Sample Category Title

US CPI and PMIs to Guide Markets Through Shutdown

In focus today

The delayed US September CPI is set to be released at 14:30 CET. We forecast headline CPI at 3.1% y/y from 2.9% and core CPI inflation at 3.1% y/y from 3.1%. We see risks skewed towards a higher reading but think the bar for the Fed skipping its planned rate cut on 29 October is very high. After the CPI, October flash PMIs will be released for the US. Private-sector data could gather more attention than usual considering the government shutdown.

In the euro area, the important October flash PMI report is released. Following stronger-than-expected growth in the first half of the year we expect the euro area economy to be close to stagnant in the second half of 2025 with 0.1% q/q GDP growth in both quarters, driven by 'front-loading' of exports at the start of the year.

The Swedish PPI figures are unlikely to have any instant market impact. However, some subindices may offer useful insights into future inflation pressures and therefore can be of value for inflation forecasts.

Economic and market news

What happened overnight

In the trade war, US President Trump abruptly ended trade negotiations with Canada over an anti-tariff ad campaign launched by the province of Ontario. In a post on Truth Social, Trump declared, "All trade negotiations with Canada are hereby terminated".

The White House confirmed that US President Trump will meet Chinese President Xi Jinping on Thursday next week. Whether it would come to pass has previously been drawn into question following the recent escalation of trade tensions.

In Japan, CPI inflation (excl. fresh food) increased to 2.9% in September from 2.7% in August. It marks the 42nd consecutive month with Bank of Japan's (BoJ) favourite inflation measure above the 2% target. Even so, we expect the BoJ will keep its policy rate on hold at 0.5% at its meeting next week. Core inflation declined to 1.3% from 1.6%, reflecting that inflation is still not a demand driven phenomenon in Japan. According to PMIs, the economy decelerated in October, with composite PMI declining to 50.9 from 51.3, driven mostly by service expansion becoming less dominant. We expect the BoJ will find room for the next rate hike in December.

What happened yesterday

In the euro area, October consumer confidence surprisingly improved to -14.2 (cons:

-15.0) from -14.9 however, the measure remained at a very low level, broadly like the past five months. The weak confidence is dampening consumption growth despite solid fundamentals such as rising employment, lower rates and rising real incomes.

In Denmark, consumer confidence declined to its lowest level since early 2023 to -19.5 from -18.7 in September. Inflation concerns remain high, driven predominantly by elevated food prices, although the perception of price developments showed a slight improvement.

In Norway, wage growth slowed to 4.3% y/y in September, down from 4.5% y/y in August. Slower wage growth is a necessary condition for Norges Bank to cut rates next year, so this is a move in the right direction even if the level still is too high. At the same time, the preliminary employment figure rose 0.1 % m/m in September, hence employment growth seems to be slowing, but only marginally weaker than Norges Bank's assumption from the September MPR and should be neutral to the monetary policy outlook. The trend-adjusted LFS unemployment rate was unchanged at 4.7% in September.

In China, a new outline of the Five-Year Plan for 2026-2030 was revealed and came with a few surprises but underlined the goal of becoming a tech superpower with a high degree of self-reliance. Boosting private consumption was again highlighted as a priority. However, on this point the language was a bit disappointing given the weak achievements on this goal in recent years. We may get more details in March when the full plan is revealed.

Equities: Equities rallied broadly yesterday in what looked like a textbook-style risk-on session. Investors turned notably more optimistic, not only on macro fundamentals, but rather on political and geopolitical developments, and to be fair, helped by some spectacular earnings releases. The result was a clear pro-cyclical rotation: cyclicals outperformed defensives, implied volatility declined, and small caps beat large caps. Add to this, the long end of the curve finally traded higher. Meanwhile, oil surged more than 5%, lifting the energy sector, though several non-energy sectors in the US still outperformed, a telling signal of how little the current oil price level worries markets. Even with such a sharp daily move, the broader equity complex remained firm. On the political side, the US and China announced a new round of trade talks, and more importantly, Trump and Xi are set to meet in Korea next week. In the US yesterday, Dow +0.3%, S&P 500 +0.6%, Nasdaq +0.9%, Russell 2000 +1.3%. Asian markets are higher this morning, led once again by tech. The KOSPI index, for example, is now up more than 70% year-to-date (!). Futures in both Europe and the US are pointing slightly higher as well.

FI and FX: Risk sentiment improved after the White House confirmed that President Trump will meet with Chinese President Xi Jinping next Thursday. US Treasury yields rose around 5bp across the curve, with the 10-year yield back near 4.00%. In the euro area, yields also moved higher, albeit more modestly, with Bund yields up roughly 2bp across the curve. EUR/USD continues to trade around 1.16, with the USD firmer across the G10. The news that Sweden intends to sell 100-150 JAS 39 Gripen E to Ukraine had a minor instantaneous and short-lived negative effect on EUR/SEK. The Norwegian krone has seen significant fluctuations in recent weeks, but nothing has occurred to alter our long-term view.

