Sample Category Title

Technical Levels for Major FX Pairs Ahead of FOMC Rate Decision

The January FOMC is one session away, and similarly to the September Meeting, Forex Market action is quite volatile ahead of the event.

Traders are still reflecting on the many themes ongoing in Markets, including Trump Administration chaos, generational runs in Metals, Q4 Earnings, Iran, and global trade deals that are getting all over the place.

This week began on a significant gap down in the US Dollar, with the past week's steep selling flows extending to test a significant 2025 Support (on the Dollar Index).

Dollar Index (DXY) 4H Chart, January 27, 2026 – Source: TradingView

Over the past week, post-Greenland threat selling flows have gathered such traction ahead of the FOMC that no mean reversion can take place.

Look for reactions around the 97.00 level after the meeting: a close above should signal further upside, and vice versa.

Some factors influencing the Dollar include the anticipated announcement of the next Fed Chair. In the meantime, there aren't many reasons except for Dollar bulls to push their bids ahead of the meeting (14:00 E.T. tomorrow).

Other FX currencies are also doing their own thing, with picture-changing releases for Antipodean currencies, the Swissie reaching its second-highest level ever against the USD, FX intervention fears in Japan, and more.

We will dive into an intraday chart outlook for all Major FX Currency pairs and provide trading levels for the upcoming huge FOMC event.

All FX Majors Charts with the key levels in play for the September FOMC

NZD/USD 4H Chart and technical levels – Holding a Tight Bull Channel

NZD/USD 4H Chart, January 27, 2026, Source: TradingView

FOMC Trading Levels for NZD/USD:

Resistance Levels

- September 2025 Resistance – Imminent test 0.60 to 0.60150

- July 2025 Resistance 0.6060 to 0.6070

- 2025 High Resistance 0.6120

Support Levels

- 0.5950 (+/- 70 pips) Key Momentum Pivot

- 0.59 (+/- 50 pips) Mini-Support

- 0.5850 December High Support

- Main Support 0.5720 to 0.5750

USD/JPY 4H Chart and technical levels – Testing key support

USD/JPY 4H Chart, January 27, 2026, Source: TradingView

The 4H 50-period MA is about to cross the 200 MA from above, a bearish sign but USD/JPY moves on Intervention fears – Be careful there!

FOMC Trading Levels for USD/JPY:

Resistance Levels

- 154.00 Momentum Pivot

- 155.00 Major Resistance, higher timeframe pivot

- 156.00 Key Resistance

- Mini-resistance 157.00 to 157.30

Support Levels

- Imminent Support from 152.80 to 153.00

- Key Momentum Support 151.50 to 152.00

- July 150.00 to 150.90 Main support

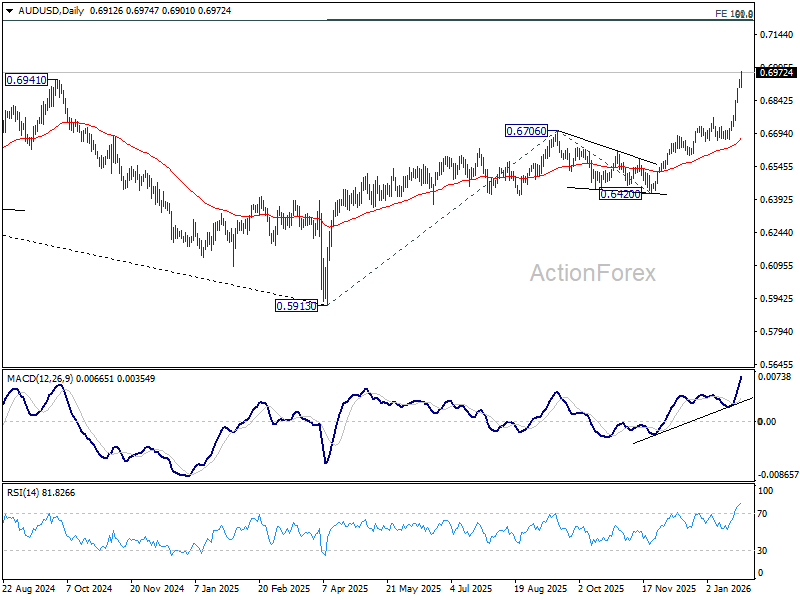

AUD/USD 4H Chart and technical levels – Breaking September 2024 highs

AUD/USD 4H Chart, January 27, 2026, Source: TradingView

The breakout is a huge one – Keep a close eye on the 4H 20-period MA which tracks the buying momentum well: Closing below would hint at a reversal (not looking close for now)

FOMC Trading Levels for AUD/USD:

Resistance levels

- Daily highs 0.69740

- Dec 2021 Lows 0.70 to 0.7050 Major Resistance

- 2023 Highs and 0.71 Resistance

Support levels

- 0.69 to 0.6945 Main 2024 Pivot

- 4H MA 20 0.68930

- Micro-support 0.6850 (+/- 30 pips)

- October 2024 Minor support 0.6750 (+/- 100 pips)

- 0.66 to 0.6630 December Support

EUR/USD 4H Chart and trading levels – Breaking 2025 highs

EUR/USD 4H Chart, January 27, 2026, Source: TradingView

EUR/USD is breaking out higher but watch the reactions to the 200-Month Moving Average (at 1.19510) which will act as a key Indicator for future action.

FOMC Levels to watch for EURUSD:

Resistance Levels:

- 200-Month Moving Average 1.19512

- Sep 2021 Highs – Resistance 1.19 to 1.1950 Zone (testing)

- 1.20 psychological level and 2021 highs

Support Levels:

- Main Pivot 1.18 to 1.1840 and Channel lows

- 1.1750 Intermediate Support (+/- 150 pips)

- 1.1640 to 1.1660 Intermediate Support

- 1.1580 to 1.16 January Bounce Support

USD/CHF 4H Chart and technical levels – Reaching 2nd lowest levels ever

USD/CHF 4H Chart, January 27, 2026, Source: TradingView

Watch out for the consequent divergence showing up on the shorter timeframes – Reactions after the FOMC could be very swift.

