." The October monthly CPI update suggested continued moderation in inflation, but did not provide substantial insights into services inflation. While wage growth accelerated in Q3, it is "not expected to increase much further". The labor market conditions are seen as "continuing to ease gradually," though they remain tight.

RBA also highlighted "still significant uncertainties" regarding the economic outlook. It pointed out the potential for persistent services inflation in Australia. Domestically, the uncertainties include the lag effects of monetary policy and household consumption patterns. On a global scale, the ongoing uncertainty around Chinese economy's trajectory and the broader implications of international conflicts were noted as significant factors influencing Australia's economic environment.

(RBA) Statement by Michele Bullock, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate target unchanged at 4.35 per cent and the interest rate paid on Exchange Settlement balances unchanged at 4.25 per cent.

Last month, the Board increased interest rates by 25 basis points, following a period of four months where it had held interest rates steady. This decision reflected the Board's view that progress in bringing inflation back to the target range of 2 to 3 per cent was looking slower than earlier forecast. While the economy has been experiencing a period of below-trend growth, it was stronger than expected over the first half of the year. Underlying inflation was higher than expected at the time of the August forecasts, including across a broad range of services. Conditions in the labour market had eased but remained tight. Housing prices were continuing to rise across the country as was the number of new mortgages. Given this, the Board judged that the risk of inflation remaining higher for longer had risen and an increase in interest rates was therefore warranted to be more assured that inflation would return to target in a reasonable timeframe.

The limited information received on the domestic economy since the November meeting has been broadly in line with expectations. The monthly CPI indicator for October suggested that inflation is continuing to moderate, driven by the goods sector; the inflation update did not, however, provide much more information on services inflation. Overall, measures of inflation expectations remain consistent with the inflation target. Wages growth picked up in the September quarter but this was expected given that it captured the earlier Fair Work Commission decision on award wages. Wages growth is not expected to increase much further and remains consistent with the inflation target, provided productivity growth picks up. Conditions in the labour market also continued to ease gradually, although they remain tight.

Higher interest rates are working to establish a more sustainable balance between aggregate supply and demand in the economy. The impact of the more recent rate rises, including last month's, will continue to flow through the economy. High inflation is weighing on people's real incomes and household consumption growth is weak, as is dwelling investment. Holding the cash rate steady at this meeting will allow time to assess the impact of the increases in interest rates on demand, inflation and the labour market.

Returning inflation to target within a reasonable timeframe remains the Board's priority. High inflation makes life difficult for everyone and damages the functioning of the economy. It erodes the value of savings, hurts household budgets, makes it harder for businesses to plan and invest, and worsens income inequality. And if high inflation were to become entrenched in people's expectations, it would be much more costly to reduce later, involving even higher interest rates and a larger rise in unemployment. To date, medium-term inflation expectations have been consistent with the inflation target and it is important that this remains the case.

There are still significant uncertainties around the outlook. While there have been encouraging signs on goods inflation abroad, services price inflation has remained persistent and the same could occur in Australia. There also remains a high level of uncertainty around the outlook for the Chinese economy and the implications of the conflicts abroad. Domestically, there are uncertainties regarding the lags in the effect of monetary policy and how firms' pricing decisions and wages will respond to the slower growth in the economy at a time when the labour market remains tight. The outlook for household consumption also remains uncertain, with many households experiencing a painful squeeze on their finances, while some are benefiting from rising housing prices, substantial savings buffers and higher interest income.

Whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks. In making its decisions, the Board will continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that outcome.

GBP/USD Remains In Uptrend But Bulls Lose Strength

Key Highlights

- GBP/USD rallied toward 1.2740 before it corrected lower.

- A key bullish trend line is forming with support near 1.2610 on the 4-hour chart.

- EUR/USD corrected lower below the 1.0880 support zone.

- The US ISM Services PMI could increase from 51.8 to 52.0 in Nov 2023.

