Sample Category Title

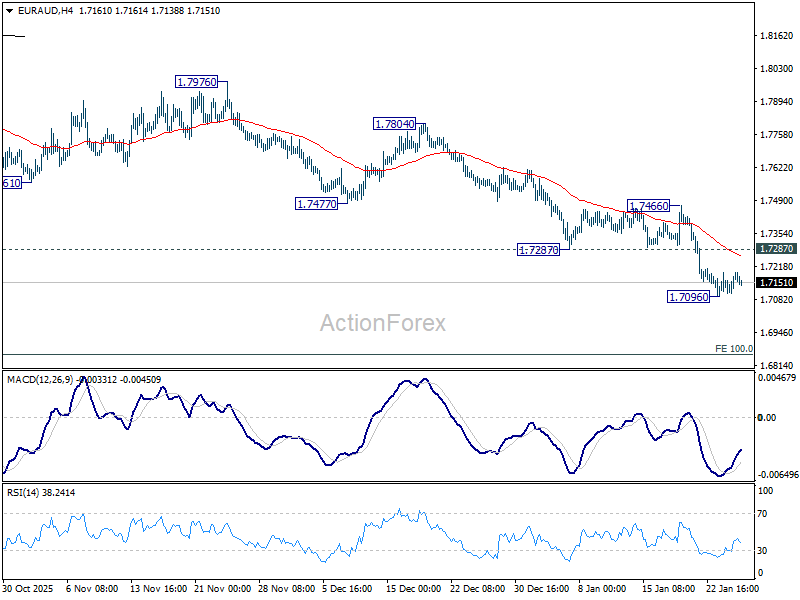

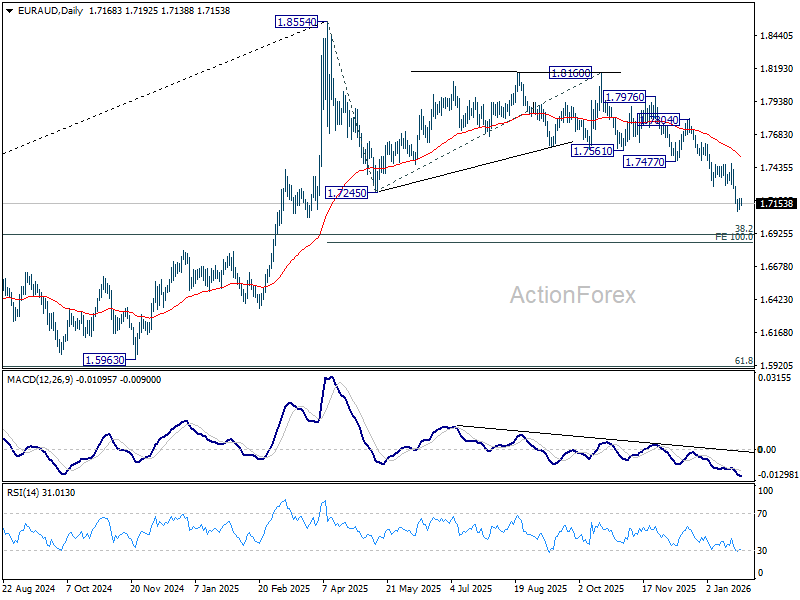

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7127; (P) 1.7161; (R1) 1.7210; More...

Intraday bias in EUR/AUD is turned neutral first with current recovery and some consolidations would be seen. Further decline is expected as long as 1.7287 support turned resistance holds. Fall from 1.8160 is seen as the third leg of the corrective pattern from 1.8554. Below 1.7096 will target 100% projection of 1.8554 to 1.7245 from 1.8160 at 1.6851.

In the bigger picture, the break of 55 W EMA (now at 1.7464) argues that fall from 1.8554 medium term top is correcting whole up trend from 1.4281 (2022 low). Deeper decline is in favor to 38.2% retracement of 1.4281 to 1.8554 at 1.6922, and possibly below. Risk will stay on the downside as long as 55 D EMA (now at 1.7537) holds, in case of strong rebound.