Breaking current lows could lead to a test of the 0.76 Psychological level

FOMC Levels to watch for USD/CHF:

Resistance Levels

- 0.7950 Key pivot

- Long-term pivot 0.80 Zone (0.80 to 0.8010)

- Main resistance 0.8150 to 0.82 (last highs 0.8165)

- May 2025 highs 0.8475 Resistance Zone

Support Levels

- Session lows support 0.7670

- 0.7660 Session lows

- 0.76 Psychological level

- 0.70696 All-Time Lows

GBP/USD 4H Chart and trading levels – Reaching 2025 highs

GBP/USD 4H Chart, January 27, 2026, Source: TradingView

FOMC Levels to watch for GBPUSD:

Resistance Levels

- 2025 Highs 1.37840

- 2025 Highs resistance 1.3760 to 1.38

- 1.3850 to 1.39 2021 Resistance

Support Levels

- Resistance turned pivot at the 1.36 zone

- December Resistance turned Support 1.35680 to 1.36

- Key Support 1.3450 to 1.34650

USD/CAD 4H Chart and trading levels – Reaching 2025 highs

USD/CAD 4H Chart, January 27, 2026, Source: TradingView

Levels to watch for USD/CAD:

Resistance Levels

- 1.3650 to 1.3770 December Pivot

- 1.3750 Pivotal Resistance

- 1.38 Handle Resistance +/- 150 pips

Support Levels

- Session lows 1.35960

- 1.3565 2025 lows

- 1.3550 to 1.3570 Main 2025 Support

- 1.34 Next Main Support

Safe Trades as the FOMC approaches!

How Long Can Fed Sill Defend Independence?

- The Fed is facing increasing political pressure, and a pause in rate cuts has become a tool to defend its institutional independence.

- The labour market remains stable but fragile, supporting a cautious Fed stance despite inflation staying above target.

- Futures markets do not expect further rate cuts in the coming months, with meaningful easing priced in only from mid year.

- The risk of a loss of confidence in the US dollar is rising, potentially leading to a self reinforcing depreciation if the Fed’s credibility is undermined.

The US policy interest rate and core inflation measures in the United States (CPI and PCE year on year), source: Bloomberg

Rising political pressure on the Fed

The Federal Reserve is currently operating in an increasingly tense political environment. Pressure from the administration for further and substantial interest rate cuts has continued to build, turning monetary policy into a political battleground. This conflict recently intensified with legal action being taken against Fed Chair Jerome Powell, widely interpreted as an attempt to exert direct pressure on the central bank’s leadership. Powell’s unusually firm and public response suggests that the Fed is not prepared to yield easily. In this context, a pause in rate cuts can serve not only as a policy decision but also as a visible signal of institutional independence.

Maintaining unity among policymakers will be essential in this phase. That task may prove difficult, given the expected dissenting vote from Governor Miran, who has consistently argued for aggressive rate cuts, and increasingly open signals from Governor Bowman in favour of lower interest rates.

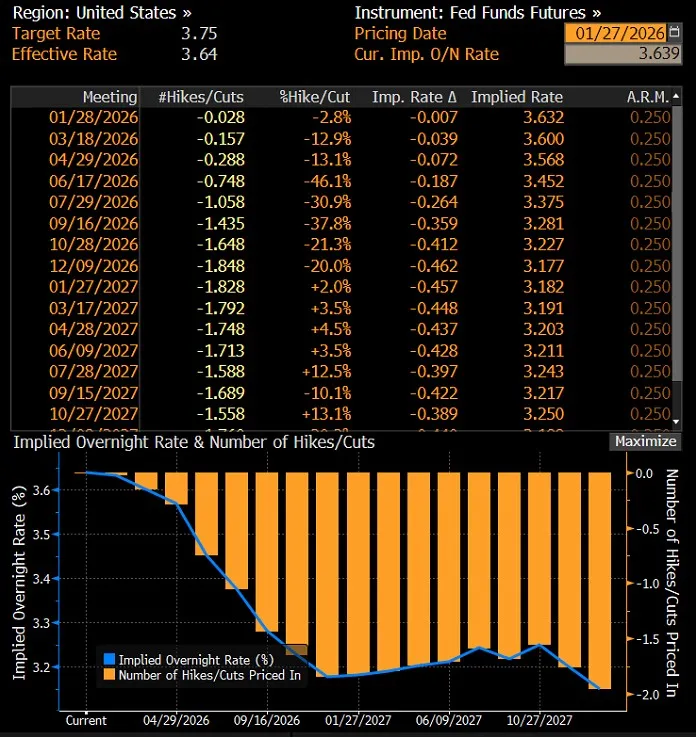

No rate cut at the upcoming meeting

Against this backdrop, the upcoming meeting of the Federal Reserve is very likely to end with interest rates left unchanged. The Fed has for some time signalled its readiness to pause after three consecutive rate cuts implemented in January. This would leave the target range for the federal funds rate at 3.50 to 3.75 per cent. Since the beginning of 2024, rates have been reduced by a total of 175 basis points.

According to Powell and many other policymakers, interest rates are now relatively close to a neutral level. This assessment supports a wait and see approach, allowing the Fed to rely more heavily on incoming data before committing to further policy adjustments.

Fed policy expectations priced in by the futures market

The federal funds futures market is also aligned in its assessment of the likelihood of changes to monetary policy parameters at tomorrow’s Fed meeting. Market pricing clearly indicates that the probability of another rate cut in January is very low. The chances of such a move in March and April are also limited. It is only in June that the market begins to see meaningful odds of a further easing of monetary conditions.

Market pricing of the future path of US interest rates, source: Bloomberg

Labour market in the spotlight

The labour market has become a central focus of the Fed’s assessment. Despite solid economic growth last year, employment momentum has clearly weakened. Layoffs in federal agencies have added to this slowdown. At the same time, while private companies have largely avoided large scale redundancies, they have also shown little appetite for new hiring.

