Sample Category Title

Crypto Has Positively Shaken Off Its Fears

Market Overview

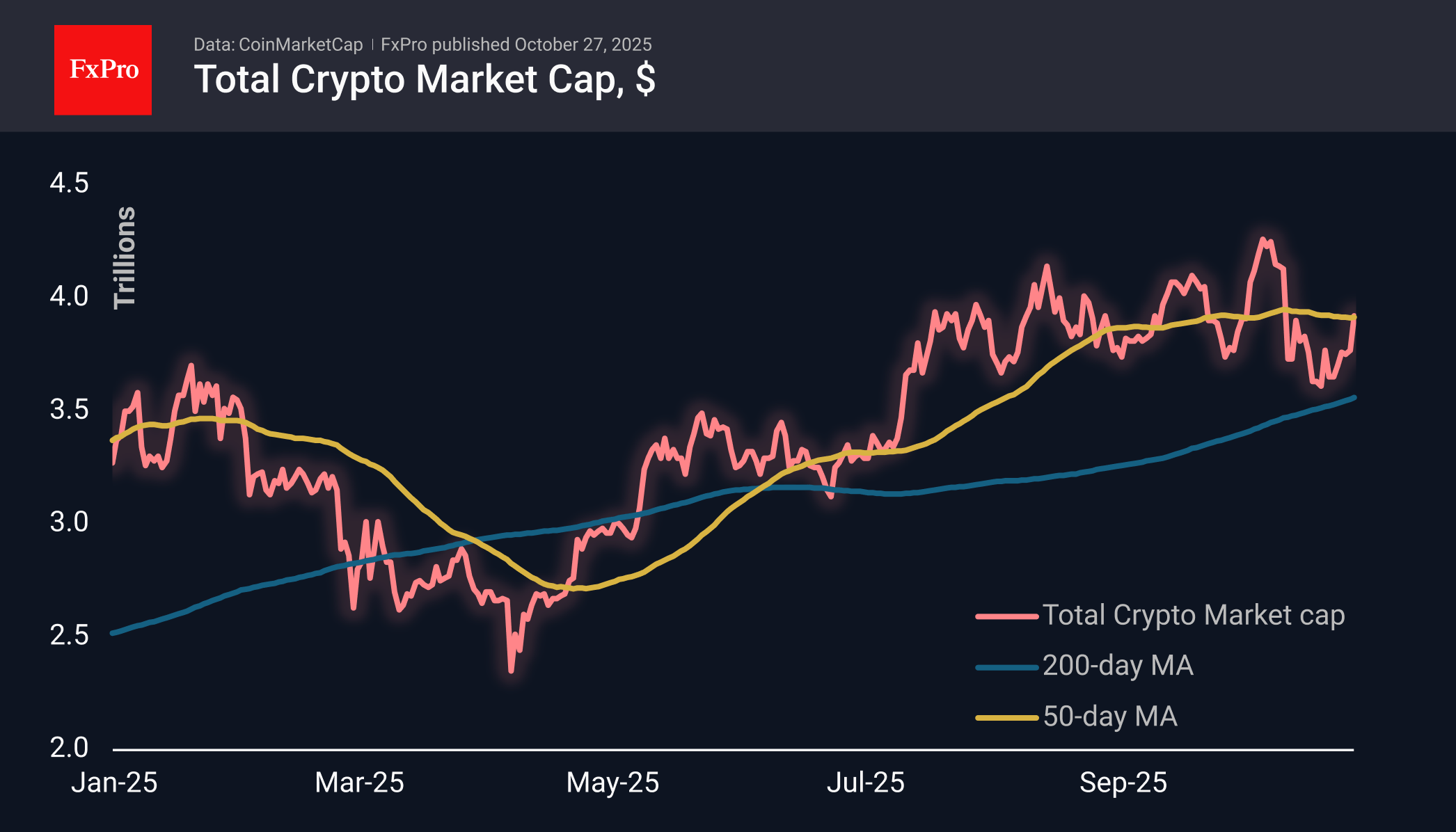

The crypto market capitalisation has gained 4% in 24 hours, confidently adding to positive signals from trade negotiations between China and the US. News from the two largest economies remains cyclical, with positive signals following meetings and high-level direct negotiations the day before. Total capitalisation reached $3.92 trillion, recovering to the 50-day moving average (MA), staying above the 200-day MA of $3.51 trillion at the start of last week.

