Sample Category Title

Dollar Staying Pressured Amid Risk-On Sentiment, Eyes on Michigan Consumer Sentiment Report

Dollar is still facing much broad-based pressure as risk-on sentiment continues to dominate the markets. A slight recovery could be on the cards due to pre-weekend profit-taking, although this largely hinges on the inflation expectation figures in the forthcoming University of Michigan Consumer Sentiment report. Should the inflation expectations display a substantial decrease, this could provide a further boost to risk appetite and potentially lead to another downturn for Dollar, before getting an opportunity to stabilize next week.

As far as this week's currency performance is concerned, Swiss Franc maintains its position as the strongest currency, outpacing even the persistently robust Japanese Yen. New Zealand and Australian dollars follow closely behind, despite their impressive runs. Canadian Dollar follows suit with Dollar as the second-weakest, while the Euro and Sterling trail somewhat behind.

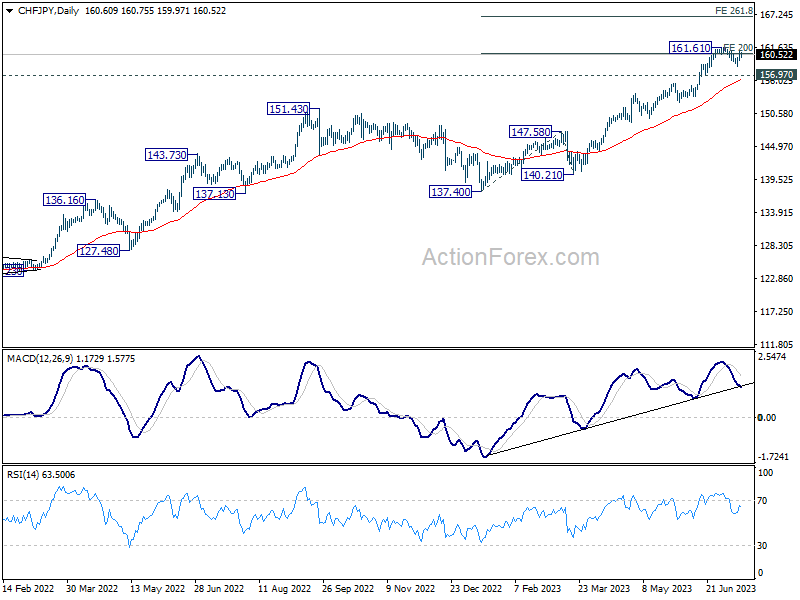

From a technical perspective, CHF/JPY stands out as an interesting pair to watch in order to gauge whether Swiss Franc can continue its domination over Yen. 200% projection of 137.40 to 147.58 from 140.21 at 160.57 was a resistance that limited CHF/JPY's advance. However, the pullback has been quite shallow, making it seem negligible in comparison to the steep decline observed in other Yen crosses. Outlook will stay bullish as long as 156.97 support holds. Firm break of 161.61 resistance will pave the way to 261.8% projection at 166.86.

In Asia, at the time of writing, Nikkei is up 0.08%. Hong Kong HSI is up 0.35%. China Shanghai SSE is up 0.27%. Singapore Strait Times is up 0.18%. Japan 10-year JGB yield is up 0.0096 at 0.477. Overnight, DOW rose 0.14%. S&P 500 rose 0.85%. NASDAQ rose 1.58%. 10-year yield dropped -0.10 to 3.761.

Fed Waller: Two more 25bps hikes this year necessary

In a speech, Fed Governor Christopher Waller expressed his support for the additional tightening to combat inflation. Despite this week's data showing a decrease in core CPI in June, Waller remains cautious, maintaining that "one data point does not make a trend."

Arguing for a proactive stance, Waller voiced his view that "two more 25-basis-point hikes" this year would be "necessary to keep inflation moving toward our target."

Waller believe there is "no reason why" the first hike should not occur this month. "If inflation does not continue to show progress and there are no suggestions of a significant slowdown in economic activity," he added", "then a second 25-basis-point hike should come sooner rather than later, but that decision is for the future."

Furthermore, Waller anticipates a need to keep policy restrictive for a while to encourage inflation to settle around the 2% target. "I am going to need to see this improvement sustained before I am confident that inflation has decelerated," he warned, calling for sustained evidence of improvement before he's fully convinced of any deceleration in inflation.