This combination has kept the labour market broadly stable, but the balance remains fragile. In the event of an economic slowdown, conditions could deteriorate quickly. Seen from this perspective, the recent rate cuts, despite inflation remaining above the 2 per cent target, can be interpreted as insurance against a sharper downturn rather than a response to immediate weakness.

Recent data offer temporary relief

So far, recent labour market data have not confirmed fears of further deterioration. In both November and December, more than 50,000 new jobs were created each month, which was sufficient to prevent an increase in the unemployment rate. This gives the Fed time to assess whether this trend continues at the start of the new year.

In parallel, more up to date inflation data will become available in the coming months. This includes the release of the PCE deflator, the Fed’s preferred inflation measure, whose publication had been delayed due to last year’s government shutdown. These data will be crucial in shaping expectations for the next phase of monetary policy.

When markets stop believing: the rising risk of a self-reinforcing dollar sell off

The current situation in the foreign exchange market clearly highlights a risk that was repeatedly flagged already last year. This risk appears to be particularly underestimated by proponents of the so called “TACO” (Trump Always Chickens Out) strategy, which is based on the belief that President Trump ultimately always backs away from his most confrontational decisions. The problem, however, is that given the unpredictable and often chaotic nature of policy making under the current US administration, there is a genuine danger that markets cross a threshold beyond which a loss of confidence becomes difficult to reverse.

From an investor’s perspective, this implies the risk of entering a phase in which even later attempts to soften the political stance will no longer be sufficient to halt negative market dynamics. In other words, markets may stop responding to deescalatory gestures if they are perceived as too late or lacking credibility.

Among the potential “critical points” long discussed are the risk of the US dollar losing its safe-haven status and a perceived erosion of the Federal Reserve’s independence in the eyes of market participants. If investors begin to seriously price in a scenario in which these pillars are permanently weakened, dollar depreciation could take on a self reinforcing character. In such an environment, even a retreat from the most controversial policy actions may fail to restore stability, resulting in a deeper and more persistent weakening of the US currency.

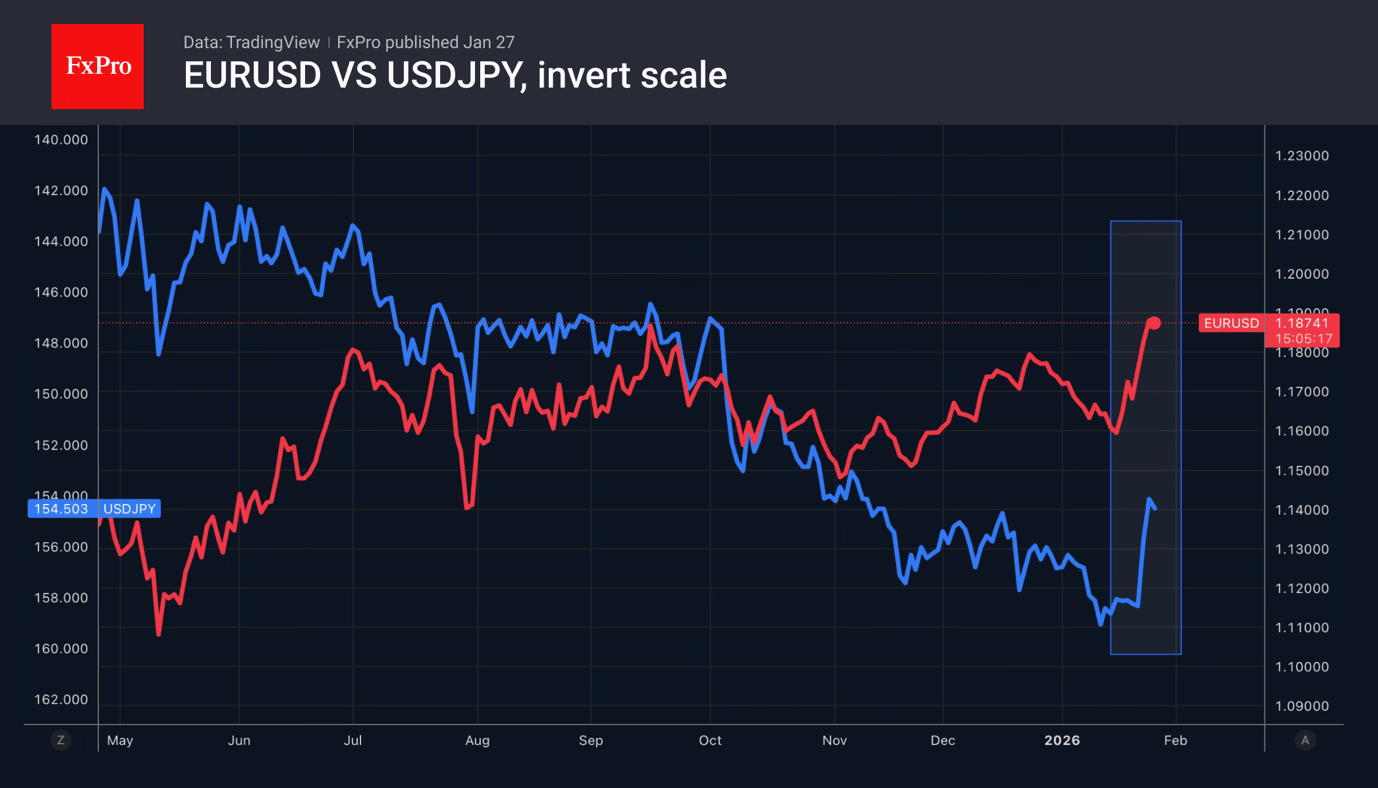

Recent market developments suggest that this scenario is becoming increasingly plausible. President Trump has indeed attempted to deescalate tensions related to Greenland by stepping back from tariff threats against parts of the European Union, which provided the dollar with only a brief period of relief. At present, downward pressure on the USD has intensified again, underscoring that ad hoc measures are insufficient to rebuild damaged investor confidence. A break above 1.19 in EUR/USD now appears highly likely.

EUR/USD has moved back into its medium-term upward channel. The declines seen in late December 2025 and early January proved to be only a temporary episode that briefly altered the direction of price action. For now, the uptrend in the main currency pair appears to remain intact.

