Sample Category Title

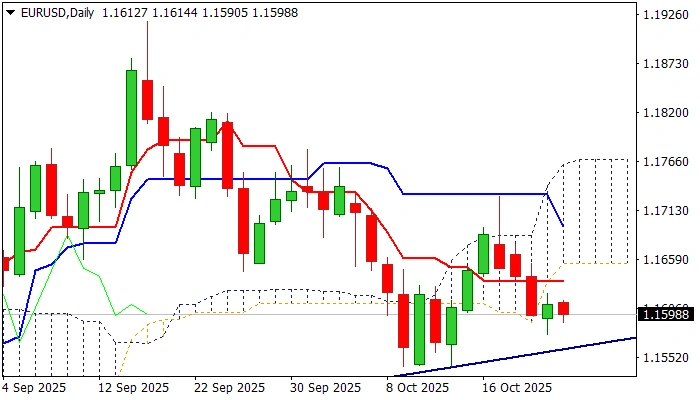

EUR/USD Mid-Day Outlook

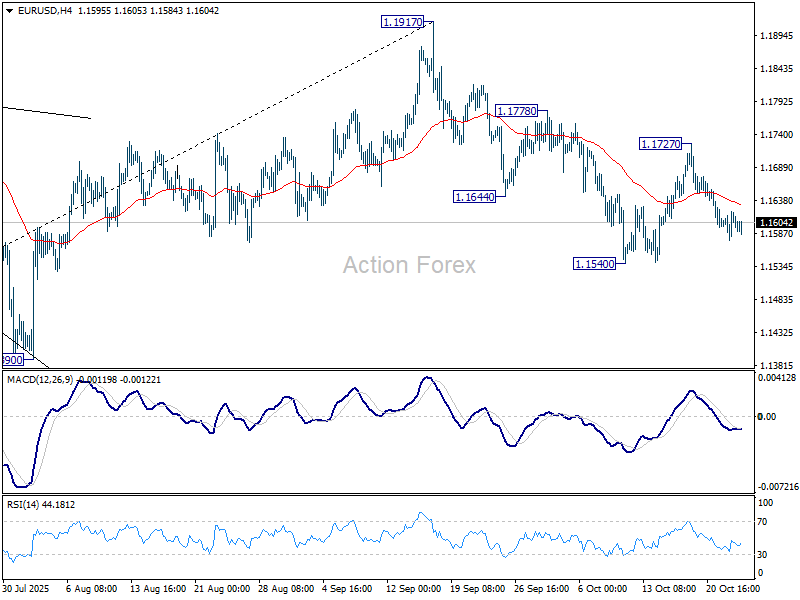

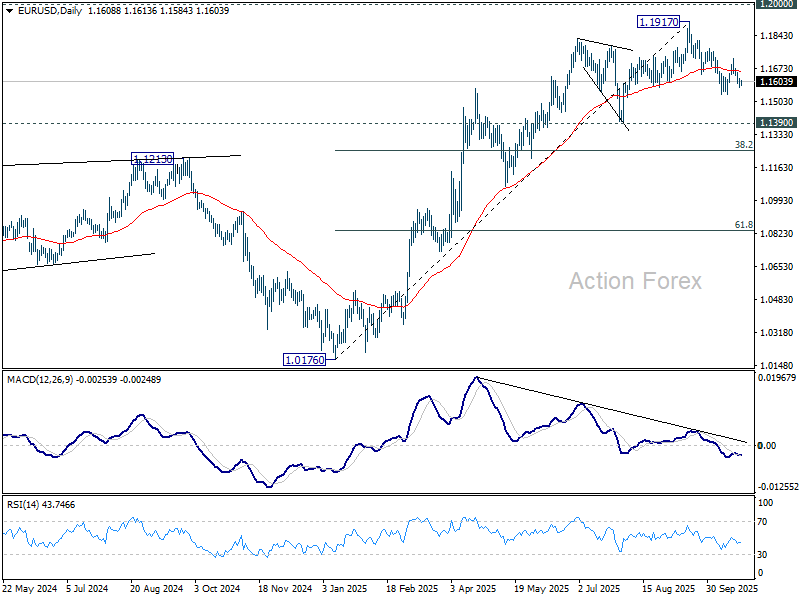

Daily Pivots: (S1) 1.1584; (P) 1.1603; (R1) 1.1629; More…

Outlook in EUR/USD is unchanged. Intraday bias stays neutral, and further decline is expected with 1.1727 resistance intact. Break of 1.1540 will resume the fall from 1.1917 to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1290) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

Geopolitics Back in Play as Oil Surges on Fresh Sanctions Against Russia

Oil prices surged today, emerging as the clear focus in otherwise subdued global markets, as geopolitical tensions flared again following a fresh wave of Western sanctions against Russia. The U.S. announced new measures targeting energy giants Rosneft and Lukoil, accusing Moscow of prolonging the conflict in Ukraine. The decision reignited fears of tighter global supply, prompting a strong rebound in crude prices.

