Sample Category Title

Euro Area Consumer Confidence, a Missing Key to Future Growth

In focus today

In the euro area, we monitor the October consumer confidence indicator. Confidence has remained low over the past half year likely due to geopolitical tensions and rising food prices. The weak confidence is hurting private consumption which remains low despite improving real incomes. Normalising consumer confidence will thus be key for the growth outlook in order for households to lower their elevated savings rate and drive consumption.

In Norway, wage growth appears to have slowed in Q3 from elevated levels close to 6% in Q2. Today, the September figures will confirm whether this trend continued or not. High wage growth remains a major concern for Norges Bank due to the risk of persistently high inflation, so further slowdown is a necessary condition for Norges Bank to deliver rate cuts next year. Also keep an eye on the LFS figures to see if the rise in unemployment continues.

Economic and market news

What happened overnight

In the Ukraine war, the US hit Russia with sanctions on Rosneft and Lukoil, two of Russia's largest oil companies. The sanctions come just after the summit between US President Trump and Russian President Putin was cancelled yesterday. The tariffs were announced as an effort to damage Moscow's ability to fund its war machine and also mark the first cost imposed by the Trump administration on Russia over the war. Oil prices rose immediately following the announcement. This move is adding fuel to the fire and comes just after the EU approving the 19th package of sanctions, which include a ban on Russian liquefied natural gas imports.

What happened yesterday

In the UK, September inflation surprised significantly to the downside. Headline inflation came in at 3.8% y/y (cons: 4.0%, prior: 3.8%), core at 3.5% (cons: 3.7%, prior: 3.6%) and importantly, services at 4.7% (cons: 4.9%, prior: 4.7%). The momentum slowed across categories, and the print was also below the BoE's expectations from the latest MPR in August, where it had headline at 4.0%. Following last week's downside surprise to wage growth and the lower-than-expected inflation, markets have increased their expectations for rate cuts from the BoE, pricing 9bp for the November meeting and 60bp for the coming 12 months.

In the EU, trade Chief Maros Sefcovic announced an urgent meeting with the Chinese Commerce Minister to address the rare earth export controls as well as the recent fallout over the chipmaker Nexperia, which was owned by a Chinese company until the Dutch government took control last week.

In China, more than 170 foreign companies gathered for a meeting with Vice Commerce Minister Ling Ji, where he aimed to clarify that the country's new rare earth export controls are not intended to obstruct regular trade. During the meeting Ling Ji said: "China will continue to approve legitimate transactions according to law and work to maintain the stability of global supply chains".

Equities: Equities traded lower yesterday, though without any clear macro or geopolitical trigger to justify the move. In the absence of major data releases, one might have looked to earnings for direction, yet it is hard to see why results should have prompted such a negative reaction. The move instead looked more like a defensive rotation following the strong run we have seen over recent months in cyclicals. The energy sector outperformed after the US announced new Russian sanctions. In the US yesterday, Dow -0.7%, S&P 500 -0.5%, Nasdaq -0.9% and Russell 2000 -1.5%. In Asia overnight, markets followed Wall Street lower, with most indices in the red, particularly the more tech-heavy ones. Futures in Europe and the US are largely unchanged this morning.

FI and FX: Risk sentiment turned sour after reports that the Trump administration is considering new restrictions on software exports to China, adding to trade uncertainty, while corporate earnings continued to underwhelm. US Treasury yields were little changed, slipping 1-2bp across the curve. In the euro area, price action was muted, with front-end Bund yields unchanged, while the long end edged 1-2bp higher in a mild bear-steepening move. EUR/USD is consolidating around 1.16 in a quiet session; with the broad USD little changed amid a lack of fresh catalysts. GBP faced significant headwinds during yesterday's session as September inflation surprised to the downside. USD/JPY has generally extended its upward trend over the past month, with JPY broadly underperforming across G10. Both EUR/SEK and EUR/NOK extended their declines again yesterday, especially NOK FX had a strong day yesterday reflecting the rise in global energy prices incl. oil.

Uneasy Ground

Trade worries resurfaced yesterday — yes, resurfaced instead of easing — after reports that the Trump administration is considering new restrictions on software exports to China. Are we surprised? Not really. These on-and-off headlines have been circulating for nearly a year, repeatedly injecting short-term anxiety into the markets. That’s exactly what happened yesterday: major US indices retreated, led by technology names. Headlines could turn better anytime, or worsen.

