Sample Category Title

EUR/USD Consolidates Ahead of Potential Further Losses

Market sentiment remains dominated by escalating geopolitical tensions in Europe, which are dampening the euro's outlook and fuelling demand for traditional safe-haven assets, notably the US dollar.

The dollar's strength is further underpinned by the persistently hawkish rhetoric from the Federal Reserve. Officials continue to signal that interest rates will need to remain at their current levels for longer than previously anticipated. This stance is reinforced by resilient US inflation data, solidifying market expectations that the Fed will maintain its current policy course.

In stark contrast, the eurozone is grappling with a marked slowdown in business activity. The latest PMI data confirms a contraction across both manufacturing and services sectors. Against this deteriorating economic backdrop, the European Central Bank (ECB) has adopted a notably cautious tone, hinting at significant downside risks to growth. This growing monetary policy divergence with the US creates a fundamental imbalance, exacerbating the downward pressure on the single currency.

Consequently, the overall fundamental picture continues to favour the US dollar, suggesting further downside potential for the EUR/USD pair.

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, EUR/USD is forming a tight consolidation range around the 1.1600 level, following a clear impulsive decline. This price action suggests the development of a third wave down. A decisive break below this consolidation range would signal the resumption of the bearish impulse, with an initial target at 1.1488. This bearish technical outlook is confirmed by the MACD indicator, whose signal line remains below zero and is pointing downward, indicating sustained selling momentum.

H1 Chart:

The H1 chart shows the completion of a downward wave to 1.1576, followed by a corrective move to 1.1620, effectively outlining the current consolidation zone. A break above this range could trigger a short-lived correction towards 1.1655 before the broader downtrend resumes, targeting 1.1500. Conversely, a break below the range would directly activate the bearish wave towards 1.1488, which is projected to complete the first leg of the larger third wave down. The Stochastic oscillator aligns with this view, with its signal line turning down from the 80 level and heading towards 20, reflecting building bearish momentum in the short term.

Conclusion

The combination of a supportive fundamental backdrop for the dollar and a deteriorating outlook for the eurozone maintains a bearish bias for EUR/USD. Technically, the pair appears to be pausing within a broader downtrend, with a breakdown below 1.1600 likely to trigger the next leg lower towards 1.1488.

WTI Oil: Crude Rallies Above $60 on Fresh US Sanctions and US Million-Barrel Purchase

Finding support at 6-month lows of around $56.40 per barrel, WTI has rallied just shy of 8.6% in the last three sessions alone.

Currently trading at $62.04, up 4.10% in yesterday’s session, recent performance marks the best three-day stint since late July.

As ever, let’s take a look at some of the macro themes at play, followed by some technical analysis as we attempt to answer the immortal question: what’s next for WTI?

WTI (West Texas Intermediate): Key takeaways 24/10/2025

- Gapping up 1.1% at Thursday’s open, WTI crude has found renewed buying support on new sanction announcements from the United States on leading Russian oil companies, including Rosneft and Lukoil

- Constrained previously by logistical problems of safe storage, and of course, funding issues, the US Department of Energy confirmed on Tuesday its intentions to purchase 1 million barrels of crude oil to replenish reserves, bolstering crude gains

- Otherwise, and in the bigger picture, a cloud of oversupply fears lingers over crude oil markets, especially considering record output from non-OPEC+ members

WTI (West Texas Intermediate): Where were we?

It’s high time I returned to my commentary roots and wrote some more coverage on crude oil markets.

Although it would be fair to say that oil has played second fiddle to precious metals in recent months, both in terms of market interest and, indeed, performance.

With that said, this appears to be changing, with recent geopolitical developments offering some welcome upside and, crucially, boosting WTI pricing above $60 for the first time since earlier this month.

WTI Crude Oil (WTICOUSD), D1 year-to-date, OANDA, TradingView, 23/10/2025

Without further ado, let’s break down some major macroeconomic themes and conclude with some market technicals, including some price targets.

WTI (WTICOUSD): Fundamental Analysis 24/10/2025

New US sanctions on Russian oil: Reported Wednesday, the United States announced new sanctions on Russian oil exports, following an apparent breakdown in ceasefire negotiations between Russia and Ukraine.

U.S. Department of the Treasury, Press Releases, 22/10/2025

Read the full press release here

Coming only one day after Trump shelved a planned meeting in Budapest with Putin, it would seem that frustrations are running high after the demands of an immediate ceasefire have fallen on deaf ears.

"I don’t want to have a wasted meeting. I don’t want to have a waste of time, so I’ll see what happens. We did all of these great deals, great peace deals, they’re all peace deals. Agreements, solid agreements every one of them"

President Donald Trump, speaking to reporters at the White House, 21/10/2025

Clearly, the sanctions are intended as a bargaining tool to help encourage a peace deal, but at least so far, words from the Kremlin suggest that the Russian domestic oil industry will remain largely unaffected, boasting of its level of immunity from Western sanctions.

