Sample Category Title

Cliff Notes: Policy’s Effect Being Felt

Key insights from the week that was.

Q3 GDP for Australia surprised to the downside, printing 0.2% (2.1%yr). Relative to expectations, the key disappointment in the quarter was consumer spending, unchanged in Q3 after just a 0.1% gain in Q2. Per capita consumption growth is in the realm of –2.0%yr, second only to the GFC experience. Interest costs and tax payments are putting households under significant pressure, the drag from the latter being the largest ever recorded. Together these detractors wiped out a robust gain in nominal gross income in Q3. Also accounting for inflation, real disposable income has deteriorated materially (–4.3%yr).

Elsewhere in the domestic economy, public demand was a key contributor to growth, rising 1.4% in the quarter. In part this explains some of the weakness in consumption – government subsidies reducing the cost of electricity for households. That public investment meanwhile extended its uptrend (+12%yr) reflects the pursuit of capacity to meet the needs of a growing population. The impetus seen in business investment H1 2023 is, in contrast, fading after the expiration of generous tax incentives. From 2.5% in Q2, quarterly growth in business investment is now just 0.6%.

On trade, Australia’s current account balance fell from a surplus of $7.8bn in Q2 to a slight deficit of –$0.2bn in Q3. That was primarily driven by a moderation in the trade position as the terms of trade continued to slip (–2.6% ), a trend that extended into October for goods. In real terms, the decline in export volumes (–0.7%) in Q3 was met with a lift in imports (+2.1%), leading net exports to subtract a material 0.6ppts from GDP in the three months to September.

As detailed by Chief Economist Luci Ellis, the RBA’s decision to leave policy unchanged earlier in the week was unsurprising given the constructive dataflow ahead of the decision. The Board’s patience – to allow careful assessment of the dataflow – was further justified by the picture the National Accounts painted of the household sector.

Westpac remains of the view that the RBA does not need to tighten any further. The Q4 CPI still holds some risk; but with the consumer clearly pulling back on discretionary spending in response to higher interest rates and a growing tax burden, not only is the Q4 CPI likely to show softer momentum, but the detail is also expected to imply persistence in this downtrend through 2024.

Before moving offshore, a final note on housing. October’s housing finance data showcased a 5.6% bounce in the value of owner-occupier loan approvals, centred on a surge in construction-related lending (+9.1%) and, to a lesser extent, loans for the purchase of existing dwellings (+4.6%). Highlighting the price-led nature of the cycle thus far, the volume of total owner-occupier loans is little-changed from last year (–0.6%) whilst the total value of loans has lifted 12.1% over the same period. Affordability will continue to have a significant bearing on housing market outcomes in 2024.

Offshore, North America was in focus.

The Bank of Canada kept rates steady at 5% in December. The statement noted “the economy is no longer in excess demand”, implying that monetary policy is achieving its aims. Despite this, the Governing Council are still cautious on risks to wages and inflation and so “remains prepared to raise the policy rate further if needed”. Arguably, the BoC are keen to restrain market participants from pricing in rate cuts too soon, thereby easing financial conditions and risking additional momentum in inflation. Having already had to resume rate hikes once, they won’t want a repeat. Elevated wage growth is the primary risk for inflation, but it is receding as job creation and vacancies slow.

South of the border, US data pointed to a gradual easing in activity and the labour market. Factory orders fell 3.6%mth, with weakness in both durable and non-durable goods. Weaker demand sets the stage for a continued cooling of the labour market. The job openings rate declined 0.3ppts in October while hiring and separation rates were broadly stable, in line with pre-pandemic levels. The official US employment report is out tonight; but, ahead of that release, the services ISM this week, and other business surveys previously, pointed to downside risks for employment from November.

