Sample Category Title

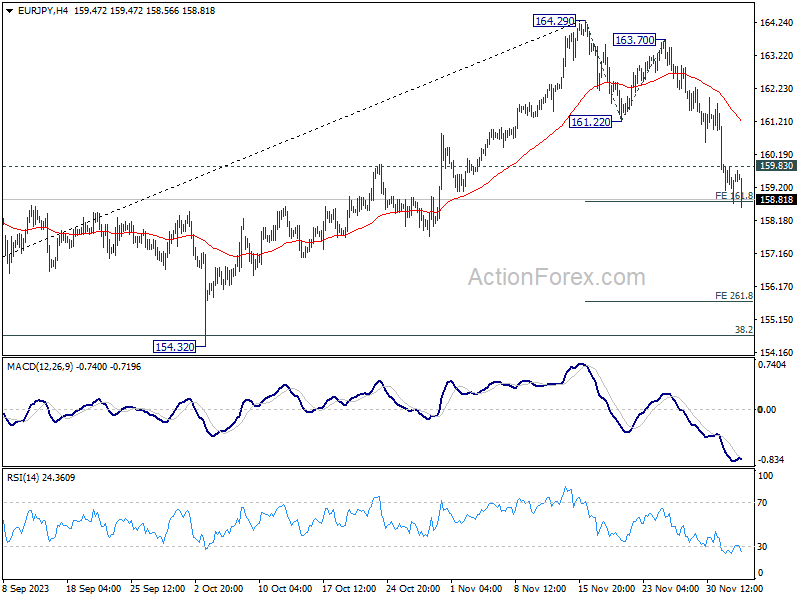

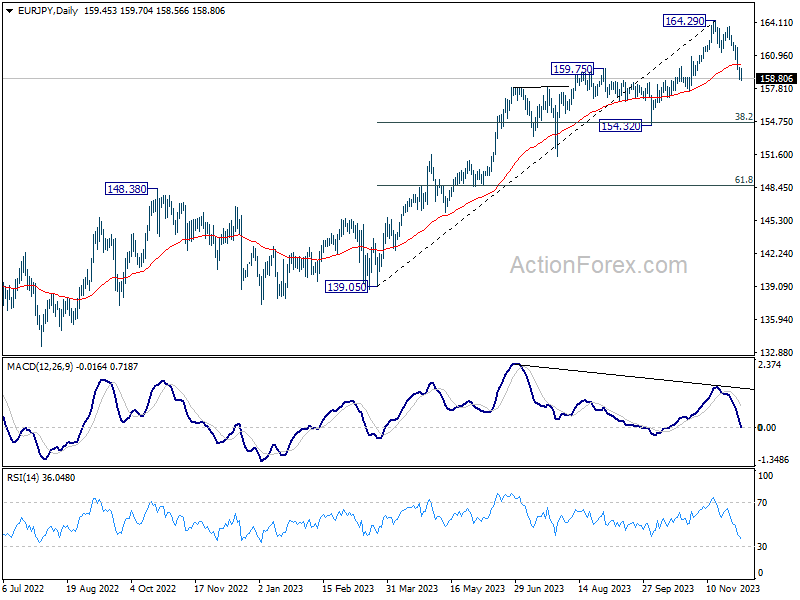

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.88; (P) 159.36; (R1) 160.02; More....

EUR/JPY's fall from 164.29 is in progress and intraday bias stays on the downside. Sustained break of 161.8% projection of 164.29 to 161.22 from 163.70 at 158.73 will target 154.32 cluster support (38.2% retracement of 139.05 to 164.29 at 154.64). On the upside, above 159.83 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, bearish divergence condition in 55 D EMA indicates that a medium term top could be formed at 164.29 already, after hitting rising channel resistance. But price actions from there are tentatively seen as a correction only. There is no clear sign that the up trend from 144.42 (2020 low) has completed yet. As long as 55 W EMA (now at 152.12) holds, another rally through 164.29 is still in favor as a later stage.