EUR/USD exchange rate chart, daily data, source: TradingView

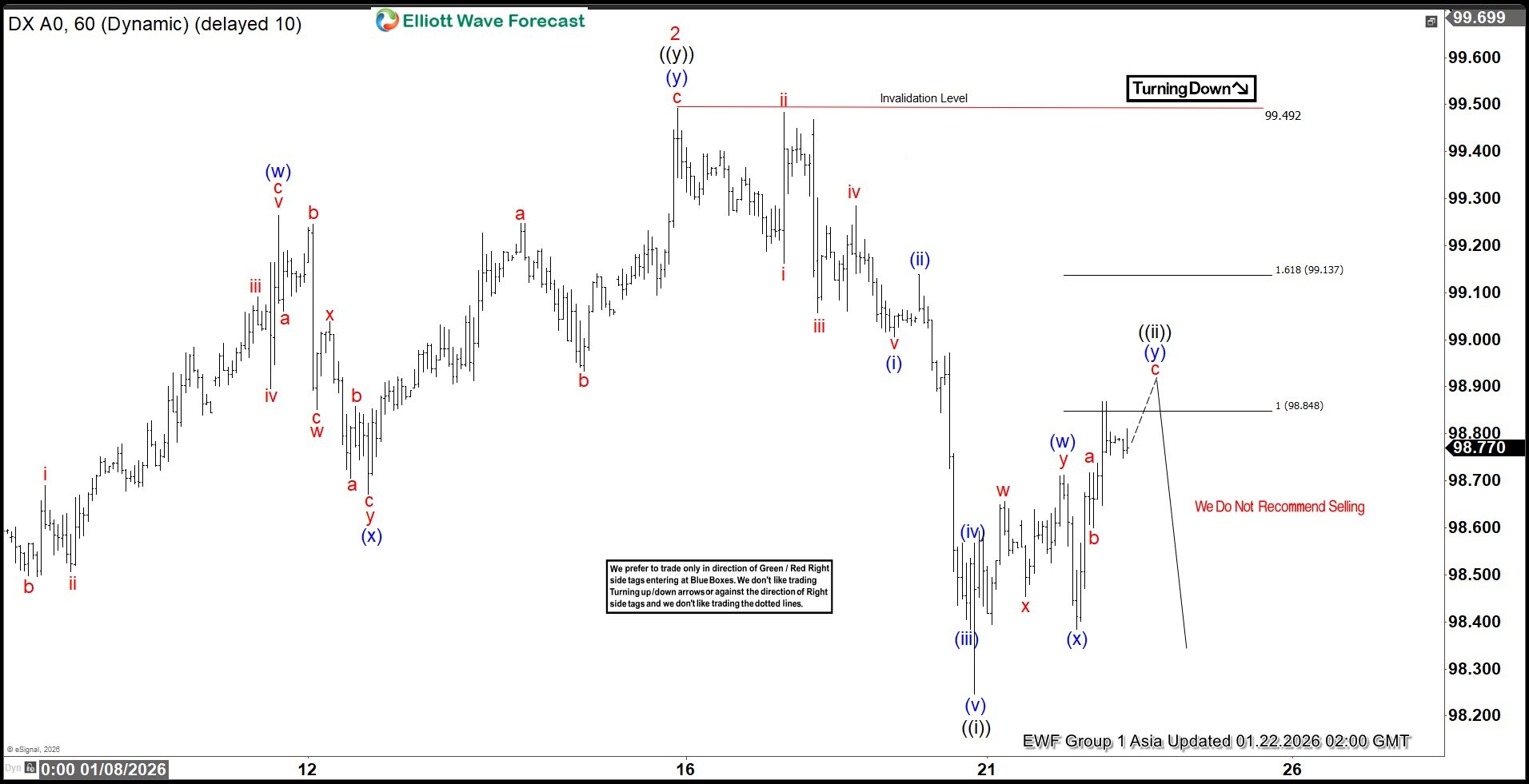

DXY Faces Persistent Selling at Extreme Equal Legs Zone

In this technical blog, we will look at the past performance of the 1-hour Elliott Wave Charts of DXY. We presented to members at the elliottwave-forecast. In which, the decline from 21 November 2025 high unfolded as an impulse structure. And showed a lower low favored more downside extension to take place. Therefore, we advised members not to buy the US dollar & sell the bounces in 3, 7, or 11 swings. Based on Elliott wave hedging area looking to get 3 wave reaction lower at least. We will explain the structure & forecast below:

DXY 1-Hour Elliott Wave Chart From 1.22.2026

Here’s the 1-hour Elliott wave chart from the 1.22.2026 Asia update. In which, the decline to $98.24 low ended in wave ((i)) as an impulse structure. Up from there, the US dollar made a bounce higher in wave ((ii)) to correct that cycle. The internals of that pullback unfolded as Elliott wave double three structure & managed to reach the extreme equal legs area at $98.84- $99.13. From there, market makers agrees for the minimum reaction lower to take place.

DXY 1-Hour Elliott Wave Chart From 1.26.2026

This is the 1-hour Elliott wave Chart from 1.26.2026 NY update. In which the DXY is showing a strong reaction lower taking place, right after ending the correction within the equal legs area. Allowed members to create a risk-free position shortly after taking the short position. Since then, the index has already made a new low below September 2025 low confirming the next leg lower.

Four Problems of US Dollar

- The EURUSD rally has solid foundations.

- Gold is insurance against Trump’s policies.

