Sample Category Title

AUD/USD Weekly Report

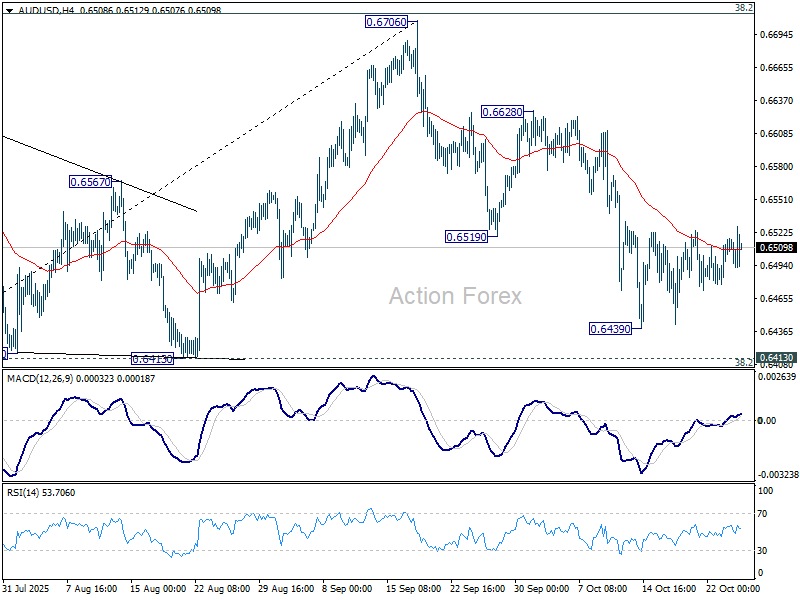

AUD/USD extended consolidations above 0.6439 last week and outlook is unchanged. Initial bias remains neutral this week first. Further decline is in favor as long as 55 D EMA (now at 0.6538) holds. Below 0.6439 will target 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403. Decisive break there will indicate bearish reversal after rejection by 0.6713 fibonacci level. Nevertheless, sustained trading above 55 D EMA will keep the rise from 0.5913 intact, and bring retest of 0.6706 high.

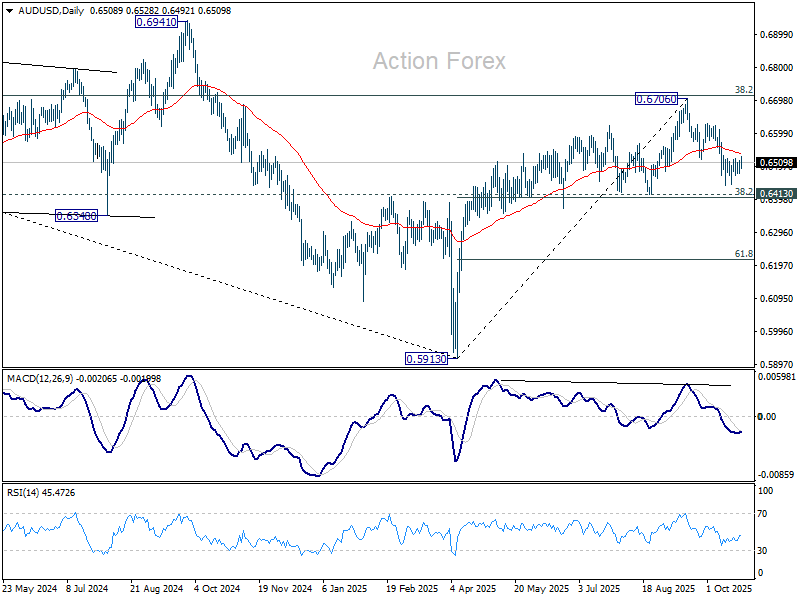

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

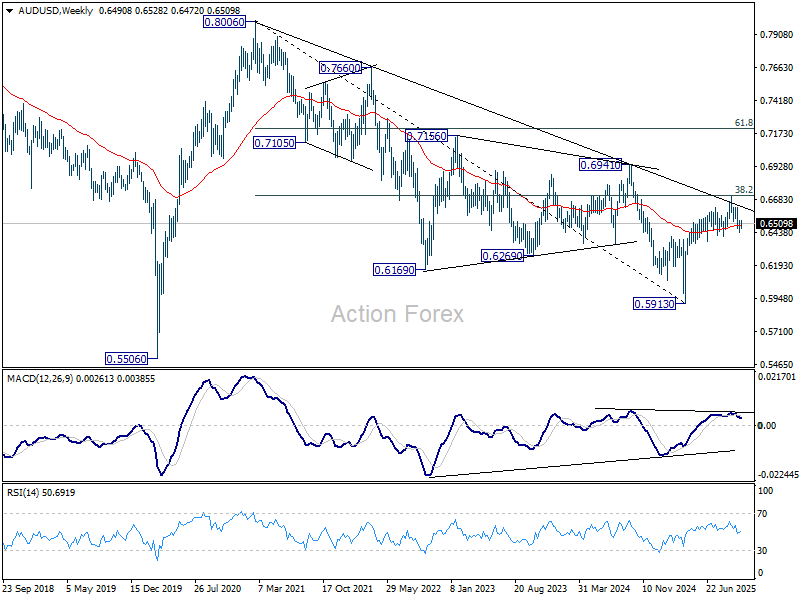

In the long term picture, fall from 0.8006 is seen as the second leg of the corrective pattern from 0.5506 long term bottom (2020 low). Hence, in case of deeper decline, strong support should emerge above 0.5506 to contain downside to bring reversal. On the upside, firm break of 0.6941 will argue that the third leg has already started back to 0.8006.

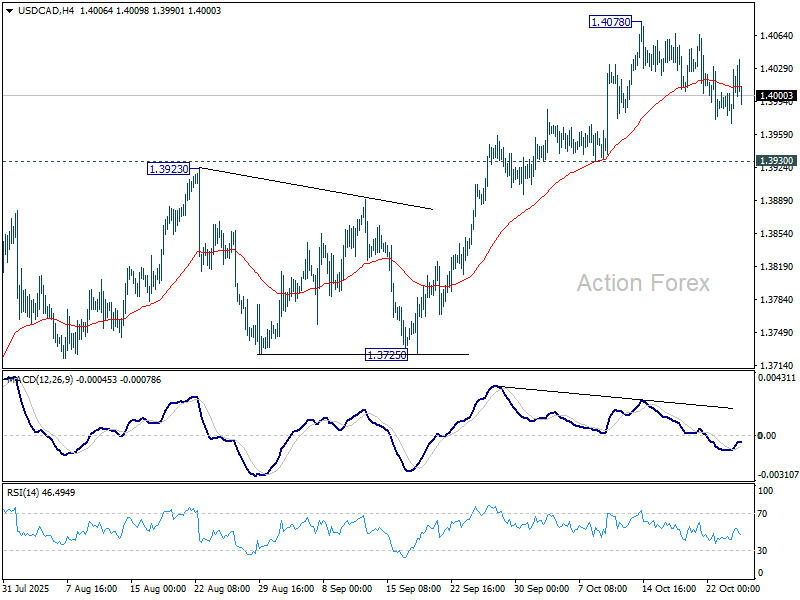

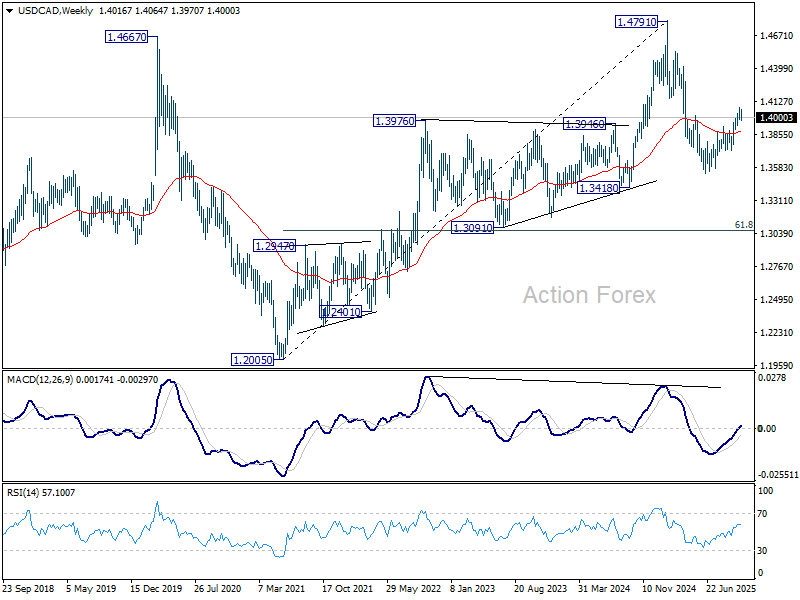

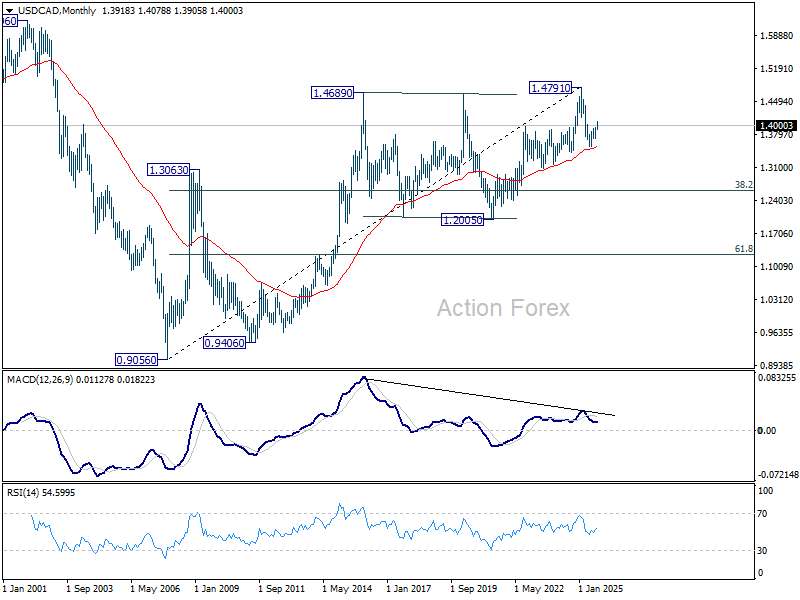

USD/CAD Weekly Outlook

USD/CAD stayed in consolidations last week and outlook is unchanged. Initial bias remains neutral this week, and further rally is expected as long as 1.3930 support holds. Break of 1.4078 will resume the rise from 1.3538 to 61.8% retracement of 1.4791 to 1.3538 at 1.4312.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds.