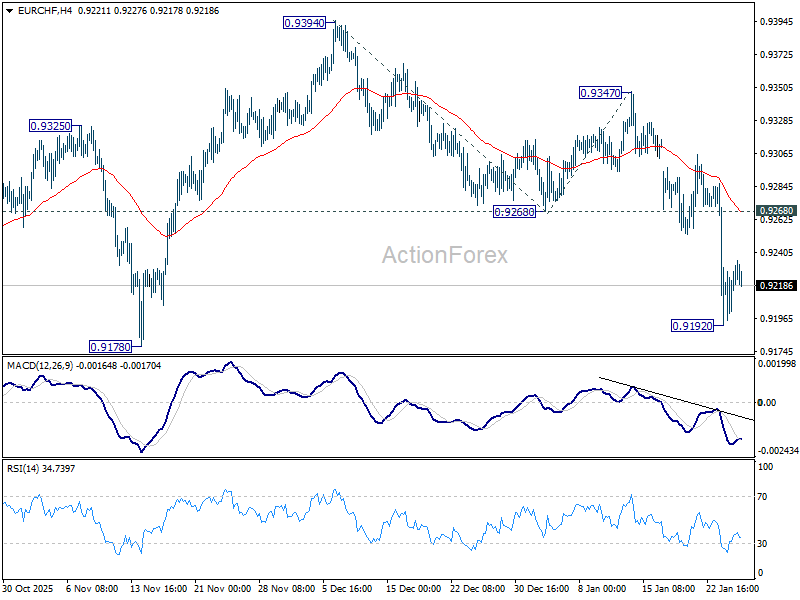

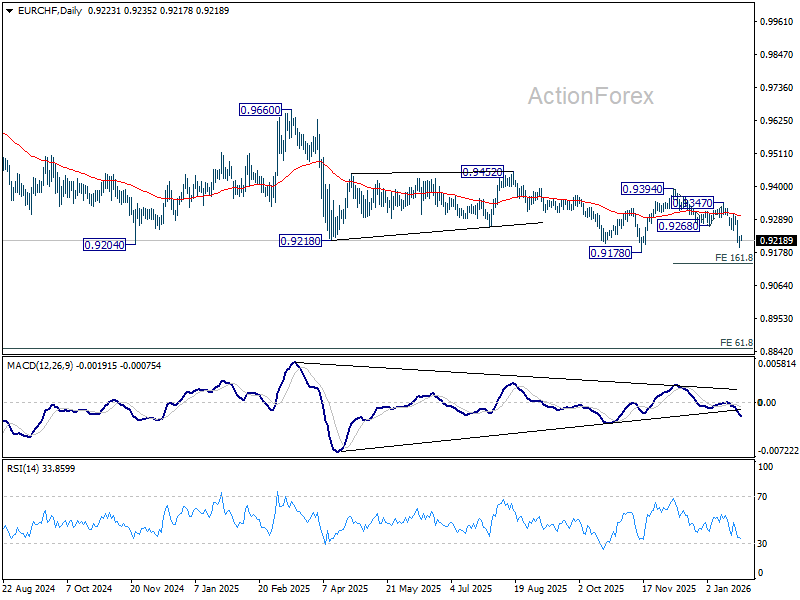

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9206; (P) 0.9219; (R1) 0.9244; More....

Intraday bias in EUR/CHF is turned neutral first with current recovery and some consolidations would be seen first. Further fall is expected as long as 0.9268 support turned resistance holds. Below 0.9192 will bring retest of 0.9178 low. Firm break there will resume larger down trend.

In the bigger picture, another rejection by 55 W EMA (now at 0.9350) keeps outlook bearish. Downtrend from 1.2004 (2018 high) is still in progress. Firm break of 0.9178 will target 61.8% projection of 1.1149 to 0.9407 from 0.9928 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

