Sample Category Title

BoC stands pat as economic slowdown eases inflationary pressures

BoC keeps overnight rate target unchanged at 5.00%, aligning with market expectations. In its policy statement, the central bank emphasized its ongoing concern about inflationary risks, stating it "remains prepared to raise the policy rate further if needed."

Nevertheless, BoC also noted recent data suggesting that the Canadian economy is "no longer in excess demand". This shift is seen as contributing to a reduction in inflationary pressures across a broad range of goods and services prices. This observation suggests a subtle yet significant change in the economic environment, potentially signaling a pivot in the central bank's future policy decisions.

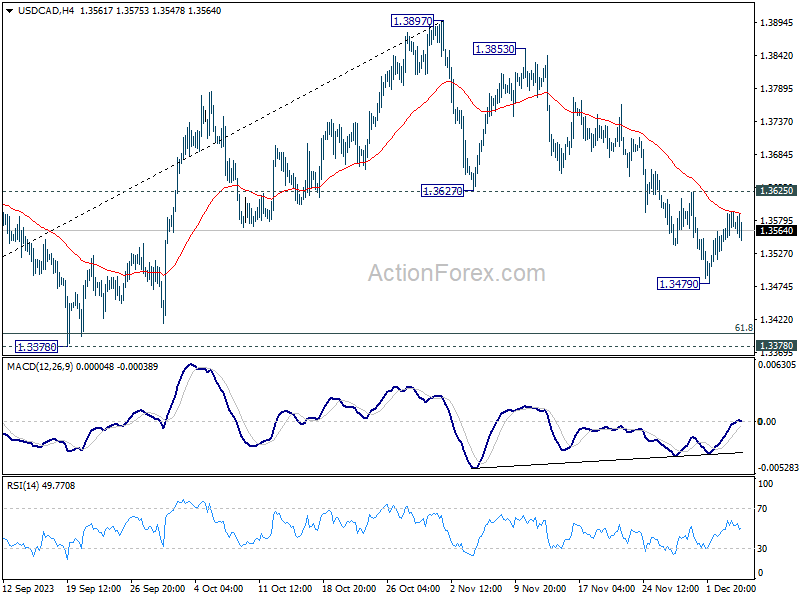

USD/CAD is steady after the policy announcement. The focus for the rest of the week will be on whether rebound from 1.3479 could extend through 1.3625 resistance decisively to confirm that whole correction from 1.3897 has completed.

(BOC) Bank of Canada maintains policy rate, continues quantitative tightening

The Bank of Canada today held its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is continuing its policy of quantitative tightening.

The global economy continues to slow and inflation has eased further. In the United States, growth has been stronger than expected, led by robust consumer spending, but is likely to weaken in the months ahead as past policy rate increases work their way through the economy. Growth in the euro area has weakened and, combined with lower energy prices, this has reduced inflationary pressures. Oil prices are about $10-per-barrel lower than was assumed in the October Monetary Policy Report (MPR). Financial conditions have also eased, with long-term interest rates unwinding some of the sharp increases seen earlier in the autumn. The US dollar has weakened against most currencies, including Canada's.

In Canada, economic growth stalled through the middle quarters of 2023. Real GDP contracted at a rate of 1.1% in the third quarter, following growth of 1.4% in the second quarter. Higher interest rates are clearly restraining spending: consumption growth in the last two quarters was close to zero, and business investment has been volatile but essentially flat over the past year. Exports and inventory adjustment subtracted from GDP growth in the third quarter, while government spending and new home construction provided a boost. The labour market continues to ease: job creation has been slower than labour force growth, job vacancies have declined further, and the unemployment rate has risen modestly. Even so, wages are still rising by 4-5%. Overall, these data and indicators for the fourth quarter suggest the economy is no longer in excess demand.

The slowdown in the economy is reducing inflationary pressures in a broadening range of goods and services prices. Combined with the drop in gasoline prices, this contributed to the easing of CPI inflation to 3.1% in October. However, shelter price inflation has picked up, reflecting faster growth in rent and other housing costs along with the continued contribution from elevated mortgage interest costs. In recent months, the Bank's preferred measures of core inflation have been around 3½-4%, with the October data coming in towards the lower end of this range.

With further signs that monetary policy is moderating spending and relieving price pressures, Governing Council decided to hold the policy rate at 5% and to continue to normalize the Bank's balance sheet. Governing Council is still concerned about risks to the outlook for inflation and remains prepared to raise the policy rate further if needed. Governing Council wants to see further and sustained easing in core inflation, and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is January 24, 2023. The Bank will publish its next full outlook for the economy and inflation, including risks to the projection, in the MPR at the same time.