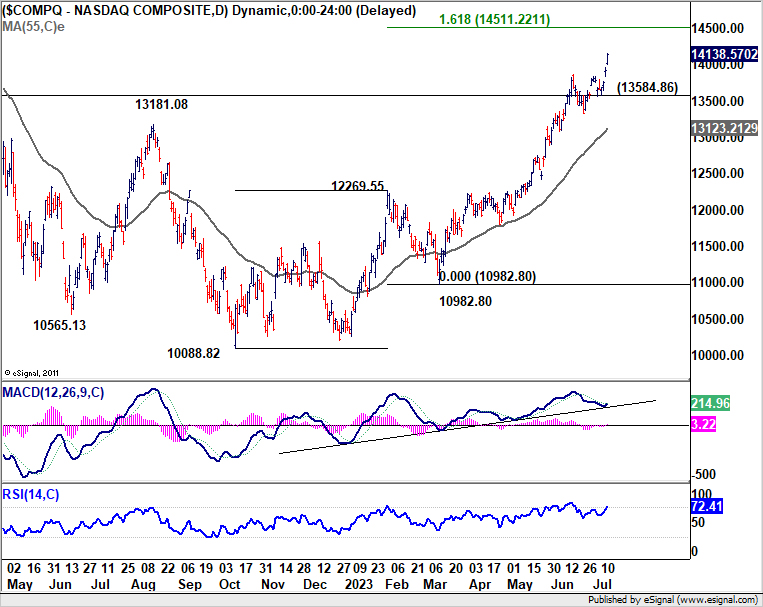

NASDAQ on track to 14511 as up trend extends

US stocks once again surged overnight, with NASDAQ and S&P 500 making new highs. Investors cheered this week CPI and PPI data from the US, which affirmed their expectation that only one more rate hike would be delivered by Fed. That came even though hawkish Fed officials continued to indicate the need for more tightening.

Technically speaking, NASDAQ's up rally from 1088.82 is still looking healthy. Outlook will stay bullish as long as 13584.86 support holds. Next target is 161.8% projection of 10088.82 to 12269.55 from 10982.80 at 14511.22. The index could start to lose upside momentum above that projection level, form a top without even testing 16212.22 high. Reading of D MACD should be watched closely to gauge the power of the move next.

Looking ahead

Swiss PPI, Italy trade balance and Eurozone trade balance will be released in European session. Canada will release manufacturing later in the day. US will release import price index and U of Michigan consumer sentiment.