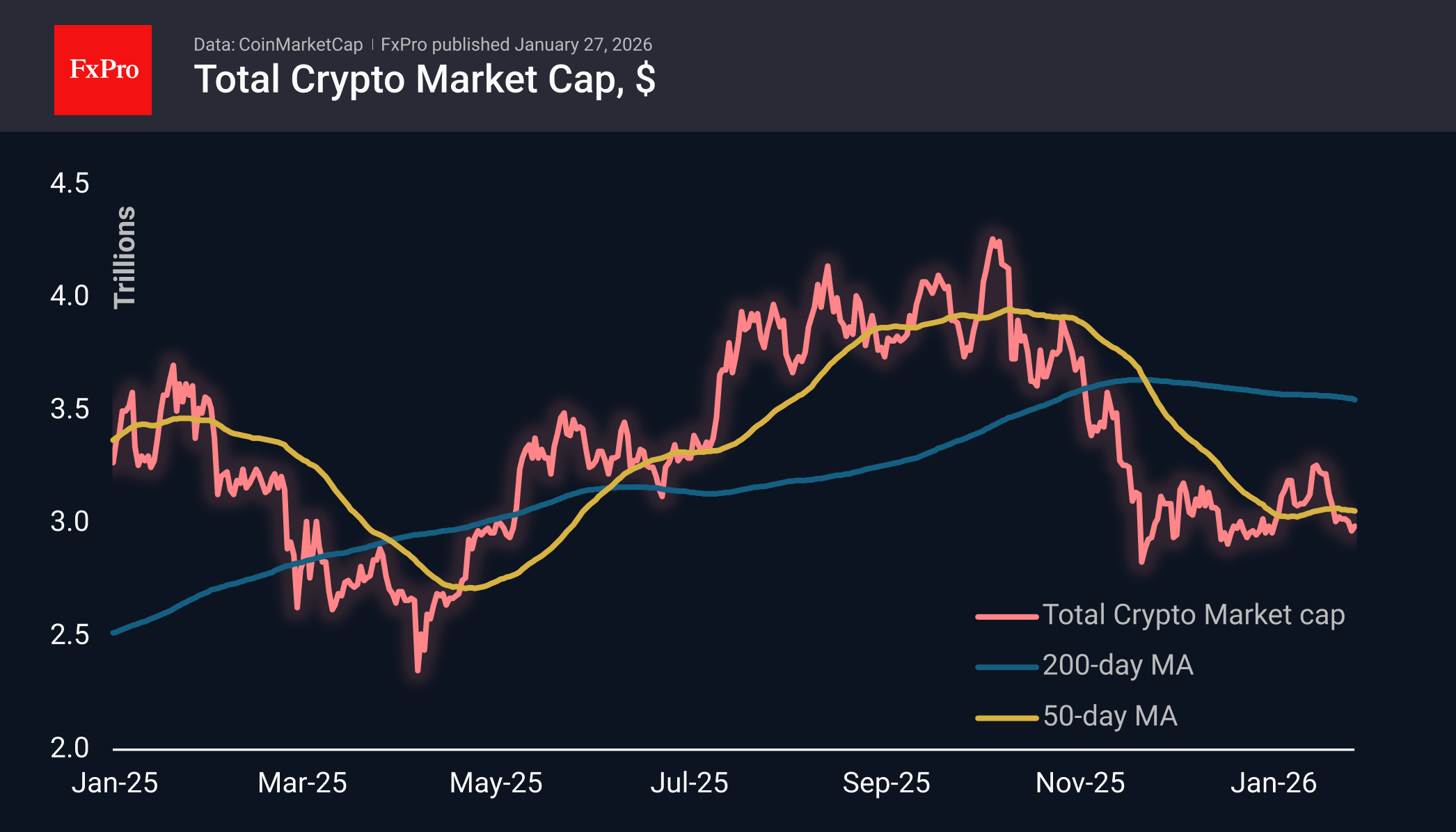

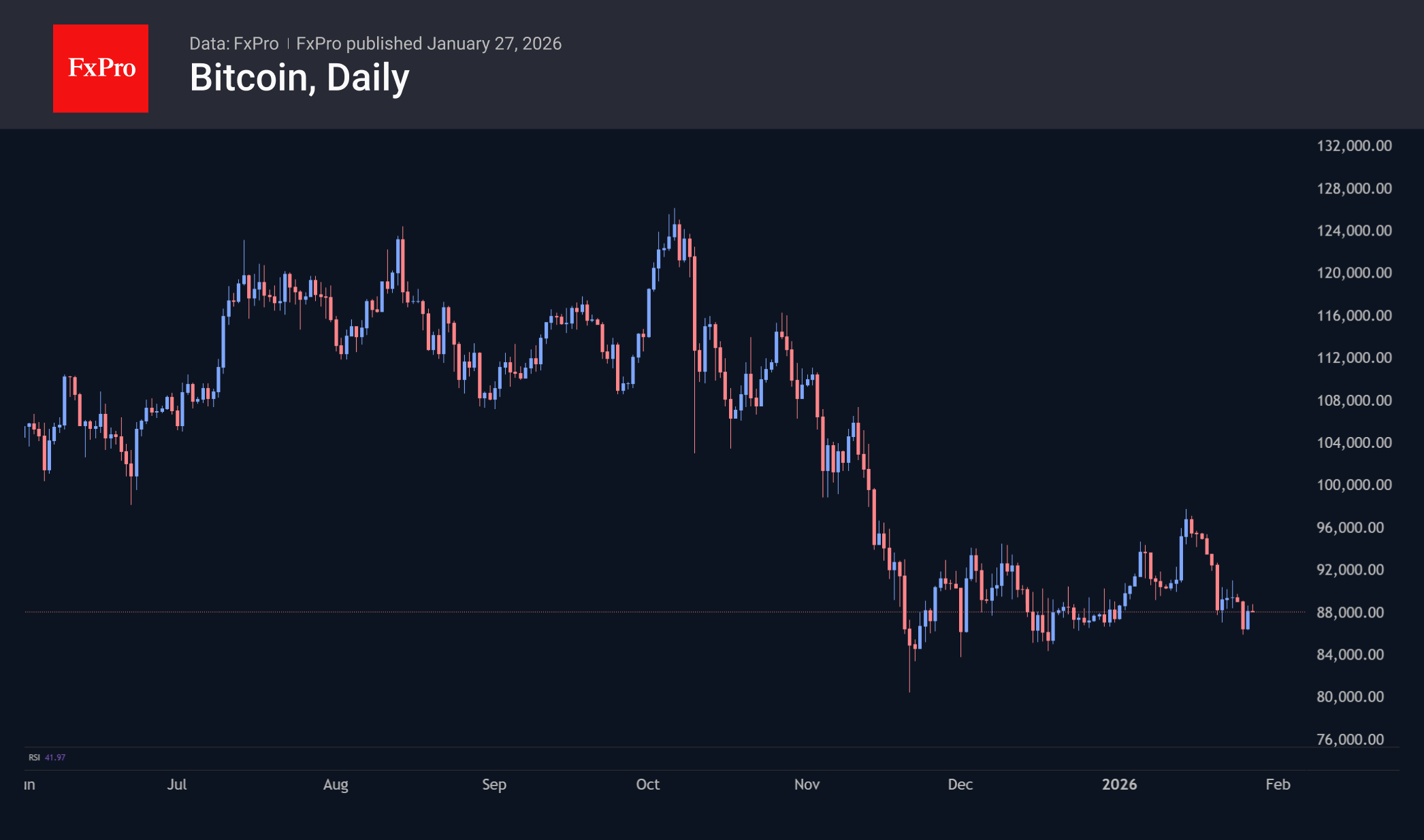

Risk-on, But Not for Crypto

Market Overview

The crypto market capitalisation grew by 0.67% over the past day to $2.99 trillion. Bulls are seeking to take advantage of increased risk appetite in traditional markets but are facing increased selling pressure as they approach the $3 trillion mark. Of course, this is not one big ‘battle for crypto,’ but a series of separate battles in cryptocurrencies, where the flagships are doing slightly better, with Ethereum, BNB, XRP, and Solana gaining about 1.5% over the past 24 hours.