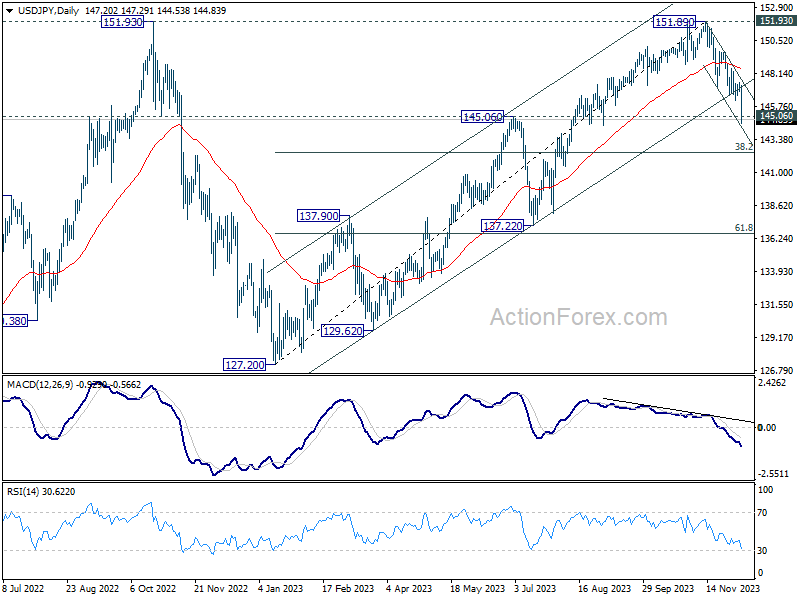

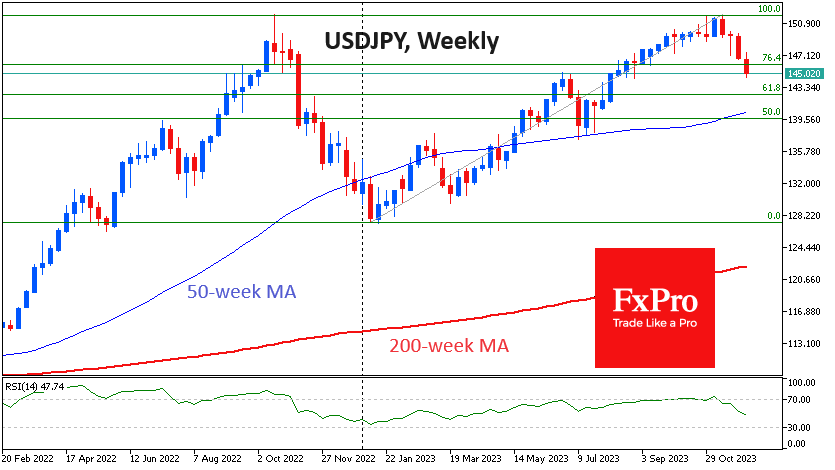

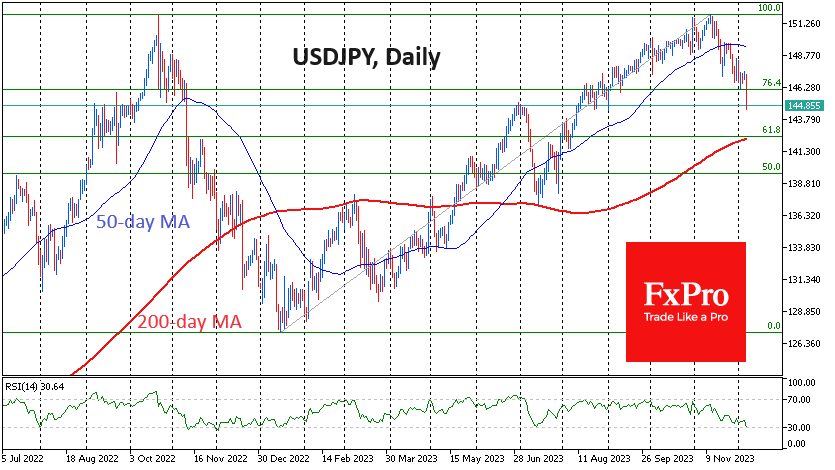

Three Pillars of Yen’s Strength

The Japanese yen was the hero of the day on Thursday, adding over 1.7% against the dollar and 1.6% against the euro since the start of the day. The yen has been sided by Japan’s regional banks, which are rumoured to be lobbying for the abandonment of the yield targeting policy. On Thursday, USDJPY dipped below 145, and EURJPY fell under 156.

