Sample Category Title

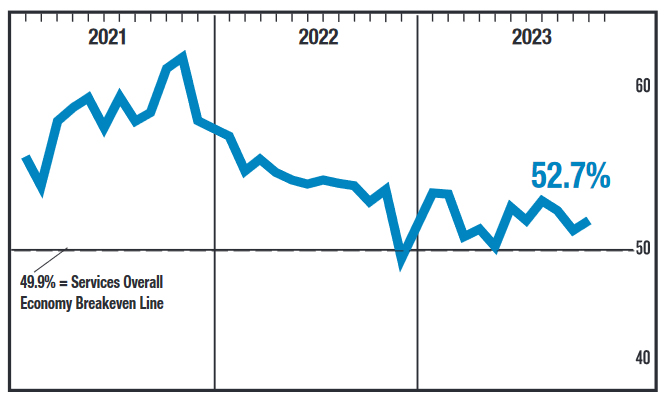

US ISM services rose to 52.7 in Nov, corresponds to 1% annualized GDP growth

US ISM Services PMI rose from 51.8 to 52.7 in November, a touch above expectation of 52.6. Looking at some details, business activity/production rose from 54.1 to 55.1. New orders was unchanged at 55.5. Employment rose slightly from 50.2 to 50.7. Price fell from 58.6 to 58.3.

ISM said: "The past relationship between the Services PMI and the overall economy indicates that the Services PMI for November (52.7 percent) corresponds to a 1-percent increase in real gross domestic product (GDP) on an annualized basis."

Sunset Market Commentary

Markets

US JOLTS job openings and the services ISM (both still to be published at CET 16:00) and to a lesser extent the ECB consumer expectations survey were supposed to provide some guidance as to whether recent decline in yields could finally slow down. Markets had frontloaded expectations on a first Fed and ECB rate hike as early as the March meetings (>70% discounted). In context, a bit surprisingly, it was ECB executive board member Schnabel who added fuel to the bond market rally. In an interview published on the ECB website, she labelled the November CPI flash estimate as a pleasant surprise, especially as underlying inflation which until now has proven more stubborn, is now falling more quickly than expected. Even as she reiterated that central banks have to err the side of caution, she concluded that a further rate increase now is rather unlikely. Reconfirming a data-dependent approach, she even didn’t formally rule out a rate cut before mid-year. She also confirmed that the ECB is going to discuss reinvestments under PEPP in a not-too-distant future. Later in the session, 1-y inflation expectations in the ECB October consumer survey remained at 4.0% while an easing to 3.8% was expected. 3-y expectations remained at 2.5%. Other topics in the survey showed that consumers turned slightly more negative on their nominal income and spending for next year. The also expect a slightly bigger economic contraction (-1.3% vs -1.2%) for the next 12 months. Expectations for unemployment over next 12 months (11.4%) was unchanged. This report evidently wasn’t enough to profoundly change the post-Schnabel sentiment on EMU interest rate markets. German yields currently again are ceding between 6 bps (2-y) and 10 bps (30-y). Markets now discount a >80% chance of a first 25 bps ECB rate cut in March. US yields also ease further though less pronounced than in EMU, declining between 1 bp (2-y) and 5 bps (30-y). Contrary to what was the case of late, UK Gilts today even slightly outperform Bunds (minus 9-11 bps across the curve. European equities opened hesitantly (spill-over from Asia/China) but gradually again received support from lower yields. The EuroStoxx 50 extends gains north of 4400 (+0.55%). The 4491.5 cycle top is within reach. US equities open with modest losses (S&P 500: -0.25%). Oil continues drifting south (Brent $77.6 p/b) even as OPEC+ tries to convince markets that it will deliver on the announced production cuts. Gold this time doesn’t profit from lower yields ($ 2028 p/oz). On FX markets, the dollar gains modestly (DXY 103.75). The yen slightly outperforms on lower core yields (USD/JPY 147). EUR/USD losses also stay modest despite the sharp further decline in EMU yields (1.082). In line with yesterday’s price action EUR/GBP is going nowhere (0.857) after last week’s sterling outperformance.

News & Views

Rating agency Moody’s changed the outlook on China’s A1 credit rating from stable to negative. The new assessment reflects rising evidence of financial support by the government and wider public sector to stressed (mostly related to property sector) regional/local governments and state-owned enterprises. These risk significantly deteriorating Chinese debt dynamics. Moody’s sees increased risks related to structurally and persistently lower growth as well. Growth is forecast at 4% for next year and 2025 before averaging 3.8% from 2026-2030. That’s significantly below this year’s official 5% growth target. Rating agency S&P uses a similar A+ rating for China though still with a stable outlook. Both Moody’s and S&P last downgraded China back in 2017 citing concerns that efforts to support growth would spur rising debt in the economy. Main Chinese stock markets closed 1.6% to 2% weaker this morning with CNY slightly weakening towards USD/CNY 7.15.

