Sample Category Title

For the First Time In History, the Price of Silver Has Exceeded $115

The weakness of the US dollar amid the White House’s ambiguous policy stance, along with other factors (including geopolitics and industrial demand for silver), has led to the XAG/USD quote rising above $115 this week.

Since the beginning of the year, the price of an ounce of silver has increased by more than 50%, continuing the steep upward trend that began back in 2025.

It seems the bull market in precious metals is unstoppable, but the chart is sending important signals that cast doubt on this view.

Technical Analysis of the XAG/USD Chart

Price fluctuations are forming a broad ascending channel. Pay attention to the following:

→ A surge in volatility, clearly visible on the ATR indicator. It began to form after the psychological level of $100 was breached.

→ A sharp drop from A to B (approximately 12% within a single day) from the upper boundary of the channel to its median. Ordinary retail traders do not have the power to generate such an effect.

Given the above, it is reasonable to assume that after silver surpassed the psychological level of $100 per ounce, demand took on a frenzy-like character. Meanwhile, “smart money” is using the broad market to take profits on long positions after a staggering rise (more than +200% over the past six months). In other words, this points to a distribution phase in terms of Richard Wyckoff’s method.

If false bullish breakouts of resistance levels appear on the chart, followed by successful breaks of support, this will add weight to the argument behind the idea outlined above.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Just a Mild Crypto Winter