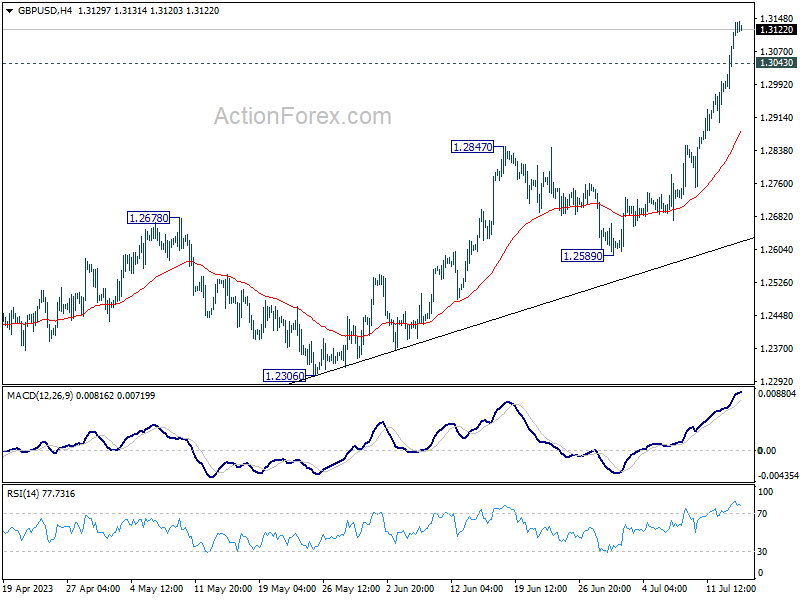

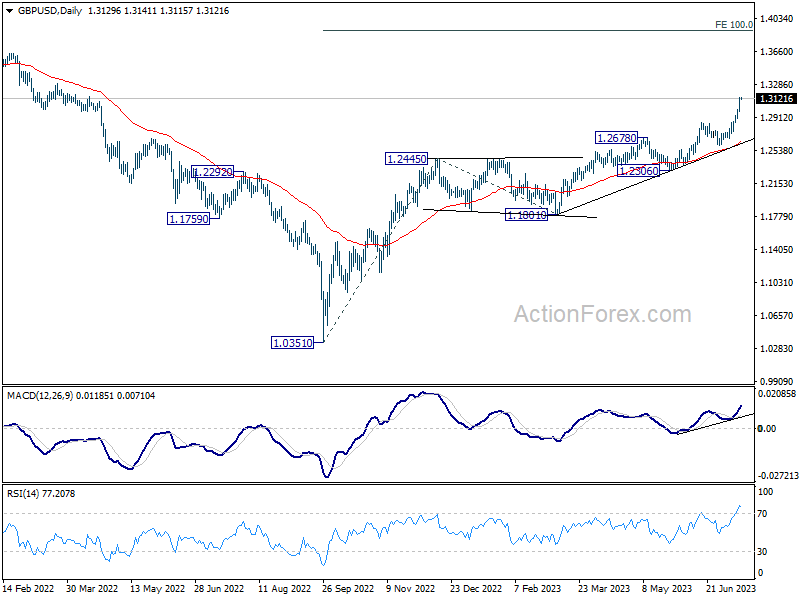

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3032; (P) 1.3087; (R1) 1.3190; More...

Intraday bias in GBP/USD remains on the upside for the moment. Current rally is part of the up trend from 1.0351. Next target is 100% projection of 1.0351 to 1.2445 from 1.1801 at 1.3895.On the downside, below 1.3043 minor support will turn intraday bias neutral first. But retreat should be contained by 1.2847 resistance turned support to bring another rally.

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2445 resistance turned support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 04:30 | JPY | Industrial Production M/M May F | -2.20% | -1.60% | -1.60% | |

| 06:30 | CHF | Producer and Import Prices M/M Jun | 0.20% | -0.30% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Jun | -0.30% | |||

| 08:00 | EUR | Italy Trade Balance (EUR) May | 1.45B | 0.32B | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | -10.3B | -7.1B | ||

| 12:30 | CAD | Manufacturing Sales M/M May | 0.80% | 0.30% | ||

| 12:30 | USD | Import Price Index M/M Jun | -0.60% | |||

| 14:00 | USD | Michigan Consumer Sentiment Index Jul P | 65.5 | 64.4 |

NASDAQ on track to 14511 as up trend extends

US stocks once again surged overnight, with NASDAQ and S&P 500 making new highs. Investors cheered this week CPI and PPI data from the US, which affirmed their expectation that only one more rate hike would be delivered by Fed. That came even though hawkish Fed officials continued to indicate the need for more tightening.

Technically speaking, NASDAQ's up rally from 1088.82 is still looking healthy. Outlook will stay bullish as long as 13584.86 support holds. Next target is 161.8% projection of 10088.82 to 12269.55 from 10982.80 at 14511.22. The index could start to lose upside momentum above that projection level, form a top without even testing 16212.22 high. Reading of D MACD should be watched closely to gauge the power of the move next.