Together, Rosneft and Lukoil account for nearly half of Russia’s crude exports, which exceed four million barrels per day. The sanctions effectively restrict these companies from accessing Western financial channels and trading networks, raising questions about how quickly buyers can adapt. The move could trigger short-term disruptions in global flows, particularly given the heavy reliance of Asian refiners in China and India on Russian crude.

In practical terms, the sanctions will force Chinese and Indian refineries to seek alternative suppliers to avoid secondary penalties and maintain access to international banking systems. Both countries could pivot more heavily toward U.S. and OPEC producers, which still have spare capacity to fill part of the gap — particularly Saudi Arabia. However, the redirection of demand toward non-sanctioned barrels will likely drive broader upward pressure on global oil prices.

The U.S. action follows the U.K.’s sanctions last week on the same Russian firms, underscoring a coordinated Western push to tighten the noose on Russia’s energy sector. Meanwhile, the European Union approved its 19th sanctions package, which includes a ban on Russian LNG imports and potentially a new plan to use frozen Russian assets to fund Ukraine over the next two years. The measures mark a further escalation of economic pressure just as Western leaders seek to reaffirm long-term support for Kyiv.

In currency markets, performance diverged along familiar lines. Aussie leads gains for the week so far, followed by Kiwi and Loonie. In contrast, Yen extended its slide, while Swiss Franc and Euro also weakened. Sterling and Dollar traded in the middle.

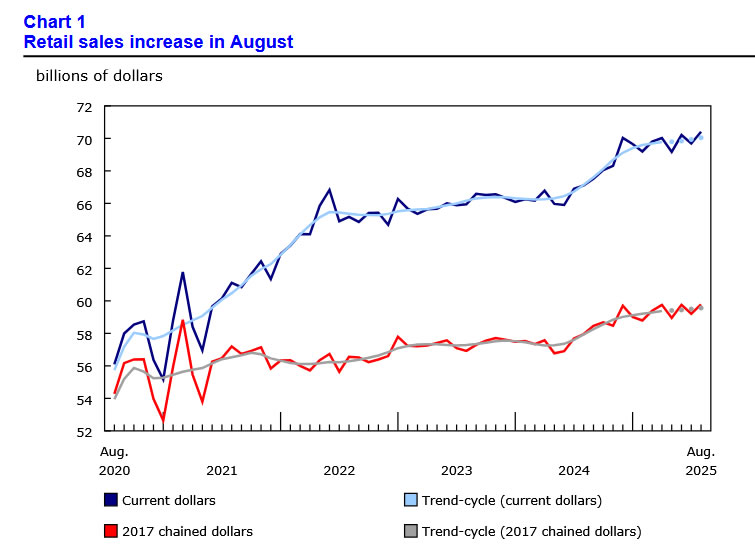

Canada retail sales rise 1.0% mom in August, but early data point to September dip

Canada’s retail sales grew 1.0% mom in August to CAD 70.4B, in line with market expectations, driven largely by strength in motor vehicle and parts dealers. Gains were recorded in six of nine subsectors, underscoring still-solid consumer activity despite higher borrowing costs.

Excluding volatile components such as autos and fuel, core retail sales rose an even stronger 1.1% mom, suggesting a firm base of household spending momentum through late summer.

However, the outlook for the following month looks weaker. Statistics Canada’s advance estimate pointed to a -0.7% mom decline in September sales, hinting at some loss of momentum heading into the fourth quarter.

SNB minutes: Price stability intact, no threat of lasting deflation

The SNB reaffirmed its accommodative stance in the summary of its September policy meeting, noting that inflation is expected to remain comfortably within the range consistent with price stability. The Governing Board discussed the outlook in detail with experts, concluding that “all available information points to inflation remaining within the range consistent with price stability” and that it is “not expected to become persistently negative.”