In the long term picture, 55 M EMA (now at 1.3525) remains intact. Thus, up trend from 0.90567 (2007 low) should still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction.

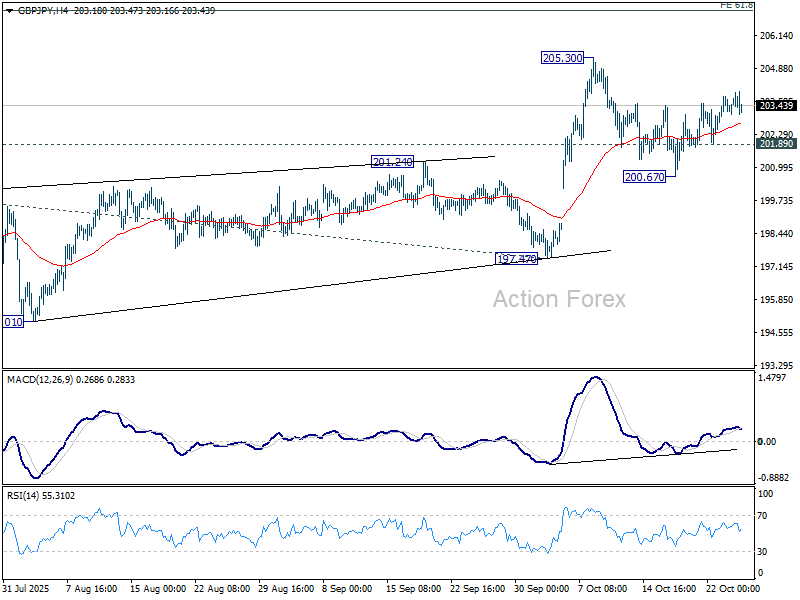

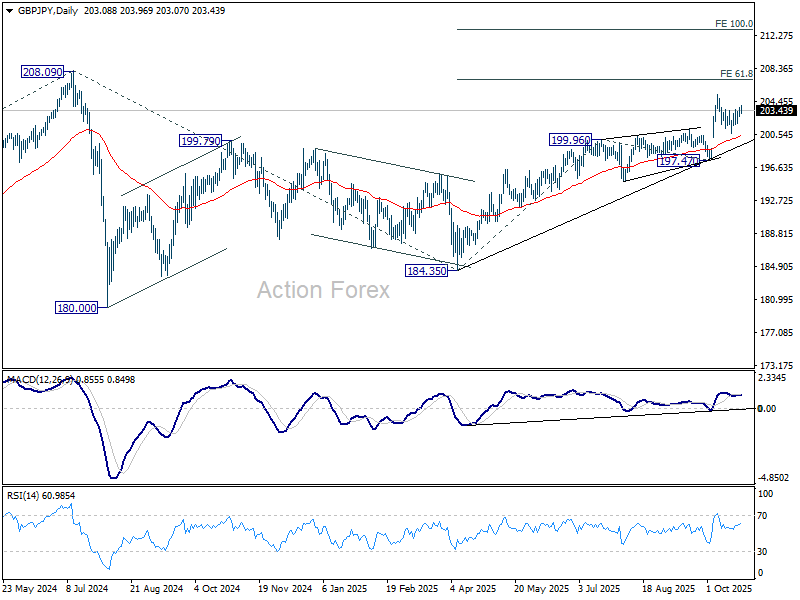

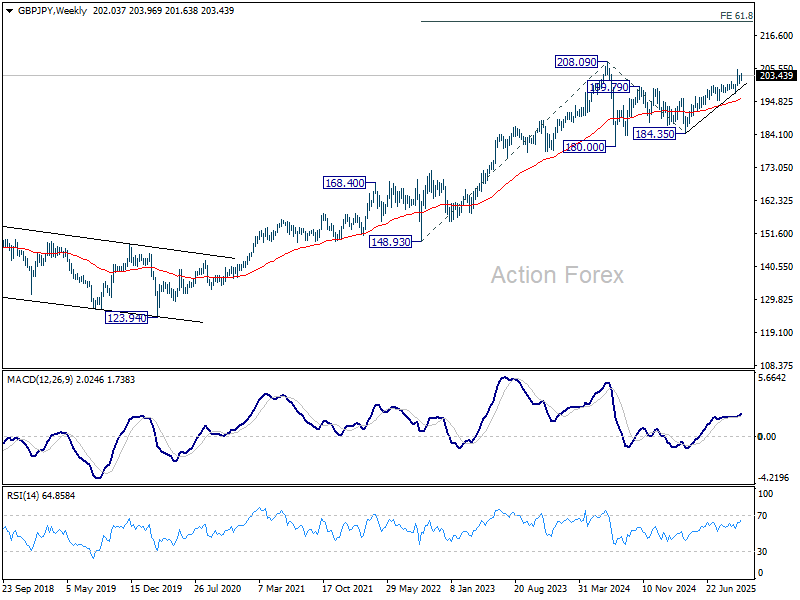

GBP/JPY Weekly Outlook

GBP/JPY's rebound last week suggests that pullback from 205.30 has completed at 200.67 already. Initial bias stays mildly on the upside for retesting 205.30 first. Firm break there will resume larger rise to 61.8% projection of 184.35 to 199.96 from 197.47 at 207.11. However, break of 201.89 will turn bias to the downside to extend the pattern from 205.30 with another falling leg.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

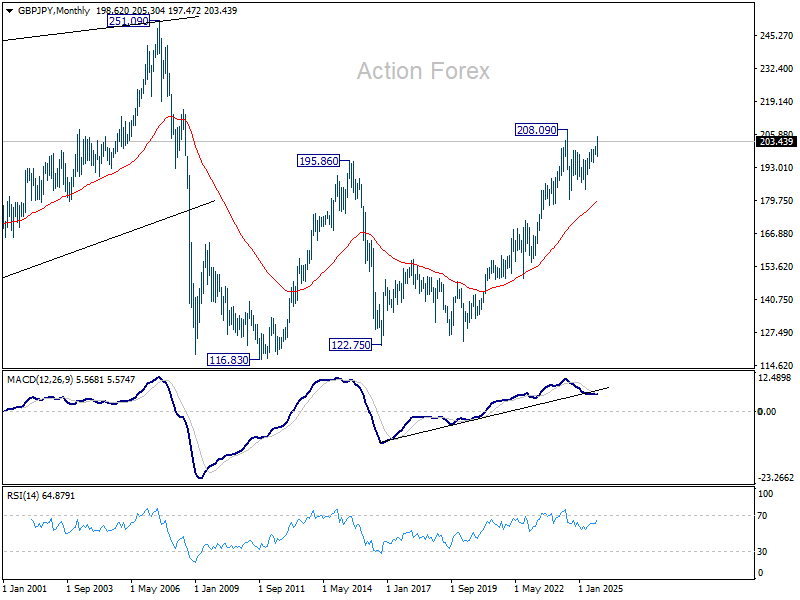

In the long term picture, there is no sign that the long term up trend from 122.75 (2016 low) has concluded. But firm break of 208.09 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.