Netflix’s 10% plunge following disappointing quarterly results didn’t help sentiment. Still, since Netflix isn’t an AI play, its earnings story remains fairly isolated and shouldn’t impact broader appetite for AI-related stocks — the key driver behind the US market’s rally.

Elsewhere in earnings, Tesla missed expectations despite record sales. The record, however, was largely due to buyers rushing to purchase EVs before the end of federal subsidies — a one-off jump unlikely to prevent Tesla from posting a second consecutive annual sales decline. Profits plunged as operating expenses rose by roughly 50%, partly due to higher costs linked to renewed trade duties, estimated at around $400 million. While Musk continues to shift focus toward AI, humanoid robots and robotaxis, those ventures won’t offset the decline in EV revenues anytime soon. And this time, unlike the previous earnings announcements, investors weren’t entirely convinced by the latest pitch, and Tesla shares dropped 3.8% in after-hours trading.

Looking at the chart, Tesla has been on a wild ride since the elections. The EV business has been under pressure for over a year and is far from delivering the 50% annual growth Musk once promised. After last year’s US elections and Musk’s alignment with Trump, the stock rose — but when that relationship cooled, it fell again. Despite a recent rebound, Tesla’s valuation remains lofty: its P/E ratio is above 300, versus around 33 for the Magnificent 7. For Tesla to justify that premium, it needs tangible progress in robotaxis, robotics and AI — but the “Musk risk” makes it a very different bet from other tech giants.

The good news is that neither Tesla nor Netflix meaningfully shifts the broader AI-driven narrative that continues to steer the major US indices. Futures point to a modest rebound this morning, suggesting sentiment remains intact despite lingering trade, geopolitical and credit risks.

Turning to geopolitics, the EU has approved its 19th sanctions package against Russia, while the US announced new sanctions on Rosneft and Lukoil — two Russian oil giants — pushing US crude prices back above $60 per barrel this morning. Such geopolitical headlines tend to generate short-term price moves, and tactical long positions may encounter resistance near $62–62.50, where the 23.6% Fibonacci retracement of the June–October selloff and the 50-DMA converge. The medium-term outlook for oil remains somewhat bearish given uncertain global demand and abundant supply. Upcoming Federal Reserve (Fed) rate cuts and a softer US dollar should, in theory, help establish a floor under oil prices, alongside rising energy needs tied to AI and data infrastructure. Yet, oil bulls have struggled to gain traction on these arguments, and speculative long positions are retreating. Any recovery is therefore likely to remain short-lived, with the medium-term bias staying bearish below the $65 level — the 38.2% Fibonacci retracement of the summer decline.

On credit, concerns about bad loans that surfaced last week have eased, as several US regional banks reported no new cases in their quarterly updates. That’s a relief, but the recent stress serves as a reminder that credit conditions remain fragile. PrimaLend Capital Partners — a subprime auto lender that finances buy-here-pay-here car dealerships — filed for bankruptcy. The case underscores growing strain among low-income US consumers, who are falling behind on car payments at the highest rate in decades.

The bottom line is that we know the stock market’s performance doesn’t fully reflect the underlying US economy (if any at all). Growth remains heavily supported by massive AI investment, while the labour market is weakening. Things could get worse before they improve, with many federal employees expected to miss paychecks next month amid a government shutdown that’s now on track to become the second longest in history.

These conditions are clearly paving the way for Fed intervention — provided inflation doesn’t reaccelerate. We’ll get more clarity on that front Friday, but the US 2-year yield, which best captures rate expectations, suggests investors are pricing in at least two rate cuts over the next two Fed meetings — a setup that, in itself, remains supportive of risk appetite.