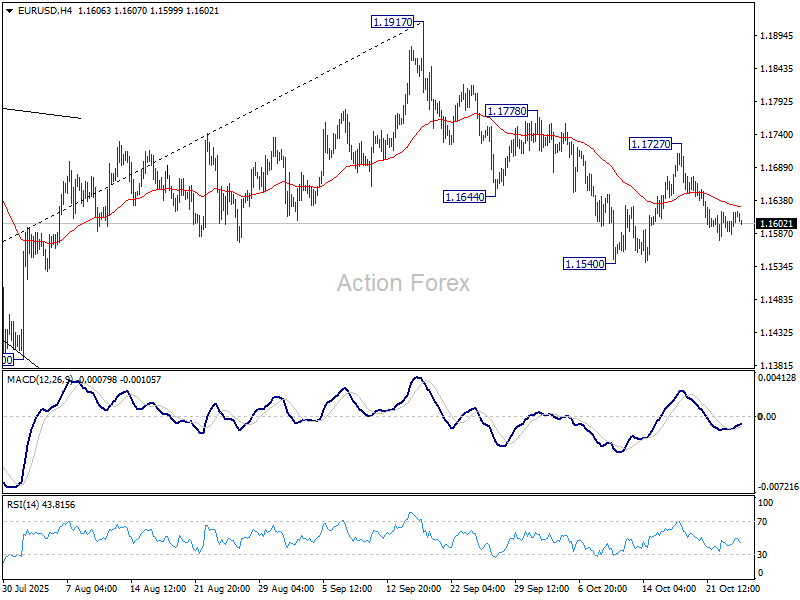

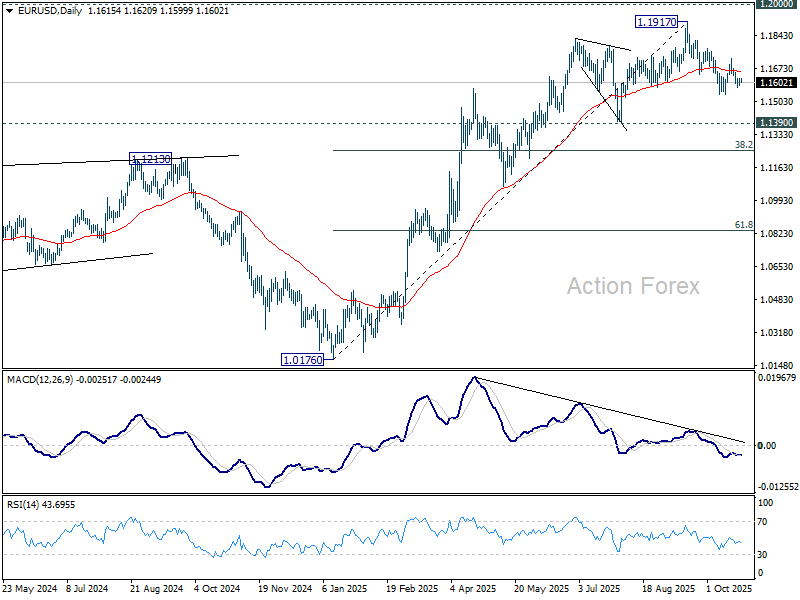

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1595; (P) 1.1608; (R1) 1.1630; More…

Intraday bias in EUR/USD remains neutral, and further decline is expected with 1.1727 resistance intact. Break of 1.1540 will resume the fall from 1.1917 to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1290) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