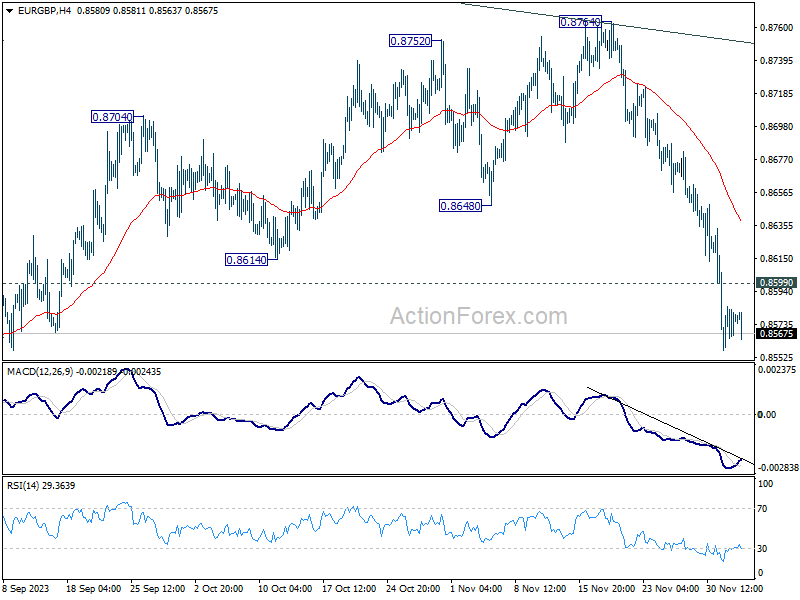

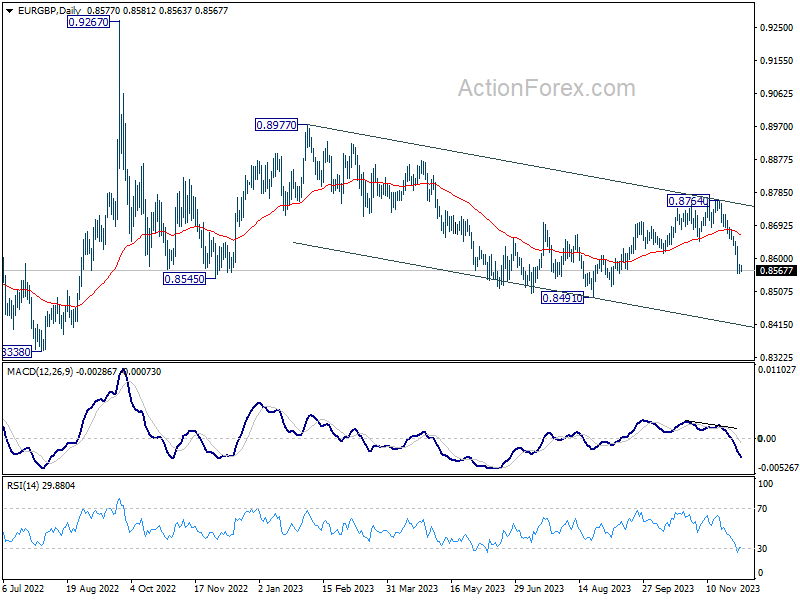

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8564; (P) 0.8574; (R1) 0.8589; More....

Intraday bias in EUR/GBP remains on the downside for the moment. As noted before, rebound from 0.8491 should have completed as a corrective move at 0.8764. Deeper fall should be seen to retest 0.8491 low first. Firm break there will resume larger down trend. On the upside, above 0.8599 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, current development suggests that down trend from 0.9267 (2022 high) is still in progress. This decline is now seen as the third leg of the pattern from 0.9499 (2020 high). Break of 0.8201 will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969. In any case, outlook will stay bearish as long as 0.8764 resistance holds.