Sunset Market Commentary

Markets

Today’s US ADP job report served as the next test for markets eager to frontrun a sharp Fed pivot. November employment grew by 103k, less than the 130k expected and a further deceleration from an already downwardly revised 106k. The biggest contributors were trade, transportation and utilities (+55k) & education and health services (+44k). But a negative print in the leisure sector (-7k) points to weakness in the services sector along with goods sector (construction -4k, manufacturing -15k), ADP said. The numbers came on the back of (admittedly outdated) Q3 unit labor costs that have been adjust to the downside as well (-1.2%). Bond markets’ first reaction was tepid and almost suggested the correction lower in yields was nearing its end. But with the joining of American investors, things shifted in higher gear again. US yields at the front end returned back to the intraday opening lows. Longer maturities at some point turned 3 bps lower with intraday moves amounting to 7 bps. Technical charts came to the rescue for the likes of the 10-y yield. Support at 4.13% (50% retracement on the 2023 rally) in the meantime narrowed losses to around 2 bps. Either way, these are not the strong moves down we’ve seen in recent weeks but note that the ADP job report doesn’t rank too high on the market influence list. Friday’s payrolls on the other hand are another story and are the litmus test for bond markets this week. German yields trailed their US peers, easing between 1.7-3.1 bps across the curve with the belly outperforming. UK gilts did best today, with yields shedding 3.1-8.1 bps. The Bank of England successfully kept markets betting on premature rate cuts on a leash but the global force is strong. The timing of a first, fully priced in rate cut moved from August to June in the last two days.

The fall-out on sterling from the latter remains limited though. EUR/GBP erased earlier losses to trade virtually unchanged around 0.857 but this is just as much technically inspired (rejected test of support at 0.8557) as it is genuine sterling weakness. EUR/USD is going nowhere with the pair unable to retake 1.08. Poland’s zloty awaits guidance from the National Bank of Poland after it kept policy rates steady (as expected) at 5.75%. Stock markets in Europe add another 0.7%. The EuroStoxx50 is nearing the YtD (intraday) high at 4491.51. Wall Street opens with gains between 0.25 and 0.4%.

News & Views

Italian foreign Minister Antonio Tajani today said that the country formally informed China that the country will end its participation in China’s Belt and Road initiative. Tajani said that the initiative hasn’t produced the desired effects and was no longer a priority for the country. Italy was the only G7 country that had subscribed to the Chinese initiative as it joined the pact in 2019. The 5-year term of the pact was due to expire in March 2022 and Italy had to decide on a prolongation before the end of the year. Italy participating in the project was a politically sensitive topic as the US and other Western countries took more balanced approach on their relationship with China amongst others due to issues on human rights, China’s positioning vis-à-vis Russia with respect to the war in Ukraine and as Western economies reevaluate their dependence on China supply in key economic sectors.

October retail and production data published by the Hungarian Statistical office today indicated that activity in the country remains sluggish. The volume of retail trade in October was 6.5% lower than in the same period last year. Sales volumes declined by 1.9% in food shops, 5.1% in non-food retailing and by 21.1% in automotive fuel sales. Sales also declined 0.3% compared to the September. Volume of industrial production in October also dropped 0.6% M/M and 3.2% Y/Y. Production dropped in the majority of manufacturing subsections, including computer, electronic and optical products as well as that of food products, beverages and tobacco products. However, as a glimmer of hope, the Statistical office mentioned that the two subsectors with the biggest weight, manufacturing of transport equipment and electrical equipment, posted an increase in production. After brining the emergency overnight rate again in line with the conventional base rate, the National Bank of Hungary (MNB) started cutting rates at a pace of 75 bps (currently 11.50%). MNB members indicated that they want to proceed at that pace at the Dec 19 meeting. Hungarian November CPI data will be published on Friday. The forint today hovered near EUR/HUF 380.

