Sample Category Title

USD/JPY: Japanese Yen Surges on Signals that BoJ is About to Exit Ultra-Loose Policy

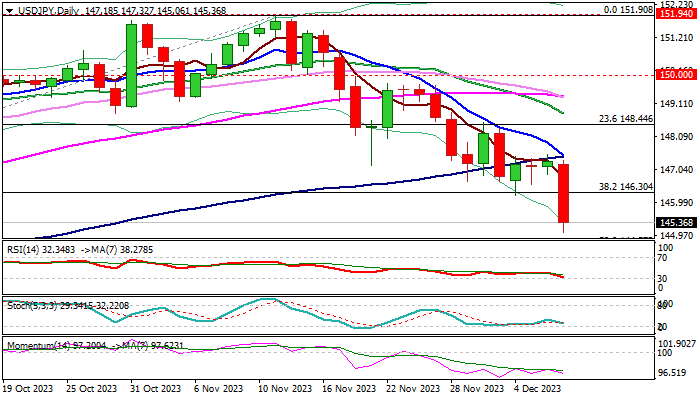

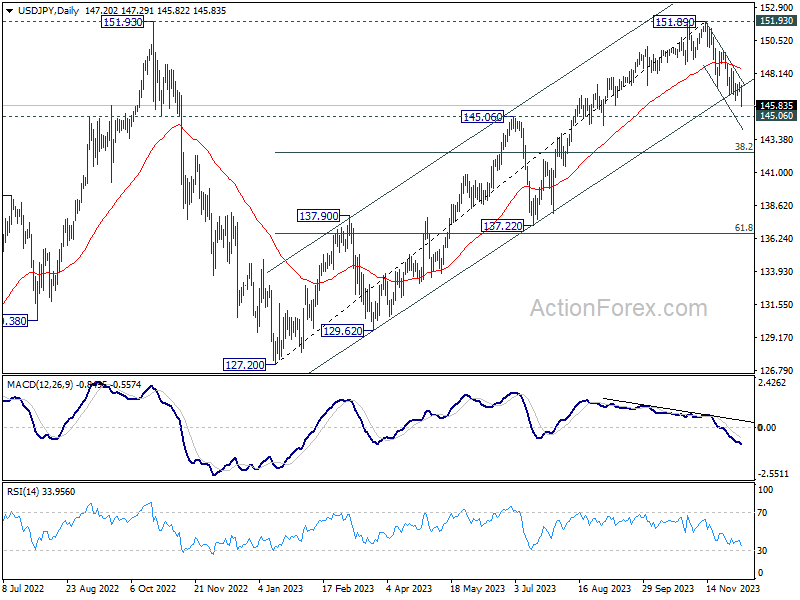

USDJPY accelerated lower (down 1.4% in Asian/early European session) on Thursday, driven by growing market expectations that the Bank of Japan will soon start exiting its long lasting ultra-low monetary policy, which strongly boosts demand for yen.

On the other hand, the US Federal Reserve is likely done with tightening and markets speculate that the US central bank may start cutting rates as early as March 2024.

Fresh weakness broke below pivotal Fibo support at 146.30 (38.2% of 137.23/151.90) which contained attacks earlier this week and kept bears on hold for consolidation.

Technical picture is getting more bearish on daily chart, as MA’s are in bearish configuration and created a number of bear-crosses and 14-d momentum turned south, deeply in the negative territory, validating bearish near-term outlook.

Bears eye next target at 144.57 (50% of 137.23/151.90) and could travel much lower in such environment, with limited corrections expected to provide better selling levels.

Broken Fibo 38.32% (146.30) reverts to resistance which should cap and keep bears intact.

Only return above converged 10/100DMA’s would harm bears and neutralize downside risk.

Res: 146.30; 147.00; 147.45; 148.44.

Sup: 145.00; 144.57; 144.00; 142.84.