Brazilian GDP growth beat consensus once more. The economy grew marginally in Q3 (0.1% Q/Q), avoiding a feared decline (-0.3% Q/Q) while the Q2 figure was slightly increased from 0.9% to 1%. A demand-side breakdown showed positive contributions from household consumption (1.1% Q/Q), government spending (+0.5% Q/Q) and net export (export +3% vs import -2.1%). Investment (-2.5% Q/Q) were the only drag on growth. The resilient Brazilian economy suggests that the Brazilian central bank will keep a cautious approach during its rate cutting cycle which started in August. Three 50 bps rate cuts brought the policy rate at the current level of 12.25% since, supported by disinflationary forces. Brazilian inflation was 4.82% Y/Y in October compared to this year’s 3.25% inflation target (with a permissible range of 1.5 ppt).

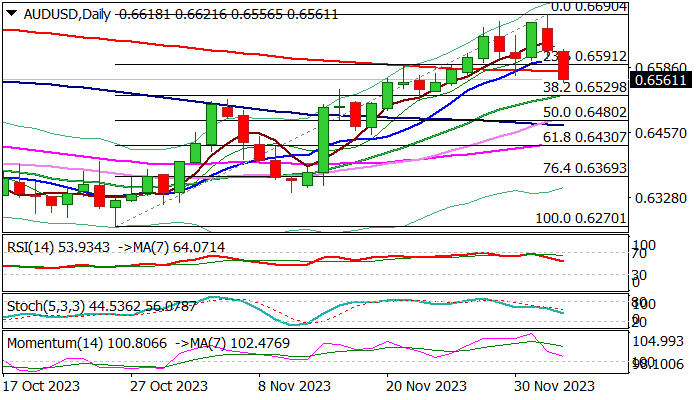

AUD/USD: Falls Further as RBA Decision Disappoints Traders

AUDUSD extends pullback from four month high (0.6690) into second straight day, additionally pressured from decision of Australian Central Bank to keep interest rates unchanged.

Although the RBA’s statement kept hawkish bias, traders were disappointed and continued to sell Aussie dollar.

Fresh weakness broke below 200DMA (0.6578), to further soften near-term structure for attack at pivotal support at 0.6529 (Fibo 38.2% of 0.6270/0.6690, reinforced by rising 20DMA) violation of which would generate reversal signal and open way for deeper drop.

Sharp loss of bullish momentum and south-heading RSI contribute to negative outlook, in addition to daily cloud twist early next week, which could be magnetic.

Upticks should stay capped under 0.6600 zone to keep bears in play.

Res: 0.6578; 0.6591; 0.6614; 0.6663.

Sup: 0.6529; 0.6502; 0.6480; 0.6430.

XAUUSD: Fake Breakout or New Reality?

Gold price experienced a notable turnaround, gaining fresh bids after a $125 pullback from its recent peak. Federal Reserve Chair Jerome Powell's recent speech suggested a reluctance towards aggressive rate cuts, dampening speculations of immediate policy easing. Market sentiment leans towards the belief that the Fed has concluded its tightening cycle, with a growing likelihood of a rate cut by March 2024. A modest uptick in the US Dollar acts as a headwind, yet gold maintains a steady bullish tone amid concerns over a potential conflict in the Middle East. The ongoing global economic uncertainties and a shift to safer assets contribute to gold's upside, with upcoming economic data and the monthly jobs report anticipated to guide future trends.

XAUUSD - BEFORE & NOW

In my last article on GOLD (XAUUSD), I mentioned that the safe approach to consider before selling Gold would be a break below the trendline, where the retest of the trendline would serve as the entry. However, due to rumors of possible conflict and civil unrest across several quarters, it is evident that earlybird investors may have already begun stacking up Gold as a hedging strategy. By the way, price didn’t break the trendline support; at least not until recently.

XAUUSD - W1 Timeframe

XAUUSD on the weekly timeframe appears to have hit the trendline resistance on the weekly timeframe, leading to a rejection of the price action, and ultimately a bearish move. It is notable to me, however, that the recent high is an actual break of structure, not a mere fakeout. This said, I expect price to drop into the demand zone I have marked in order to regain its bullish momentum. The confluences at that ‘point-of-interest’ include;

- Bullish array of the moving averages;

- 50-period moving average support;

- Trendline support;

- 70% of the Fibonacci retracement; and

- A rally-base-rally demand zone.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1938.50

- Invalidation: 2071.28

CONCLUSION

The trading of CFDs comes at a risk. To succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

Australian Dollar Slides as RBA Holds Rates

- RBA maintains cash rate at 4.35%

- Australian dollar extends slide

The Australian dollar is down sharply for a second straight day. In the European session, AUD/USD is trading at 0.6561, down 0.88%. The Australian dollar has taken a tumble this week, falling 1.70%.

