Sample Category Title

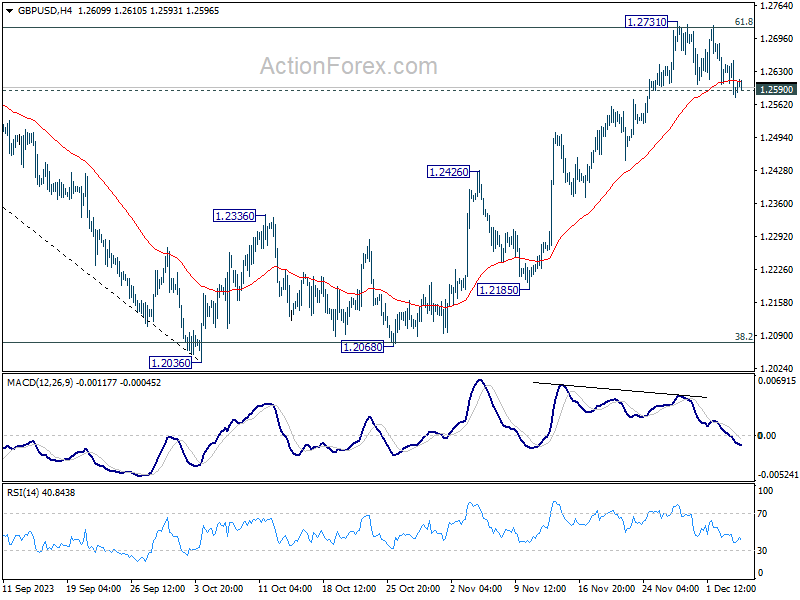

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2565; (P) 1.2608; (R1) 1.2640; More...

GBP/USD's breach of 1.2590 minor support suggests short term topping at 1.2731, on bearish divergence condition in 4H MACD. Intraday bias is mildly on the downside for deeper pull back to 55 D EMA (now at 1.2427). For now, risk will stay on the downside as long as 1.2731 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

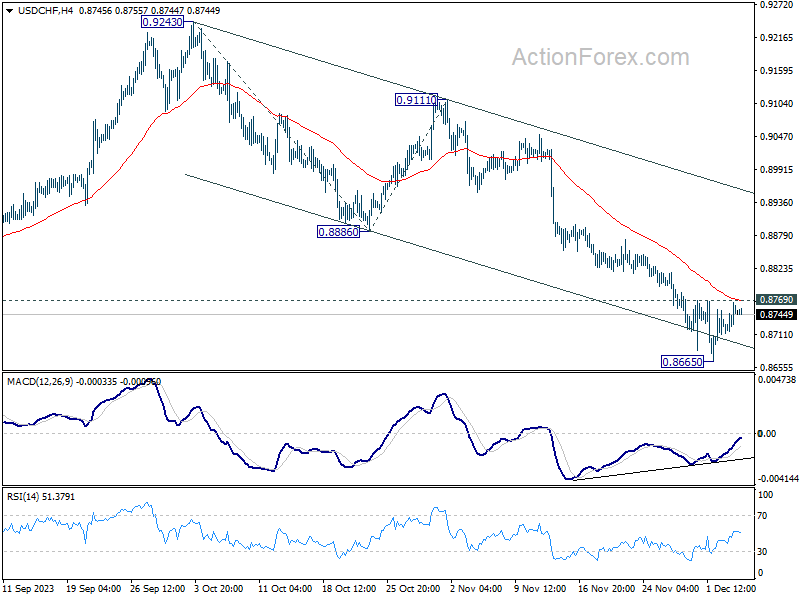

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8743; (R1) 0.8773; More....

Range trading continues in USD/CHF and intraday bias remains neutral for the moment. Another fall is in favor as long as 0.8769 minor resistance holds. Below 0.8665 will resume the decline from 0.9243 to 161.8% projection of 0.9243 to 0.8886 from 0.9111 at 0.8533, which is close to 0.8551 low. However, break of 0.8769 minor resistance should indicate short term bottoming, and turn bias back to the upside for stronger recovery to 0.8886 support turned resistance.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. For now, this will remain the favored case as long as 0.8886 support turned resistance holds.