Market Overview

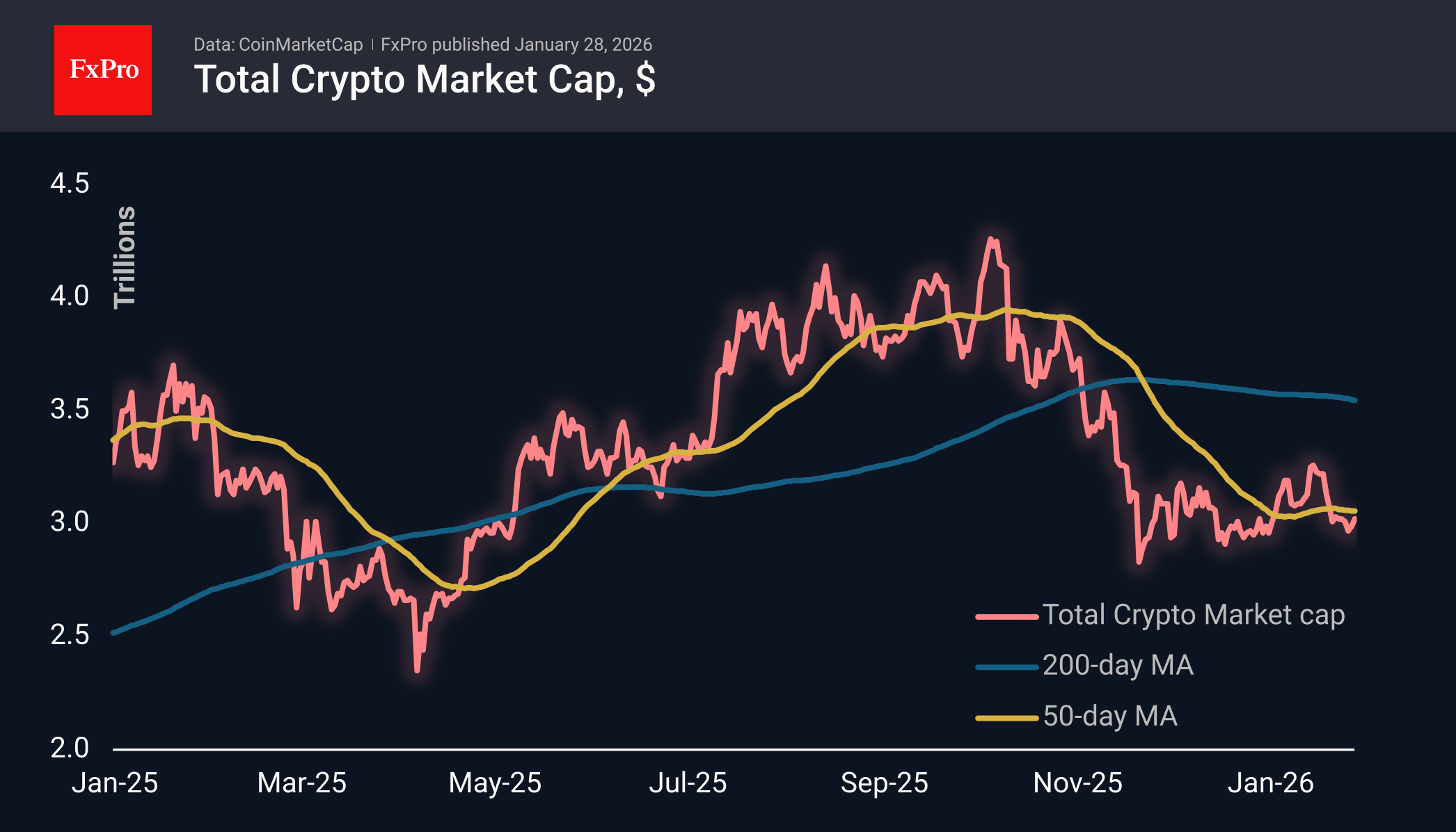

The crypto market capitalisation rose by another 1.1% over 24 hours to $3.02 trillion, mirroring the dollar’s weakening during this period. But this strengthening looks pale, as high-risk assets such as cryptocurrencies often move in much larger steps. For example, along with an 8% weakening of the dollar from April to June last year, Bitcoin rose by more than 50%. Without delving too deeply into history, it is easy to see that the 4% drop in the dollar index in less than two weeks was met with a 30% jump in silver and a 15% jump in gold. The US S&P 500 is also rewriting historical highs. Against this backdrop, even a slight increase in market capitalisation looks like a mild winter for cryptocurrencies, and a deeper decline is only a matter of time.

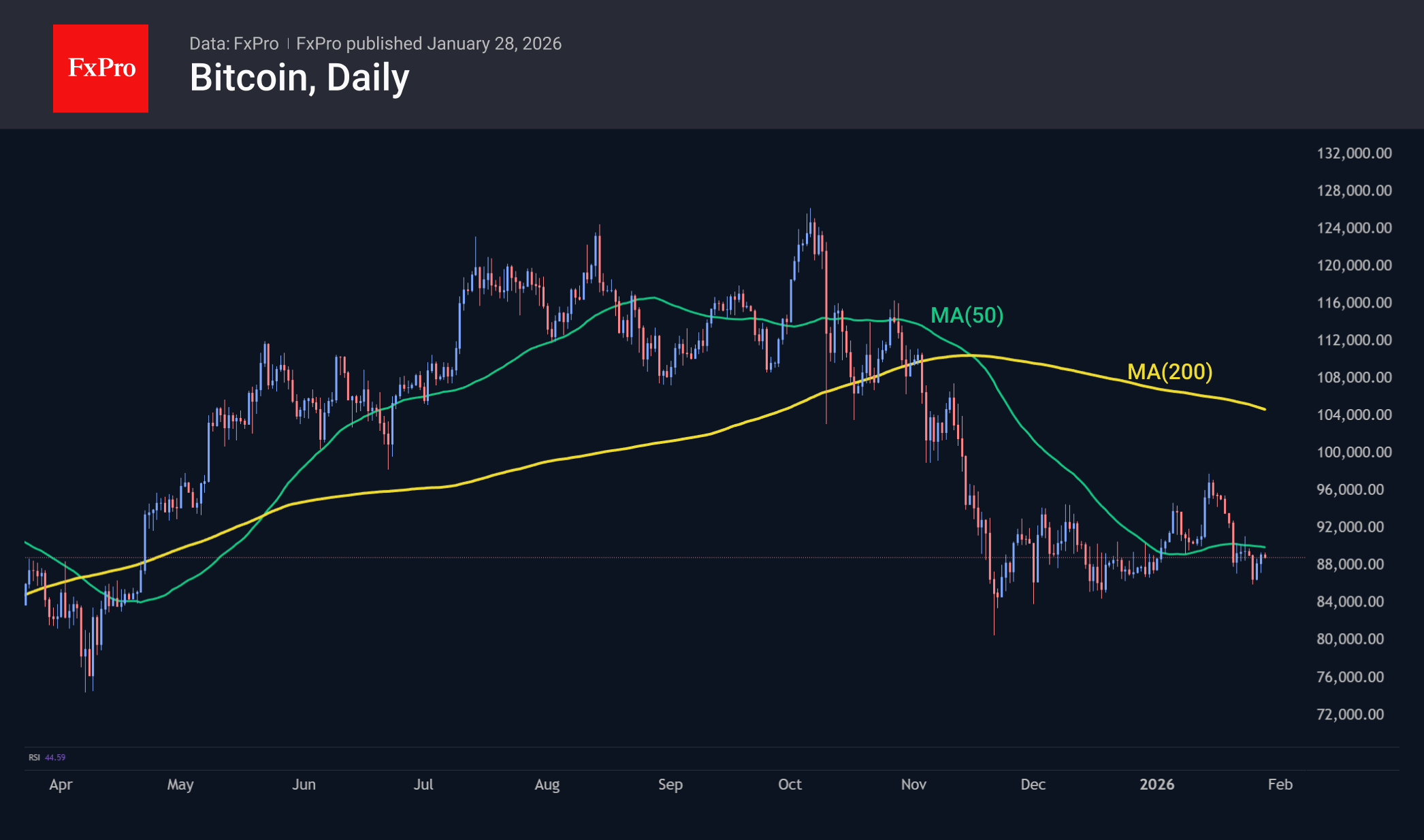

Bitcoin continues to attempt to consolidate above $89K. This resistance level, approaching a round number, is reinforced by the 50-day moving average. BTC’s position relative to this curve indicates a bearish market. Due to a relatively favourable external environment, it has managed to successfully defend support near $85K. Still, fluctuations about a third below the highs of the last two months are cause for pessimism. Neither institutional demand nor the president’s pro-cryptocurrency administration has helped to overcome the accumulated fatigue after the rally of the previous three years.

