Sample Category Title

USD/JPY Declines Amid Trump’s Visit to Japan

The Japanese yen strengthened on Monday, pushing the USD/JPY pair below the ¥152 mark. The move can be seen as a market reaction to U.S. President Donald Trump’s visit to Japan, where he met with the newly elected Prime Minister, Sanae Takaichi.

During the visit, the two leaders proclaimed a “new golden era” in U.S.–Japan relations and signed:

→ an official trade agreement introducing a 15% tariff on Japanese exports;

→ a deal on the supply of rare earth metals.

According to several media reports, Sanae Takaichi plans to nominate Donald Trump for the Nobel Peace Prize and invest around $550 billion in the U.S. economy.

Technical Analysis of the USD/JPY Chart

Applying a regression channel from the key low recorded on 17 September reveals a clear upward structure, which effectively illustrates major price movements (marked with arrows):

1 & 3 → rebounds from the lower boundary of the channel;

2 → reversal from the upper boundary;

4 → a consolidation phase near the median line, where supply and demand are balanced.

The latest decline from the median can be viewed as a sign of shifting sentiment, suggesting that sellers may now target the lower boundary of this channel. However:

→ the 151.50 level represents a notable support zone, having held firm on 21–22 October;

→ bearish conviction is also reinforced by the pair’s repeated failure to close above ¥153, forming what appears to be a Double Top pattern.

Whether the pair will reach the lower edge of the regression channel largely depends on the broader fundamental backdrop:

→ Trump’s international tour continues, with traders awaiting his meeting with China’s leadership;

→ this week’s key events include interest rate decisions from the Federal Reserve on Wednesday and the Bank of Japan on Thursday — the latter drawing particular attention given the recent change in Japan’s leadership.

These developments could significantly shift sentiment in the USD/JPY market — traders should be prepared for potential spikes in volatility.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Little Overnight News to Sustain Risk Rally

Markets

Stock markets in Europe and the US soared to new record highs. Investors are banking on the US and China nearing a trade agreement, or at least an extension to the truce, after constructive talks last weekend. US president Trump and his Chinese counterpart Xi are expected to seal the deal during their in-person meeting on Thursday. The tech-heavy Nasdaq rallied 1.9%. The EuroStoxx50 had to settle for 0.6%. Core bond yields gapped higher at the open but pared losses going through the session. Net daily changes in the US varied between +0.9 (2-yr) to -4.1 bps (30-yr). The double US auction ($69bn 2-year and $70bn 5-yr) went without any hiccups. German rates finished flat to slightly lower at the very long end of the curve (-1.7 bps). Spreads across the euro area steadied, including in France, where the political atmosphere is growing tenser again. After a delayed vote on a wealth tax last Saturday, the Socialists are threatening to topple the government by the end of the week if there’s no significant tax increase on the wealthier segment in next year’s budget. The French parliament adopted an amendment yesterday that would increase taxes on the country’s largest companies but it’s yet unclear whether it suffices for the Socialist Party. The French topic has become an evergreen and an escalation could soon haunt the euro again. From a daily perspective, though, EUR/USD eked out another be it tiny gain for a fourth day straight. The pair rose to 1.1645. DXY turned south in technical irrelevant trading. The Aussie dollar outperformed global peers.

There’s little overnight news to sustain the risk rally, causing it to fizzle. It also makes sense against the backdrop of important central bank policy meetings from the Fed, ECB and BoJ, Q3 GDP and October inflation numbers in the euro area and five big US companies (accounting for about 25% of the S&P500) due to report earnings over the coming days. The eco calendar today has some interesting elements in store, even though they are most likely of secondary importance to trading. Consumer confidence (Conference Board) is on tap in the US. The Bank Lending Survey and Q3 negotiated wages are to be released for the euro area. Both are closely watched by the ECB but won’t change the expected rates status quo. We expected technical consideration to take over FI and FX trading. The Japanese yen stands out though. A combination of verbal warnings and a constructive meeting between Trump and Takaichi push USD/JPY towards 152. Some were worried ahead of the reunion that Japan’s increased defense spending efforts would have fallen short of US demands.

