Sample Category Title

Gold (XAU/USD), Silver (XAG/USD) Technical Outlook: Navigating the Current Climate as Gold Taps $5300/oz, Silver Eyes Wedge Breakout

- Gold (XAU/USD) peaking at $5,311/oz and Silver (XAG/USD) trading around $115.10.

- The surge is driven by a "perfect storm" of factors

- Traders eyeing a potential entry for Gold at the swing high of $5190 and monitoring Silver's wedge pattern breakout for a potential $15 rally.

- Key levels to watch for Silver with support at $110.00 and resistance at $116.00 before the all-time high of $117.75.

January 2026 continues to prove historic for commodity markets. If you have been watching the charts, you likely saw Gold smashing through records while Silver continues its impressive climb.

Now the reasons for these moves and the potential targets are what most people are discussing. Rightly so, and I thought we could take a look at the various factors at work and how to navigate the current environment from a trading perspective.

The Current Rally

The Gold (XAU/USD) price broke through the psychological barrier of $5,300, reaching a peak of $5,311 in early trading. This marks the eighth straight day of record-setting gains for the yellow metal.

Silver (XAG/USD) Silver is also performing exceptionally well, trading around $115.10. It is currently holding steady above the $115.00 mark and pushing back toward its own record high of $117.74, set just a few days ago on Monday, January 26.

Why Are Prices Rising Today?

There isn't just one reason for this surge; it is a "perfect storm" of several factors driving investors toward safe assets.

Safe-Haven Demand (Fear in the Markets) Markets are nervous, and when they get nervous, they buy Gold and Silver. Current geopolitical tensions are high. News of friction between the US and NATO regarding Greenland, alongside ongoing issues in the Russia-Ukraine war and Iran-US tensions has people looking for safety.

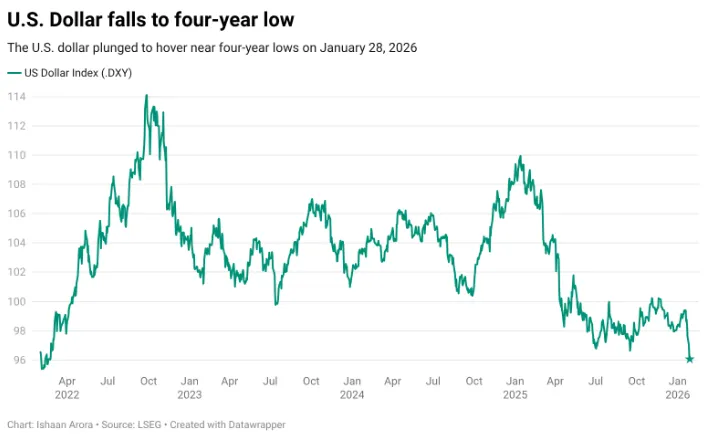

A Weaker US Dollar. One of the main reasons for this week's sharp rally in Gold and Silver has been the ‘demise’ of the US Dollar that has slid to its lowest level in four years.

Since commodities like Gold and Silver are priced in dollars, a weaker dollar makes them cheaper for foreign buyers, driving up demand. Reports suggest a growing "crisis of confidence" in some US assets is fueling this drop which include concerns about Fed independence.

Source: LSEG

Federal Reserve Expectations. All eyes are on the Federal Reserve today. The market expects the Fed to keep interest rates unchanged at 3.50%–3.75%. However, there is a strong belief that interest rates will be cut later this year. Lower interest rates are generally good for Gold and Silver because they don't pay interest like bonds do; when rates fall, metals become more attractive and this hope continues to underpin the longer term bull trend.

Trade War & Tariff Fears Talk of new tariffs and trade disputes involving the US, Canada, and China is adding to the uncertainty. This "trade war" atmosphere is a classic driver for precious metal rallies.

Potential Opportunities Moving Forward - Gold & Silver

Moving forward and the bulls look to be firmly in control.

Going against the strong trend at the moment does not appear to be a wise move. The lack of historic price action will make a potential short at this stage guesswork at best.

Picking a top is not easy in the best of circumstances let alone one with such little price action to evaluate.

Now that is not to say that short-term intraday opportunities may not present themselves. The current volatility evident in markets means attractive risk-to-reards may be achieved even from an intraday perspective.

Looking at the Gold one-hour chart, and trying to keep things simple, the ideal move from here for those looking to get involved would be a pullback to the 50-day MA and breakout level of $5105. However that level is quite far from current prices and may not materialize.

A more immediate area that would be bulls could eye for an entry may be the swing high from January 27 at the $5190 handle. This may provide bulls with an excellent risk-to-reward opportunity either heading into or post the FOMC event later today.