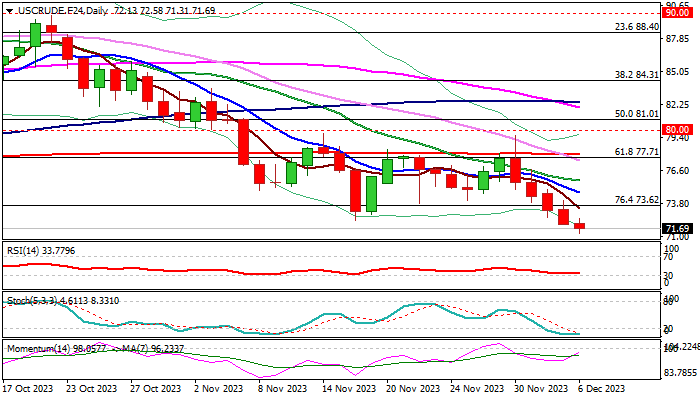

WTI Oil: Bears Hold Grip on Demand Concerns, OPEC+ Decisions

WTI oil price fell below $72 on Wednesday and trading at the lowest levels in five months.

Bear-leg from $79.57 (Nov 30 peak) extends into fifth straight day, as decision of OPEC+ to extend production cuts and further reduce output from January did not satisfy market expectations, with growing concerns over fuel demand on clouded outlook for China’s economic health, additionally souring the sentiment.

Daily technical studies are weak as 14-d momentum stays in the negative territory and moving averages are in bearish configuration (multiple death-crosses contributing to negative near-term outlook.

Tuesday’s close below former low at $72.36 (Nov 16) generated fresh signal of bearish continuation, after larger bears were paused for $72.36/$79.57 consolidation, opening way for attack at $70.31 (200WMA) and psychological $70 support.

Meanwhile, bears may take a breather on oversold conditions, with upticks to provide selling opportunities while the price stays below falling 10DMA ($74.77).

Res: 72.36; 74.10; 74.77; 75.76.

Sup: 71.31; 71.00; 70.31; 70.00.

Canada’s Trade Accounts Register a $3.0 Billion Surplus in October

Canada's merchandise trade account recorded a trade surplus of $3 billion in October, the third consecutive month in black ink. This comes after September's surplus was revised slightly upward to $1.1 billion.

Exports advanced slightly by 0.1% month-on-month (m/m) in October, though 6 of 11 sectors posted decreases in export values. The large increase in aircraft and other transportation equipment (+15% m/m) did just enough to offset export declines in energy products (-1.2% m/m), industrial chemical, plastic, and rubber products (-3.5% m/m), and industrial machinery and equipment (-2.4% m/m).

Meanwhile, total imports slipped by 2.8% m/m in October, with 8 of 11 sectors declining on the month. Imports of motor vehicles and parts (-5.8% m/m) posted its first decline in seven months, while the highly volatile imports of unwrought gold, silver and platinum contributed most to the decline (-41.2% m/m). Energy products (-8.0% m/m) and farm, fishing and food products (-4.1% m/m) also meaningfully declined.

In volume terms, overall imports decreased by 3.2% m/m in October while exports edged down slightly by 0.1% m/m.

Canada's trade surplus with the United States widened for a fourth consecutive month to $12.1 billion in October.

Key Implications

October trade data provides a first look for how net trade will feed into GDP growth in the fourth quarter. Recall that growth revisions over the past two quarters hit net trade more than any other GDP component, with net exports acting as one of the largest drags to Q3 growth. With export volumes tracking higher than imports in October, trade may shape up to be a small tailwind for Q4 growth.

The trade effects induced by shocks over the past quarter appear to have been reversed over the past few months, potentially leading to cleaner readings going forward. That said, the details in the trade data suggest some slowing momentum in international demand with key trading partners. This will be an important factor to watch over the coming months.