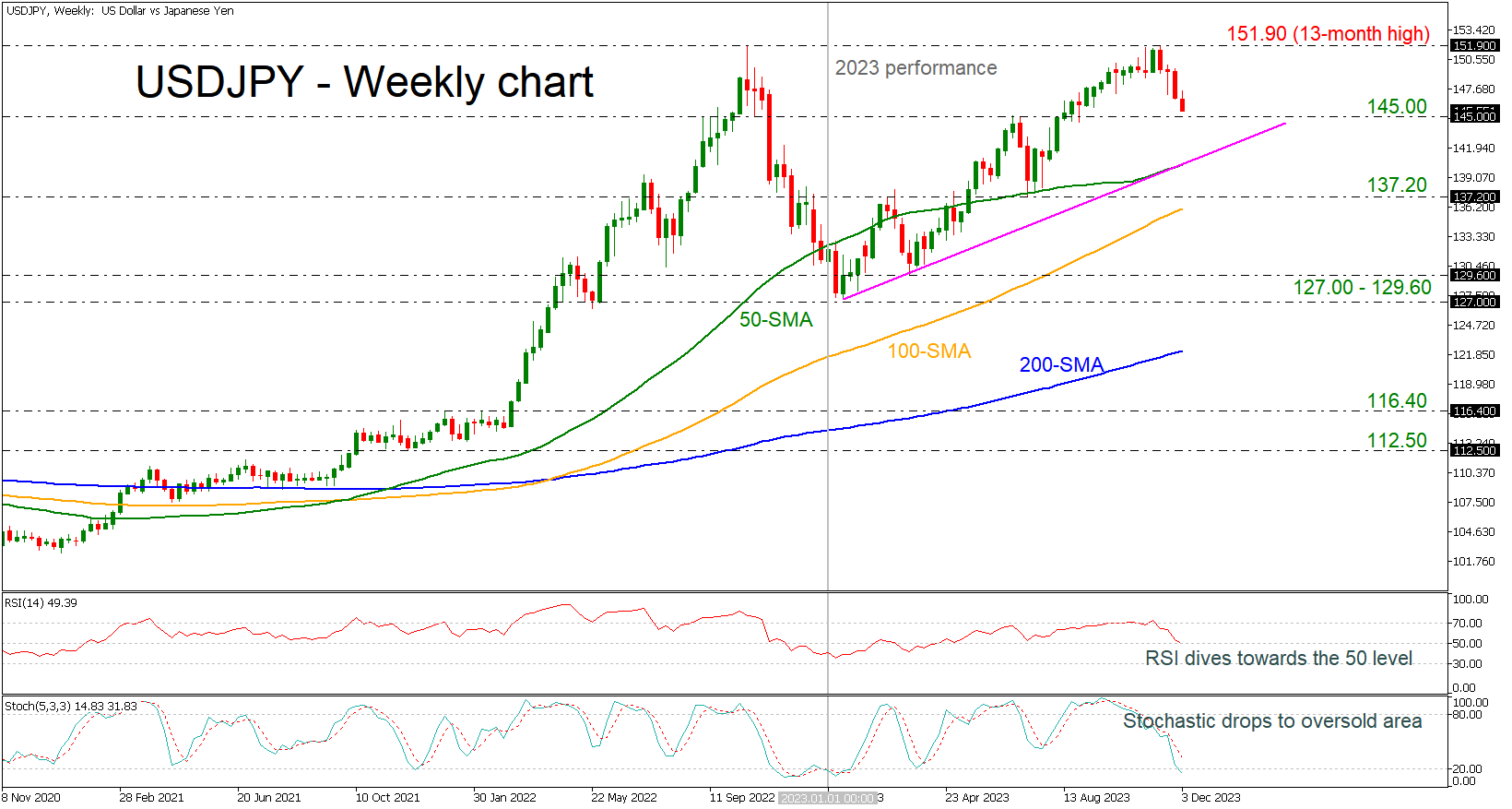

USDJPY’s 2023 Performance is Positive

- USDJPY remains above uptrend line

- Bearish correction may be on the cards

- RSI and stochastic indicate negative move

USDJPY has been in ascending movement since the beginning of 2023, but now is creating the fourth consecutive red week after the pullback off the 13-month high of 151.90.

Technically, the bulls might still be in the town as the market is developing above the long-term uptrend line. However, the technical indicators are suggesting a bearish correction, mirroring the latest downward move in price. The RSI is diving towards the neutral threshold of 50, while the stochastic is moving towards the oversold territory.

In the event the price stays resilient above the 145.00 handle, the bulls might push for a close above the 13-month peak of 151.90. Therefore, a successful move higher could immediately shift the attention to the April 1990 peak at 160.70, only if the market surpasses the next psychological levels such as, 152.00 and 155.00.

On the other hand, if downside pressure continues, selling forces could intensify towards the 145.00 support. Then, additional losses from there could retest the uptrend line, which overlaps with the 50-day simple moving average (SMA) at 140.00. A move south below this hurdle could open the way for a negative structure until 137.20.

In a nutshell, USDJPY may remain supported in the coming sessions, though room for improvement could be limited before the next bearish round takes place above the uptrend line.