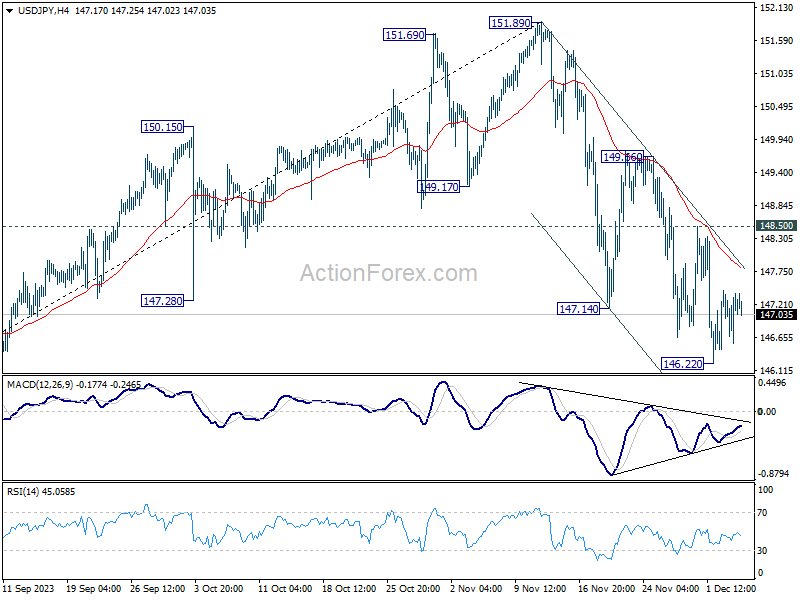

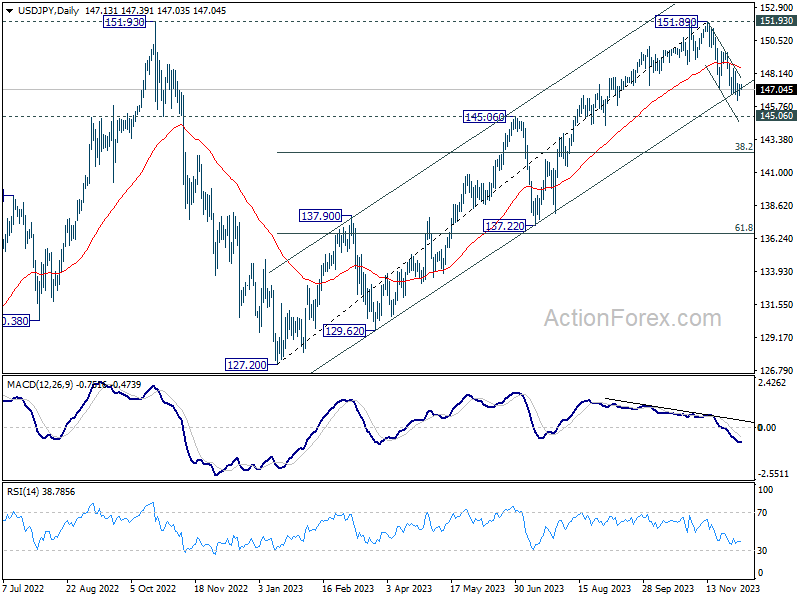

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.68; (P) 147.03; (R1) 147.51; More...

USD/JPY is still bounded in consolidation from 146.22 and intraday bias stays neutral for the moment. Further decline is expected as long as 148.50 resistance holds, even in case of stronger recovery. On the downside, firm break of 146.22 will resume the fall from 151.89 to 145.06 key support level.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