RBA holds rates as expected

The Reserve Bank of Australia maintained the cash rate at 4.35% today. The move had been fully priced in by the markets, so that was no surprise. Nevertheless, the Australian dollar is down sharply, largely on speculation that the RBA’s pause is further speculation that the central bank’s tightening cycle is over.

RBA Governor Michele Bullock trotted out her familiar script that further tightening was on the table if warranted by the data, but after five straight pauses, the markets have their focus on a rate cut in mid-2024. Bullock mentioned that were “significant uncertainties around the outlook” and expressed concern about China. Bullock’s somewhat hawkish rhetoric didn’t help the Australian dollar but was a reminder that although a rate hike is unlikely at the next meeting in February, it can’t be ruled out.

China has endured a bumpy recovery from Covid and earlier today Moody’s rating agency cut its credit outook for China from stable to negative. Moody’s cited concern over slowing growth, rising debt and the crisis in the property sector. China is Australia’s largest export market and a weaker Chinese economy is bad news for Australia’s export sector and the Australian dollar.

The US releases the ISM Services PMI later today. The October print fell to 51.8, down from 53.6 and the lowest in five months. The PMI isn’t expected to show much change in November, with a consensus estimate of 52.0.

Australia releases GDP on Wednesday. The economy is expected to have grown by 1.8% in the third quarter, compared to 1.8% in Q2. An unexpected GDP reading could have a strong impact on the movement of the Australian dollar.

AUD/USD Technical

- There is support at 0.6530 and 0.6494

- 0.6639 and 0.6712 are the next resistance lines

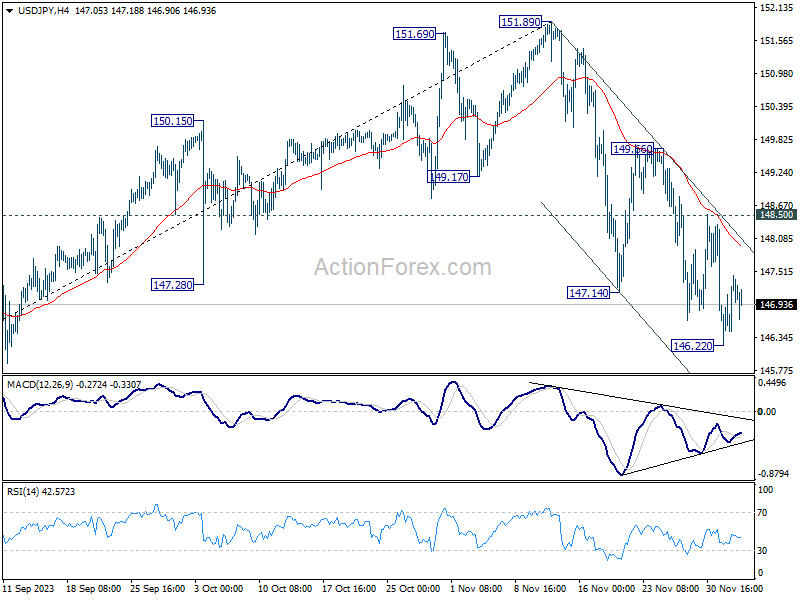

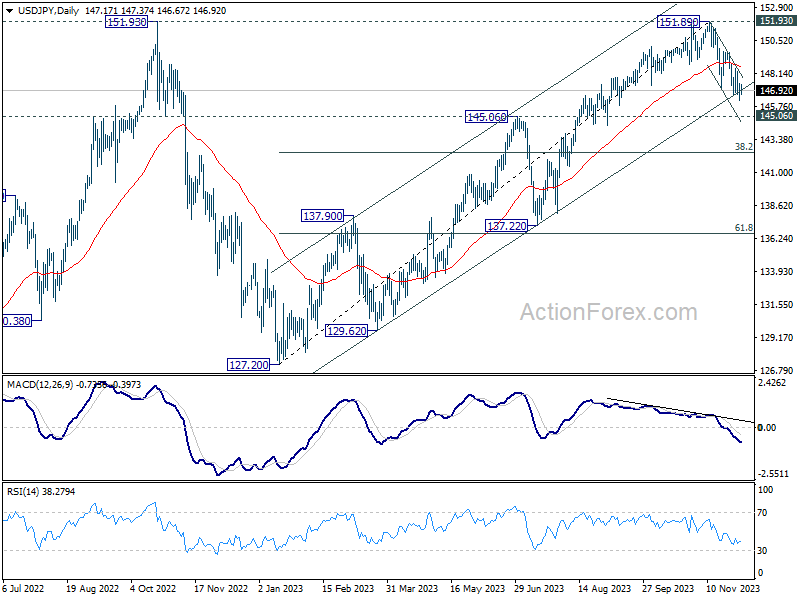

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.48; (P) 146.97; (R1) 147.70; More...