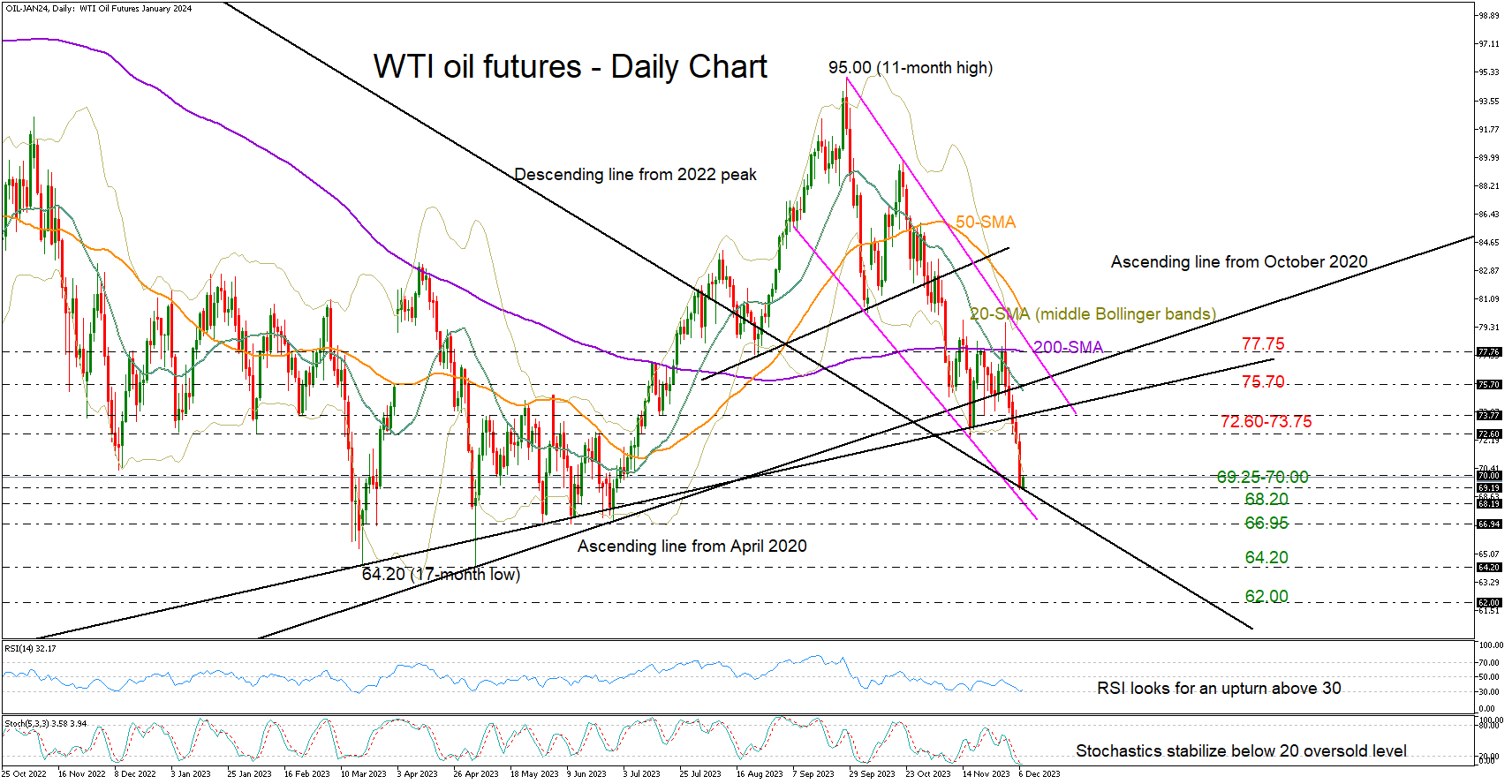

WTI Oil Futures: Is the Sell-off Overdone?

- WTI oil futures test critical 2023 support zone

- Technical signals point to oversold levels

- Sellers await a weekly close below 70

WTI oil futures were sold dramatically on Wednesday, extending their weekly losses to a more than a four-month low of 69.10.

The bears are leading for the seventh consecutive week, increasing speculation that a bullish correction could soon take place as the RSI and the stochastic oscillators are looking for an upside reversal near their oversold levels. Moreover, the market action is developing below the lower Bollinger band, suggesting that the latest downfall might be overdone.

It’s worthy to note that the market is currently testing the critical 200-period simple moving average (SMA) in the weekly chart at 70. The line paused the downtrend from 14-year highs in March and prevented a negative outlook revision in 2023. Hence, sellers might stay patient until a clear close below that threshold is achieved.

Meanwhile, in the daily timeframe, the price is struggling to crawl back above 70. If downside pressures dominate, the slide could halt immediately around the falling line from September at 68.20. The extension of the descending line drawn from the 2022 top could also block the bears around the important March-June 2023 floor of 66.95. Should the bear run continue, all the attention will turn to the 2023 base of 64.20 ahead of the 2021 floor of 62.00.

In the bullish scenario, where the recovery stretches above 70.00, buyers might drive towards the 72.60-73.75 constraining region. The ascending line from the October 2020 low is adding some credence to the area, while slightly higher, the bulls will need to climb above the 20-day SMA and the upward-sloping line from April 2020 at 75.70 to gain direct access to the 200-day SMA at 77.75.

All in all, WTI oil futures are looking oversold near a major support area after an aggressive decline. A continuation below 70 could add more fuel to the bearish wave.

