Sample Category Title

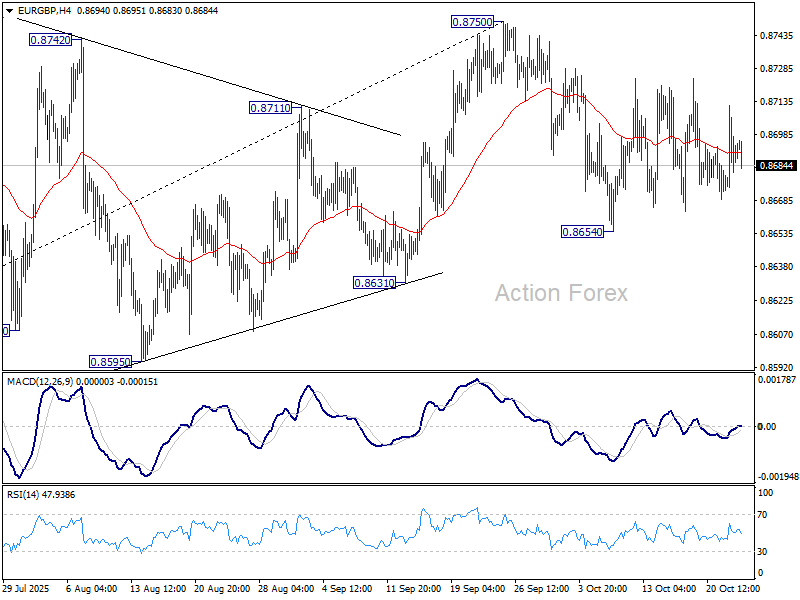

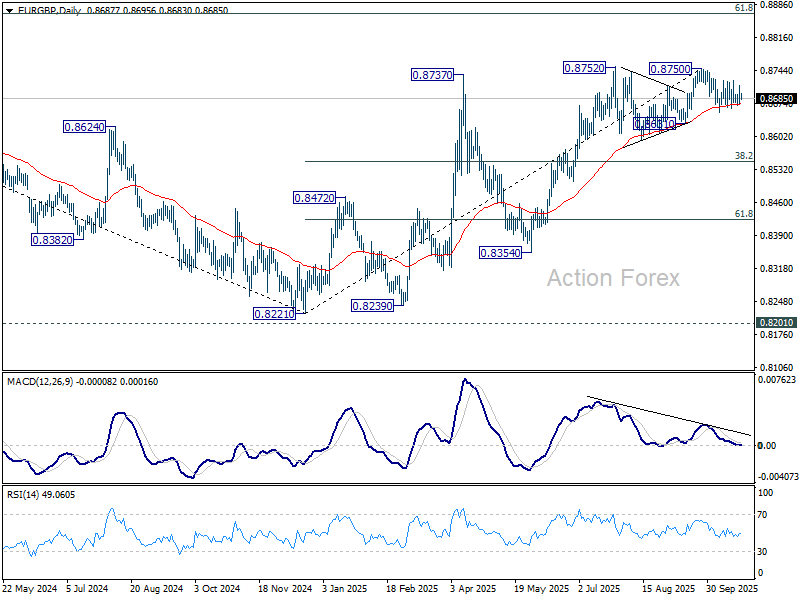

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8670; (P) 0.8692; (R1) 0.8712; More…

Intraday bias in EUR/GBP remains neutral as sideway trading continues. On the downside, break of 0.8654 will resume the fall from 0.8750 to 0.8631 support. Decisive break there will indicate bearish reversal and target 38.2% retracement of 0.8221 to 0.8750 at 0.8548. Nevertheless, on the upside, break of 0.8750/2 will resume the rise from 0.8221 towards 0.8867 fibonacci level.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8631 support will be the first sign that this corrective bounce has completed. Sustained trading below 55 W EMA (now at 0.8549) will confirm, and bring retest of 0.8221 low.