News & Views

By September 2025 year-to-date (YTD), new EU car registrations increased by 0.9% compared to the same period last year, marking the third consecutive month of growth. Recent momentum has been somewhat driven by the launch of new models, with September alone posting a strong 10% increase. The battery-electric car (BEV) market share held steady at 16.1% YTD (up from +13.1% YTD September 2024). Three of the four largest markets in the EU, accounting for 62% of BEV registrations, saw gains: Germany (+38.3%), Belgium (+12.4%), and the Netherlands (+3.9%). Hybrid-electric vehicles (HEV) remained the most popular power type choice among EU buyers (34.7%, up from 30.1%). The combined market share of petrol and diesel cars fell to 37%, down from 46.8% over the same period in 2024. The preferred power source of new car registrations in Belgium remains petrol (41.9% YTD 2025 vs 42.1% YTD 2024). Together with BEV’s (33.4% YTD 2025 share vs 27% YTD 2024) they account for over 75% of all new registrations.

The British Retail Consortium’s (BRC) shop price monitor showed retail prices falling by 0.3% M/M in October. It’s the first decline since March with both food (-0.4% M/M; largest drop since December 2020) and non-food prices (-0.2% M/M) falling. Lower food prices are important for the hawkish BoE members who warn for the outsized role they have in shaping inflation expectations. Last week’s official CPI numbers also showed lower food price growth (September) than feared. BRC CEO Dickinson highlighted fierce competition amongst retailers, widespread discounting and an easing of global sugar prices which helped to bring down prices of chocolate and confectionary ahead of Halloween. Some retailers already started promotions for electrical goods and beauty products before the Black Friday sales that typically fall in November. On an annual basis, overall retail price growth slowed from 1.4% Y/Y to 1% Y/Y with higher food prices (3.7% Y/Y) more than compensating for lower non-food prices (-0.4% Y/Y).

Not a Bubble Until It Bursts

Major global indices climbed yesterday — many to fresh all-time highs — on news that the US and China are inching closer to a trade deal that would prevent the two countries from imposing triple-digit tariffs on their mutual exports. Today, that optimism continues: talks between President Trump and Japan’s new Prime Minister, Sanae Takaichi, reportedly went very well, leading to an agreement on critical minerals trade. Trump praised Japan, calling this the “new golden age” for the US-Japan alliance. It could hardly have gone better.

On the Chinese front, investors are now bracing for a positive outcome as well. Yet fundamentally, the US and Chinese objectives remain difficult to align. The US wants to bring manufacturing back home — which comes at China’s expense — while also encouraging Beijing to spend more domestically, something Xi has tried and largely failed to achieve. As two Bloomberg journalists aptly wrote this morning, China’s latest five-year plan “appears to show Trump’s rebalancing dream to be — as far as Beijing is concerned — a fantasy.”

Still, personal rapport between the two leaders could help keep relations as stable as possible under the circumstances. But any trade deal is unlikely to mark an endgame or magically eliminate policy volatility under Trump. Fortunately, markets have acclimated to that since January. The S&P 500 hasn’t waited for perfect news to extend its rally to new highs — it’s been doing so since June — while Chinese and Hong Kong equities are clawing back past losses, led by tech names.

In Japan, the Nikkei on Monday crossed the 50’000 level for the first time in history, though we’re seeing some profit-taking this morning. But overall, the news flow remains supportive of risk-taking: trade deals with the US are lining up, the Federal Reserve (Fed) and the Bank of Canada (BoC) are both expected to cut rates this week, and the Bank of Japan (BoJ) outlook has turned softer under Takaichi.

What could go wrong? Time will tell — but for now, equity investors around the world are enjoying the rally, while safe-haven assets pull back. Gold, for instance, slipped below $4,000 per ounce, in what looks like a healthy correction after its exponential rally. The pullback could deepen by 10–20%, bringing prices back toward $3,400, the key 38.2% Fibonacci retracement of the past two-year surge. Above $3,400, gold’s uptrend remains intact, and bulls still have their eyes on $5,000.

