Sample Category Title

Sunset Market Commentary

Markets

Friday’s risk rally continued going into the start of a busy week. US and Chinese negotiators have agreed on key matters during trade talks in the sidelines of the ASEAN leaders summit in Malaysia. Some of the sticky points that have been resolved include a resumption of Chinese purchases of US soybeans and a delay (allegedly by one year) of the tighter Chinese export controls on rare earths. In return the US shelves the threat of an additional 100% tariff on Chinese imports. They pave the way for an extension to the trade truce when Trump and Xi meet later this week. Additional positive headlines came from Brazil, which according to president Lula is closing in on having a definitive resolution to the trade conflict. All this follows Indian newspaper Mint mid-last week reporting that the world’s 4th largest economy is closing in on a deal that would cut levies to 15% from the current 50%. The constructive trade vibes hurl US stock markets to yet another record high, unhindered by the additional 10% Canadian levy Trump introduced. The Nasdaq outperforms by rising 1.3%. European stocks add up to 0.5% (EuroStoxx50). The French CAC40 lags peers, perhaps over renewed political concerns. The Socialist Party will decide by the end of the week whether or not to topple Lecornu II. It ties the PM and his government’s fate to a wealth tax to be introduced in the 2026 budget. It would be another major win for the Socialists, after securing a suspension to the pension reform until after the presidential elections in 2027. It underscores the difficulty of addressing a spiraling debt-deficit problem in the fractured French parliament where every party can basically act as kingmaker. Moody’s last Friday downgraded the rating outlook to negative from stable for that exact reason. The OAT/swapspread (80 bps) holds steady today and remains the euro area’s highest (topping Italy). Core bond yields in general continue to bottom out, jumpstarted by Friday’s PMIs. Doing so marks an end to the diverging message brought by equity and FI markets since the beginning of October. Treasuries underperform with yields adding up to 2.7 bps in a bear flattener. European yields gapped higher at the open but currently trade more or less flat. FX markets show little direction. Looming key events such as the Fed and ECB policy meeting could act as a paralyzing force, though we doubt they’ll produce tidal shifts in the market. EUR/USD treads water around 1.164. EUR/GBP is similarly going nowhere around 0.873. The NZD and especially AUD as important trade partners to China are the key beneficiaries from the US/Sino trade thaw. AUD/USD rises to 0.655. Gold and silver drop materially with the former at risk of losing support at 4k.

News & Views

The Confederation of British Industry’s October retail sales report shows that the sector remains in a prolonged downturn with annual sales volumes falling for a thirteenth consecutive month. Persistent uncertainty ahead of the Autumn Budget is deepening the strain on retailers and other distribution firms that are still grappling with the effects of last year’s fiscal decisions. Weak demand conditions were also reflected in further sales declines across wholesaling and motor trades given overall poor consumer confidence. CBI data suggested there was a small increase in online retail sales volumes but would contract next month. The CBI measure comparing sales with a year earlier improved marginally in October, from -29 to -27 but remains firmly negative. The gauge for expected sales for the month ahead slipped from -36 to -39.

Slovak debt management agency Ardal today announced a new 12-yr EUR benchmark deal which will follow in the near future, subject to market conditions. Ardal already did one other new (15-yr) benchmark this year in February raising €3bn. They raised another combined €6.7bn via multiple regular auctions and retail bond offerings. This year’s funding need consists of €6.55bn redemptions and an expected state budget deficit of €6.7bn. Next year’s outlook suggest a somewhat lower gross bond issuance (€10bn) with redemptions (€4.9bn) and the expected budget deficit (€5.1bn) both being lower. Slovakia has an A+ credit rating at S&P (negative outlook, confirmed last Friday) and A- and the equivalent A3 at Fitch and Moody’s (both stable outlook).