News Background

In these times of uncertainty and stress in the markets, investors are selling the first cryptocurrency en masse to get cash, turning Bitcoin into an ‘ATM,’ according to NYDIG. This is damaging Bitcoin’s reputation.

According to Santiment, against the backdrop of the gold rally, the capitalisation of stablecoins has fallen by $2.24 billion over the past 10 days. This indicates an outflow of capital from the cryptocurrency market into traditional safe-haven assets and may delay its recovery.

Strategy has reduced its Bitcoin purchases by almost eight times in a week. The company purchased 2,932 BTC ($264.1 million) between 19 and 25 January at an average price of $90,061 per coin. Strategy now owns 712,647 BTC, purchased for $54.2 billion at an average price of $76,037 per Bitcoin.

Japanese company Metaplanet incurred an unrealised loss of $680 million in 2025 due to the depreciation of its Bitcoin reserve. According to BitcoinTreasuries, the ‘Asian Strategy’ owns 35,102 BTC worth $3.1 billion.

Bitmine, the largest corporate holder of Ethereum, reported that it has accumulated 4,243,338 ETH worth more than $12 billion. This represents 3.52% of the total ETH supply, with a target of 5%.

Tether has launched a separate stablecoin for the US market. USAT was created in accordance with last year’s Genius Act, which sets rules for stablecoins and is the first significant piece of legislation for the crypto industry in the country.

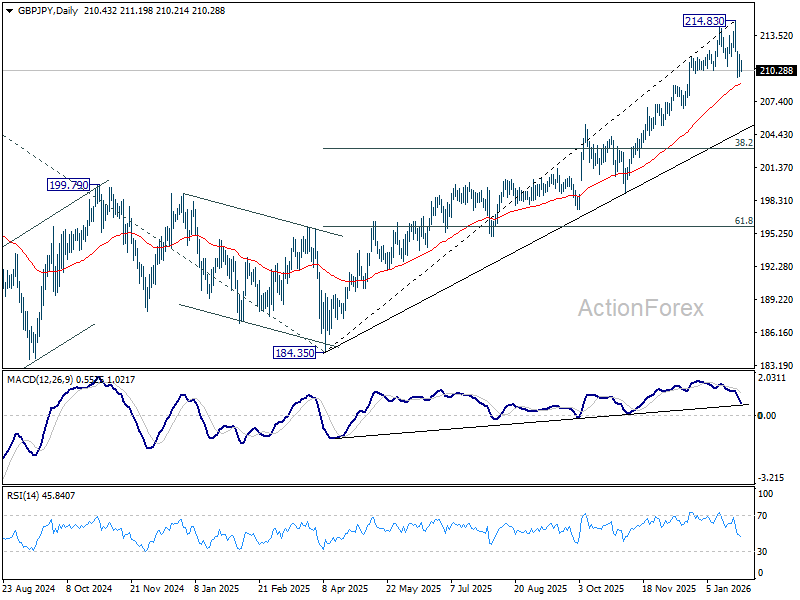

GBP/JPY Daily Outlook

Daily Pivots: (S1) 209.80; (P) 210.78; (R1) 211.76; More...

Intraday bias in GBP/JPY is turned neutral for consolidations above 209.61 temporary low. Risk will stay on the downside as long as 214.83 holds, even in case of strong recovery. Below 209.61, and sustained break of 55 D EMA (now at 209.00) will argue that it's correcting whole rise from 184.35 and target 38.2% retracement of 184.35 to 214.83 at 203.18.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, break of 205.30 resistance turned support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.