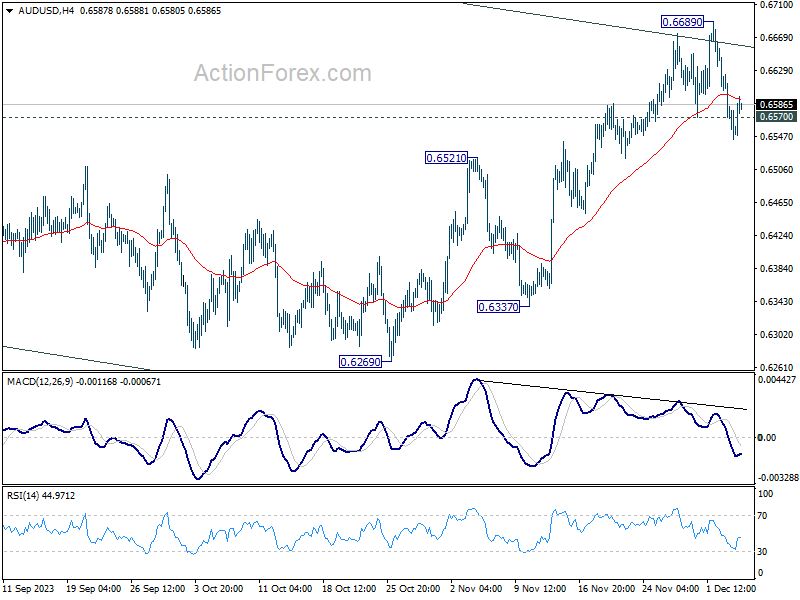

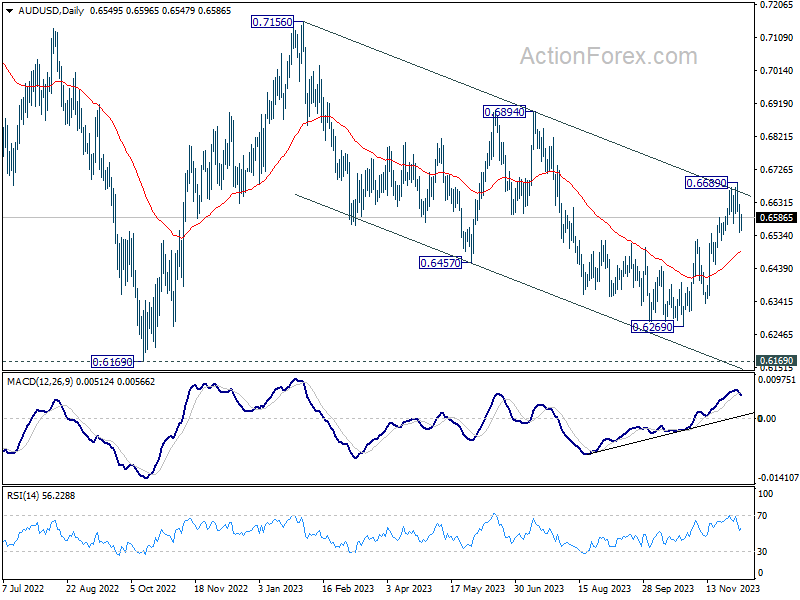

AUD/USD Daily Report

Daily Pivots: (S1) 0.6523; (P) 0.6573; (R1) 0.6601; More...

AUD/USD's breach of 0.6570 support suggests that a short term top was formed at 0.6689, after rejection by falling channel resistance. Intraday bias is now mildly on the downside for 55 D EMA (now at 0.6488). For now, risk is mildly on the downside as long as 0.6689 resistance holds, in case of recovery.

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. price actions from 0.6169 (2022 low) could be just a medium term corrective pattern, with rise from 0.6269 as the third leg. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

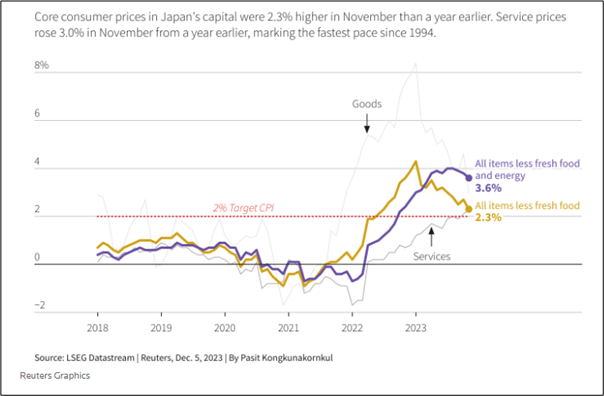

USD/JPY: Bearish Momentum Remains Intact Despite Softer Tokyo CPI

- Tokyo’s CPI for November slowed down further due to a recent drop in oil prices.

- Tokyo’s services prices accelerated to 3% y/y in November, its fastest pace since 1994.

- Japan’s latest consumer sentiment data for November also improved to its highest level since August 2023.

- A boost in consumer sentiment coupled with services inflation on the uptick indicates signs of a potential demand-driven increase in prices has emerged in Japan.

- Technical analysis suggests a further potential weakness in USD/JPY.

Yesterday Japan’s statistical government agency released November’s CPI data for Tokyo, which tends to be a leading economic indicator for Japan’s nationwide inflationary environment.

The headline Tokyo’s CPI print for November has continued to decelerate to 2.6% y/y from 3.3% y/y in October which indicated the lowest inflationary growth reading in around one and a half-year due to the recent drop in oil prices since late September 2023.

In addition, the Tokyo core-core CPI (after stripping out fresh food and energy components), a closely watched inflationary gauge by the Bank of Japan (BoJ) also slowed to 3.6% y/y from 3.8% y/y in October.

Tokyo services inflation has risen at a faster pace since 1994

Fig 1: Tokyo CPI readings for November 2023 (Source: Reuters, click to enlarge chart)

In contrast, service prices in Tokyo rose at their fastest pace since 1994 to a record gain of 3% y/y in November, indicating an increase in the odds of sustainable wage-driven inflationary growth that BoJ is monitoring to justify more tweaks to normalize its current ultra-accommodative monetary policy.

BoJ Governor Ueda has stressed in his public speeches that the recent cost-push inflation needs to be replaced by a sustainable demand-driven increase in prices backed by wage gains before BoJ can consider exiting its current short-term negative interest rate policy, an outlier among developed nations.

Another encouraging sign of a potential uptick in demand-driven domestic spending is the recent uptick in consumer sentiment in Japan where it rose to 36.1 in November from 35.7, surpassed consensus expectations of 35.6, and has been on an increasing upward trend since August 2023.

No significant change in BoJ’s monetary policy on 18 December but keep a lookout on 23 January next year

Given the “conservative modus operandi” of BoJ, it is likely that it will not make a significant policy change in the upcoming 18 December monetary policy meeting but keep a lookout on the next meeting on 23 January next year where BoJ will release its latest economic outlook report that highlights latest inflation and growth forecasts.

A rise in inflation forecast for 2024 and 2025 is likely to bring BoJ closer to ending its short-term negative interest rate policy which in turn may kickstart a herding behaviour that favors a potential further strengthening of the JPY.

Looking vulnerable for a medium-term bearish breakdown in USD/JPY

Fig 2: USD/JPY medium-term trend as of 6 Dec 2023 (Source: TradingView, click to enlarge chart)

The current four-week decline seen in the price actions of the USD/JPY since a test on its major resistance level of 151.95 on 13 November 2023 has reached the lower boundary of a medium-term ascending channel in place since 24 March 2023 low, now acting as a near-term support at 146.20.