Bitcoin is up 0.6% on the day, trading above $88K, having encountered increased selling pressure over the last two days in attempts to climb above $89K, despite the collapse of the dollar, which has already helped the stock and metals markets. At times, it seems that speculators’ capital and attention are now focused exclusively on precious metals (mainly gold and silver), and there is simply no strength left for crypto.

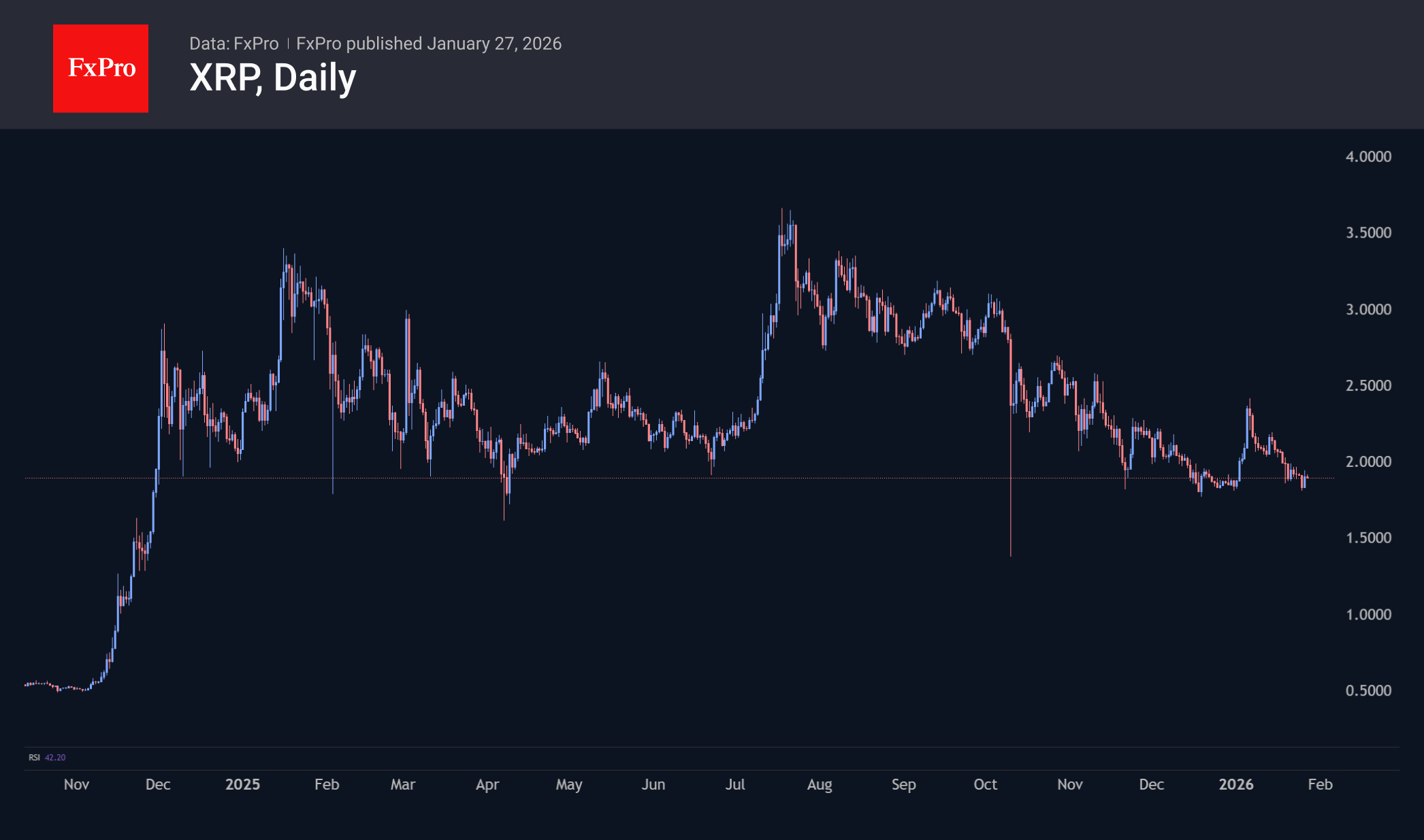

XRP has stabilised at $1.9, a horizontal support level where the coin’s sell-off has been halted since December 2024. A breakdown of this support could lead to a more profound decline in the market to the $0.5 area, which is the most important long-term support. If XRP manages to form a bottom, this will open the way to the $3.10-3.50 area.

News Background

The largest outflow from global crypto ETFs since mid-November 2025 was likely fuelled by lower expectations of interest rate cuts, according to CoinShares. This indicates that investor sentiment has still not improved since the price collapse on 10 October 2025.

Investors’ realised losses on Bitcoin reached $4.5 billion, a three-year high. CryptoQuant calls what is happening a market capitulation. The last time this happened was after an annual correction, when Bitcoin was trading at $28,000.