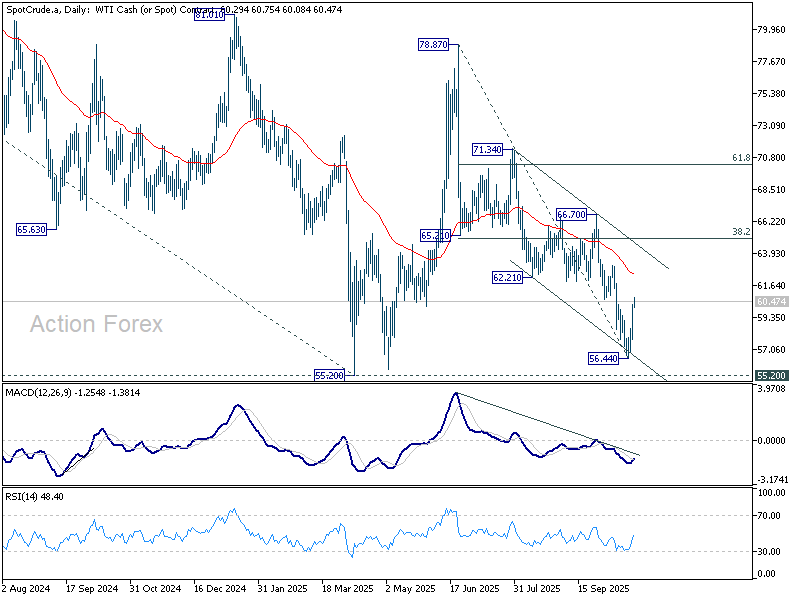

WTI climbs Past 60 after US sanctions on Russia Fall from 78.87 run its course?

Oil prices rebounded sharply today, with WTI crude rising back above the 60 mark, as geopolitical tensions re-entered focus after the Trump administration imposed new sanctions on Russia’s two largest oil producers, Rosneft and Lukoil.

The U.S. Treasury said the move was in response to Moscow’s “lack of serious commitment” to a peace process to end the war in Ukraine. Announcing the sanctions, Treasury Secretary Scott Bessent said “now is the time to stop the killing and for an immediate ceasefire,” warning that Washington is prepared to “take further action if necessary.” He urged U.S. allies to join in applying pressure on Moscow. Reports suggested that the new round of sanctions followed the collapse of a planned Trump–Putin meeting in Budapest, which had raised hopes for progress toward de-escalation.

The sanctions created a short-covering wave across crude futures, helping oil snap its recent losing streak. While demand signals remain mixed, the reemergence of supply-side uncertainty has stabilized sentiment, halting a multi-week slide that had dragged prices persistently.

Technically, the rebound has taken on added significance. The firm break above 59.47 resistance confirms that a short-term bottom has likely formed at 56.44, accompanied by bullish convergence in 4H MACD after testing the channel floor.

The focus now shifts to whether the fall from 78.87 has completed as a corrective move as second leg of the broader pattern from 55.20 (2025 low made in April).

In either case, further gains are favored toward key resistance zone between 62.21 support turned resistance and 55 EMA (now at 62.46). Sustained break above this area would strengthen the case for near-term bullish reversal, opening the way to 38.2% retracement of 78.87 to 56.44 at 65.00.

However, failure to clear this zone would suggest the rebound remains corrective, keeping risks skewed toward another dip back toward 55.20 before a more durable bottom forms.