While Trump hopes the economic impact of new sanctions will encourage Putin to return to the negotiating table, only time will tell how effective these measures will be.

As for oil pricing, the associated fallout raises questions about supply, which is a positive development for pricing. This holds even more true when considering that the market narrative has been almost exclusively one of oversupply - the most recent geopolitical developments question this assumption somewhat, especially if tensions escalate.

US to buy 1 million crude barrels to replenish reserves: I think most would agree that, especially when compared to previous presidents, Trump shares a very particular relationship with the crude oil markets. After all, who could forget this legendary catchphrase?

@realDonaldTrump, TruthSocial, 23/06/2025

If put simply, however, Trump policy surrounding crude oil centers almost exclusively revolves around two core tenets:

- To maintain America’s lead as #1 producer of crude oil worldwide, therefore establishing control over supply

- To keep oil prices low to promote economic growth

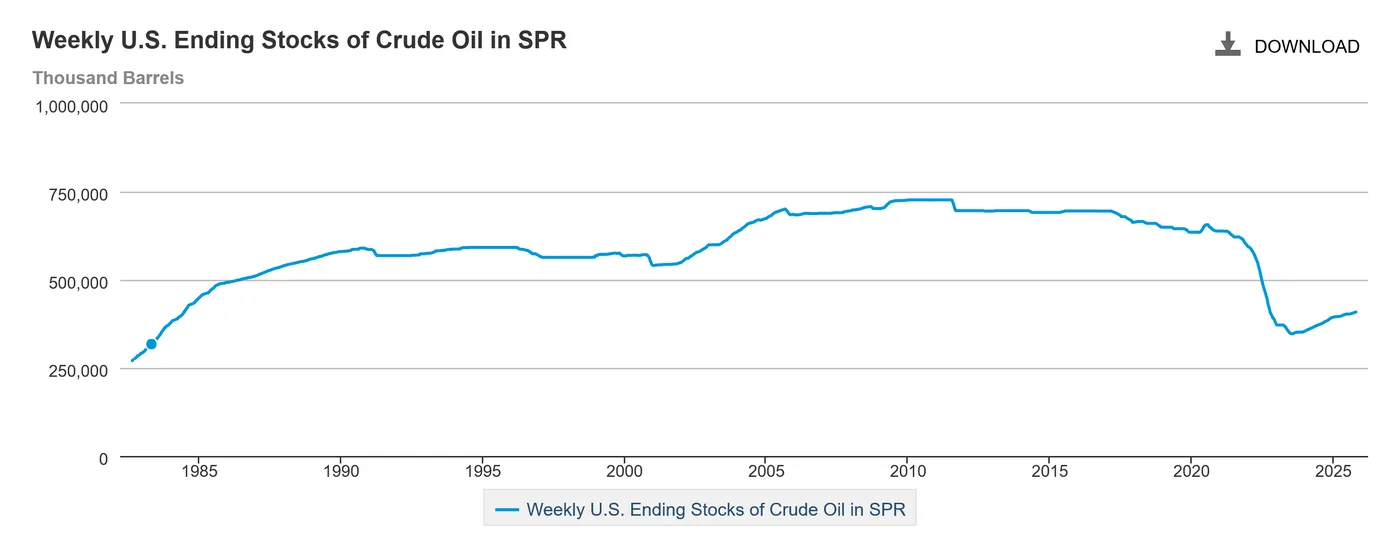

On this basis, the latest development is the intent to purchase 1 million barrels of crude oil to replenish the Strategic Petroleum Reserve (SPR), which recently saw record levels of depletion under the administration of former President Joe Biden.

US Energy Information Administration (EIA), Weekly U.S. Ending Stocks of Crude Oil in SPR, 23/10/2025

Being previously constrained by logistical matters and, of course, funding, the EIA will undoubtedly want to capitalise on historically low crude oil prices to increase its stockpile.

Naturally, markets have interpreted this information as positive for crude oil, helping to boost pricing.

Non-OPEC+ members report record crude output: While not as contemporaneous as the other two themes, a significant macro headwind continues to dictate the direction of crude markets: the fear of oversupply.

Most recently, this is reflected in record output from non-OPEC countries, which have contributed to the current bearish bias. Otherwise, the aforementioned EIA has also confirmed sustained high levels of production.

While there have been some attempts to stagger output increases by OPEC, which have proved limited in effectiveness, with crude oil inventories rising globally.

In a nutshell, although the previous two themes are bullish for crude oil, the longer-term bias likely remains bearish from a supply standpoint.