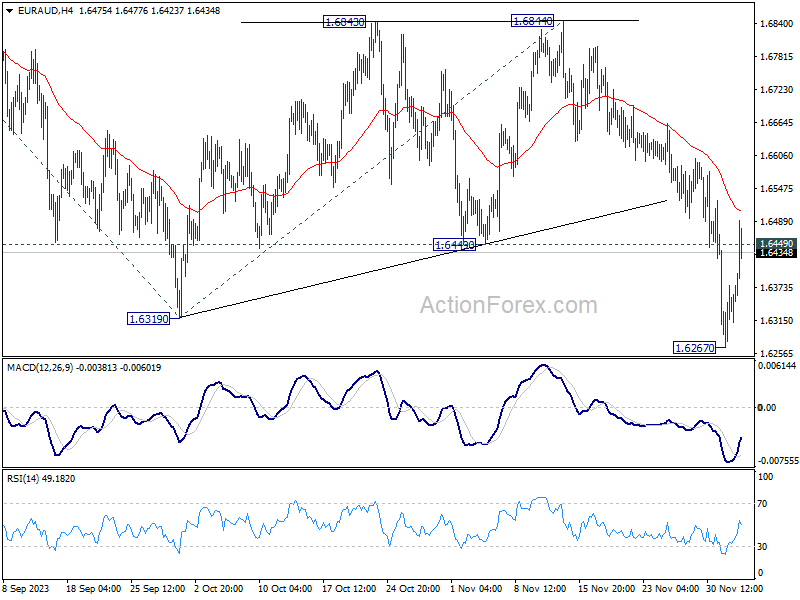

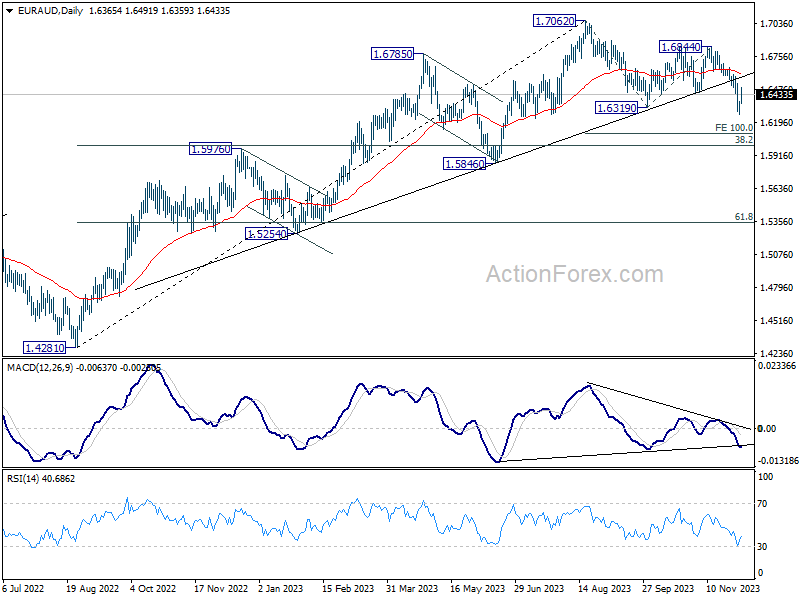

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6300; (P) 1.6339; (R1) 1.6410; More...

Intraday bias in EUR/AUD is turned neutral first with break of 1.6449 support turned resistance. Some consolidations should be seen first, but another fall is expected. Break of 1.6267 will resume the decline from 1.7062 to 100% projection of 1.7062 to 1.6319 from 1.6844 at 1.6106 next.

In the bigger picture, the break of medium term trend line support now suggests fall from 1.7062 correcting the whole up trend from 1.4281 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.4281 to 1.7062 at 1.6000. Strong support could be seen there to bring rebound on first attempt. But risk will stay on the downside as long as 1.6844 resistance holds. Sustained break of 1.6000 would bring further fall to 61.8% retracement at 1.5343.