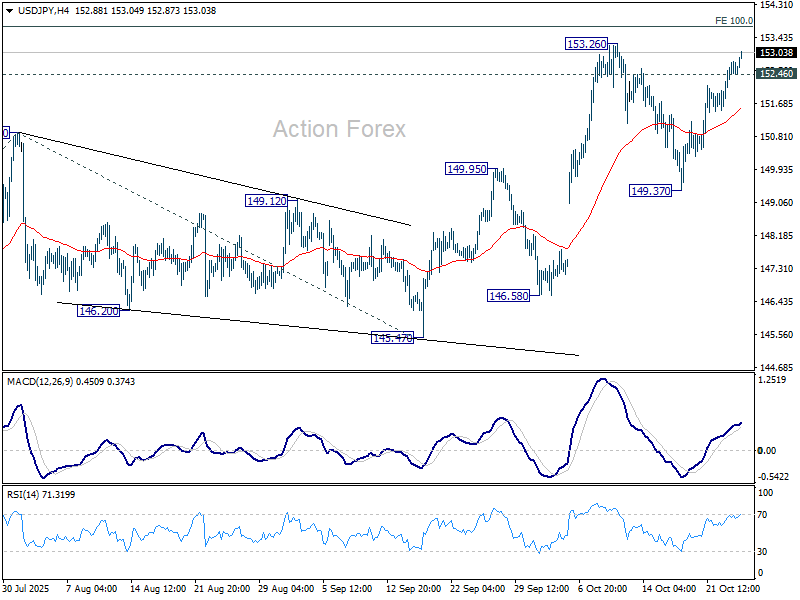

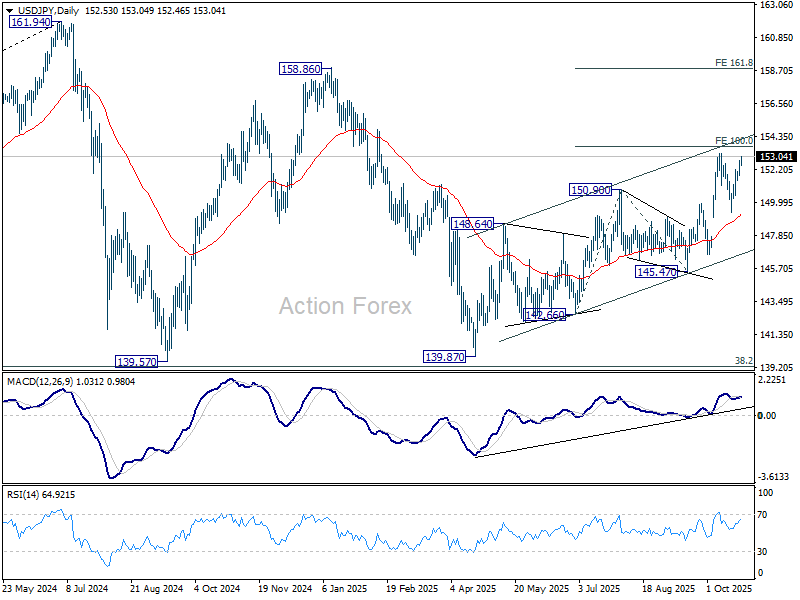

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.01; (P) 152.40; (R1) 152.99; More...

Intraday bias in USD/JPY stays on the upside at this point. Break of 153.26 will larger rally from 139.87 to 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there would prompt upside acceleration to 161.8% projection at 158.80. On the downside, below 152.46 minor support will turn intraday bias neutral again first.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