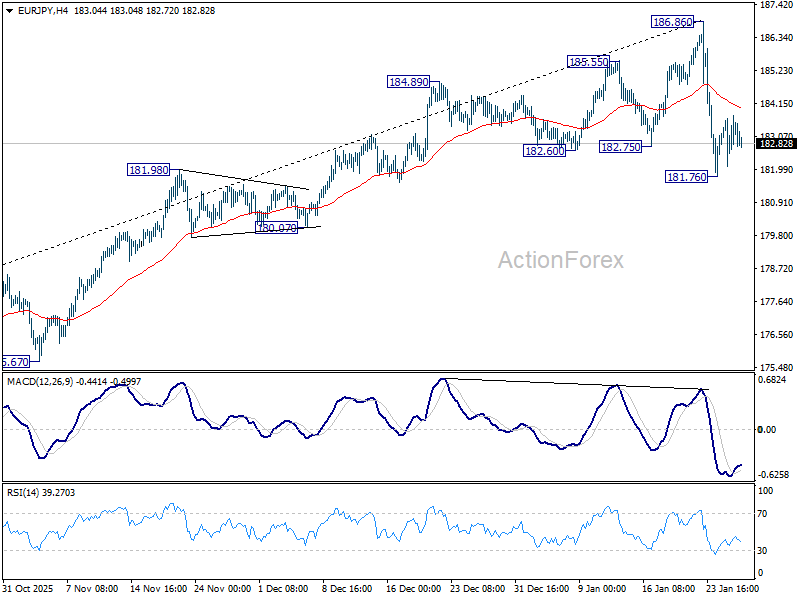

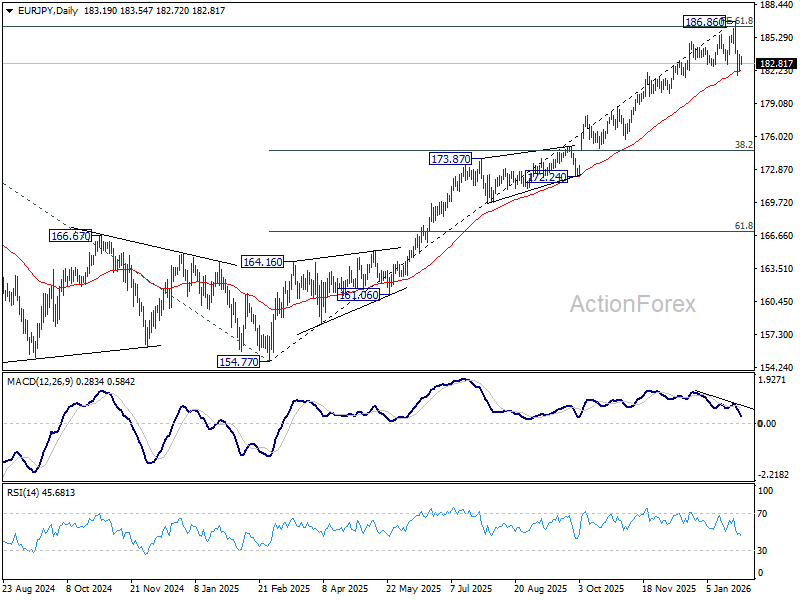

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.33; (P) 183.06; (R1) 184.01; More...

Intraday bias in EUR/JPY is turned neutral for consolidations above 181.76 temporary low. But risk will stay on the downside as long as 186.86 holds, in case of strong recovery. Break of 181.76 and sustained trading below 55 D EMA (now at 182.14) should solidify the case that fall from 186.86 medium term top is correcting whole rise from 154.77. Deeper decline should then be seen to 38.2% retracement of 154.77 to 186.86 at 174.60.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and and met 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 173.32) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 78.6% projection at 194.88 next.