GBP/USD Technical Analysis

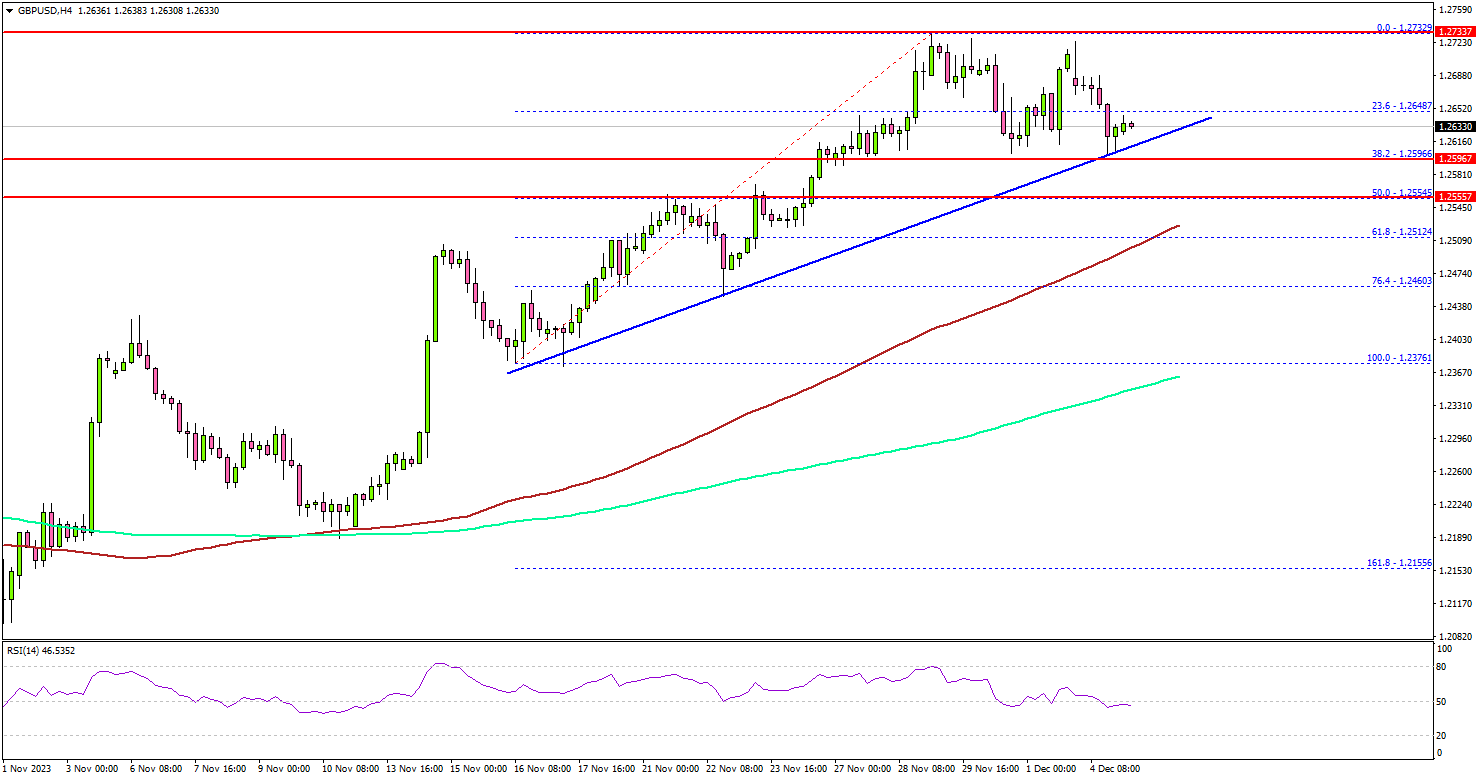

The British Pound started a steady increase above the 1.2500 resistance against the US Dollar. GBP/USD even spiked above 1.2700 before the bears appeared.