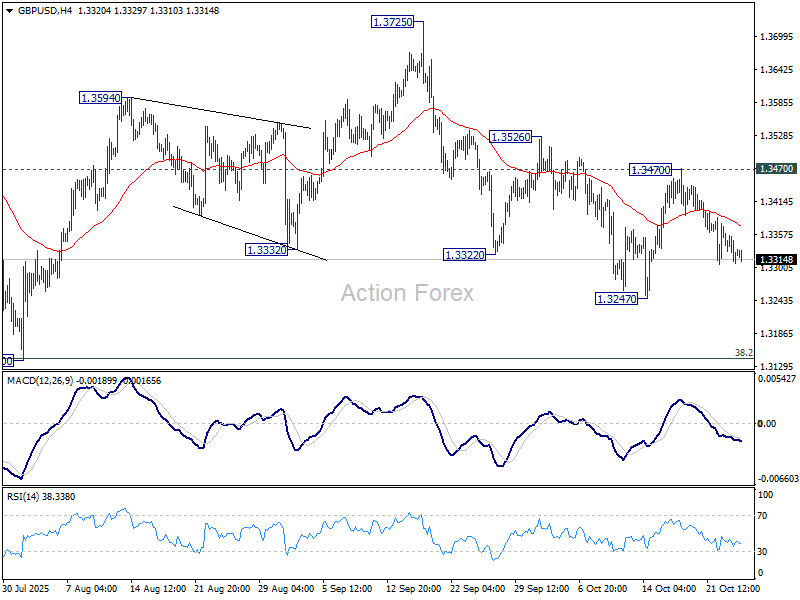

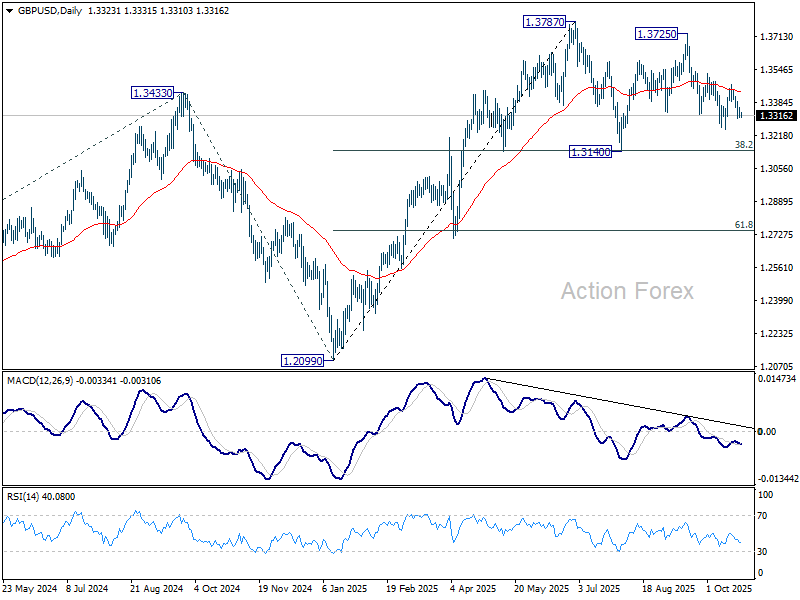

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3301; (P) 1.3333; (R1) 1.3358; More...

No change in GBP/USD's outlook and intraday bias stays neutral. Fall from 1.3725 could extend lower and break of 1.3247 will target 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, break of 1.3170 resistance will turn bias back to the upside for 1.3526 resistance. Firm break there will target 1.3725/87 resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

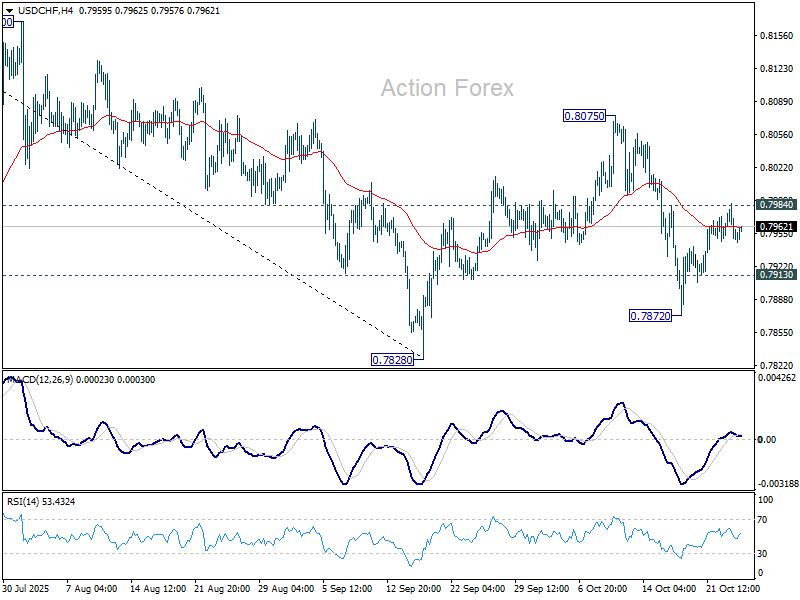

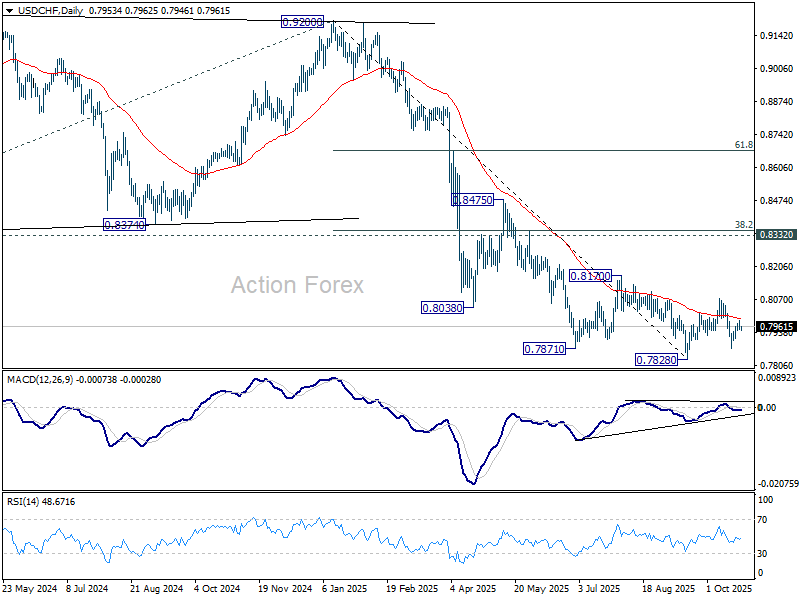

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7939; (P) 0.7963; (R1) 0.7976; More…

No change in USD/CHF's outlook and intraday bias remains neutral. With 0.7984 resistance intact, further decline is in favor. On the downside, below 0.7913 minor support will turn bias to the downside for 0.7872 and then 0.7828 low. Firm break there will resume larger down trend. However, break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