Gold One-hour chart, January 28, 2026

Source: TradingView.com (click to enlarge)

Silver Technical Outlook

Looking at the one-hour silver chart and we do have more to work with.

SIlver is trading in a wedge pattern, with a breakout opening up a potential $15 rally. This is about a 10% move which is significant to say the least.

This is definitely a setup worth monitoring. A break to the downside may find support at the psychological 110.00 handle before the 100-day MA at 105.48 and the psychological 100.00 mark come into play.

A move to the upside here faces hurdles at the 116.00 handle before the all-time highs at 117.75 comes into focus.

Silver one-hour chart, January 28, 2026

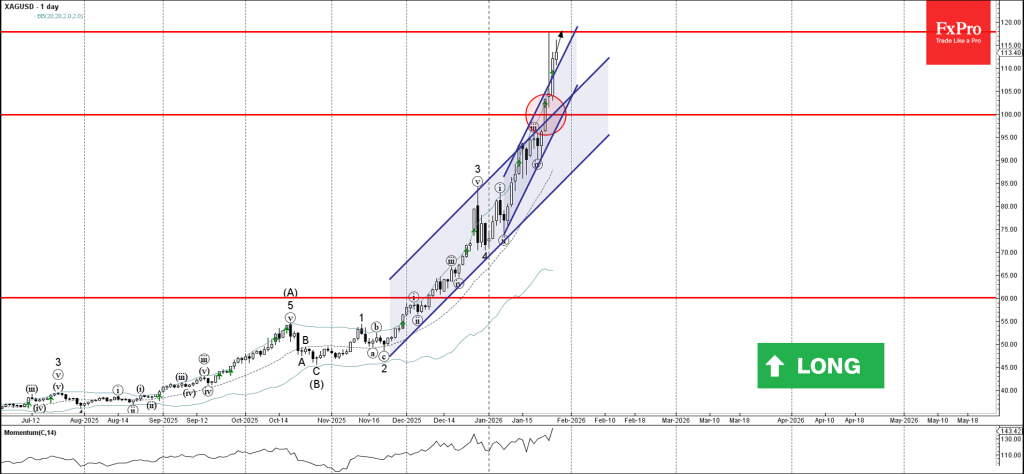

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver broke round resistance level 100.00

- Likely to rise to resistance level 117.85

Silver recently broke through the resistance area at the intersection of the round resistance level 100.00 and the resistance trendline of the sharp daily up channel from the start of January.

The breakout of the resistance level 100.00 accelerated the active short-term impulse wave 5 – which belongs to the strong impulse wave (C) from October.

Silver can be expected to rise to the next resistance level 117.85 (which formed the daily Shooting Star earlier this month).

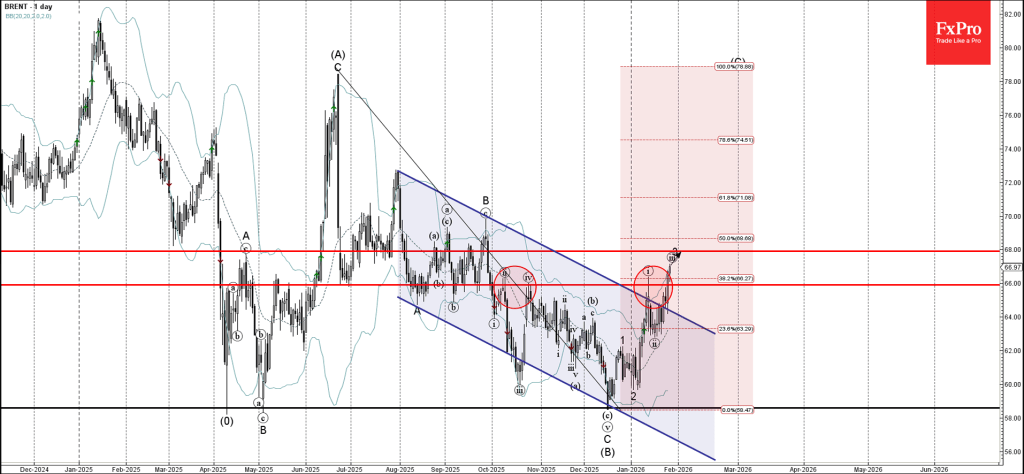

Brent Crude Oil Wave Analysis

Brent Crude Oil: ⬆️ Buy

- Brent Crude Oil broke resistance level 66.00

- Likely to rise to resistance level 68.00

Brent Crude Oil recently broke through the resistance area between the resistance level 66.00 (which has been reversing the price from October) and the resistance trendline of the daily down channel from August.