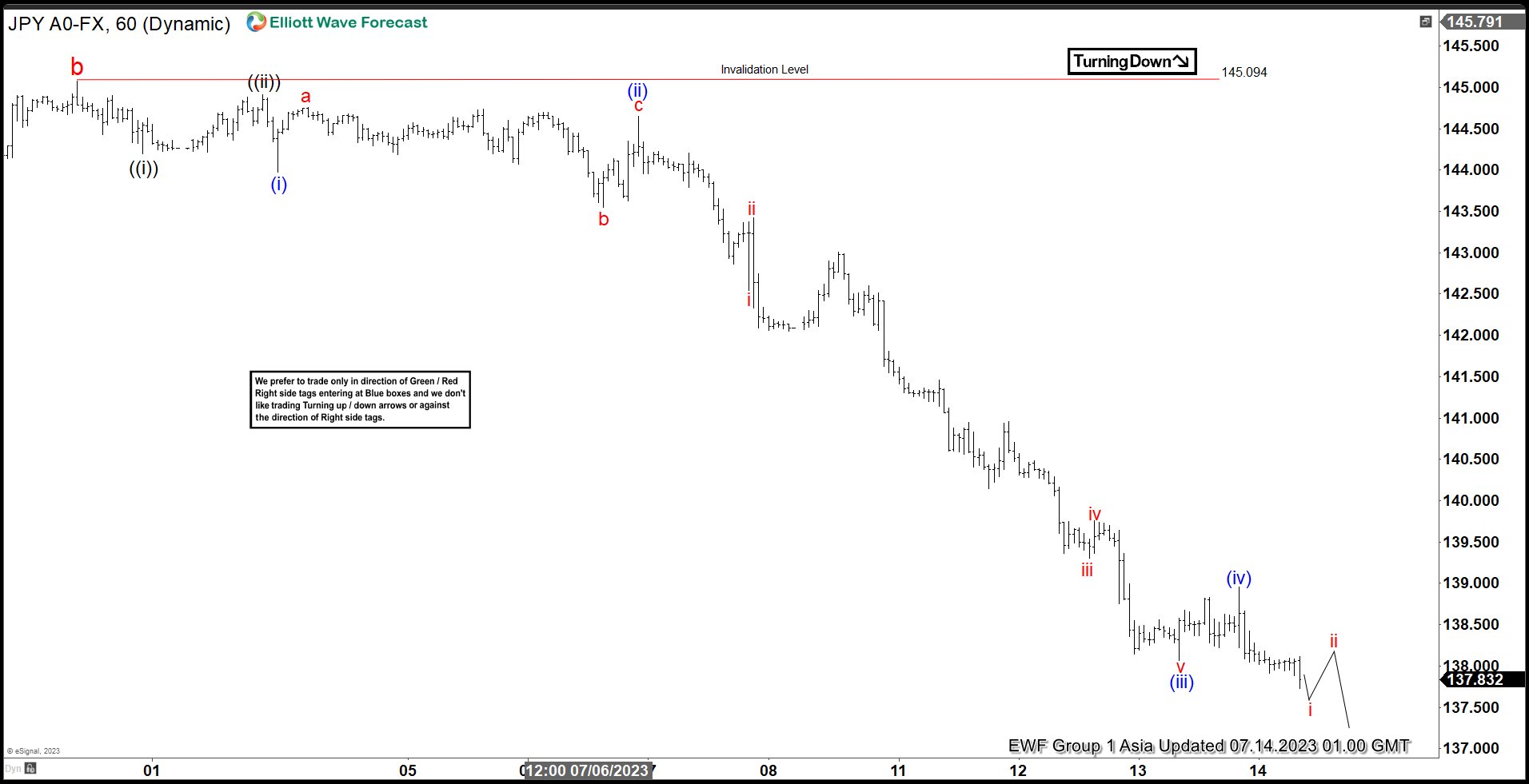

USDJPY Impulsive Decline Portends Further Weakness

Cycle from 10.21.2022 high is in progress as a zigzag Elliott Wave structure. Down from 10.21.2022 high, wave a ended at 127.22 and rally in wave b ended at 145.09. Pair has resumed lower in wave c. Down from wave b, wave ((i)) ended at 144.19 and rally in wave ((ii)) ended at 144.91. Pair resumes lower in wave ((iii)). Down from wave ((ii)), wave (i) ended at 143.97 and rally in wave (ii) ended at 144.65. Internal subdivision of wave (ii) unfolded as a running flat. Up from wave (i), wave a ended at 144.75, wave b ended at 143.54, and wave c ended at 144.65. This completed wave (ii).

Down from wave (ii), wave i ended at 142.54 and rally in wave ii ended at 143.41. Pair resumes lower in wave iii towards 139.3 and rally in wave iv ended at 139.75. Pair then resumes lower in wave v towards 138.06 which completed wave (iii) in higher degree. Corrective rally in wave (iv) ended at 138.95. Near term, as far as pivot at 145.09 high stays intact, expect rally to fail in 3, 7, or 11 swing for further downside.

USDJPY 60 Minutes Elliott Wave Chart

USDJPY Elliott Wave Video

https://www.youtube.com/watch?v=Npjk1aS1MFc

Fed Waller: Two more 25bps hikes this year necessary

In a speech, Fed Governor Christopher Waller expressed his support for the additional tightening to combat inflation. Despite this week's data showing a decrease in core CPI in June, Waller remains cautious, maintaining that "one data point does not make a trend."