The medium-term momentum indicator as represented by the daily RSI is still showing a bearish momentum condition (has not reached its oversold region of below 30 & continued to flash out lower lows since its bearish breakdown below the 50 level).

Hence, the ascending channel support at 146.20 may not be impregnable.

Watch the 148.40 key short-term resistance

Fig 3: USD/JPY minor short-term trend as of 6 Dec 2023 (Source: TradingView, click to enlarge chart)

The short-term downtrend phase of the USD/JPY remains intact as price actions continue to oscillate within a minor descending channel in place since the 13 November 2023 high.

The recent retest near the upper boundary of the minor descending channel on last Friday, 1 December has led to a bearish reaction in price actions that has been accompanied by a short-term bearish momentum reading seen in the hourly RSI momentum indicator (capped by a parallel descending resistance after it hit overbought reading on last Thursday, 30 November).

Watch the 148.40 short-term pivotal resistance and a break below 145.90 may trigger a medium-term downtrend phase towards the next intermediate support at 144.95/80 in the first step.

On the other hand, a clearance above 148.40 negates the short-term bearish tone to see the medium-term resistance coming in at 149.70 (also the downward sloping 20 and 50-day moving averages).

Gold Price Retreats From Highs and Crude Oil Price Dives

Gold price is correcting gains below the $2,050 support. Crude oil prices declined steadily below the $75.90 support and moved into a bearish zone.

Important Takeaways for Gold and Oil Prices Analysis Today

- Gold price rallied to new highs above $2,120 before it corrected lower against the US Dollar.

- A key bearish trend line is forming with resistance near $2,025 on the hourly chart of gold at FXOpen.

- Crude oil prices extended downsides below the $75 support zone.

- A major bearish trend line is forming with resistance near $73.35 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price rallied heavily above the $2,000 resistance. The price even traded to a new high at $2,135 before there was a downside correction.

There was a move below the $2,072 support level. The bears even pushed the price below the $2,050 support and the 50-hour simple moving average. It tested the $2,010 zone. A low is formed near $2,009.78 and the price is now attempting a fresh increase.

It is now facing resistance near a key bearish trend line at $2,025. The next major resistance is near the 23.6% Fib retracement level of the downward move from the $2,135 swing high to the $2,009 low at $2,040.

The main resistance could be $2,050, above which the price could test the $2,072 resistance. The next major resistance is $2,135. An upside break above the $2,135 resistance could send Gold price toward $2,220. Any more gains may perhaps set the pace for an increase toward the $2,350 level.

Initial support on the downside is near the $2,010 level. The first major support is near the $2,000 level. If there is a downside break below the $2,000 support, the price might decline further. In the stated case, the price might drop toward the $1,965 support.

Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price struggled to continue higher above $80.00 against the US Dollar. The price formed a short-term top and started a fresh decline below $78.00.

There was a steady decline below the $75.90 pivot level. The bears even pushed the price below $73.90 and the 50-hour simple moving average. Finally, the price tested the $72.15 zone. A low was formed near $72.14, and the price is now consolidating losses.

Immediate support is near the $72.15 level. The next major support on the WTI crude oil chart is near $71.50. If there is a downside break, the price might decline toward $70.00. Any more losses may perhaps open the doors for a move toward the $68.00 support zone.

On the upside, immediate resistance is near a major bearish trend line at $73.35. The next resistance is near the 23.6% Fib retracement level of the downward move from the $79.60 swing high to the $72.14 low at $73.90.

A clear move above the trend line resistance and $73.90 could send the price toward $75.90. It coincides with the 50% Fib retracement level of the downward move from the $79.60 swing high to the $72.14 low.

The next key resistance is near $79.60. If the price climbs further higher, it could face resistance near $80.00. Any more gains might send the price toward the $82.00 level.

Start trading commodities with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Bonds Rally, Equities Watch

The central bank doves are forcefully back following a significantly lower-than-expected US JOLTS print, and on the back of a surprisingly dovish comment from an otherwise… hawkish Isabel Schnabel from the European Central Bank (ECB).

Jolts

Released yesterday, the JOLTS data showed that the US job openings fell below 8.8 mio jobs in October – when strikes in Detroit’s three big carmakers may partly explain why the job openings saw such a meaningful decline. But whatever it is, the US offered a lot less jobs in October than it did the previous month, and that has come to cement the idea that the US jobs market is further loosening. Again, the October numbers should be taken with a pinch of salt as they were certainly impacted by the strikes, and November numbers could also be influenced by the distortions of October – meaning that we could see some robust numbers after a depressed month of October. Yet overall, the US jobs market had started giving signs of cooling before the strikes, and this week’s numbers may not be representative of the underlying trend. However, the US jobs figures gain a crucial importance as the Federal Reserve (Fed) approaches a policy pivot.

Due today, the ADP is expected to print 130K private job additions in the US last month, and the Atlanta Fed’s GDP forecast is expected to hint at a sharp decline in Q4 growth to 1.2% from above 5% printed last quarter. If that’s the case, the Fed doves will remain in charge of the market, but the everything rally will likely turn into a… bond rally as we are now at a juncture where the bond optimism might only persist with increased recession probabilities, which doesn't bode well for equity appetite.