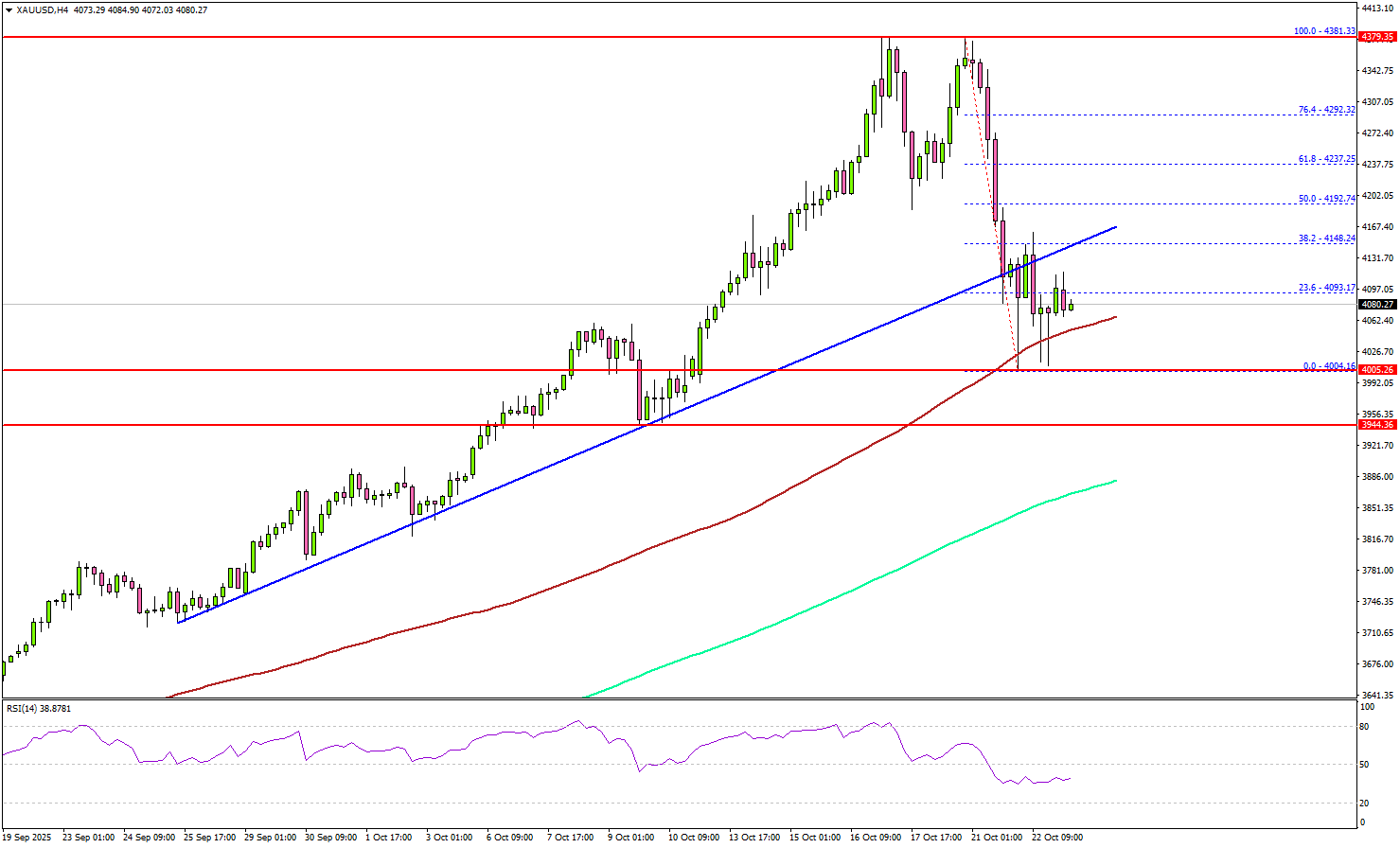

Gold Retreats From All-Time High — Market Awaits Next Catalyst For Direction

Key Highlights

- Gold extended its rally and traded to a new record high above $4,380 before correcting lower.

- It traded below a key bullish trend line with support at $4,120 on the 4-hour chart.

- WTI Crude Oil prices could struggle to recover above $60.00.

- EUR/USD is again moving lower below 1.1650 and 1.1620.

Gold Price Technical Analysis

Gold prices formed a base above $4,000 and started a fresh increase against the US Dollar. It cleared many hurdles near $4,150 and $4,250.

The 4-hour chart of XAU/USD indicates that the price settled above the $4,000 level, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours). The upward move was such that the price spiked above $4,350.

Gold traded to a new record high near $4,381 before the bears took a stand. There was a sharp downside correction below $4,200. The price traded below a key bullish trend line with support at $4,120.

It tested $4,000 and is currently consolidating losses. On the upside, immediate resistance is near the $4,150 level. The next major resistance sits near the $4,180 level.

A clear move above $4,180 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $4,250, above which the price could rally toward the milestone level of $4,350.

On the downside, initial support is near the $4,000 level. The first key support is $3,945. The next major support is near the $3,850 level. A downside break below $3,850 might call for more downsides. The next key zone to watch could be $3,750.

Looking at WTI Crude Oil, the price attempted a decent recovery wave, but the bears remained active below the $60.00 level.

Economic Releases to Watch Today

- US Initial Jobless Claims - Forecast 227K, versus 218K previous.

- US New Home Sales for Sep 2025 (MoM) – Forecast +2.9% versus +20.5% previous.