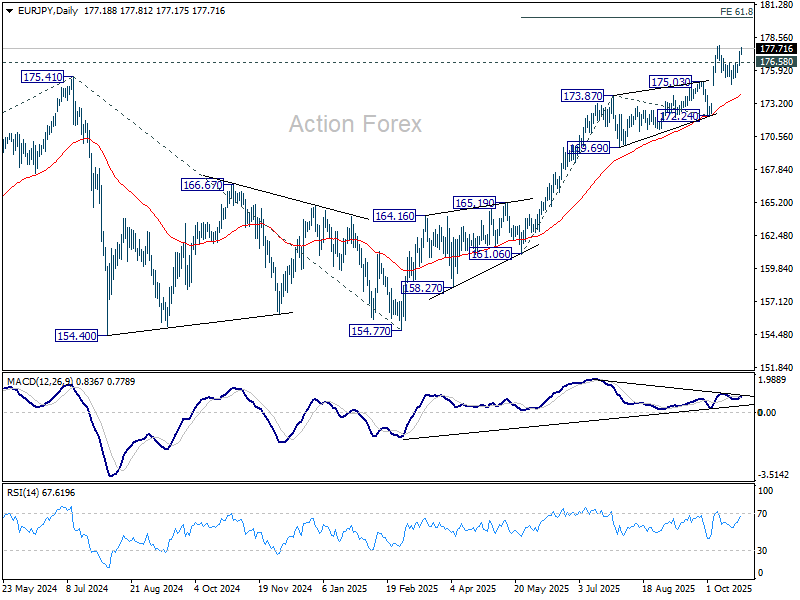

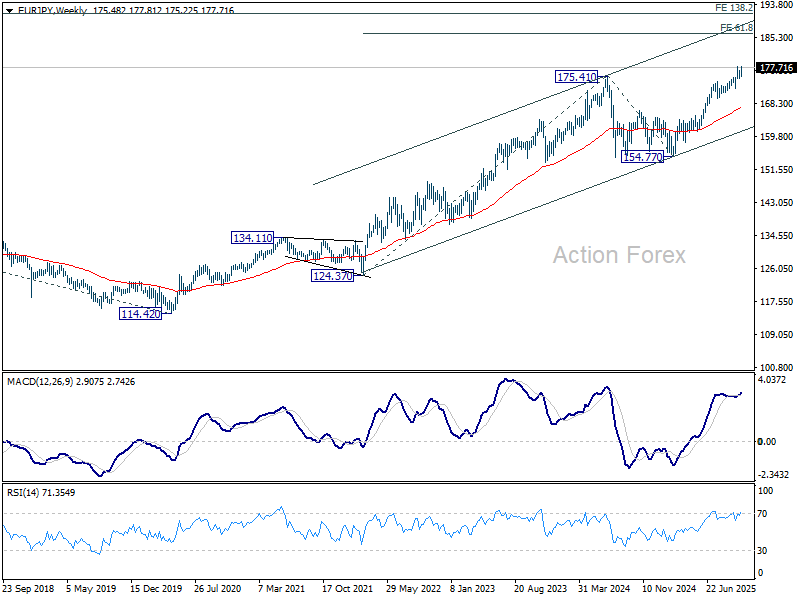

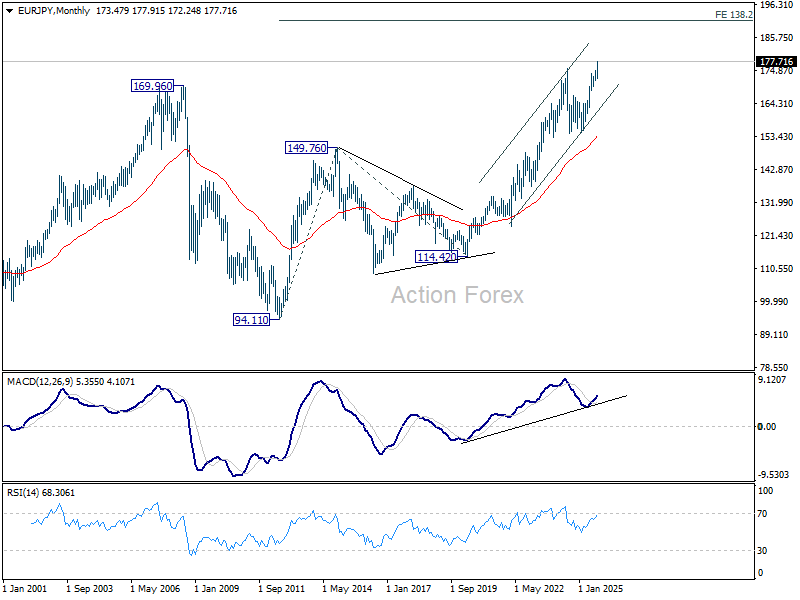

EUR/JPY Weekly Outlook

EUR/JPY's extended rebound last week suggests that pullback from 177.91 has completed at 174.80 already. Initial bias stays on the upside this week. Firm break of 177.91 will confirm larger up trend resumption, and target 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next. On the downside, though, below 176.58 will turn bias to the downside and extend the corrective pattern form 177.91 with another falling leg.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Firm break of 172.24 support will suggests that it has turned into consolidations again. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 167.16) holds, even in case of deep pullback.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

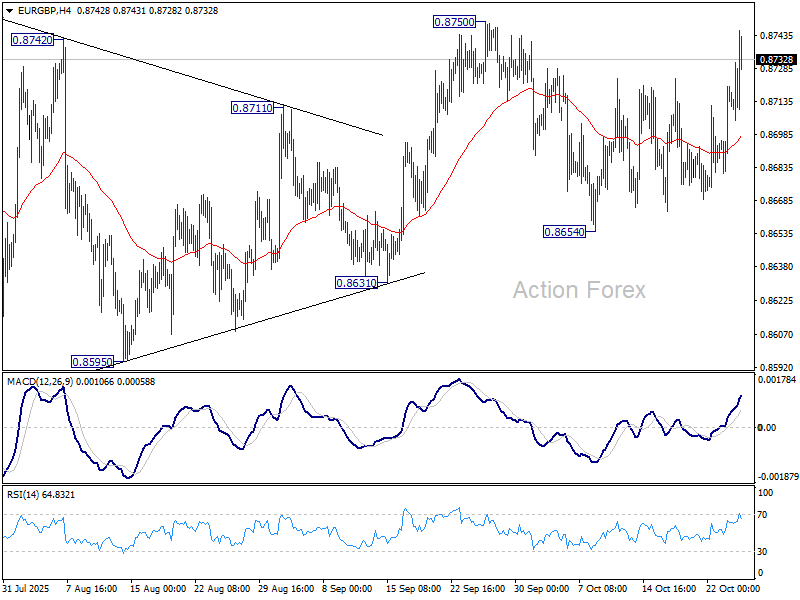

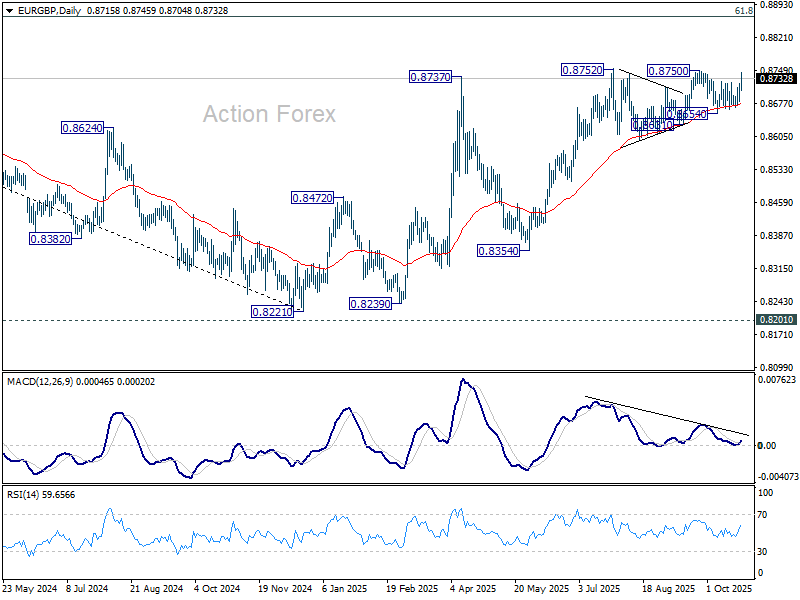

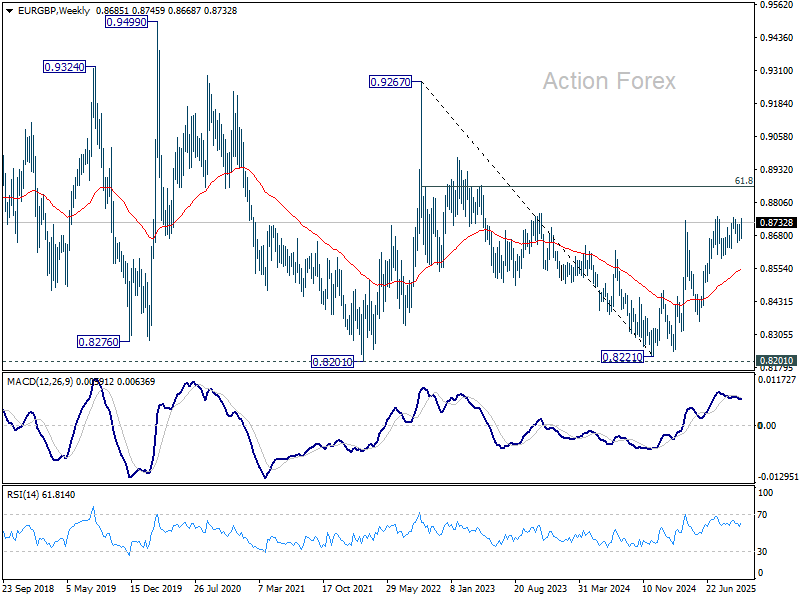

EUR/GBP Weekly Outlook

EUR/GBP's strong rally last week argues that pullback from 0.8750 might have completed, after drawing support from 55 D EMA (now at 0.8672). Initial focus is now on 0.8750 resistance this week. Firm break there will resume larger rise from 0.8221 to 0.8867 fibonacci level. On the downside, through, break of 0.8654 support will now indicate near term bearish reversal.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8654 support will be the first sign that this corrective bounce has completed. Sustained trading below 55 W EMA (now at 0.8556) will confirm, and bring retest of 0.8221 low.