Simultaneously, markets are laying that Fed and ECB rates have reached a plateau, and the next step will be to lower them. The logical outcome of this divergence is an accelerated narrowing of yield spreads between Japanese government bonds and other major economies, which brings capital back into the yen.

Yen appreciation has been on a steady course since early November, a couple of weeks after the peak in US 10-year yields, when markets became convinced that their decline had become a trend.

Also, the yen may work the cautious mood of the stock markets in recent days. The yen is very often used as a funding currency to buy risky assets. The shift of market sentiment to profit-taking on major indices triggered a predictable deleveraging on the yen.

Technically, USDJPY formed a double top at 151.9, which was touched in October 2022 and November 2023. The most conservative approach suggests a final reversal signal only after a failure under the local low below 128, which took four months last time but may take two or three quarters.

On lower – daily – timeframes, we can talk about the breaking of the uptrend if the USDJPY falls below 142.4. The 200-day moving average and the level of 61.8% of this year’s growth amplitude intersect here. A consolidation below will indicate the breakdown of the uptrend and open the way to 128. Still, we should be ready for a long tug-of-war and recharging of the JPY bulls on the approach to 143, as the pair will be significantly oversold by RSI even on weekly charts. At the same time, an oversold exit on daily timeframes is likely to be just a reason for local stops in the declines, just as it was in the yen strengthening cycle a year ago.

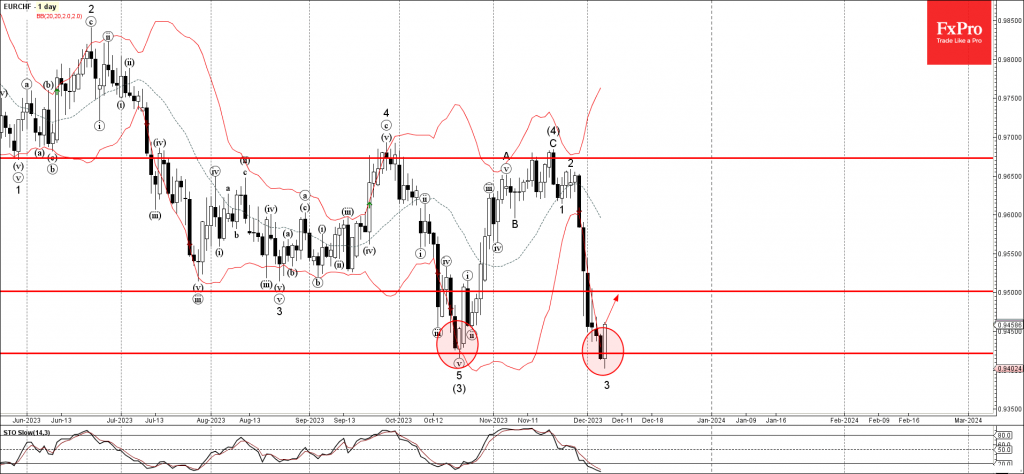

EURCHF Wave Analysis

- EURCHF reversed from support level 0.9420

- Likely to rise to resistance level 0.9500

EURCHF recently reversed from the strong support level 0.9420, which stopped the previous strong downtrend in the middle of October.

The upward reversal from the support level 0.9420 is likely to form today the Bullish Engulfing – strong buy signal for this currency pair.

Given the strength of the support level 0.9420 and the oversold daily Stochastic, EURCHF can be expected to rise further to the next resistance level 0.9500.