Looking at the 4-hour chart, the pair settled above the 1.2600 pivot level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours).

A high was formed near 1.2732 before the pair corrected lower. There was a move below the 1.2700 and 1.2765 levels. The pair even declined below the 23.6% Fib retracement level of the upward move from the 1.2376 swing low to the 1.2732 high.

It is now testing the 1.2620 support. There is also a key bullish trend line forming with support near 1.2610 on the same chart.

The next key support is near 1.2550 or the 50% Fib retracement level of the upward move from the 1.2376 swing low to the 1.2732 high, below which the pair could test the 1.2500 level in the near term. Any more losses might call for a move toward 1.2440.

On the upside, immediate resistance is near the 1.2680 level. The next key resistance is near the 1.2720 level. A close above the 1.2720 zone could open the doors for more upsides. The next stop for the bulls might be 1.2800.

Looking at EUR/USD, the pair started a downside correction, and it even broke the 1.0880 support zone.

Economic Releases

- Euro Zone Services PMI for Nov 2023 – Forecast 48.2, versus 48.2 previous.

- UK Services PMI for Nov 2023 – Forecast 50.5, versus 50.5 previous.

- US Services PMI for Nov 2023 – Forecast 50.8, versus 50.8 previous.

- US ISM Services PMI for Nov 2023 – Forecast 52.0, versus 51.8 previous.

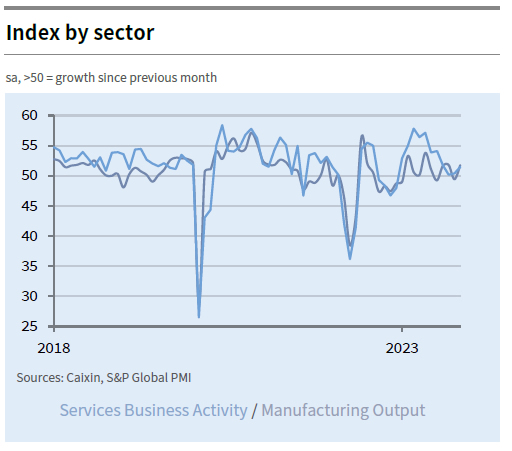

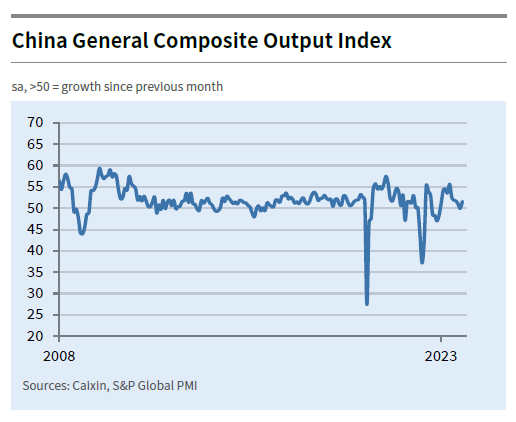

China’s PMI services rose to 51.5 in Nov, composite rose to 51.6

China's Caixin PMI Services rose from 50.4 to 51.5 in November, above expectation of 50.8. PMI Composite rose from 50.0 to 51.6.

Wang Zhe, Senior Economist at Caixin Insight Group said: "Overall, the macroeconomy showed signs of a positive recovery, with steady growth in consumer spending, solid progress in industrial production and improved market expectations.

"However, due to various unfavorable factors, both domestic and external demand still face challenges and employment pressures remain relatively high. The foundation for economic recovery needs to be further consolidated."