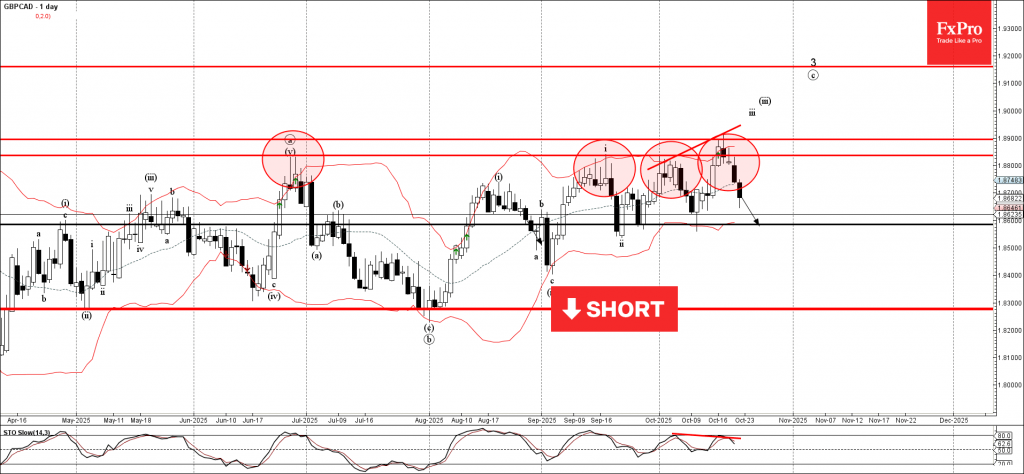

GBPCAD Wave Analysis

GBPCAD: ⬇️ Sell

- GBPCAD reversed from resistance area

- Likely to fall to support level 1.8600

GBPCAD currency pair recently reversed down from the resistance area located between the resistance levels 1.8835 and 1.8900 (which has been reversing the price from June).

The downward reversal from this resistance area formed the daily Japanese candlesticks reversal pattern Dark Cloud Cover – which started the active downward correction.

Given the strength of the nearby resistance area and the bearish divergence on the daily Stochastic indicator, GBPCAD cryptocurrency can be expected to fall to the next support level 1.8600.

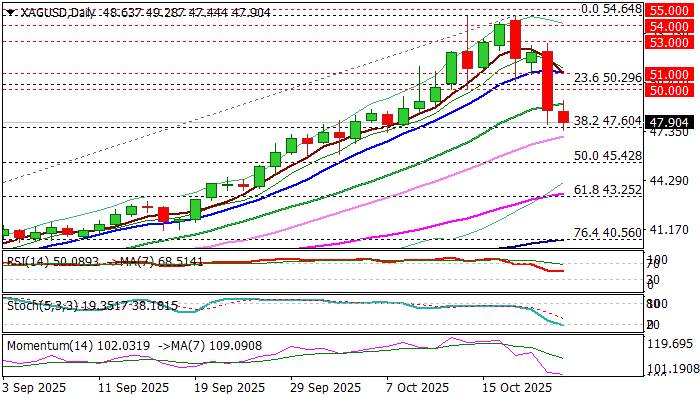

Silver: Sharp Pullback May Extend as Near-Term Sentiment Negative

Silver stabilized after finding temporary footsteps at important Fibo support at $47.60 (38.2% retracement of $36.20/$54.64 rally).

Fresh bears take a breather after massive loss on Tuesday, when the metal’s price fell 7%, in the biggest daily drop since 11 Aug 2020.

Pullback from new record high ($54.64) started on Friday and accelerated on Tuesday, as traders opted for more aggressive profit-taking, dragged by strong pullback of gold price and stronger dollar.

Change in key fundamental factors, such as lower demand from India and restored supply, that would help renewing stocks, recently used due to supply shortage, eased upside pressure and shifted near term sentiment into opposite direction for now.

Strong acceleration on Tuesday broke the most significant support at $50 zone (psychological / former record highs of 1980 and 2011) signaled deeper correction.

Although the latest pullback was significant and weakened near term structure, larger picture still shows strong uptrend in play, with current action to be described as a healthy correction which would provide better levels to re-enter broader bullish market.

The Fibo support at $47.60 is reinforced by daily Kijun-sen and should ideally contain dips, but consolidation attempts were so far fragile and signal that the downside remains vulnerable.

Violation of $47.60 to unmask $45.42 (50% retracement of $36.20/$54.64) and rising 55DMA ($43.44) above which extended dips should find firm ground.

Broken 20DMA marks initial resistance ($49.14), with near-term action expected to remain biased lower while broken $50 pivot (now acting as solid resistance) caps upticks.