Intraday bias in USD/JPY remains neutral for consolidation above 146.22 temporary top. Further decline is expected as long as 148.50 resistance holds, even in case of stronger recovery. On the downside, firm break of 146.22 will resume the fall from 151.89 to 145.06 key support level.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

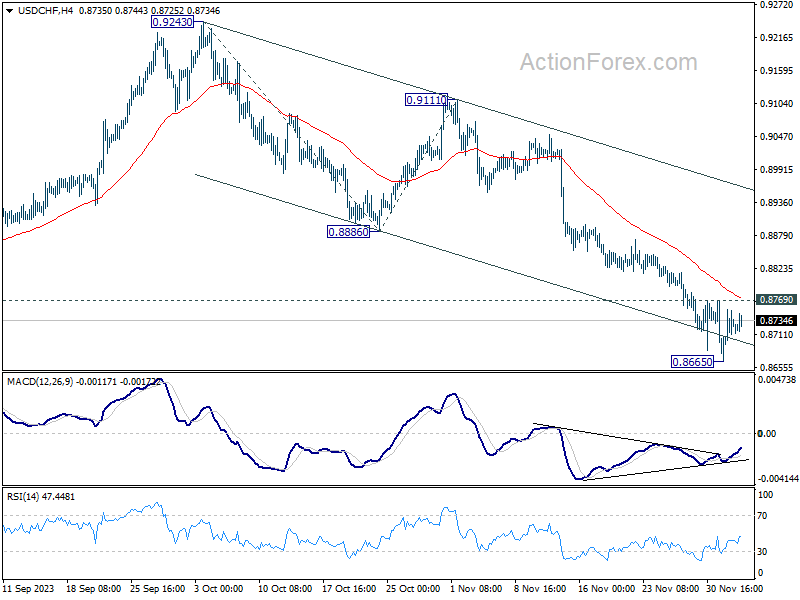

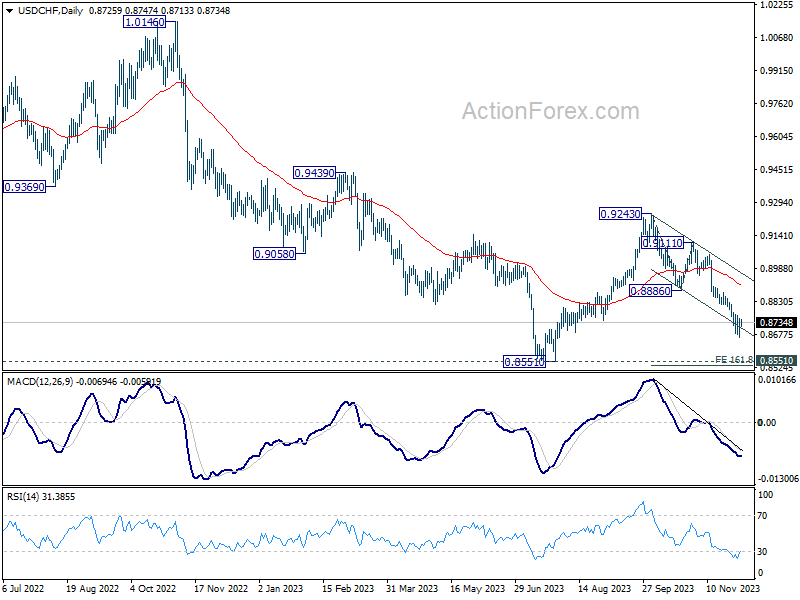

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8678; (P) 0.8717; (R1) 0.8766; More....

Intraday bias in USD/CHF stays neutral and outlook is unchanged. Another fall is in favor as long as 0.8769 minor resistance holds. Below 0.8665 will resume the decline from 0.9243 to 161.8% projection of 0.9243 to 0.8886 from 0.9111 at 0.8533, which is close to 0.8551 low. However, break of 0.8769 minor resistance should indicate short term bottoming, and turn bias back to the upside for stronger recovery to 0.8886 support turned resistance.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. For now, this will remain the favored case as long as 0.8886 support turned resistance holds.