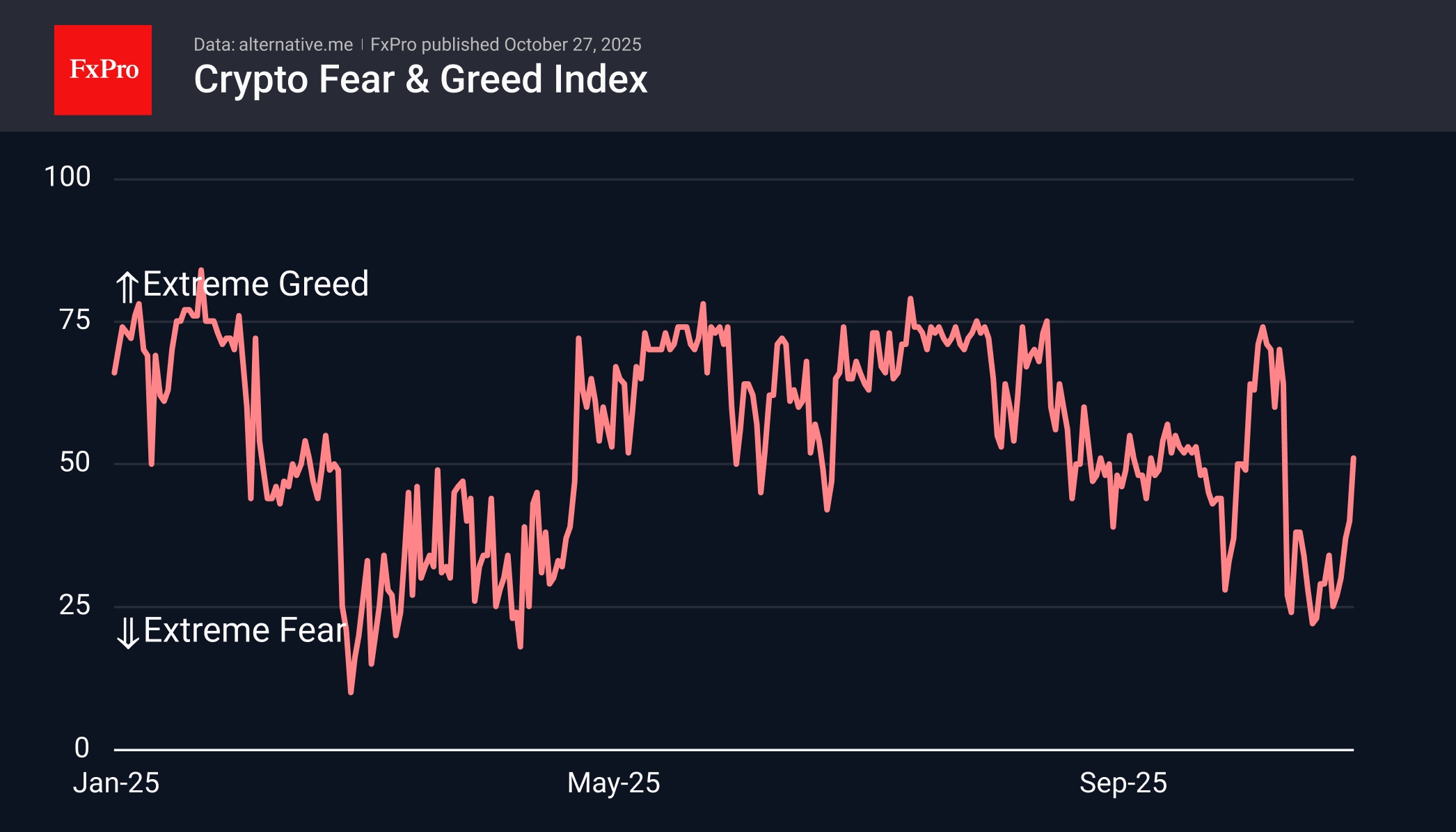

The sentiment index recovered to 51, quickly returning to neutral territory. Unlike the spring episode, this time the recovery came almost immediately after touching levels of extreme fear.