Elsewhere in commodities, copper remains volatile but broadly positive, while US crude tested — but failed to clear — its 50-day moving average yesterday despite the trade optimism. Tactical bullish bets placed after last week’s sanctions against Rosneft and Lukoil are now being closed. There’s speculation the sanctions may prove less severe than initially feared, as Trump likely wants to avoid triggering a price spike. Add to that Saudi Arabia’s efforts to expand market share and expectations that OPEC will bring additional barrels to market, and the bears are likely to push for a return below $60 per barrel.

In FX, the US dollar retreated to a one-week low as the Fed began its two-day policy meeting. The central bank is widely expected to deliver a second 25-bp cut this year, amid growing speculation it may also announce an end to quantitative tightening (QT). Some suggest QT could end immediately, arguing that post-pandemic excess liquidity has now been fully absorbed and that the Fed wants to avoid draining it further. If that’s the case — if this week’s much-expected, fully priced-in rate cut is sweetened by the end of QT — equity bulls will have little reason to reverse the current rally. Short-term yields and the dollar would likely move lower.

Inside equities, AI and tech remain the centre of attention this week. While investors await Big Tech earnings on Wednesday and Thursday, Qualcomm stood out yesterday by announcing plans to launch new AI chips to compete with Nvidia and AMD in the rapidly expanding AI-chip market. Its AI200 and AI250 chips will hit the market next year, with Saudi Humane as its first customer. Nvidia and AMD could’ve felt queasy on the news — but no: both rose about 2.7–2.8%, as optimism spread that chip appetite keeps growing and there’s enough cake for everyone to have a generous slice. Qualcomm, meanwhile, jumped more than 20% intraday and closed the session roughly 11% higher.

In the coming days, we’ll find out Big Tech’s spending plans, which will directly affect chip-demand forecasts. Together, Amazon, Microsoft, Alphabet, and Meta are expected to have spent over $100 billion in Q3, most of it on chips and data centres. Bubble or not, the money is being spent, the rally is on — and it’s not a bubble until it bursts.

Euro Area Credit Stability Supports Modest Q3 GDP Outlook

In focus today

In Sweden, the Riksbank will release the semi-annual Business Survey at 9.30 CET. While often overlooked by markets, the survey has historically been a key input for the Riksbank's monetary policy deliberations. We expect it to align with the view of the Riksbank's main scenario at this juncture, with a still weak but gradually recovering economy. Given persistently high inflation, we are paying particular attention to the quantitative measures on expected price changes. The May 2025 report showed that companies selling to households planned to raise prices over the next 12 months, reflecting higher purchasing costs and their inability to fully offset previous cost increases.

Economic and market news

What happened overnight

The US and Japan have signed a framework agreement aimed at securing supply chains for critical minerals and rare earths, reducing dependence on China. In a statement, the White House emphasised that the deal seeks to enhance the resilience and security of critical mineral and rare earth supply chains for both nations.

What happened yesterday

In the euro area, bank lending continued to grow in September, with loans to non-financial corporations increasing by 2.9% y/y. The credit impulse, which correlates more closely with GDP growth, remained stable at 0.3% of GDP, indicating that lower policy rates are still supporting the economy. This suggests euro area GDP likely grew in Q3, albeit at a slower pace than in the first half of the year. We expect Thursday's GDP data to confirm a modest 0.1% q/q growth for Q3.

The German Ifo indicator rose slightly more than expected in October, rising to 88.4 from 87.7. However, the current situation assessment declined unexpectedly to 85.3 - the lowest since February - pointing to ongoing economic challenges. In contrast, expectations rose sharply to 91.6 from 89.8, signalling optimism. While Ifo's current situation assessment remains weaker than the recent uptick in PMIs, the rebound in expectations and stronger PMIs suggest a gradual recovery in the German economy over the coming year.