The key danger to the Bitcoin blockchain is posed by ‘ambitious opportunists’ seeking to change the protocol, said Strategy founder Michael Saylor. This could refer to developers promoting controversial use cases for the network, such as NFT issuance or image storage.

The hash rate of the largest mining pool, Foundry USA, has fallen by 60%. Data centre operators in the US are shutting down equipment en masse due to extreme weather caused by winter storm Fern.

US Dollar Index (DXY) Falls to Its Lowest Level Since September

As the DXY chart shows, the US dollar index is trading today at its lowest level since September 2025. From this month’s peak, the decline has exceeded 2%.

Why Is the Dollar Weakening?

→ The Fed factor. The interest rate decision is due tomorrow. Markets are expecting dovish rhetoric from Jerome Powell to offset economic risks stemming from tariff wars. It cannot be ruled out that the Fed Chair may soften his stance under unprecedented pressure from the White House administration, including threats of criminal prosecution.

→ Loss of safe-haven status. The dollar is losing appeal as a defensive asset amid geopolitical tensions (the US–EU dispute over Greenland and strained relations with Canada). Capital is actively flowing out of fiat currencies into real assets, as confirmed by yesterday’s historic breakout in gold prices above $5,000.

That said, the technical picture offers some grounds for optimism among bulls.

Technical Analysis of the DXY Chart

On 20 January, when analysing the US Dollar Index (DXY), we:

→ updated the descending channel (marked in red);

→ suggested that the downtrend could continue, with a move towards the channel median.

However, bears exceeded our expectations and, after testing the upper boundary on 21 January (as shown by the arrow), pushed the price towards the lower boundary of the channel, which tends to act as support.

Moreover, the DXY index is now hovering near a long-term support zone from which the price rebounded twice in the second half of 2025.

This suggests that the aggressive downward momentum may be running out of steam, with the market likely to shift into a wait-and-see mode ahead of the Fed’s decision. Be prepared for spikes in volatility tomorrow between 22:00 and 22:30 GMT+3.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Nasdaq 100 Advances Ahead of Tech Giants’ Earnings

As early as tomorrow, after the close of the main trading session, quarterly results will be released by Microsoft (MSFT), Meta Platforms (META) and Tesla (TSLA), with Apple (AAPL) scheduled to report on Thursday.

As the chart shows, the Nasdaq 100 index (US Tech 100 mini on FXOpen) climbed today to its highest level since early November, rising above 25,900. Since the start of the week, the index has gained around 1.8%. This appears to reflect a shift in market sentiment:

→ Geopolitical risks are fading. Market participants seem to have adapted to the news flow surrounding tariffs and Greenland. After the initial shock, current political rhetoric is increasingly viewed as a negotiating stance rather than a genuine threat to business.

→ Confidence in market leaders. Prices are factoring in expectations that tech giants will outline roadmaps showing how their record AI spending will begin to generate net profits as early as this year.

Technical Analysis of the Nasdaq 100 Chart

Price action in the Nasdaq 100 index (US Tech 100 mini on FXOpen) points to demand-side dominance:

→ the downward trajectory seen between 16 and 21 January was broken by bulls on the 22nd, with a spike in volatility (visible on the ATR indicator) highlighting a sharp change in market behaviour;

→ recent fluctuations have formed an ascending channel (shown in blue);

→ the market has confidently recovered from the bearish gap seen at the start of the week;

→ the broad bullish candle on Monday, 26 January, signals a demand imbalance, with the rally zone showing signs of support (marked by a rectangle).

From the supply-side perspective:

→ the move above the 13 January high could turn out to be a false bullish breakout (another one, judging by Nasdaq 100 price action over recent months);

→ price is currently hovering near the upper boundary of the existing channel.

A modest technical pullback in the coming days cannot be ruled out, although the key driver is likely to be market reactions to upcoming corporate earnings.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

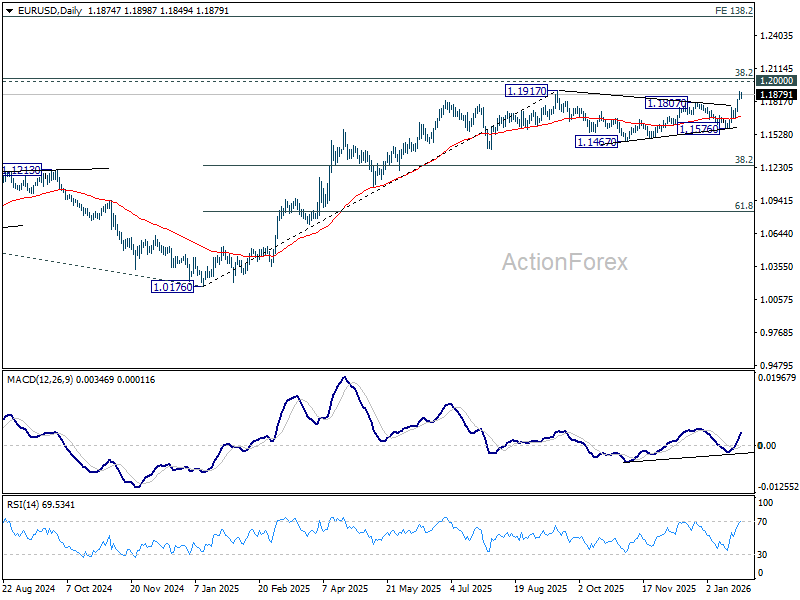

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1842; (P) 1.1874; (R1) 1.1914; More….