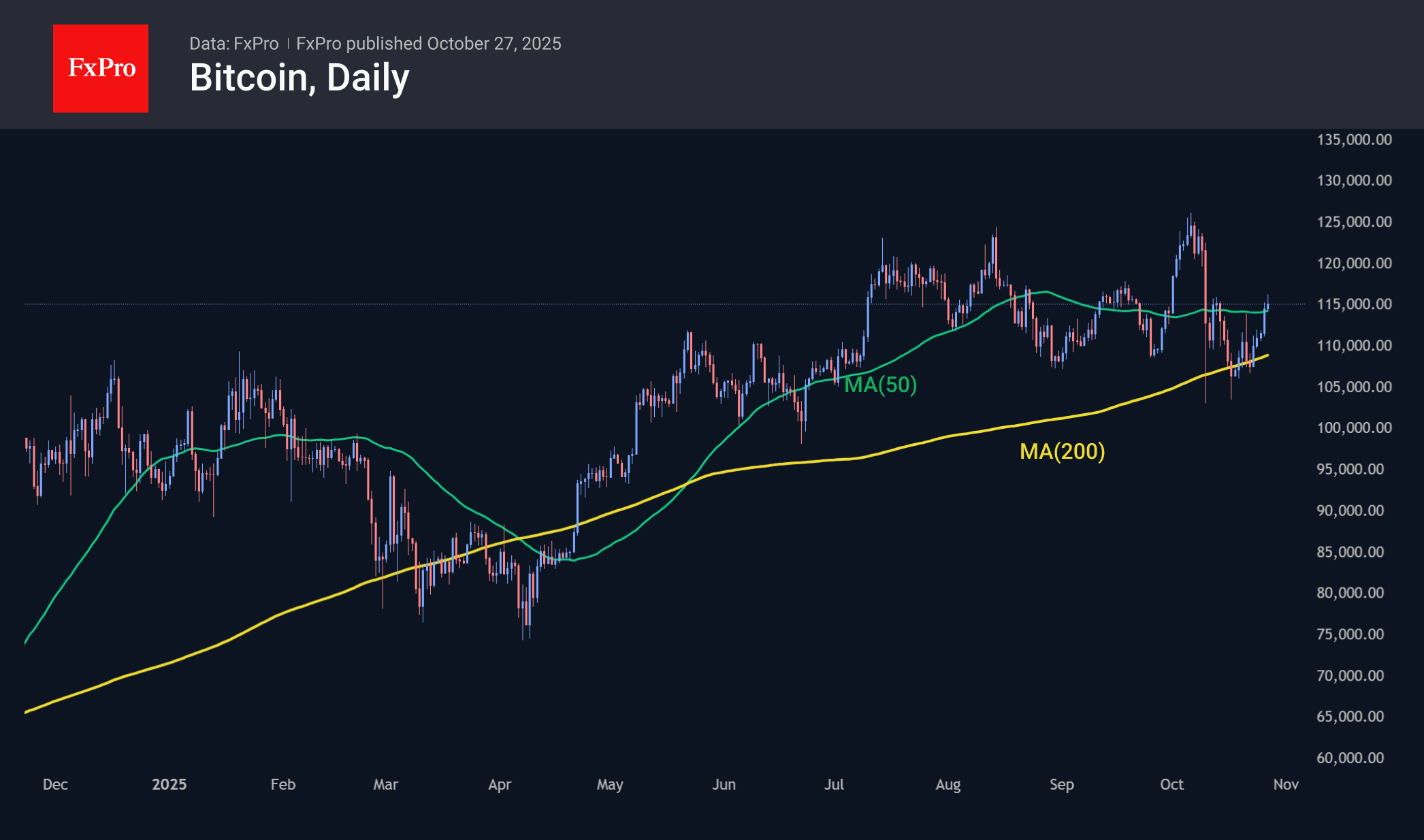

Bitcoin rose above $116K on Monday morning, pushing off the 200-day MA as support last week and exceeding the 50-day moving average at the start of the new week. The $117K–120K area is a strong resistance zone. The rallies in August and early October proved to be unsustainable. Perhaps, by bouncing off the 200-day MA, BTC, as it did in April, will gain enough momentum to renew its highs.

News Background

According to SoSoValue, net inflows into spot BTC ETFs totalled $446.4 million last week, marking the lowest level in the last seven weeks. This brings the total inflows since the approval of Bitcoin ETFs in January 2024 to $61.54 billion.

Net outflows from spot ETH ETFs fell to $243.9 million for the week, reducing the cumulative net inflow since the launch of ETFs in July 2024 to $14.35 billion.

According to OnChainSchool, the volume of bitcoins that have been inactive for more than seven years and have been moved since the beginning of the year has reached a historic high. Long-term BTC holders continue to take profits by actively selling coins.

Owners of 100-1,000 BTC, so-called Dolphins, control the largest share of bitcoins — about 26%, making their activity a key market factor in the late stage of the bullish phase, CryptoQuant notes. CryptoQuant considers ETFs, corporations and other large holders to be dolphins.

BitMine CEO Tom Lee suggested that Bitcoin could fall by 50% to $55,000 in the event of a significant correction in the US S&P 500 stock index.

Altcoins could have had $800 billion more in capitalisation this year were it not for BTC ETFs. Growing interest in Bitcoin and BTC ETFs could cause an even greater decline in the alternative coin market, according to 10x Research.

German Ifo rises to 88.4 as business expectations improve

Germany’s Ifo Business Climate Index rose to 88.4 in October from 87.7, topping expectations of 87.8. The uptick was driven mainly by stronger optimism about the outlook, even as assessments of current conditions softened. Expectations Index climbed to 91.6 from 89.8, while Current Assessment slipped to 85.3 from 85.7, highlighting that the recovery remains more hopeful than tangible.

By sector, the data painted a mixed but improving picture. Manufacturing sentiment strengthened from –13.2 to –11.7, with Ifo noting that “expectations in particular brightened” and the decline in new orders has “come to a halt.” The service sector saw a sharp rebound, rising from –3.0 to –0.1, as providers turned less skeptical about the coming months. Trade confidence also improved from –23.9 to –21.5, while construction slipped slightly from –14.8 to –15.0.

GBP/USD And USD/CAD Decline As Dollar Sees Mixed Flows

GBP/USD started a downside correction from the 1.3470 zone. USD/CAD declined and now consolidates below 1.4000.

Important Takeaways for GBP/USD and USD/CAD Analysis Today

- The British Pound started a fresh decline and settled below the 1.3400 zone.

- There is a connecting bearish trend line forming with resistance at 1.3330 on the hourly chart of GBP/USD at FXOpen.

- USD/CAD started a fresh decline after it failed to surpass 1.4065.

- There was a break below a key bullish trend line with support at 1.3995 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair struggled above 1.3450. The British Pound started a fresh decline below 1.3400 against the US Dollar, as discussed in the previous analysis.

The pair dipped below the 1.3350 and 1.3300 levels. A low was formed at 1.32874 and the pair is now consolidating losses. On the upside, the pair is facing resistance near 1.3330 and a bearish trend line. It is close to the 23.6% Fib retracement level of the downward move from the 1.3471 swing high to the 1.3287 low.

The next key hurdle on the GBP/USD chart could be near the 50% Fib retracement at 1.3380. The main breakout zone is 1.3400. An upside break above 1.3400 could send the pair toward 1.3470.