Equities: Equities were on a steady grind higher through yesterday's session. S&P 500 ended 1.2% higher, Nasdaq 1.9% and Russel 2000 0.3% higher, driven by (yet again) tech and cyclical stocks. Qualcomm announced that they will start shipping their new AI chip next year and led the rally. Overnight, Asian markets are somewhat mixed with Nikkei down 0.4% and Shenzen 300 up 0.2%.

FI and FX: USD continued to weaken overnight, with EURUSD moving towards 1.1670 and USDJPY dropping below 152 as a readout from Scott Bessent's meeting with Japan's Katayama indicated that BoJ policy and exchange rate volatility were discussed, serving as a reminder that the US administration prefers a weaker dollar. US yields fell from late afternoon and the 10y UST is now back just below 4%. We expect the Fed to announce an end to QT in Treasuries at Wednesday's meeting, and as a rate cut of 25bp is widely expected, this could be a bigger market mover in our view. With cuts fully priced for both October and December, we think near-term risks for the USD remain asymmetrically tilted to the upside. EURSEK remains at the lower end of the recent 10.90-11.10 range and EURNOK has been mostly sideways since Friday afternoon in a 11.62-11.66 range.

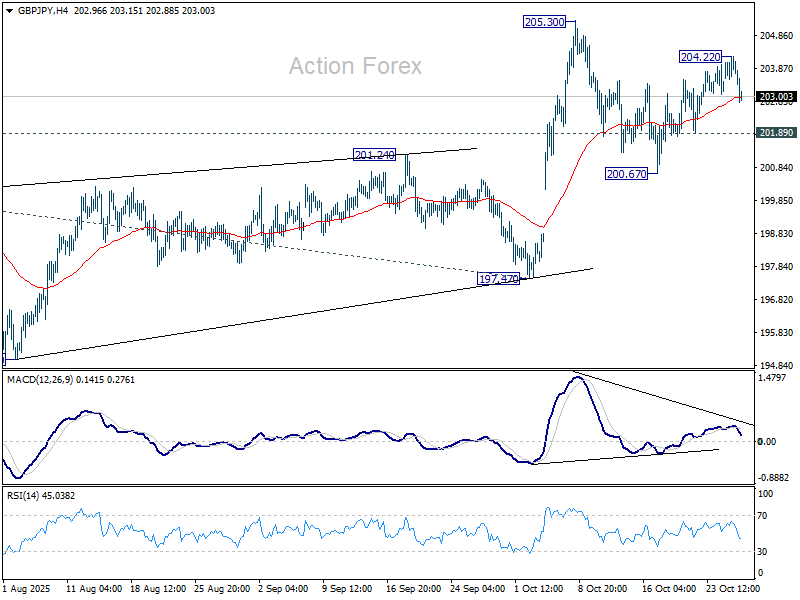

GBP/JPY Daily Outlook

Daily Pivots: (S1) 203.56; (P) 203.90; (R1) 204.27; More...

Intraday bias in GBP/JPY is turned neutral with current retreat and some consolidations would be seen first. On the upside, above 204.22 will target a retest on 205.30 high. Break there will resume larger rise to 61.8% projection of 184.35 to 199.96 from 197.47 at 207.11. However, break of 201.89 will turn bias to the downside to extend the pattern from 205.30 with another falling leg.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