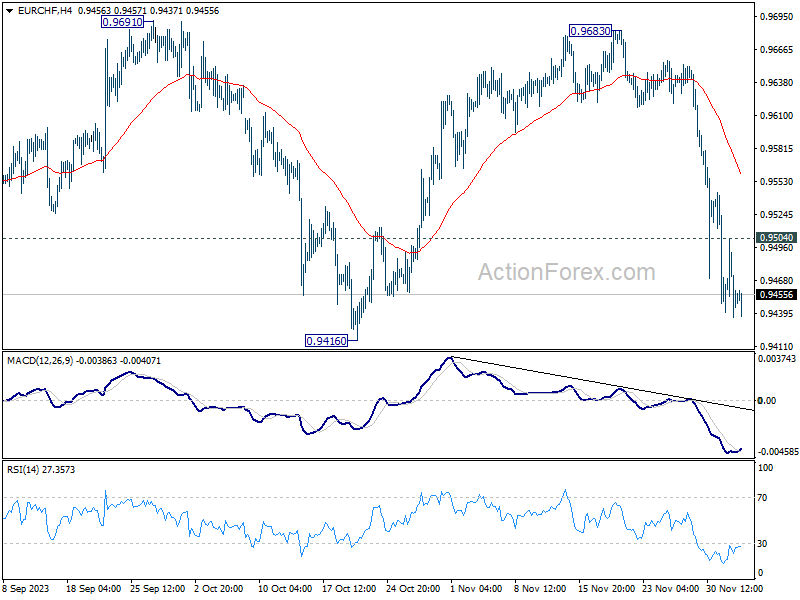

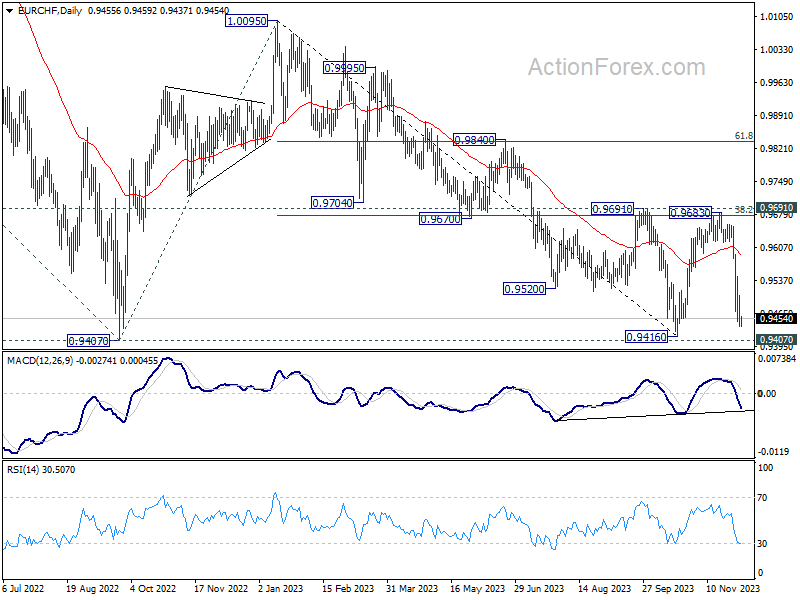

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9429; (P) 0.9467; (R1) 0.9497; More...

Intraday bias in EUR/CHF stays on the downside for retesting 0.9407/16 support zone. Decisive break there will resume larger down trend. On the upside, touching 0.9504 minor resistance will delay the bearish case and turn intraday bias neutral for consolidation first.

In the bigger picture, rejection by 0.9691 cluster resistance (38.2% retracement of 1.0095 to 0.9416 at 0.9675) maintains medium term bearishness in EUR/CHF. Firm break of 0.9047 support (2022 low) will resume long term down trend. Next target will be 61.8% projection of 1.1149 to 0.9407 from 1.0095 at 0.9018. For now, outlook will be neutral at best as long as 0.9683 holds.