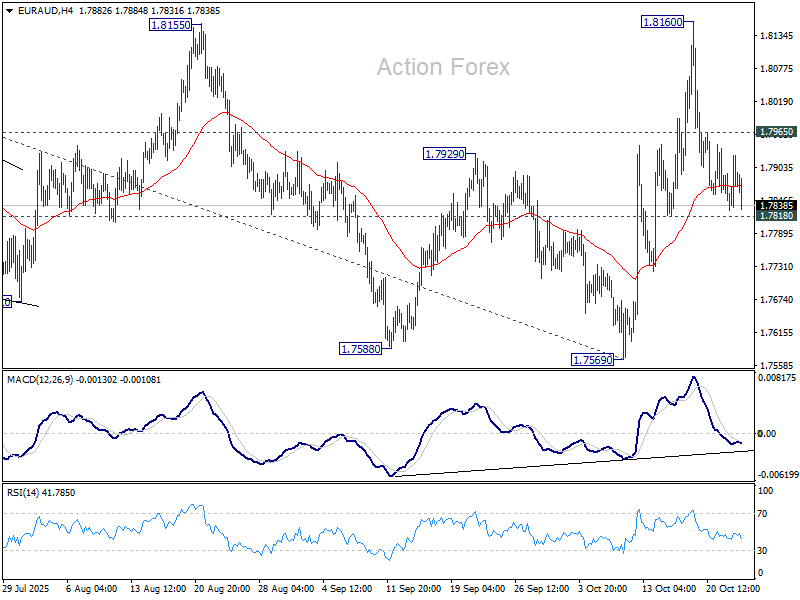

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7840; (P) 1.7884; (R1) 1.7936; More...

Intraday bias in EUR/AUD remains neutral and further rally is in favor with 1.7818 support intact. On the upside, above 1.7965 will turn bias back to the upside for retesting 1.8160 first. Firm break there will affirm the case that larger up trend is resuming, and target 1.8554 high next. On the downside, however, break of 1.7818 will dampen this bullish view and turn focus back to 1.7569 support instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern, which might have completed already. Firm break of 1.8554 will resume larger up trend from 1.4281 (2022 low), and target 61.8% projection of 1.5963 to 1.8554 from 1.7569 at 1.9170. Nevertheless, break of 1.7569 support will delay the bullish case and extend the correction from 1.8554.

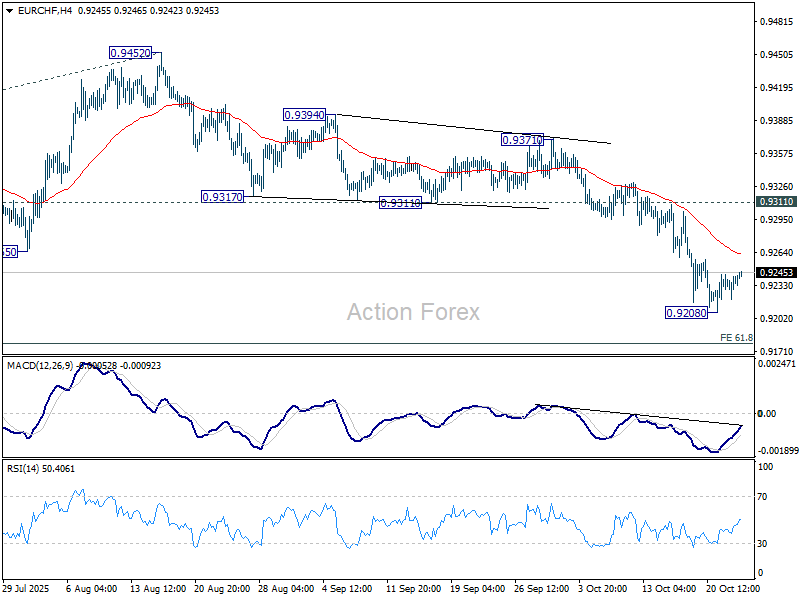

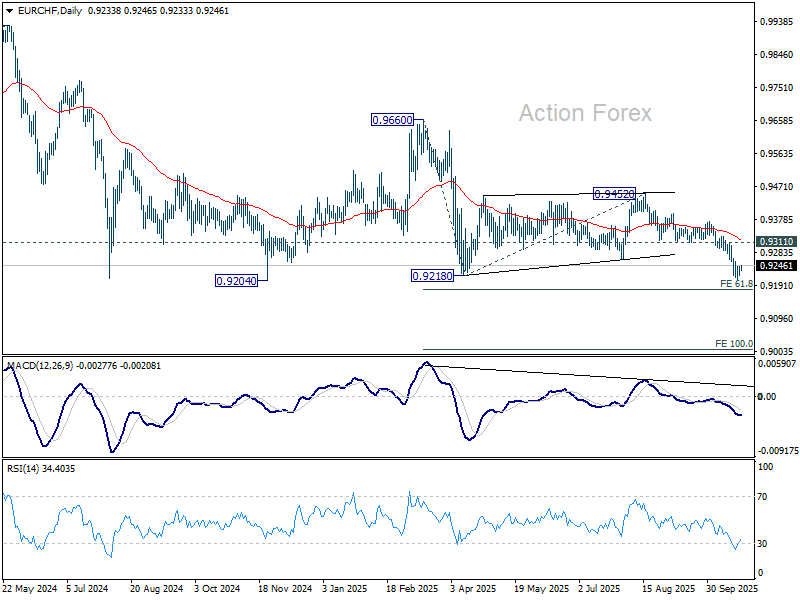

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9227; (P) 0.9237; (R1) 0.9251; More...

