Sample Category Title

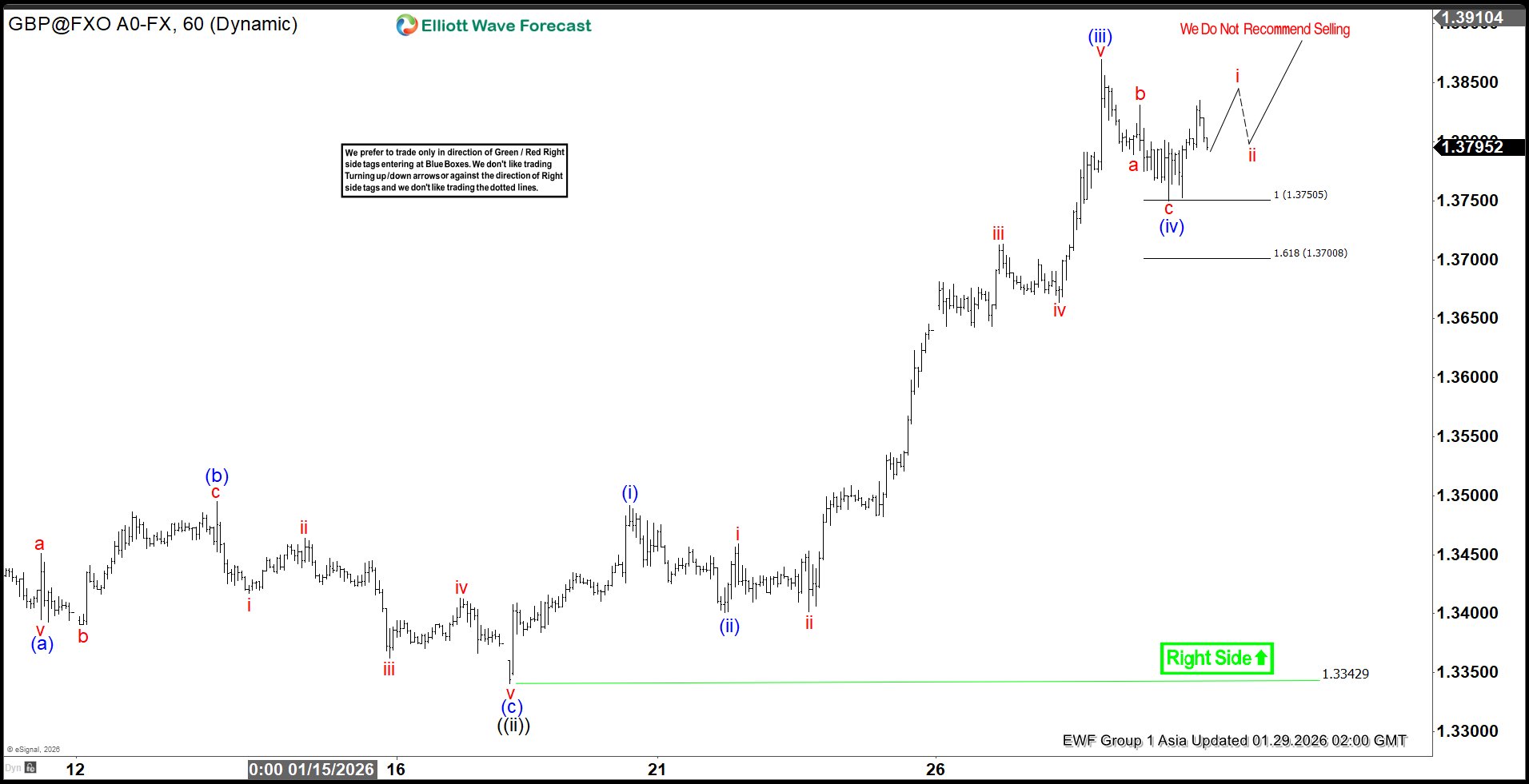

GBPUSD Extends Impulsive Move Higher; Elliott Wave Targets 1.39 and Beyond

GBPUSD continues to demonstrate a constructive bullish sequence from the November 5, 2026 low, favoring further upside potential. The rally from that low is unfolding in the form of an impulse Elliott Wave structure, which provides clarity on the ongoing trend. From November 5, wave ((i)) concluded at 1.3568, followed by a corrective pullback in wave ((ii)) that ended at 1.334. The internal subdivision of wave ((ii)) developed as a zigzag formation, with wave (a) finishing at 1.339, wave (b) rallying to 1.3495, and wave (c) declining to 1.334. This sequence completed wave ((ii)) at a higher degree and set the stage for renewed strength.