Any more gains might open the doors for a test of 1.3500. If there is another decline, the pair could find support near 1.3285. The first key zone for the bulls might be 1.3250. A clear move below 1.3250 might send GBP/USD toward 1.3220. The next target for the bears might be 1.3200, below which the price could dive and test 1.3050.

USD/CAD Technical Analysis

On the hourly chart of USD/CAD at FXOpen, the pair climbed toward 1.4065 before the bears appeared. The US Dollar formed a swing high near 1.4065 and recently declined below 1.4020 against the Canadian Dollar.

There was a break below a key bullish trend line with support at 1.3995. Finally, there was also a close below the 50-hour simple moving average and 1.4000. The bulls are now active near 1.3970. The pair is now consolidating losses below the 23.6% Fib retracement level of the downward move from the 1.4039 swing high to the 1.3978 swing low.

If there is a fresh increase, the pair could face resistance near 1.4000 and the 50-hour simple moving average. The first major pivot level is 1.4015 and the 61.8% Fib retracement.

The next stop for the bulls on the USD/CAD chart could be 1.4040. If there is an upside break above 1.4040, the pair could rise toward 1.4070. A close above 1.4070 might start a steady increase toward 1.4150.

If there is another decline, the pair might find bids near 1.3970. The first major support is near 1.3950. A close below the 1.3950 level might trigger a strong decline. In the stated case, USD/CAD might test 1.3880. Any more losses may possibly open the doors for a drop to 1.3840.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

USD/CAD Declines Amid a Flurry of Market News

The Canadian dollar strengthened against the U.S. dollar today, pushing USD/CAD down to 1.39750 – a level that acted as resistance in early October but has since turned into support.

The pair’s fluctuations come amid a busy news backdrop. On Friday:

→ President Trump announced the suspension of trade talks with Canada, reportedly due to his dissatisfaction with Canadian advertising campaigns using Ronald Reagan’s image to criticise tariffs.

→ The CPI report came in weaker than expected. According to Forex Factory, U.S. annual inflation stood at 3.0%, compared with the 3.1% forecast by analysts.

This week could bring heightened volatility as markets await two key rate decisions on Wednesday:

→ At 16:45 GMT+3, the Bank of Canada is expected to cut its policy rate from 2.50% to 2.25%;

→ At 21:00 GMT+3, the Federal Reserve is forecast to lower the Federal Funds Rate from 4.25% to 4.0%.

Both announcements will be accompanied by policy statements that could significantly influence USD/CAD price action.

Technical Analysis: USD/CAD Chart

Last month’s analysis highlighted two key structures:

→ A red long-term descending channel originating in early February;

→ A blue ascending channel formed by price swings since mid-summer.

Since then:

→ Bulls managed to break above the red channel’s upper boundary;

→ The price consolidated around the median line of the blue channel in early October.

From a bearish perspective:

→ The price failed to hold above the psychological level of 1.4000;

→ A sequence of lower highs forms a descending trendline.

From a bullish perspective:

→ The blue channel remains intact;

→ 1.39750 serves as support;

→ An additional support zone lies just below, near the breakout point of the red channel where buying pressure was previously strong.

Given these factors, the red trendline may represent a corrective pattern within the broader bullish structure. Whether buyers can resume the uptrend successfully will largely depend on the upcoming central bank decisions and any further statements from President Trump.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

A Flurry of Positive Trade News Keeps the Party Going

Markets

Friday’s US combination of slightly softer than expected September inflation with strong headline October PMIs & weaker output price pressures offered fertile breeding ground for stock markets. Business confidence for the year ahead deteriorated on lingering tariff concerns but that nuance was lost on Wall Street. Bourses gapped higher towards new record highs. US yields wiped out most if not all of the CPI driven losses, resulting in net daily changes varying between -0.9 bps (2-yr) to +1.4 bps (30-yr). An improving services sector (Germany) pushed euro area PMIs to a 17-month high, topping expectations and causing European bond underperformance vs Treasuries. Bund yields rose 3.8-5 bps across the curve. The implied money market probability for another ECB rate cut dropped again after creeping higher (and weighing on front end yields) in the past few weeks. EUR/USD was nicely balanced with the pair closing near its opening levels around 1.163. EUR/GBP’s closing level (0.874) was the highest since end-September. UK PMIs beat consensus as well but were sub-par compared to the European (and US) version. They imply a mere 0.1% growth for the ongoing quarter.

A flurry of positive trade news keeps the party going during the Asian session this morning. Equities bathe in a sea of green. The Nikkei 225 (2.5%) topped the 50k mark for the first time. SK and Chinese exchanges rise up to 2.5% and 1.2% respectively. US and Chinese trade negotiators during a two-day marathon in Malaysia (ASEAN summit) wrapped up yesterday said they came to terms on several critical issues related to fentanyl, soybean purchases and China’s recently announced tighter export controls on rare earths. USTS Bessent said Trump’s 100% tariff threat is now off the table. The stars seem aligned for Trump and Xi to now finalize an extension of the trade truce during their first in-person meeting since 2019 on October 30. The likes of copper, iron, steel and oil are all rising. Brazilian president Lula meanwhile said he had a “surprisingly good” meeting with Trump on the sidelines of the ASEAN summit. He expects a ”definitive resolution” in the coming days. The US slapped Brazil with 50% tariffs on some key goods. Canada is the odd one out here. Trump said he’s increasing tariffs on Canadian goods by 10% in response to an advertisement aired by the Ontario government in which former president Reagan lashed out at tariffs and defended free trade. We don’t expect that to spoil the current risk-on mood though. Core bond yields grind higher, with Treasuries particularly eying supply today ($69bn 2-year and $70bn 5-yr). The euro and dollar tread water going into central bank meetings by both the Fed (Wednesday) and the ECB (Thursday). The Bank of Japan follows on Thursday. Euro area inflation and Q3 GDP numbers are also on tap.