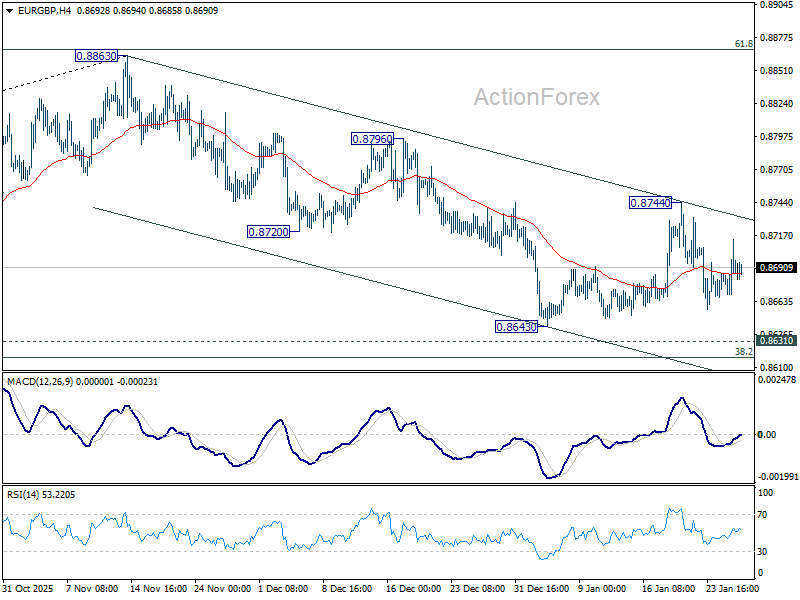

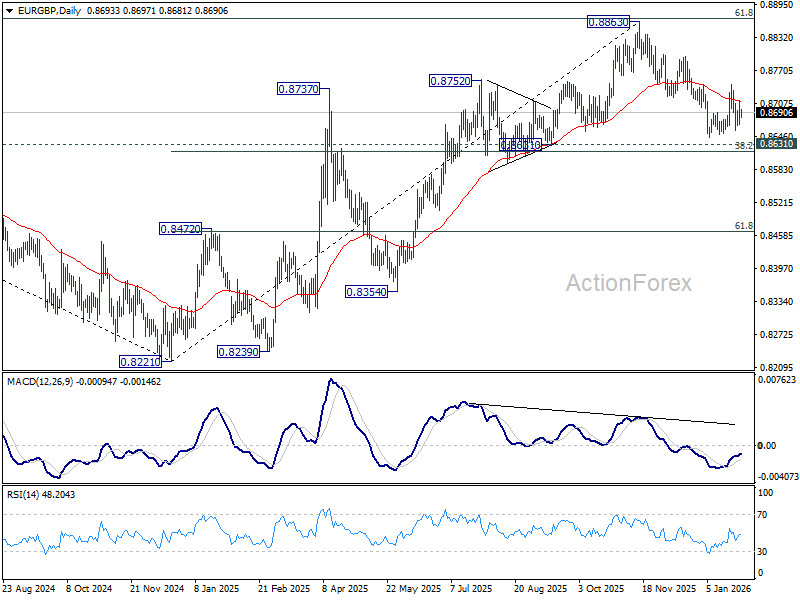

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8671; (P) 0.8693; (R1) 0.8717; More…

Intraday bias in EUR/GBP stays neutral as range trading continues. But risk will remain on the downside as long as 0.8744 resistance holds. Further decline is expected to 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618). Decisive break there will carry larger bearish implications and pave the way to 61.8% retracement at 0.8466.

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8625) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

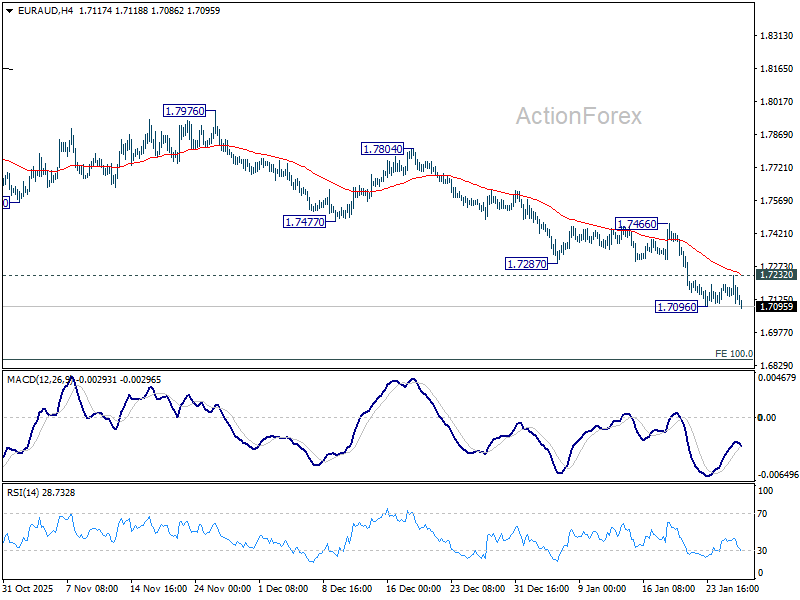

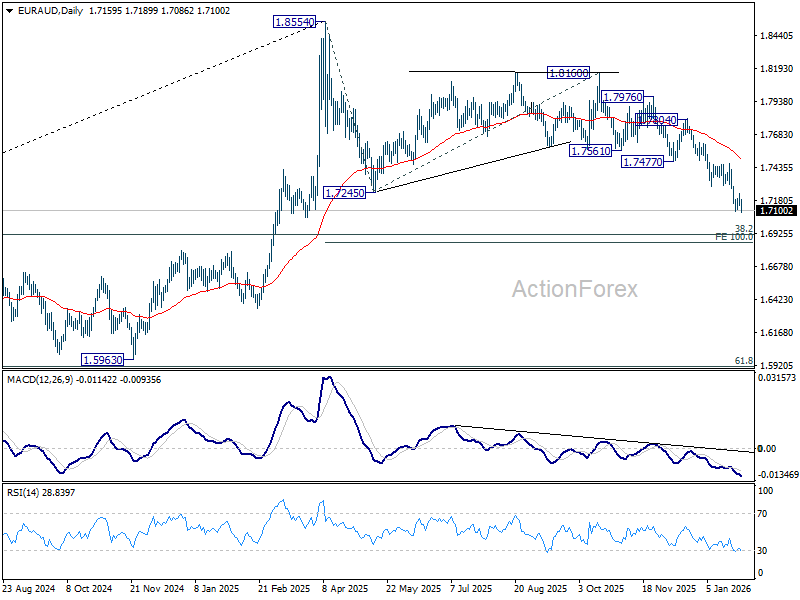

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7131; (P) 1.7183; (R1) 1.7223; More...

Intraday bias in EUR/AUD is back on the downside with breach of 1.7096 temporary low. Current fall from 1.8160 is seen as the third leg of the corrective pattern from 1.8554. Deeper decline should be seen to 100% projection of 1.8554 to 1.7245 from 1.8160 at 1.6851. Nevertheless, break of 1.7232 resistance will now indicate short term bottoming, and turn bias back to the upside for stronger rebound to 1.7466.