The pair has since resumed its advance in wave ((iii)), which is unfolding as another impulse of lesser degree. From the termination of wave ((ii)), wave (i) ended at 1.3491, while wave (ii) corrected to 1.34. The subsequent rally in wave (iii) reached 1.3869, and the pullback in wave (iv) settled at 1.3749. The structure suggests that the pair is poised to extend higher in wave (v), thereby completing wave ((iii)). Once this occurs, a corrective phase in wave ((iv)) should follow, addressing the cycle from the January 19 low before the broader rally resumes.

In the near term, as long as the pivot at 1.334 remains intact, dips are expected to attract buyers. These retracements are likely to unfold in 3, 7, or 11 swings, offering opportunities for continuation of the bullish sequence. The overall outlook remains constructive, with the technical framework supporting further appreciation in GBPUSD.

GBPUSD 60 minute chart

GBPUSD Elliott Wave video:

https://www.youtube.com/watch?v=j2N2jCuBCbk

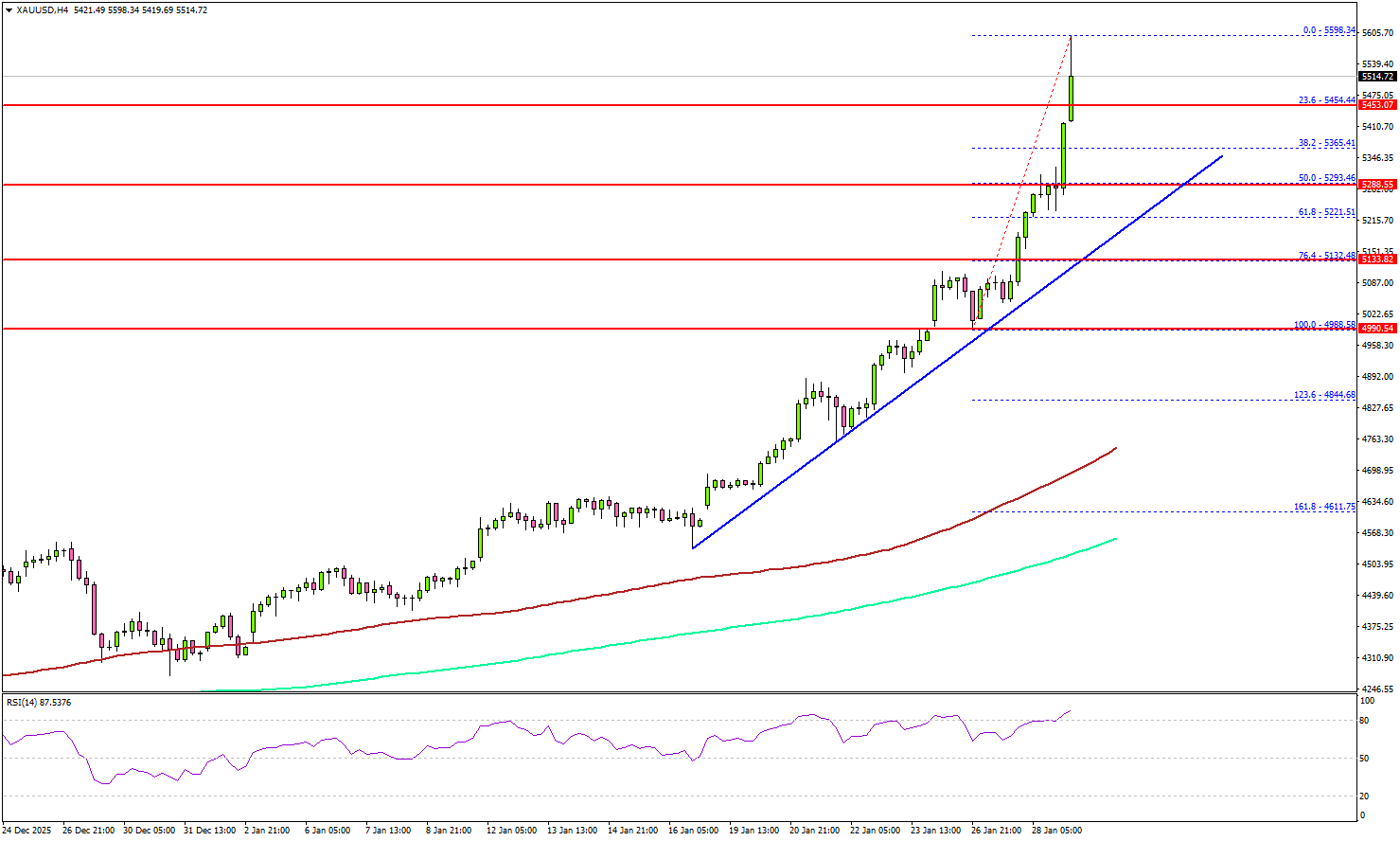

Gold Stretches Rally Above $5,550, Key Supports To Watch

Key Highlights

- Gold started a fresh surge and traded to a new all-time high above $5,590.

- A connecting bullish trend line is forming with support at $5,280 on the 4-hour chart.

- WTI Crude Oil prices climbed higher above $62.00 and $63.00.

- USD/JPY and USD/CHF saw an increase in selling pressure.

Gold Price Technical Analysis

Gold prices started a fresh rally above $4,880 and $5,000 against the US Dollar. It settled above $5,250 and gained momentum for a new uptrend.