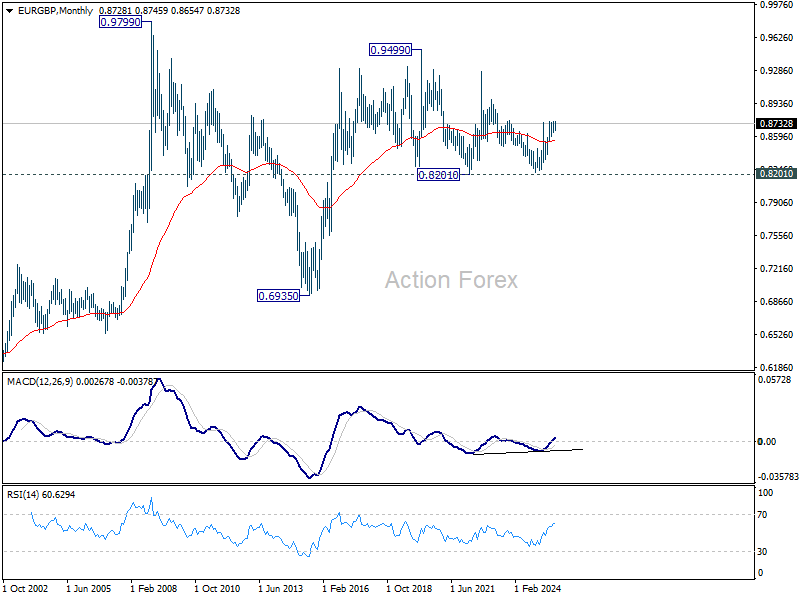

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

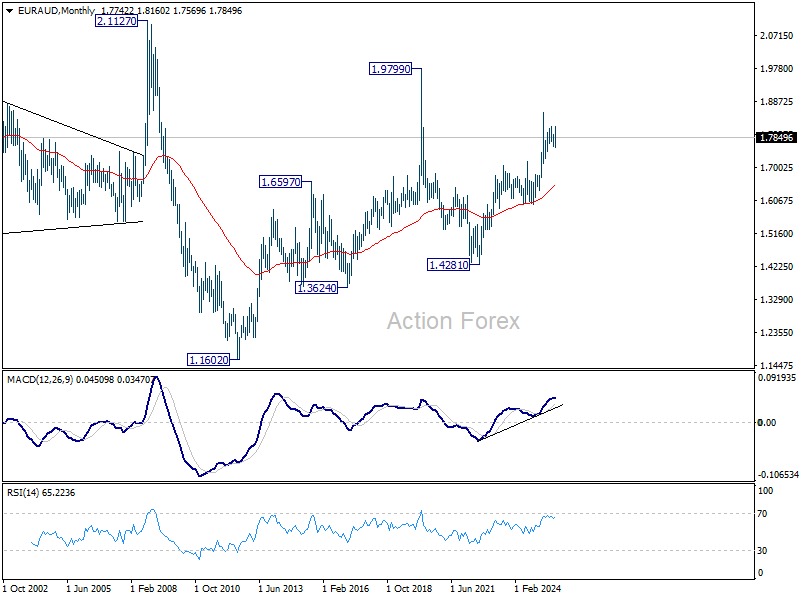

EUR/AUD Weekly Outlook

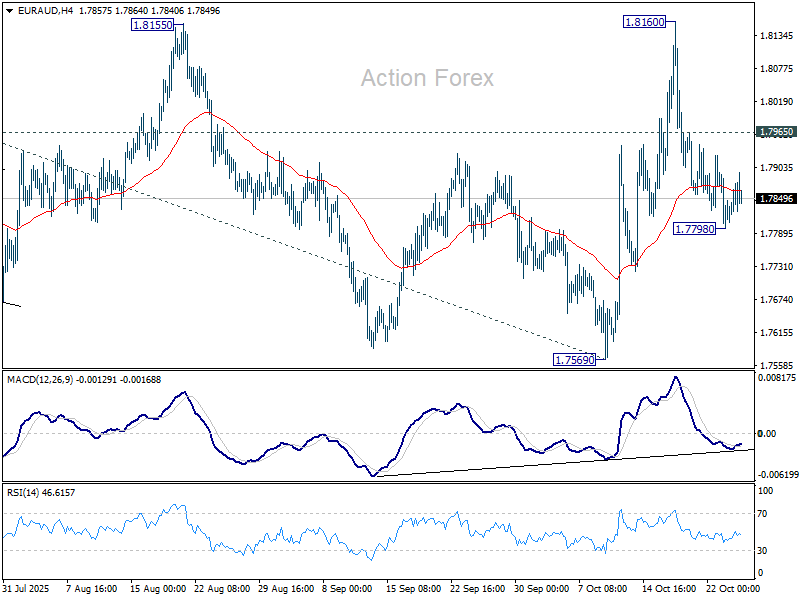

EUR/AUD's pullback was a little deeper than expected last week, but it nonetheless recovered after hitting 1.7798. Initial bias remains neutral first. On the upside, break of 1.7965 minor resistance will bring retest of 1.8160. Firm break there will solidify the case that larger up trend is resuming. However, below 1.7798 will dampen this week and suggest that corrective pattern from 1.8554 is still extending. In this case, deeper fall should be seen to 1.7569 support instead.

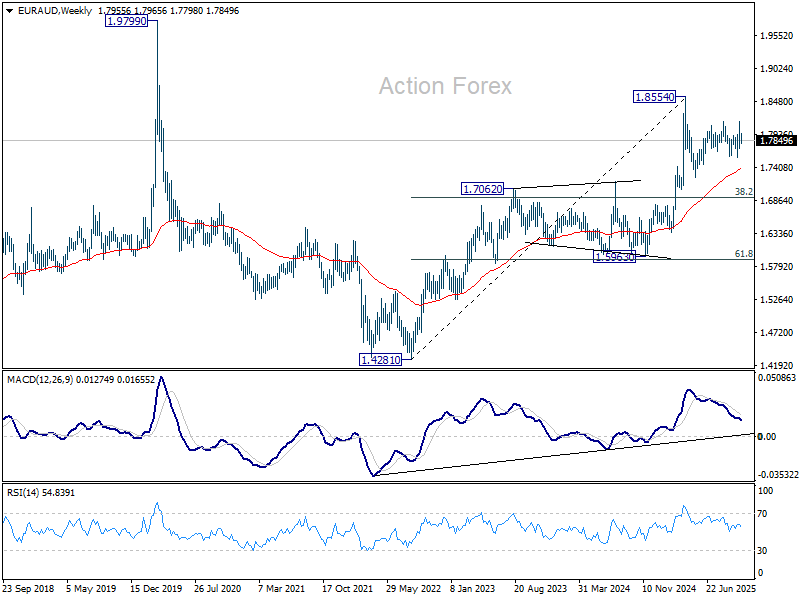

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern, which might have completed already. Firm break of 1.8554 will resume larger up trend from 1.4281 (2022 low), and target 61.8% projection of 1.5963 to 1.8554 from 1.7569 at 1.9170. Nevertheless, break of 1.7569 support will delay the bullish case and extend the correction from 1.8554.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6506) holds, this second leg could still extend higher.

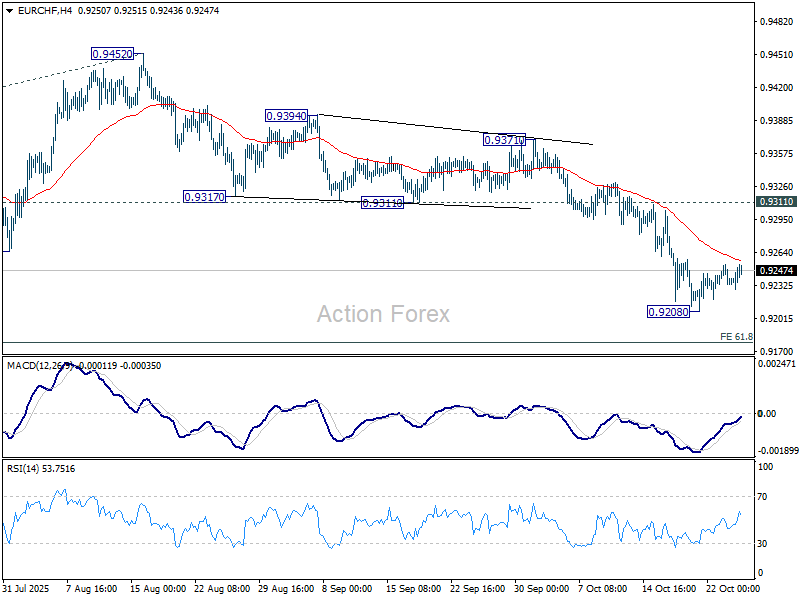

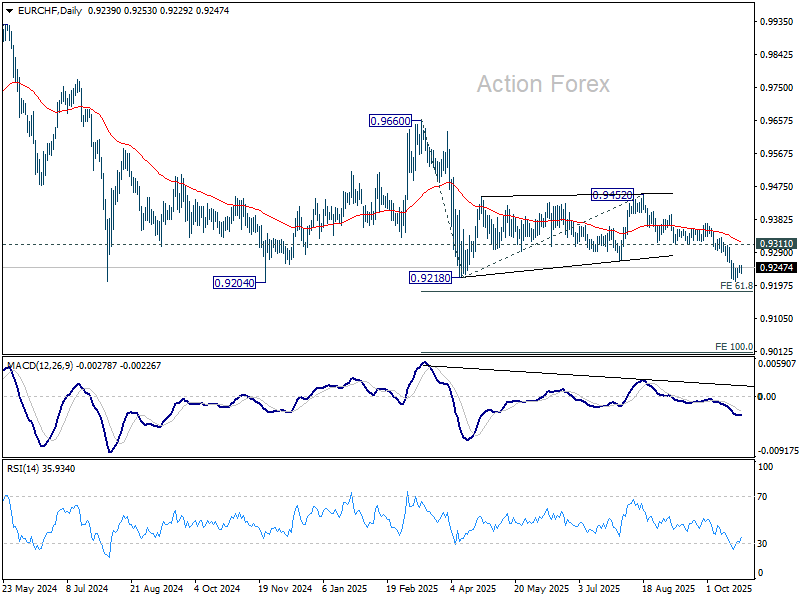

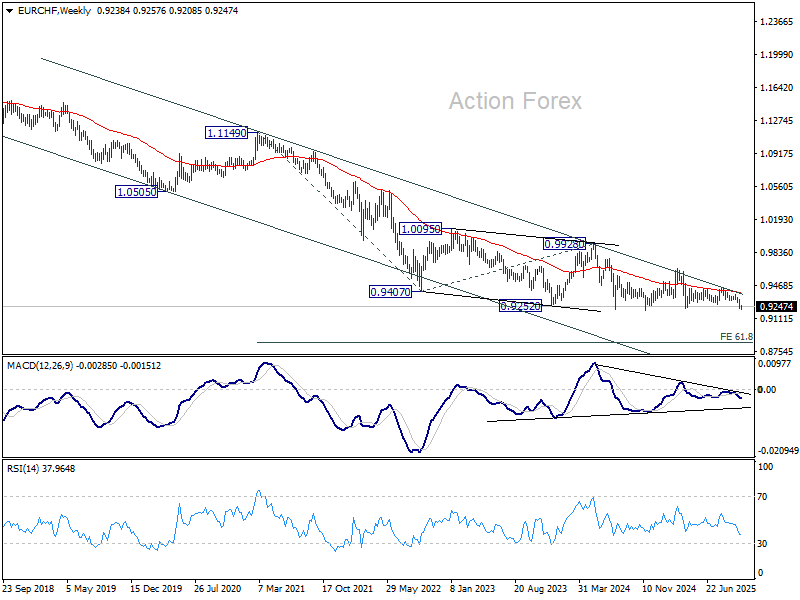

EUR/CHF Weekly Outlook

EUR/CHF edged lower last week but recovered ahead of 0.9204 support. Initial bias remains neutral this week first, and some more consolidations could be seen. But upside should be limited below 0.9311 support turned resistance. On the downside, break of 0.9204 will confirm larger down trend resumption. Next target is 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179. Firm break there will target 100% projection at 0.9010.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9395). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.