WTI (WTICOUSD): Technical Analysis 24/10/2025

WTI Crude Oil (WTICOUSD), D1, OANDA, TradingView, 24/10/2025

While recent upside has been impressive, rallying by almost 8.6%, there is still plenty of work to be done if oil is to break the current downtrend.

While on a macro level, the narrative surrounding supply would have to change significantly to support this, technically, here’s some level to watch to the upside:

Price targets and support/resistance levels:

- Price target #1 - Previous support turned resistance - $62.564

- Price target #2 - $63.564 - 61.8% Fib

What is encouraging, however, is that one of my personal favourite indicators, the SSL channel, has flipped to report a bullish bias. While this can occur during periods of market consolidation, when combined with a rising OBV volume, it may perhaps signify that a larger change is afoot.

With that said, price action remains overwhelmingly bearish, assuming crude cannot break above ~$63.564, which might shake things up somewhat.

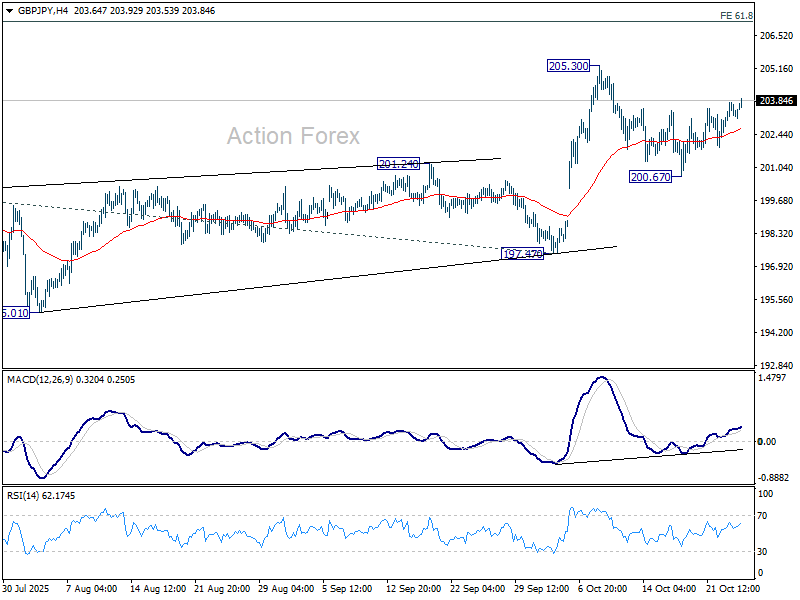

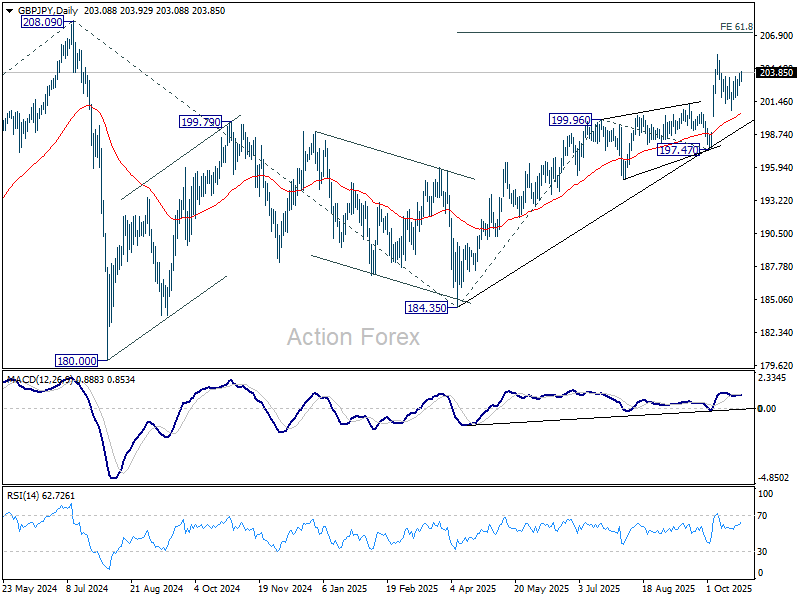

GBP/JPY Daily Outlook

Daily Pivots: (S1) 202.85; (P) 203.33; (R1) 203.83; More...

Intraday bias in GBP/JPY remains on the upside for retesting 205.30. Firm break there will resume larger rally to 61.8% projection of 184.35 to 199.96 from 197.47 at 207.11. For now, risk will stay on the upside as long as 200.67 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 will dampen this view and could extend the corrective pattern with another fall.