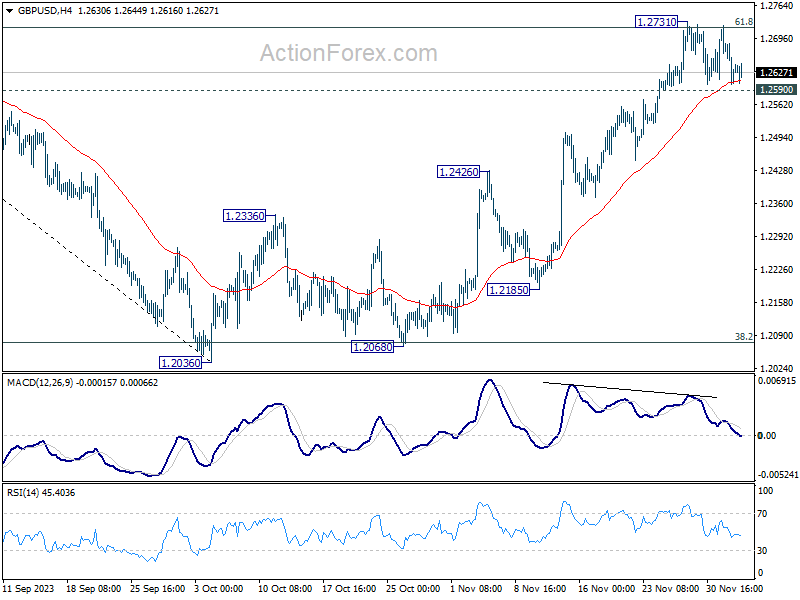

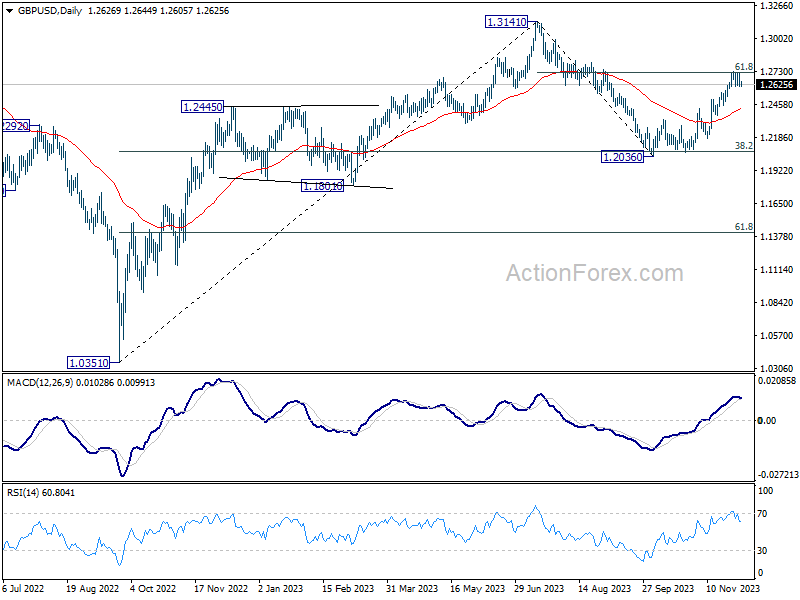

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2582; (P) 1.2654; (R1) 1.2703; More...

GBP/USD is still bounded in range of 1.2590/2731 and intraday bias remains neutral. On the upside, decisive break of 1.2731 will resume the rally from 1.2036 for retesting 1.3141 high next. However, firm break of 1.2590 will confirm short term topping, and turn bias back to the downside for deeper pullback to 55 D EMA (now at 1.24328).