In the long term picture, overall long term down trend is still in progress in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9820) holds.

Week Ahead – Jittery Markets Await Central Bank Bonanza

- Fed to highlight busy week for central bank decisions

- BoC expected to cut too, ECB and BoJ to likely stand pat

- Eurozone GDP and Australian CPI to also be important

- US government shutdown to delay more crucial US data

BoC to cut again despite CPI spike

Kickstarting the central bank bonanza is the Bank of Canada on Wednesday. After a six-month pause, the BoC resumed its rate-cutting cycle in September and is expected to ease again in October. Governor Tiff Macklem recently indicated that policymakers will be putting more emphasis on risks at the next decision.

Moreover, with relations between Canada and the US souring again after President Trump abruptly terminated trade talks over an anti-tariff TV ad, a deal has become elusive again.

Subsequently, an October cut seems like a done deal, although for the rest of the year and for 2026, investors have scaled back their bets following the stronger-than-expected acceleration in Canadian CPI in September.

Still, dollar/loonie’s shallow uptrend since April is safe for now and it may be some time before the BoC rules out further rate reductions.

Fed meets amid ongoing shutdown

The US government is no closer to ending the shutdown that has gripped the country since October 1 and is about to enter its fourth week. Democrats are still refusing to agree to the Republican party’s stopgap funding bill as they’re seeking guarantees from the Republicans that a vote will be held on extending the health care subsidies that are due to expire at the end of the year.

However, Donald Trump is holding firm in insisting that there will be no negotiations with the Democrats whilst the government is in shutdown. This intransigent stance of both sides increases the probability of a more material impact on the economy from a prolonged shutdown – something the Fed will likely be mindful about.

If by Wednesday, when the Fed concludes its two-day monetary policy gathering, it doesn’t look like Republican and Democratic Senators are closer to clinching a deal on a funding bill, downside risks to the economy will probably be more prominent in policymakers’ minds.

Will the Fed turn more dovish?

Back in September, FOMC members had pencilled in two more rate cuts for 2025 and one for 2026. Judging by the most recent commentary from officials, including from Chair Powell, it doesn’t seem that their views have altered much. Whilst the Fed is clearly worried about the labour market and is watching it carefully, it sees the rate cuts as more of an insurance against any unexpected spikes in unemployment rather than a necessary policy step.

On the other hand, the Fed remains vigilant about sticky price pressures and has signalled it won’t tolerate above-target inflation indefinitely. The caution about the pace of reductions in 2026 and 2027 stems from the uncertainty about what the full impact of Trump’s tariffs will be on domestic prices. Until the Fed has a clearer picture on both inflation and the jobs market, it’s unlikely that Powell will significantly change his language on the future policy path as he announces a 25-basis-points reduction.

Hence, Powell & Co. may strike a somewhat more dovish tone on Wednesday given the latest flare-up in US and China trade relations and the ongoing shutdown, but probably not by much. Even dovish members like Waller are reluctant to pre-commit to a series of rate cuts. This then raises the risk of some disappointment among traders if the Fed casts doubt on the market rate path that implies an additional 100-basis-points of cuts after October.

Some US data still in the pipeline

With the government shutdown continuing, more economic releases look set to be put on the backburner next week, including Monday’s durable goods orders, Thursday’s advance GDP estimate for the third quarter and Friday’s personal income and outlays report that contains consumer spending numbers and the core PCE price index.

However, investors and policymakers will have access to some data, mainly the business surveys, such as Tuesday’s consumer confidence index and the Chicago PMI on Friday.

Should the incoming surveys raise any concerns about the economy, it would give investors more reason to question the Fed’s cautious stance. Alternatively, a combination of solid indicators and a not-so-dovish Fed meeting could give the US dollar a notable leg up.

Takaichi win creates a dilemma for the BoJ

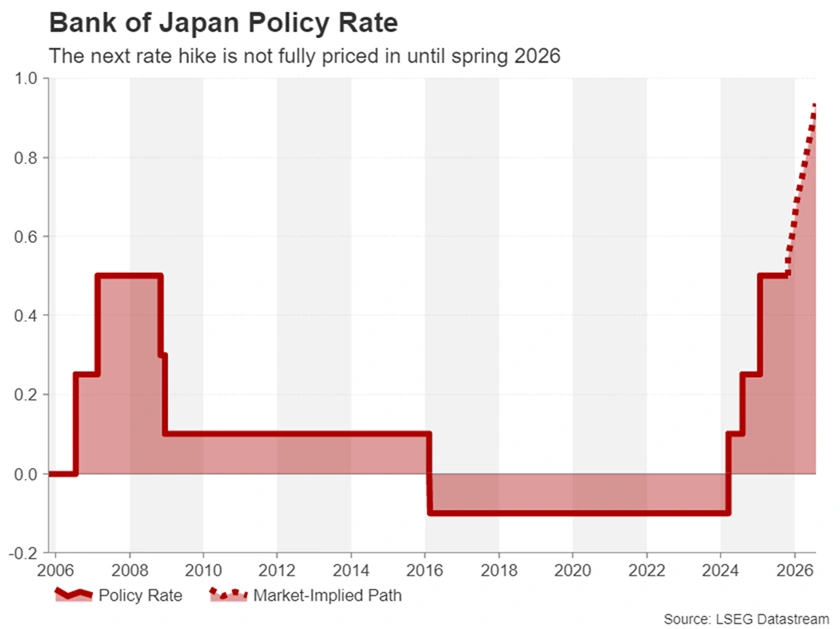

The Bank of Japan will announce its latest policy decision on Thursday less than a day after the Fed. Recent remarks from BoJ policymakers have been somewhat on the hawkish side, suggesting that a rate hike is firmly on the table for the October meeting. However, the odds of a 25-bps increase have fallen following newly elected LDP leader Sanae Takaichi’s confirmation as prime minister.

Far from toning down her Abenomics-inspired policies on massive government spending and accommodative monetary policy, Takaichi has doubled-down on the need for a fresh fiscal package to help households struggling from higher prices and for the Bank of Japan to align itself with the government’s economic policies.

This puts the BoJ in a tight spot when it comes to how soon it should raise interest rates again. Although inflation has been declining over the past few months, it remains well above the Bank’s 2% target. The Bank has also been sounding more upbeat lately about Japan’s economic outlook, as trade tensions ease with the United States, and is anticipated to revise up its growth forecasts.

The question now is how strong is the urgency to raise rates sooner rather than later? Takaichi’s appointment as PM has likely removed the immediate need for action, with investors pricing in only a 20% probability of a hike in October.

If the BoJ keeps rates unchanged as expected and simply hints that it’s moving closer to a hike without providing any explicit signals, there won’t be much of a reaction in the yen and traders will turn their attention to the Tokyo CPI figures out on Friday.

ECB meeting could be a non-event

The European Central Bank also meets on Thursday to set policy but it’s unlikely that there will be any fireworks. The Bank has been on pause since July and there seems to be a strong consensus within the Governing Council to hold rates at 2.0% for the foreseeable future.

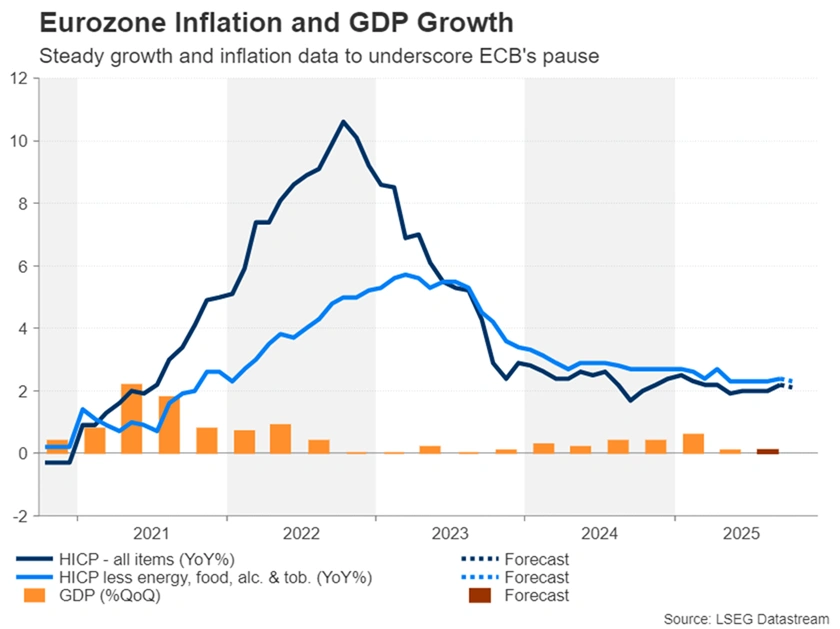

With inflation hovering around the ECB’s 2% target and the Eurozone economy proving surprisingly resilient in the face of steep US tariffs, policymakers would prefer to preserve some firepower for a rainier day, even as some officials acknowledge that the next move is more likely to be down than up.

For the euro, however, this can only be good news for the bulls, especially as the Fed only recently resumed its easing cycle. The preliminary CPI estimates for October due Friday are also not expected to generate any significant moves even though they will be watched closely, and the bigger risk for the euro will be the flash Q3 GDP readings on Thursday.

The Eurozone economy is projected to have expanded by just 0.1% q/q in the three months to September. A weaker number could revive expectations of a further rate cut by the ECB, weighing on the euro.