Arguing for a proactive stance, Waller voiced his view that "two more 25-basis-point hikes" this year would be "necessary to keep inflation moving toward our target."

Waller believe there is "no reason why" the first hike should not occur this month. "If inflation does not continue to show progress and there are no suggestions of a significant slowdown in economic activity," he added", "then a second 25-basis-point hike should come sooner rather than later, but that decision is for the future."

Furthermore, Waller anticipates a need to keep policy restrictive for a while to encourage inflation to settle around the 2% target. "I am going to need to see this improvement sustained before I am confident that inflation has decelerated," he warned, calling for sustained evidence of improvement before he's fully convinced of any deceleration in inflation.

Cliff Notes: Confidence is Critical

Key insights from the week that was.

Beginning in Australia, the Westpac-MI Consumer Sentiment survey delivered a lacklustre update on confidence. At 81.3, the headline index remains firmly entrenched at extremely pessimistic levels, an outcome that has only been associated with major economic dislocations over the survey’s near fifty-year history. Driving this sustained weakness in sentiment has been a marked deterioration in views over the economy’s prospects and family finances for the year ahead, with these sub-indexes now 10% and 16% below their respective long-run averages. The cost-of-living remains a considerable constraint for households, the sub-index covering spending intentions on ‘major household items’ nearly 40% below its long-run average.

Another key theme discussed by Chief Economist Bill Evans after the July survey’s release is the impact of inflation and interest rates on confidence. Curiously, the RBA’s decision to leave the cash rate unchanged in July offered no support; indeed, sentiment was much weaker after the meeting than before (77.9 vs. 88.0). Available data gives context to this result. Evidence over the past year suggests inflation has had a greater impact on confidence than interest rates. May’s deceleration in the Monthly CPI Indicator from 6.8%yr in April to 5.6%yr and the consequent rally in sentiment pre-RBA to 88.0 also support this thesis. However, in noting “Some further tightening of monetary policy may be required”, the RBA made clear that policy will likely have to be tightened further to get inflation sustainably back to target. The material chance of further hikes and a lengthy period of above-target inflation arguably drove confidence back down to 77.9 post-RBA, 1.6% below the final June outcome.

The emerging weakness evident in business conditions is becoming more consistent with consumers’ pessimistic view on the state of the economy. The NAB business survey indicates that the current assessment of business conditions has taken a material step back over the last two months, down from +15 in April to +9 in June. With forward orders posting consecutive declines over May/June against a backdrop of soft and fragile business confidence, the survey’s shift in tone is clear, foreshadowing the prospect of a further slowing in the economy over the remainder of the year.

Before moving offshore, it is worth highlighting that RBA Deputy Governor Michele Bullock has been appointed as RBA Governor for a seven year term commencing September 18. This development comes at a time where the RBA’s monetary policy processes and communication guidelines are being assessed and modified in light of the Government’s Review.

Events offshore this week also provided a number of notable headlines.

The Bank of Canada raised rates again by 25bps to 5% as fears of persistent inflation prompted action. This is the second rate hike since the BoC decided to pause earlier this year. Inflation has eased off the back of lower energy prices; however, broad-based strength remains elsewhere. Spending data shows evidence of excess demand across the economy, with household consumption driving GDP growth in the March quarter and more timely indicators like retail sales suggesting consumers have plenty of cash to splash. This comes alongside a housing market that is starting to find its floor. New projections suggest the CPI will hover around 3% for a year. The BoC experience is a perfect example of why central banks must be wary of the risks of ending their tightening cycle too soon.

South of the border, the US CPI made headlines as it came in softer than expected at 0.2%mth for both headline and core inflation. There were clear signs of a broad-based deceleration as momentum in goods and services ex-shelter continued to slow. However, shelter continues to cause concern, contributing a whopping 2.1ppts to annualised headline inflation in Q2 thanks to its 35% weight and 6.0% gain. Here is evidence that shelter has the capacity to create at or above target outcomes for inflation by itself should rent inflation hold up rather than decelerate as is our base expectation.

The Federal Reserve’s July Beige Book was also constructive for the inflation outlook. Economic activity was reported to have “increased slightly since May”, employment only “modestly”. Most significant for inflation is that the “unusually high [labour market] turnover rates in recent years appear to be returning to pre-pandemic norms” and contacts “in multiple Districts reported that wage increases were returning to or nearing pre-pandemic levels”. Despite this, signs of labour market slack have yet to show up meaningfully. Initial jobless claims fell to 237k, driving down the four-week average to 246.8k.