Intraday bias in EUR/CHF remains neutral and more consolidations would be seen above 0.9208. Outlook will remain bearish as long as 0.9311 support turned resistance holds. On the downside, break of 0.9208 will target 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179. Firm break there will target 100% projection at 0.9010.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9390). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.

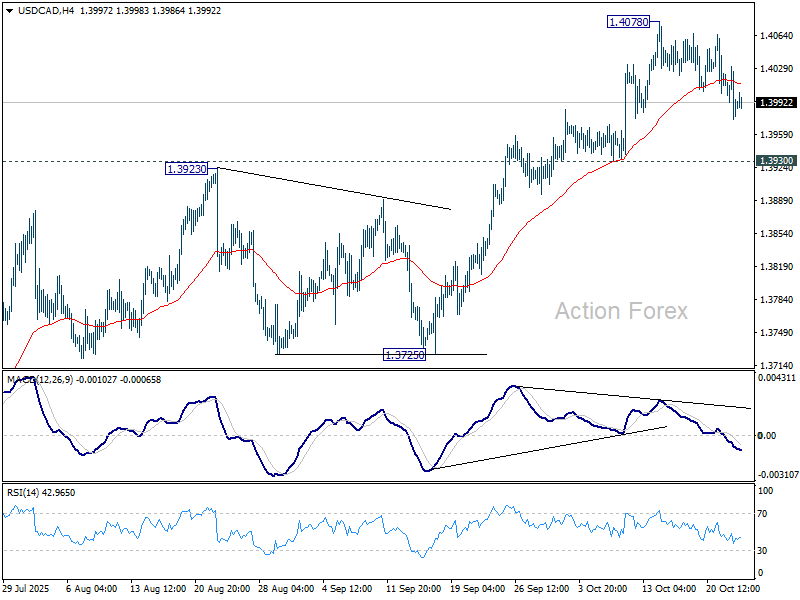

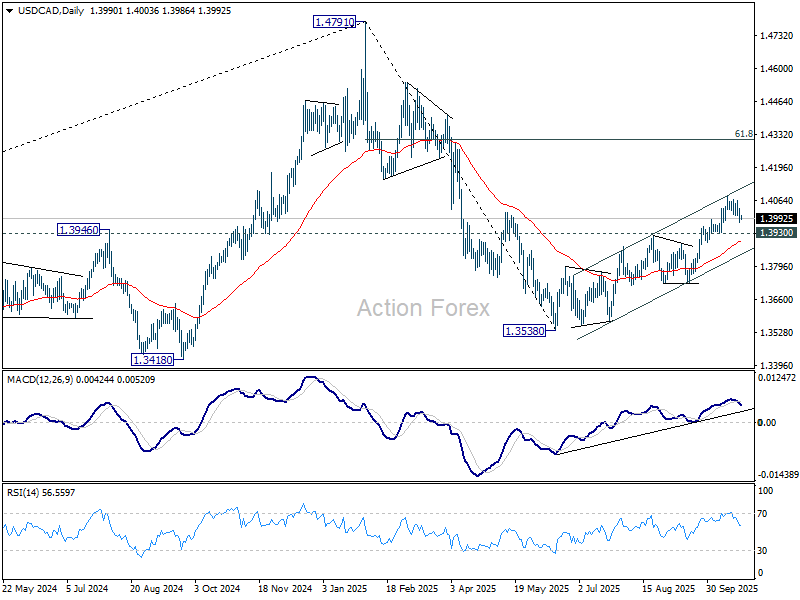

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3970; (P) 1.4001; (R1) 1.4026; More...

USD/CAD is extending the consolidation pattern from 1.4078 and intraday bias remains neutral. While deeper retreat cannot be ruled out, further rally is still expected as long as 1.3930 support holds. Current development suggest that rise from 1.3538 is reversing whole fall from 1.4791. Above 1.4078 will target 61.8% retracement of 1.4791 to 1.3538 at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds.