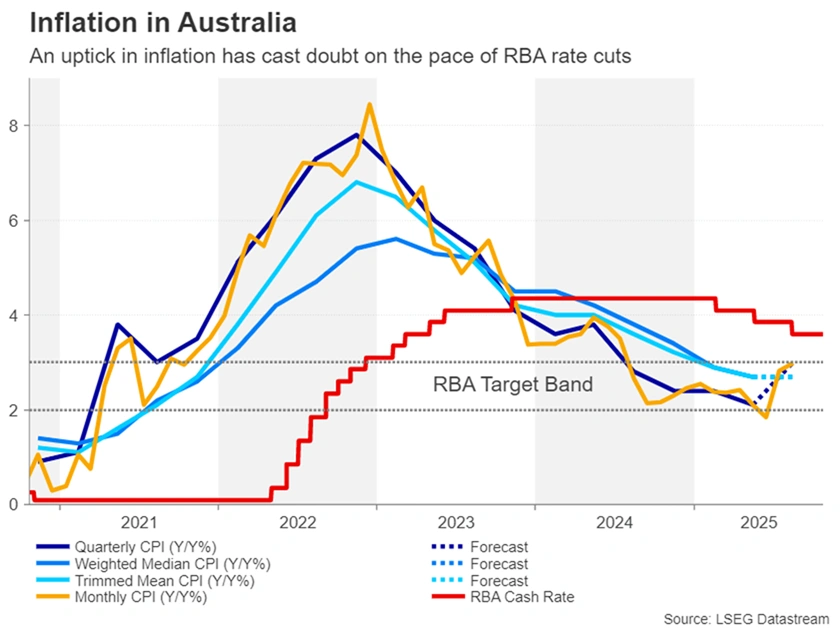

Aussie eyes CPI data ahead of RBA decision

The Reserve Bank of Australia’s next policy meeting is in a little over a week’s time so the timing of Wednesday’s CPI report couldn’t be more ideal.

The report will include data for both the third quarter and September, potentially swaying the November vote as a 25-bps rate cut is less than 70% priced in. The recent economic figures out of Australia haven’t been going the RBA’s way as the unemployment rate jumped to 4.5% in September, while monthly inflation has edged up towards the upper target band of 3.0%.

However, in the quarterly readings, underlying measures of CPI have been declining and if this trend continued in Q3, the RBA is almost certain to trim the cash rate in November. That’s not to say, though, that there aren’t some upside risks for the Australian dollar should any of the CPI prints come in above forecasts.

Markets Weekly Outlook – Trump-Xi Meeting, Earnings & Central Banks

Week in review

A rollercoaster week draws to a close for Global Markets. US-China trade talks were driving volatility and the mixed messages from both parties kept things interesting. Markets also saw harsher sanctions on Russian which has renewed the geopolitical risk premium when factoring in the Russia/Ukraine situation.

President Trump went back and forth this week, keeping markets guessing as his rhetoric went from diplomatic to combative and back to diplomatic by the end of the week regarding China. A date has now officially been set for a Trump-Xi meeting which at this stage is set for October 30.

President Trump is heading on an Asia visit this weekend with a senior US official stating that President Trump will sign economic agreements, including trade and critical minerals, on his trip this weekend.

The news of a Trump-Xi meeting which markets had expected since the start of the week led to a rise in equities globally. European stocks closed at record highs.

The S&P 500 and the Nasdaq are set to have their best week in terms of percentage gain since August. Meanwhile, the Dow Jones Industrial Average is heading for its biggest weekly jump since June.

The moves in Global stocks were also helped by the cooler than expected US CPI data.as well as US earnings.

The current third-quarter earnings season is moving very fast, with 143 companies in the S&P 500 having already reported their results.

So far, 87% of those companies have surpassed Wall Street's expectations.

Because of these strong results, analysts have raised their overall forecast for S&P 500 earnings growth for the quarter to 10.4% year-over-year, which is a solid improvement from the 8.8% growth that was expected at the beginning of October.

How has the US Dollar and FX Performed?

The US Dollar was nearly flat on Friday, steadying after a brief dip following the release of the inflation report, though it remained on track for a small gain for the week.

The euro rose slightly after a survey showed that business activity in the Eurozone, led by the services sector, grew faster than expected in October.

The Canadian dollar was slightly weaker but saw a minimal reaction overall.

Meanwhile, the Japanese yen fell to a two-week low despite data released earlier on Friday showing that Japan's core consumer prices remained above the central bank's 2% target, which kept alive expectations for an interest rate hike soon.

Taking a brief look at how commodities ended the week and Gold prices reduced their losses on Friday after a slightly cooler-than-expected US inflation report reinforced expectations that the Federal Reserve will cut interest rates next week.

Despite this recovery, gold was still set for its first weekly loss in ten weeks.

Meanwhile, oil prices fell slightly as investors grew skeptical about how strongly the Trump administration would enforce its new sanctions on Russia's two largest oil companies.

Even though both oil benchmarks retreated near the end of trading, giving up some of the previous day's large gains, they still finished the week more than 7% higher, marking their biggest weekly jump since mid-June.

The Week Ahead

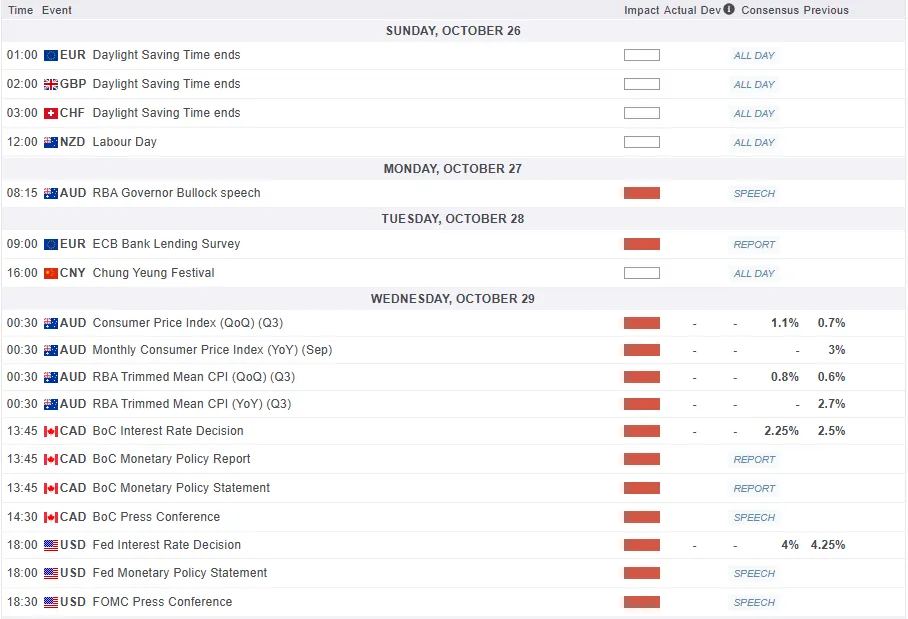

Given that next week brings a host of central bank decisions, FX markets could have a busy week.

Beyond the data, markets will be focused on the Trump-Xi meeting, Russia-Ukraine developments as well as renewed tensions between the US and both Venezuela and Colombia. Any signs of US military intervention in Venezuela could add to the risk premium and affect overall market sentiment.

US earnings will also be key with a host of ‘magnificent 7’ companies all reporting Q3 earnings.

Let us take a look at some of the key data releases which could shake markets next week.

Asia Pacific Markets

In the coming week, all attention will be on the US-China trade talks.

The talks begin this weekend in Malaysia with top officials (led by China’s He Lifeng and US Treasury Secretary Scott Bessent) and are expected to lead to the long-awaited face-to-face meeting between President Xi Jinping and President Trump on October 30th in South Korea. This will be their first meeting since 2019, following months of increasing trade fights and threats.

Because the recent language has cooled, and President Trump has spoken optimistically about reaching a "fantastic deal" and even visiting China in 2026, we expect a positive outcome. This deal will likely at least continue the current uneasy trade truce.

However, Trump has kept his options open by suggesting the meeting might not happen. If the meeting does go ahead, it likely means the top officials (He and Bessent) have already agreed on the basic terms of a deal.

Regarding economic news, next week is quieter. The main data release will be China's manufacturing report next Friday, which is expected to show that manufacturing activity is still shrinking.

The Bank of Japan (BoJ) is expected to keep its interest rate at 0.5% on October 30th.

Even though the BoJ's board members still disagree on policy, the majority is not ready to change course yet. I believe that inflation has been firmly rising and the economy is holding up well despite challenges like US trade tariffs. These factors should support the BoJ's policy of eventually raising interest rates.

However, because most board members are cautious about raising rates too soon, a rate increase might be delayed until December. Supporting this view, I expect key data next week, like the Tokyo consumer price index, to show a strong rise of 2.5%, and for economic activity (like factory output and retail sales) to recover.

Central Bank Decisions and US-China Talks in Focus

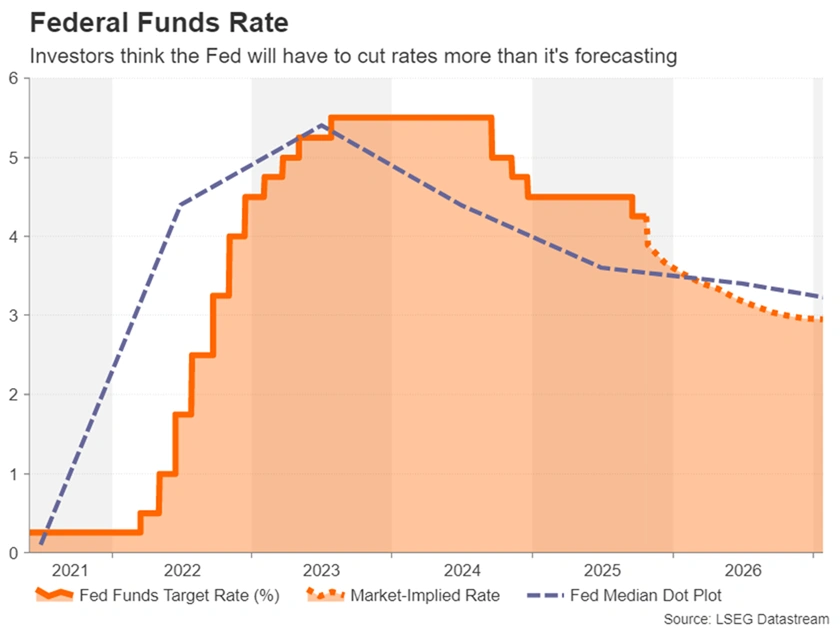

The Federal Reserve is widely expected to cut its interest rate by another 0.25% on October 29th, following a similar cut last month. While the US economy looks decent and inflation is still a bit high, the Fed is shifting its focus because the risks are changing.