The 4-hour chart of XAU/USD indicates that the price extended gains above $5,500 and traded to a new all-time high above $5,590. The bulls seem unstoppable, and they could soon aim for more upside in the coming sessions.

On the upside, immediate resistance is near the $5,600 level. The next major resistance sits near the $5,625 level. A clear move above $5,625 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $5,700. The main target for the bulls could be $5,800.

If there is a pullback, Gold might find bids near the $5,450 level. The first major support sits at $5,280. There is also a connecting bullish trend line forming with support at $5,280, below which the price might slide to $5,000.

The main support sits at $5,000. Any more losses might call for a test of the 100 Simple Moving Average (red, 4 hours) at $4,700 or even the 200 Simple Moving Average (green, 4 hours) at $4,550.

Looking at WTI Crude Oil, the price started a recovery wave, and the bulls pushed the price above the key hurdle at $62.00.

Economic Releases to Watch Today

- US Initial Jobless Claims - Forecast 212K, versus 198K previous.

- US Factory Orders for Nov 2025 (MoM) - Forecast +1.6%, versus -1.3% previous.

Eco Data 1/29/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Dec | 52M | 40M | -163M | -335M |

| 00:00 | NZD | ANZ Business Confidence Jan | 64.1 | 73.6 | ||

| 00:00 | NZD | ANZ Activity Outlook Jan | 51.6 | 60.9 | ||

| 00:30 | AUD | Import Price Index Q/Q Q4 | 0.90% | -0.20% | -0.40% | |

| 05:00 | JPY | Consumer Confidence Index Jan | 37.9 | 37.1 | 37.2 | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Dec | 2.80% | 3.00% | 3.00% | |