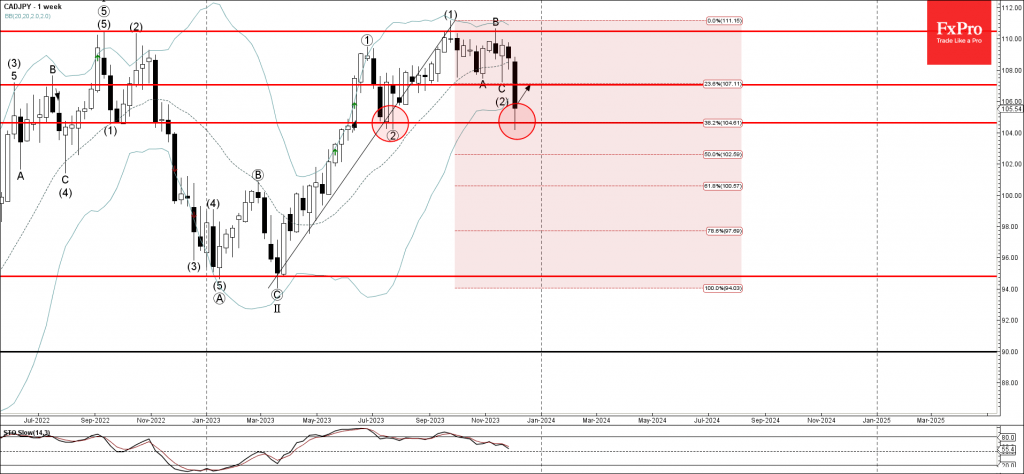

CADJPY Wave Analysis

- CADJPY reversed from support level 104.60

- Likely to rise to resistance level 107.00

CADJPY rising strongly after the price reversed up from the key support level 104.60, which reversed the price twice in July.

The support level 104.60 was strengthened by the 38.2% Fibonacci correction of the upward impulse from March.

Given the strength of the support level 104.60 and the clear daily uptrend, CADJPY can be expected to rise further to the next resistance level 107.00.

Sunset Market Commentary

Markets

A fairly thin eco calendar and blackout-periods for major central bankers made this morning’s Japanese moves the main talking point. Comments by deputy governor Himino and governor Ueda suggest a sense of urgency within the BoJ to normalize policy rates before the window of opportunity closes. November Tokyo inflation figures suggest a faster return to the 2% inflation target while markets on a global level are betting on H1 2024 pivot points in monetary policy. It kind of resembles efforts by the Swedish Riksbank in late 2018-2019 (when Fed rates already peaked at 2.5% coming from the zero border) to get rid of negative interest rates even as the growth momentum window was rapidly closing. In hindsight, the ECB missed out on that opportunity. Japanese officials seem to replace the question “should we end our negative interest rate policy” by “when should we end it and how far can we take it?” The timing of the Himino/Ueda comments is peculiar as well given that the Japanese yen finally got some breathing space over the past month as global core bond yields fell significantly. We always figured that a final swoon in JPY would eventually force the BoJ’s hand at gunpoint. Now all of sudden, it’s the BoJ December policy meeting which might have the biggest market impact instead of the Fed, ECB or BoE. A flopped 30-yr Japanese bond auction this morning proves that investors all of a sudden are on red alert. Japanese bond yields closed 6 bps (2-yr) to 11.9 bps (10-yr) higher. The Japanese yen rallied from 147.31 to currently 145, falling out of this year’s upward trend channel and testing the end of August/early September lows at 144.45/54. EUR/JPY declines from 158.60 to 156.30 with first important support looming around 155.

US weekly jobless claims served as distraction today between US JOLTS & non-manufacturing ISM on Tuesday, ADP employment change yesterday and finally payrolls tomorrow. Claims printed… bang in line with consensus (220k). The sharp uptrend in continuing claims however came to an unexpected and abrupt end, declining from 1925k (highest since end of November 2021) to 1861k (vs 1910k forecast). Markets ignored the release with US Treasuries and UK Gilts following the Japanese drift south (to a lesser extent) and Bunds trading more or less flat. EUR/USD is some technically insignificant ticks higher at 1.0780 as is EUR/GBP at 0.8575. Stock markets marginally lose ground.

The Belgian Debt Agency announced its 2024 borrowing requirements today. The gross requirement is almost €53bn, mainly compelling a net financing need of €21.5bn and redemptions of slightly over €29bn. The OLO funding need is estimated at €41bn, down from €44.82bn this year. News & Views

The Swiss franc briefly touched the strongest level since the Swiss National Bank ditched a currency cap in 2015. EUR/CHF hit an intraday low of 0.94, moving just south of the previous multiyear low seen in September 2022. It then pared losses in a technically inspired rebound back to 0.944. The Swiss franc is profiting from euro area bond yields having declined dramatically over the recent weeks on rising bets for quick ECB rate cuts, potentially as soon as March 2024. A first, full cut by the Swiss National Bank isn’t priced in before June 2024. This discrepancy comes even as Swiss inflation (1.4%) is considerably lower than in the euro area (2.4%). It are the SNB’s strong (hawkish) credentials that prevent markets from running ahead of themselves in ways similar to the Fed and ECB. The central bank’s credible readiness to intervene in FX markets serves as a backstop that markets aren’t willing to test.