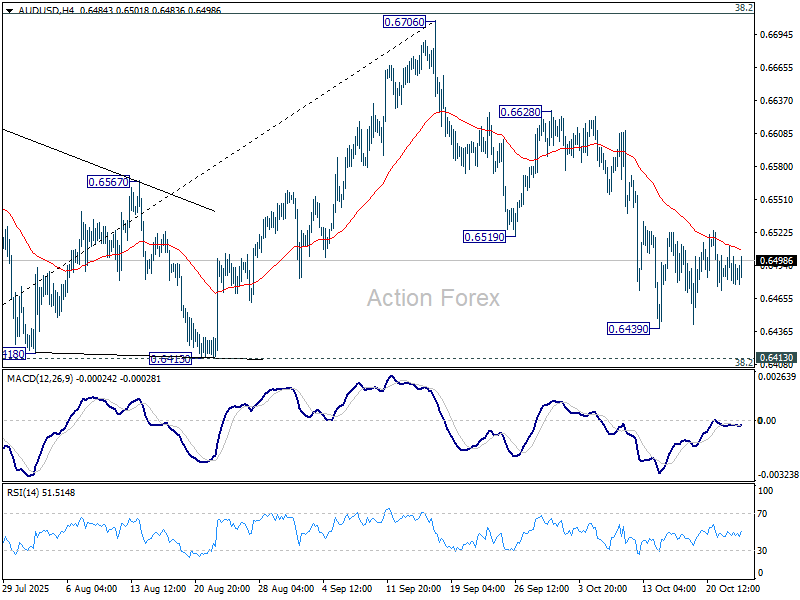

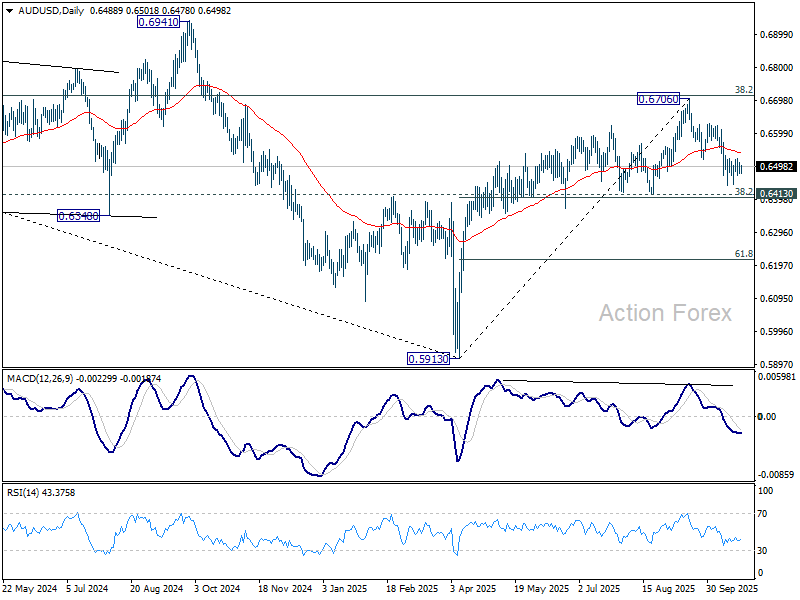

AUD/USD Daily Report

Daily Pivots: (S1) 0.6475; (P) 0.6493; (R1) 0.6509; More...

AUD/USD is still bounded in sideway trading and intraday bias stays neutral. Further decline is in favor as long as 55 D EMA (now at 0.6540) holds. Below 0.6439 will target 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403. Decisive break there will indicate bearish reversal after rejection by 0.6713 fibonacci level. Nevertheless, sustained trading above 55 D EMA will keep the rise from 0.5913 intact, and bring retest of 0.6706 high.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