Across the Tasman meanwhile, the Reserve Bank of New Zealand kept rates steady at 5.5% in line with expectations. The statement noted “monetary conditions are constraining domestic spending as expected” and there was nothing to indicate their thinking had changed vis a vis keeping the OCR on hold until the second half of 2024. The next meeting will reflect the Committee's view of the June CPI print and labour report. Should either come in stronger than expected, the central bank will be keen to get on the front foot and raise the policy rate by 25bps. It is Westpac’s view that they likely will.

Over east, the Chinese June price outcomes were weak, the CPI flat year-over-year and the PPI down 5.4%yr. Base effects are significant for these outcomes, the impact of Russia's invasion of Ukraine on supply chains and energy and commodity prices falling out. However, excess capacity across the economy and a continued push to grow industry further amid a modest post-COVID rebound is also at play.

To counteract some of this weakness, the government has eased key policy rates and increased liquidity. They are also likely encouraging lending by the banks behind the scenes. Aided by these steps, M2 money supply rose 11.3%yr off a strong base in 2022, and new loans came in well above expectation in June at CNY3050bn. Benefitting both now and the medium-term, the trade balance remained wide in June at US$70.6bn albeit shy of expectations, US$74.9bn. To sustain this sizeable income inflow, Asian demand has to make up for weak and deteriorating developed-world demand.