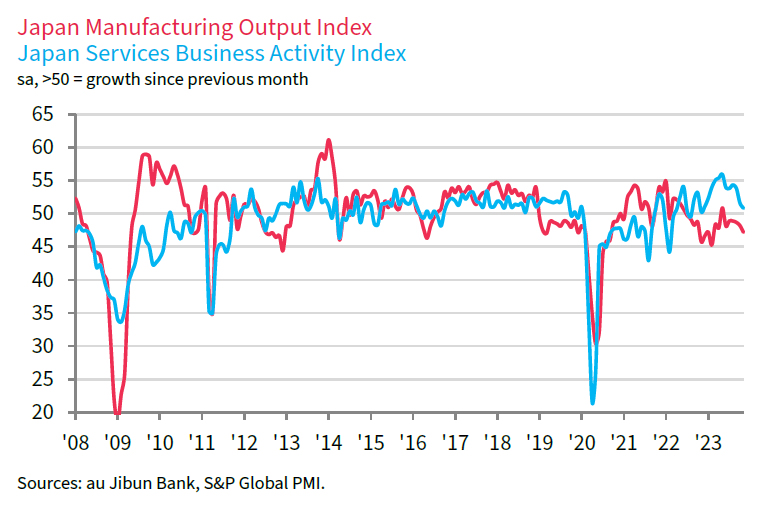

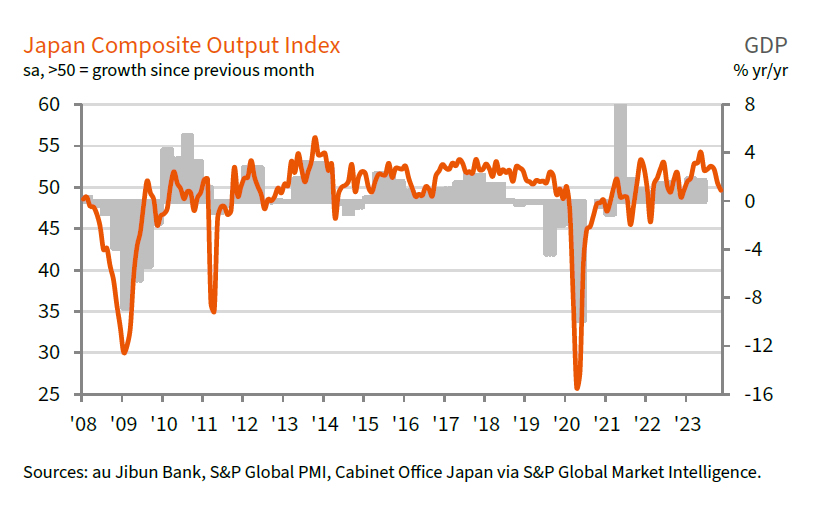

Japan’s PMI services finalized at 50.8, weakening in a year of strong growth

Japan's PMI Services for November was finalized at 50.8, down from October's 51.6, marking the weakest reading since November 2022. PMI Composite also fell to 49.6, down from 50.5 in the previous month, indicating the first contraction since December 2022.

Trevor Balchin, Economics Director at S&P Global Market Intelligence, contextualized these numbers, stating, "November data signalled a further loss of momentum in the services sector, but this should be viewed in the context of a year of strong growth." He highlighted that Business Activity Index for 2023 is trending at 53.7, the highest annual reading since the survey's inception in 2007.

Balchin also pointed out several positive aspects in the latest survey. The rise in new business, sustained employment growth, and the increase in outstanding work indicate ongoing economic activity. Furthermore, the 12-month outlook for activity improved and was "among the strongest on record". Despite these optimistic signs, price pressures in November eased but remained above long-term trends.

Japan’s Tokyo CPI core slows to 2.3% yoy in Nov, core-core still stick at 3.6% yoy

November's inflation data in Japan's capital Tokyo shows a notable slowdown. CPI core, which excludes fresh food, dropped from 2.7% yoy to 2.3% yoy, falling slightly below the expected 2.4%. This decline brings the reading further towards BoJ target of 2%.

Headline CPI also experienced a decrease, falling back to 2.6% yoy. This reduction comes after an unexpected rise from 2.8% yoy in September to 3.2% yoy in October.