Res: 49.14; 50.00; 50.30; 51.00

Sup: 47.01; 45.90; 45.42; 43.65

DAX Extends Gains in Five Wave Diagonal Formation

The short-term Elliott Wave analysis for the DAX Index indicates it is nearing the completion of a cycle from its April 2025 low, unfolding as wave (5). From the June 19 low, wave (5) has developed as an ending diagonal Elliott Wave structure. The rally from this low saw wave 1 peak at 24639.1, followed by a wave 2 pullback concluding at 23284.67. The Index then advanced in wave 3, structured as a five-wave impulse. From the wave 2 low, wave ((i)) reached 23785.24, with a corrective dip in wave ((ii)) at 23383.84. The subsequent wave ((iii)) climbed to 24524.11, followed by a wave ((iv)) retracement to 24269.94. The final wave ((v)) culminated at 24771.34, completing wave 3.

Wave 4 unfolded as a double zigzag structure. From the wave 3 high, wave ((w)) declined to 23986.93, wave ((x)) rebounded to 24339.27, and wave ((y)) fell to 23682.73, finalizing wave 4. The Index has since turned upward in wave 5. From the wave 4 low, wave ((i)) reached 24384.24. A wave ((ii)) pullback is expected to correct the cycle from the October 17 low before the Index resumes its ascent. As long as the pivot at 23682.73 holds, pullbacks should attract buyers in a 3, 7, or 11 swing, supporting further upside in the near term.

DAX Latest 1-Hour Elliott Wave Chart From 10.23.2025

DAX Elliott Wave Video:

https://www.youtube.com/watch?v=lL7FHkTe5tI

Sunset Market Commentary

Markets

UK gilts rally, outperforming their US and European peers dramatically in the process. British yields drop between 8.1 and 8.9 bps after sub-consensus inflation numbers. September headline CPI flatlined on a monthly basis and caused the annual print to match August’s 3.8%. The Bank of England for the last couple of months had been warning for inflation to peak last month at 4% before disinflation would kick in again. The current 3.8% in other words means a better starting point. Core inflation unexpectedly eased to 3.5% from 3.6% and services CPI defied expectations for an acceleration to 4.8% by coming in at 4.7%, the same as in August. Producer price inflation gauges also came in below analyst estimates. The price report is a sigh of relief, including for the Bank of England. The central bank is torn between supporting the economy through rate cuts and stubborn above-target inflation. Since it last cut rates back in August the BoE started floating the possibility of going even slower than the quarterly pace it followed until then. Markets dramatically reduced bets for a November 6 reduction to near zero in response. That’s now going in reverse: the market implied probability shot higher to 35% currently. Governor Bailey will be the swing vote in a split MPC. The sharp yield drop is a boon for UK’s dire public finances too. Depending on the cut-off used by the Office of Budget Responsibility in drafting the pre-Autumn Budget forecast, estimates (Bloomberg) of borrowing cost savings vary between £2 and £4.5bn. When looking for money to fill a £35bn fiscal hole, every bit counts. Cratering yields weigh on GBP but it could have been a lot worse. EUR/GBP bounced to 0.871 before halving those gains. The euro himself isn’t exactly showcasing strength. EUR/USD drifts further south with the 1.16 big figure again at risk of being lost. The US dollar remains the better bid currency against most major peers. DXY is back above 99. Precious metals remain in the defensive. Gold and silver’s pullback continues, extending yesterday’s slide. Stock markets are taking a breather near the record highs. Decent-to-strong corporate earnings have supported the recent upleg. Markets are now eyeballing the next batch from bellwethers such as Tesla & Alcoa (after-market).

News & Views

The monthly consumer confidence report published by the National Bank of Belgium today, showed the overall confidence level continuing its upward trajectory. At 0 (up from -1) the index reached the best level for 2025. The move was mainly due to a sharp decline in consumers’ fears about unemployment. The subindex improved from 2 to -6, the best level since January 2018. The improved in expectations on unemployment offset greater pessimism concentrating the economic situation in the country (-27 from -23). On a personal level, households have slightly downgraded their expectations regarding their own financial situation (-2 from 0) and they intend to save a little more 23 from 22).