| 10:00 | EUR | Eurozone Economic Sentiment Jan | 99.4 | 97 | 96.7 | |

| 10:00 | EUR | Eurozone Industrial Confidence Jan | -6.8 | -8.1 | -9 | -8.5 |

| 10:00 | EUR | Eurozone Services Sentiment Jan | 7.2 | 6 | 5.6 | 5.8 |

| 10:00 | EUR | Eurozone Consumer Confidence Jan F | -12.4 | -12.4 | -12.4 | |

| 13:30 | CAD | Trade Balance (CAD) Nov | -2.2B | -0.7B | -0.6B | -0.4B |

| 13:30 | USD | Initial Jobless Claims (Jan 23) | 209K | 202K | 200K | 210K |

| 13:30 | USD | Trade Balance (USD) Nov | -56.8B | -44.6B | -29.4B | -29.2B |

| 13:30 | USD | Nonfarm Productivity Q3 F | 4.90% | 4.90% | 4.90% | |

| 13:30 | USD | Unit Labor Costs Q3 F | -1.90% | -1.90% | -1.90% | |

| 15:00 | USD | Wholesale Inventories Nov F | 0.20% | 0.20% | 0.20% | |

| 15:00 | USD | Factory Orders M/M Nov | 2.70% | 0.50% | -1.30% | -1.20% |

| 15:30 | USD | Natural Gas Storage (Jan 23) | -242B | -237B | -120B |

| 21:45 | NZD |

| Trade Balance (NZD) Dec | |

| Actual | 52M |

| Consensus | 40M |

| Previous | -163M |

| Revised | -335M |

| 00:00 | NZD |

| ANZ Business Confidence Jan | |

| Actual | 64.1 |

| Consensus | |

| Previous | 73.6 |

| 00:00 | NZD |

| ANZ Activity Outlook Jan | |

| Actual | 51.6 |

| Consensus | |

| Previous | 60.9 |

| 00:30 | AUD |

| Import Price Index Q/Q Q4 | |

| Actual | 0.90% |

| Consensus | -0.20% |

| Previous | -0.40% |

| 05:00 | JPY |

| Consumer Confidence Index Jan | |

| Actual | 37.9 |

| Consensus | 37.1 |

| Previous | 37.2 |

| 09:00 | EUR |

| Eurozone M3 Money Supply Y/Y Dec | |

| Actual | 2.80% |

| Consensus | 3.00% |

| Previous | 3.00% |

| 10:00 | EUR |

| Eurozone Economic Sentiment Jan | |

| Actual | 99.4 |

| Consensus | 97 |

| Previous | 96.7 |

| 10:00 | EUR |

| Eurozone Industrial Confidence Jan | |

| Actual | -6.8 |

| Consensus | -8.1 |

| Previous | -9 |

| Revised | -8.5 |

| 10:00 | EUR |

| Eurozone Services Sentiment Jan | |

| Actual | 7.2 |

| Consensus | 6 |

| Previous | 5.6 |

| Revised | 5.8 |

| 10:00 | EUR |

| Eurozone Consumer Confidence Jan F | |

| Actual | -12.4 |

| Consensus | -12.4 |

| Previous | -12.4 |

| 13:30 | CAD |

| Trade Balance (CAD) Nov | |

| Actual | -2.2B |

| Consensus | -0.7B |

| Previous | -0.6B |

| Revised | -0.4B |

| 13:30 | USD |

| Initial Jobless Claims (Jan 23) | |

| Actual | 209K |

| Consensus | 202K |

| Previous | 200K |

| Revised | 210K |

| 13:30 | USD |

| Trade Balance (USD) Nov | |

| Actual | -56.8B |

| Consensus | -44.6B |

| Previous | -29.4B |

| Revised | -29.2B |

| 13:30 | USD |

| Nonfarm Productivity Q3 F | |

| Actual | 4.90% |

| Consensus | 4.90% |

| Previous | 4.90% |

| 13:30 | USD |

| Unit Labor Costs Q3 F | |

| Actual | -1.90% |

| Consensus | -1.90% |

| Previous | -1.90% |

| 15:00 | USD |

| Wholesale Inventories Nov F | |

| Actual | 0.20% |

| Consensus | 0.20% |

| Previous | 0.20% |

| 15:00 | USD |

| Factory Orders M/M Nov | |

| Actual | 2.70% |

| Consensus | 0.50% |

| Previous | -1.30% |

| Revised | -1.20% |

| 15:30 | USD |

| Natural Gas Storage (Jan 23) | |

| Actual | -242B |

| Consensus | -237B |

| Previous | -120B |

January FOMC: The Window To Cut Is Closing

Summary

As was widely expected, the FOMC held the fed funds rate steady at its January meeting. The statement and Chair Powell's press conference suggested that the Committee is finely balanced between worries about a gradually deteriorating labor market and still above-target inflation. Our main takeaway from today's meeting is that the hurdle to additional cuts has been raised under Chair Powell's watch.