The EUR/USD slips into bearish consolidation zone

ECB’s Isabel Schnabel, who has been one of the most hawkish voices during the bank’s latest monetary policy tightening campaign, started to sound dovish this week. Schnabel said that inflation is slowing at a ‘remarkable’ pace. The 10-year bund yield melted to 2.23% level – last seen back in June.

Yes, but Schnabel also said that officials ‘have been surprised many times in both directions’. But traders are now set to sell the euro on dovish ECB expectations until inflation proves the contrary. The EURUSD slipped below 1.08 and to the 100-DMA, where it found some support. Following yesterday’s selloff below the major 38.2% Fibonacci retracement, the pair is now in the bearish consolidation zone, with a strengthening bearish momentum that hints that the selloff could continue to 1.07/1.0730. Note that the market could absorb a further selloff at the current levels as the RSI is now at a mid-range: we are far from oversold conditions.

Gold sees support near the $2000 per ounce as falling US yields and fading appetite for equities continue to push capital into the precious metal.

Crude oil remains sold in a lower-highs-lower-lows pattern that paves the way for a further fall to the $70pb target, and China is not happy because Moody’s cut its outlook for the Chinese sovereign bonds to negative warning that the country’s usage of fiscal stimulus to support local governments and its spiraling property downturn pose risks to its economy. The Chinese CSI 300 fell to the lowest levels in almost 5 years, and nothing helps to undo the damage that government crackdowns and the COVID-zero policy have inflicted on investor confidence. China’s stimulus measures brought Moody’s to cut its sovereign debt outlook but couldn’t bring investors or homebuyers back to the market.

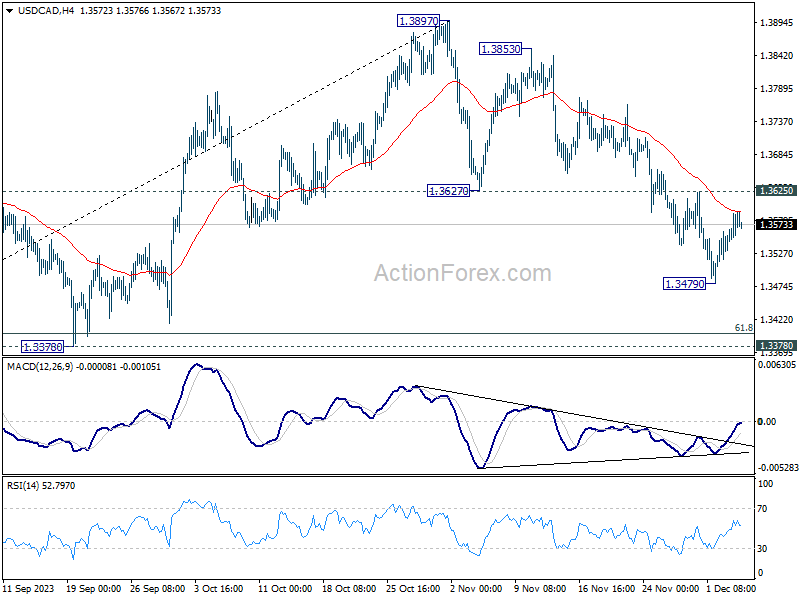

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3551; (P) 1.3574; (R1) 1.3615; More...

No change in USD/CAD's outlook and intraday bias stays neutral at this point. Below 1.3479 will resume the corrective fall from 1.3897. But downside should be contained by 1.3378 support, which is close to 61.8% retracement of 1.3091 to 1.3897 at 1.3399, to bring rebound. On the upside, break of 1.3625 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rise.

In the bigger picture, rise from 1.3091 is seen as the fifth leg of the whole rise from 1.2005 (2021 low). Further rally is expected as long as 1.3378 support holds, to 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. However, decisive break of 1.3378 will dampen this view and bring deeper fall back to 1.3091 instead.

Market Sentiment Stabilizes, Attention on BoC Decision and US ADP Job

Global market sentiment shows signs of stabilization in Asia today, marked by gains in major indices like Nikkei Hong Kong's HSI. This shift indicates that the markets have largely absorbed the impact of Moody's downgrade of China's rating outlook, redirecting attention towards economic data and central bank policies. The spotlight is now on BoC's interest rate decision and the release of US ADP private employment report.

In the currency markets, Australian Dollar is showing resilience, trading higher despite the release of GDP data that fell short of expectations. Canadian Dollar, meanwhile, is having a slight uptick as traders await BoC's decision, speculating on whether the central bank will adopt a dovish stance given current economic conditions. However, the New Zealand Dollar is emerging as the strongest performer, outpacing its Australian and Canadian counterparts. Concurrently, Dollar, Euro, and Yen are showing signs of softening, while Sterling and Swiss Franc are mixed.