The breakout of the resistance level 66.00 coincided with the breakout of the 38.2% Fibonacci correction of the downward ABC correction (B) from June.

Brent Crude Oil can be expected to rise to the next resistance level 68.00 (target for the completion of the active impulse wave 3).

Gold Benefits from Weak Dollar

- The US Dollar decline looks like a part of the White House’s plan.

- Gold is rising on capital inflows.

Donald Trump has added fuel to the fire of the falling US dollar. The president’s words that the value of the dollar is ‘great’ underlined that US officials are comfortable with the dollar’s decline, only reinforcing the drop to its lowest level since February 2022. This is causing a rally of the main forex pair to 1.20, despite the forecasted 5.4% growth in US GDP in the fourth quarter, and the FOMC’s unwillingness to cut rates until at least June, according to leading indicators from the Atlanta Fed.

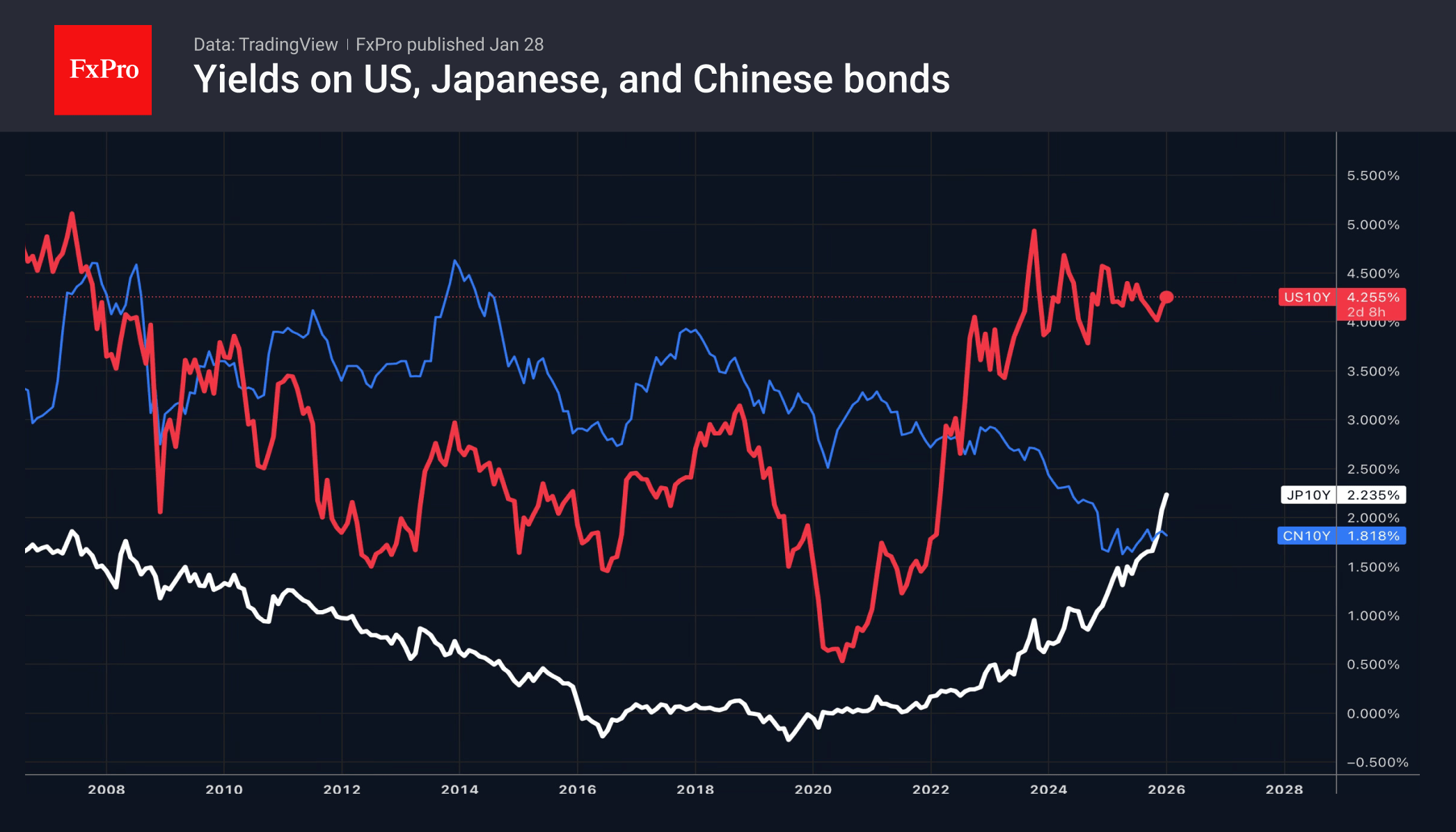

The White House is sticking to its guns. In Davos, Trump asked a rhetorical question: why is the US economy strong, the risk of default low, and interest rates higher than in other countries? The United States pays 4.2% on its 10-year debt, while Japan pays 2.2% and China 1.8%. And this is a heavy amount ticking on top of the $38 trillion debt, a staggering additional cost to the budget.