Furthermore, CPI core-core, which excludes both food and energy, showed some progress. It declined from 3.8% yoy to 3.6% yoy, a reduction from its peak of 4.0% seen in July and August. However, the still relatively high CPI core-core reading indicates that underlying inflationary pressures remain persistent within the economy, despite the overall slowdown.

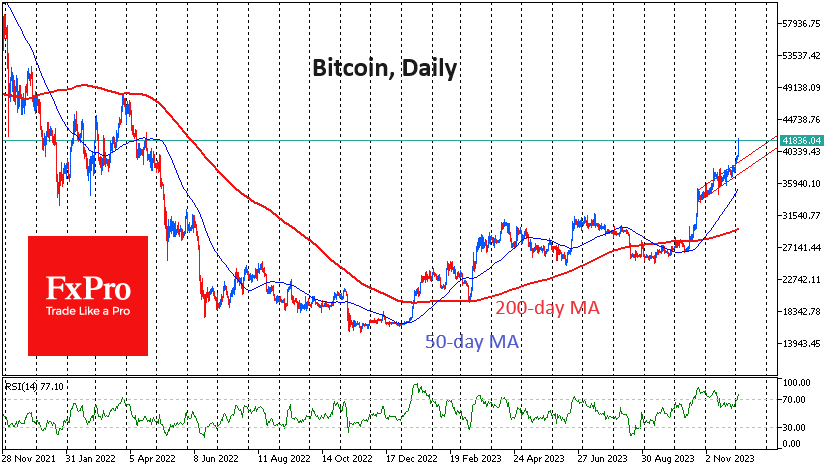

Bitcoin Accelerated Growth

Market picture

Gold’s historic highs and the surge in risk demand at the end of last week did not spare cryptocurrencies. Cryptos experienced impressive gains on Monday, but one cannot leave aside the weekend bull run as well. The crypto market capitalisation reached 1.55 trillion, adding 10.5% in seven days.

Bitcoin proved that the smooth uptrend since late October was just a long consolidation before a new upward spurt. Bitcoin has added over 11.5% since Friday, surpassing $42K at one point on Monday. While Bitcoin is overbought on daily timeframes, this is not necessarily a reason for a correction. In this mode, the first cryptocurrency can move for many more days, drawing more and more layers of investors into FOMO. Technically, up to $46K is thin-air territory for Bitcoin, and price swings between $40K and $46K can be pretty wild.

News background

Matrixport reiterated its forecast for Bitcoin to rise to $63K by April 2024 and $125K by the end of next year. Among the reasons for the rally are halving; geopolitical, monetary, and macroeconomic factors.

Grayscale expects that the emergence of spot bitcoin-ETFs has the potential to reduce the supply of BTC in the market, which in turn will have a positive impact on the first cryptocurrency’s rate. Halving in April will also reduce supply from mining companies.

DeFi and NFT activity is showing “tentative” signs of recovery from a two-year slump as the pending approval of spot bitcoin-ETFs has improved sentiment in the crypto market, JPMorgan noted.

Cryptocurrency exchange Kraken, which has been charged by the SEC, is going to fight the regulator and answer all complaints in court, the company’s general counsel said. He said the authorities’ accusations that “Kraken is a clearing house and a broker-dealer are completely made up.”

Circle, the issuer of the USDC stablecoin, denied reports of illegal funding and ties to the TRON Foundation, HTX and Tron founder Justin Sun.

Meanwhile, Cryptocurrency exchange Binance has entered into an agreement with an unnamed bank for the sake of attracting large legal entity investors and eliminating counterparty risk. Binance is preparing the foundation for the launch of spot bitcoin-ETFs in the US, which many market players have been waiting for a long time.