Japanese Yen Outperforms This Morning

Markets

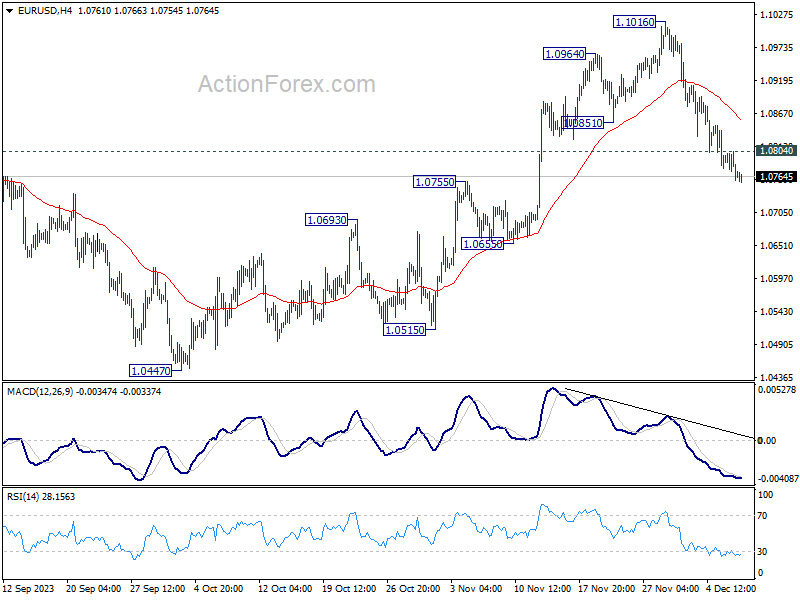

Yesterday’s slightly disappointing US ADP job report reverberated through the long end of the yield curve in particular. Maturities from 10 year to 30 year shed between 6.1 and 8.9 bps. The 10-y tenor dropped below support at 4.13% (50% retracement on the 2023 rise) but held above the next reference that pops up shortly after at 4.09%. Declines in the 5-7y bucket amounted to 3.1 and 5 bps while the front even managed to eke out a marginal 1.6 bps gain. It could mean that current pricing for Fed rate cuts (66% chance for a start in March with a cumulative 125 bps discounted by end 2024) went far enough. We don’t want to draw that conclusion just yet with Friday’s official payrolls report still due. German yields trailed US peers in a similar shift of the curve. Moves varied between +1 bp up front and -7.5 bps at the long end. Gilts outperformed. As bets for a quick and sharp Fed/ECB pivot rise, markets find it increasingly harder to assume the Bank of England to buck the trend. Money markets are currently pricing in a first full rate cut in June compared to August last week with a 60% chance for a move in May. We immediately shift towards Asian dealings this morning to dive into the Japanese bond market. JGB’s hugely underperform, with extensions to US Treasuries, following a triple whammy. Japanese yields rally 6.2 (2-y) to 12.6 (10-y) bps. It started with BoJ deputy governor Himino yesterday portraying the different scenarios in case the era of negative interest rates would be over. He indicated that the first rate hike since 2007 wouldn’t be as harmful as some fear. Governor Ueda in an appearance before parliament this morning flagged several options about which policy rate to target upon ending the sub zero rate experiment. Simply talking about hikes fuels market speculation about actually doing so, turning the December meeting into a live one. The third blow was directly related to bets for a BoJ policy twist with a 30-year bond auction completely flopping. Bid-to-cover dropped to the lowest since 2015 with the tail the biggest on record. The Japanese yen outperforms this morning, pushing USD/JPY to the lowest (146.32) since early September. EUR/JPY extends a losing streak to nine days with the pair currently trading at 157.45. Moves in other currency pairs are muted. EUR/USD is trading stable after a late-session hit yesterday pushed the pair sub 1.08 towards 1.076. Sterling’s momentum eased. EUR/GBP bounced off support at 0.8557 to finish at 0.857. Today’s uninspiring economic calendar paves the way for technical trading going into tomorrow’s payrolls as the final input for the Fed’s policy meeting next week.

News & Views

The National bank of Poland (NBP) yesterday left its policy rate as expected unchanged at 5.75%. Activity remains low, despite increasing again in Q3. The labour market remains strong but employment growth slows. Inflation slowed to 6.5% in November, which the NBP mainly attributes to a decline in core inflation. In underpinning the decision, the NBP stated that ‘the adjustment in the NBP interest rates introduced in previous months, together with uncertainty about a future course of fiscal and regulatory policies and their impact on inflation, the Council decided to keep the NBP interest rates unchanged’. As the political situation (formation of a new government is in the early stages) apparently is an important factor the NBP, the policy rate might stay stable through early 2024. The prospect of a guarded easing cycle and a new EU-friendly government keeps the zloty near the strongest levels since the corona crisis (currently EUR/PLN 4.32). NBP governor Glapinski holds a press conference this afternoon.

The Bank of Canada also kept the policy rate steady at 5.0% yesterday. The BoC indicated that it is still concerned about the risks to the inflation outlook and that it remains prepared to raise to policy rate further if needed. However, in its economic assessment, the BoC acknowledges that higher interest rates are clearly restraining spending while the labour market continues to ease as job creation has been slower than labour force growth. The BoC assumes that this quarter, the economy is no longer in excess demand. Inflation eased to 3.1% Y/Y in October. As is the case for most other central banks of developed countries, including the US, markets ‘are sure’ that the BoC has finished its hiking cycle and even see a >50% chance of the BoC starting its easing cycle in March of next year. The BoC decision had no noticeable impact on the Canadian dollar. USD/CAD followed the broader USD rebound closing near 1.36. In a broader perspective the loonie is holding op rather well considering the decline in the oil price.