Donald Trump wants to reduce borrowing costs. The Fed’s models show a direct link between a strong economy and the risks of accelerating inflation. However, fundamental analysis suggests that a strong economy cannot have a weak currency. The example of the US dollar shows that it can.

Will the Fed put a spoke in the wheel of the EURUSD bulls? Jerome Powell can do so with his hawkish rhetoric. However, if the central bank retains the phrase about considering additional rate adjustments in the accompanying statement, this could, on the contrary, accelerate the fall of the dollar. The markets will perceive such a move as a signal of resistance to a prolonged pause in the cycle of monetary expansion.

The collapse of the USD index allowed gold to break above $5,300 per ounce for the first time in history. Precious metals act as a politically neutral asset. They react to White House policy but are not dependent on it in the same way as stocks, bonds and the US dollar. As a result, investors are increasing their gold holdings to hedge against political risks.

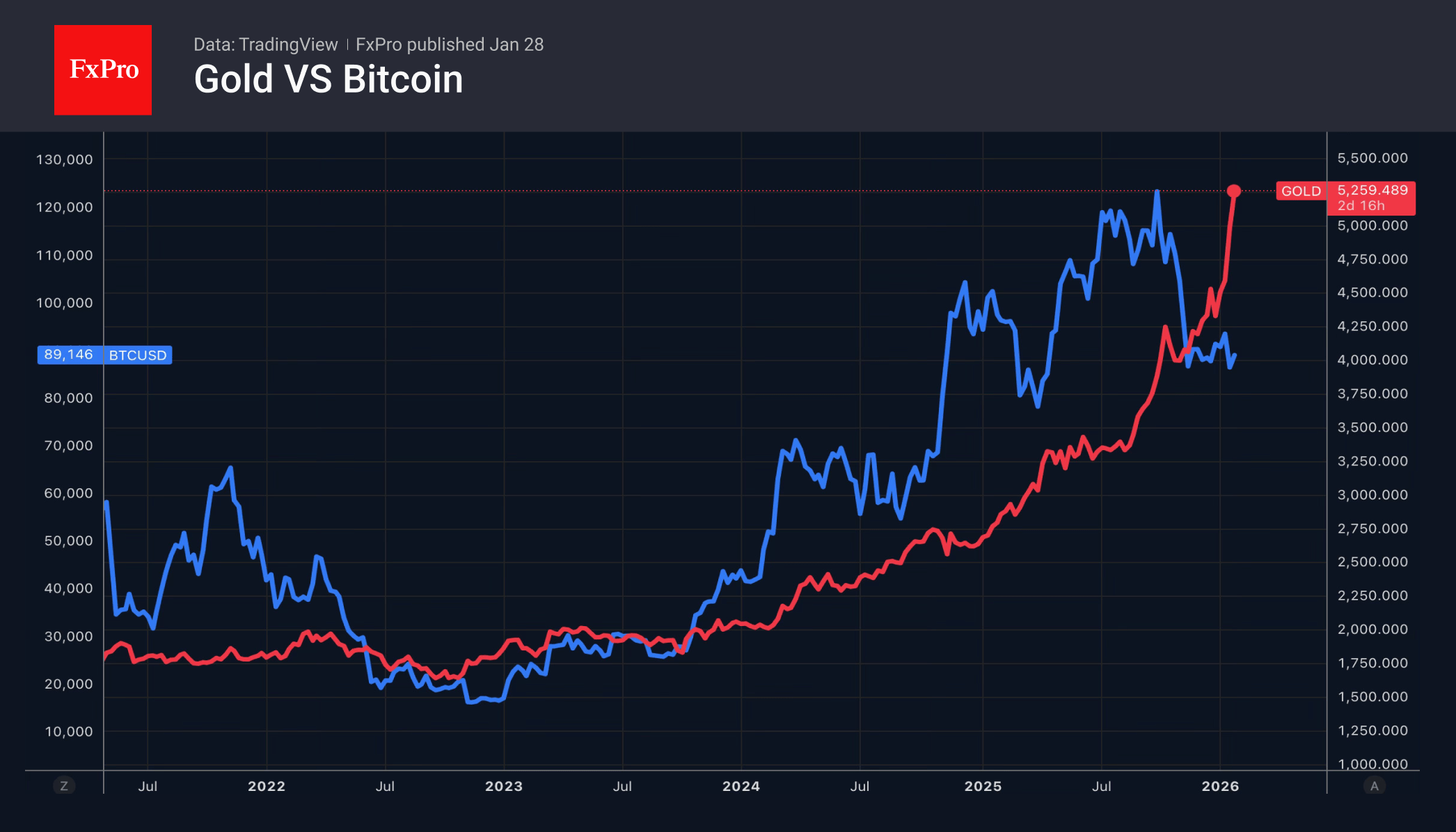

Gold got support from both capital flights from the US and capital outflows from the cryptocurrency market. Many believed that Donald Trump’s promise to turn America into the world crypto capital would cause Bitcoin to break record after record. In fact, it has become an asset dependent on White House policy.

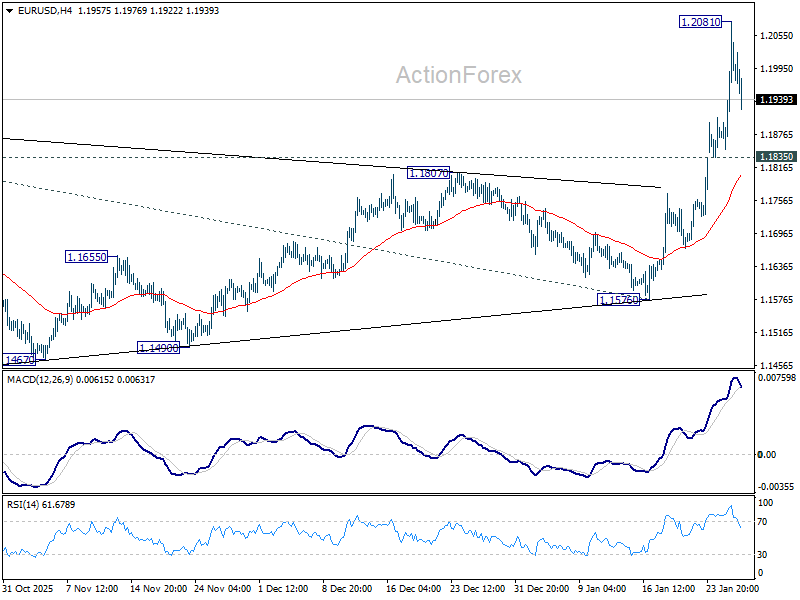

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1902; (P) 1.1992; (R1) 1.2134; More….

A temporary top is formed at 1.2081 in EUR/USD with current retreat. Intraday bias is turned neutral for consolidations. Downside should be contained by 1.1835 support. Decisive break above 1.2 will carry larger bullish implications. Next near term target will be 38.2% projection of 1.0176 to 1.1917 from 1.1576 at 1.3434. However, break of 1.1835 will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, as long as 55 W EMA (now at 1.1443) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