Intraday bias in EUR/USD stays on the upside as current rally should target a test on 1.1917 key resistance. Firm break there will resume larger up trend to 1.2000 key psychological resistance. On the downside, below 1.1812 minor support will mix up the outlook and turn intraday bias neutral again.

In the bigger picture, as long as 55 W EMA (now at 1.1443) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.25841. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

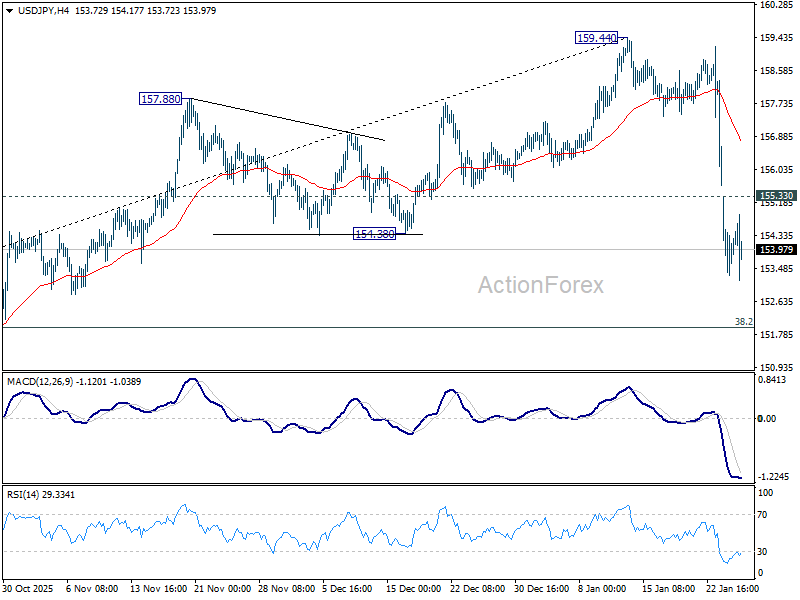

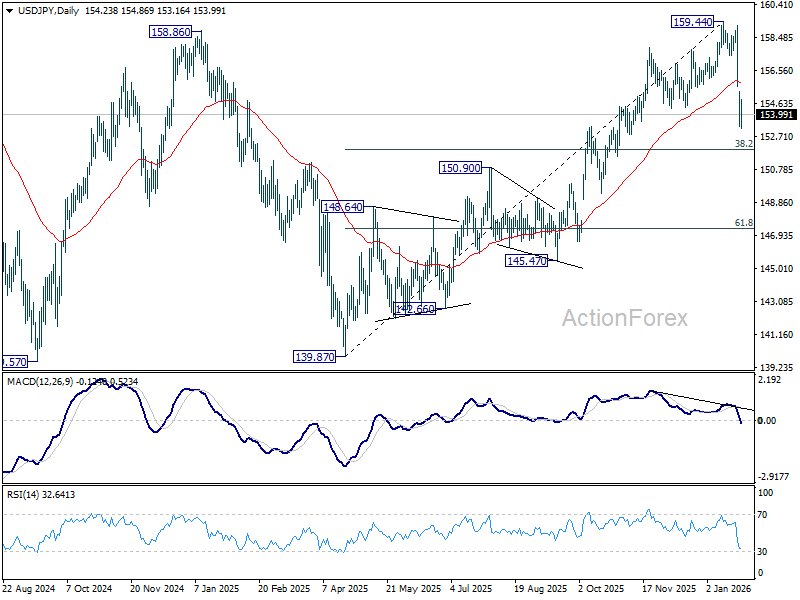

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.23; (P) 154.29; (R1) 155.27; More...

Intraday bias in USD/JPY stays on the downside at this point. For now, fall from 159.44 is seen as correcting the rise from 139.87. Deeper decline should be seen to 38.2% retracement of 139.87 to 159.44 at 151.96. Strong support should be seen there to bring rebound, at least on first attempt. On the upside above 155.33 minor resistance will turn intraday bias neutral and bring consolidations first. However, decisive break of 151.96 will argue that it is reversing whole rise from 139.87. Deeper decline would then be seen to 61.8% retracement at 147.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.35) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