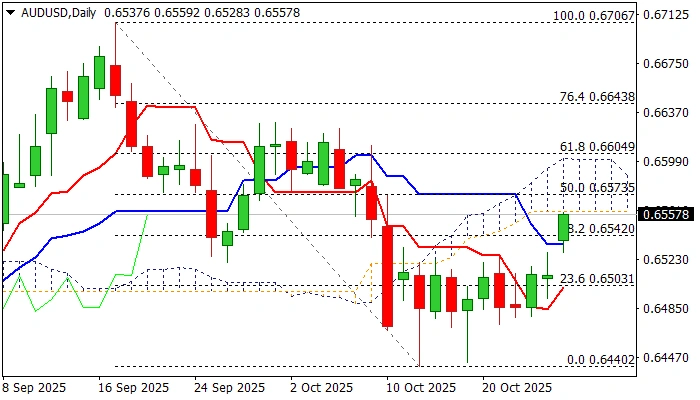

AUD/USD: Fresh Risk Appetite Lifts Australian Dollar to Two-Week High

AUDUSD opened with a gap higher and hit two-week high in almost 1% advance in early Monday trading.

Fresh risk appetite dominated in the market at the start of the week, as growing optimism of US-China trade deal, fueled demand for riskier assets and inflated risk-sensitive Aussie dollar.

Softer US dollar on cooler than expected US inflation in September (report released on Friday) also contributes to fresh strength.

Monday’s acceleration pressures significant resistance at 0.6560 (base of daily Ichimoku cloud, spanned between 0.6560 and 0.6600) where increased headwinds could be expected, as daily studies are mixed (north-heading 14-d momentum is still in the negative territory / stochastic is overbought against rising RSI that moved above 50 and MA’s turning to bullish setup).

Bullish scenario requires penetration of daily cloud and rise above nearby 0.6573 Fibo barrier (50% retracement of 0.6706/0.6440) to strengthen near-term structure and open way for attack at next key barriers at 0.6600 zone (cloud top / Fibo 61.8%).

Conversely, failure at cloud base may keep an action on hold, but biased higher while holding above 100DMA (0.6533).

Investors await Fed’s rate decision, due on Wednesday (0.25% rate cut is widely expected, with focus on speech of Fed chief Powell, expected to provide signals of central bank’s next steps, as well as release of US PCE Index on Friday, Fed’s preferred inflation gauge).

Res: 0.6560; 0.6573; 0.6600; 0.6629.

Sup: 0.6542; 0.6533; 0.6500; 0.6472.