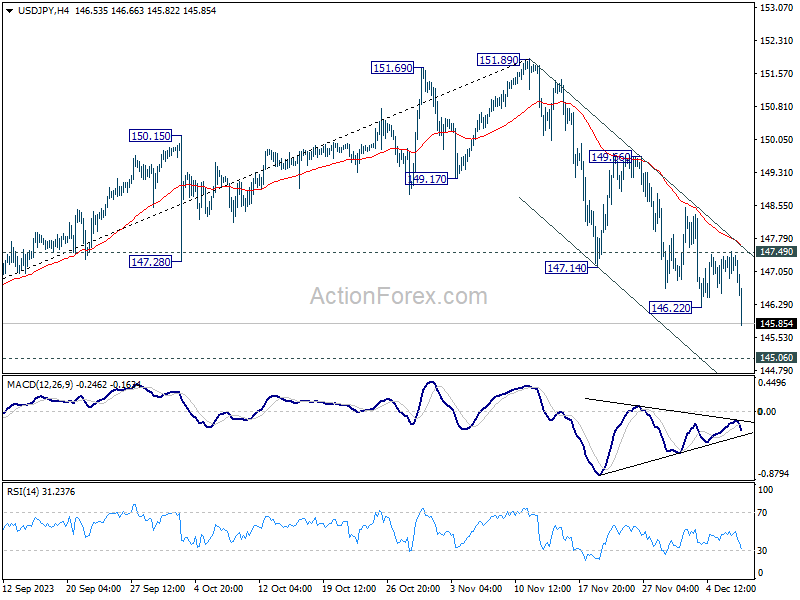

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.97; (P) 147.23; (R1) 147.57; More...

USD/JPY's fall from 151.89 resumed by breaking through 146.22 today. Intraday bias is back on the downside for 145.06 key support. Decisive break there will carry larger bearish implication and target 142.45 fibonacci level next. On the upside, break of 147.49 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0747; (P) 1.0776; (R1) 1.0792; More...

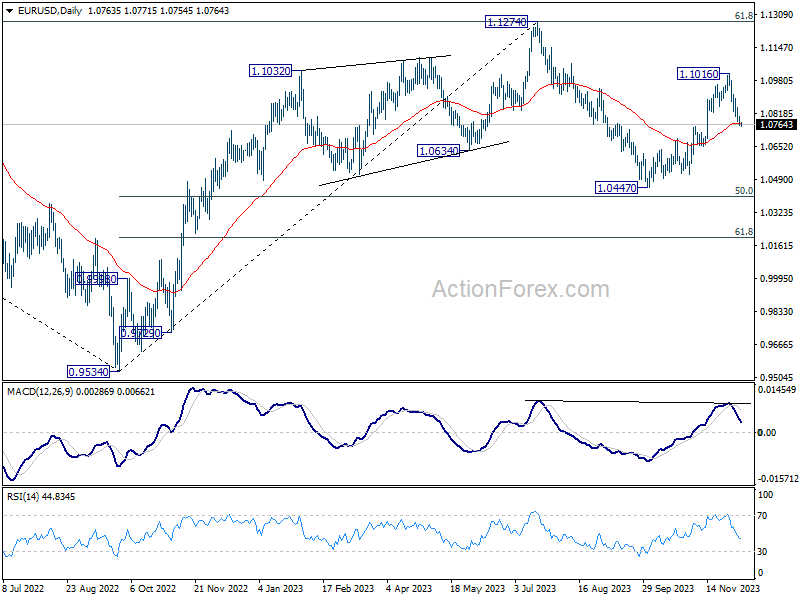

Intraday bias in EUR/USD stays on the downside for the moment, as fall from 1.1016 short term top is in progress. Sustained break of 55 D EMA (now at 1.0770) will pave the way to retest 1.0447 support. On the upside, above 1.0804 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1016 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

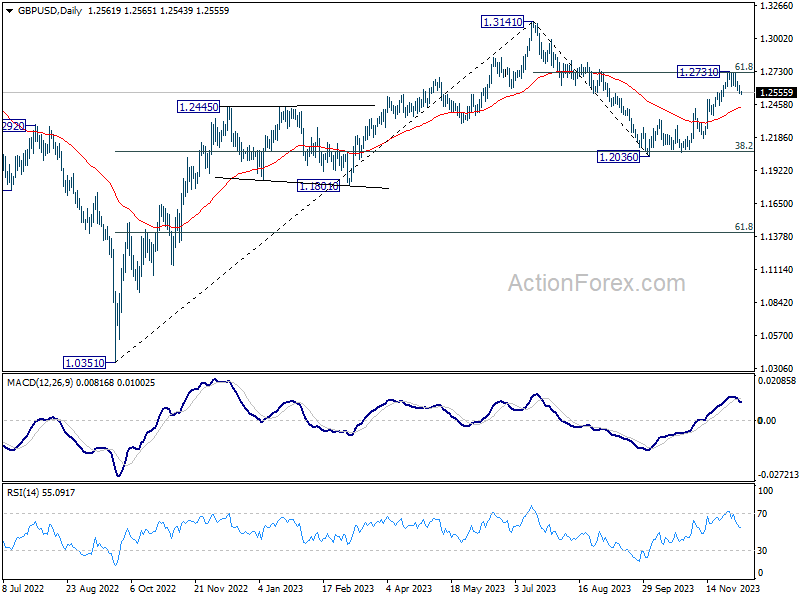

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2536; (P) 1.2575; (R1) 1.2598; More...