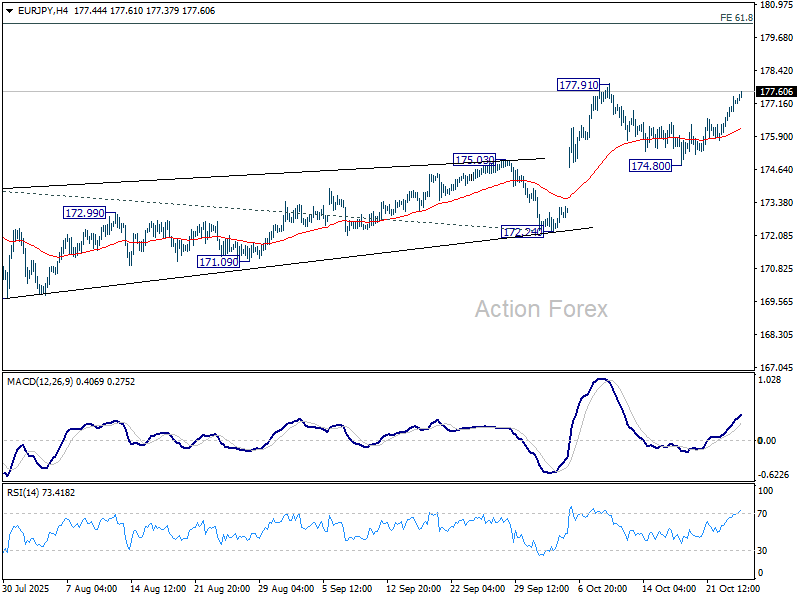

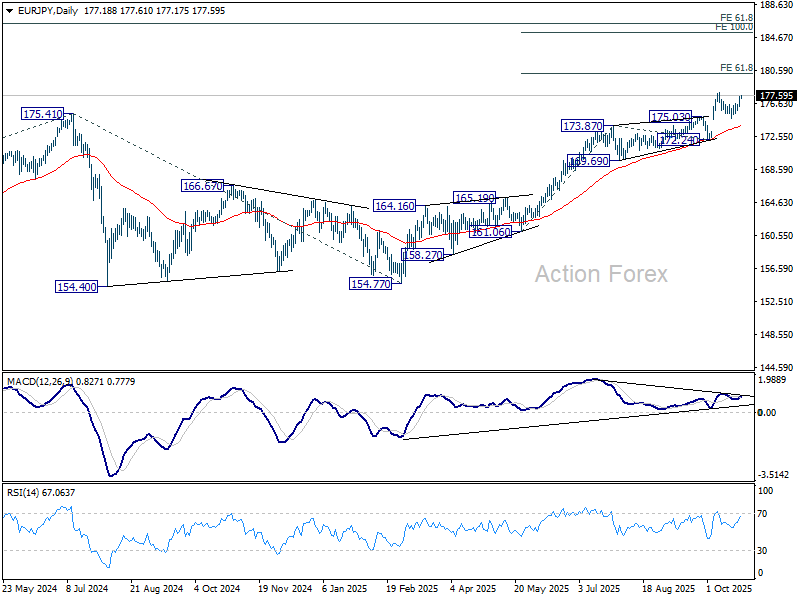

EUR/JPY Daily Outlook

Daily Pivots: (S1) 176.58; (P) 177.01; (R1) 177.72; More...

Intraday bias in EUR/JPY remains on the upside for retesting 177.91. Firm break there will resume larger up trend to 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next. For now, risk will stay on the upside as long as 174.80 support holds, in case of retreat.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Firm break of 172.24 support will suggests that it has turned into consolidations again. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 167.43) holds, even in case of deep pullback.