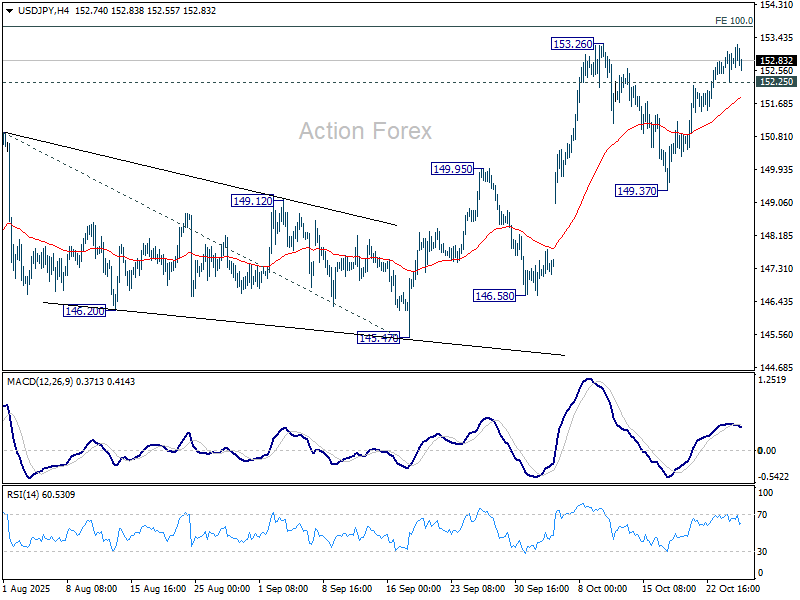

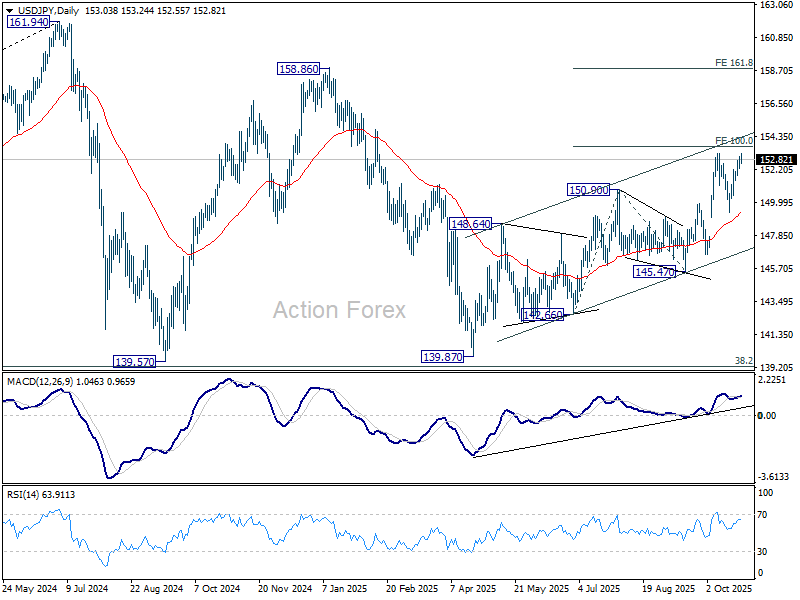

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.45; (P) 152.76; (R1) 153.18; More...

Intraday bias in USD/JPY stays mildly on the upside for 153.26 and then 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break would extend the rise from 139.87 to 100% projection of 142.66 to 150.90 from 145.47 at 153.71. On the downside, below 152.25 minor support will turn intraday bias neutral again first.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