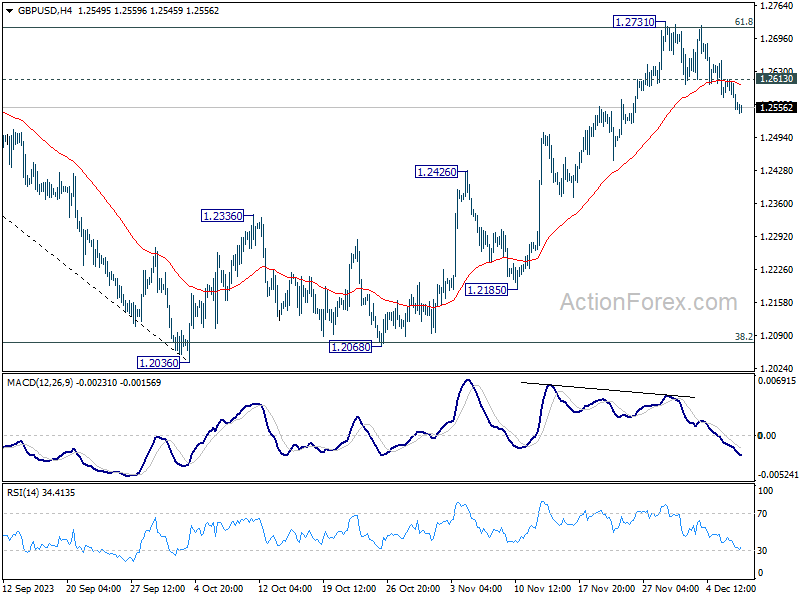

GBP/USD's fall from 1.2731 short term top is in progress. Intraday bias stays on the downside for 55 D EMA (now at 1.2436). On the upside, above 1.2613 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.2731 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

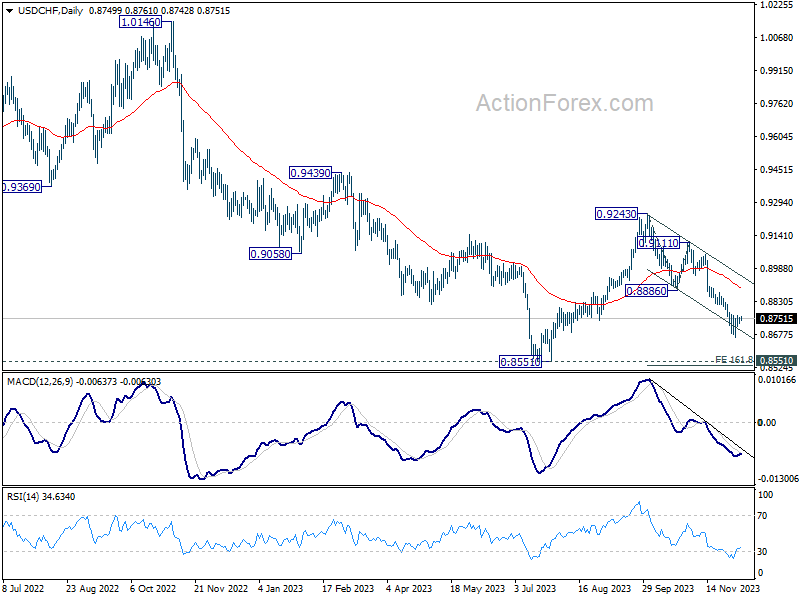

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8731; (P) 0.8746; (R1) 0.8762; More....

Intraday bias in USD/CHF remains neutral as range trading continues. Another fall is in favor as long as 0.8769 minor resistance holds. Below 0.8665 will resume the decline from 0.9243 to 161.8% projection of 0.9243 to 0.8886 from 0.9111 at 0.8533, which is close to 0.8551 low. However, break of 0.8769 minor resistance should indicate short term bottoming, and turn bias back to the upside for stronger recovery to 0.8886 support turned resistance.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. For now, this will remain the favored case as long as 0.8886 support turned resistance holds.

Hang Seng Index Technical: Entrenched in a Downward Spiral

- China’s negative import growth in November suggests a sticky weak domestic demand environment.

- China and Hong Kong stock markets have failed to reignite bullish animal spirits despite the weakening trend seen in the US 10-year Treasury yield in the past month.

- Hang Seng Index now faces a potential major bearish breakdown that may retest the 12,200 October 2008 GFC swing low area in Q1 2024.