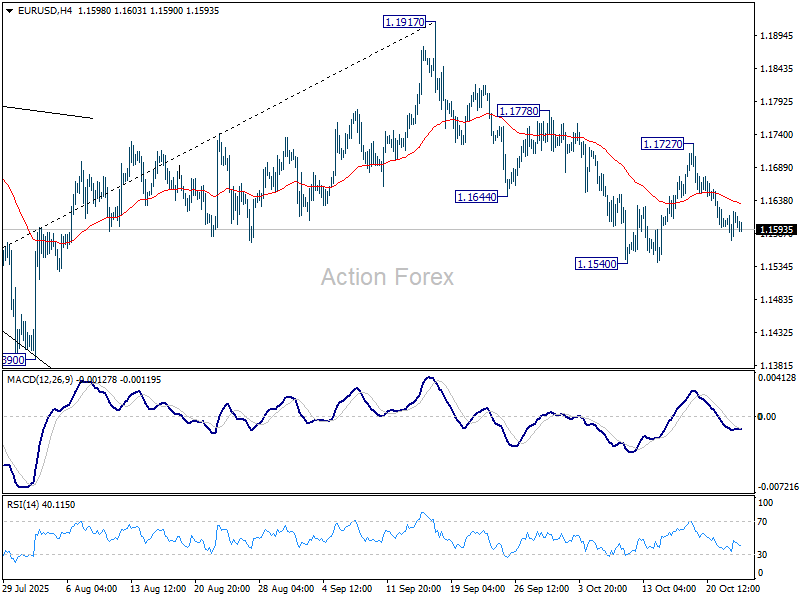

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1584; (P) 1.1603; (R1) 1.1629; More…

Intraday bias in EUR/USD remains neutral for the moment. With 1.1727 resistance intact, further decline is expected. Break of 1.1540 will resume the fall from 1.1917 to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

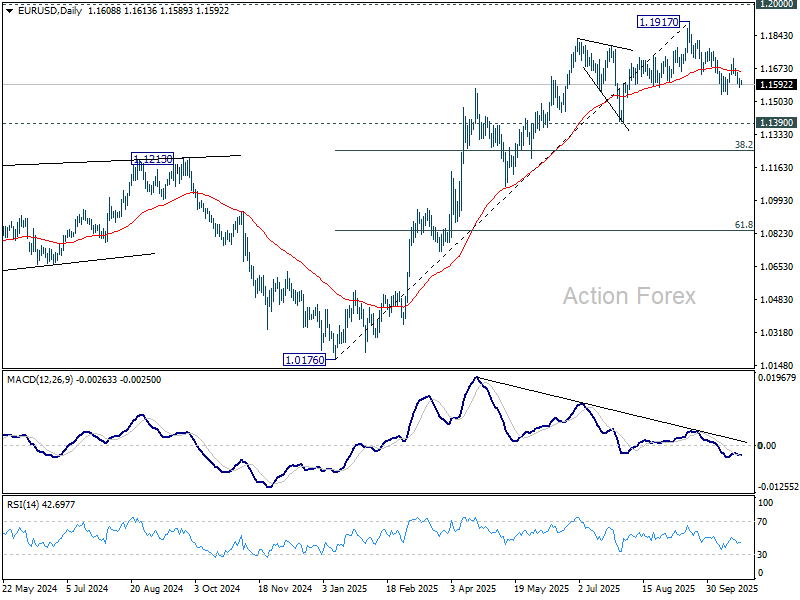

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1290) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