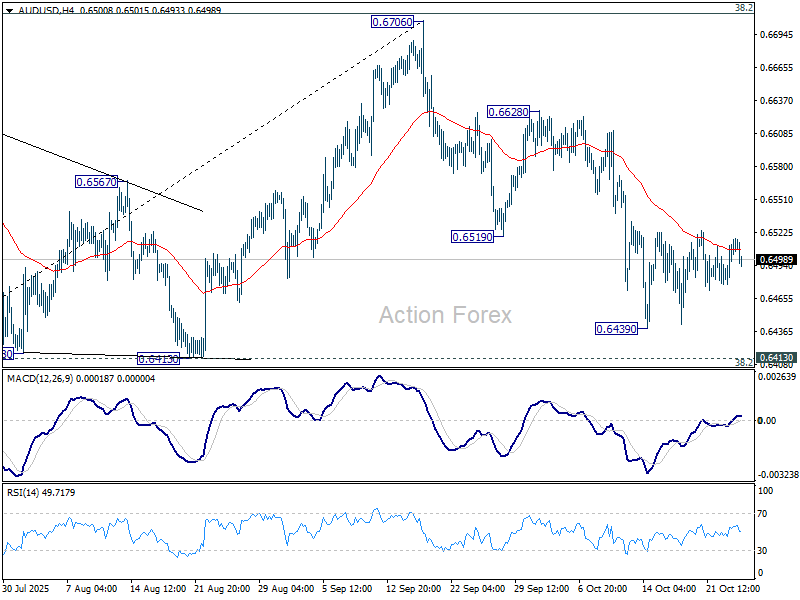

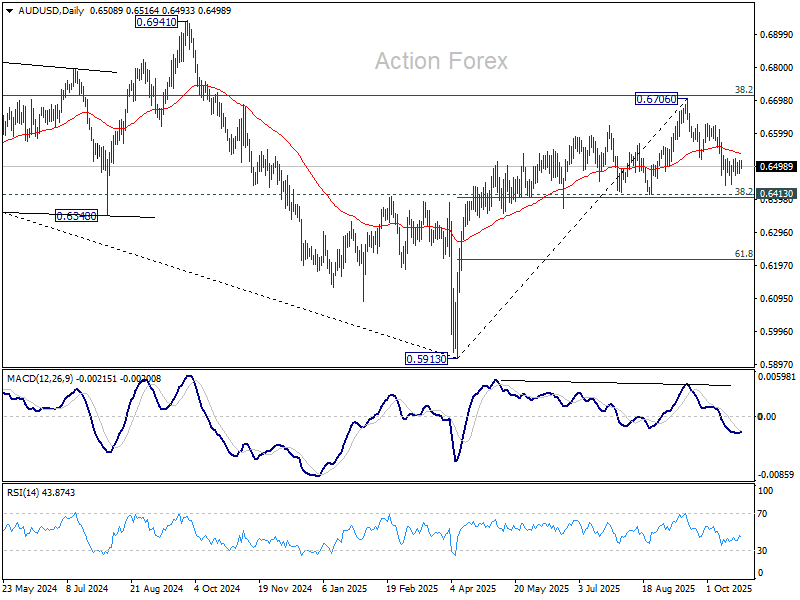

AUD/USD Daily Report

Daily Pivots: (S1) 0.6489; (P) 0.6503; (R1) 0.6528; More...

No change in AUD/USD's outlook as consolidations continues. Intraday bias remains neutral at this point. Further decline is in favor as long as 55 D EMA (now at 0.6539) holds. Below 0.6439 will target 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403. Decisive break there will indicate bearish reversal after rejection by 0.6713 fibonacci level. Nevertheless, sustained trading above 55 D EMA will keep the rise from 0.5913 intact, and bring retest of 0.6706 high.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