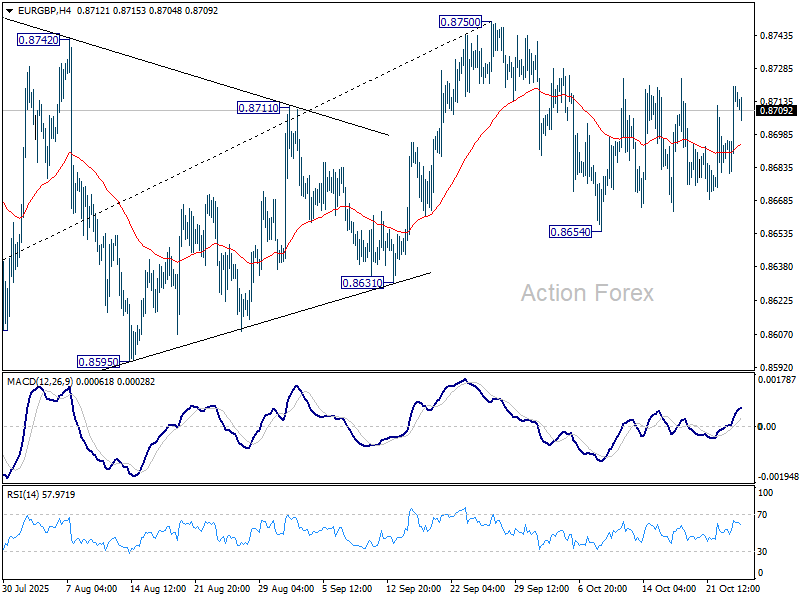

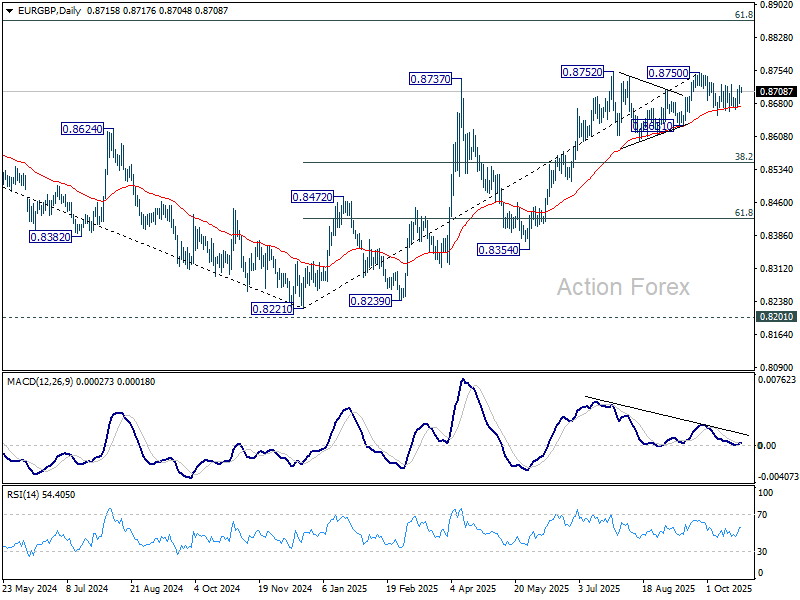

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8692; (P) 0.8707; (R1) 0.8732; More…

Range trading continues in EUR/GBP and intraday bias stays neutral. On the downside, break of 0.8654 will resume the fall from 0.8750 to 0.8631 support. Decisive break there will indicate bearish reversal and target 38.2% retracement of 0.8221 to 0.8750 at 0.8548. Nevertheless, on the upside, break of 0.8750/2 will resume the rise from 0.8221 towards 0.8867 fibonacci level.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8631 support will be the first sign that this corrective bounce has completed. Sustained trading below 55 W EMA (now at 0.8549) will confirm, and bring retest of 0.8221 low.

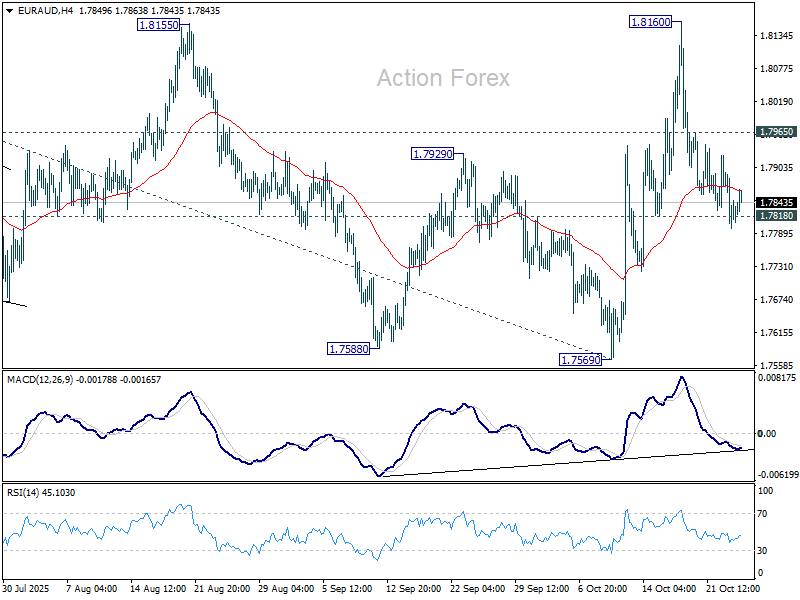

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7792; (P) 1.7848; (R1) 1.7897; More...

EUR/AUD breached 1.7818 support but quickly recovered. Intraday bias stays neutral first. On the upside, above 1.7965 will turn bias back to the upside for retesting 1.8160 first. Firm break there will affirm the case that larger up trend is resuming, and target 1.8554 high next. On the downside, however, firm break of 1.7818 will dampen this bullish view and turn focus back to 1.7569 support instead.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern, which might have completed already. Firm break of 1.8554 will resume larger up trend from 1.4281 (2022 low), and target 61.8% projection of 1.5963 to 1.8554 from 1.7569 at 1.9170. Nevertheless, break of 1.7569 support will delay the bullish case and extend the correction from 1.8554.