In the bigger picture, the break of 55 W EMA (now at 1.7464) argues that fall from 1.8554 medium term top is correcting whole up trend from 1.4281 (2022 low). Deeper decline is in favor to 38.2% retracement of 1.4281 to 1.8554 at 1.6922, and possibly below. Risk will stay on the downside as long as 55 D EMA (now at 1.7537) holds, in case of strong rebound.

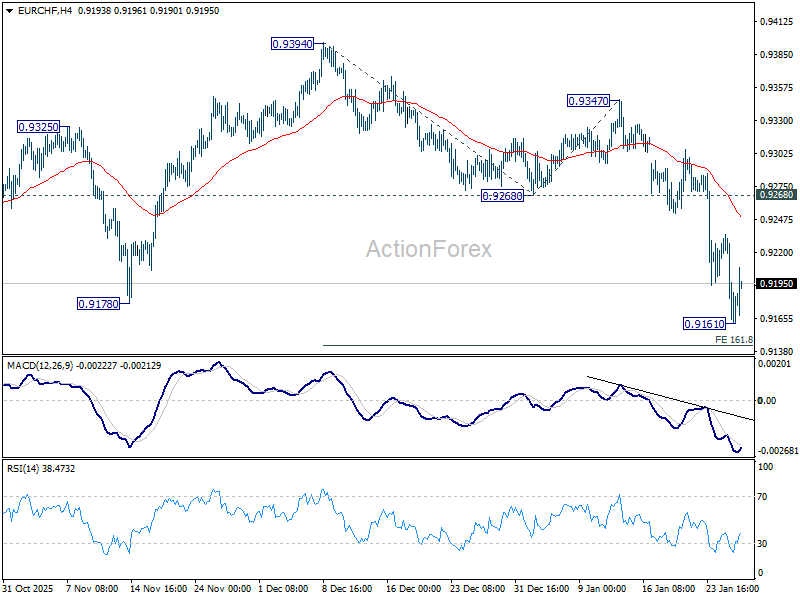

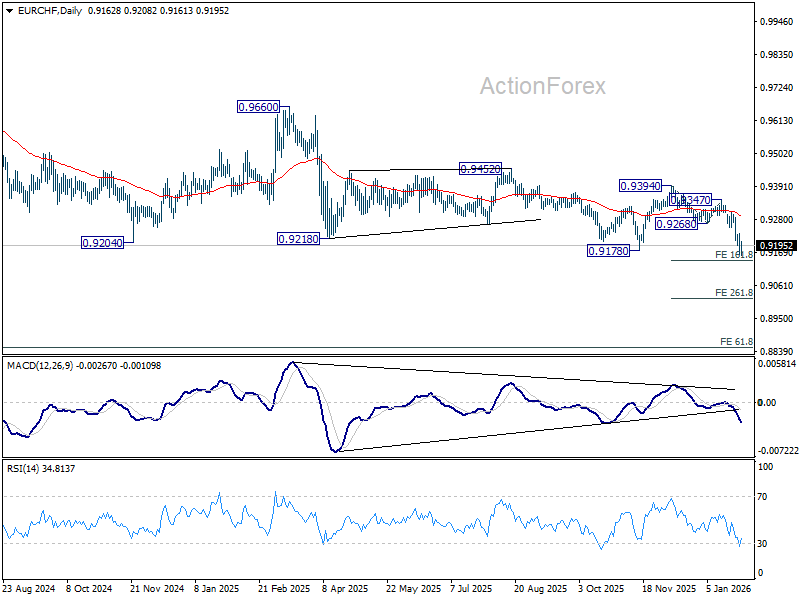

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9141; (P) 0.9189; (R1) 0.9214; More....

Intraday bias in EUR/CHF is turned neutral with current recovery. Some consolidations would be seen first, but upside should be limited below 0.9268 support turned resistance. Firm break of 161.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143 will target 261.8% projection at 0.9017.

In the bigger picture, another rejection by 55 W EMA (now at 0.9350) keeps outlook bearish. Downtrend from 1.2004 (2018 high) is still in progress. Firm break of 0.9178 will target 61.8% projection of 1.1149 to 0.9407 from 0.9928 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.