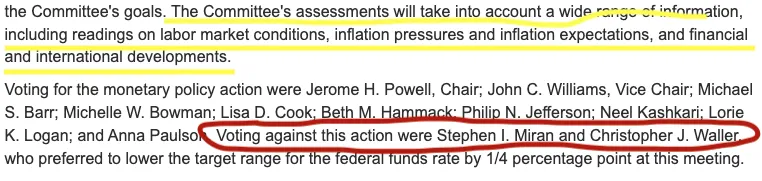

Governors Miran and Waller dissented in favor of a 25 bps cut. Interestingly, Michelle Bowman voted in favor of holding rates unchanged, and Miran's dissent was for 25 bps, not 50 bps. Even the Committee's doves appear to have become relatively less dovish recently.

January's hold follows 25 bps cuts at each of the FOMC's three previous meetings that have left the policy rate modestly above most participants' estimates of neutral (chart). The post-meeting statement struck us as slightly hawkish. References to downside risks to the labor market were removed, with new language saying that the unemployment rate has "shown some signs of stabilization."

Like the labor market characterization, the language around inflation was cautiously more optimistic. While the statement maintained that "inflation remains somewhat elevated," it removed the reference to inflation moving up since early last year.

The more balanced risks to the Fed's dual mandate came through in Chair Powell's press conference. According to Powell, "We still have some tension between employment and inflation, but it's less than it was. I think the upside risks to inflation and the down risks [to employment] are probably both diminished a bit."

Powell also seemed more upbeat on the economic outlook, saying that it's "overall a stronger forecast" compared to the December meeting. That said, he was not ready to sound the all clear: he stressed that the Committee has not made any decisions about future meetings, and on the labor market he stated that "we saw data coming in which suggests some signs of stabilization. I wouldn't go too far with that, but some signs of stabilization."

Against this backdrop, Powell stressed that the current policy rate is well-positioned after the three cuts to "let the data speak to us."

Powell refrained from commenting on the Department of Justice investigation into the Federal Reserve as well as his plans to leave or stay on the Board of Governors after his term as Chair expires. When asked about his attendance of Lisa Cook's case at the Supreme Court, he noted that the case is "perhaps the most important legal case in the Fed's 113-year history. And as I thought about it, I thought it might be hard to explain why I didn't attend."

While the statement and Chair Powell's press conference suggested the Committee is not in a hurry to resume policy easing, both were careful to preserve flexibility for the months ahead, including keeping the door cracked to another rate cut in March should the labor market weaken and/or inflation slow further. Our forecast remains for two additional 25 bps cuts at the March and June meeting this year. Yet, as we have stressed recently, the risks to this call look increasingly skewed toward later and less easing as our expectations for solid GDP growth and a stabilizing labor market later this year leave a narrow window to cut.

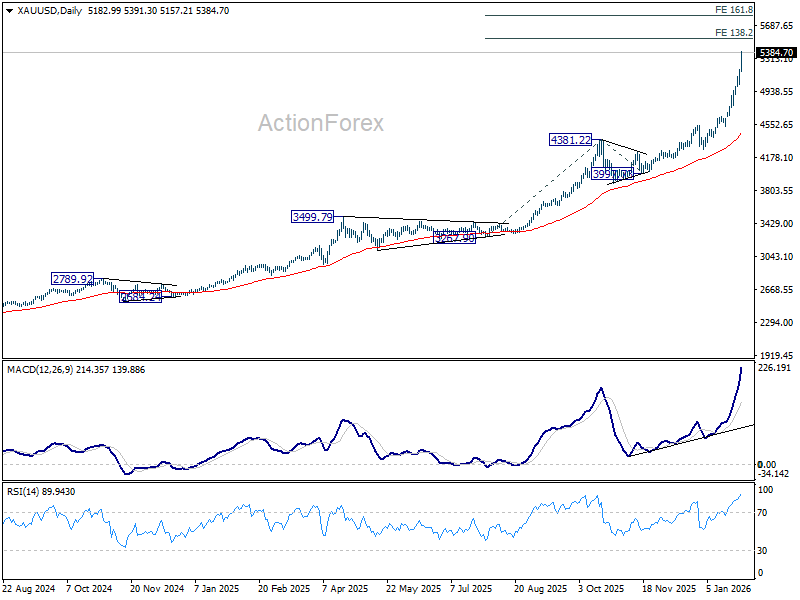

Gold buyers return after Fed hold, heading to 5,800

Gold’s record-breaking rally resumed today after only a brief consolidation, with buyers stepping back in once the Fed decision passed without surprise. The clearing of event risk proved enough to reignite upside momentum.