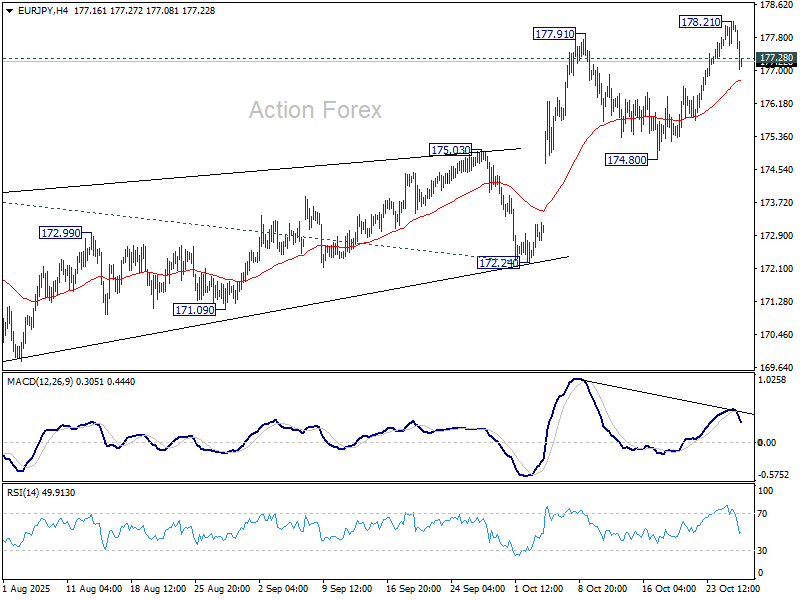

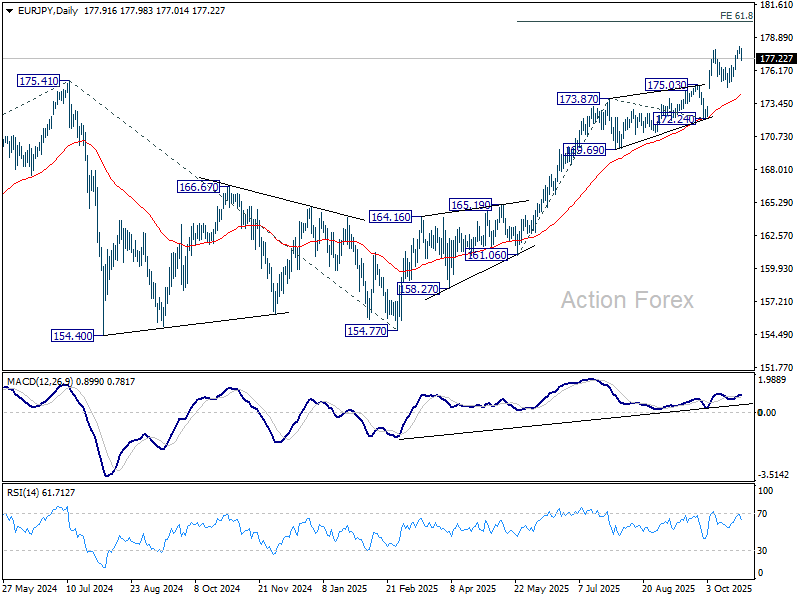

EUR/JPY Daily Outlook

Daily Pivots: (S1) 177.70; (P) 177.96; (R1) 178.30; More...

Intraday bias in EUR/JPY is turned neutral first with current retreat. Some consolidations would be seen below 178.21 temporary top, but downside should be contained well above 174.80 to bring another rally. ON the upside, break of 178.21 will resume larger up trend to 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Firm break of 172.24 support will suggests that it has turned into consolidations again. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 167.87) holds, even in case of deep pullback.