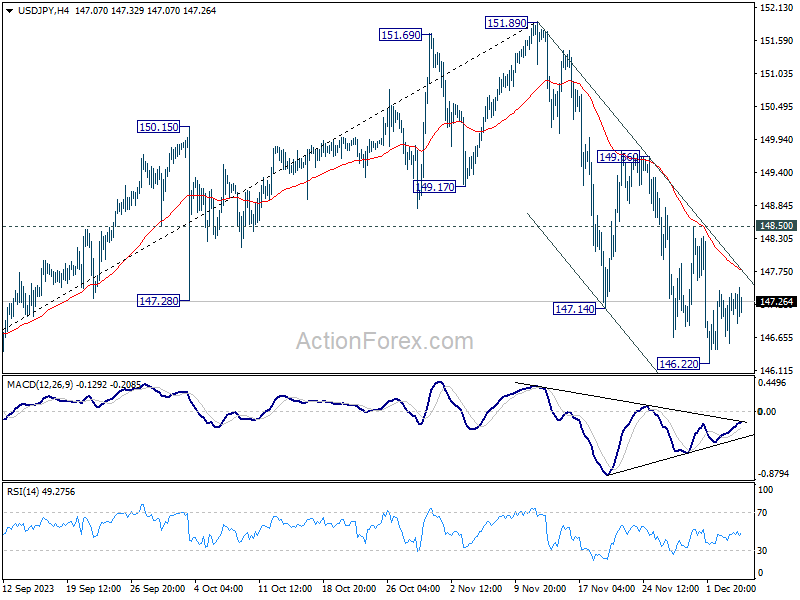

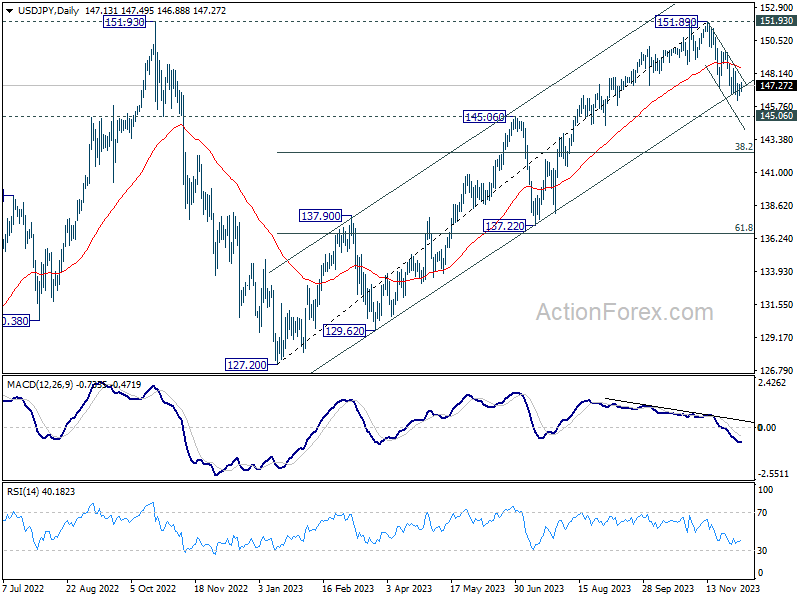

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.68; (P) 147.03; (R1) 147.51; More...

Intraday bias in USD/JPY remains neutral as consolidation from 146.22 is extending. Further decline is expected as long as 148.50 resistance holds, even in case of stronger recovery. On the downside, firm break of 146.22 will resume the fall from 151.89 to 145.06 key support level.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

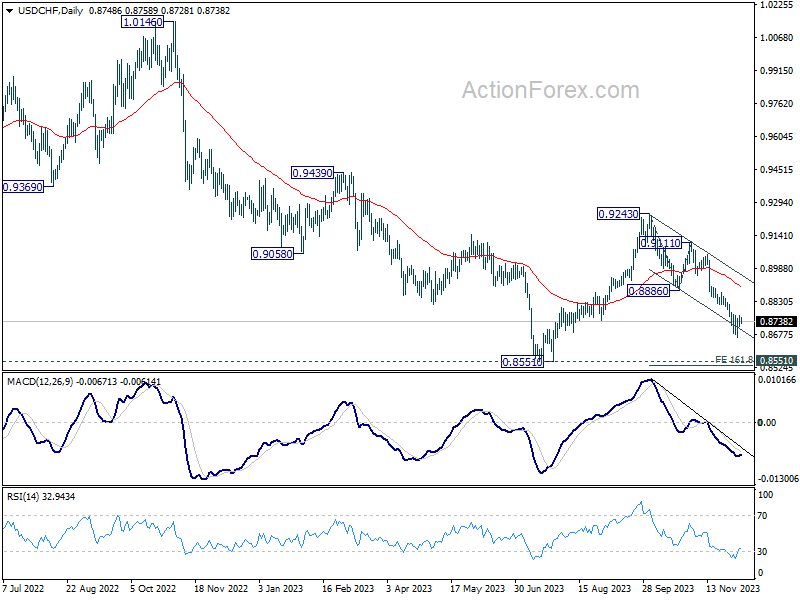

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8743; (R1) 0.8773; More....

Intraday bias in USD/CHF stays neutral at this point. Another fall is in favor as long as 0.8769 minor resistance holds. Below 0.8665 will resume the decline from 0.9243 to 161.8% projection of 0.9243 to 0.8886 from 0.9111 at 0.8533, which is close to 0.8551 low. However, break of 0.8769 minor resistance should indicate short term bottoming, and turn bias back to the upside for stronger recovery to 0.8886 support turned resistance.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. For now, this will remain the favored case as long as 0.8886 support turned resistance holds.