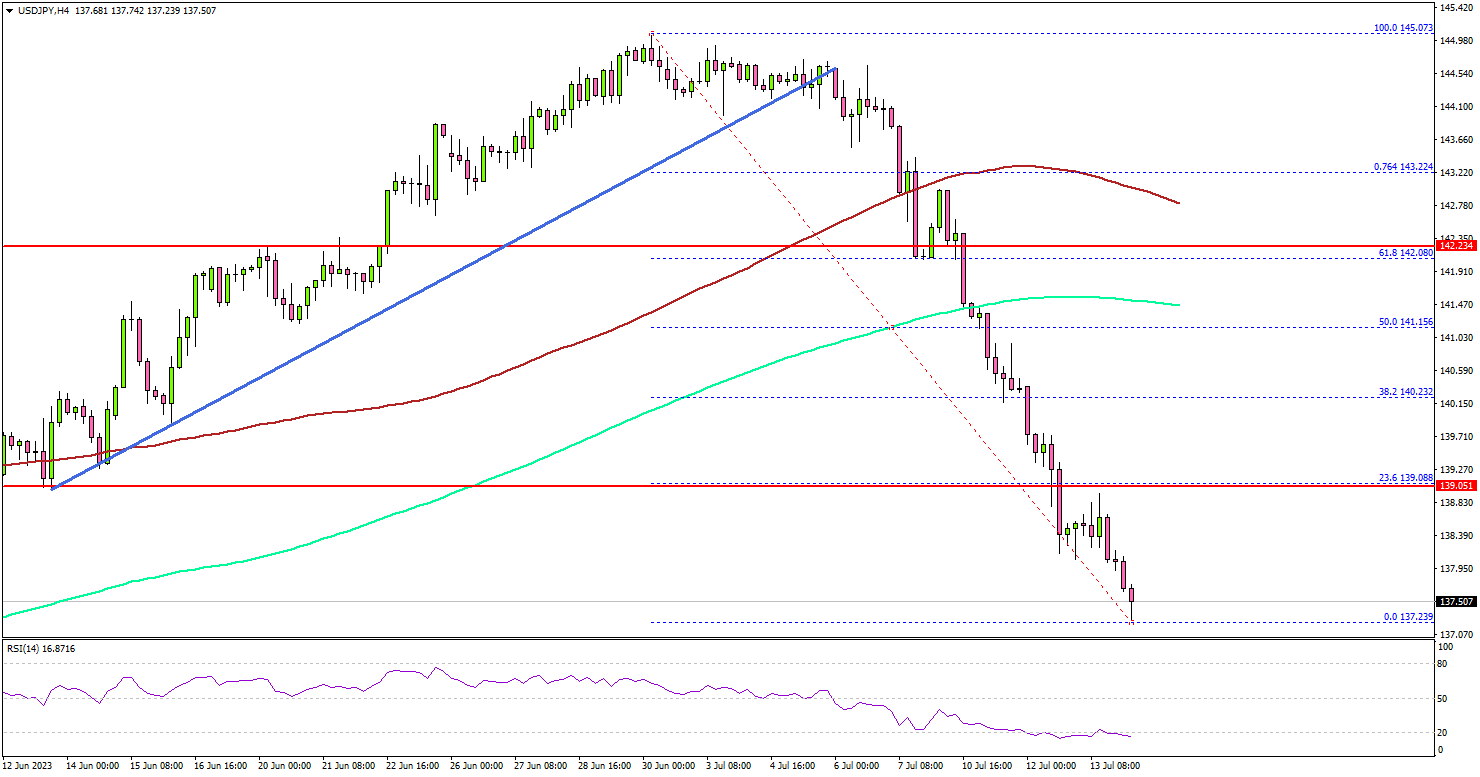

USD/JPY Takes Big Hit, EUR/USD and GBP/USD Extend Rally

Key Highlights

- USD/JPY declined heavily below 142.00 and 140.00.

- It traded below a key bullish trend line with support near 144.20 on the 4-hour chart.

- EUR/USD rallied further above 1.1150.

- GBP/USD surged above the key 1.3000 resistance zone.

USD/JPY Technical Analysis

The US Dollar started a major decline from the 145.00 zone against the Japanese Yen. USD/JPY traded below a key bullish trend line with support near 144.20.

Looking at the 4-hour chart, the pair settled below the 142.00 support, the 200 simple moving average (green, 4 hours), and the 100 simple moving average (red, 4 hours).

There was a sharp move below the 140.00 support. The pair tested the 138.00 zone and remains at risk of more losses. Immediate support is near the 138.00 level. The next major support is at 137.40, below which there could be a drop to 136.50.

On the upside, immediate resistance is near the 139.10 level. The next major resistance is near 139.80. The first major resistance is near the 140.00 level.

If there is a move above the 140.00 resistance, the pair could rise toward 140.80. Any more gains might send the pair toward the 142.00 resistance zone, where the bears might emerge.

Looking at EUR/USD, the pair gained strength and rallied above 1.1150. Similarly, GBP/USD surged above the 1.3000 and 1.3050 resistance levels.

Economic Releases

- US Import Price Index for June 2023 (MoM) – Forecast -0.2%, versus -0.6% previous.

- US Export Price Index for June 2023 (MoM) – Forecast -0.2%, versus -1.9% previous.

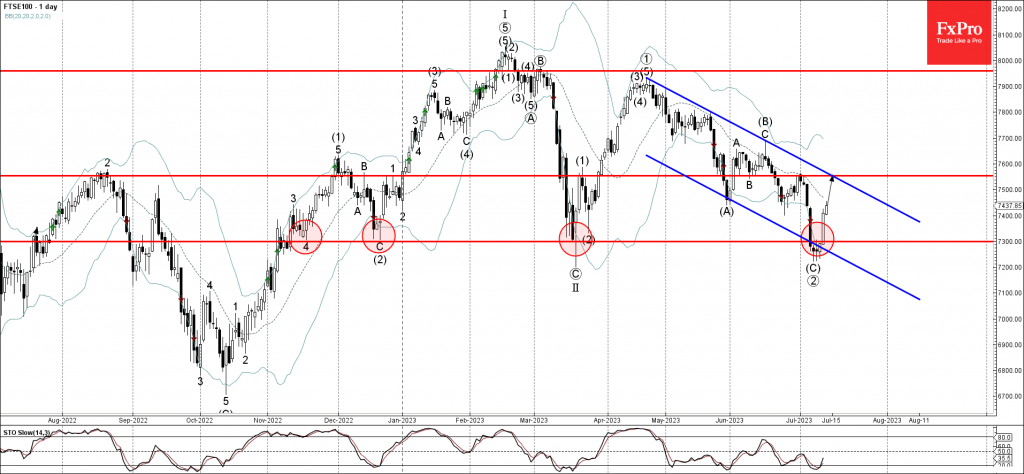

FTSE 100 Wave Analysis

- FTSE100 reversed from key support level 7300.00

- Likely to rise to resistance level 7550.00

FTSE100 index recently reversed up sharply after the index failed to break below the key support level 7300.00, which has been reversing the price from last November.

The upward reversal from the support level 7300.00 stopped the intermediate downward impulse (C)-wave from June.