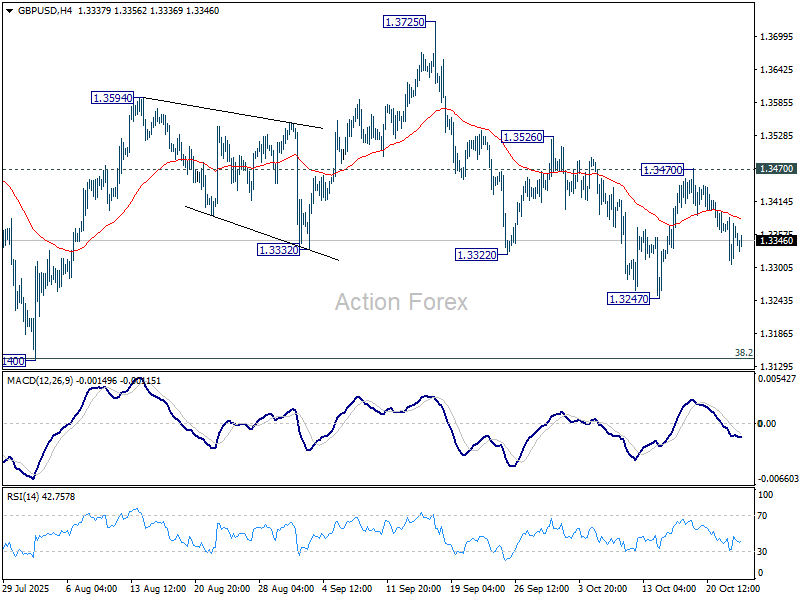

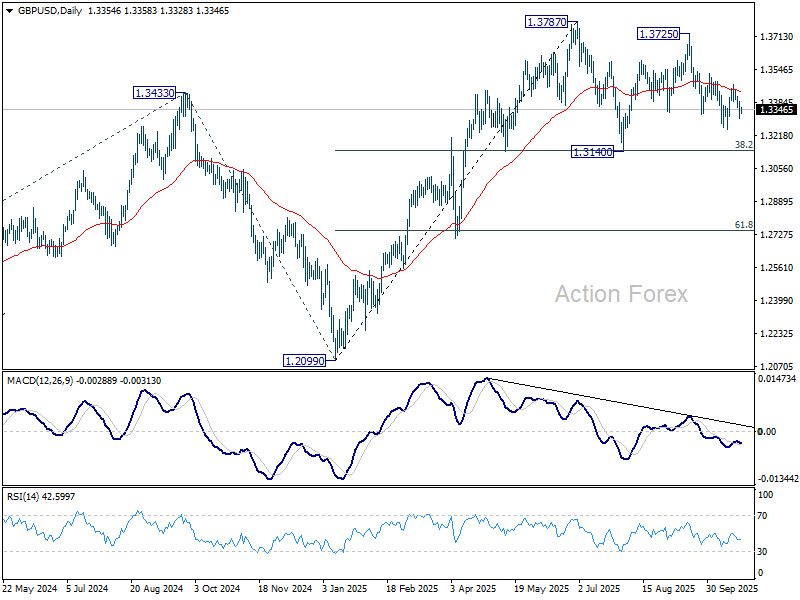

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3313; (P) 1.3350; (R1) 1.3394; More...

Intraday bias in GBP/USD remains neutral for the moment. Fall from 1.3725 could extend lower, and break of 1.3247 will target 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, break of 1.3170 resistance will turn bias back to the upside for 1.3526 resistance. Firm break there will target 1.3725/87 resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