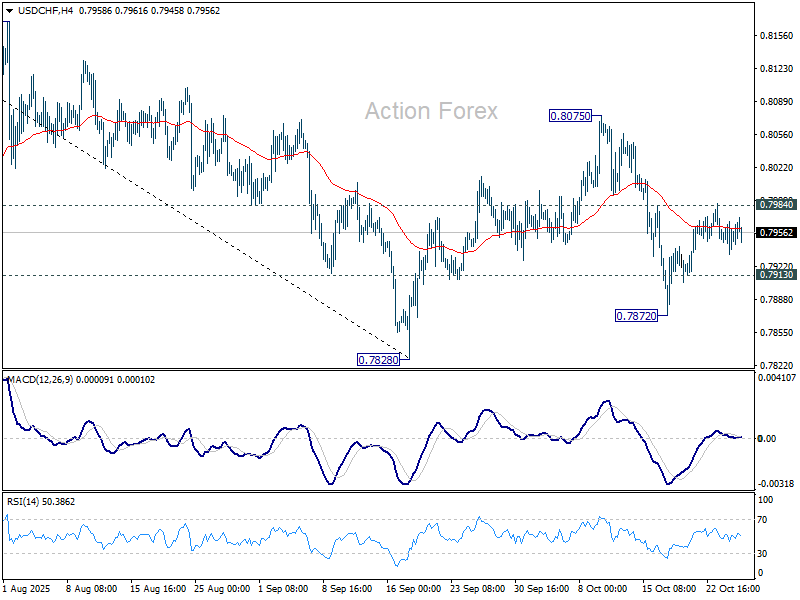

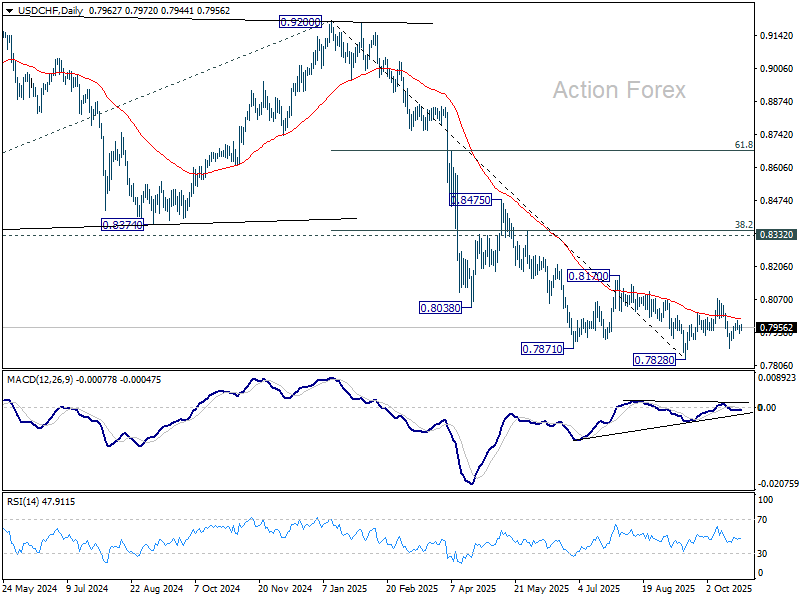

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7939; (P) 0.7954; (R1) 0.7972; More…

Intraday bias in USD/CHF stays neutral as range trading continues. Deeper decline is still in favor with 0.7984 resistance intact. On the downside, below 0.7913 will turn bias to the downside for 0.7872 support, and then 0.7828 low. However, firm break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