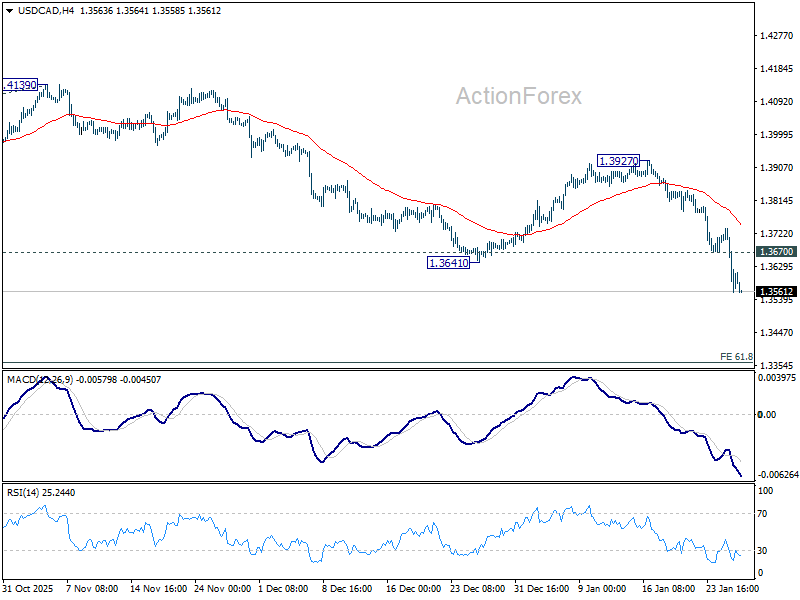

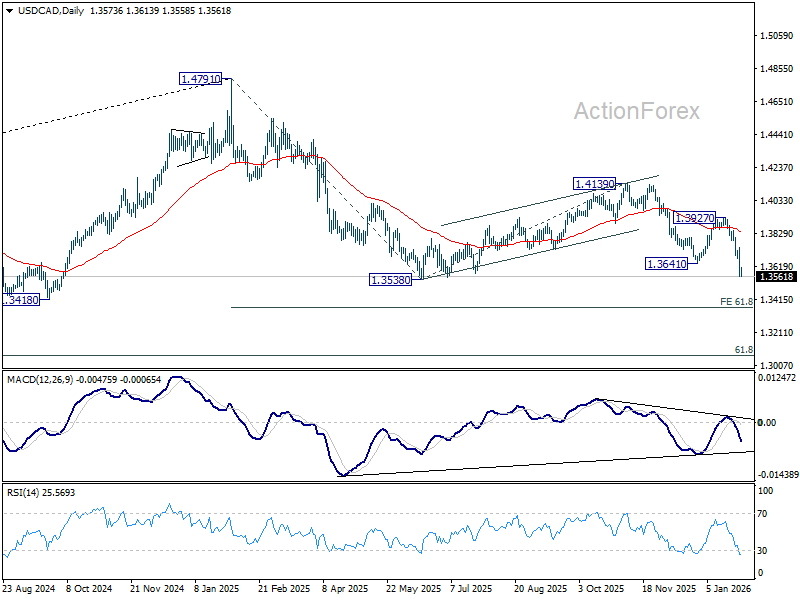

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3512; (P) 1.3626; (R1) 1.3693; More...

Intraday bias in USD/CAD remains on the downside for retesting 1.3538 low. Firm break there resume whole fall from 1.4971. Next target is 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. On the upside, above 1.3670 minor resistance will turn intraday bias neutral and bring consolidations, before staging another fall.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, and break of 1.3538 will target 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