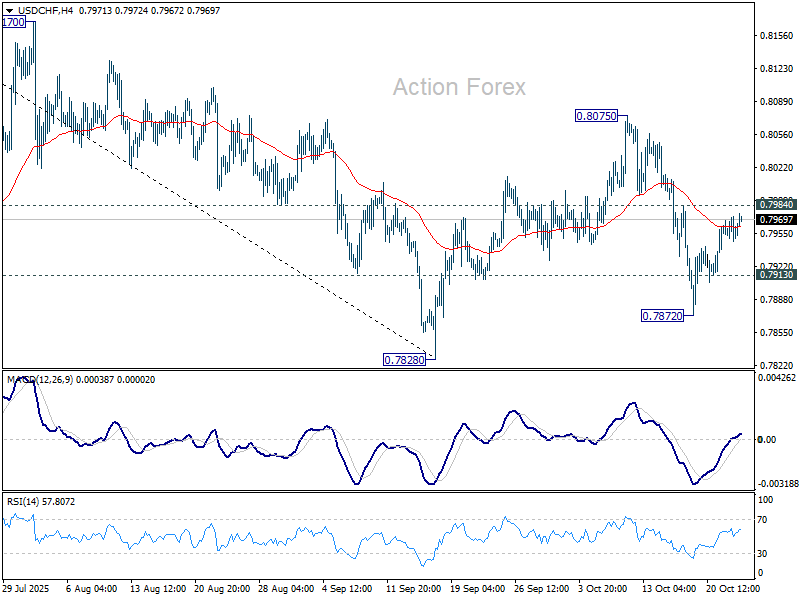

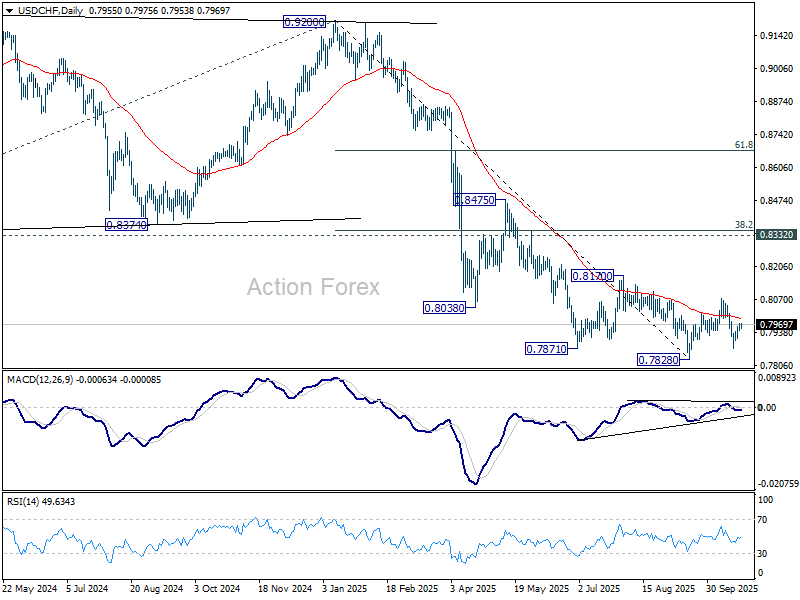

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7948; (P) 0.7961; (R1) 0.7973; More…

No change in USD/CHF's outlook and intraday bias stays neutral. With 0.7984 resistance intact, further decline is in favor. On the downside, below 0.7913 minor support will turn bias to the downside for 0.7872 and then 0.7828 low. Firm break there will resume larger down trend. However, break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

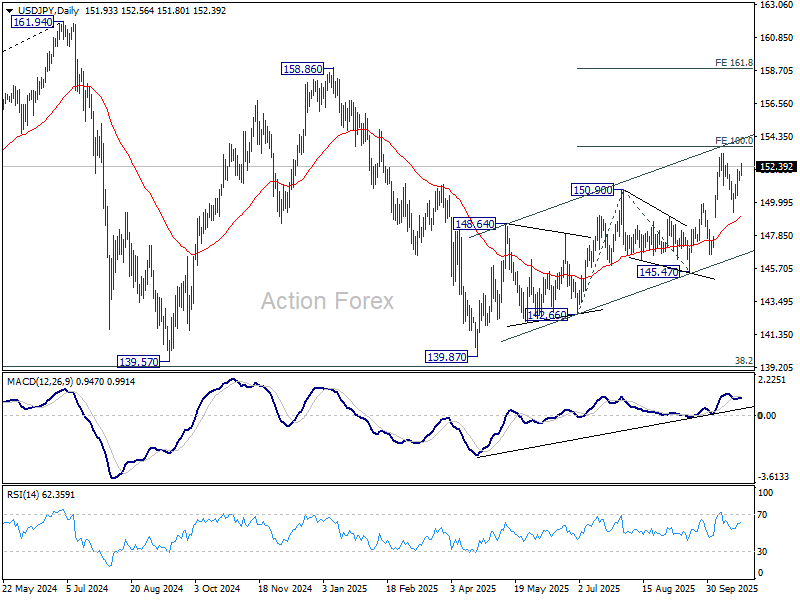

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.62; (P) 151.84; (R1) 152.18; More...

Intraday bias in USD/JPY remains on the upside for retesting 153.26 resistance. Break there will resume larger rally from 139.87 to 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there would prompt upside acceleration to 161.8% projection at 158.80. On the downside, below 151.49 minor support will turn intraday bias neutral again first.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Dollar Strengthens, Risk Tone Softens Ahead of US-China Trade Talks

Risk sentiment turned slightly softer again, as Asian equities pulled back following Wall Street’s modest decline overnight. Investors took a more cautious stance after recent rallies, with profit-taking emerging ahead of key global data and fresh developments on the U.S.–China trade front. Nikkei 225 led the regional retreat, slipping after its record-breaking run earlier this week driven by optimism over newly appointed Prime Minister Sanae Takaichi’s pro-stimulus policy stance.

While sentiment toward Takaichi’s leadership remains positive, markets appear to be digesting earlier gains, with 50,000 level acting as a strong psychological barrier for the Nikkei. The pullback is viewed as a technical correction following an extraordinary advance rather than a reversal in momentum. Investors are waiting for more clarity on the new administration’s fiscal measures and trade posture before re-engaging at higher levels.

Elsewhere in the region, South Korea’s KOSPI initially jumped to a new record high after the Bank of Korea held its benchmark interest rate steady at 2.50%, extending a policy pause that began in May. The index later trimmed gains, mirroring the broader regional tone as risk appetite faded into the afternoon session.

On the trade front, U.S. President Donald Trump struck a cautiously optimistic tone, saying he expected to reach several agreements with Chinese President Xi Jinping when they meet in South Korea next week — including possible soybean purchase commitments and nuclear arms limits. Meanwhile, Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer headed to Malaysia for talks aimed at easing tensions over China’s rare earth export curbs. Bessent said he was optimistic that two days of “fulsome” discussions would lay the groundwork for a productive leaders’ meeting, though U.S. officials have prepared additional measures should talks stall.