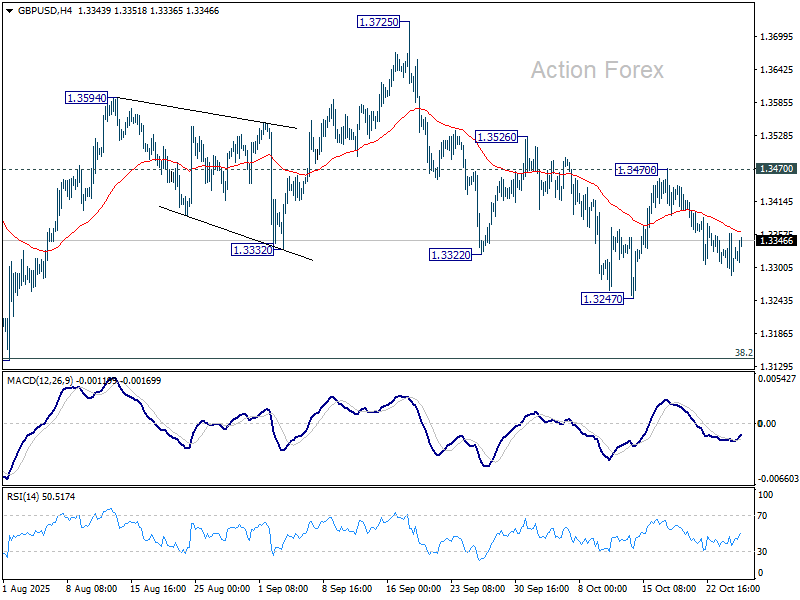

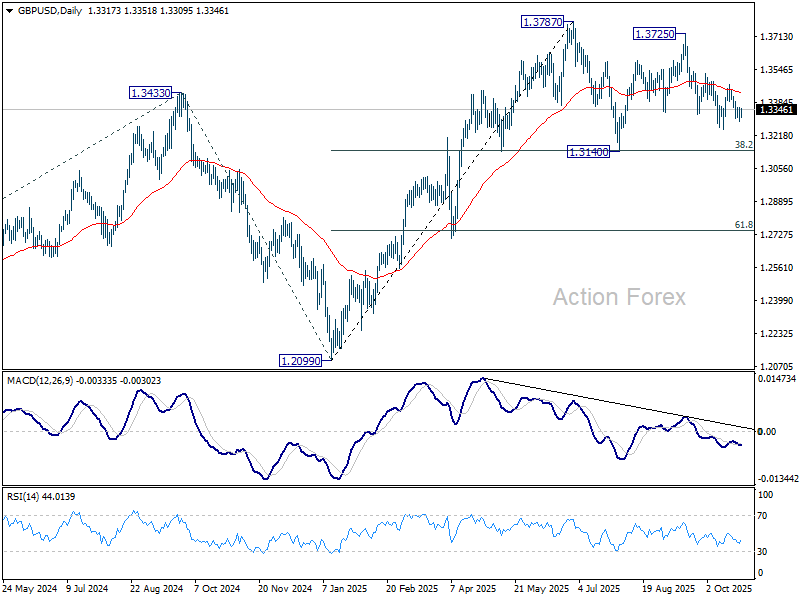

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3280; (P) 1.3319; (R1) 1.3351; More...

GBP/USD is still bounded in range of 1.3247/3470 despite today's mild recovery. Intraday bias stays neutral for the moment. On the downside, break of 1.3247 will target 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, break of 1.3470 resistance will turn bias back to the upside for 1.3526, and then 1.3725/87 resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

