Sample Category Title

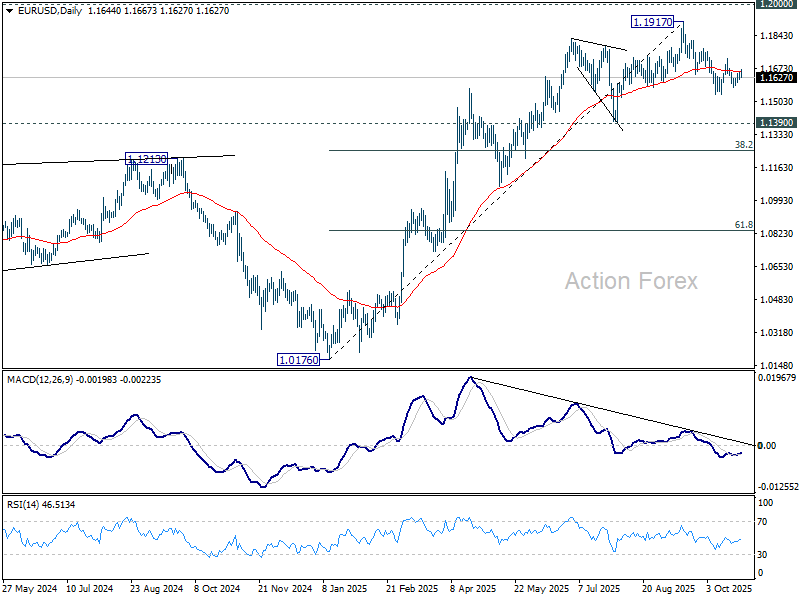

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1625; (P) 1.1638; (R1) 1.1659; More…

Range trading continues in EUR/USD and intraday bias stays neutral. On the downside, below 1.1540 will resume the fall from 1.1917 and target 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1301) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

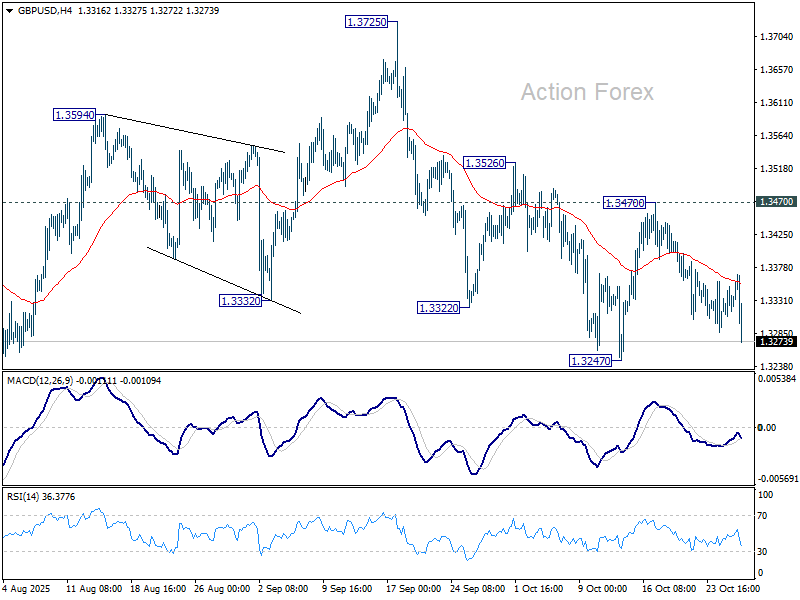

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3314; (P) 1.3333; (R1) 1.3356; More...

GBP/USD dips notably today and focus is now on 1.3247 support. Firm break there will resume whole decline from 1.3725 and target 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, break of 1.3470 resistance will turn bias back to the upside for 1.3526, and then 1.3725/87 resistance zone.