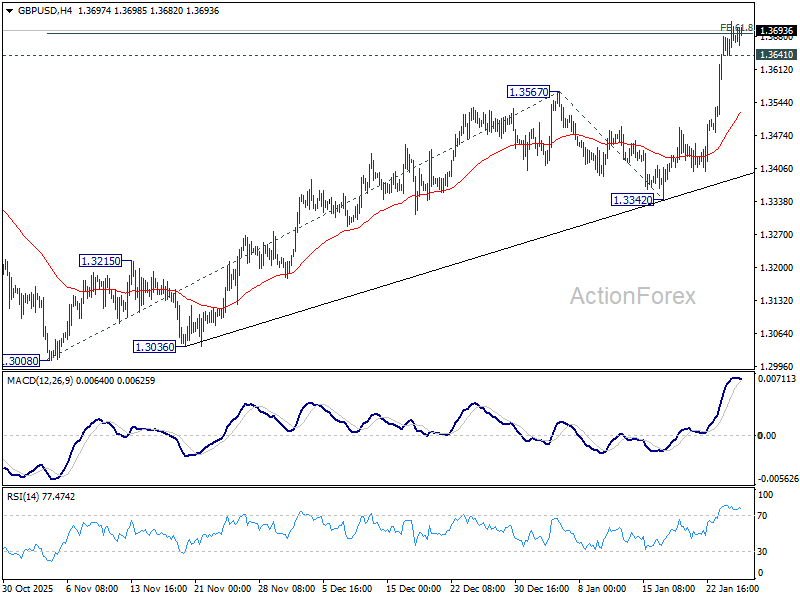

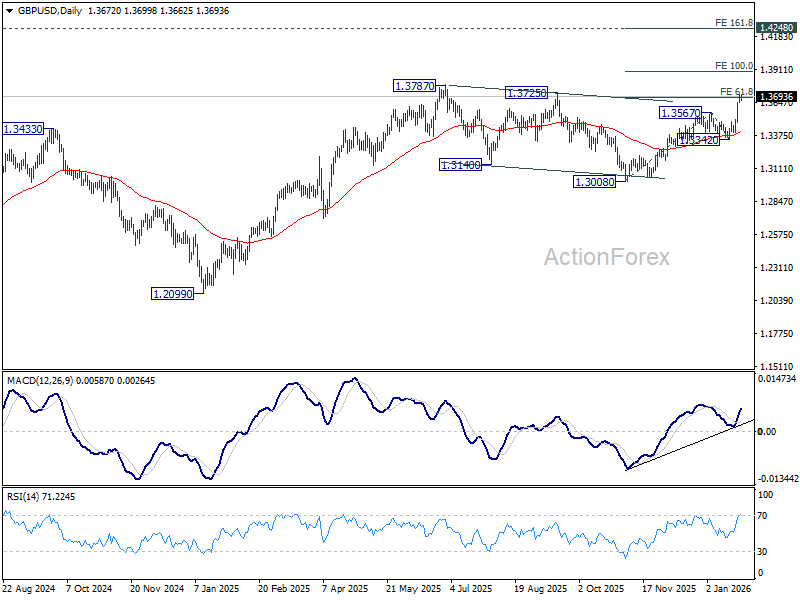

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3644; (P) 1.3678; (R1) 1.3714; More...

Intraday bias in GBP/USD stays on the upside at this point. Sustained trading above 61.8% projection of 1.3008 to 1.3567 from 1.3342 at 1.3687 should prompt upside acceleration through 1.3787 high to 100% projection at 1.3901. On the downside, below 1.3641 minor support will turn intraday bias neutral. But retreat should be contained well above 1.3342 support to bring another rally.

In the bigger picture, price actions from 1.3787 (2025 high) are seen as a correction to the larger up trend from 1.3051 (2022 low). That might have completed at 1.3008 already. Firm break of 1.3787 will confirm up trend resumption. Next target is 1.4284 key resistance (2021 high). This will remain the favored case as long as 1.3008 support holds.

Dollar Consolidates as Geopolitics Take a Breather

The forex market has finally slipped into a period of stabilization, with Dollar shifting into consolidation after several volatile sessions. All major pairs and crosses are trading within yesterday’s ranges, signaling a collective pause. Part of the calm reflects a temporary cooling in geopolitical and trade-war rhetoric. Recent fears of an imminent joint US–Japan intervention to support the Yen have faded. At the same time, broader trade tensions appear contained for now.

Attention is also shifting to tomorrow’s FOMC rate decision. With little fresh macro impetus elsewhere, markets appear content to wait on guidance from policymakers rather than force directional moves prematurely. There is little doubt about the outcome itself. The Fed is universally expected to keep rates unchanged at 3.50–3.75%, making this meeting more about communication than action.

As such, focus will fall on the policy statement and Chair Jerome Powell’s press conference. With the outlook still clouded by political and trade uncertainty, expectations for dramatic shifts in tone remain low. The most likely outcome is a reaffirmation of a wait-and-see approach, emphasizing data dependence and flexibility. Policymakers have little incentive to pre-commit in an environment where fiscal, trade, and geopolitical risks remain fluid.

Still, subtle nuances could matter. The Fed may seek to reassure markets that the current hold is merely a pause within an easing cycle, awaiting clearer confirmation before delivering another cut. Alternatively, though less likely, the messaging could evolve toward a more open-ended pause, dropping any implicit bias toward future easing. The distinction is small on paper, but meaningful for market expectations and forward pricing.

On the trade front, fresh headlines reminded markets that policy risk has not disappeared. US President Donald Trump threatened to raise tariffs on South Korean exports to 25% from 15%, citing delays in Seoul’s parliament approving a bilateral trade framework agreed last year. South Korea moved quickly to respond. A spokesperson for the ruling Democratic Party said Trump was likely referring to legislation linked to the USD 350 billion investment commitment to the US, adding that multiple related bills are already under review and likely to pass with bipartisan support.

Elsewhere, trade developments offered a more constructive signal. Prime Minister Narendra Modi announced that India and the EU had finalized a “landmark” free trade agreement, with details expected to be unveiled later alongside President Ursula von der Leyen. The deal would link economies representing roughly a quarter of global GDP.