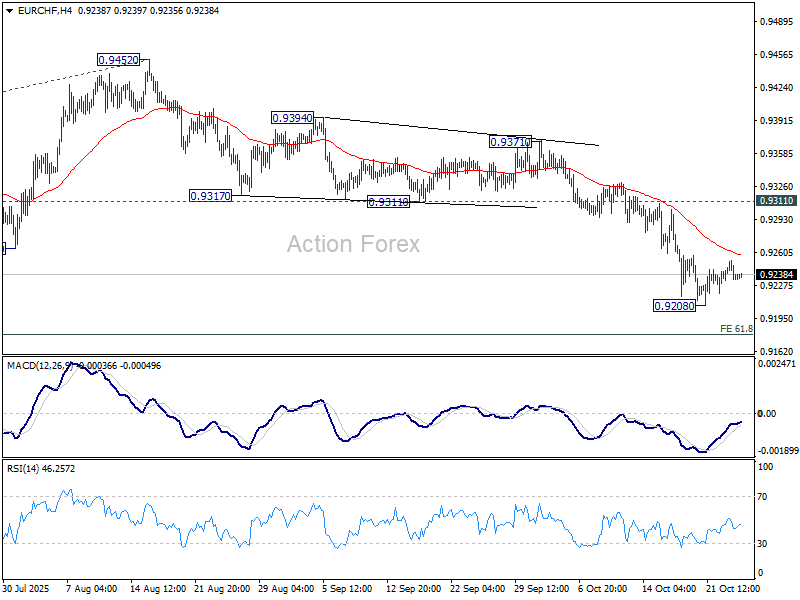

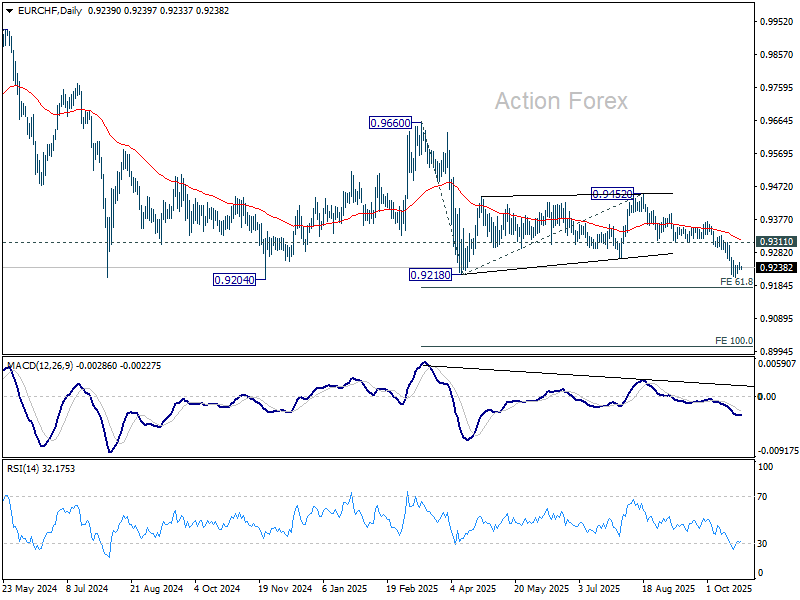

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9231; (P) 0.9242; (R1) 0.9250; More....

EUR/CHF is staying in consolidations above 0.9208 and intraday bias remains neutral. Outlook will remain bearish as long as 0.9311 support turned resistance holds. On the downside, break of 0.9208 will target 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179. Firm break there will target 100% projection at 0.9010.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9390). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.

Even as ECB in Firm Wait-and-See Modus, Markets Not Convinced on EU Eco Momentum

Markets

Different market segments to some extent again focused on different markets themes/drivers. Core yields showed tentative signs of bottoming yesterday, after a protracted decline throughout most of this month. A jump in oil prices (Brent $65.75 p/b currently compared to low $60 p/b early this week) after the US announced sanctions against the two largest Russian Oil companies made investors’ pondering recent gradual easing in inflation expectations. Uncertainty ahead of today’s US CPI release probably also injected some caution. US yields yesterday rebounded between 4.5 bps and 5.6 bps with the belly of the curve slightly underperforming. The US 10-y yield is testing the 4% barrier. European yields followed at a distance with German yields rising about 2 bps across the curve. The rise in oil prices/higher yields hardly had any (negative) impact on equity markets. Equity investors apparently focused on a potential easing of trade tensions between the US and China as US president Trump and Chinese President Xi Jinping will meet next week. US indices added between 0.31% (Dow) and 0.89% (Nasdaq). No clear tend in for USD trading yet. EUR/USD closed marginally higher at 1.1618. The yen still underperforms (USD/JPY close at 152.6). EUR/GBP closed north of 0.87 as markets are still considering the timing of further BoE easing after this week’s better/less worse than expected UK inflation data.