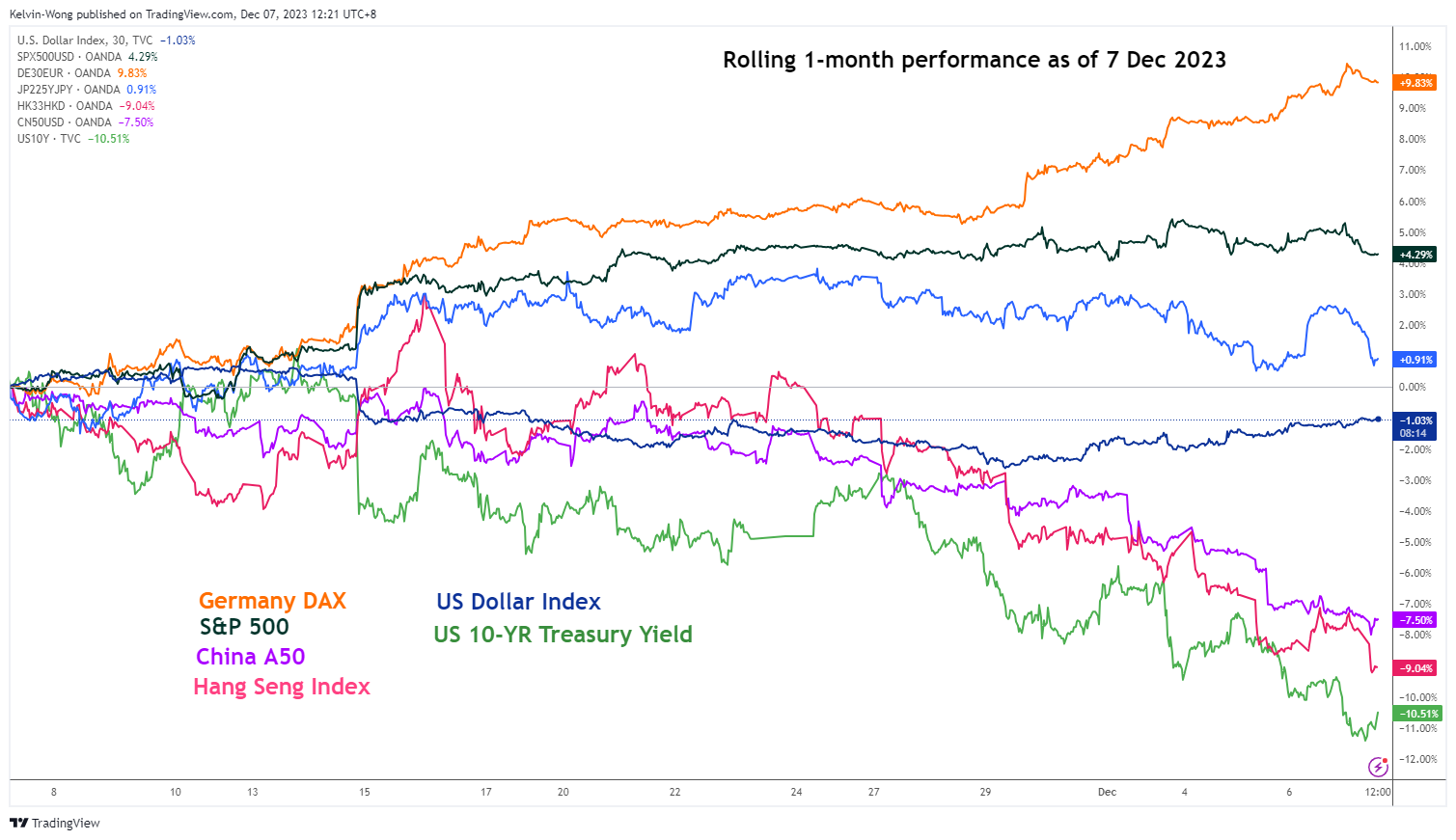

China and Hong Kong stock markets have continued to wobble despite the recent one-month of risk-on-herding behaviour seen in other global stock markets triggered by the medium-term downtrend phases of the US 10-year Treasury yield and US dollar weakness (see Fig 1).

Underperformance of China & Hong Kong benchmark stock indices

Fig 1: Rolling 1-month performances of global benchmark stock indices with US Dollar Index & US 10-year Treasury yield as of 7 Dec 2023 (Source: TradingView, click to enlarge chart)

The month of November 2023 has witnessed stellar monthly performances in the S&P 500 (+8.9%), Germany DAX (+9.5%), Nikkei 225 (+8.5%), and MSCI Emerging Markets ex China (+9.7%). In contrast, bears dominated China A50 (2%), CSI 300 (-2.1%), and Hang Seng Index (-0.4%) over the same period.

The persistent weakness seen in the China and Hong Kong stock markets since China’s COVID re-opening optimism fizzled out in Q1 2023 has been primarily driven by structural vulnerabilities due to rising debt risks in major property developers that may trigger a deflationary spiral in China.

Domestic demand has also remained lacklustre in China despite ongoing revival efforts by policymakers via targeted monetary and fiscal stimulus measures. The latest trade data for November has indicated a surprise contraction in China’s imports which slipped to -0.6% y/y, below consensus estimates of a further improvement in growth to 3.3% y/y from 3% recorded in October.

Hence, it seems that the prior one-month recovery of import growth recorded in October is likely a “blip” and November’s negative y/y growth rate suggests the rolling twelve months of negative growth trend in imports remains intact.

Hang Seng Index faces the risk of a major bearish breakdown

Fig 2: Hang Seng Index long-term secular trend as of 7 Dec 2023 (Source: TradingView, click to enlarge chart)

Through the lens of technical analysis, bearish momentum readings have been flashed out in the long-term monthly chart of the Hang Seng Index.

It is now retesting a long-term secular ascending support in place since the major August 2028 low (Asian Financial Crisis), the last retest and rebound occurred on October 2022 in line with China’s COVID re-opening theme play that coincided with an extremely oversold reading of 21.90 seen in monthly RSI momentum indicator.

In contrast, the current retest on the long-term secular ascending trendline now acting as support at around 16,100 has not been accompanied by bullish reading seen in the monthly RSI indicator; not in the oversold region at this juncture, and bearish momentum remains intact as it traced out a lower high right below a parallel resistance at the 50 level.

Therefore, the Hang Seng Index may see further potential weakness in Q1 2024 with the next major support coming in at 12,200 (October 2008 GFC swing low area & the lower limit of a major sideways range configuration in place since October 2007 major swing high).