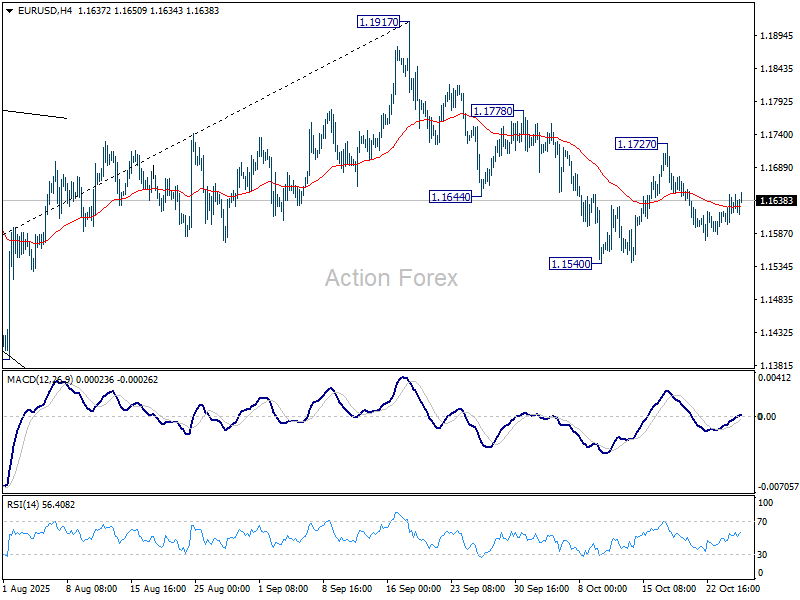

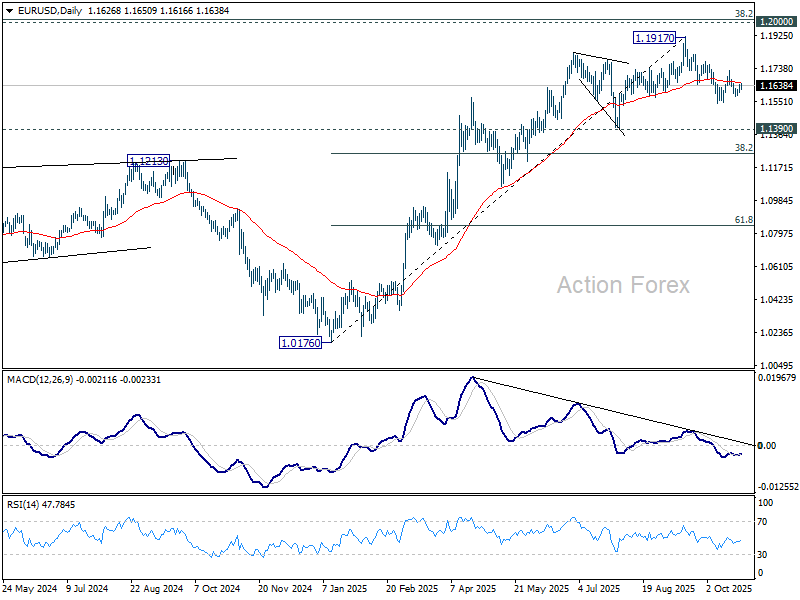

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1603; (P) 1.1626; (R1) 1.1650; More…

EUR/USD recovers mildly today but remains bounded in range of 1.1540/1727. Intraday bias stays neutral and further decline is in favor. On the downside, below 1.1540 will resume the fall from 1.1917 and target 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1301) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

Dollar on Back Foot as Markets Cheer Prospects of US–China Tariff Truce

Optimism dominated Asian markets on Monday, with Japan’s Nikkei 225 surging to a fresh record high above the 50,000 mark. The risk-on tone carried through to U.S. futures, which pointed to another higher open as Wall Street looks set to continue its record-breaking run. In contrast, European markets lagged behind, trading mostly flat as regional investors adopted a more cautious stance.

The upbeat sentiment in Asia and the US was driven by renewed confidence that the U.S.–China trade conflict will avoid a fresh escalation. Reports suggested that the threatened 100% tariffs on Chinese goods, previously due to take effect on November 1, are now effectively off the table. This follows a weekend of constructive talks between top U.S. and Chinese trade officials that laid the groundwork for a broader framework agreement.

Investors are now looking ahead to Thursday’s highly anticipated meeting between U.S. President Donald Trump and Chinese President Xi Jinping at the APEC summit. The two leaders are expected to endorse the new framework, which reportedly includes a delay to China’s rare-earth export restrictions and the resumption of Chinese soybean purchases from the U.S. While the fate of the TikTok dispute remains uncertain, markets appear reassured that both sides are prioritizing de-escalation.

The tone from the weekend meetings was viewed as better than expected, reinforcing hopes that the trade truce will hold into next year. For now, traders are taking the view that a formal agreement between Trump and Xi would further cement global risk appetite and underpin equities, commodities, and pro-growth currencies.

In currency markets, Aussie remains the day’s top performer, followed by Kiwi and then Sterling. The Dollar is the weakest, trailed by Swiss franc and Yen, while Euro and Loonie sit mid-pack.

In Europe, at the time of writing, FTSE is up 0.12%. DAX is down -0.01%. CAC is down -0.12%. UK 10-year yield is down -0.01 at 4.425. Germany 10-year yield is up 0.007 at 2.635. Earlier in Asia, Nikkei rose 2.46%. Hong Kong HSI rose 1.05%. China Shanghai SSE rose 1.18%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield rose 0.015 to 1.674.

German Ifo rises to 88.4 as business expectations improve

Germany’s Ifo Business Climate Index rose to 88.4 in October from 87.7, topping expectations of 87.8. The uptick was driven mainly by stronger optimism about the outlook, even as assessments of current conditions softened. Expectations Index climbed to 91.6 from 89.8, while Current Assessment slipped to 85.3 from 85.7, highlighting that the recovery remains more hopeful than tangible.

By sector, the data painted a mixed but improving picture. Manufacturing sentiment strengthened from –13.2 to –11.7, with Ifo noting that “expectations in particular brightened” and the decline in new orders has “come to a halt.” The service sector saw a sharp rebound, rising from –3.0 to –0.1, as providers turned less skeptical about the coming months. Trade confidence also improved from –23.9 to –21.5, while construction slipped slightly from –14.8 to –15.0.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1603; (P) 1.1626; (R1) 1.1650; More…

EUR/USD recovers mildly today but remains bounded in range of 1.1540/1727. Intraday bias stays neutral and further decline is in favor. On the downside, below 1.1540 will resume the fall from 1.1917 and target 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1301) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

USD/JPY Tests Key February Highs

The USD/JPY pair rallied sharply on Monday, reaching the 153.00 level and testing levels not seen since February 2025. This bullish momentum is being driven by expectations of significant fiscal stimulus from Japan's new government and ongoing uncertainty surrounding the Bank of Japan's (BoJ) policy path.