While price pressures remain subdued, policymakers highlighted a rising degree of external uncertainty, particularly stemming from U.S. trade policy. The SNB warned particularly that tariffs on pharmaceutical products — one of Switzerland’s key export sectors — could weigh on GDP in both the short and medium term. The extent of the drag, however, remains uncertain and will depend on how global supply chains and exchange rates evolve. Large currency swings were cited as a key risk factor for the inflation outlook.

The Governing Board noted that monetary policy remains "expansionary", with the full effects of previous easing still filtering through the economy. Despite weak inflationary pressure and a modest deterioration in the growth outlook, policymakers believe the current stance is supporting a gradual rise in prices and providing essential backing for domestic activity.

Given this backdrop, the SNB concluded that “a further easing of monetary policy was not appropriate.” The conditional inflation forecast and the overall growth assessment justify holding rates steady, and the policy rate was left unchanged at 0%.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1584; (P) 1.1603; (R1) 1.1629; More…

Outlook in EUR/USD is unchanged. Intraday bias stays neutral, and further decline is expected with 1.1727 resistance intact. Break of 1.1540 will resume the fall from 1.1917 to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1290) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

Canada retail sales rise 1.0% mom in August, but early data point to September dip

Canada’s retail sales grew 1.0% mom in August to CAD 70.4B, in line with market expectations, driven largely by strength in motor vehicle and parts dealers. Gains were recorded in six of nine subsectors, underscoring still-solid consumer activity despite higher borrowing costs.

Excluding volatile components such as autos and fuel, core retail sales rose an even stronger 1.1% mom, suggesting a firm base of household spending momentum through late summer.

However, the outlook for the following month looks weaker. Statistics Canada’s advance estimate pointed to a -0.7% mom decline in September sales, hinting at some loss of momentum heading into the fourth quarter.

EUR/USD: Bearish Bias Below Daily Cloud

The Euro eased on Thursday morning and signal that near-term bears off 1.1728 (Oct 17 lower top) are regaining control after limited and short-lived recovery attempts on Wednesday.

The price has established below relatively thick daily Ichimoku cloud which continues to weigh on near-term action, after Wednesday’s bounce attempts stalled under initial barriers at 1.1631/35 (Fibo 23.6% of 1.1918/1.1542 / daily Tenkan-sen) guarding cloud base (1.1655).

Negative daily studies (14-d momentum moves deeper in the negative territory, RSI at 42 and MA’s in full bearish setup) contribute to scenario of probe through trendline support (1.1566) and potential retest of daily higher base at 1.1542 (formed in past two weeks).

Firm break here would generate stronger negative signals (bearish continuation on completion of bearish failure swing) and open way towards 1.1400 zone (higher base of late July/early Aug).

Res: 1.1635; 1.1655; 1.1686; 1.1700.

Sup: 1.1566; 1.1542; 1.1500; 1.1391.

XTI/USD Chart Analysis: Oil Prices Rise Following Trump’s Sanctions Decision

According to the XTI/USD chart, WTI crude is now trading above the key psychological level of $60, marking a sharp rebound of over 3% from October’s lows.

The surge came after U.S. President Donald Trump announced sanctions against major Russian oil producers Rosneft and Lukoil, which together account for more than 5 million barrels of oil per day.

The move is expected to reduce global oil supply; however, media outlets point out that:

→ there is no certainty that China and India will refrain from purchasing Russian crude;

→ previous sanctions introduced under the Biden administration — targeting companies such as Gazprom Neft and Surgutneftegaz — had little impact on Russian oil exports.

What could happen next?

Technical Analysis of the XTI/USD Chart

On 20 October, we noted that two descending channels had formed:

→ Red channel – a long-term pattern that developed following the Middle East escalation in June;

→ Purple channel – indicating accelerated downside pressure driven by rising OPEC+ output and hopes for a U.S.–China trade accord.

Our earlier assumption that the market was oversold and that the Falling Wedge pattern might trigger a bullish reversal proved correct (as shown by the arrow). Following the formation of an inverted head and shoulders pattern, oil prices climbed towards the median line of the purple channel.

At this stage, consolidation appears the most likely scenario, as supply and demand may stabilise around the channel’s median. Much will depend on statements from the White House, since higher oil prices could threaten U.S. inflation objectives.