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

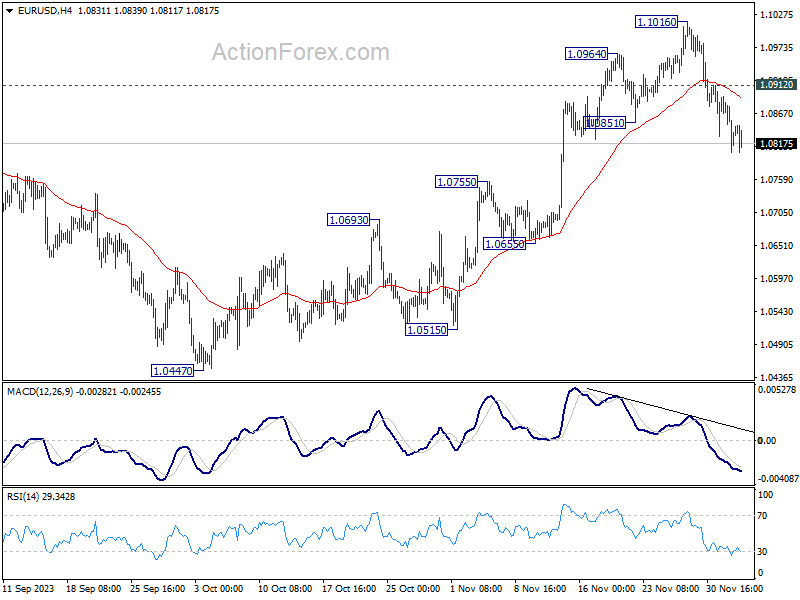

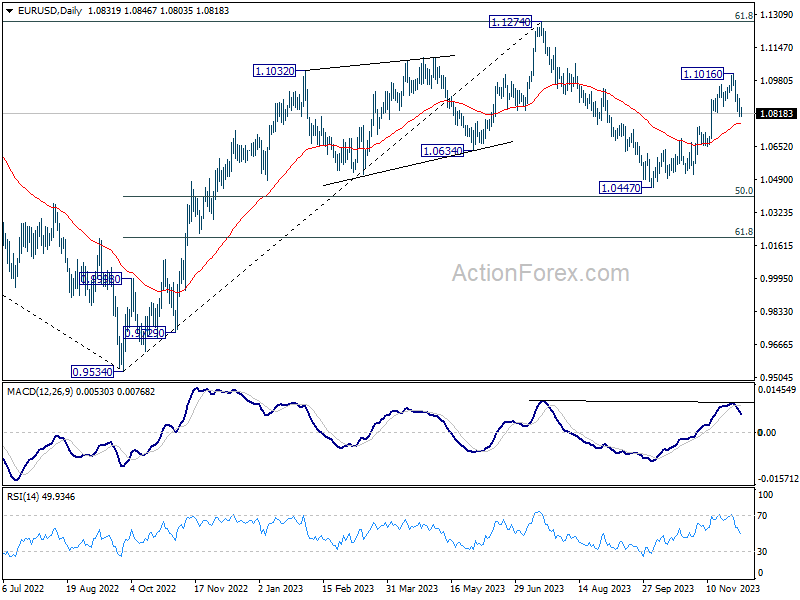

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0795; (P) 1.0845; (R1) 1.0886; More...

EUR/USD's fall from 1.1016 is still in progress and intraday bias remains on the downside. Next target is 55 D EMA (now at 1.0770. Sustained break there will target 1.0447 support next. On the upside, above 1.0912 minor resistance will turn intraday bias neutral again first. Further break of 1.1016 will resume the rise from 1.0447 to retest 1.1274 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

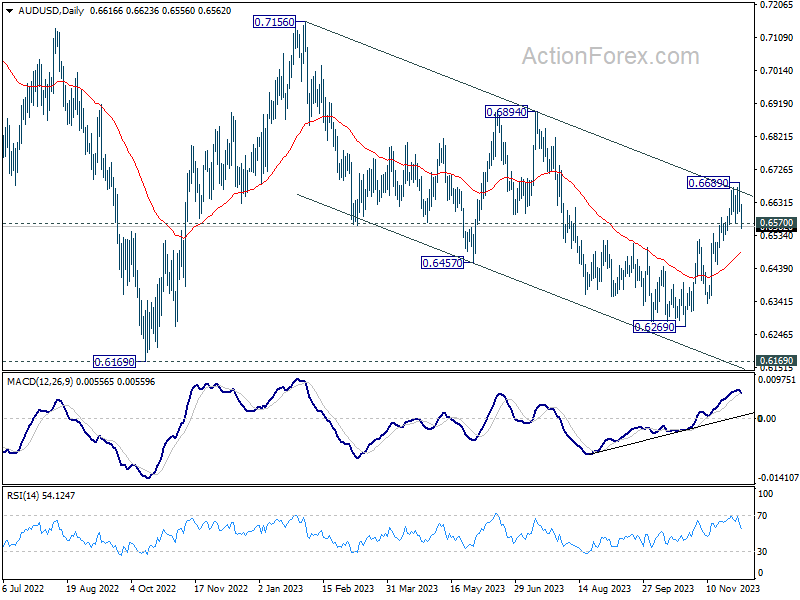

Moody’s Downgrade on China Weighs on Commodity Currencies, AUD Leads Decline

Commodity currencies, particularly Australian Dollar, are experiencing notable selling pressure today. However, it should be noted that European investor sentiment, while not explicitly full-blown risk-on, clearly lacks the typical features of risk aversion. In the US, futures markets are just slightly down, indicating a cautious rather than outright negative sentiment among traders. This subdued response across markets suggests that investors are not engaging in widespread risk aversion but are instead selectively cautious.

A key factor influencing market sentiment is the today's decision by Moody's to downgrade its outlook on China's government credit ratings from stable to negative. This adjustment reflects increasing expectations that the Chinese government will be compelled to provide additional financial support to heavily indebted local governments and state-owned enterprises. According to Moody's, this necessity poses significant risks to China's overall fiscal, economic, and institutional integrity. The statement from Moody's emphasizes concerns about "structurally and persistently lower medium-term economic growth" and challenges within China's property sector, indicating broader economic issues that could impact global markets.

In other currency markets, Yen and Dollar are emerging as stronger contenders, followed by Sterling and Swiss Franc. Euro is trailing behind its European counterparts, especially after dovish remarks fro a know hawk ECB Executive Board member Isabel Schnabel.