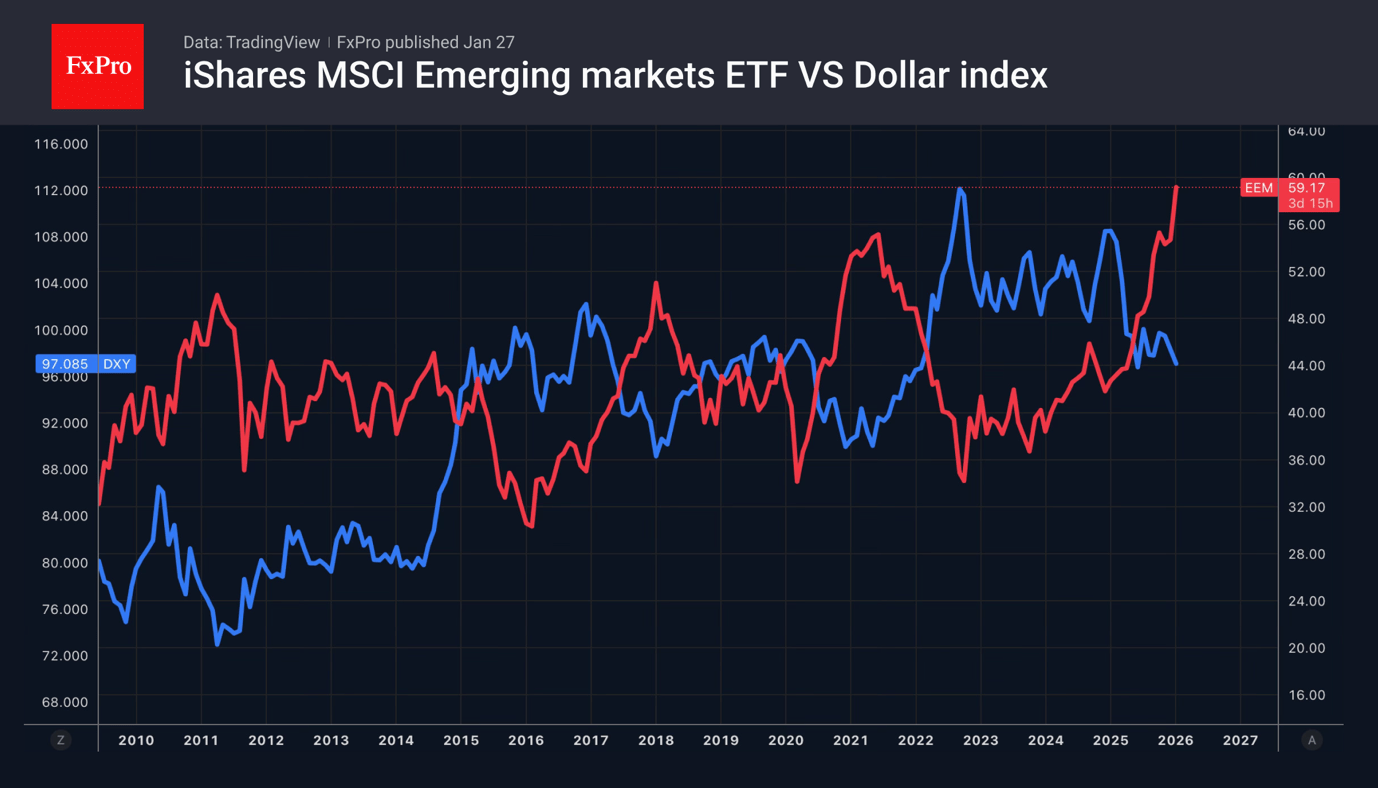

The dollar index returned to last year’s lower bound, which we had not seen since 2022. The drivers are investment portfolio diversification, concerns about the US economic growth slowdown, rumours of FX interventions and active selling by carry-traders. With the weakening of the dollar and the interest rate differential across the eight most liquid emerging-market currencies, this strategy yielded 18% last year. The best result since 2009.

Since the beginning of the year, the strategy has already yielded 1.3%. According to Morgan Stanley, Bank of America and Citigroup, the carry trade will continue to work effectively in 2026. They advise choosing currencies of countries with tight monetary policy, high interest rates and trustworthy central banks.

The US dollar is under pressure from the rotation of investment portfolios away from American assets. By the end of the week on January 21st, capital outflows from ETFs focused on these assets amounted to $17 billion. There are inflows into Europe and Japan, but they are not comparable to those into emerging markets. Specialised exchange-traded funds working with these assets have attracted $134 billion since the beginning of January, which is the best start since 2012.

Rumours of another government shutdown are contributing to the decline in the USD index. Polymarket estimates the chances of such an outcome at 78%. This has risen significantly following the public and Democrats’ reaction to the incidents in Minneapolis, which has intensified criticism of Donald Trump’s anti-immigration policy. A shutdown could slow US GDP growth and lead to a faster-than-expected return to monetary easing by the Fed.

Rumours that the US and Japan will conduct coordinated currency intervention to weaken the greenback and strengthen the yen are adding fuel to the EURUSD rally. Recently, Finance Minister Scott Bessent said that there is no connection between the exchange rate and the “strong dollar policy”. The White House is keen to weaken the US currency to boost the competitiveness of companies.