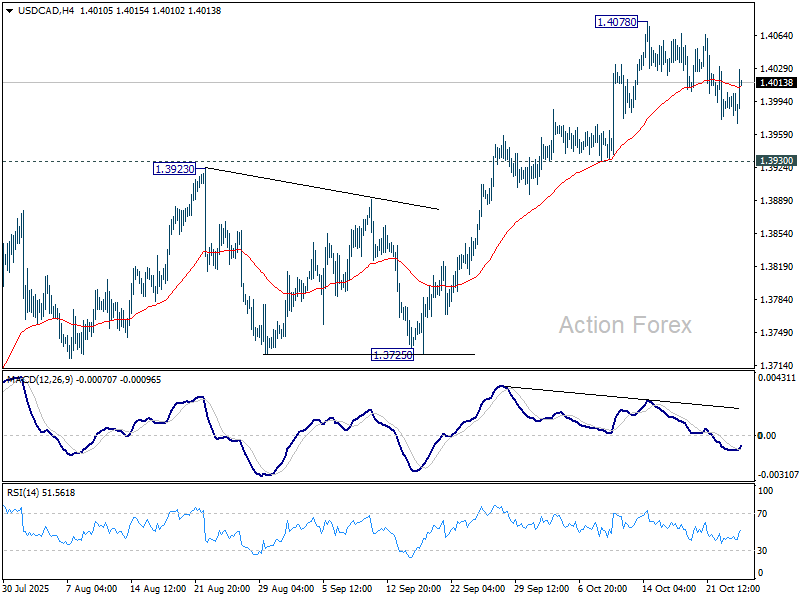

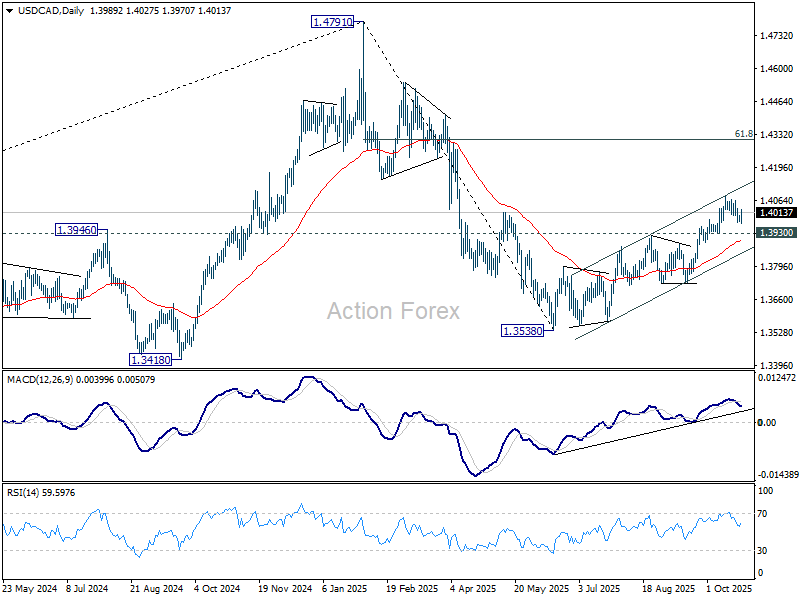

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3981; (P) 1.3993; (R1) 1.4006; More...

USD/CAD is still extending the corrective pattern from 1.4078. Intraday bias stays neutral for the moment. While deeper retreat cannot be ruled out, further rally is still expected as long as 1.3930 support holds. Current development suggest that rise from 1.3538 is reversing whole fall from 1.4791. Above 1.4078 will target 61.8% retracement of 1.4791 to 1.3538 at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds.

Markets Hold Breath Ahead of US CPI, US–China Talks in KL

Dollar traded steady in Asian session, with traders showing little appetite for new positions ahead of key inflation data. The September CPI report, due later in the day, is expected to show a 0.4% monthly increase in headline prices and a 0.3% gain in core CPI, which would push the annual headline rate up to 3.1% while leaving core steady at 3.1%.

While the CPI outcome is unlikely to derail the Fed’s plan to ease this month, it could help determine the pace of cuts going forward. Markets are currently assigning more than 90% probability to another reduction in December. A hotter print could raise the chance of delaying the next move. Beyond Fed implications, the CPI release is also seen as a volatility trigger for broader markets that have drifted without clear direction.

On the trade front, U.S.–Canada trade relations took a sudden turn after US President Donald Trump declared all negotiations with Ottawa “terminated,” citing a “fraudulent” advertisement featuring Ronald Reagan criticizing tariffs. The Ronald Reagan Presidential Foundation later said the ad used “selective audio and video,” adding that it was reviewing legal options. Canadian Prime Minister Mark Carney on the other hand, vowed not to grant “unfair access” to U.S. markets if ongoing trade discussions collapse.

At the same time, attention is shifting to Kuala Lumpur, where senior officials from the U.S. and China are set to meet on Friday to defuse trade tensions. Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer will hold talks with Chinese Vice Premier He Lifeng to prevent a further escalation ahead of next week’s planned Trump–Xi summit. The talks are crucial to averting a new wave of 100% tariffs on Chinese goods, set to take effect on November 1, in retaliation for Beijing’s expanded export controls on critical rare earth materials.

Overall for the week so far, commodity currencies are generally strong, with Kiwi leading, followed by Aussie and Loonie. Yen is pinned at the bottom, followed by Sterling and Euro. Swiss Franc and Sterling are trading mid-pack.

In Asia, at the time of writing, Nikkei is up 1.33%. Hong Kong HSI is up 0.47%. China Shanghai SSE is up 0.45%. Singapore Strait Times is up 0.23%. Japan 10-year JGB yield is down -0.01 at 1.651. Overnight, DOW rose 0.31%. S&P 500 rose 0.58%. NASDAQ rose 0.89%. 10-year yield rose 0.038 to 3.991.