The Fed left rates unchanged as widely expected. While two governors—Stephen Miran and Christopher Waller—dissented in favor of a cut, the broader statement offered no clear signal of imminent easing, keeping policy guidance broadly intact.

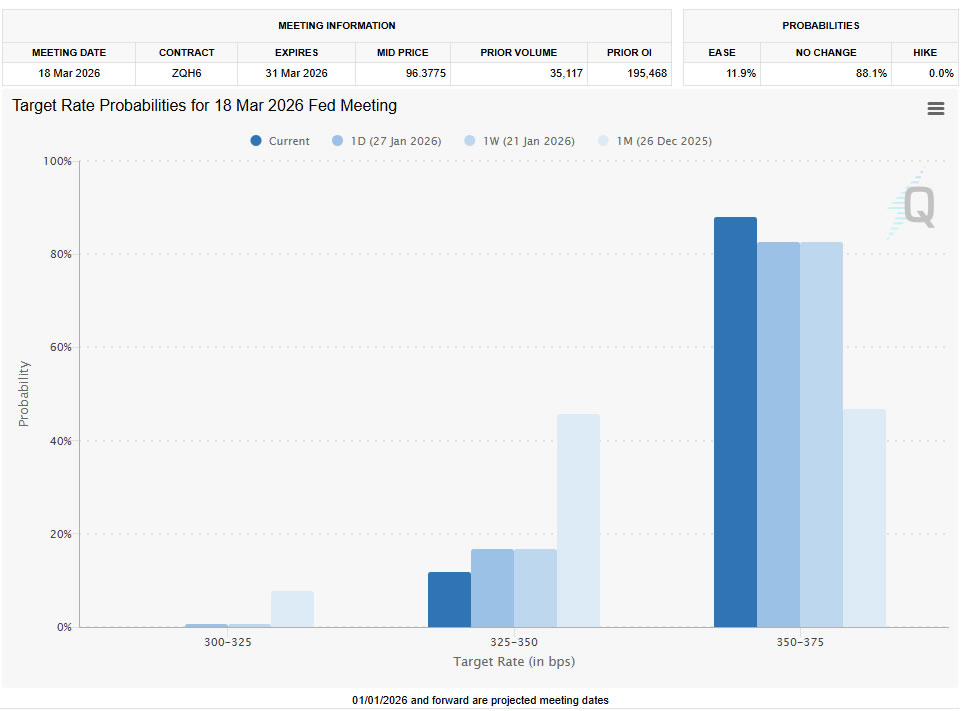

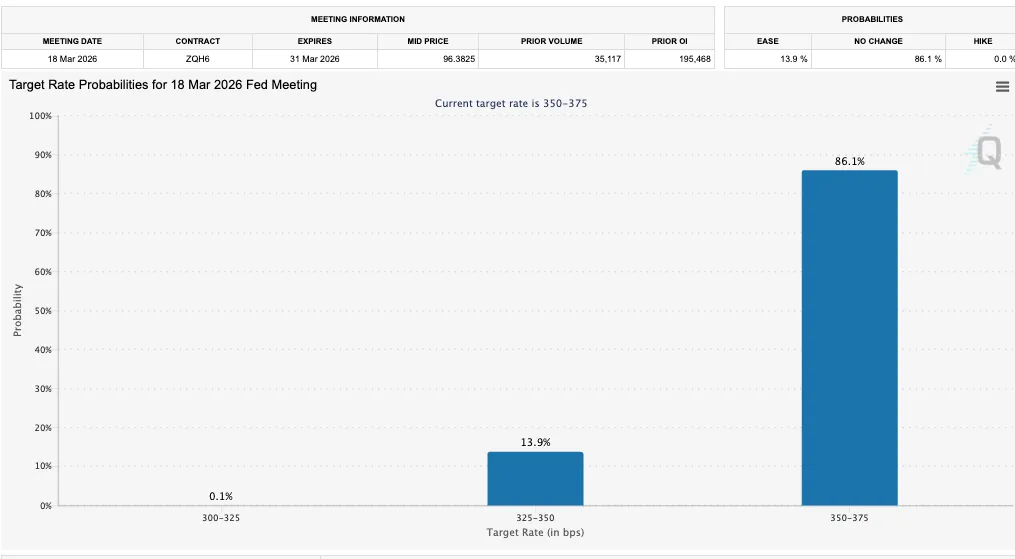

Chair Jerome Powell’s press conference reinforced that message. His tone remained balanced and non-committal, emphasizing data dependence rather than preparing markets for near-term action. As a result, expectations shifted further toward another hold in March.

Market pricing now assigns roughly 88% odds to a March hold, up from about 82% a day earlier. Yet that repricing has failed to generate meaningful support for Dollar, which continues to struggle to attract buyers.

Gold, by contrast, benefited from the reduced uncertainty. With the Fed outcome largely neutral and no hawkish surprise, investors were quick to re-engage on the long side, extending the broader uptrend.

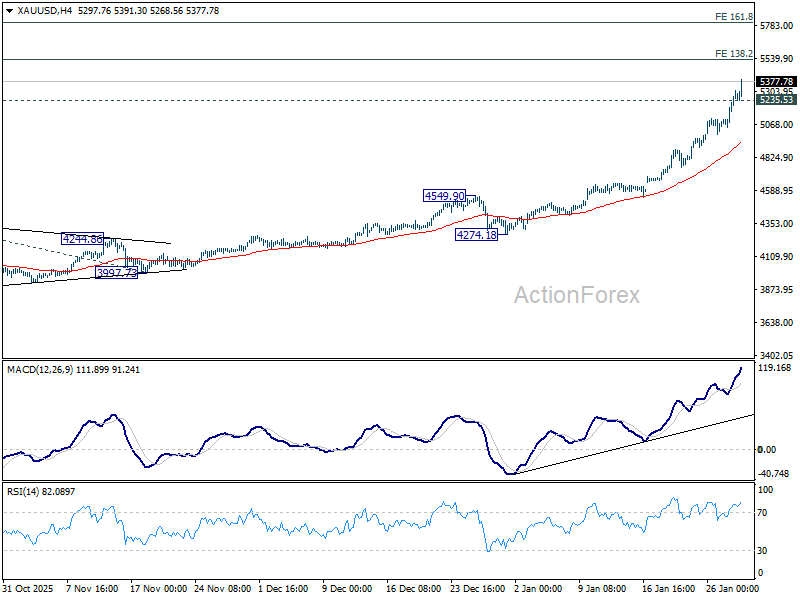

Technically, Gold is still in upside acceleration as seen in both 4H and D MACD. The next target of 138.2% projection of 3,267.90 to 4,381.22 from 3,997.73 at 5,536.33 will likely be taken out without any problem.

Gold could indeed head to 161.8% projection at 5,799.08 before taking a breather. Meanwhile, below 5,235.53 minor support will likely bring some brief consolidations before staging another rise.

Fed Powell pushes back on political pressure narrative

Fed Chair Jerome Powell said in the post meeting press conference that the US economy expanded at a solid pace last year and is entering 2026 on "firm footing". He added that monetary policy is "not on a preset course", reiterating that future rate adjustments will depend on incoming data, the evolving outlook, and the balance of risks. He said the Fed is “well positioned” to determine the extent and timing of any additional moves, emphasizing a meeting-by-meeting approach rather than signaling near-term action.

The press conference turned more pointed when Powell was asked about the implications for American households if the Fed were to lose its independence. He argued that independence is not about protecting policymakers, but about safeguarding credibility, noting that every advanced democracy has converged on the practice of insulating monetary policy from direct political control.

Powell warned that losing independence would make it difficult to restore institutional credibility, stressing that central banks serve the public best when allowed to operate free from political interference. He said he remains confident that the Fed can maintain that independence, adding that both he and his colleagues are firmly committed to preserving it.