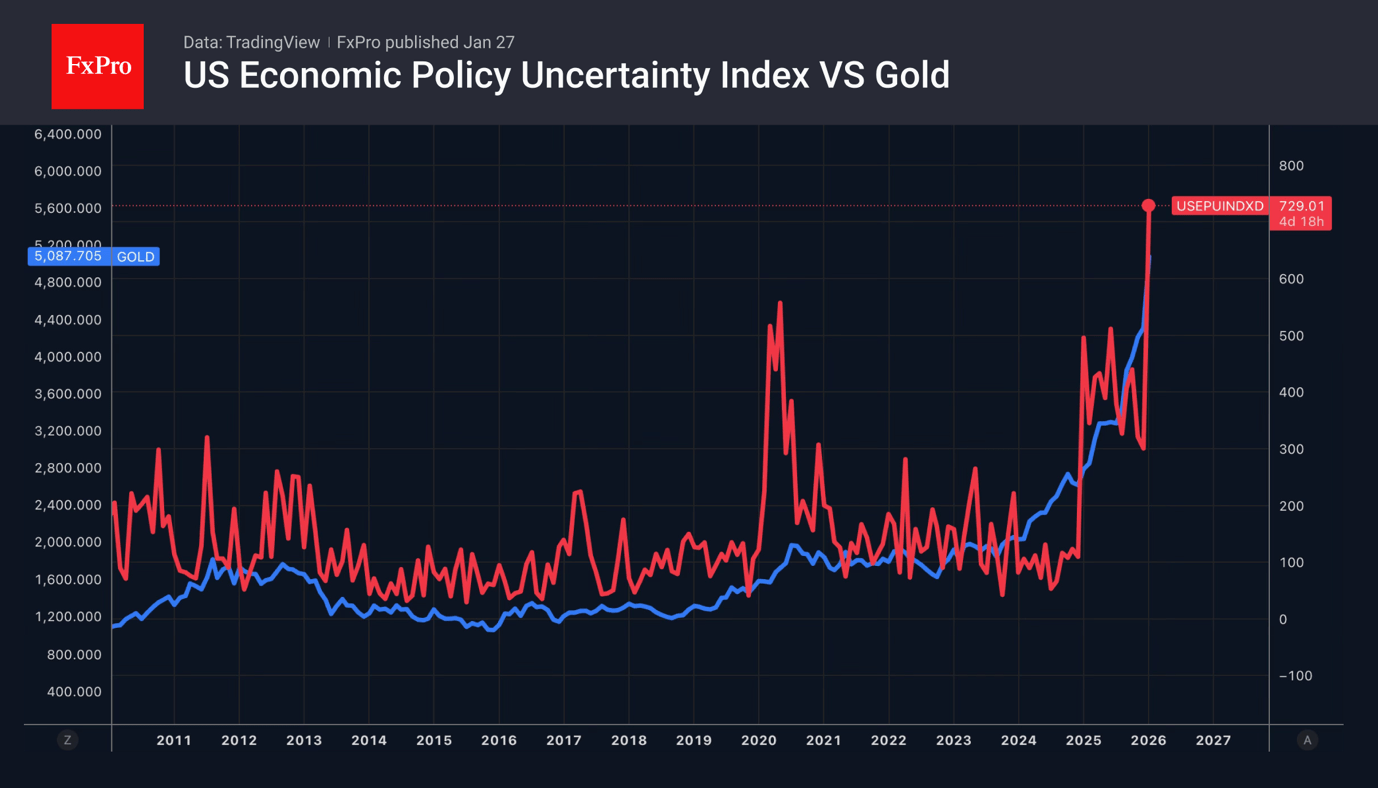

In this environment, it should come as no surprise that gold has soared to historic highs. There is growing talk in the market that the precious metal has turned from a hedge against inflation into insurance against Donald Trump’s policies.

USD/JPY Extends Steep Descend into Third Straight Day and Breaks Key Support

USDJPY remains in a steep fall for the third consecutive day (down almost 4%) with speculations that intervention may be behind the move, along with increased safe-haven demand and month-end flows.

Fresh extension lower on Tuesday broke through significant supports at 153.62 (the base of thick ascending daily Ichimoku cloud / 100 DMA) and cracked Fibo 50% retracement of 146.58/159.45 upleg (153.01).

Daily technical studies show strong negative momentum and MAs above the price and turning south that supports current action.

Broken cloud base/100 DMA reverted to significant resistance which should ideally cap and keep fresh bears in play for firm break of 153.01 that would expose targets at 151.50 (Fibo 61.8%) and 150.20/00 (bull-trendline / psychological) in extension.

Res: 153.62; 154.00; 154.53; 155.61.

Sup: 152.15; 151.50; 150.20; 150.00.

EUR/USD: Bulls Approach 1.2000 Barrier

The Euro keeps firm tone and holds near fresh multi-month high (1.1907, posted on Monday) following last week’s strong rally and gap-higher opening at the start of this week.

Weak dollar with signals of possible deeper drop, was mainly behind the latest advance.

Friday’s close above broken Fibo 76.4% of 1.1918/1.1468 (1.1812) confirmed firm bullish stance.

Monday’s action, despite opening with gap-higher, showed signs of hesitation on approach to key barrier at 1.1918 (2025 peak, the highest since June 2021), due to significance of resistance, as well as overbought daily studies, but fresh strength on Tuesday sidelined concerns about potential pause, on push through 1.1918 pivot.

Daily close above this level is needed to confirm signal and fully expose next strong barriers at 1.1950 (200MMA); 1.1984 (bear-trendline connecting peaks of 2018 and 2021) and 1.2000 (psychological).

Multiple daily MAs bull-crosses and very strong positive momentum, support scenario, but overbought conditions require caution.

Consolidative/corrective action should hold above 1.1850 (today’s low / broken upper boundary of bull-channel) to keep larger bulls in play.

Res: 1.1950; 1.1984; 1.2000; 1.2025.

Sup: 1.1900; 1.1850; 1.1812; 1.1760.