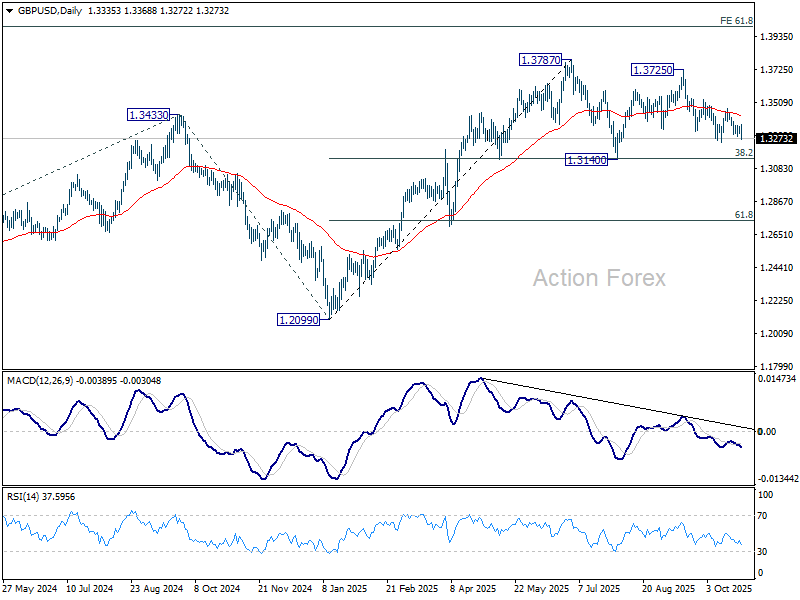

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

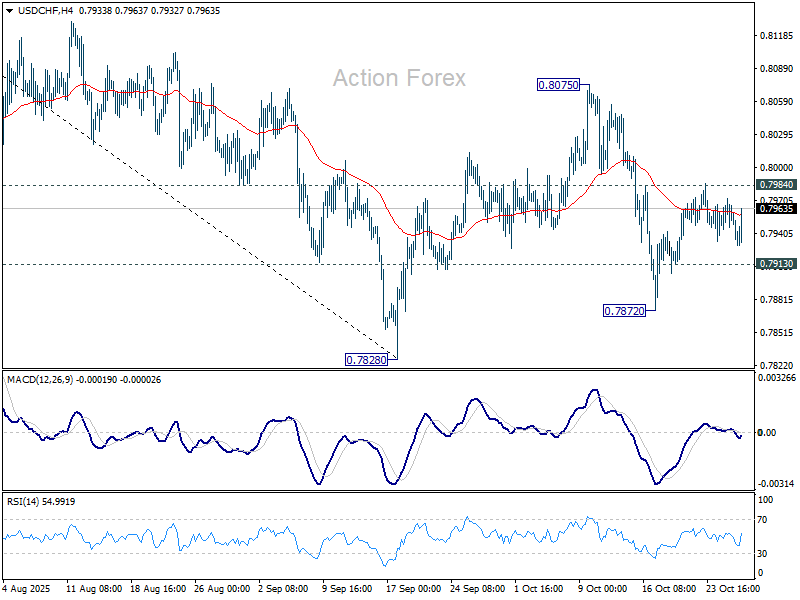

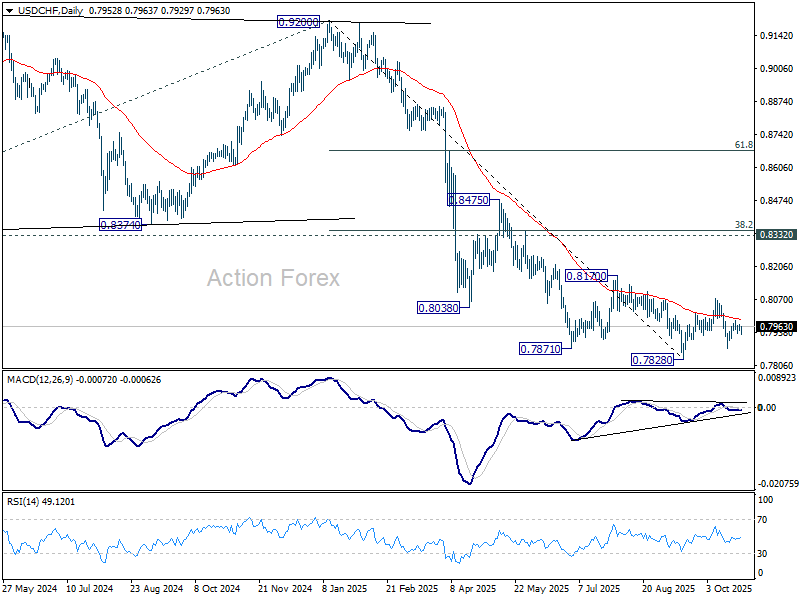

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7942; (P) 0.7957; (R1) 0.7970; More…

USD/CHF is still bounded in range and intraday bias remains neutral. On the downside, below 0.7913 will turn bias to the downside for 0.7872 support, and then 0.7828 low. However, firm break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