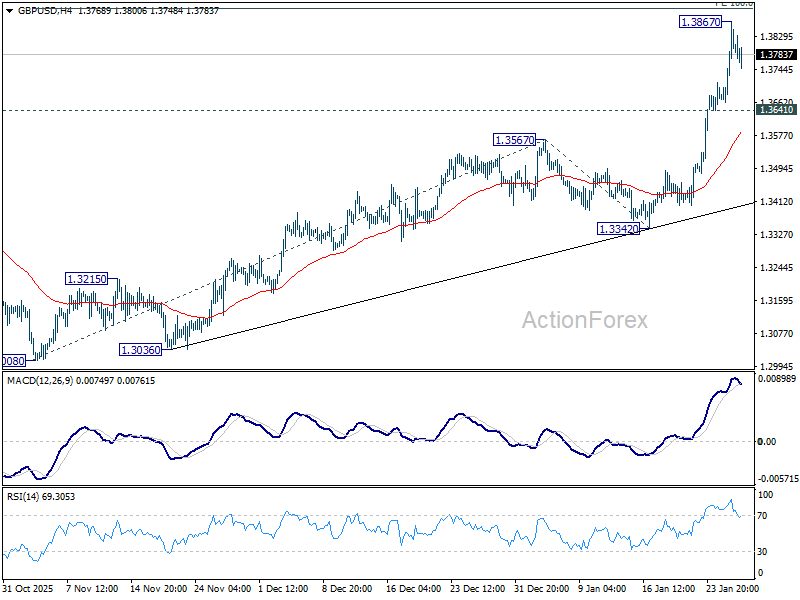

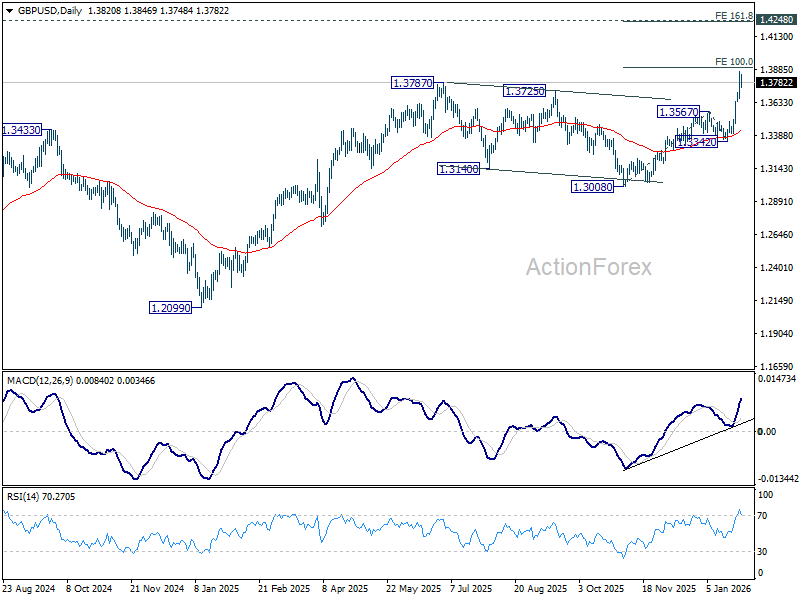

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3719; (P) 1.3794; (R1) 1.3923; More...

A temporary top was formed at 1.3867 with current retreat, and intraday bias is turned neutral in GBP/USD first. Downside of consolidations should be contained by 1.3641 to bring another rally. Firm break of 100% projection of 1.3008 to 1.3567 from 1.3342 at 1.3901 will pave the way to 161.8% projection at 1.4246, which is close to 1.4248 key structural resistance. However, break of 1.3641 will turn bias to the downside for deeper pullback.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