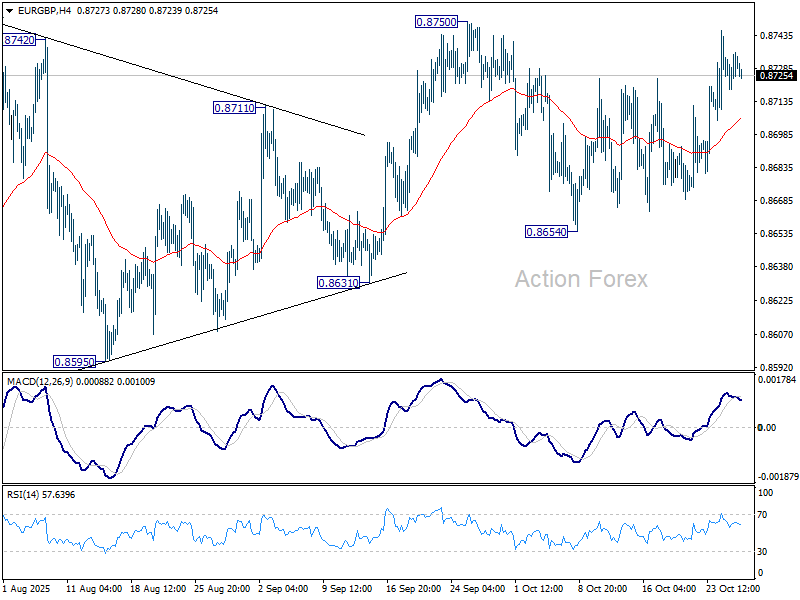

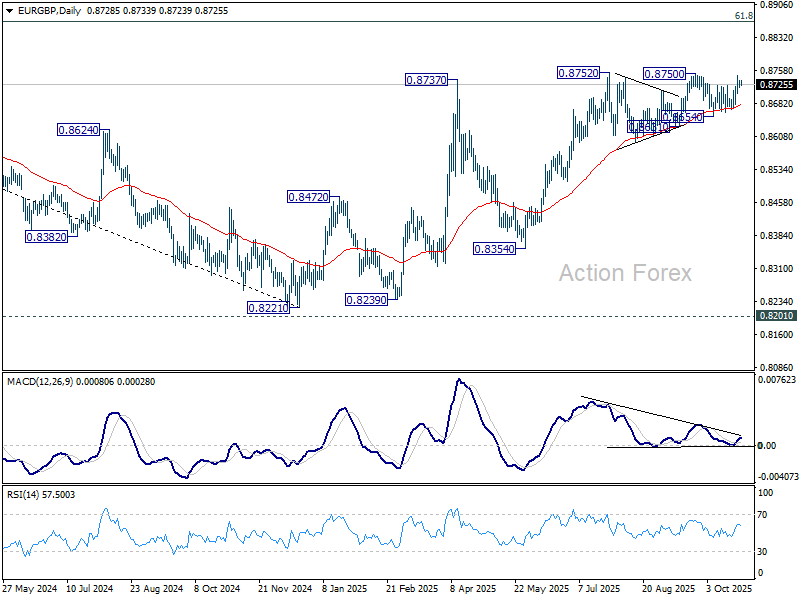

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8729; (R1) 0.8738; More…

EUR/GBP retreated ahead of 0.8750 resistance and intraday bias remains neutral. On the upside, firm break of 0.8750 will resume larger rise from 0.8221 to 0.8867 fibonacci level. On the downside, though, break of 0.8654 support will now indicate near term bearish reversal.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8654 support will be the first sign that this corrective bounce has completed. Sustained trading below 55 W EMA (now at 0.8562) will confirm, and bring retest of 0.8221 low.