News & Views

Rating agency Moody’s changed the outlook on France’s Aa3 rating from stable to negative. The decision reflects the increased risk that political instability hampers the government’s ability to address key policy challenges such as an elevated fiscal deficit, rising debt burden and durable increase in borrowing costs. Political fragmentation also risks the long-lasting reversal of previously adopted structural reforms, in particular the 2023 pension reform. A downgrade of France's ratings would likely result from further evidence that the ability of the legislative institutions to effectively tackle the country's key credit challenges has durably weakened. A lasting pause or reversal of reforms would also add to downward pressure on the rating. Rating agencies S&P and Fitch already moved the French rating into single A category (A+) because of similar concerns. Also on Friday, S&P confirmed both the Belgian (AA) and the Slovakian (A+) credit rating while sticking with negative outlooks on both of them.

The People’s Bank of China implemented a new strategy on the country’s currency in the wake of the Communist Party Central Committee’s plenum. In the previous five-year plan (2020) it called for advancing the yuan’s role in a prudent and steady manner. The central bank now embraces the internationalization of the currency, aiming to expand the currency’s use in trade, deepen the two-way opening of financial markets in an orderly manner and further developing the offshore yuan market. The strategic move suggests that China hopes to boost its currency to a leading role, reducing the global reliance on the dollar. The PBOC set the yuan’s fixing at the strongest since October 2024 this morning with USD/CNY currently trading at 7.11.

Trade Headlines, Fed Expectations Support Risk Taking

Another week of trading starts on a positive footing, buoyed by a range of news items pleasing investors. The first came from the long-awaited US inflation data released on Friday after weeks of official data drought during the government shutdown. Headline inflation advanced to 3% in September – the highest since early 2021 and still well above the Fed’s 2% target. However, the figure was slightly lower than analysts expected, while core inflation eased from 3.1% to 3% over the same month.

So, despite the uncomfortably high absolute figures, the fact that they came in softer than expected reinforced expectations for a 25bp Federal Reserve (Fed) rate cut this week, with markets also assigning roughly a 93% probability to another cut in December. As such, the US dollar and 2-year Treasury yield came under pressure on Friday but are both firmer this morning amid renewed risk appetite and optimism that the US and China are inching closer to a trade deal. Early reports suggest the two sides have reached an initial agreement on major issues, including export controls, shipment levies and fentanyl, raising hopes that Thursday’s meeting between Trump and Xi could yield tangible progress. The CSI 300 is up about 1% at the time of writing, also supported by signs of stabilizing foreign investment flows and improved industrial profits.

In the US, the combination of softer-than-expected CPI figures, the prospect of two more rate cuts, and trade optimism pushed the S&P 500 to a fresh record high on Friday. Futures are pointing to a bullish start today. Earnings season, too, is shaping up well: around 30% of S&P 500 companies have reported so far, and 87% have delivered a positive EPS surprise, while 83% have beaten revenue expectations, according to FactSet. The blended year-on-year earnings growth rate for Q3 stands at 9.2%, marking what would be the ninth consecutive quarter of earnings growth — well above the roughly 5–6% growth expected at the start of the season.

This week, the tech heavyweights — Microsoft, Alphabet, Meta, Apple and Amazon — are set to report Q3 results. Because they account for roughly a quarter of the S&P 500’s total market capitalization, invest heavily in AI and have shouldered the market rally since early 2023 despite wars, rate hikes and global economic headwinds, their results will be crucial in determining whether the tech-led rally can extend further.

Investors are looking for:

- Concrete payoffs from AI investments.

- Growth trends in data centers and AI-related businesses.

- Commitments to continued spending, as one company’s investment is another’s revenue stream.

On Friday, Intel rose as much as 8% in pre-market trading after beating expectations, but the enthusiasm quickly faded as investors questioned whether the company’s revival is policy-driven rather than organic. Washington wants Intel to reclaim its role as America’s semiconductor champion and anchor Trump’s push to reshore chip manufacturing. That ambition has spurred cooperation with AI giants such as Nvidia and SoftBank, creating periodic price spikes. Yet for now, Intel looks more like a strategic instrument of industrial policy than a pure investment play. Government support may keep it buoyant, but whether this will translate into sustainable, profitable growth remains an open question.

Elsewhere, both the Stoxx 600 and Nikkei 225 hit fresh all-time highs. In Europe, stronger-than-expected PMI readings and the dovish Fed narrative lifted risk appetite, helping the index to new highs. This week, preliminary October CPI data are expected to show a slight moderation in inflation, and the European Central Bank (ECB) is widely expected to hold rates steady. In Japan, Takaichi’s calls for looser Bank of Japan (BoJ) policy and increased fiscal spending on tech, defense, nuclear power and cybersecurity continue to fuel the Nikkei’s exponential rally. The USDJPY is extending gains toward 153, with scope to test the 155–160 range if policy divergence persists.