FTSE100 index can be expected to rise further toward the next resistance level 7550.00 (previous minor reversal high from the end of last month).

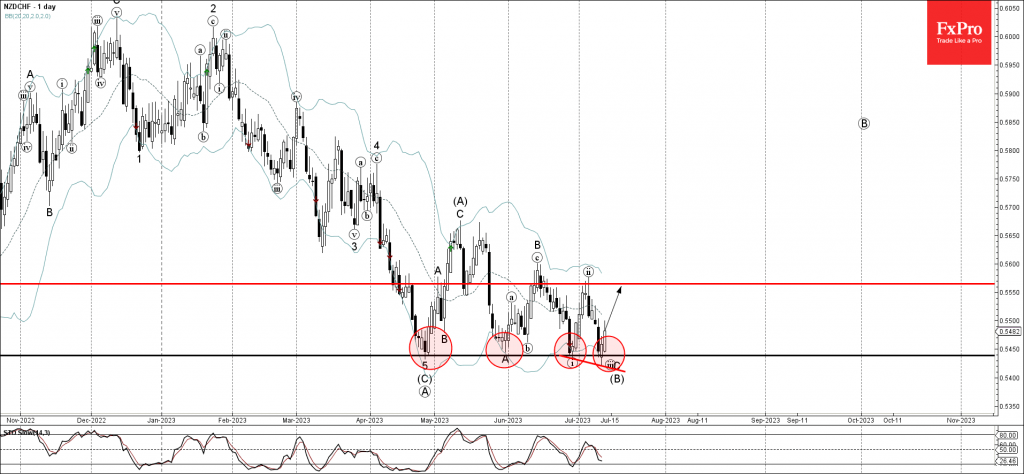

NZDCHF Wave Analysis

- NZDCHF reversed from support level 0.5440

- Likely to rise to resistance level 0.5565

NZDCHF recently reversed up with the daily Morning Star from the key multi-month support level 0.5440, which has been reversing the price from the end of April.

The upward reversal from the support level 0.5440 stopped the C-wave of the previous ABC correction B from May.

Given the strength of the support level 0.5440, NZDCHF can be expected to rise further toward the next resistance level 0.5565 (top of the previous minor correction (ii)).

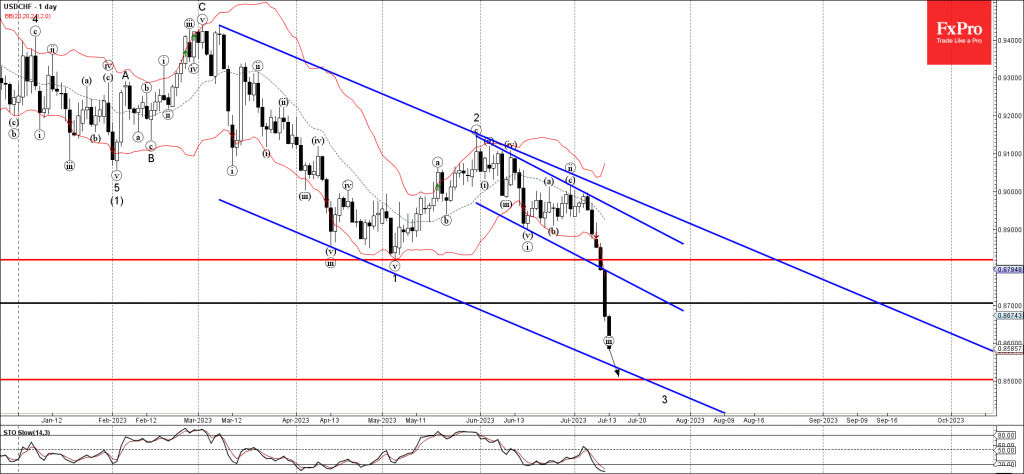

USDCHF Wave Analysis

- USDCHF falling inside impulse wave 3

- Likely to fall to support level 0.8500

USDCHF continues to fall strongly after the price broke below the pivotal support level 0.8820, former monthly low from May.

The breakout of the support level 0.8820 accelerated the active short-term impulse wave 3 of the weekly downward impulse wave C from the start of March.

Given the strong multi-year downtrend and widespread dollar sales, USDCHF can be expected to fall further toward the next support level 0.8500 (target for the completion the active impulse wave 3).