Technically, AUD/USD's break of 0.6570 support today indicates first rejection by medium term channel resistance from 0.7156. It's still early to conclude if the rise from 0.6269 has completed. But deeper fall is now in favor back to 55 D EMA (now at 0.6482). Sustained break there will argue that the whole fall from 0.7156 is still in progress for another low. Nevertheless, strong bounce from the EMA will keep the bullish scenario alive, that is, fall from 0.7156 has completed as a correction with three waves down to 0.6269.

In Europe, at the time of writing, FTSE is down -0.50%. DAX is up 0.26%. CAC is up 0.33%. Germany 10-year yield is down -0.0070 at 2.289. Earlier in Asia, Nikkei fell -1.37%. Hong Kong HSI fell -1.91%. China Shanghai SSE fell -1.67%. Singapore Strait Times fell -0.22%. Japan 10-year JGB yield fell -0.0179 to 0.673.

ECB's Schnabel: Another rate hike now rather unlikely

In an interview with Reuters, ECB Executive Board member Isabel Schnabel remarked that the slowdown to 2.4% in Eurozone's November flash CPI a "very pleasant surprise." More importantly, that made "further rate increase rather unlikely".

Schnabel emphasized the significance of the decline in "underlying inflation", which has proven "more stubborn", is now also "falling more quickly than we had expected". Such trends have bolstered her confidence in achieving ECB's 2% inflation target no later than 2025.

However, she cautioned against premature victory declarations over inflation, expecting some upticks in the coming months due to fiscal changes and base effects, and not ruling out potential new spikes in energy or food prices.

On the growth front, Schnabel acknowledged mixed signals. While some hard data points are concerning, softer indicators, like PMI, are showing signs of stabilization and are "giving us hope."

She forecasts a gradual uptick in growth next year, driven by rising real incomes, which should boost confidence and consumption. Regarding the labor market, she noted some softening but does not anticipate a significant deterioration or a deep, prolonged recession.

Eurozone PPI at 0.2% mom, -9.4% yoy in Nov, matches expectations

Eurozone PPI came in at 0.2% mom, -9.4% yoy in November, matched expectations. For the month, industrial producer prices increased by 1.0% mom in the energy sector and by 0.1% mom for durable consumer goods, while prices remained stable for capital goods, and prices decreased by -0.1% mom for non-durable consumer goods and by -0.3% mom for intermediate goods. Prices in total industry excluding energy decreased by -0.2% mom.

EU PPI was at 0.2% mom, -8.7% yoy. The biggest monthly increases in industrial producer prices were observed in Ireland (+4.9%), Italy (+2.2%) and the Netherlands (+0.7%), while the largest decreases were recorded in Luxembourg (-3.7%), Latvia (-2.7%) and Greece (-1.9%).

Eurozone PMI composite finalized at 47.5, on the brink of recession

Eurozone's PMI Services for November showed a slight improvement, finalizing at 48.7, up from 47.8 in October. PMI Composite also experienced an uptick, reaching 47.5 from the previous month's 46.5.

Looking at individual member states, PMI composite revealed mixed results. Ireland registered a three-month high at 52.3, while Spain hit a three-month low at 49.8. Italy reported a two-month high at 48.1, and Germany saw a four-month high at 47.8. France remained unchanged, with its PMI holding steady at 44.6.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, stated, "The service sector maintained its downward slide in November." He noted that the modest improvement in the activity index offers little optimism for a swift recovery in the immediate future. De la Rubia also highlighted concerning trends, such as the fifth consecutive monthly decline in new business and subdued business expectations, which remain "well below the long-term average."

Outlook for Eurozone's economy, as inferred from these PMI indicators, is not encouraging. De la Rubia mentioned, "As per our GDP nowcast, factoring in the latest PMI indicators, a fall in GDP is on the cards for the fourth quarter." He warned that if two consecutive quarters of negative growth define a recession, the Eurozone is currently "on the brink" of one.

UK PMI services finalized at 50.9, composite at 50.7

UK's PMI Services for November improved to 50.9 from October's 49.5, indicating expansion for the first time in four months. PMI Composite also rose to 50.7, crossing the critical 50 mark for the first time since July.

Tim Moore of S&P Global Market Intelligence remarked on the positive shift: "UK service providers moved back into expansion mode" However, he cautioned about inflation, noting "another round of strong input cost pressures" mainly due to rising staff wages. This improvement in the service sector, although positive, is shadowed by ongoing inflationary challenges.

RBA holds rates following sparse information since last meeting

RBA kept its cash rate target unchanged at 4.35%, aligning with market expectations. The central bank's latest statement indicates continued openness to further rate hikes, but emphasizes that any such decision "will depend upon the data and the evolving assessment of risks." This stance reflects a careful approach, as RBA awaits more comprehensive data, particularly the Q4 inflation figures due in January, before its next meeting in early February.