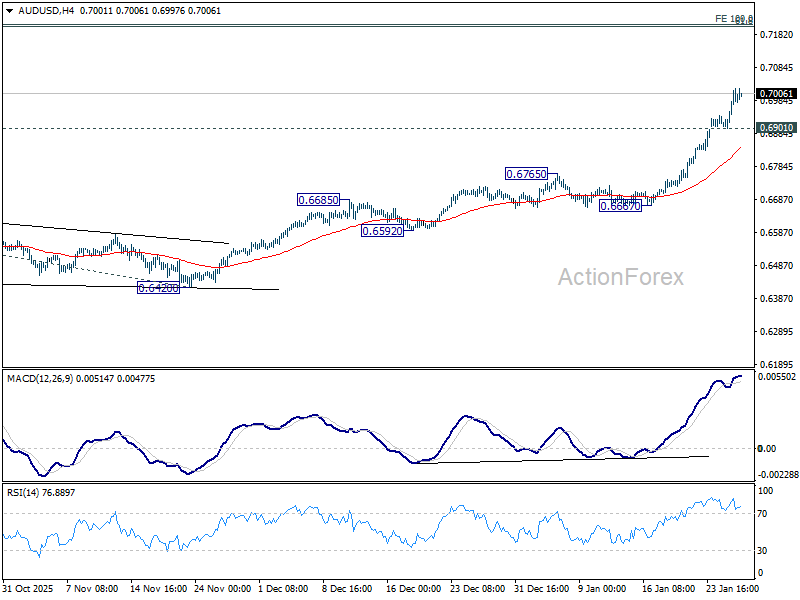

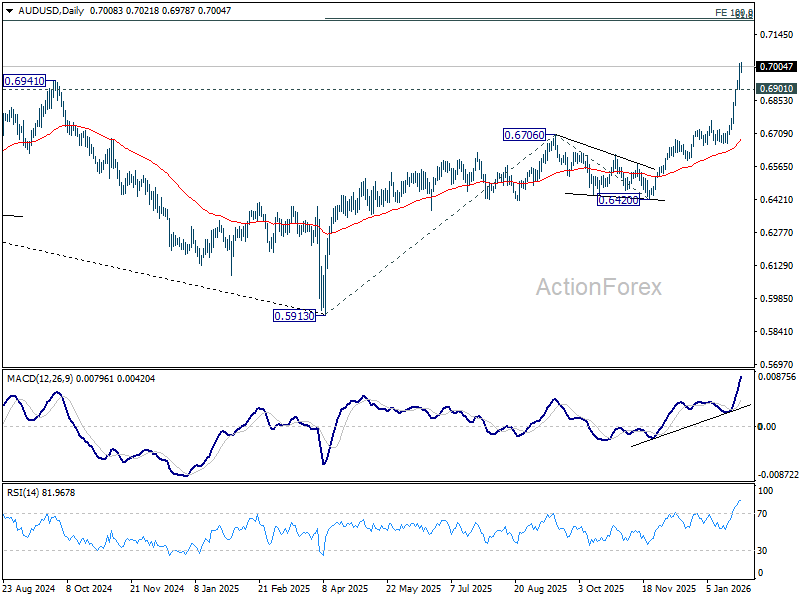

AUD/USD Daily Report

Daily Pivots: (S1) 0.6937; (P) 0.6976; (R1) 0.7051; More...

Intraday bias in AUDUSD stays on the upside for the moment. Current rally is part of the up trend form 0.5913 and should target 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213 next. On the downside, below 0.6901 minor support will turn intraday bias neutral and bring consolidations. Downside of retreat should be contained above 0.6765 resistance turned support to bring another rally.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

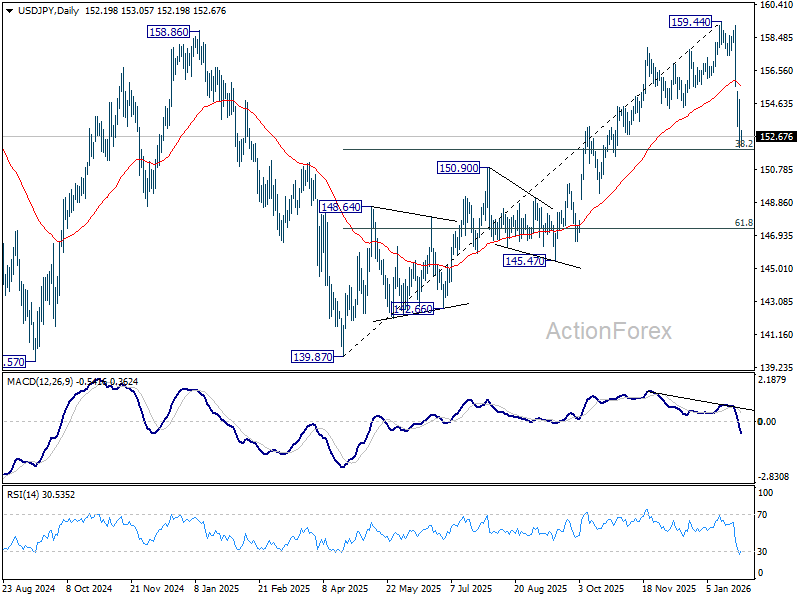

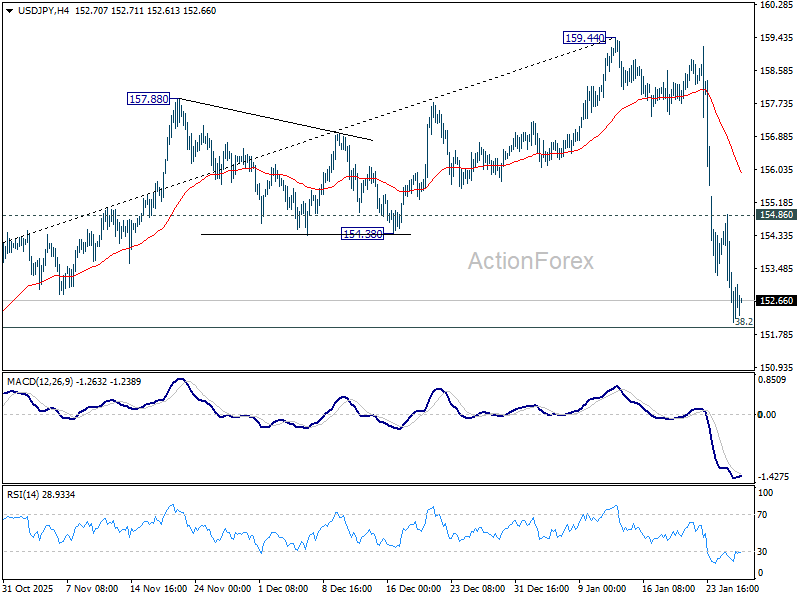

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.25; (P) 153.06; (R1) 154.04; More...

Intraday bias in USD/JPY is turned neutral first with loss of downside momentum. Fall from 159.44 is seen as correcting the rise from 139.87. Strong support should be seen from 38.2% retracement of 139.87 to 159.44 at 151.96 to bring rebound, at least on first attempt. On the upside above 154.86 minor resistance will turn intraday bias to the upside for recovery. However, decisive break of 151.96 will argue that it is reversing whole rise from 139.87. Deeper decline would then be seen to 61.8% retracement at 147.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.35) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.