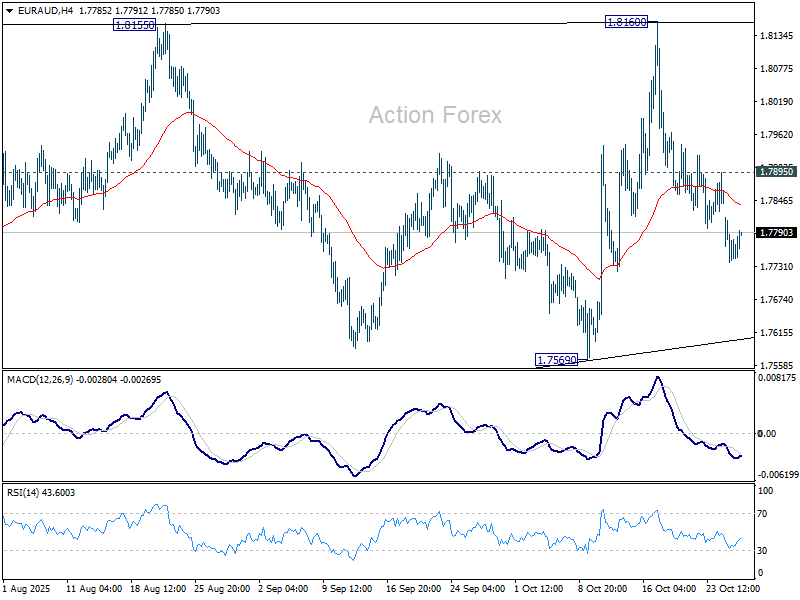

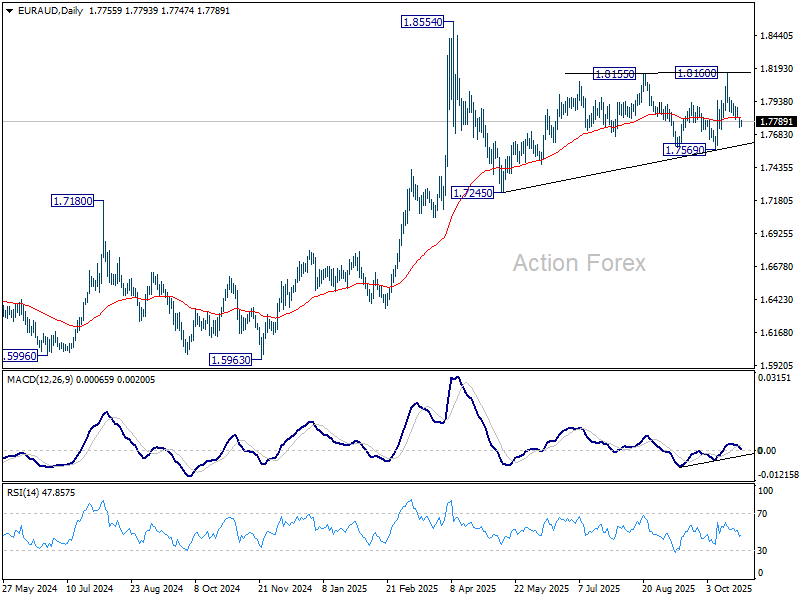

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7729; (P) 1.7774; (R1) 1.7808; More...

Intraday bias in EUR/AUD stays on the downside as fall from 1.8160 is in progress for 1.7569 support. Break there will indicate that corrective pattern from 1.8554 already in its third leg, and target 1.7245. On the upside, above 1.7895 minor resistance will turn intraday bias neutral.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern, which might still be in progress. But outlook will stay bullish as long as 55 W EMA (now at 1.7391) holds, and up trend from 1.4281 (2022 low) is expected to resume through 1.8554 at a later stage.

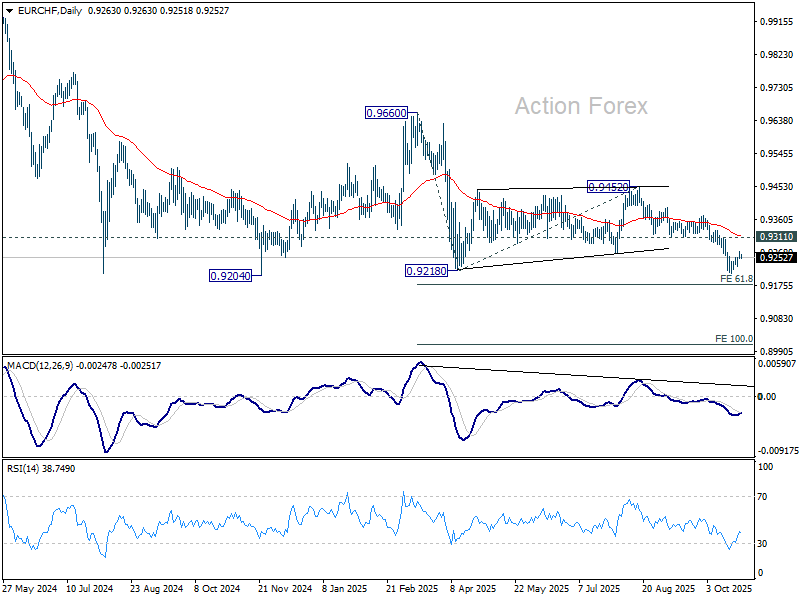

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9252; (P) 0.9262; (R1) 0.9272; More....