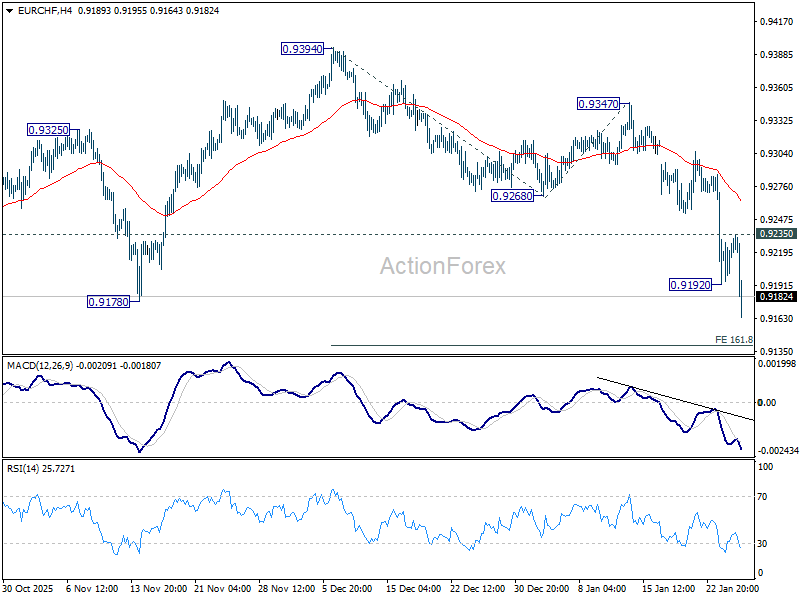

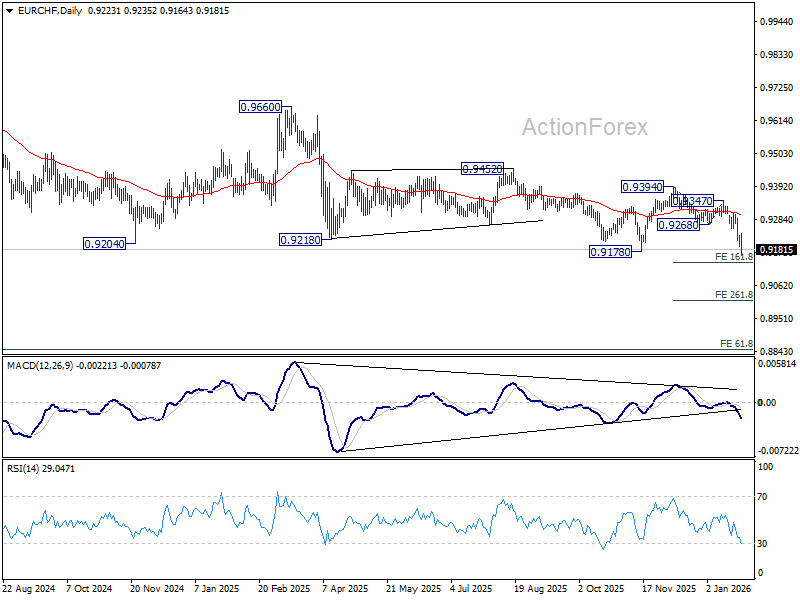

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9206; (P) 0.9219; (R1) 0.9244; More....

EUR/CHF's fall resumed after brief consolidations. Break of 0.9178 suggests larger down trend resumption too. Intraday bias is back on the downside for 161.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143. Firm break there will target 261.8% projection at 0.9017. On the upside, above 0.9235 minor resistance will turn intraday bias neutral again and bring consolidations first, before staging another fall.

In the bigger picture, another rejection by 55 W EMA (now at 0.9350) keeps outlook bearish. Downtrend from 1.2004 (2018 high) is still in progress. Firm break of 0.9178 will target 61.8% projection of 1.1149 to 0.9407 from 0.9928 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

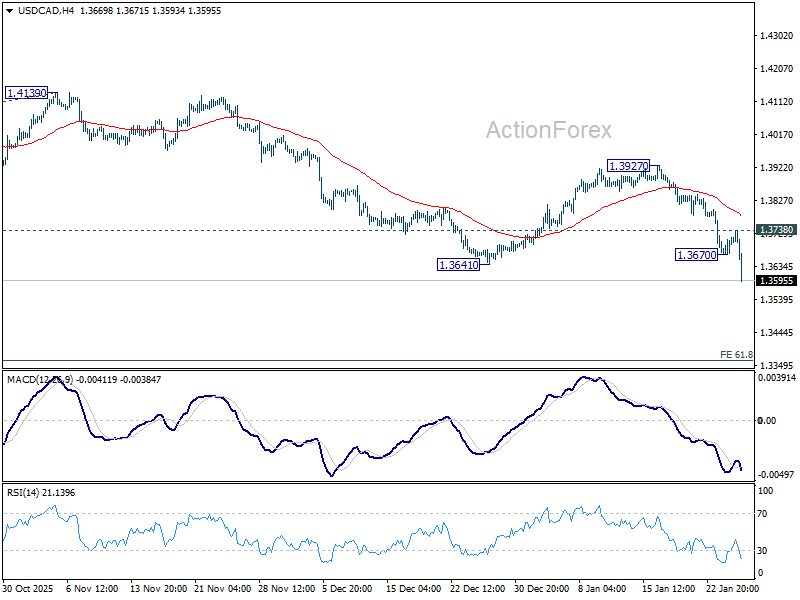

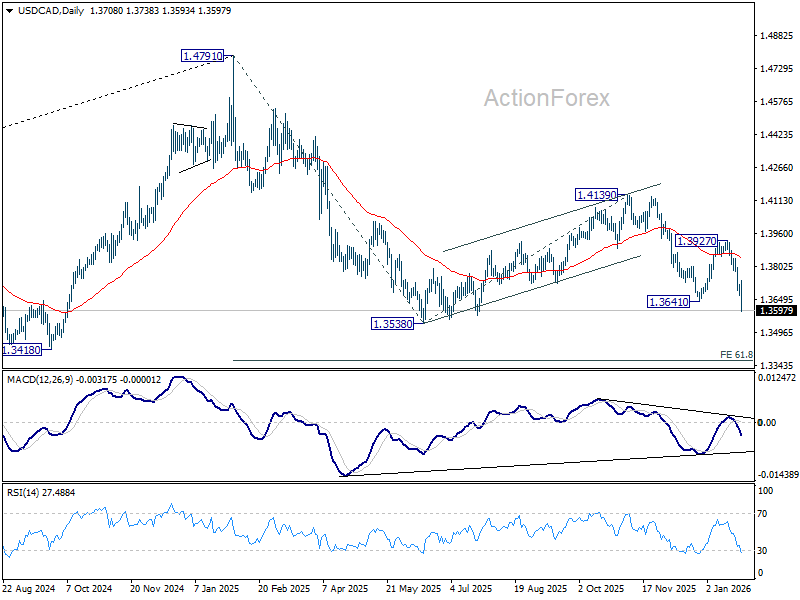

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3682; (P) 1.3701; (R1) 1.3730; More...