In its review of the "limited information" available since November meeting, RBA acknowledged that the data were "broadly in line with expectations." The October monthly CPI update suggested continued moderation in inflation, but did not provide substantial insights into services inflation. While wage growth accelerated in Q3, it is "not expected to increase much further". The labor market conditions are seen as "continuing to ease gradually," though they remain tight.

RBA also highlighted "still significant uncertainties" regarding the economic outlook. It pointed out the potential for persistent services inflation in Australia. Domestically, the uncertainties include the lag effects of monetary policy and household consumption patterns. On a global scale, the ongoing uncertainty around Chinese economy's trajectory and the broader implications of international conflicts were noted as significant factors influencing Australia's economic environment.

Japan's Tokyo CPI core slows to 2.3% yoy in Nov, core-core still stick at 3.6% yoy

November's inflation data in Japan's capital Tokyo shows a notable slowdown. CPI core, which excludes fresh food, dropped from 2.7% yoy to 2.3% yoy, falling slightly below the expected 2.4%. This decline brings the reading further towards BoJ target of 2%.

Headline CPI also experienced a decrease, falling back to 2.6% yoy. This reduction comes after an unexpected rise from 2.8% yoy in September to 3.2% yoy in October.

Furthermore, CPI core-core, which excludes both food and energy, showed some progress. It declined from 3.8% yoy to 3.6% yoy, a reduction from its peak of 4.0% seen in July and August. However, the still relatively high CPI core-core reading indicates that underlying inflationary pressures remain persistent within the economy, despite the overall slowdown.

Japan's PMI services finalized at 50.8, weakening in a year of strong growth

Japan's PMI Services for November was finalized at 50.8, down from October's 51.6, marking the weakest reading since November 2022. PMI Composite also fell to 49.6, down from 50.5 in the previous month, indicating the first contraction since December 2022.

Trevor Balchin, Economics Director at S&P Global Market Intelligence, contextualized these numbers, stating, "November data signalled a further loss of momentum in the services sector, but this should be viewed in the context of a year of strong growth." He highlighted that Business Activity Index for 2023 is trending at 53.7, the highest annual reading since the survey's inception in 2007.

Balchin also pointed out several positive aspects in the latest survey. The rise in new business, sustained employment growth, and the increase in outstanding work indicate ongoing economic activity. Furthermore, the 12-month outlook for activity improved and was "among the strongest on record". Despite these optimistic signs, price pressures in November eased but remained above long-term trends.

China's PMI services rose to 51.5 in Nov, composite rose to 51.6

China's Caixin PMI Services rose from 50.4 to 51.5 in November, above expectation of 50.8. PMI Composite rose from 50.0 to 51.6.

Wang Zhe, Senior Economist at Caixin Insight Group said: "Overall, the macroeconomy showed signs of a positive recovery, with steady growth in consumer spending, solid progress in industrial production and improved market expectations.

"However, due to various unfavorable factors, both domestic and external demand still face challenges and employment pressures remain relatively high. The foundation for economic recovery needs to be further consolidated."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0795; (P) 1.0845; (R1) 1.0886; More...

EUR/USD's fall from 1.1016 is still in progress and intraday bias remains on the downside. Next target is 55 D EMA (now at 1.0770. Sustained break there will target 1.0447 support next. On the upside, above 1.0912 minor resistance will turn intraday bias neutral again first. Further break of 1.1016 will resume the rise from 1.0447 to retest 1.1274 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Nov | 2.60% | 3.30% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Nov | 2.30% | 2.40% | 2.70% | |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Nov | 3.60% | 3.80% | ||

| 00:30 | AUD | Current Account (AUD) Q3 | -0.2B | 3.5B | 7.7B | 7.8B |

| 01:45 | CNY | Caixin Services PMI Nov | 51.5 | 50.8 | 50.4 | |

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.35% | |

| 07:45 | EUR | France Industrial Output M/M Oct | -0.30% | -0.20% | -0.50% | -0.60% |

| 08:45 | EUR | Italy Services PMI Nov | 49.5 | 48.2 | 47.7 | |

| 08:50 | EUR | France Services PMI Nov F | 45.4 | 45.3 | 45.3 | |

| 08:55 | EUR | Germany Services PMI Nov F | 49.6 | 48.7 | 48.7 | |

| 09:00 | EUR | Eurozone Services PMI Nov F | 48.7 | 48.2 | 48.2 | |

| 09:30 | GBP | Services PMI Nov F | 50.9 | 50.5 | 50.5 | |

| 10:00 | EUR | Eurozone PPI M/M Oct | 0.20% | 0.20% | 0.50% | |

| 10:00 | EUR | Eurozone PPI Y/Y Oct | -9.40% | -9.40% | -12.40% | |

| 14:45 | USD | Services PMI Nov F | 50.8 | 50.8 | ||

| 15:00 | USD | ISM Services PMI Nov | 52.6 | 51.8 |