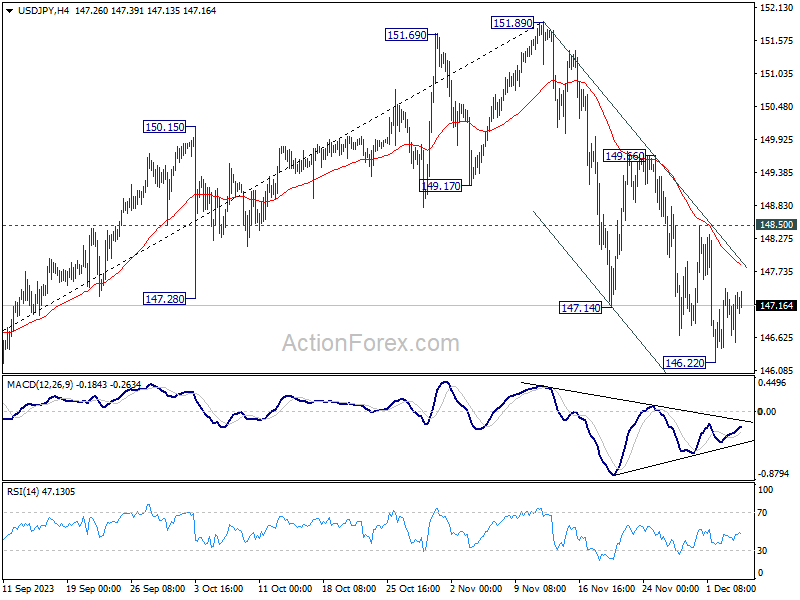

Technically, USD/JPY is staying in consolidation above 146.22 for now. Despite the steep decline in the US 10-year yield overnight, the pair has yet to react, but this could change with a delayed response. In any case, outlook will stay bearish as long as 148.50 resistance holds. Break of 146.22 temporary low will resume the fall from 151.89 to 145.06 key support level next.

In Asia, at the time of writing, Nikkei is up 1.92%. Hong Kong HSI is up 1.15%. China Shanghai SSE is up 0.12%. Singapore Strait Times is down -0.04%. Japan 10-year JGB yield is down -0.0322 at 0.640. Overnight, DOW fell -0.22%. S&P 500 fell -0.06%. NASDAQ rose 0.31%. 10-year yield fell -0.117 to 4.171.

Australia's Q3 GDP growth slows to 0.2% qoq, per capita output declines

Australia's GDP for Q3 showed a modest increase of 0.2% qoq, falling short of the expected 0.5% qoq growth. On a year-on-year basis, GDP grew by 2.1%. However, a contrasting picture emerges when considering GDP on a per capita basis, which revealed a decline of -0.5% qoq and a -0.3% yoy.

Katherine Keenan, ABS head of national accounts, said: "This was the eighth straight rise in quarterly GDP, but growth has slowed over 2023." She pointed out that government spending and capital investment were the primary contributors to GDP growth in this quarter.

Specifically, government final consumption expenditure rose by 1.1%. Additionally, gross fixed capital formation also saw a 1.1% rise.

An interesting aspect of the September quarter's GDP was the contribution of 0.4% points from changes in inventories. Notably, mining inventories increased by AUD 2.4B, a reflection of the larger fall in exports compared to production volumes.

On the other hand, trade in services had a negative impact on growth. Imports of services surged by 8.4%, significantly outpacing the 1.9% growth in services exports.

BoJ's Himino stresses patience in monetary easing to prevent return to "frozen state"

BoJ Deputy Governor Ryozo Himino, in a speech today, affirmed the central bank's commitment to continued monetary easing. He noted, "the Bank will patiently continue with monetary easing until sustainable and stable achievement of the price stability target, accompanied by wage increases, comes in sight."

He acknowledged the positive changes in firms' wage- and price-setting behavior, noting "solid progress" and "signs in the right direction." However, he warned of the risks of reverting to a deflationary state if a virtuous cycle between wages and prices is not established.

Explaining further, Himino commented on the longstanding norm in Japan where neither wages nor prices could rise significantly. "Japan had worked for many years to break free from this," he added, "and simply returning to such a frozen state after the current high inflation comes down would not be a desirable outcome either."

Himino highlighted the longstanding norm in Japan where "neither wages nor prices could rise". He stressed that Japan's efforts to break free from this stagnation, adding, "simply returning to such a frozen state after the current high inflation comes down would not be a desirable outcome".

He also outlined the multiple challenges facing Japanese monetary policy, including addressing current inflation, supporting moderate economic recovery, encouraging wage increases, and preventing a return to deflation. "The Bank is struggling to find a solution and this is by no means an easy task," he admitted.

BoC set to stand pat, will dovish shift follow?

BoC is widely expected to hold overnight rate target steady at 5.00% today, amidst a backdrop of increasing economic challenges. Current market climate suggests the potential for a slightly dovish shift in the central bank's statement. However, while there is speculation among some investors about the possibility of BoC commencing rate cuts as early as the second quarter of next year, it seems premature for the central bank to signal any definite intentions in this regard at the current juncture.

Governor Tiff Macklem's recent comments have significantly influenced market expectations. He noted that "the excess demand in the economy that made it too easy to raise prices is now gone" and the economy is "approaching balance". His observation that softening economic activity will exert "more downward pressure on inflation" and the acknowledgment that "interest rates may now be restrictive enough" have nearly eliminated the odds of further rate hikes.