World’s biggest job site Indeed said that the UK’s labour market remains tight, despite a fall in job postings over the course of 2023 and broader weakness in the economy. Indeed said that there are still 10% more job postings at the start of December than before the Covid-19 pandemic. While that has shrunk from the 48% at the start of December 2022, it still suggests ongoing resilience with the imbalance of labour demand and supply only gradually easing, the platform’s economist Jack Kennedy said. The labour market is a key variable in the Bank of England’s inflation judgement. Wage growth in particular is considered a critical component to the notoriously more sticky services inflation. Advertised salaries in the UK on the Indeed website were 7% higher in the three months to end October. This compares to 4.2% in the US and 3.8% in the euro area.

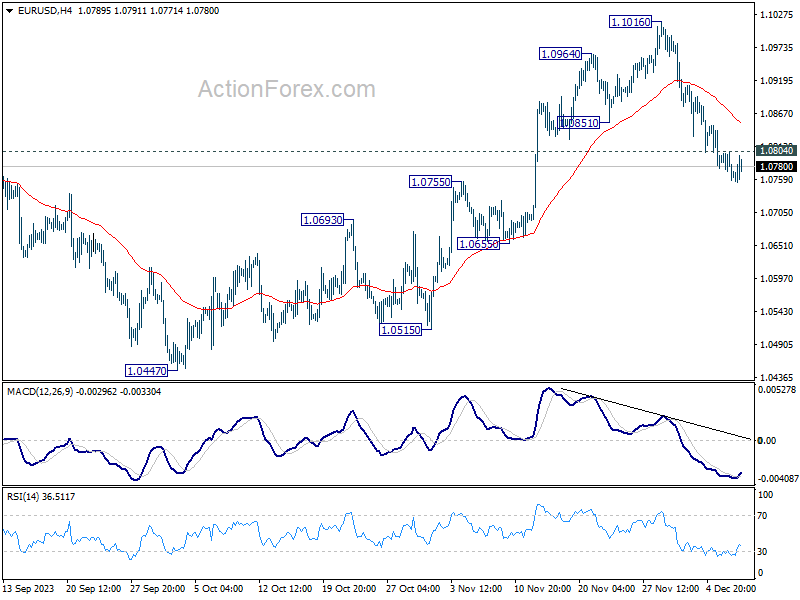

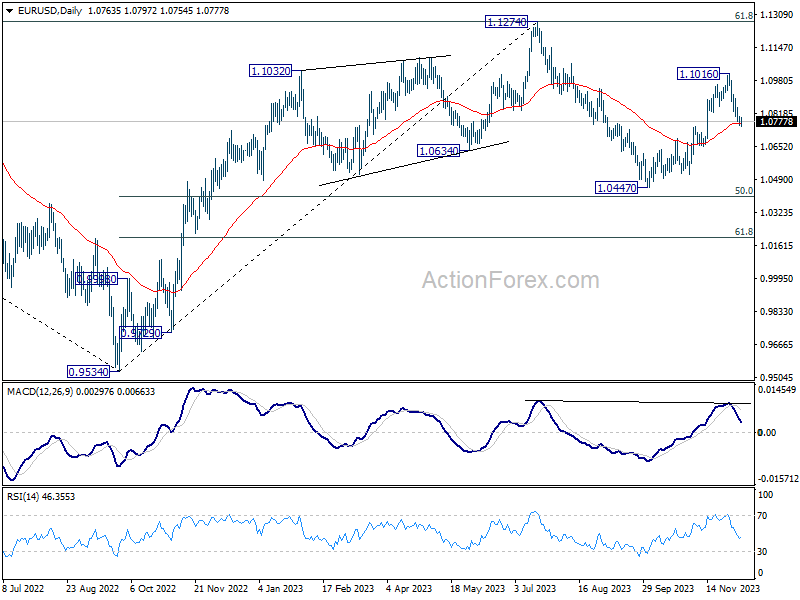

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0747; (P) 1.0776; (R1) 1.0792; More...