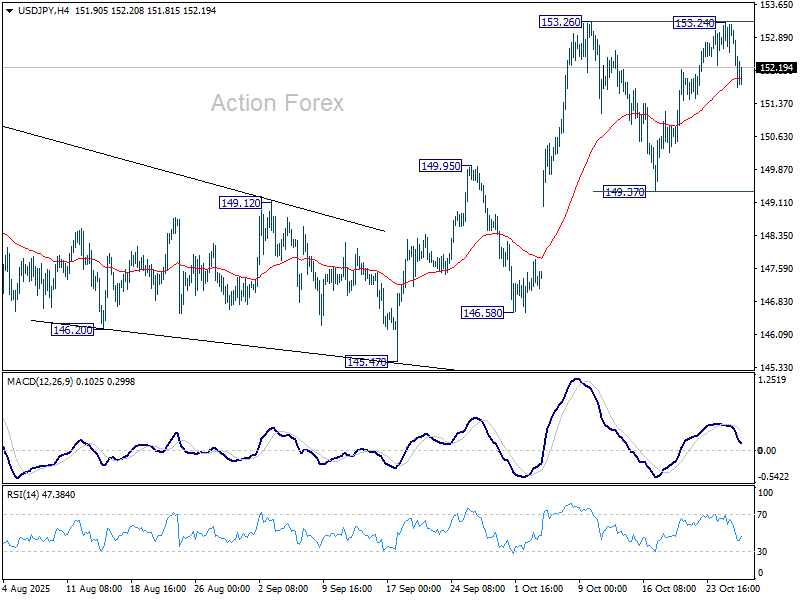

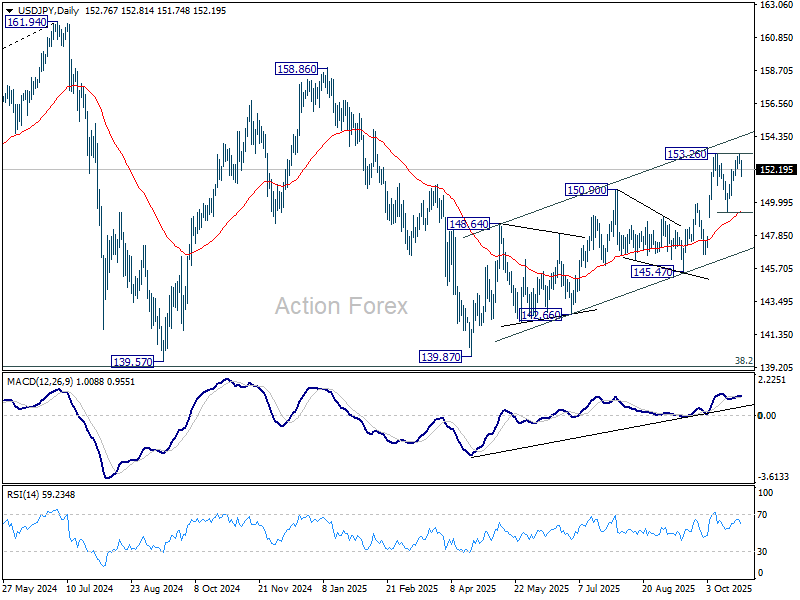

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.54; (P) 152.90; (R1) 153.23; More...

Intraday bias in USD/JPY stays mildly on the downside for the moment. Fall from 153.24 is seen as the third leg of the corrective pattern from 153.26. Sustained trading below 55 4H EMA (now at 151.95) will target 149.37 support next. On the upside, though, break of 153.24 will resume larger rally from 139.87.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