Japan CPI core Rises to 2.9%, ending three-month slowdown

Japan’s inflation picked up in September, with core CPI (excluding fresh food) rising from 2.7% to 2.9% yoy, matching expectations and marking the first acceleration in four months. The key gauge has stayed at or above the BoJ’s 2% target since April 2022. Headline CPI also rose from 2.7% to 2.9% yoy, in line with the core measure.

Underlying momentum was uneven. Core-core CPI, which strips out both energy and fresh food and is considered a closer measure of domestic demand, slowed to 3.0% from 3.3% yoy, suggesting that broader inflationary pressures are gradually easing.

Food prices continued to rise, but at a slower pace — non-fresh food prices gained 7.6%, down from 8.0% in August. Rice prices, which spiked earlier this year, rose 49.2%, their fourth consecutive month of deceleration after peaking at more than 100% growth in May.

Meanwhile, service prices, a metric closely watched by the BoJ for its link to wage growth, increased 1.4%, slightly below August’s 1.5%.

Japan PMI composite falls to 50.9, weak Yen keeps inflation hot

Japan’s private sector lost further momentum in October, with both manufacturing and services activity softening, according to S&P Global’s Flash PMI survey. The Manufacturing PMI slipped from 48.5 to 48.3, extending its contraction, while Services PMI fell from 53.3 to 52.4. As a result, Composite index eased from 51.3 to 50.9, signaling the slowest pace of overall growth since May.

Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, said the survey showed the first decline in new business in 16 months. While the services sector remained the key driver of growth, its fading strength “will be a point of concern” as manufacturing continues to struggle. The factory sector’s downturn deepened, with new orders falling at the fastest pace in 20 months.

Inflationary pressures, however, remained elevated. Both input costs and output charges continued to rise at historically strong rates, driven by higher wage, fuel, and material costs, and alongside by a weaker Yen.

Australia PMI composite ticks up to 52.6, easing inflation keeps RBA on easing track

Australia’s private sector activity sent mixed signals in October, according to the S&P Global Flash PMI survey. Manufacturing PMI slipped back into contraction, falling from 51.4 to 49.7, while Services PMI rose to 53.1 from 52.4, lifting the Composite PMI modestly from 52.4 to 52.6. The data suggest that overall business activity grew at a slightly faster pace at the start of Q4, though the underlying picture remains uneven across sectors.

According to Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, the divergence between sectors was striking. Manufacturing “notably worsened,” with new orders dropping further and factories shedding jobs amid pressure on profit margins.

In contrast, services activity expanded at a solid pace, but even there, new business growth and hiring momentum slowed, and business confidence weakened.

On a positive note, price pressures continued to ease, with output price inflation falling to a five-year low. This cooling in inflation dynamics should reassure the RBA, which remains on track to pursue further monetary easing.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3981; (P) 1.3993; (R1) 1.4006; More...

USD/CAD is still extending the corrective pattern from 1.4078. Intraday bias stays neutral for the moment. While deeper retreat cannot be ruled out, further rally is still expected as long as 1.3930 support holds. Current development suggest that rise from 1.3538 is reversing whole fall from 1.4791. Above 1.4078 will target 61.8% retracement of 1.4791 to 1.3538 at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds.