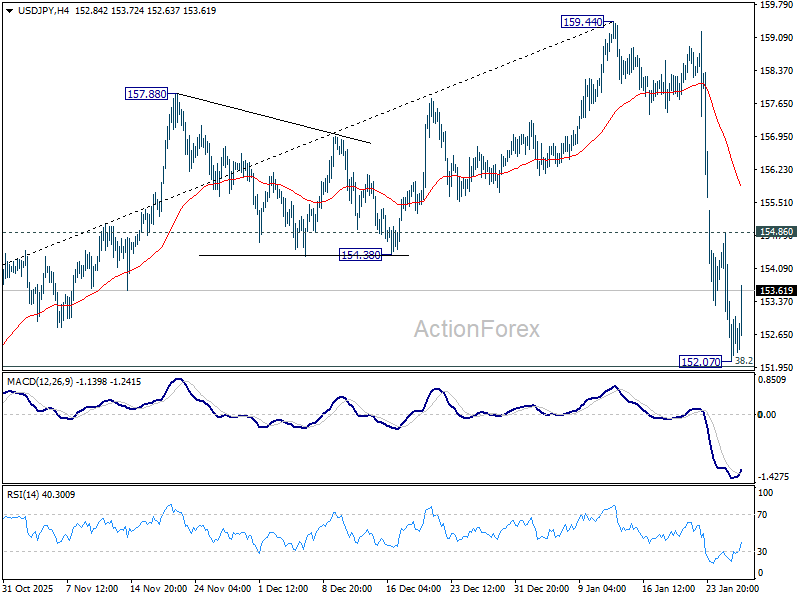

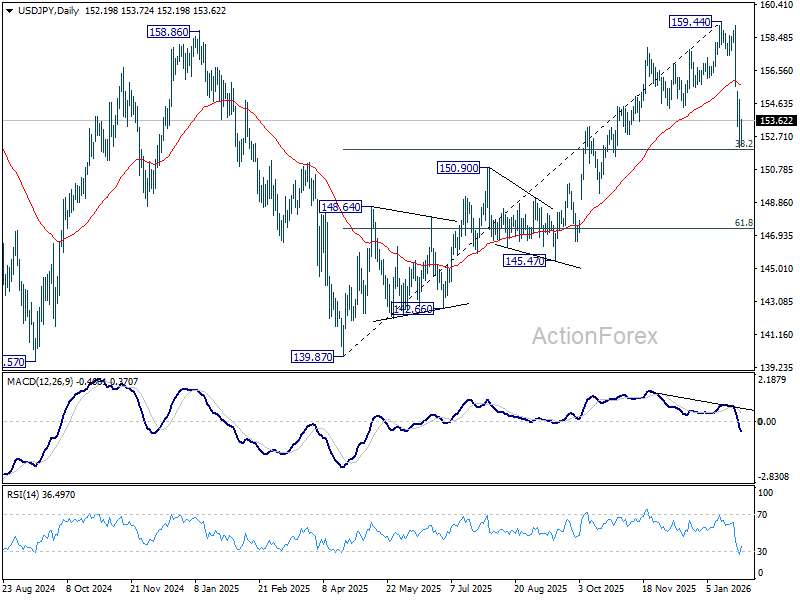

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.25; (P) 153.06; (R1) 154.04; More...

Intraday bias in USD/JPY stays neutral first. As noted before, fall from 159.44 is seen as correcting the rise from 139.87. Strong support should be seen from 38.2% retracement of 139.87 to 159.44 at 151.96 to bring rebound, at least on first attempt. On the upside above 154.86 minor resistance will turn intraday bias to the upside for recovery. However, decisive break of 151.96 will argue that it is reversing whole rise from 139.87. Deeper decline would then be seen to 61.8% retracement at 147.34.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.35) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

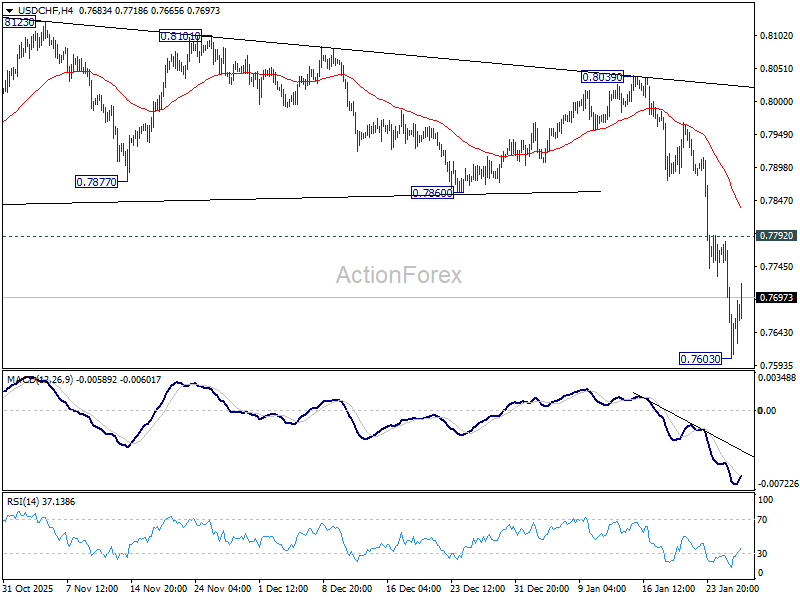

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7550; (P) 0.7667; (R1) 0.7730; More….

A temporary low is formed at 0.7603 in USD/CHF with current recovery and intraday bias is turned neutral first. Outlook will stay bearish as long as 0.7792 resistance holds Break of 0.7603 will resume the larger down trend to 0.7382 projection level next. However, firm break of 0.7792 will turn bias back to the upside, for stronger rebound to 0.7860 support turned resistance.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

Bessent’s Strong Dollar Talk Fails to Convince as Recovery Lacks Conviction

Dollar found modest support in early US trading, managing a mild recovery as markets position cautiously ahead of the Federal Reserve’s rate decision. The move looked more like a pause in selling than a decisive shift in sentiment, with traders reluctant to press positions before policy clarity.

Some stabilization came after comments from US Treasury Secretary Scott Bessent, who reiterated that the US maintains a “strong Dollar policy.” The remarks helped temper immediate nervousness, but failed to materially change the broader tone. That is largely because Bessent’s message stands in clear contrast to President Donald Trump’s comments a day earlier. Trump said Dollar was “doing great” despite sliding more than 10% over the past year, effectively signaling comfort with continued weakness.

As a result, markets have interpreted Bessent’s remarks as an attempt to smooth volatility rather than to reverse the White House’s permissive stance. The comments were seen as damage control, not a policy pivot. Technically, Bessent’s assertion is not entirely inaccurate. With the Dollar Index still hovering around 96, the currency remains well above its cycle lows near 70 seen during the 2008 financial crisis.

But that historical context has done little to inspire fresh Dollar demand. Traders appear fully adept at filtering political rhetoric. Rather than betting on verbal assurances, markets are focused on policy actions and institutional signals, leaving Bessent’s comments with limited traction.