In a recent Reuters poll, a majority of economists, specifically 18 out of 26, projected that BoC's rate would decrease to 4.0% or lower by the end of 2024. Nevertheless, Macklem is expected to reiterate that discussions about rate cuts are still premature, indicating a cautious approach from the central bank in the face of uncertain economic conditions.

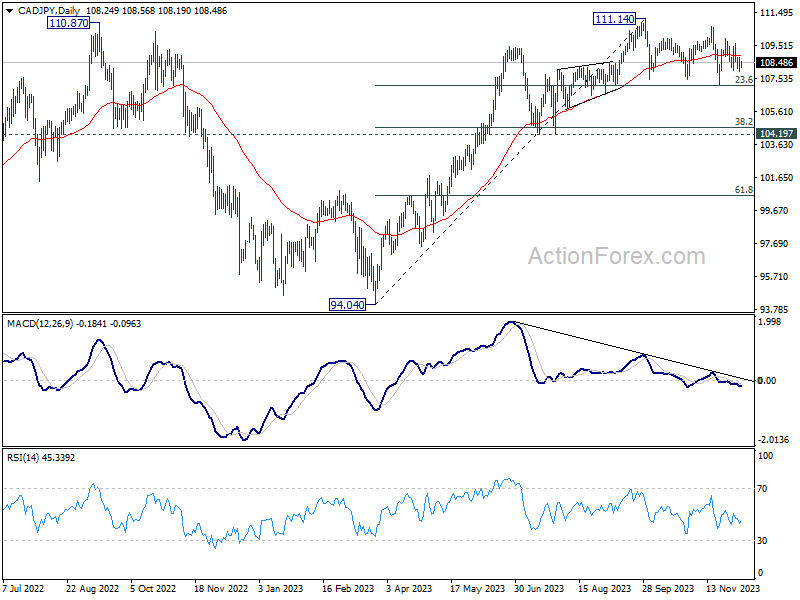

CAD/JPY has been bounded in range trading below 111.14 since September. The pull back is so far rather shallow as contained by 23.6% retracement of 94.04 to 111.14 at 107.10. There is not sign of trend reversal, and another rise through 111.14 is still in favor. However, considering bearish divergence condition in D MACD, upside potential could be relatively limited.

On the other hand, firm break of 107.10 could indicate that deeper decline is underway to 38.2% retracement of 104.60, or even further to 61.8% retracement at 100.57. However, such a significant decline would likely require concurrent dovish policy shifts from BoC and hawkish turn from BoJ, potentially materializing early in the next year.

Elsewhere

Germany factor orders, UK PMI construction, and Eurozone retail sales will be released in European session. Later in the day, US will release ADP employment and trade balance. In addition to BoC rate decision, Canada will release labor productivity, trade balance, and Ivey PMI.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3551; (P) 1.3574; (R1) 1.3615; More...

No change in USD/CAD's outlook and intraday bias stays neutral at this point. Below 1.3479 will resume the corrective fall from 1.3897. But downside should be contained by 1.3378 support, which is close to 61.8% retracement of 1.3091 to 1.3897 at 1.3399, to bring rebound. On the upside, break of 1.3625 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rise.

In the bigger picture, rise from 1.3091 is seen as the fifth leg of the whole rise from 1.2005 (2021 low). Further rally is expected as long as 1.3378 support holds, to 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. However, decisive break of 1.3378 will dampen this view and bring deeper fall back to 1.3091 instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | 0.20% | 0.40% | 0.40% | |

| 07:00 | EUR | Germany Factory Orders M/M Oct | 0.50% | 0.20% | ||

| 09:30 | GBP | Construction PMI Nov | 47.1 | 45.6 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | 0.20% | -0.30% | ||