The yen has been under sustained pressure since the election of Prime Minister Sanae Takaichi, whose administration is expected to pursue expansive fiscal spending while endorsing an accommodative monetary stance. Reports suggest a substantial stimulus package, valued at over ¥13.9 trillion, could be unveiled as early as November. The plan aims to support households and mitigate inflationary pressures.

While the BoJ is widely expected to keep interest rates unchanged at its meeting this week, market participants will be watching closely for any communication regarding the conditions for a future rate hike should inflationary pressures ease. Additionally, an upcoming meeting between Prime Minister Takaichi and US President Donald Trump is being monitored for further signals on the direction of Japan's economic policy.

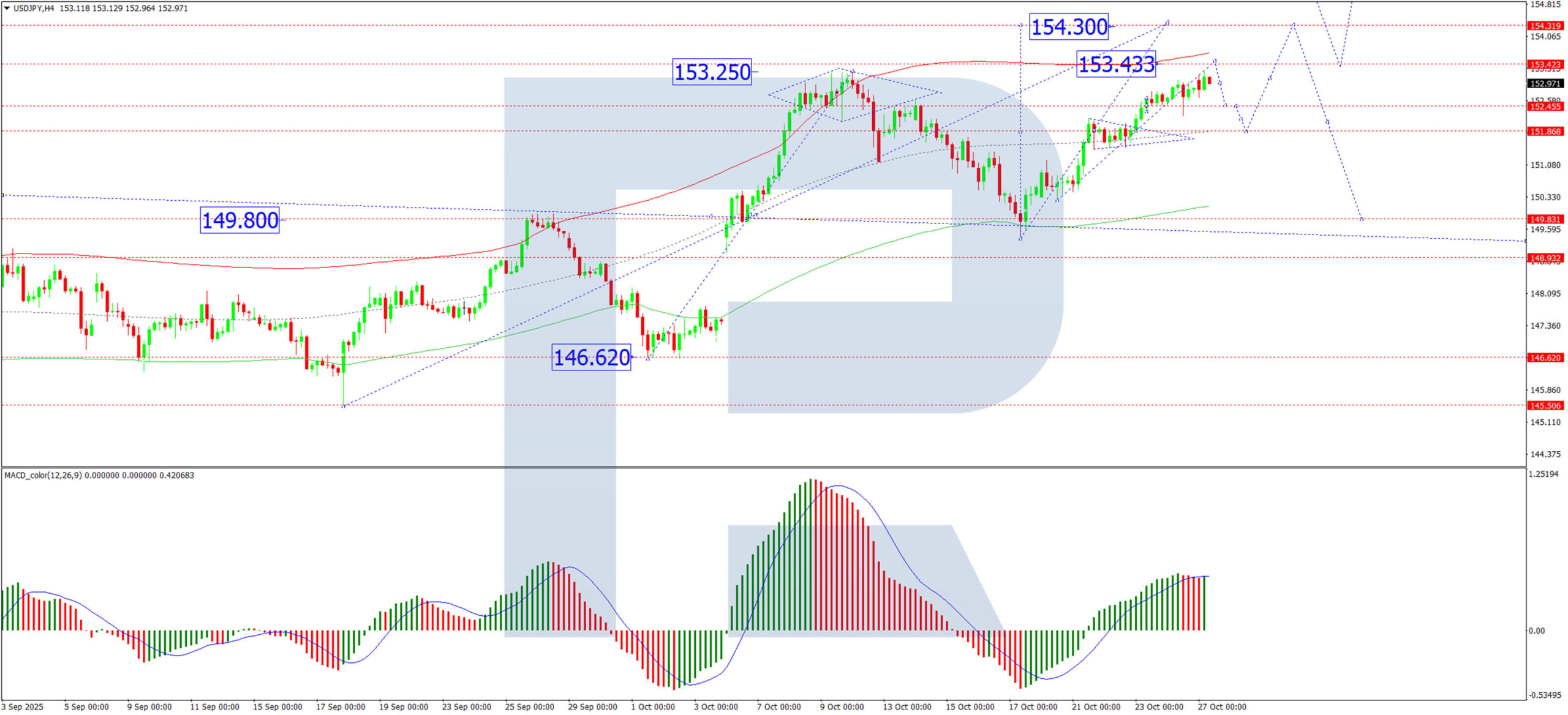

Technical Analysis: USD/JPY

H4 chart:

On the H4 chart, USD/JPY broke out upwards from a consolidation range around 151.80, confirming a renewed uptrend with an initial target at 153.43. The pair has since completed a leg higher to 153.24 and is now undergoing a technical retracement, currently testing the 152.43 level from above. We expect this pullback to be followed by another impulse higher towards the 153.43 target. Following that, a more pronounced correction towards 151.80 is anticipated before the broader uptrend resumes, with the next major objective at 154.33. The MACD indicator supports this outlook, with its signal line firmly above zero and pointing upwards, confirming sustained bullish momentum.

H1 chart:

The H1 chart shows the completion of an initial growth wave to 153.25. The immediate focus is on a further push to 153.33. Upon reaching this local target, a corrective decline to at least 152.43 is likely. Once this correction is complete, the next leg of the uptrend is projected to drive the pair towards 154.33. This scenario is technically confirmed by the Stochastic oscillator, whose signal line is above 50 and trending strongly towards 80, indicating that near-term bullish momentum remains intact.

Conclusion