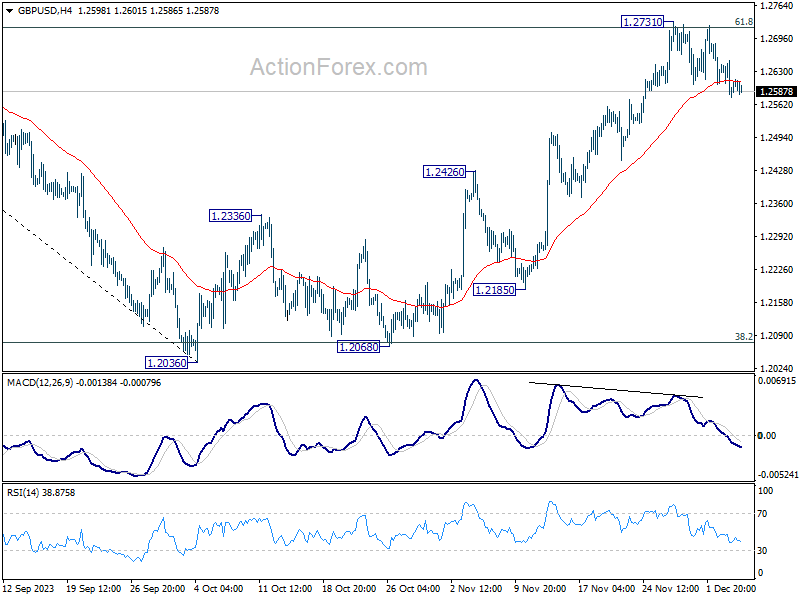

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2565; (P) 1.2608; (R1) 1.2640; More...

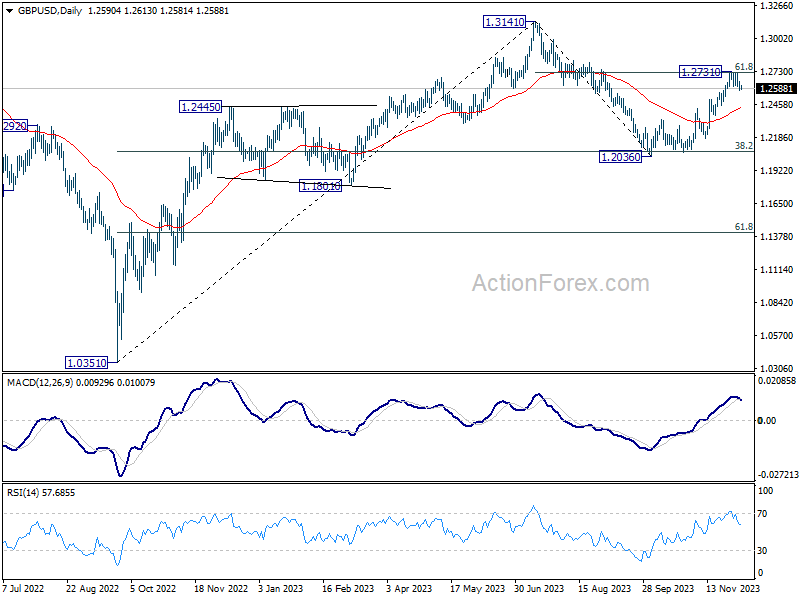

Intraday bias in GBP/USD remains on the downside at this point. Fall from 1.2731 short term top should extend to 55 D EMA (now at 1.2427). For now, risk will stay on the downside as long as 1.2731 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