Meanwhile, the EURUSD remains under pressure from French political turmoil.

Moody’s affirmed France’s credit rating on Friday but revised its outlook to negative, while the Socialist Party has threatened to topple the fragile government as soon as this week. The widening spread between French and German 10-year yields should keep EUR/USD capped below its 50-day moving average, now near 1.0690.

In the UK, last week’s data painted a mixed picture: headline inflation unexpectedly eased to 3.5%, but retail sales surprised to the upside for a fourth consecutive month, leaving the Bank of England’s (BoE) rate-cut debate as muddled as ever. In all cases, sterling remains unappealing heading into next month’s Autumn Budget.

Trade Negotiations Advance as Framework Set for Xi-Trump Meeting

In focus today

Starting off a busy week in the euro area, today sees the release of September credit data and October's German Ifo indicator. Credit growth has been strong in 2025 with recent growth rates of around 2.5% y/y, though the slowing credit impulse signals weaker GDP growth in the second half of the year. In Germany, the Ifo index has been trending lower amid softer growth momentum and dimming expectations for next year. Today's data will reveal whether this downward trend continued in October.

The week also features key central bank meetings, including the Fed's rate decision on Wednesday and the ECB and BoJ decisions on Thursday. Additionally, the highly anticipated Xi-Trump meeting is set to take place against the backdrop of increasing tensions. With US-China trade talks in Malaysia now concluded, market attention will turn to comments from both sides for signs of progress towards a broader trade deal.

Economic and market news

What happened during the weekend

US-China trade negotiations concluded on Sunday with both sides describing the talks as constructive, setting the stage for a potential mini deal at the upcoming Xi-Trump meeting. The framework deal, which still requires confirmation by the two leaders, includes commitments such as China purchasing soybeans, delaying export controls on rare-earth minerals by a year, and addressing issues like the Fentanyl crisis, shipping fees, and a 90-day trade truce extension. In return, China is likely to seek assurances that the US will hold off on imposing further tech sanctions. The agreement is expected to de-escalate tensions and move the trade war into the background for markets once again.

What happened Friday

In the US, headline inflation rose to 3.0% y/y in September from 2.9% in August, while core inflation declined to 3.0% y/y, below expectations. Monthly CPI gains were also softer than expected, with headline inflation up 0.3% m/m (cons: 0.4%). Tariff effects remained evident, with apparel prices rising 0.7% and goods overall up 0.5%. However, the data leans dovish and is unlikely to shift market expectations for upcoming Fed meetings.

In the euro area, October PMIs exceeded expectations, with the composite rising to 52.2, its highest level since May 2023, as services PMI strengthened to 52.6. Manufacturing PMI surprised marginally to 50.0 from 49.8. The data suggests positive momentum, particularly in Southern Europe, while France's weakness appears idiosyncratic. Despite the improvement, euro area growth is expected to remain modest at approximately 0.2% q/q in Q4. The stronger PMIs are unlikely to alter the ECB's "good place" assessment from its September meeting.

In Sweden, the September PPI decreased to 0.7% m/m but increased 0.5% y/y. While import and export prices declined, domestic prices saw an uptick. The rise was primarily driven by higher prices for food products, basic metals, and trade services for electricity. Prices for non-durable consumer goods, often a key indicator of food price trends, recorded a modest but not alarming increase.

Equities: Equities really liked the long-awaited US inflation print on Friday. If there was doubt in markets, the better-than-expected inflation report solidified the Fed cut that is widely expected on Wednesday night this week. In a classic risk-on with cyclicals beating defensives move, we saw S&P500 ending 0.8% higher, and both Nasdaq and Russell 2000 ended 1.2% higher. Stoxx 600 ended only 0.2% higher on Friday after a rollercoaster ride after being subject to a sharp sell-off in European rates that hit equities following the European PMIs. That said, had equity markets put more weight on the reason for higher rates (and not the higher rate itself), we should not have seen the knee-jerk lower reaction in equities in our view. Overall, last week's narrative can mostly be characterised as goldilocks at the beginning and risk-on towards the back end.

Asian markets are strongly higher across the board this morning, led once again by tech. Futures in both Europe and the US are also pointing to a solid opening. Much can be attributed to the US and Chinese negotiation teams as they both reported a looming trade deal to be agreed on Thursday at the Trump - Xi meeting.

FI and FX: Risk sentiment continues to be positive following the constructive US-China trade negotiations over the weekend, setting the scene for the expected meeting between Trump and Xi Jinping later this week. 10y UST is trading around 3bp higher compared to the close on Friday and the 2y UST, which initially fell below the 3.44% mark on Friday just after the US inflation release, has moved back to the 3.51% level. EURUSD trades around the 1.1625 level, but printed as high as 1.1648 overnight, a level which also marked the intraday high on Friday. The Fed is widely expected to cut on Wednesday, and the ECB is expected to stay on hold on Thursday.