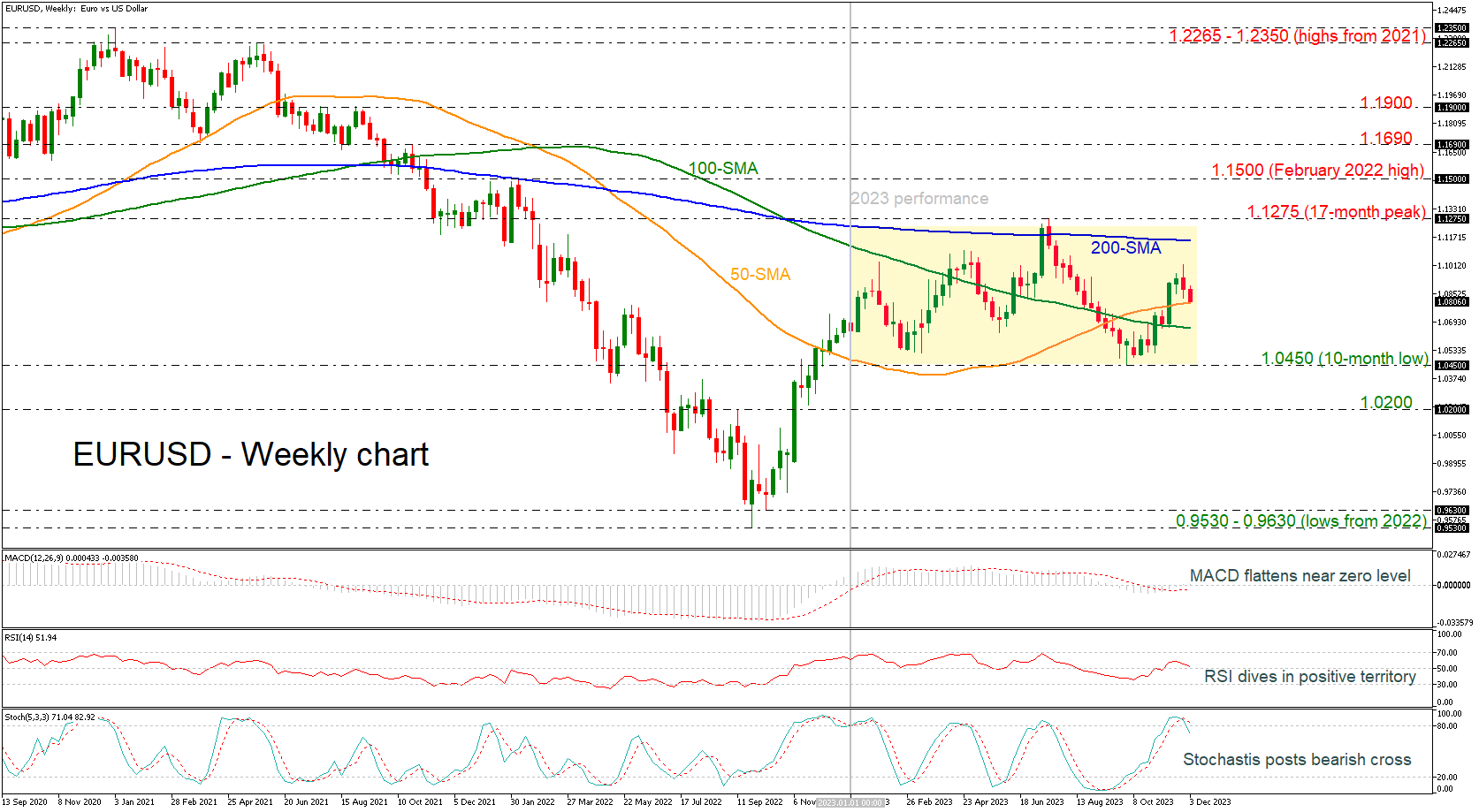

EURUSD Fails to Surprise During 2023

- EURUSD holds in trading range in weekly chart

- 50-week SMA acts as strong support

- RSI and stochastic suggest more losses

As the year is coming to an end, EURUSD’s market price is holding slightly higher than at the beginning of 2023. The pair is consolidating within a consolidation area with upper boundary the 200-week simple moving average (SMA) around 1.1150, despite the move above it in July, and lower boundary the ten-month low of 1.0450.

Currently, the price is testing the 50-week SMA at 1.0800, which is acting as strong support level for the bulls. Weekly oscillators suggest that upside momentum is losing steam, reflecting the latest pullback in the market. The RSI has turned down in the positive territory, while the stochastic oscillator posted a bearish crossover within its %K and %D lines in the overbought area, indicating bearish retracement. However, the MACD oscillator is flattening near its zero level, mirroring the bigger neutral outlook in the pair.

In case buyers take back control and pierce above the 200-week SMA of 1.1150, that would bring the price towards the 17-month high of 1.1275. Surpassing this level, the door could open for the 1.1500 psychological mark, registered in February 2022 ahead of the 1.1690 resistance, which would potentially be tested during next year.

Now should sellers stay in charge, the first obstacle to the downside might be the 100-week SMA at 1.0650, which has acted both as support and resistance in recent weeks. If violated, the spotlight would then shift to the 1.0450 barrier, which halted the retreat in early October.

Summarizing, the long-term outlook remains neutral. A decisive break above 1.1275 is needed to bring the positive outlook back into play. On the other hand, a decline below 1.0450 could switch the bias to bearish.

ECB’s Schnabel: Another rate hike now rather unlikely

In an interview with Reuters, ECB Executive Board member Isabel Schnabel remarked that the slowdown to 2.4% in Eurozone's November flash CPI a "very pleasant surprise." More importantly, that made "further rate increase rather unlikely".

Schnabel emphasized the significance of the decline in "underlying inflation", which has proven "more stubborn", is now also "falling more quickly than we had expected". Such trends have bolstered her confidence in achieving ECB's 2% inflation target no later than 2025.

However, she cautioned against premature victory declarations over inflation, expecting some upticks in the coming months due to fiscal changes and base effects, and not ruling out potential new spikes in energy or food prices.

On the growth front, Schnabel acknowledged mixed signals. While some hard data points are concerning, softer indicators, like PMI, are showing signs of stabilization and are "giving us hope."

She forecasts a gradual uptick in growth next year, driven by rising real incomes, which should boost confidence and consumption. Regarding the labor market, she noted some softening but does not anticipate a significant deterioration or a deep, prolonged recession.