Watch the 16,680 key short-term resistance

Fig 3: Hong Kong 33 minor short-term trend as of 7 Dec 2023 (Source: TradingView, click to enlarge chart)

Based on the shorter-term hourly chart, the price actions of the Hong Kong 33 Index (a proxy of the Hang Seng Index futures) are still evolving within a minor downtrend phase in place since the 16 November 2023 high of 18,400.

Key short-term pivotal resistance will be at 16,680 (also the upper boundary of the minor descending channel). A breakdown below 16,100 exposes the next near-term support at 15,800 (lower boundary of the minor descending channel & Fibonacci extension cluster) in the first step.

On the flip side, a clearance above 16,680 negates the bearish tone for a potential minor counter-trend rebound towards 17,100 intermediate resistance (also close to the downward-sloping 20-day moving average).

Scream Correction

US crude plummeted 4% yesterday and sank below the $70pb mark and Brent slipped below $75pb. Momentum traders and falling volumes worsened crude’s recent plunge while OPEC’s latest announcement of output cuts and Saudi’s additional threats that they will extend their solo cut beyond Q1 went totally unheard. Worse, as the bears saw that investors ignored the supply cuts and threats, they feel more confident to increase their bets against crude. And indeed, the cartel’s shrinking share of global output and frictions among members regarding the supply cut strategy mean that either the supply cuts don’t make much difference, or further action will be difficult and perhaps too costly. Add the global slowdown woes into that mix, the dwindling falling interest and algorithmic trades’ lack of emotion regarding the OPEC news, you understand why the barrel of crude is below $70pb and not above $100pb this December, as many banks had forecasted at the start of the year. And if a more than 4.5mio barrel fall in the US oil reserves last week couldn’t halt yesterday’s oil selloff, it is because the most recent number was blurred by a big margin error, the biggest on record – or the bulls just couldn’t find the energy to swim against such a strong tide.

The question on the back of everyone’s mind is: could crude oil extend losses? At the current levels, crude oil is trading near oversold market territory, therefore your algorithmic models based on market metrics should take than into account and slow selling. As such, we shall see a certain rebound at the current levels. Yet any price recovery could remain limited at $75/78 range, including the minor 23.6% Fibonacci retracement and the 200-DMA, and once the time is right, we could see this negative move extent to $65/67 region.

Remains the question of US strategic reserves that the US is said to consider refilling between $67/72 region. Yes, that will certainly help slow the downside pressure at this range but keep in mind that these buybacks are limited to about 3 mio barrels per month due to physical constraints and won’t reverse the tide.

Now that OPEC risk is out of the way, the biggest upside risk for oil is Middle East tensions.

Too dovish

Falling energy prices help softening global inflation expectations and keep the central bank doves in charge of the market, along with sufficiently soft economic data that points at the end of the global monetary policy campaign. This week, the Reserve Bank of Australia (RBA) and the Bank of Canada (BoC) kept rates unchanged – although the RBA said that they could hike again if home-grown inflation doesn’t slow. But overall, the Federal Reserve (Fed) is expected to cut as soon as in May next year, and the European Central Bank (ECB) is expected to announce six 25 basis point cuts next year. If that’s the case, the ECB should start cutting before the Fed, sometime in Q1. It sounds overstretched to me.

Data released earlier this week showed that French industrial production fell unexpectedly for the 3rd straight month in October, Spanish output declined, and German factory orders fell 3.7% in October versus a 0.2% increase penciled in by analysts. The slowing European economies and falling inflation help building a case in favour of an ECB rate cut, but I don’t see the ECB cutting rates anytime in the H1. Remember, economic slowdown is the natural response that the ECB was looking for to slow inflation. Now that it happens, the bank won’t leave the battlefield before making sure that inflation shows no sign of life. But the EURUSD is understandable extending its losses within the bearish consolidation zone, as the German 10-year yield sinks below the 2.20% level. The EURUSD is now testing the 100-DMA to the downside. Trend and momentum indicators are comfortably bearish and the RSI hints that we are not yet dealing with oversold market conditions. Therefore, the selloff could deepen toward the 1.07/1.730 region.

The direction of the EURUSD is of course also dependent on what the USD leg of the pair will do. We see the dollar index recover this week despite the falling yields driven lower by a soft set of US jobs data released so far this week. The JOLTS data showed a significant fall in job openings in October, while yesterday’s ADP print revealed around 100K new private job additions last month, much less than 130K penciled in by analysts. There is no apparent correlation between this data and Friday’s official NFP read, but the fact that independent data point at further loosening in the US jobs market comforts the Fed doves in the idea that, yes, the US jobs market is finally giving in. On the yields front, the US 2-year yield remains steady near 4.60%/4.65% region, while the 10-year yield fell to 4.10% yesterday, from above 5% by end of October. This is a big, big decline, and it means that investors are now ramping up the US slowdown bets. That’s also why we don’t see the US stocks react to the further fall in yields. The S&P500 and Nasdaq both fell yesterday, while their European peers extended gains regardless of the overbought conditions. The Stoxx 600 closed yesterday’s session above the 470 level. The softening ECB expectations are certainly the major driver of the European stocks toward the ytd highs; German stocks hit an ATH yesterday despite the undoubtedly morose economic outlook. Actual levels scream correction.