Fed Keeps Rates Steady – Market Reactions to FOMC

The Fed is keeping rates unchanged at the 3.50% to 3.75% range – Slightly hawkish tone and the US Dollar is strengthening.

Changes to the previous statement include a more robust outlook on employment and the economy – This could take out future cuts but for now participants are awaiting for Powell.

The votes for the pause are at 10-2 – Fed's Waller and Miran dissented.

The pause was 98% priced so not surprising to observe the quiet atmosphere in Markets.

You can get access to the detailed report and Fed Statement right here.

Nothing surprising is appearing in the Statement – Except for a continued rebound in the US Dollar, volatility is low for now.

Traders will be awaiting closely for Powell's Press Conference – Log in to his Live speech (at 14:30 E.T.) right here.

Notable quotes from the Statement – Source: Federal Reserve

Pre-Conference Market Pricing

Market Pricing for the March meeting (14:20) – Source: FedWatch Tool

Pre-Conference Asset Board – Courtesy of Finviz

Market Reactions

Dollar rallies

US Dollar (DXY) 1H Chart – Source: TradingView – January 28, 2026

Fed Moves Back to the Sidelines, Following Three “Risk Management” Cuts

The Federal Open Market Committee (FOMC) held the policy rate fixed at the target range of 3.5%-3.75%. The move comes after three consecutive quarter-point "risk management" cuts at the past three meetings.

The FOMC's press release struck a relatively balanced tone. Importantly, the prior reference to "the downside risks to employment having increased" was removed – suggesting the Committee no longer feels the need for further risk management cuts. The characterization of the labor market largely reflects a "mark-to-market" with job gains now described as "remaining low" (as opposed to "having slowed") and the unemployment as "showing some signs of stabilizing" (as opposed to "has moved up since earlier this year").

Inflation is still viewed as "somewhat elevated", but the Committee dropped the prior reference of "has moved up since earlier in the year", reflecting more recent readings, which came in on the cooler side.

The Committee also upgraded its assessment of recent economic activity to "solid" from "moderate".

Ten of the twelve Committee members voted in favor of today's decision. Stephen Miran and Christopher Waller both dissented in favor of another quarter-point cut.

Key Implications

Today's decision was widely expected. With the risk management cuts now in the rearview mirror and the policy rate nearing a more neutral setting, the FOMC is content to take a pause and better assess how last year's easing filters through to the broader economy.

The changes in today's statement suggest there's now a higher bar for further rate cuts – and rightfully so. Not only has the labor market shown some signs of stabilizing in recent months, but economic activity also appears to have ended last year on a more solid footing. This suggests a stronger growth impulse coming into 2026, which is likely to be further amplified by fiscal stimulus included in the One Big Beautiful Bill. Absent an unexpected deterioration in the labor market, we think that the FOMC will remain on the sidelines until there's more visible progress towards the Fed's 2% inflation target, which is unlikely to come until later this year.

Fed holds, two votes for a cut, but no signal of action

The Fed left interest rates unchanged at 3.50–3.75%, in line with expectations, but the decision was not unanimous. Two governors—Stephen Miran and Christopher Waller—dissented, preferring an immediate 25bp rate cut.

Despite the dissent, the statement offered no clear signal that a rate cut is imminent at the next meeting. The overall tone remained cautious rather than preparatory, suggesting the majority remains unconvinced that conditions yet warrant an easing move.

The Fed described economic activity as expanding at a "solid pace",. While noting that job gains have remained low and the unemployment rate has shown signs of stabilization. Inflation was again characterized as "somewhat elevated".

Uncertainty around the outlook remains high. The Committee emphasized it is attentive to risks on "both sides of its dual mandate" and reiterated its willingness to adjust policy if needed. For now, however, the message is one of flexibility rather than urgency, leaving markets without a clear near-term easing signal.

(FED) Federal Reserve Issues FOMC Statement

Available indicators suggest that economic activity has been expanding at a solid pace. Job gains have remained low, and the unemployment rate has shown some signs of stabilization. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 3‑1/2 to 3‑3/4 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Beth M. Hammack; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Anna Paulson. Voting against this action were Stephen I. Miran and Christopher J. Waller, who preferred to lower the target range for the federal funds rate by 1/4 percentage point at this meeting.