Sunset Market Commentary

Markets

Gold grabbed most headlines today. The price of bullion spiked to an all-time high in illiquid Asian dealings of $2130/ounce. The spike didn’t last with gold prices falling back towards Friday’s closing levels near $2060/ounce. The move smells like an exhaustion move after the October/November core bond rally pushed gold prices up by around 15%. A quick look at the bitcoin graph (+5% today; +60% since early October; highest since April 2022) also suggests that the air is becoming thin. US Treasuries for the first time show some tentative signs of topping off. US yields add 4.5 bps (30-yr) to 9.7 bps (2-yr). Investors are chewing on Fed Chair Powell’s comments Friday in absence of eco data. He pushed back against premature rate cut bets though his warning initially fell on deaf ears, being overtaken by a weak manufacturing ISM. We don’t draw firm conclusions yet though as it will be tough sailing this week with US non-manufacturing ISM, JOLTS job openings, ADP employment and official payrolls all scheduled for release. We still need first evidence that Treasuries no longer rally on weak (or in line with consensus) data or sell-off on better figures. UK Gilts underperformed Bunds and Treasuries the past weeks with the topping off pattern being strengthened today. UK gilt yields add 3 bps (30-yr) to 5.1 bps (5-yr). Collective action by BoE members succeeded in convincing markets that a BoE rate cut won’t arrive in H1 2024. Sterling no longer profits today with EUR/GBP steady around 0.8580. GBP/USD loses a big figure at 1.2620. German Bunds are exception to the rule with Bund yields ceding another 1.5 bps (2-yr) to 4.8 bps (30-yr). There’s no specific outperformance of French OAT’s after they dodged a possible credit rating cut by S&P. The outlook on the AA rating remains negative though. EUR/USD can’t defy the gravity law, testing last week’s low around 1.0830. Risk sentiment starts the week a little heavy with main European indices mixed and key US gauges opening on the backfoot (Nasdaq up to 1% lower).

News & Views

Swiss inflation slowed more than expected in November. Prices fell by 0.2% M/M slowing the Y/Y measure from 1.7% to 1.4%. Core inflation eased from 1.5% Y/Y to 1.4%. Price decreases were broad-based, especially in the goods sector, with housing rental costs (+1.1% M/M and 2.4% Y/Y) the exception to the global trend. Goods prices declined 0.7% M/M and are only 1.1% higher compared to the same month last year. Services inflation printed at 0.1% M/M and 1.7% Y/Y (unchanged). Recent inflation data came out below the SNB forecast from the September policy meeting, when it expected inflation to average 2% in Q4 2023 and to return slightly north of the 2% top of the tolerance band throughout 2024. The November data suggest a lower starting point for new projections to be published alongside the Dec 14 SNB decision. Even as SNB recently indicated that it remains prepared to raise the policy rate further if needed, the central bank next week can keep a wait-and see approach. The franc declined modestly to test EUR/CHF 0.95 after the CPI release.

At the other end of the inflation-spectrum Turkish prices continued to rise in November. Headline inflation printed at 3.28% M/M and 61.98% Y/Y (from 61.36%). Core inflation rose slightly to 69.9% Y/Y. Still, both measures were slightly softer than expected. In a monthly perspective, housing related costs added 11.17% with alcoholic beverages and tobacco prices 9.16% higher. The CBRT in its November inflation report upwardly revised its outlook for 2023 eoy inflation to 65%. It expects inflation to continue to rise in the first half of 2024. It might reach a peak near 75% Y/Y, before staging a steady decline to 36% at the end of next year. The CBRT raised its policy rate to 40% two weeks ago. The hike was bigger than expected, but the central bank indicated that the current level of tightness is significantly close to the required level. So, the pace of tightening will slow from here and the cycle is expected to be completed soon. The lira is holding near historic low levels against the dollar (USD/TRY 28.92) and the euro (EUR/TRY 31.48), but the pace of depreciation recently almost came to a halt.