In currency markets, Yen remains the strongest performer for the week, though momentum has started to fade. Swiss Franc follows, with Aussie also holding firm. Loonie is the weakest, weighed down by trade concerns, followed by Dollar and Sterling, while Euro and Kiwi sit in the middle.

Australia NAB business survey reinforces solid backdrop for RBA

Australia’s NAB business survey showed a modest but broad-based improvement in December, pointing to resilient momentum into year-end. Business Confidence edged up from 2 to 3, while Business Conditions rose from 7 to 9.

The details underline that improvement. Trading conditions climbed from 13 to 16, while profitability rose from 4 to 7. Employment conditions were unchanged at 4, suggesting hiring demand remains steady rather than accelerating. Capacity utilisation eased slightly to 83.2%, down from its recent peak but still well above its long-run average.

Cost pressures also edged higher, with purchase costs rising from 1.3% to 1.4% in quarterly equivalent terms, labour costs from 1.5% to 1.8%, and product prices from 0.6% to 0.9%, even as retail price growth slowed to 0.4% from 0.8% in November.

Overall, the survey suggests the economy ended the year on a firm footing, with most indicators sitting modestly above late-Q3 levels. Meanwhile, NAB noted that for the RBA, the small pullback in capacity utilisation is unlikely to materially ease concerns that the economy remains close to capacity.

AUD/CAD rises to 0.95, waits on Ausssie CPI verdict for next surge

Aussie has steadied after last week’s strong advance, entering consolidation as markets brace for Q4 inflation data that could prove pivotal for RBA's policy in the near term. With expectations firmly skewed toward a firm print, traders appear to wait for confirmation before extending long positions.

Consensus forecasts point to a renewed pickup in inflation. Headline CPI is expected to rise to 3.6%, while trimmed mean CPI is forecast at 3.2%, pushing both measures further above the RBA’s target band. The upcoming release is likely to reinforce concerns that inflation pressures remain sticky. That would make it harder for the RBA to justify an extended pause, particularly with labor market conditions showing renewed strength.

Market opinion remains divided on timing. Some see scope for a 25bp hike as early as next week, while others argue the RBA may prefer to wait another quarter to avoid premature action. Ultimately, the decision will hinge on the size and composition of the inflation print, alongside the bank’s assessment of broader economic conditions.

Technically, AUD/CAD edged higher this week and remains on upward acceleration mode as seen in D MACD. With current momentum, AUD/CAD should be on track to 161.8% projection of 0.l8902 to 0.9225 from 0.9055 at 0.9578, or even further to 200% projection at 0.9701. Outlook wil stay bullish as long as 0.9344 resistance turned support holds, in case of retreat.

In the bigger picture, last week's strong break of 0.9375 key resistance (2024 high) should confirm that whole down trend from 0.9991 (2020 high) has completed as a correction to 0.8440 (2025 low). There is prospect for the current up trend to extend in the medium term to have a test on 0.9991 at least.

How far and how fast AUD/CAD extends will ultimately depend two factors: The pace and extent of RBA tightening; and the depth of deterioration in Canada–US trade relations.

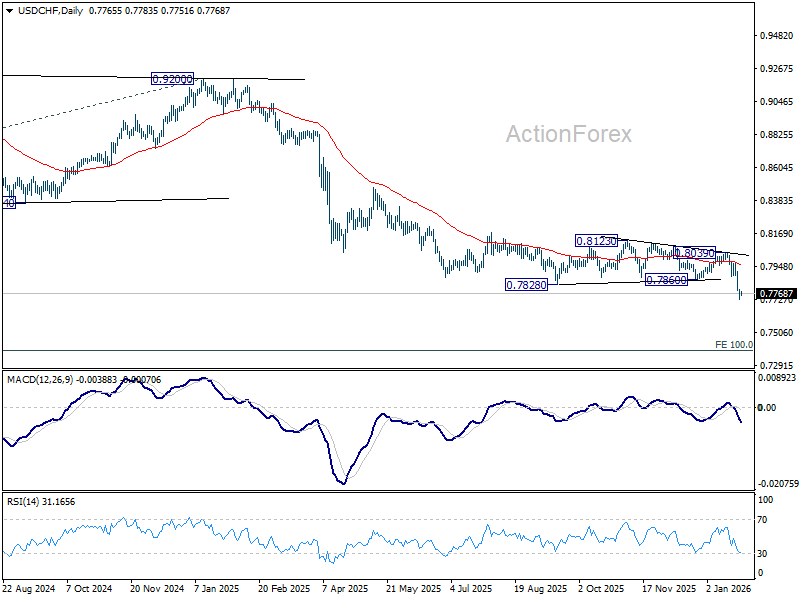

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7736; (P) 0.7765; (R1) 0.7799; More….

Intraday bias in USD/CHF is turned neutral with 4H MACD crossed above signal line, and some consolidations would be seen. But upside of recovery should be limited by 0.7860 support turned resistance. On the downside, break of 0.7729 will resume larger down trend to 0.7382 projection level.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7736; (P) 0.7765; (R1) 0.7799; More….

Intraday bias in USD/CHF is turned neutral with 4H MACD crossed above signal line, and some consolidations would be seen. But upside of recovery should be limited by 0.7860 support turned resistance. On the downside, break of 0.7729 will resume larger down trend to 0.7382 projection level.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.