In currency markets, Dollar extended its lead while Loonie and Aussie followed. Japanese Yen remained the weakest performer, trailed by Swiss Franc and New Kiwi, while Sterling and Euro stayed mid-pack.

In Asia, at the time of writing, Nikkei is down -1.46%. Hong Kong HSI is down -0.19%. China Shanghai SSE is down -0.83%. Singapore Strait Times is down -0.03%. Japan 10-year JGB yield is up 0.001 at 1.656. Overnight, DOW fell -0.71%. S&P 500 fell -0.53%. NASDAQ fell -0.93%. 10-year yield fell -0.010 to 3.953.

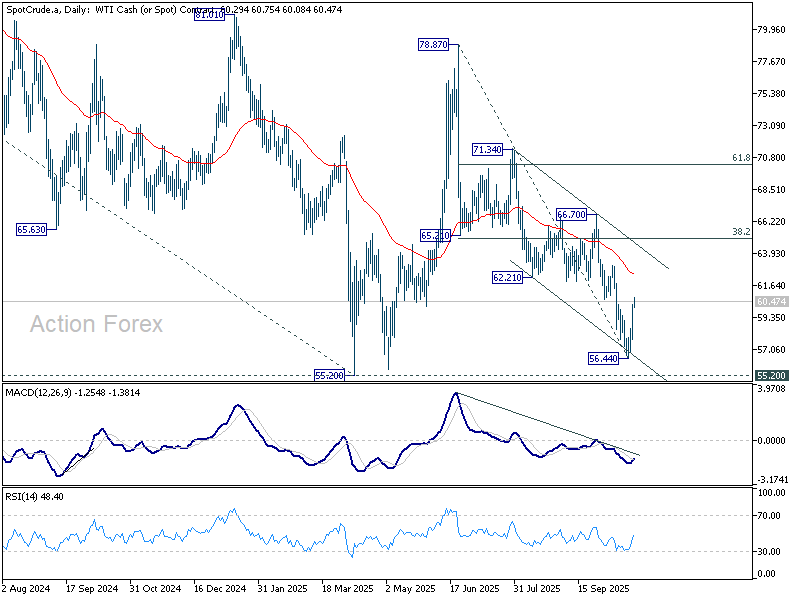

WTI climbs Past 60 after US sanctions on Russia Fall from 78.87 run its course?

Oil prices rebounded sharply today, with WTI crude rising back above the 60 mark, as geopolitical tensions re-entered focus after the Trump administration imposed new sanctions on Russia’s two largest oil producers, Rosneft and Lukoil.

The U.S. Treasury said the move was in response to Moscow’s “lack of serious commitment” to a peace process to end the war in Ukraine. Announcing the sanctions, Treasury Secretary Scott Bessent said “now is the time to stop the killing and for an immediate ceasefire,” warning that Washington is prepared to “take further action if necessary.” He urged U.S. allies to join in applying pressure on Moscow. Reports suggested that the new round of sanctions followed the collapse of a planned Trump–Putin meeting in Budapest, which had raised hopes for progress toward de-escalation.

The sanctions created a short-covering wave across crude futures, helping oil snap its recent losing streak. While demand signals remain mixed, the reemergence of supply-side uncertainty has stabilized sentiment, halting a multi-week slide that had dragged prices persistently.

Technically, the rebound has taken on added significance. The firm break above 59.47 resistance confirms that a short-term bottom has likely formed at 56.44, accompanied by bullish convergence in 4H MACD after testing the channel floor.

The focus now shifts to whether the fall from 78.87 has completed as a corrective move as second leg of the broader pattern from 55.20 (2025 low made in April).

In either case, further gains are favored toward key resistance zone between 62.21 support turned resistance and 55 EMA (now at 62.46). Sustained break above this area would strengthen the case for near-term bullish reversal, opening the way to 38.2% retracement of 78.87 to 56.44 at 65.00.

However, failure to clear this zone would suggest the rebound remains corrective, keeping risks skewed toward another dip back toward 55.20 before a more durable bottom forms.

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.62; (P) 151.84; (R1) 152.18; More...

Intraday bias in USD/JPY remains on the upside for retesting 153.26 resistance. Break there will resume larger rally from 139.87 to 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there would prompt upside acceleration to 161.8% projection at 158.80. On the downside, below 151.49 minor support will turn intraday bias neutral again first.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.