ECB’s Influential Hawk Takes Further Rate Hikes Off the Table

Markets

Markets started off choppy yesterday, suggesting the bond-inspired everything-rally is losing steam. A backloaded eco calendar is keeping investors at bay as well. US yields recouped 2.1-9.6 bps from the huge losses incurred last month. The front end underperformed. German yields lagged behind but finished off intraday lows nevertheless. Changes varied between -0.8 bps (10-y) and +1.3 bps (2-y) with a noticeable outperformance of the very long end (30-y -4.4 bps). Stocks ended virtually flat in Europe while losing some ground in the US (Nasdaq -0.84%). The trade-weighted dollar index extended its recent bottoming out by rising above 103.62 (23.6% recovery on the Oct-Nov decline). EUR/USD lost mirror support at 1.0883. The pair neared the next reference at 1.08 (38.2% retracement) fast but it never came to an actual test. EUR/USD closed at 1.0836. Sterling’s stellar run grinded to a halt at the EUR/GBP 0.8558 resistance. Technical trading lifted the pair to 0.8578 at the close. Asian markets copy Wall Street’s meagre performance yesterday by losing ground. South Korea underperforms (-1.8%). News flow concentrates around inflation in the country as well as the Tokyo reading in Japan (see below). The Reserve Bank of Australia kept rates steady with further hikes, if any, contingent on the data. The Aussie dollar underperforms global peers this morning. For Europe, we retain ECB’s Schnabel interview by Reuters published this morning. The influential hawk took further rate hikes off the table in a dovish shift compared to just one month ago. Three unexpectedly benign inflation readings in a row changed Schnabel’s mind. She noted last month’s “remarkable” drop in the core gauge. Schnabel also warned against guiding markets to far ahead given how inflation is surprising. Dropping forward guidance was fitting when prices surged well beyond expectations but that works both ways, she reasons. On finishing PEPP reinvestments earlier than currently communicated (2025), Schnabel called it not a big deal as purchasing volumes are low and markets anticipate it already. The euro erased tiny gains after headlines hit the wires while Bund future price action suggests a lower open for cash yields. Attention later today shifts to the US with the JOLTS report as well as the services ISM for November. Market’s mindset suggests there’s still a risk for an asymmetric response to a negative surprise. That said, there’s only little room left to add to current market pricing which already assumes a 66% chance for a March cut. US bond spillovers, if any, to Europe should limite the damage for the dollar against the euro, especially after Schnabel’s comments. EUR/USD 1.08 is the first reference, followed by 1.0733/56.

News & Views

The Reserve bank of Australia kept its policy rate unchanged at 4.35%. The RBA raised the policy rate by 25 bps last month after 4 month pause as progress in bringing inflation to target was developing slower than forecast. The RBA now indicated that the new information it received since has been broadly in line with expectations. Monthly data suggested a further decline in goods inflation. The development of services inflation remains uncertain. Wage growth picked up in September, but the RBA doesn’t expect it to increase much further. Higher interest rate are working to establish a more sustainable balance between aggregate supply and demand as previous rate hikes continue to flow through the economy. This gives RBA the time to assess the impact of precious tightening in a data-dependent approach. RBA concludes that ‘whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks’. The tone of the RBA assessment maybe was a bit less hawkish than the market expected. The 2-y yield (4.08%) dropped 5 bps. AUD/USD fell from the 0.6610 area to currently 0.6585.

November inflation in South Korea and Japan this morning were softer than expected. CPI in SK declined 0.6% M/M slowing the Y/Y measure from 3.8% to 3.3% (3.5% was expected). Core inflation cooled from 3.0%. The BoK last week raised its inflation forecast for this year (3.6%) and next year (2.6%), but today indicated that it expects inflation to continue to decelerate at a moderate pace, assuming oil prices won’t significantly rise. November CPI excluding fresh food (monitored by the BoJ) in the Tokyo region dropped from 2.7% to 2.3%. The measure ex. fresh food and energy slowed to 3.6% from 3.8. The Tokyo data are seen as a good pointer for the national data that will be published on December 22. The BoJ holds its final meeting of the year on December 19. Softer inflation probably will reinforce the BoJ’s assessment that in can proceed very gradually when considering policy normalization.