However, if bullish momentum persists, WTI may continue to rise towards the next resistance area, defined by:

→ the upper boundary of the purple channel;

→ the 8–9 October highs, where a false breakout similar to the bear trap seen on 26 September cannot be ruled out.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

SNB minutes: Price stability intact, no threat of lasting deflation

The SNB reaffirmed its accommodative stance in the summary of its September policy meeting, noting that inflation is expected to remain comfortably within the range consistent with price stability. The Governing Board discussed the outlook in detail with experts, concluding that “all available information points to inflation remaining within the range consistent with price stability” and that it is “not expected to become persistently negative.”

While price pressures remain subdued, policymakers highlighted a rising degree of external uncertainty, particularly stemming from U.S. trade policy. The SNB warned particularly that tariffs on pharmaceutical products — one of Switzerland’s key export sectors — could weigh on GDP in both the short and medium term. The extent of the drag, however, remains uncertain and will depend on how global supply chains and exchange rates evolve. Large currency swings were cited as a key risk factor for the inflation outlook.

The Governing Board noted that monetary policy remains "expansionary", with the full effects of previous easing still filtering through the economy. Despite weak inflationary pressure and a modest deterioration in the growth outlook, policymakers believe the current stance is supporting a gradual rise in prices and providing essential backing for domestic activity.

Given this backdrop, the SNB concluded that “a further easing of monetary policy was not appropriate.” The conditional inflation forecast and the overall growth assessment justify holding rates steady, and the policy rate was left unchanged at 0%.

British Pound Extends Its Losses

The pound remains on the back foot against the US dollar, pressured by growing market conviction that the Bank of England (BoE) will sustain its accommodative monetary policy stance for longer than the US Federal Reserve. The latest UK inflation figures showed a noticeable cooling in price pressures, effectively extinguishing expectations of further interest rate hikes from the British central bank.

Conversely, Federal Reserve officials continue to strike a hawkish tone in their public remarks, signalling that US interest rates are likely to remain at elevated levels for an extended period. This policy divergence is bolstering the US dollar's appeal, strengthening its position as a high-yielding, safe-haven asset.

Domestic headwinds are also weighing heavily on sterling. A recent contraction in business activity across both the services and manufacturing sectors (with PMI readings falling below the 50.0 threshold) points to a potential recession in the fourth quarter. Faced with a slowing economy, weakening domestic demand, and persistent cost pressures, the BoE is expected to pause its tightening cycle, leaving the currency vulnerable to further selling.

Compounding these factors, a strong intermarket backdrop for the dollar – characterised by rising US Treasury yields and a strengthening DXY index – is providing both technical and fundamental support for the GBP/USD downtrend.

Technical Analysis: GBP/USD

H4 Chart:

On the H4 chart, GBP/USD has been consolidating around 1.3340. The primary scenario suggests a downward breakout from this range, initiating a third wave of decline towards 1.3213. It is important to note that this is only an intermediate target; the broader bearish wave structure carries a primary objective near the 1.2963 area. This outlook is technically confirmed by the MACD indicator, whose signal line remains below zero and is pointing firmly downward, indicating sustained bearish momentum.

H1 Chart:

The H1 chart shows the market forming the first leg of a broader third wave downward. The immediate downside target is 1.3276. Upon reaching this level, a short-term corrective rebound to at least 1.3330 is possible. Following such a correction, a resumption of the decline towards 1.3240 and 1.3213 is expected, which would likely complete the current wave structure. The Stochastic oscillator corroborates this view; its signal line is below 50 and is trending towards the oversold territory (20), reinforcing the probability of continued downward movement.

Conclusion

The confluence of a dovish BoE policy shift, resilient US hawkishness, and deteriorating UK economic data creates a powerfully bearish environment for Sterling. Technically, the path of least resistance is firmly to the downside, with key targets established at 1.3213 and ultimately 1.2963.