Intraday bias in EUR/USD remains mildly on the downside for the moment. Sustained break of 55 D EMA (now at 1.0770) will extend the fall from 1.1016 short term top to retest 1.0447 support. On the upside, above 1.0804 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1016 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

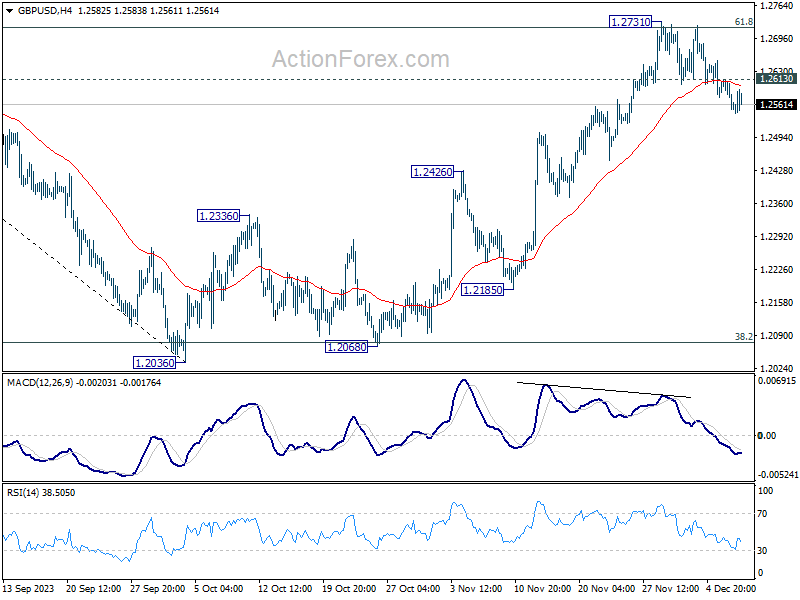

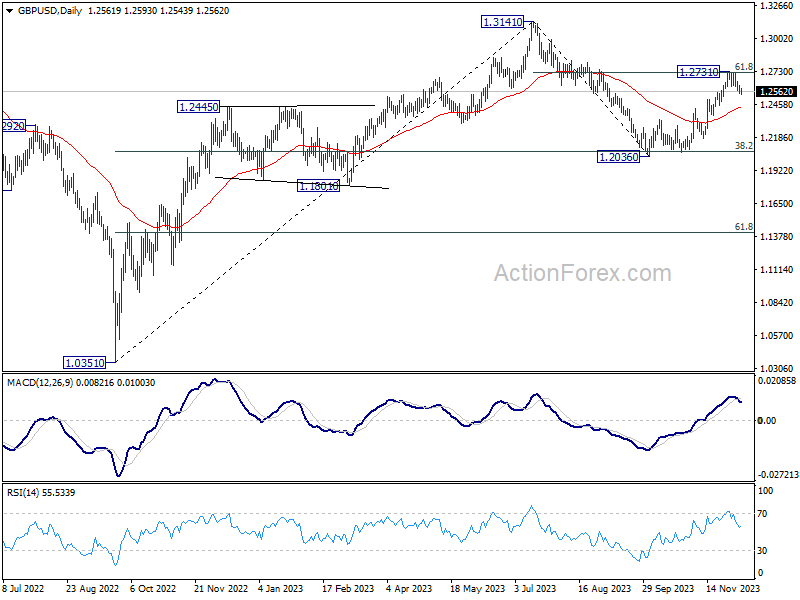

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2536; (P) 1.2575; (R1) 1.2598; More...