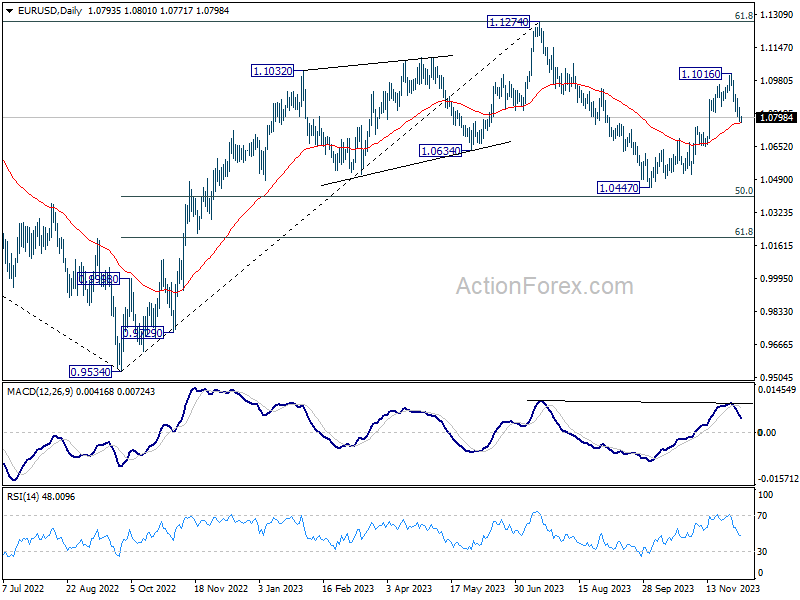

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0768; (P) 1.0808; (R1) 1.0838; More...

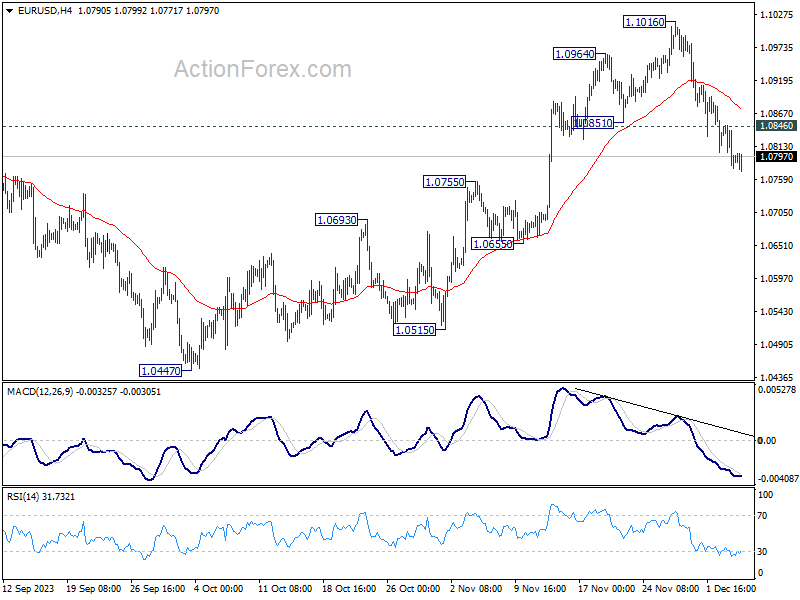

EUR/USD's fall from 1.1016 is still in progress and intraday bias stays on the downside. Sustained break of 55 D EMA (now at 1.0770) will pave the way to retest 1.0447 support. On the upside, above 1.0846 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1016 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

Falling Yields Drive Euro and Sterling Down

Euro and Sterling are falling broadly in European session today, a trend largely driven by notable decrease in benchmark yields in Germany and the UK. German 10-year bund yield has reached its lowest point since June. Simultaneously, UK 10-year gilt yield has dipped below 4% mark for the first time since May

These movements in bond markets reflect increasing expectations among investors for upcoming rate cuts by ECB and BoE. Current market pricings suggest the likelihood of four rate cuts from ECB and three from the BoE in 2024. This aggressive pricing-in of rate cuts underscores growing concerns about the economic outlook in Europe and while disinflation is making significant progress.

In the broader currency markets, commodity currencies are displaying robustness, particularly led by New Zealand Dollar, with Australian Dollar also showing strength but not to the same extent. Canadian Dollar's performance is keenly watched as traders and investors await the upcoming rate decision from BoC. There is a focus on whether the BoC will introduce dovish elements in its policy statement, which could significantly influence the Loonie's next move.

Meanwhile, Swiss Franc is showing mixed performance, gaining strength against its European peers while maintaining a balanced position overall. Dollar turns softer after weaker than expected ADP Job data, while Yen is digesting this week's gains.