Fundamentally, the combination of anticipated Japanese fiscal stimulus and a steady BoJ continues to weigh on the yen, while technically, USD/JPY retains a constructive bullish bias. While a short-term correction is expected, the path of least resistance remains to the upside, with key targets at 153.43 and ultimately 154.33.

Nasdaq 100 Analysis: Index Reaches an All-Time High

As the chart shows, trading in the Nasdaq 100 (US Tech 100 mini on FXOpen) opened with a bullish gap today, with the price rising above the 25,600 mark for the first time in history.

The upbeat sentiment is being driven by:

→ expectations of a potential interest rate cut, with the Federal Reserve’s decision due on Wednesday;

→ the upcoming meeting between Chinese and U.S. leaders, where the presidents may announce a new trade agreement;

→ anticipation of quarterly earnings reports from major tech firms – Amazon (AMZN), Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL) and Meta Platforms (META) are all set to release results this week.

Technical Analysis of the Nasdaq 100 Chart

A closer look at the hourly Nasdaq 100 (US Tech 100 mini on FXOpen) chart, within the context of this month’s volatility, shows a steady recovery from the sharp drop on 10 October – the day President Trump suggested imposing 100% tariffs on Chinese goods.

The contours of that sell-off can now be used to outline an ascending channel, which neatly captures the market’s current price swings. Notably, today the index climbed into the upper half of that channel, overcoming resistance levels at:

→ the channel’s median line;

→ the 25,220 mark.

Since last Thursday’s low, the price has advanced by more than 3.5% – a strong rally – forming a steep upward trajectory (highlighted in orange). In this context:

→ the next potential target lies at the upper boundary of the blue channel, which would mark a new record high near 26,000 for the Nasdaq 100;

→ however, with RSI signalling overbought conditions, a short-term correction towards 25,500 would be a healthy development.

Should this week’s key events deliver the optimism investors are hoping for, the bulls may well succeed in reaching those ambitious targets.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.