USD/CAD's fall resumed after brief consolidations and intraday bias is back on the downside for retesting 1.3538 low. Firm break there resume whole whole fall from 1.4971. Next target is 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. On the upside, above 1.3738 minor resistance will turn intraday bias neutral and bring consolidations, before staging another fall.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, and break of 1.3538 will target 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

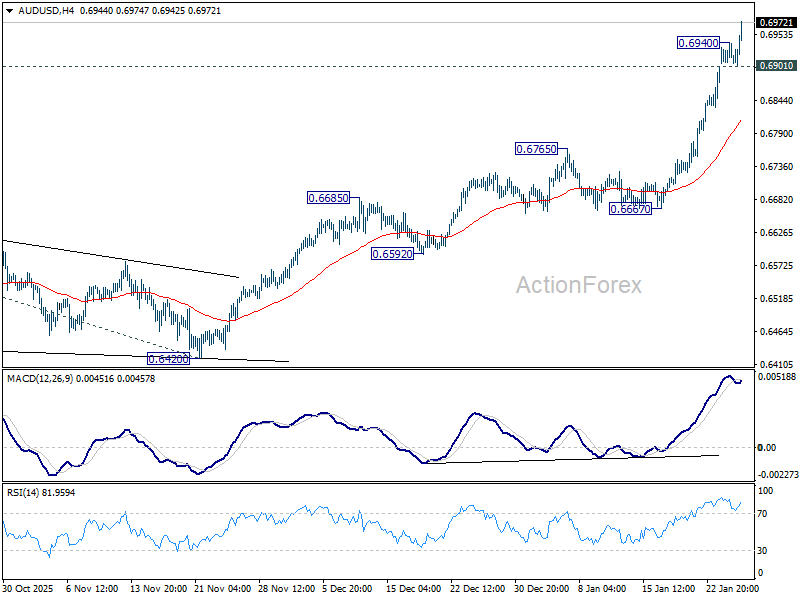

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6902; (P) 0.6922; (R1) 0.6937; More...

AUD/USD's rally resumed after brief consolidations and intraday bias is back on the upside. Current rally is part of the up trend form 0.5913 and should target 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 next. On the downside, below 0.6901 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

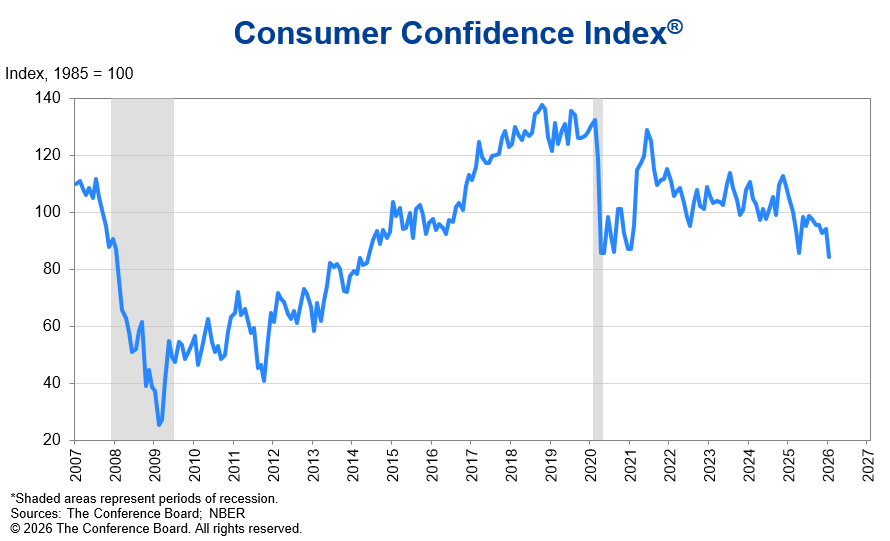

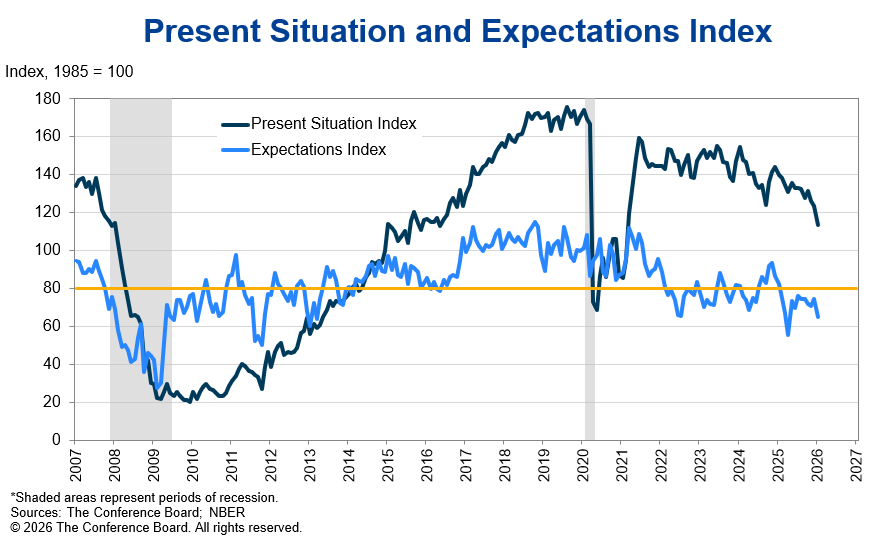

US Consumer confidence collapses to 94.5, worst since 2014

US consumer confidence suffered a sharp setback in January, with the Conference Board Consumer Confidence Index plunging -9.7 points to 94.5. The drop pushed confidence to its lowest level since 2014, falling even below levels seen during the pandemic, and marking one of the steepest monthly declines in recent years.

The deterioration was broad-based. Present Situation Index slid -9.9 points to 113.7, while the forward-looking Expectations Index fell -9.5 points to 65.1. The latter is particularly alarming, as readings below 80 have historically been associated with recessions ahead.

According to Dana M. Peterson, confidence “collapsed in January” as concerns about both current conditions and the outlook intensified. She noted that all five components of the index weakened, dragging the headline measure to its lowest level since May 2014.

Peterson added that consumer comments remained heavily skewed toward pessimism. Inflation pressures, especially food, fuel, and energy costs, dominated responses, while mentions of tariffs, trade, politics, and labor market concerns increased. References to health insurance and war also edged higher, reinforcing the picture of households growing more anxious on multiple fronts.