Eco data for once might capture the market focus today with the EMU and US September PMI’s and the (delayed) US September CPI. The EMU composite PMI is expected to confirm sluggish growth at the start of Q4 (51.1). Even as the ECB is in a firm wait-and-see modus, markets recently were not convinced on the EU eco momentum, raising the implied probability of an additional rate cut next year to >50%. EMU yields and EUR/USD still might be a bit more sensitive to negative news rather than to in line/slightly better data. In the US, September headline CPI is expected to accelerate to 0.4% M/M and 3.1% Y/Y (from 2.9%). Core inflation is seen unchanged from August at 0.3% M/M and 3.1% Y/Y. Such data would only confirm rather stubborn inflation since April. Even so, with the Fed focus shifting to labour market softness rather than inflation, it’s unlikely the report will profoundly change expectations on the Fed further reducing policy tightening by 25 bps next week and in December, bringing it closer to neutral. Given the Fed focus on the labour market/economic activity, the US PMI’s (composite expected at 53.5 from 53.9) and, to a lesser extent, (final) Michigan consumer confidence also deserve attention. Overall, we see a slightly higher chance for US yields to take a breather after recent decline. It’s probably too early to step up expectations on the pace of further Fed easing next year. EMU yields might be a bit more vulnerable in case of negative news. In this context, the dollar might have slightly better cards compared to the euro. The 1.1542/43 area marks first intermediate support. In the UK, consumer confidence and especially September retail sales were much stronger than expected. In a first reaction, EUR/GBP is ceding some ground but for new still holds north of 0.87.

News & Views

Japanese headline inflation accelerated to 2.9% from 2.7% in September. The gauge excluding fresh food (preferred by the Bank of Japan) was a copy paste while the series without both fresh food and energy eased to 3% from 3.3%. Services CPI slowed to 1.4% from 1.5%. The waiver of child fees in Tokyo and slower gains in dining out on a drop in (still-elevated) rice prices are among the reasons cited. Other labor-intensive services showed quicker price rises. The umpteenth above-target (3%) reading is unlikely to result in a rate hike next week as reports suggested the BOJ sees no urgency to do so just yet. It may first need a clearer view on domestic policies by the freshly announced PM Takaichi. Japanese data also included the October PMIs. They all eased from last month with the composite signaling the slowest growth since May (50.9). Services momentum is dwindling (52.4 from 53.3) and manufacturing remains stuck in decline. The latter has become more upbeat on the year ahead though. Price indicators continue to point at strong inflationary pressures. JPY loses ground this morning with USD/JPY pushing towards 153.

US president Trump said he’ll terminate all trade negotiations with Canada. That announcement came after he having seen a Canadian advertisement in which former Republican president Reagan hailed the benefits of free trade and slammed tariffs. Trump said the move appears timed to interfere with the Supreme Court case that’s looking in the legality of his Liberation Day levies. It’s scheduled to hear oral arguments on November 5. It’s not the first time Trump has threatened to call off trade talks but the Loonie nevertheless is feeling selling pressures. USD/CAD this morning rises above 1.40.

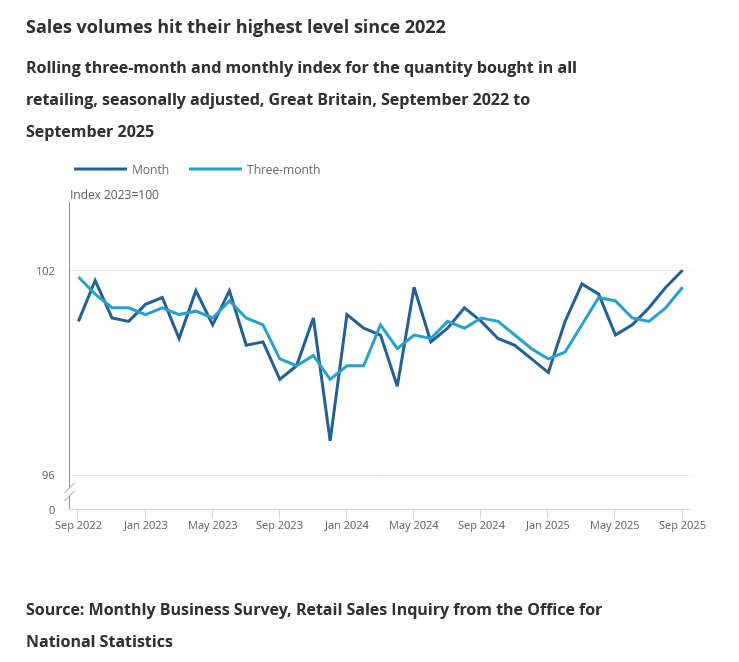

UK retail sales rise 0.5% mom in September, hitting highest level mid-2022

UK retail activity surprised to the upside in September, with sales volumes rising 0.5% mom, defying expectations of a -0.2% mom decline. The gain marked the fourth consecutive monthly increase, lifting total sales to their highest level since July 2022. Stronger non-store and clothing sales helped offset weakness in fuel and other discretionary categories.