| 13:15 | USD | ADP Employment Change Nov | 120K | 113K | ||

| 13:30 | CAD | Labor Productivity Q/Q Q3 | 0.20% | -0.60% | ||

| 13:30 | CAD | Trade Balance (CAD) Oct | 1.8B | 2.0B | ||

| 13:30 | USD | Trade Balance (USD) Oct | -63.0B | -61.5B | ||

| 13:30 | USD | Nonfarm Productivity Q3 | 4.70% | 4.70% | ||

| 13:30 | USD | Unit Labor Costs Q3 | -0.80% | -0.80% | ||

| 15:00 | CAD | BoC Rate Decision | 5.00% | 5.00% | ||

| 15:00 | CAD | Ivey PMI Nov | 54.2 | 53.4 | ||

| 15:30 | USD | Crude Oil Inventories | -1.3M | 1.6M |

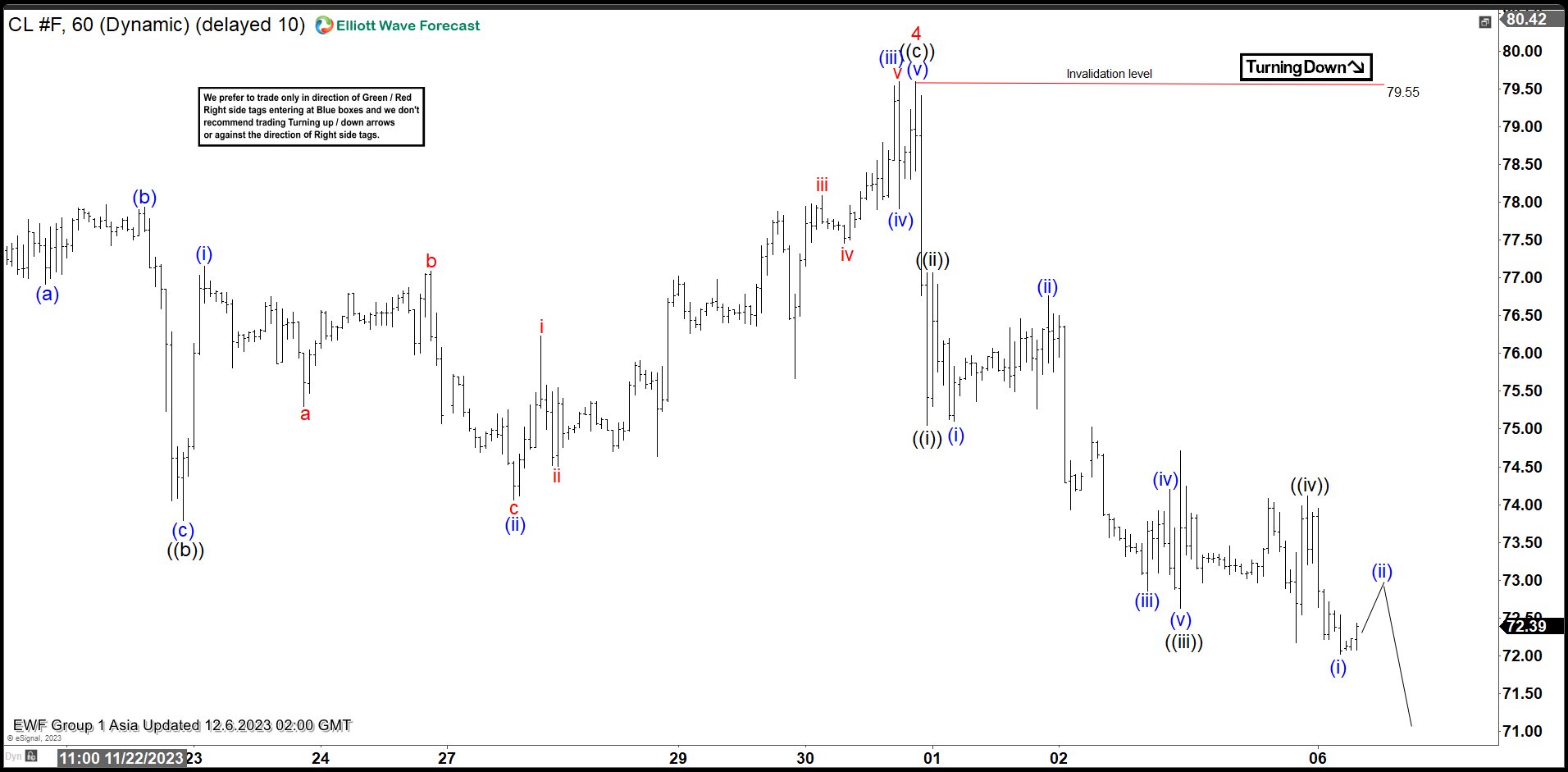

Oil (CL) Should See at Least 3 Waves Rally Soon

Cycle from 9.28.2023 high in Oil (CL) is in progress as a 5 waves impulse Elliott Wave structure. Down from 9.28.2023 high, wave 1 ended at 81.50 and rally in wave 2 ended at 90.78. Oil then extended lower in wave 3 towards 72.16. Wave 4 at 79.55 as the 1 hour chart below shows. Up from wave 3, wave ((a)) ended at 78.22, and dips in wave ((b)) ended at 73.79. Wave ((c)) higher ended at 79.55 which completed wave 4. Up from wave ((b)), wave (i) ended at 77.15 and wave (ii) ended at 74.06. Wave (iii) ended at 79.6, wave (iv) ended at 77.91, and wave (v) ended at 79.55 which completed wave ((c)) of 4.

Oil has turned lower in wave 5. Internal subdivision of wave 5 is unfolding as a 5 waves impulse structure. Down from wave 4, wave ((i)) ended at 75.05 and wave ((ii)) rally ended at 77.07. Oil then turns lower in wave ((iii)). Down from wave ((ii)), wave (i) ended at 75.1 and rally in wave (ii) ended at 76.76. Oil extends lower in wave (iii) towards 72.86, wave (iv) ended at 74.20, and final leg wave (v) ended at 72.63 which completed wave ((iii)). Wave ((iv)) correction ended at 74.12. Expect Oil to extend lower in wave ((v)) of 5. Near term, as far as pivot at 79.55 stays intact, Oil has scope to extend a bit lower to end the 5 waves move before larger 3 waves rally takes place.

Oil Futures (CL_F) 60 Minutes Elliott Wave Chart

CL Elliott Wave Video

https://www.youtube.com/watch?v=a9pLmgHuF0w