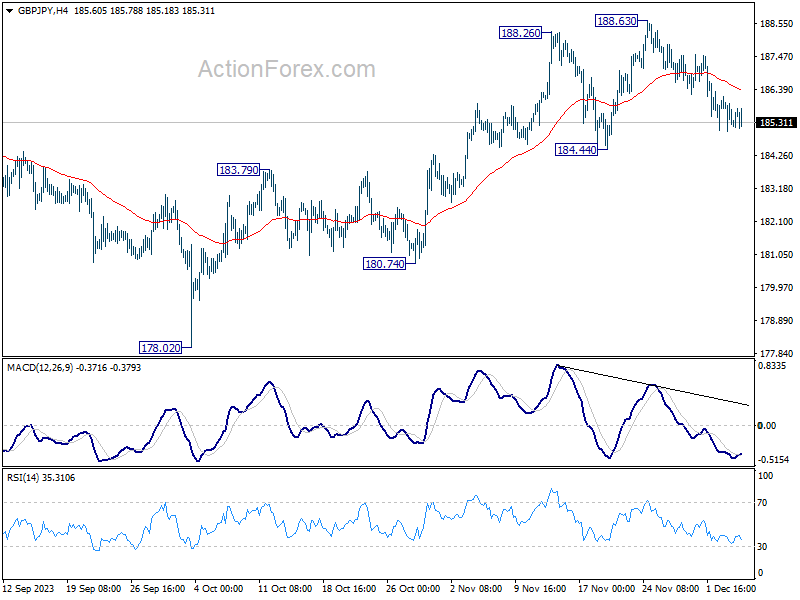

Technically, GBP/JPY is so far still resilient, holding above 184.44 support despite extending the pull back from 188.63. However, firm break of 184.44 will align the outlook with EUR/JPY. That is this decline is actually a larger scale correction. That would open up deeper fall to 180.74 support, or even further to 178.02 key structural support level.

In Europe, at the time of writing, FTSE is up 0.51%. DAX is up 0.58%. CAC is up 0.60%. German 10-year yield is down -0.013 at 2.237. UK 10-year yield is down -0.039 at 3.998. Earlier in Asia, Nikkei rose 2.04%. Hong Kong HSI rose 0.83%. China Shanghai SSE fell -0.11%. Singapore Strait Times rose 0.33%. Japan 10-year JGB yield fell -0.0246 to 0.648.

US ADP jobs grows 103k, pay rise slows further

US ADP private sector employment grew 103k in November, below expectation of 120k. By sector, goods-producing jobs fell -14k while service-providing jobs rose 117k. By establishment size, small companies added 6k jobs, medium companies added 68k, large companies added 33k.

Job-stays saw a 5.6% yoy pay increase, down from 5.7% yoy, and the slowest since September 2021. Job-changes saw a 8.3% yoy pay rise, down from 8.4% yoy, slowest since June 2021.

"Restaurants and hotels were the biggest job creators during the post-pandemic recovery," said Nela Richardson, chief economist, ADP. "But that boost is behind us, and the return to trend in leisure and hospitality suggests the economy as a whole will see more moderate hiring and wage growth in 2024."

Eurozone retail sales rises 0.1% mom in Oct, EU up 0.3% mom

Eurozone retail sales volume rose 0.1% mom in October, below expectation of 0.2% mom. Volume of retail trade increased by 0.8% mom for non-food products, while it decreased by -0.8% mom for automotive fuels and by -1.1% mom for food, drinks and tobacco.

EU retail sales rose 0.3% mom. Among Member States for which data are available, the highest monthly increases in the total retail trade volume were registered in Croatia (+3.1%), the Netherlands (+2.4%) and Slovakia (+1.9%). The largest decreases were observed in France (-1.0%), Belgium and Austria (both -0.8%), Spain and Portugal (both -0.4%).

UK PMI construction fell to 45.5, ongoing sectoral downturn

UK PMI Construction ticked down from 45.6 to 45.5 in November, remaining below the neutral 50 mark and underperforming against the expected 47.1. This level indicates continued contraction in the construction sector for the third month, marking it as the second-lowest reading since May 2020.

Tim Moore of S&P Global Market Intelligence highlighted the sector's issues, stating, "A slump in house building has cast a long shadow over the UK construction sector." He pointed out that the downturn in residential construction has persisted for the past 12 months, with recent reductions among the steepest since 2009.

Elevated mortgage costs and adverse market conditions were cited as key reasons for the decline in housing projects. Additionally, rising interest rates and economic uncertainty are adversely affecting commercial construction, while civil engineering activity saw its sharpest drop since July 2022.

Moore also noted a significant decrease in overall input prices for the second consecutive month, marking the fastest rate of decline since July 2009. Despite this decrease in costs, the sector continues to face substantial challenges.

BoE's Bailey: Rates to stay high for an extended period

BoE Governor Andrew Bailey, in a press conference today, stated that "rates are likely to need to remain at these levels for an extended period to bring inflation back to target on a sustained basis," referring to the current bank rate at 5.25%.