Most Asian Equity Markets Trade With Risk-Off Bias

Markets

UK inflation data illustrated yesterday that market-/policy relevant data still have the potential to move markets. UK Gilts decisively outperformed Bunds and Treasuries after less worse than feared UK September inflation data. UK headline inflation at 3.8% avoided a spike toward the 4% psychological barrier. The core measure even unexpectedly eased to 3.5% from 3.7%. Gilt yields declined between 9.1 bps (2-y) and 4.5 bps (30-year). The debate on the pace/timing of follow-up BoE easing is again open. Markets see a chance of about 70% for a December rate cut. The odds for a November cut rose from 10% to about 1 in 3. We assume it might be a closer call, subject to the BoE’s assessment of the content of the new policy report that accompanies the November decision. Admittedly, recent BoE worries on financial stability and leverage in some parts of the financial system to some extent also might play in the background. Lower inflation might be relatively better news for the UK budget via (inflation-linked) interest rate payments and expenses. This probably helps to explain the rather orderly market reaction of sterling to the loss of interest rate support. After an initial spike from the 0.8675 area to 0.8710, EUR/GBP finally eased back just below 0.87. (close 0.869). US and EMU markets didn’t ‘enjoy’ this kind of market relevant data releases. The risk rebound since last week’s (trade/credit-related) noise finally ran into resistance with US equity indices easing between 0.53% (S&P) and 0.93% (Nasdaq). Moves in US and EMU German bond markets this time were limited. US yields declined marginally (1 bp across the curve). A $13bn 20-y US Treasury auction met decent investor buying interest. German bonds took a breather after their recent rally with yields ‘rising’ between 0.1 bp (2-y) and 1.9 bps (30-y). The oil price jumped about $3/b as the US announced sanctions against two Russian oil majors (cf infra). However, the direct impact on bond and FX markets was limited. Following an initial gain, DXY closed the session marginally lower at 98.9. EUR/USD ‘gained’ to close at 1.1611 compared to 1.1600. A Similar insignificant move for USD/JPY (close 152).

Most Asian equity markets are trading with a risk-off bias this morning. Headlines that the US is considering broad export restrictions on China with respect to critical software again rekindles trade uncertainty. Markets also still might assess the broader impact of the US sanctions against Russian oil majors. Regular US data publications will again be limited. An EU summit in Brussels plans to address a wide range of topics ranging from the response to the war in Ukraine, over EU defense, the situation in the Middle East, competitiveness, housing and migration,... However, it is far from sure the debate will yield any direct input for markets. We look out whether a (mild) risk-off supports further gains in core bonds. For now, the dollar at least shows no unequivocal reaction function.

News & Views

The US imposed further sanctions on Russia yesterday as a result the country’s lack of serious commitment to a peace process to end the war in Ukraine. The actions target Russia’s two largest oil companies, Rosneft and Lukoil. The US increases pressure on Russia’s energy sector to degrade the Kremlin’s ability to raise revenue for its war machine and support its weakened economy. The sanctions freeze all US-based assets of both oil companies and their subsidiaries and prohibit US persons from engaging in financial transactions with them. Last week, the UK unleased strongest sanctions yet on Russia by also directly targeting both oil majors. The EU is set to announce its 19th package against Moscow, including a ban on imports of Russian LNG. Oil prices rose after the announcement with Brent crude moving from $62/b to $65/b..

The Bank of Korea kept its policy rate unchanged at 2.5%. The central bank maintained its growth forecasts at 0.9% for this year and 1.6% for next while inflation is expected to stay anchored near the 2% target. The central bank kept its easing bias going forward with 4 out of 7 board members leaning to a 25 bps rate cut in the next three months while 2 preferred a steady course because of rising financial stability risks linked to the hot (Seoul) housing market. Previously, the split was 5-1. BoK Rhee doesn’t disclose his own views. The Korean won weakens this morning against an overall firm dollar with USD/KRW touching 1440 for the first time since May.

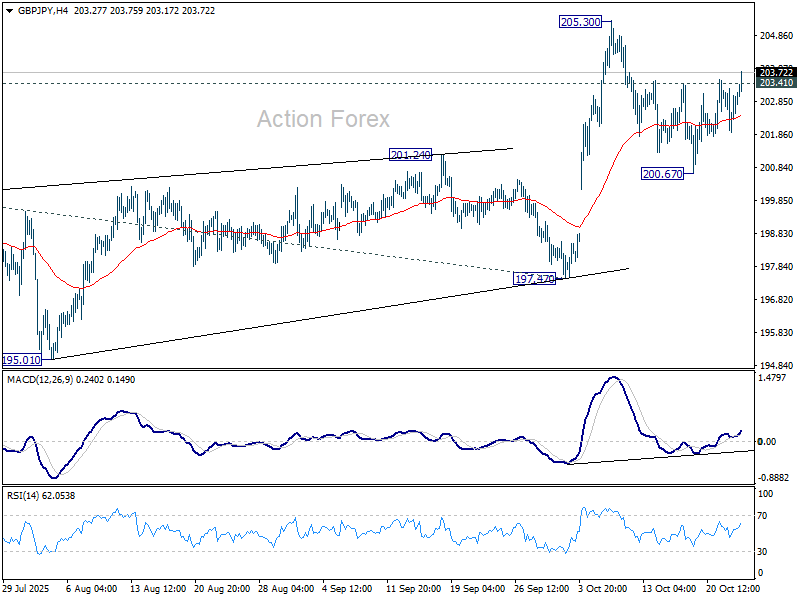

GBP/JPY Daily Outlook

Daily Pivots: (S1) 202.19; (P) 202.73; (R1) 203.53; More...