Intraday bias in EUR/CHF stays neutral for the moment, and more consolidations could be seen above 0.9206. Upside should be limited below 0.9311 support turned resistance. On the downside, break of 0.9204 will confirm larger down trend resumption. Next target is 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179. Firm break there will target 100% projection at 0.9010.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9385). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.

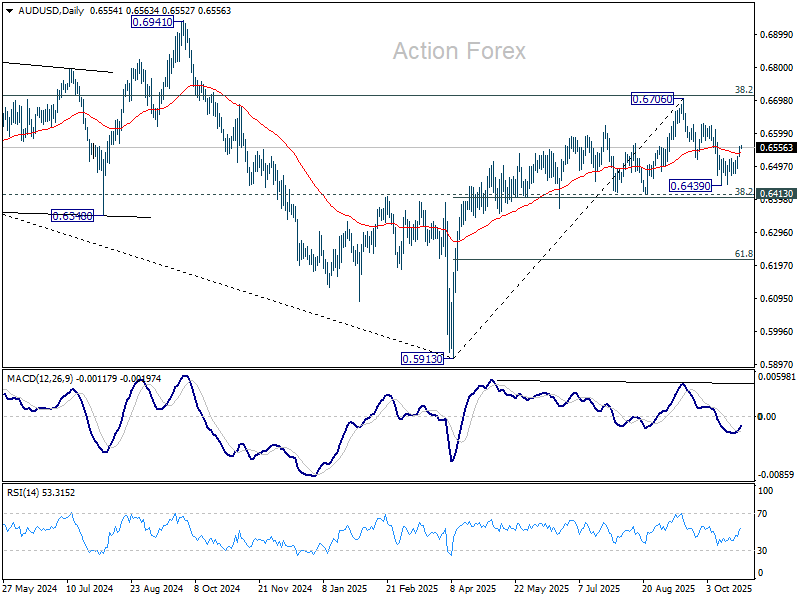

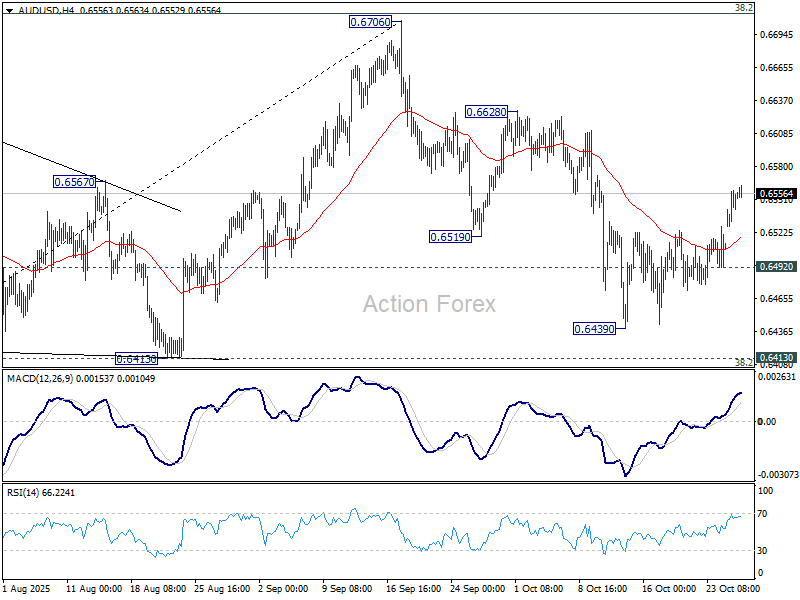

AUD/USD Daily Report

Daily Pivots: (S1) 0.6536; (P) 0.6548; (R1) 0.6567; More...

AUD/USD's break of 55D EMA suggests that corrective fall from 0.6706 has already completed with three waves down to 0.6439. Intraday bias is back on the upside for 0.6628 resistance first. Firm break there will target a retest on 0.6706 high. ON the downside, however, break of 0.6492 will resume the correction to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.