Price increases due to tariffs haven't been as severe as feared, giving time for factors like lower energy prices, slowing wage growth, and easing housing rents to help bring inflation down. At the same time, the job market is starting to look more concerning, with many indicators suggesting an increasing risk of job losses. Because this trend points to both weaker economic growth and lower inflation in the future, the Fed feels that moving interest rates closer to a neutral level is the sensible thing to do.

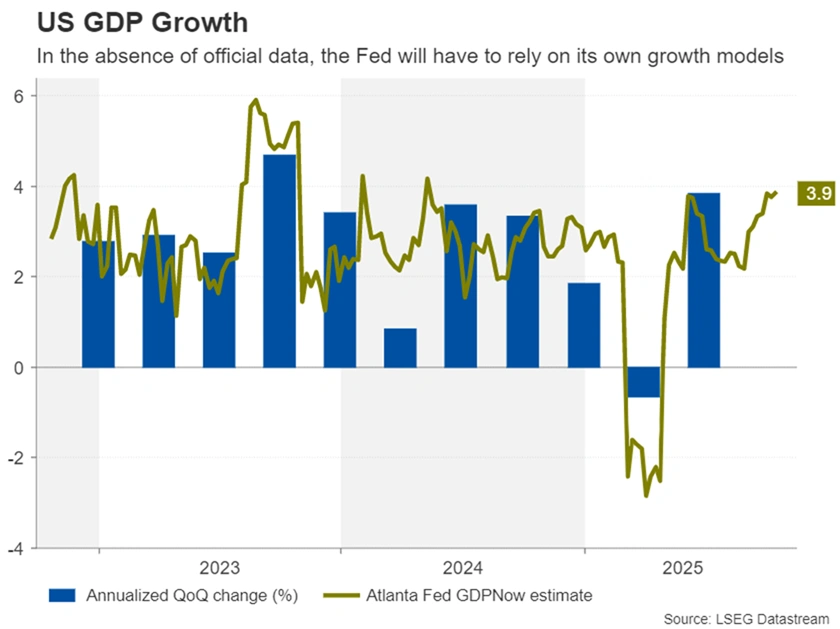

The report on third-quarter economic growth (3Q GDP) is unlikely to be released next week because of the ongoing government shutdown.

The upcoming European Central Bank (ECB) meeting should be uneventful. Since the last meeting, economic data for the Euro area has been mixed: some surveys improved, but August's official data disappointed. While September inflation briefly went above 2%, the new, important figures such as the third-quarter GDP growth and the October inflation rate will both be released on the day of the meeting itself.

With political risks calming down and officials signaling no rush, the ECB is expected to reaffirm its current stable position, with any potential decision on an interest rate cut pushed to December.

My opinion is that the October inflation rate will remain around 2%, and third-quarter economic growth will be a muted 0.1%, showing the economy is avoiding a recession despite global problems but is nowhere near a strong rebound.

Essentially, these data releases are expected only to confirm that the Eurozone economy is holding steady at a slow pace, so the ECB is unlikely to react to them strongly.

The Bank of Canada is expected to cut interest rates by 0.25% this week, even though recent reports showed job growth and inflation were a bit stronger than expected.

The central bank is under pressure to help Canada's economy, which has been severely damaged by US tariffs (since three-quarters of Canada's exports go to the US).

Additionally, Canadian consumers have very high debt levels, so the Bank is likely stepping in to provide needed support.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week - US Dollar Index

US Dollar Index (DXY) Daily Chart - October 24, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 97.70

- 96.90

- 96.37

Resistance

- 99.57

- 100.00

- 100.61

The Weekly Bottom Line: Persistent Inflation, Shutdown Pose Challenges for Federal Reserve

Canadian Highlights

- Headline inflation came in stronger than expected, but core measures remained stable, supporting the case for another interest rate cut next week.

- Long-term inflation expectations edged higher, but firms’ pricing power remained limited. Retail sales rose in August but declined in September, losing momentum on a three-month basis.

- Attention increasingly shifts to Carney’s forthcoming budget for signs of a broader growth strategy.

U.S. Highlights

- The federal government shutdown entered its 4th week, becoming the 2nd longest in history.

- The CPI data release for September, delayed by the shutdown, showed inflation moderated during the month but remained elevated on aggregate.

- Trade negotiations with China will ramp up over the next week in advance of the November 1st deadline for 100% additional tariffs threatened by the President.

Canada – Final Puzzle Pieces Before the Bank’s Rate Decision

This week’s Business Outlook Survey, CPI inflation and retail sales reports offered the final puzzle pieces before the Bank of Canada’s interest rate decision on October 29th. The TSX briefly wavered after the CPI release on tempered expectations for rate cuts, but quickly recovered, finishing the week 0.9% higher (as of writing). They also seem to have brushed off President Trump ending trade talks with Canada over an Ontario ad quoting President Reagan. Taken together, the data supports expectations for another Bank of Canada cut next week, while attention increasingly shifts to fiscal policy and Carney’s forthcoming budget for signs of a broader growth strategy.

The week began with the release of the Bank’s Q3 surveys on business and consumer sentiment. Both measures improved modestly but remain subdued, with roughly one-third of firms and two-thirds of consumers still expecting a recession. From a policy perspective, the most important signal was that firms reported limited pricing power amid weak demand. That should offset the slight rise in longer-term inflation expectations among consumers, especially given that the survey was conducted before the federal government announced its plan to remove counter-tariffs.

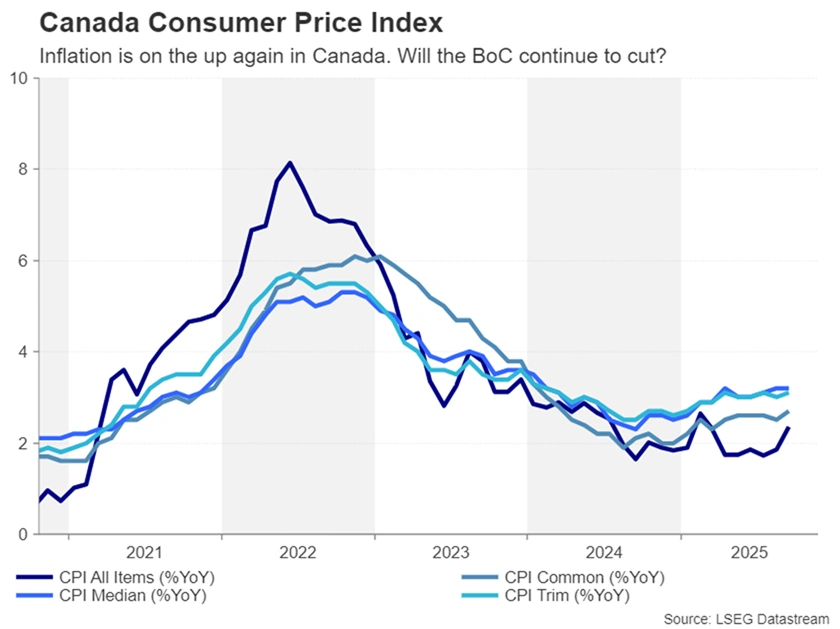

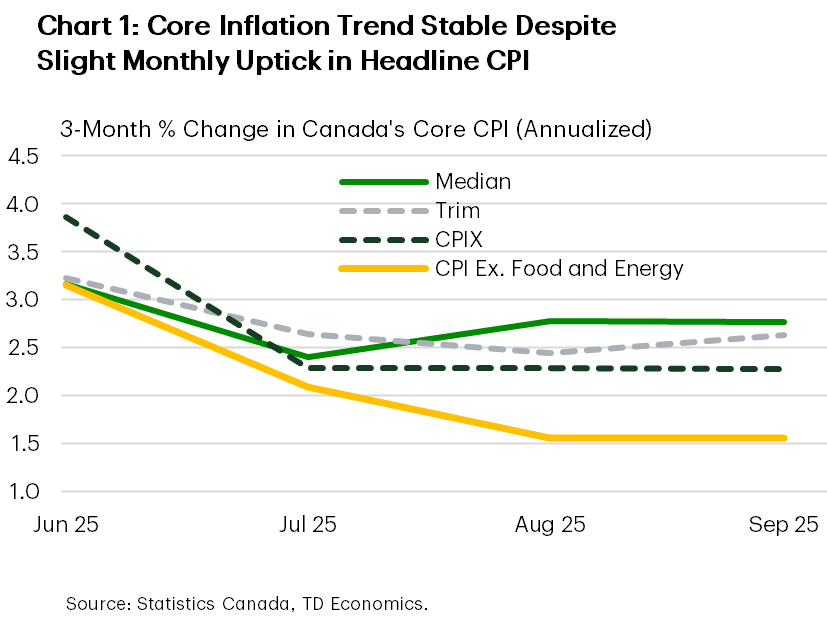

More difficult to ignore is the September inflation report, which showed headline CPI rising 2.4% year-on-year, above expectations for 2.2%. The acceleration was due to base effects, slower declines in gasoline prices, higher food prices, and a pickup in travel services prices. Still, inflation remains within the Bank’s 1-3% target range, while three-month trends in most core measures moved sideways (Chart 1). The breadth of inflationary pressure also held steady and should ease some of the Bank’s lingering concerns.