GBP/JPY's break of 203.41 resistance suggests that pullback from 205.30 has completed. Intraday bias is back on the upside for retesting 205.30 first. Firm break there will resume larger rally to 61.8% projection of 184.35 to 199.96 from 197.47 at 207.11. For now, risk will stay on the upside as long as 200.67 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 will dampen this view and could extend the corrective pattern with another fall.

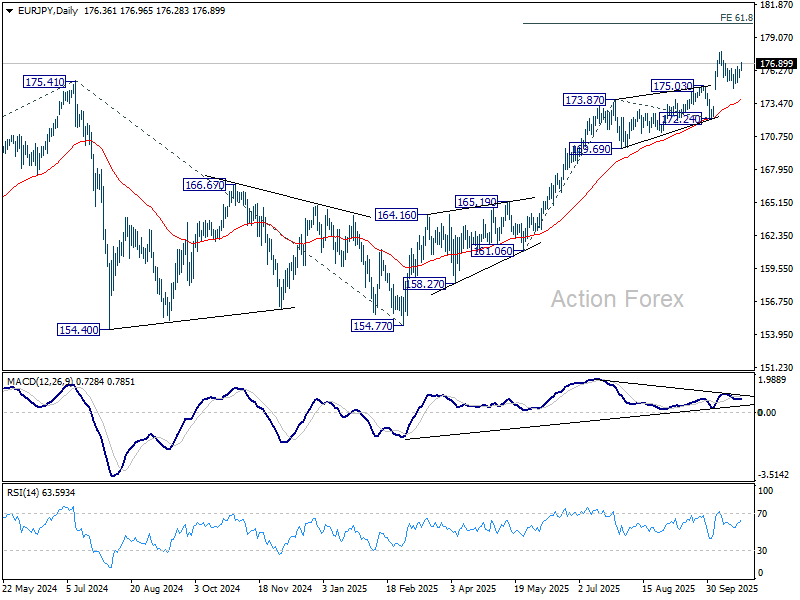

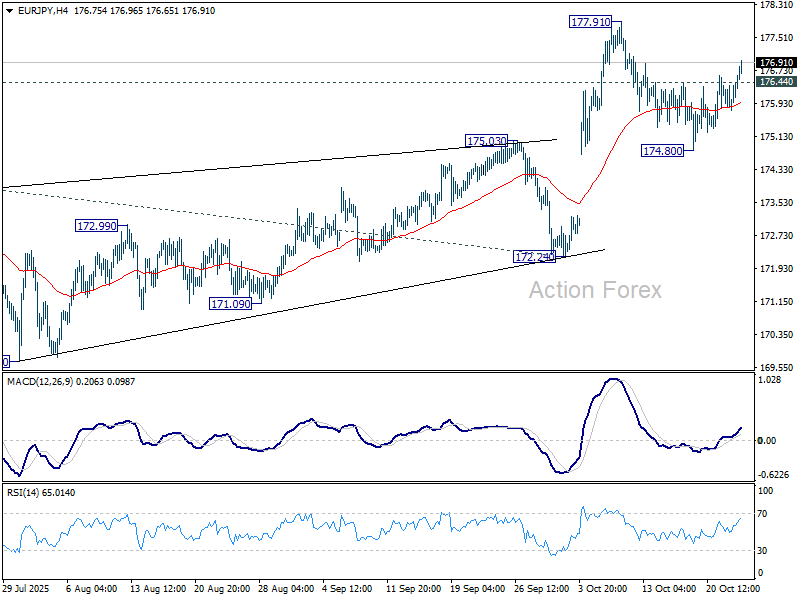

EUR/JPY Daily Outlook

Daily Pivots: (S1) 175.97; (P) 176.21; (R1) 176.64; More...

EUR/JPY's break of 176.44 minor resistance suggests that pullback from 177.91 has completed. Intraday bias is back on the upside for retesting 177.91. Firm break there will resume larger up trend to 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next. For now, risk will stay on the upside as long as 174.80 support holds, in case of retreat.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Firm break of 172.24 support will suggests that it has turned into consolidations again. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 167.43) holds, even in case of deep pullback.