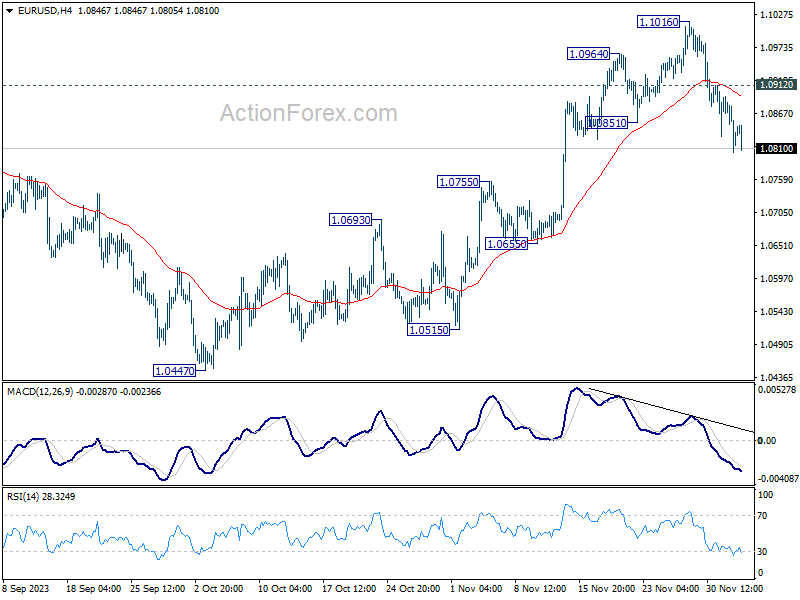

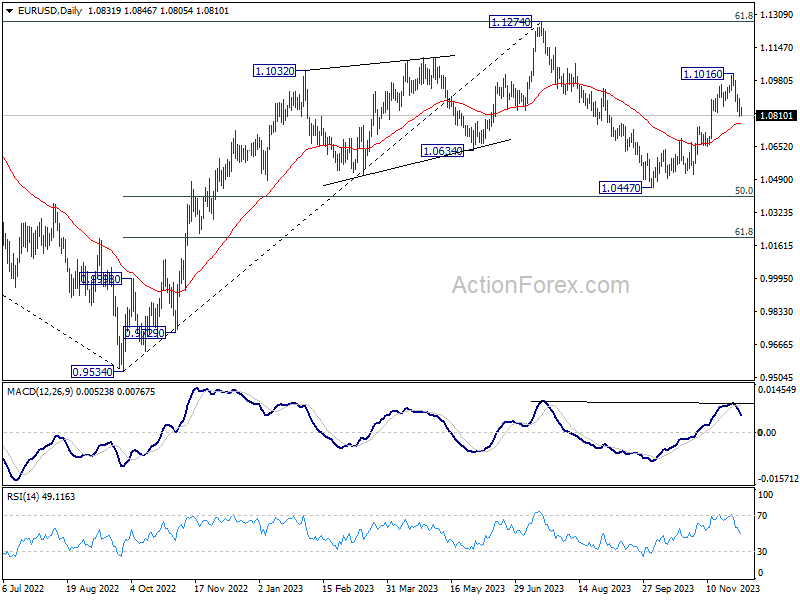

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0795; (P) 1.0845; (R1) 1.0886; More...

Intraday bias in EUR/USD remains on the downside for the moment. Current fall from 1.1016 short term to is in progress for 55 D EMA (now at 1.0770). On the upside, above 1.0912 minor resistance will turn intraday bias neutral again first. Further break of 1.1016 will resume the rise from 1.0447 to retest 1.1274 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

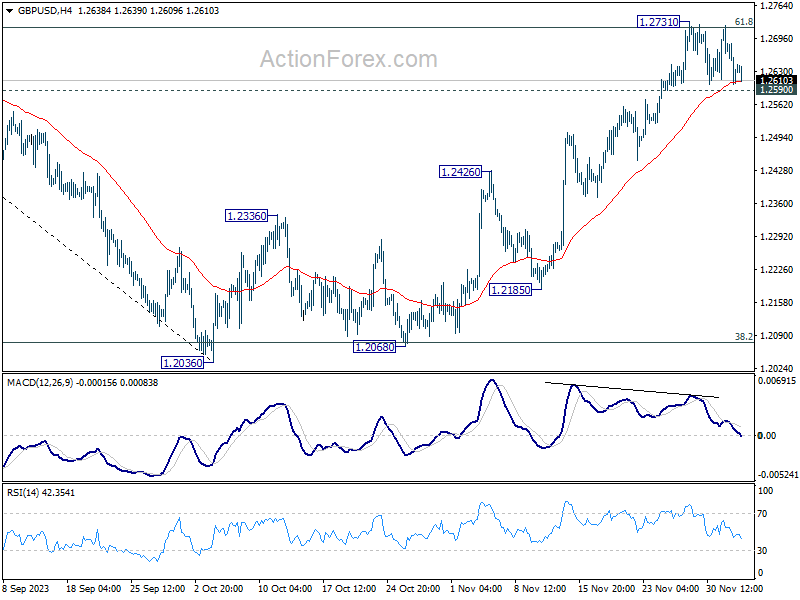

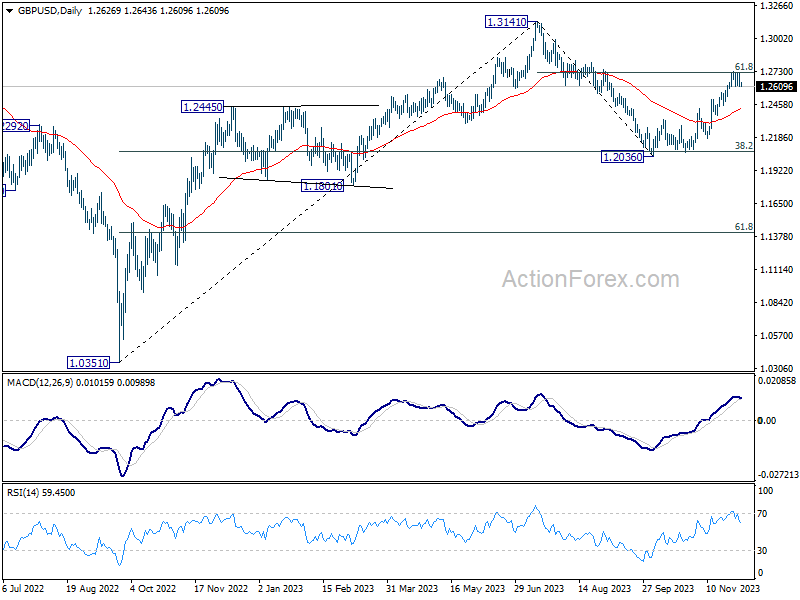

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2582; (P) 1.2654; (R1) 1.2703; More...