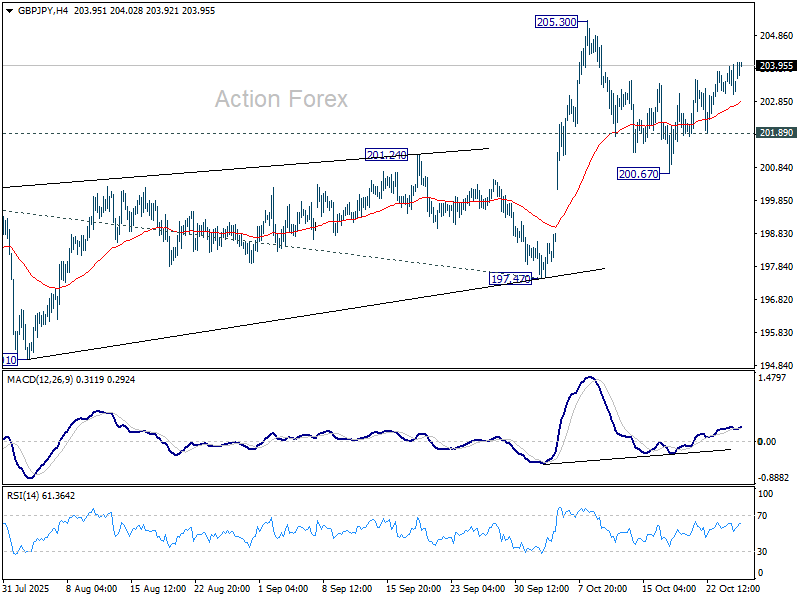

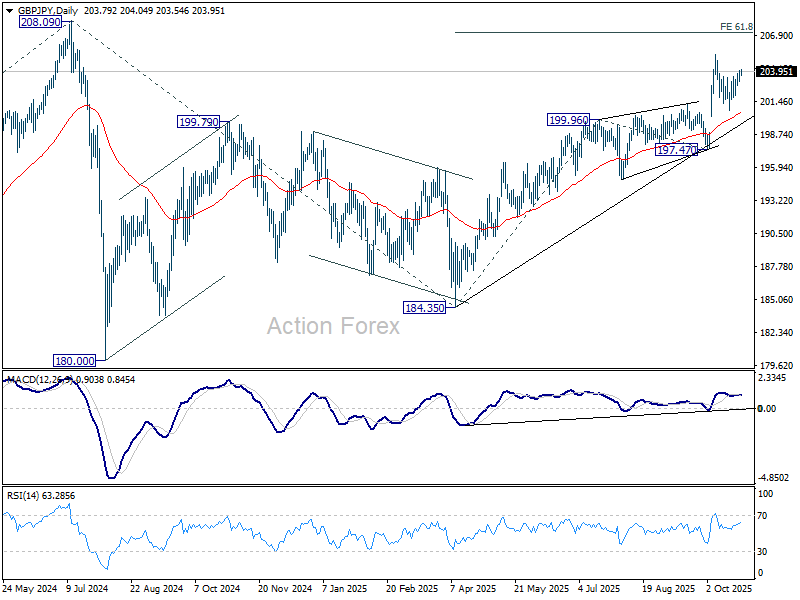

GBP/JPY Daily Outlook

Daily Pivots: (S1) 202.85; (P) 203.33; (R1) 203.83; More...

Intraday bias in GBP/JPY remains mildly on the upside for retesting 205.30 resistance. Firm break there will resume larger rise to 61.8% projection of 184.35 to 199.96 from 197.47 at 207.11. However, break of 201.89 will turn bias to the downside to extend the pattern from 205.30 with another falling leg.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