Over the third quarter, retail volumes grew 0.9% compared with the previous quarter, confirming a steady rebound in household demand through the summer. The good weather in July and August was cited as a key driver, boosting clothing sales and supporting outdoor-related spending. Online and non-store retailers also enjoyed sustained gains.

Finally, Data

Trade tensions between the US and China eased — after flaring up, easing and flaring up again over recent weeks — on news that Trump and Xi will meet next Thursday at a summit in Asia. Optimism, however, is fragile after Trump said trade talks with Canada were terminated due to an ad opposing US tariffs that targeted Republican-held districts and used Ronald Reagan’s words. There’s no guarantee the US-China meeting will happen or lead to a durable truce — I’m extremely skeptical — but it would mark the first face-to-face encounter since Trump returned to the White House and follow a wild ride of tariff and chip wars that have only intensified since January.

Make no mistake: Xi knows that America won’t be an ideal partner for China, with or without Trump in the White House. Relations may have been less chaotic before, but the first chip export restrictions actually came during the Biden administration — and China remains determined to gain tech independence from the West. And it’s doing well. The country now has its own tech giants, social media platforms, communication systems, EVs, smartphones, robots and chips. Beijing wants those tech leaders to use homegrown components to keep production in-house. Many domestic chipmakers are thriving. SMIC shares, for instance, have soared nearly 500% since last September Alibaba has climbed up to 140% since DeepSeek’s chatbot launch early this, and the Hang Seng Index has recovered roughly two-thirds of its post-2018 selloff. With limited foreign investor exposure and Beijing’s clear push to make the sector shine, Chinese tech could still have room to run.

Returning to the trade story — the Trump-Xi meeting next Thursday could keep hope, and the bears, at bay for now.

Meanwhile, the prospect of robust tech earnings and lower Fed rates continues to sweeten investor sentiment. Earnings from Netflix, Tesla, IBM, Super Micro Computer and SAP came in mixed, but markets are now in wait-and-see mode ahead of next week, when the AI heavyweights are expected to deliver standout results and the Federal Reserve (Fed) a 25bp cut.

Finally some data! Economic data remains scarce due to the ongoing US government shutdown, but the Bureau of Labor Statistics decided to publish September CPI figures today to give policymakers and investors some direction ahead of next week’s decision. Both headline and core inflation are expected to land around 3.1% YoY for September, and some analysts warn CPI could rise toward 3.5% in the coming months amid tariff-driven pressures. That’s well above the Fed’s 2% target, but markets broadly believe the central bank will tolerate higher inflation to avoid an economic meltdown.

Even so, inflation remains an issue. Today’s numbers are unlikely to be a game-changer if they align with the 3% expectation. A softer print could fuel speculation of a third rate cut in December, boosting risk appetite while dragging US yields and the dollar lower. Conversely, a stronger CPI could trigger a reassessment of dovish expectations and raise questions about whether major indices deserve to keep pushing into uncharted highs.

Despite risks, global equities continue to rally. The S&P 500 and Nasdaq keep hitting records — largely on AI enthusiasm — while the Dow Jones, Stoxx 600, and even the FTSE 100 are near all-time highs. Indices, of course, don’t always reflect underlying fundamentals, but in a high-inflation environment, equities remain one of the few ways to keep pace with price pressures. For now, despite bubbling bubble concerns, consensus still points to an extension of the global rally — unless US inflation data challenge that view before the weekly close. In the absence of a big deviation, focus will remain squarely on the Fed and earnings.

In FX, the US dollar held firm this week — stronger than expected given the extended government shutdown — as political headlines elsewhere offset dollar weakness. French political turmoil kept the euro under pressure, while Takaichi’s appointment as Japan’s new prime minister push the USDJPY higher on expectations of a softer Bank of Japan (BoJ) stance.

In metals and energy, gold is consolidating just above $4,100 per ounce, suggesting the early-week selling pressure has eased alongside volatility. US crude tested but failed to sustain gains above its 50-day moving average near $62.50/bbl after new sanctions targeting two Russian oil giants triggered conflicting reports on whether India might halt Russian oil imports to avoid secondary sanctions. From a technical standpoint, recent headlines have likely exhausted their upside potential, leaving room for a minor correction into the weekly closing bell.