Attention now turns to the Fed. Rates are widely expected to be held at 3.50–3.75%, making the decision itself largely a non-event. The real focus will be on the statement language and Jerome Powell’s press conference. The base case remains an easing bias framed within a wait-and-see stance. The Fed’s latest dot plot points to one rate cut this year, making a cautious tilt toward easing a logical extension of current guidance.

Still, a more non-committal tone cannot be ruled out. Solid pockets of economic data, still-elevated inflation, and renewed trade threats involving Europe and Canada give policymakers reason to retain flexibility rather than pre-commit.

That nuance matters politically. Even a straightforward hold is likely to draw renewed criticism from Trump. Any shift toward a more neutral or less dovish bias would almost certainly provoke sharper attacks, further testing perceptions of Fed independence. Against that backdrop, outcomes and market reactions remain highly fluid.

In FX performance terms, the picture remains unfavorable for Dollar. For the week so far, it is the worst-performing major, followed by Sterling and Euro. Yen leads, followed by Aussie and Kiwi. Loonie sits mid-pack after the BoC held rates and maintained a neutral stance. Swiss Franc has drifted back toward the middle as risk sentiment modestly improves.

BoC holds at 2.25%, US trade risk as key source of vulnerability

The BoC left its policy rate unchanged at 2.25%, in line with expectations, and reiterated a neutral bias. The Governing Council said the current setting “remains appropriate,” conditional on the economy evolving broadly in line with its outlook.

The Bank judged that the outlook for both the global and Canadian economies is little changed from the October MPR. However, it cautioned that the balance of risks remains tilted by external factors, particularly “unpredictable US trade policies and geopolitical risks.”

Near-term growth is expected to remain "modest". Growth forecasts were left broadly unchanged, with GDP expected to expand 1.1% in 2026 and 1.5% in 2027. A major source of uncertainty remains the upcoming review of the Canada-US-Mexico Agreement, which could materially affect trade flows and investment decisions. On inflation, the BoC expects price growth to stay close to its 2% target over the projection horizon.

Australia CPI surges to 3.6% in Q4, 3.8% in December

Australia’s Q4 CPI showed little relief for RBA where it matters most for policy. Headline inflation rose 0.6% qoq, slightly below expectations of 0.7% and slowing sharply from the prior quarter’s 1.3% gain. However, on an annual basis, CPI accelerated from 3.2% yoy to 3.6% yoy, matching forecasts and keeping inflation well above the RBA’s target band.

The more important signal came from underlying inflation. Trimmed mean CPI rose 0.9% qoq, easing marginally from 1.0% previously but beating expectations of 0.8%. Annual trimmed mean inflation climbed from 3.0% yoy to 3.4% yoy, above the expected 3.2%, reinforcing concerns that price pressures remain persistent.

December’s monthly details added to that unease. Headline CPI jumped 1.0% mom, lifting the annual rate from 3.5% yoy to 3.8%, both above expectations. Trimmed mean CPI rose a more modest 0.2% mom, but annual core inflation still edged up from 3.2% yoy to 3.3% yoy.

Price pressures remain broad in December. Goods inflation accelerated from 3.2% yoy to 3.4%, driven largely by a 21.5% surge in electricity prices. Services inflation climbed from 3.6% yoy to 4.1%, led by domestic travel and accommodation and rising rents.

Markets are now firming up their expectation that RBA will return to rate hike in February.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7550; (P) 0.7667; (R1) 0.7730; More….

A temporary low is formed at 0.7603 in USD/CHF with current recovery and intraday bias is turned neutral first. Outlook will stay bearish as long as 0.7792 resistance holds Break of 0.7603 will resume the larger down trend to 0.7382 projection level next. However, firm break of 0.7792 will turn bias back to the upside, for stronger rebound to 0.7860 support turned resistance.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

BoC holds at 2.25%, US trade risk as key source of vulnerability

The BoC left its policy rate unchanged at 2.25%, in line with expectations, and reiterated a neutral bias. The Governing Council said the current setting “remains appropriate,” conditional on the economy evolving broadly in line with its outlook.

The Bank judged that the outlook for both the global and Canadian economies is little changed from the October MPR. However, it cautioned that the balance of risks remains tilted by external factors, particularly “unpredictable US trade policies and geopolitical risks.”

Near-term growth is expected to remain "modest". Growth forecasts were left broadly unchanged, with GDP expected to expand 1.1% in 2026 and 1.5% in 2027. A major source of uncertainty remains the upcoming review of the Canada-US-Mexico Agreement, which could materially affect trade flows and investment decisions. On inflation, the BoC expects price growth to stay close to its 2% target over the projection horizon