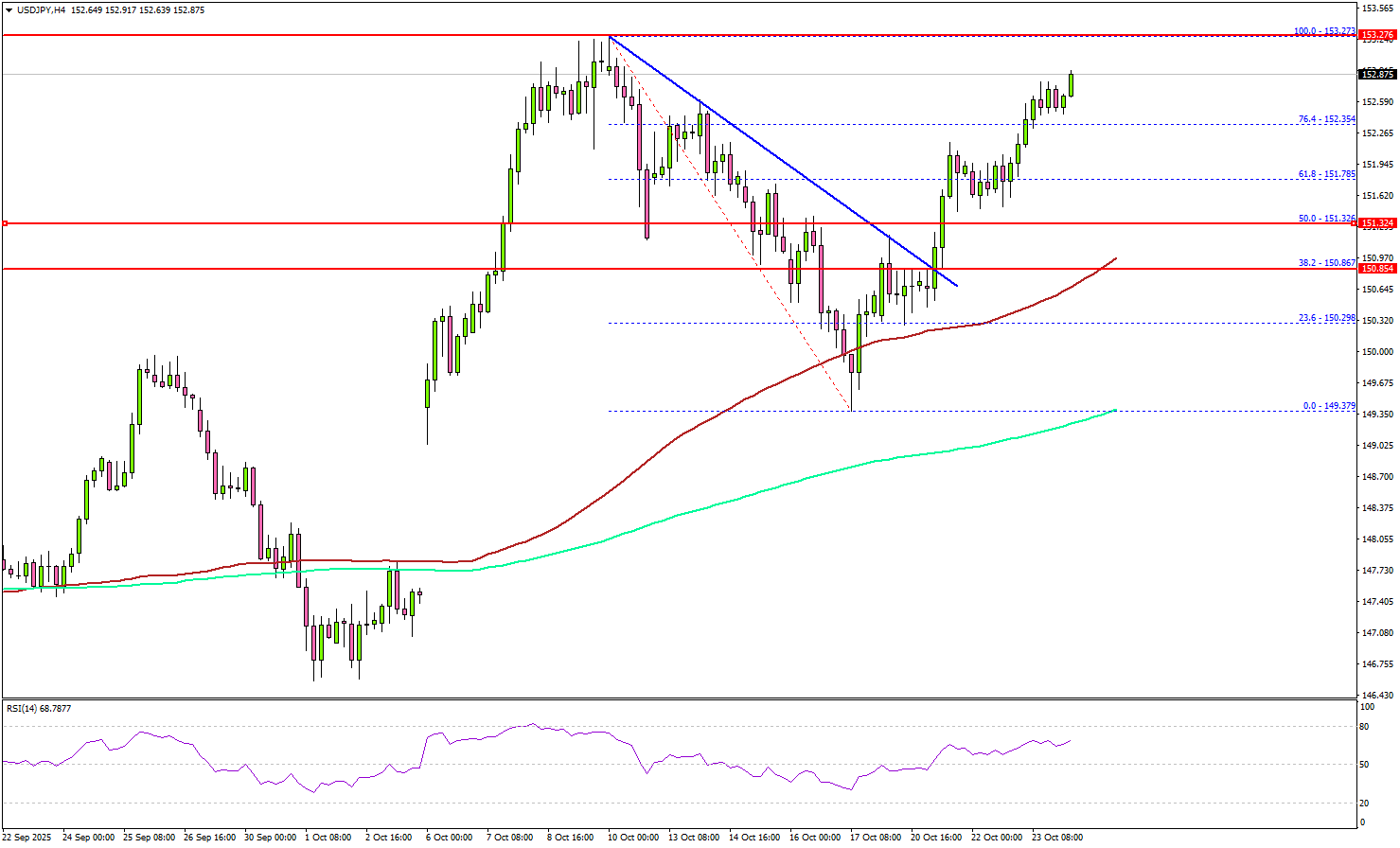

USD/JPY Restarts Increase As Dollar Strengthens Ahead Of Key U.S. Data

Key Highlights

- USD/JPY started a fresh increase above 151.50.

- It cleared a key bearish trend line with resistance at 150.85 on the 4-hour chart.

- EUR/USD is again moving below the 1.1620 support.

- The US CPI could increase 3.1% in Sep 2025 (YoY).

USD/JPY Technical Analysis

The US Dollar remained supported near 149.40 against the Japanese Yen. USD/JPY started a fresh increase above 150.00 and 150.50.

Looking at the 4-hour chart, the pair traded above a key bearish trend line with resistance at 150.85. It settled above the 151.50 resistance, the 200 simple moving average (green, 4-hour), and the 100 simple moving average (red, 4-hour).

There was a clear move above the 50% Fib retracement level of the downward move from the 153.27 swing high to the 149.37 low. On the upside, the pair faces resistance near the 153.27 high.

The next hurdle could be near 153.50. A close above 153.50 resistance might push the pair to 155.00. On the downside, the pair might find support at 152.00. The main support might be 150.85 and the 100 simple moving average (red, 4-hour).

A close below the 100 simple moving average (red, 4-hour) could start a major pullback toward 150.00. Any more losses might open the doors for a test of 148.80.

Looking at EUR/USD, the pair started a recovery wave, but the bears might remain active below the 1.1700 and 1.1720 levels.

Upcoming Key Economic Events:

- US Consumer Price Index for Sep 2025 (MoM) – Forecast +0.4%, versus +0.4% previous.

- US Consumer Price Index for Sep 2025 (YoY) – Forecast +3.1%, versus +2.9% previous.

Japan CPI core Rises to 2.9%, ending three-month slowdown

Japan’s inflation picked up in September, with core CPI (excluding fresh food) rising from 2.7% to 2.9% yoy, matching expectations and marking the first acceleration in four months. The key gauge has stayed at or above the BoJ’s 2% target since April 2022. Headline CPI also rose from 2.7% to 2.9% yoy, in line with the core measure.

Underlying momentum was uneven. Core-core CPI, which strips out both energy and fresh food and is considered a closer measure of domestic demand, slowed to 3.0% from 3.3% yoy, suggesting that broader inflationary pressures are gradually easing.

Food prices continued to rise, but at a slower pace — non-fresh food prices gained 7.6%, down from 8.0% in August. Rice prices, which spiked earlier this year, rose 49.2%, their fourth consecutive month of deceleration after peaking at more than 100% growth in May.

Meanwhile, service prices, a metric closely watched by the BoJ for its link to wage growth, increased 1.4%, slightly below August’s 1.5%.