Consumer price inflation in South Africa in September rose slightly by 0.2% M/M and 3.4% Y/Y (from -0.1% and 3.3% in August). Core inflation (excluding food & non-alcoholic beverages, fuel and energy) also rose 0.3% M/M and 3.2% Y/Y (from 0.1% M/M and 3.1% Y/Y). Goods inflation eased from 3.1% Y/Y to 2.9%, but services inflation accelerated from 3.6% to 3.9%. In its September monetary policy statement, the South Africa Reserve Bank (SARB) indicated that it expected the inflation rate to rise to 4% over the next few months. Overall, it expected headline inflation to average 3.4% this year, and 3.6% next year, before reverting to 3% during 2027. In its assessment it saw higher electricity prices as well has upwardly revised food and services prices. This was partially offset by a stronger exchange rate assumption. In September, the SARB paused its easing cycle, leaving the policy rate at 7% as it wanted to see the impact of the previous 125 bps of rate cuts over the previous year. As the SARB aims to bring inflation to the bottom of the 3-6% official target range, current inflation development only leaves room for very gradual policy easing going forward. The rand today eases modestly to USD/ZAR 17.425. The USD/ZAR cross rate earlier this month touched 17.07, coming close to the 2024 low (high for the rand).

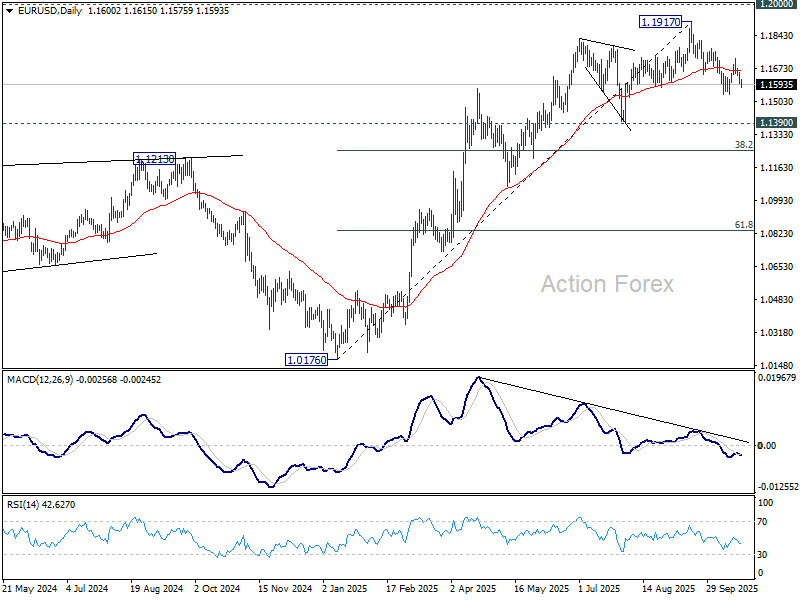

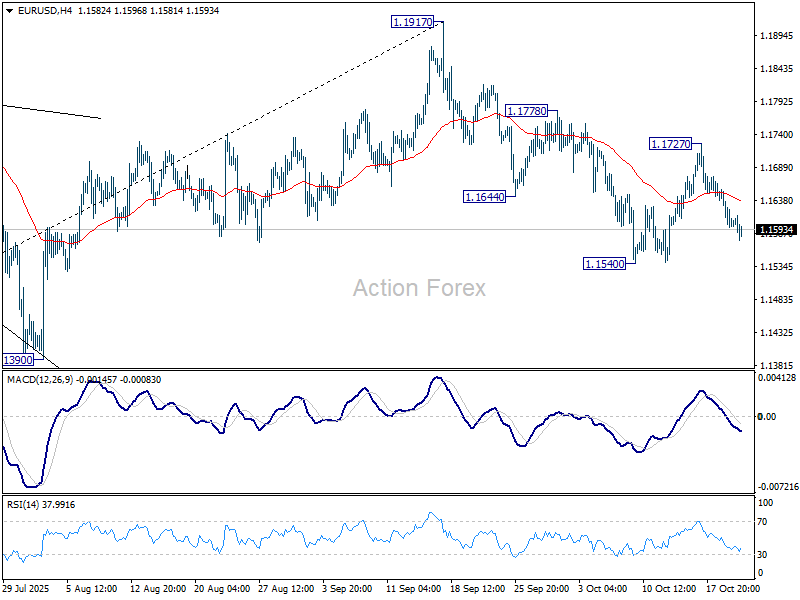

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1580; (P) 1.1618; (R1) 1.1637; More…

Intraday bias in EUR/USD remains neutral and further decline is expected. Break of 1.1540 will resume the fall from 1.197 to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1290) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.