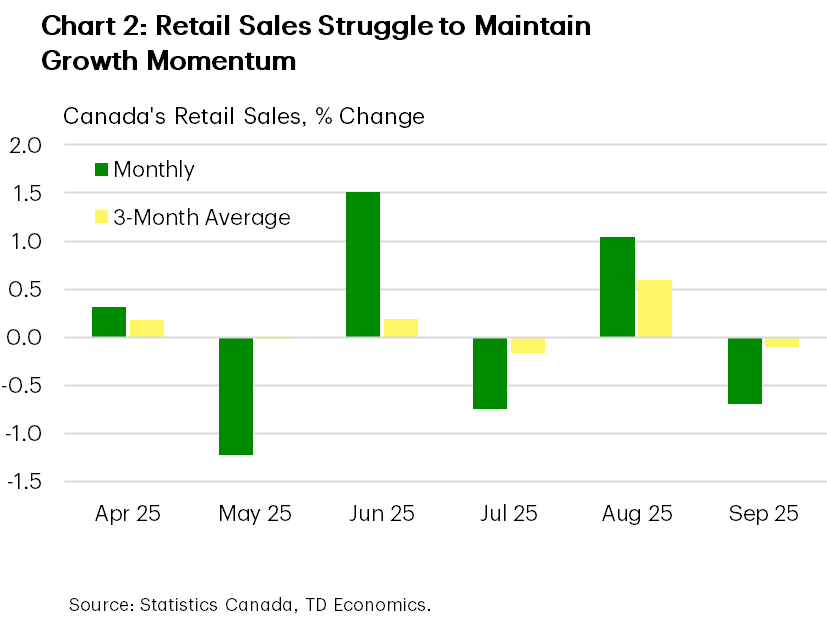

While the Bank remains laser-focused on inflation, its recent communication placed greater emphasis on economic slack, albeit with the caveat that monetary policy has limited ability to deal with tariffs. In this context, August retail sales provided some insight into consumer demand. Sales expanded in line with the flash estimate, largely driven once again by autos. However, the September flash estimate suggests demand deteriorated again. Parsing through the noise, retail sales have clearly lost momentum (Chart 2). This is particularly obvious in autos and home-related goods, which will likely weigh on durable goods spending. That said, some discretionary goods categories are still growing at a decent clip, while services spending, especially on travel, appears to have accelerated in Q3 as signalled by our internal spending data.

Beyond these mixed signals, the Bank has sufficient evidence of slack to justify one more rate cut, particularly given the subdued outlook for exports and investment. This weakness framed the Prime Minister Carney’s address to university students on Wednesday, where he announced an ambitious goal to double Canada’s non-U.S. exports over the next decade. Given the limits of monetary policy, the strategic fiscal push from November’s budget has the chance to shape Canada’s economic trajectory in the coming quarters and years. Let’s hope it proves as potent as the Prime Minister’s speech was inspiring.

U.S. – Persistent Inflation, Shutdown Pose Challenges for Federal Reserve

The ongoing government shutdown became the 2nd longest in history this week, as it stretched into week 4. With divisions in Congress largely unchanged relative to September, a resolution remains out of sight, but as the economic impacts become more material, intransigence will likely yield. Elsewhere in D.C., President Trump called off trade negotiations with Canada over the use of anti-tariff television advertisements broadcast in the U.S., forestalling a near-term trade agreement with the nation’s second largest trading partner. Despite political dysfunction in the Capitol and rising trade tensions in recent weeks, the S&P 500 still managed to rise 2% this week from a host of positive third quarter earnings reports.

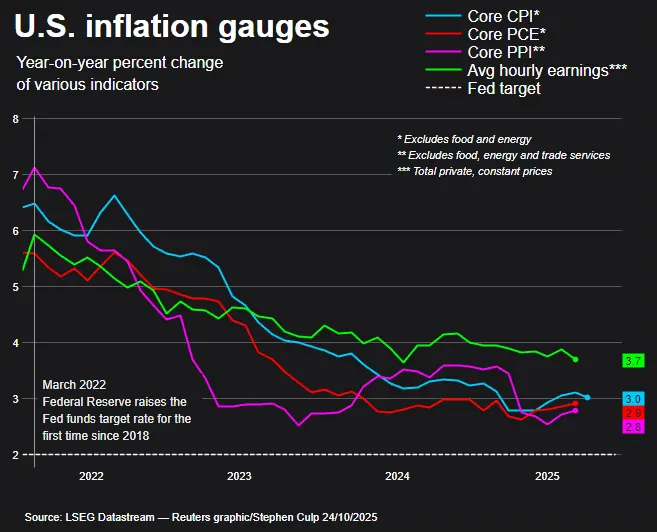

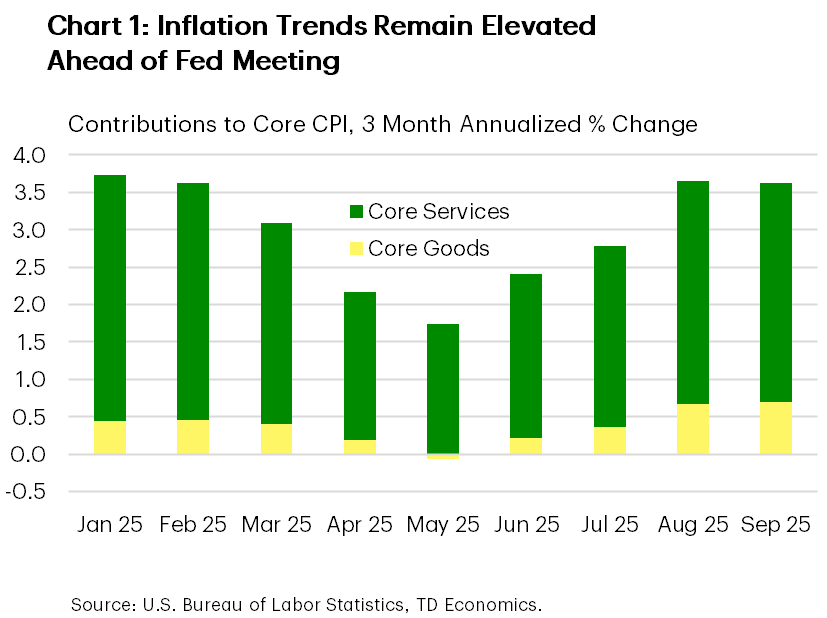

While the Department of Labor remains unfunded, the CPI data for September was released on Friday owing to its use in the annual inflation adjustment to social security payments. The data showed that recent inflationary pressures moderated slightly in September but remained elevated on aggregate, with the three-month annualized percentage change in core CPI running above 3.5% (Chart 1). With price growth still well above the Fed’s 2% target and the timing of future data releases uncertain, policy decisions are expected to be cautious moving forward.

The shift in the Federal Reserve’s stance on monetary policy over the past few months came on the heels of a slowdown in the labor market, tracking of which has been obscured by the lapse in data releases. As the FOMC begins deliberations next week, they will likely assume that the slowdown persisted through September and opt to meet financial market expectations for a quarter-point rate cut. Chair Powell’s press conference will be closely watched for insights into how the policy response function of the Federal Reserve will adapt to a prolonged government shutdown, as inference becomes more difficult the further we are from the last official data release.

On the trade front, U.S. Treasury Secretary Bessent will be meeting with a Chinese delegation in Malaysia over the weekend. The deadline to reach some form of agreement is becoming tight, with President Trump’s threat of 100% tariffs on China starting November 1st. The President will also be travelling to Asia Friday night, with plans to visit Malaysia, Japan, and South Korea, culminating with the Asia Pacific Economic Cooperation (APEC) summit where he is expected to meet with his Chinese counterpart. Amid rising trade tensions in recent weeks, financial markets will be watching for any signs of de-escalation.

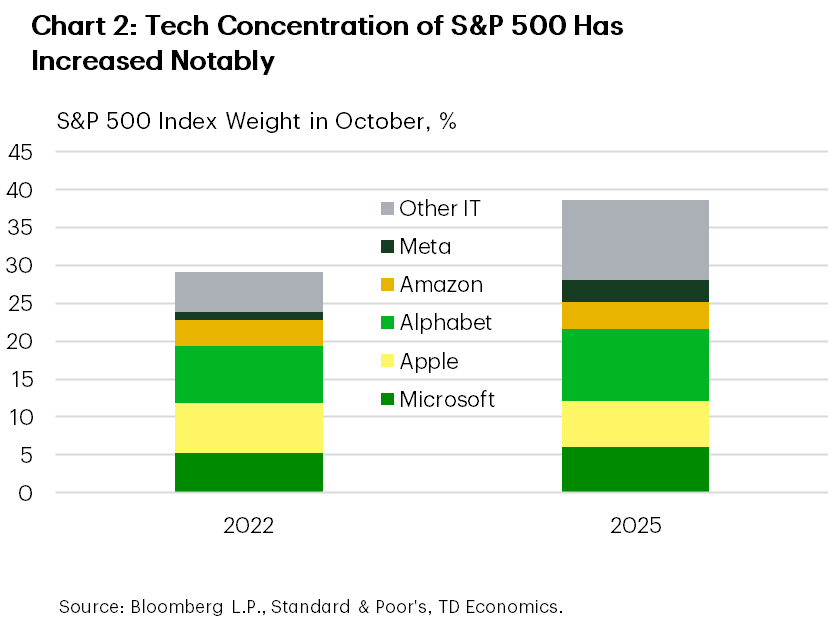

Markets will also be watching for several big tech earnings reports next week, including Microsoft, Apple, Alphabet, Amazon, and Meta, which collectively account for nearly a quarter of the S&P 500 (Chart 2). Given the high level of concentration in equity markets, growing concerns about elevated valuations, and the influence of these trends on the economy, these results will be monitored closely on the heels of Wednesday’s Federal Reserve decision.