He also noted that the full impact of the higher interest rates is yet to be fully realized, and highlighted the central bank's vigilance towards potential financial stability risks that might emerge as a result.

Separately, BoE's half-yearly Financial Stability Report noted, "The overall risk environment remains challenging, reflecting subdued economic activity, further risks to the outlook for global growth and inflation, and increased geopolitical tensions."

The report also drew attention to the strains on household finances due to rising living costs and higher interest rates. It pointed out that some effects of these higher rates, particularly in terms of mortgage repayments, have yet to fully manifest.

Australia's Q3 GDP growth slows to 0.2% qoq, per capita output declines

Australia's GDP for Q3 showed a modest increase of 0.2% qoq, falling short of the expected 0.5% qoq growth. On a year-on-year basis, GDP grew by 2.1%. However, a contrasting picture emerges when considering GDP on a per capita basis, which revealed a decline of -0.5% qoq and a -0.3% yoy.

Katherine Keenan, ABS head of national accounts, said: "This was the eighth straight rise in quarterly GDP, but growth has slowed over 2023." She pointed out that government spending and capital investment were the primary contributors to GDP growth in this quarter.

Specifically, government final consumption expenditure rose by 1.1%. Additionally, gross fixed capital formation also saw a 1.1% rise.

An interesting aspect of the September quarter's GDP was the contribution of 0.4% points from changes in inventories. Notably, mining inventories increased by AUD 2.4B, a reflection of the larger fall in exports compared to production volumes.

On the other hand, trade in services had a negative impact on growth. Imports of services surged by 8.4%, significantly outpacing the 1.9% growth in services exports.

BoJ's Himino stresses patience in monetary easing to prevent return to "frozen state"

BoJ Deputy Governor Ryozo Himino, in a speech today, affirmed the central bank's commitment to continued monetary easing. He noted, "the Bank will patiently continue with monetary easing until sustainable and stable achievement of the price stability target, accompanied by wage increases, comes in sight."

He acknowledged the positive changes in firms' wage- and price-setting behavior, noting "solid progress" and "signs in the right direction." However, he warned of the risks of reverting to a deflationary state if a virtuous cycle between wages and prices is not established.

Explaining further, Himino commented on the longstanding norm in Japan where neither wages nor prices could rise significantly. "Japan had worked for many years to break free from this," he added, "and simply returning to such a frozen state after the current high inflation comes down would not be a desirable outcome either."

Himino highlighted the longstanding norm in Japan where "neither wages nor prices could rise". He stressed that Japan's efforts to break free from this stagnation, adding, "simply returning to such a frozen state after the current high inflation comes down would not be a desirable outcome".

He also outlined the multiple challenges facing Japanese monetary policy, including addressing current inflation, supporting moderate economic recovery, encouraging wage increases, and preventing a return to deflation. "The Bank is struggling to find a solution and this is by no means an easy task," he admitted.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0768; (P) 1.0808; (R1) 1.0838; More...

EUR/USD's fall from 1.1016 is still in progress and intraday bias stays on the downside. Sustained break of 55 D EMA (now at 1.0770) will pave the way to retest 1.0447 support. On the upside, above 1.0846 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1016 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | 0.20% | 0.40% | 0.40% | |

| 07:00 | EUR | Germany Factory Orders M/M Oct | -3.70% | 0.50% | 0.20% | 0.70% |

| 09:30 | GBP | Construction PMI Nov | 45.5 | 47.1 | 45.6 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | 0.10% | 0.20% | -0.30% | -0.10% |

| 13:15 | USD | ADP Employment Change Nov | 103K | 120K | 113K | 106K |

| 13:30 | CAD | Labor Productivity Q/Q Q3 | -0.80% | 0.20% | -0.60% | |

| 13:30 | CAD | Trade Balance (CAD) Oct | 3.0B | 1.8B | 2.0B | |

| 13:30 | USD | Trade Balance (USD) Oct | -64.3B | -63.0B | -61.5B | -61.2B |

| 13:30 | USD | Nonfarm Productivity Q3 | 5.20% | 4.70% | 4.70% | |

| 13:30 | USD | Unit Labor Costs Q3 | -1.20% | -0.80% | -0.80% | |

| 15:00 | CAD | BoC Rate Decision | 5.00% | 5.00% | ||

| 15:00 | CAD | Ivey PMI Nov | 54.2 | 53.4 | ||

| 15:30 | USD | Crude Oil Inventories | -1.3M | 1.6M |