Range trading continues in GBP/USD and intraday bias remains neutral at this point. Further rally is expected as long as 1.2590 minor support holds. On the upside, decisive break of 1.2731 will resume the rally from 1.2036 for retesting 1.3141 high next. However, firm break of 1.2590 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

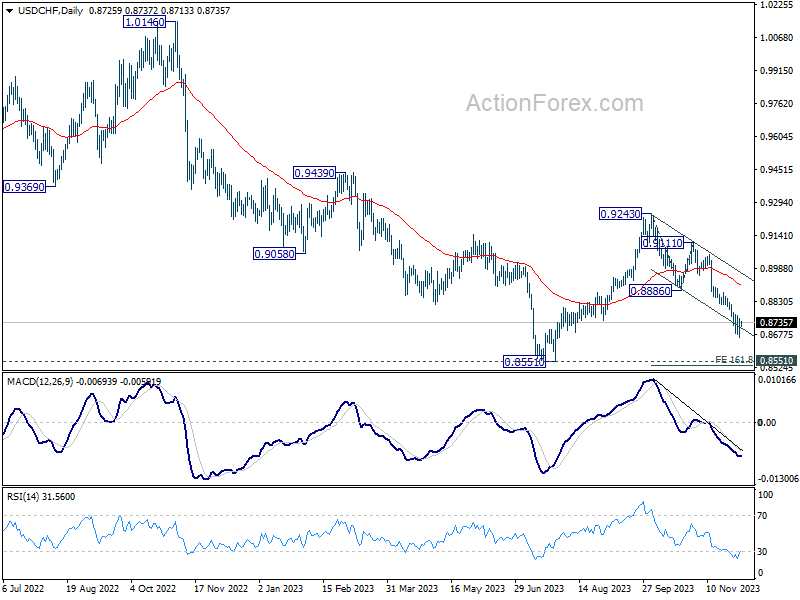

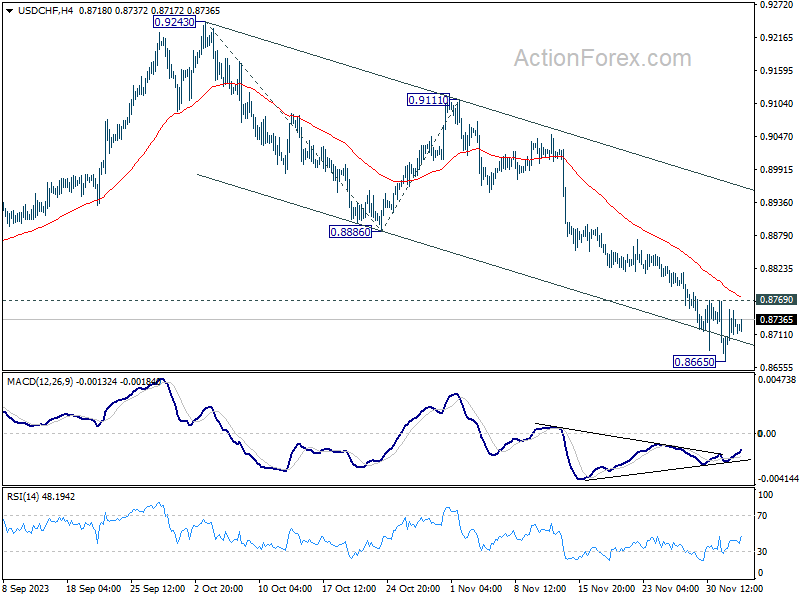

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8678; (P) 0.8717; (R1) 0.8766; More....

USD/CHF is staying in consolidation from 0.8665 and intraday bias stays neutral. Another fall is in favor as long as 0.8769 minor resistance holds. Below 0.8665 will resume the decline from 0.9243 to 161.8% projection of 0.9243 to 0.8886 from 0.9111 at 0.8533, which is close to 0.8551 low. However, break of 0.8769 minor resistance should indicate short term bottoming, and turn bias back to the upside for stronger recovery.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. For now, this will remain the favored case as long as 0.8886 support turned resistance holds.