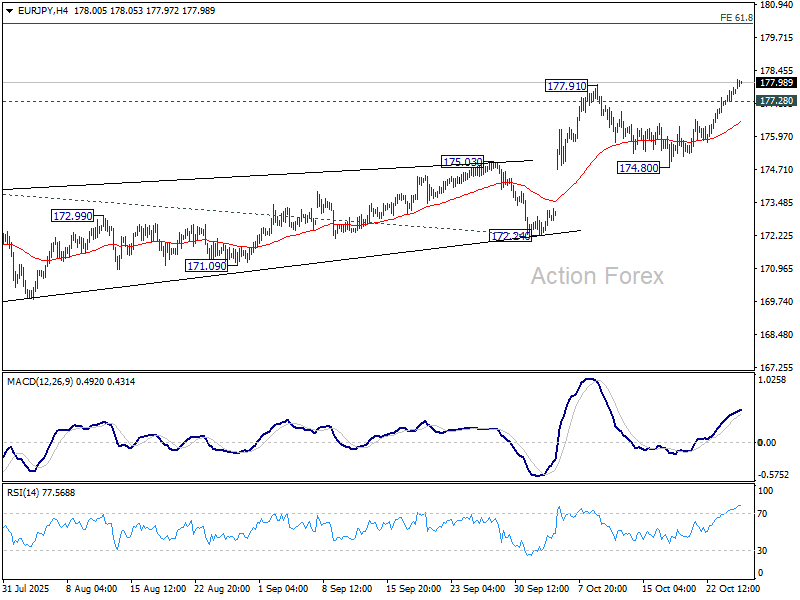

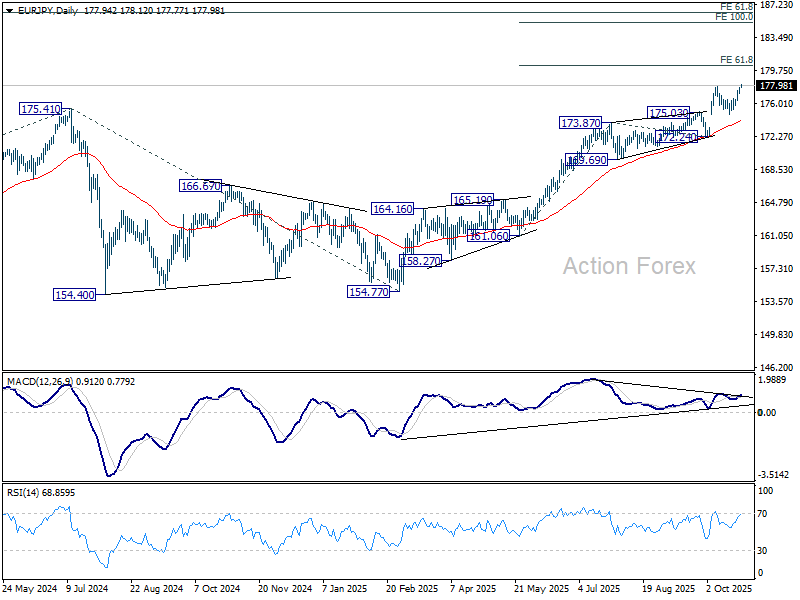

EUR/JPY Daily Outlook

Daily Pivots: (S1) 177.37; (P) 177.60; (R1) 178.00; More...

EUR/JPY's break of 177.91 resistance confirms resumption of larger up trend. Intraday bias stays on the upside for 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next. On the downside, below 177.28 minor support will turn bias neutral for consolidations. But pullback should be contained above 174.80 support.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Firm break of 172.24 support will suggests that it has turned into consolidations again. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 167.87) holds, even in case of deep pullback.

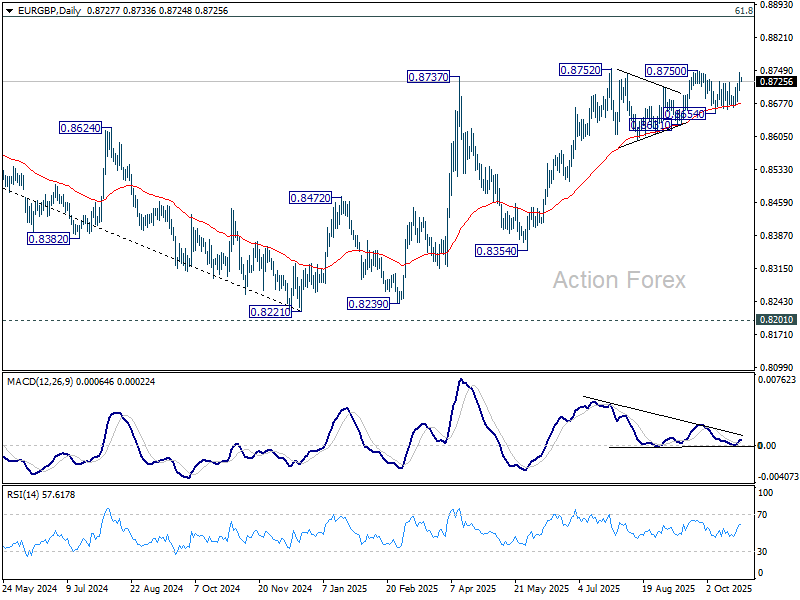

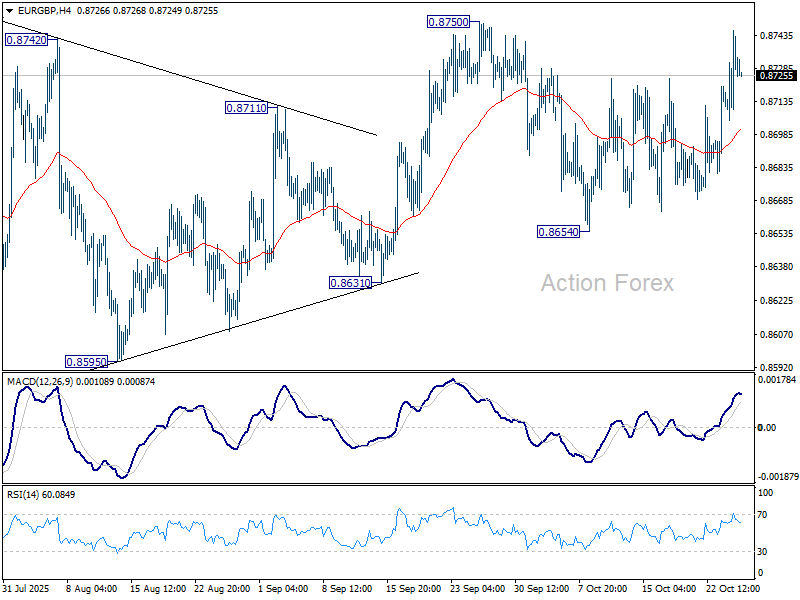

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8712; (P) 0.8729; (R1) 0.8753; More…

Intraday bias in EUR/GBP remains neutral with immediate focus on 0.8750 resistance. Firm break there will resume larger rise from 0.8221 to 0.8867 fibonacci level. On the downside, though, break of 0.8654 support will now indicate near term bearish reversal.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8654 support will be the first sign that this corrective bounce has completed. Sustained trading below 55 W EMA (now at 0.8562) will confirm, and bring retest of 0.8221 low.