Intraday bias in GBP/USD stays on the downside at this point. Fall from 1.2731 short term top would target 55 D EMA (now at 1.2436). On the upside, above 1.2613 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.2731 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

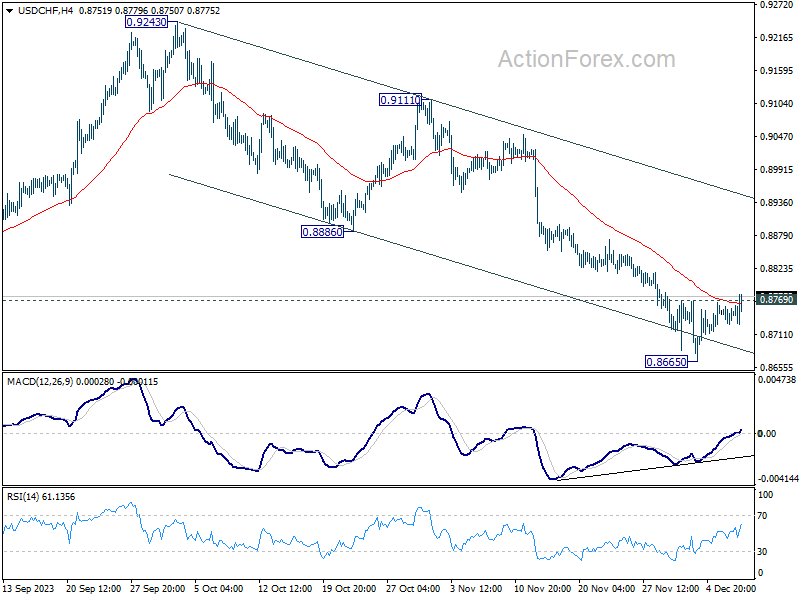

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8731; (P) 0.8746; (R1) 0.8762; More....

USD/CHF's break of 0.8769 minor resistance indicates short term bottoming at 0.8665, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 0.8886 support turned resistance first. Decisive break there will indicate that whole fall from 0.9243 has completed, and bring stronger rally to 0.9111 resistance next. For now, risk is mildly on the upside as long as 0.8665 support holds, in case of retreat.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. For now, this will remain the favored case as long as 0.8886 support turned resistance holds.

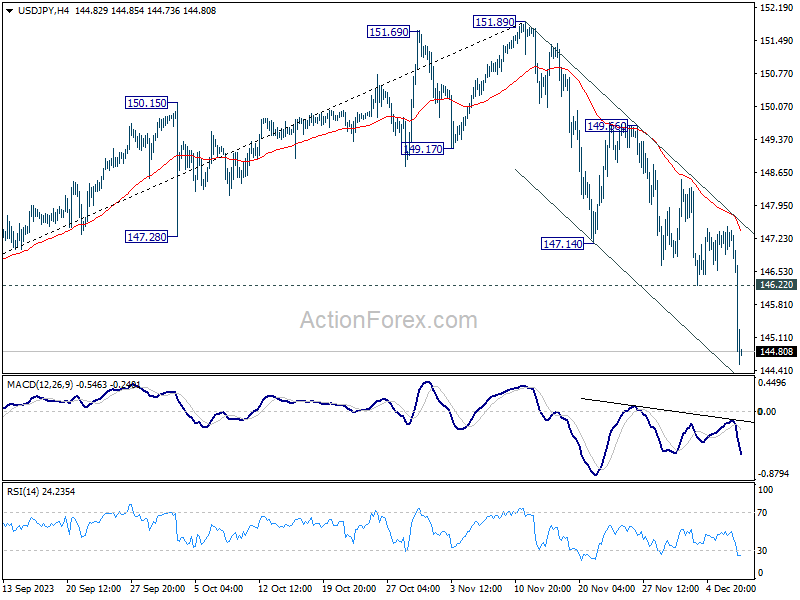

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.97; (P) 147.23; (R1) 147.57; More...

USD/JPY's decline accelerates to as low as 144.53 so far and there is no sign of bottoming yet. Intraday bias remains on the downside. Sustained trading below 145.06 will carry larger bearish implication and target 142.45 fibonacci level next. On the upside, break of 146.22 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, rise from 127.20 (2023 low) is seen as the second leg of the pattern from 151.93 (2022 high). Decisive break of 145.06 resistance turned support will confirm that this second leg has completed, after rejection by 151.93. Deeper fall would be seen through 38.2% retracement of 127.20 to 151.89 at 142.45 to 61.8% retracement at 136.63. Nevertheless strong bounce from 145.06 will retain medium term bullishness for another test on 151.93 at a later stage.