Brent “Does Not Believe” OPEC+

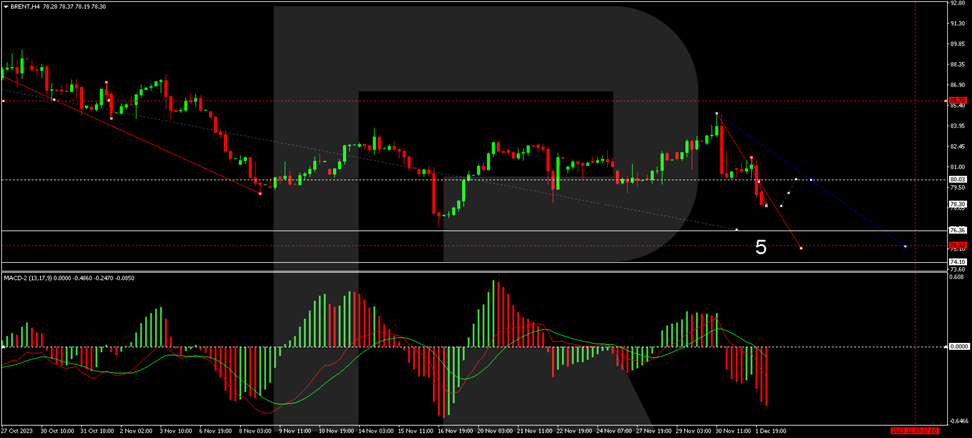

Brent oil prices fell to 78.30 USD per barrel on Monday.

Despite OPEC+ decisions at the November meeting, oil prices are falling. The issue is that the actual parameters of OPEC+ quotas turned out to be lower than investors expected. This does not cancel out the Cartel's powerful support on prices. However, the market cannot cope with emotional reactions.

Escalating tensions in the Middle East observed last weekend may bolster the oil quotes. The factor of a strong US dollar is working oppositely. While the USD is rising, commodity assets appear less attractive to buyers.

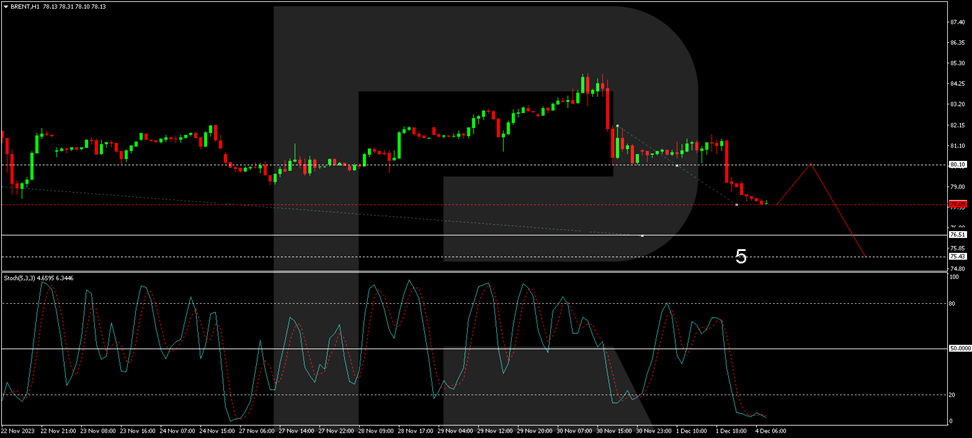

Brent technical analysis

On the H4 Brent chart, there was a rebound from the 84.81 level. The market has fallen to 80.10 and is forming a consolidation range around this level today. A decline to 78.10 is expected, followed by a rise to 80.00 (a test from below). Subsequently, the price could continue its downward trajectory to 76.50. A growth wave might start after the price reaches this level, targeting 85.80. This is the first target for the growth wave. Technically, this scenario is confirmed by the MACD, with its signal line breaking the zero mark, aimed strictly downwards.

On the H1 Brent chart, a consolidation range has expanded downwards to 78.10. Today, a rise to 80.10 is expected, followed by a drop to 76.50, potentially continuing to 75.40. Technically, this scenario is confirmed by the Stochastic oscillator, with its signal line below 20 and poised to rise to the 50 mark.