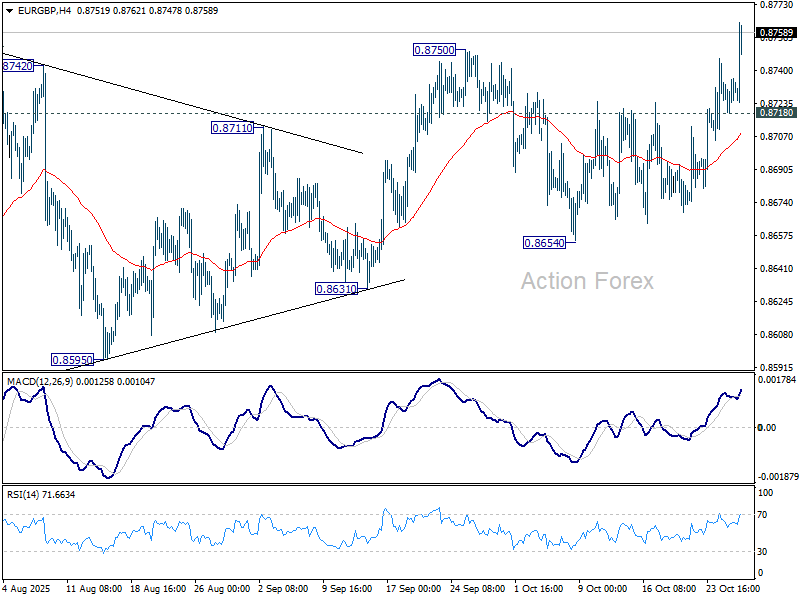

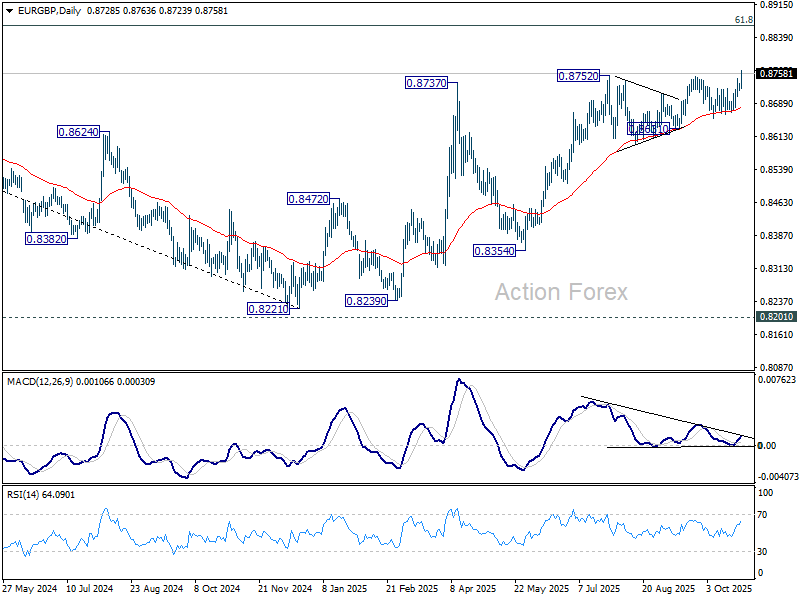

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8729; (R1) 0.8738; More…

EUR/GBP's break of 0.8750 resistance confirms resumption of whole rally from 0.8221. Intraday bias is back on the upside for 0.8867 fibonacci level. On the downside, below 0.8718 minor support will turn intraday bias neutral again first. But near term outlook will now stay bullish as long as 0.8654 support holds, in case of retreat.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).

Sterling Sinks on UK Fiscal Shock; Aussie Steady Ahead of CPI

Sterling tumbled sharply today, hitting its lowest level against Euro in nearly a year as renewed fiscal concerns dominated sentiment. The selloff followed reports from the Financial Times that UK Chancellor Rachel Reeves will face a deeper-than-expected deterioration in the UK’s public finances, delivering an early setback ahead of next month’s crucial Budget.

According to the report, the Office for Budget Responsibility is preparing to slash its long-term productivity growth forecast by 0.3 percentage points, a more severe downgrade than markets had anticipated. The revision reflects persistent weakness in productivity growth since the 2008 financial crisis and would force the Treasury to account for roughly GBP 20–21B in additional borrowing by 2029–30.

The Institute for Fiscal Studies, which provided the underlying calculations cited by the Financial Times, noted that each 0.1-point reduction in productivity growth adds roughly GBP 7B to public borrowing. Markets had previously expected a smaller downgrade of between 0.1 and 0.2 points, implying a fiscal hit closer to GBP 7–14B. The larger revision leaves Chancellor Reeves with far less room for maneuver .

Elsewhere, Aussie traded mixed as risk sentiment cooled ahead of the highly anticipated Q3 CPI report due in the next Asian session. Economists expect headline inflation to rise 1.1% qoq, lifting the annual rate to 3.0% yoy from 2.1%. The trimmed mean CPI—the RBA’s preferred core measure—is forecast to rise 0.8% qoq, keeping the yearly rate steady at 2.7% yoy.

RBA Governor Michele Bullock signaled this week that an upside surprise in core inflation could be a “material miss.” She warned that a 0.9% quarterly increase—just 0.3 percentage points above the RBA’s own forecast—would raise concerns about inflation persistence. Her comments dampened market expectations for near-term rate cuts.

Money markets now assign just a 40% probability of a 25bps cut in November, down sharply from near 60% before Bullock’s remarks and over 80% a week ago. The CPI data will therefore be pivotal in shaping the RBA’s near-term guidance and the path of Australian Dollar into year-end.

In the broader currency space, Aussie remains the week’s top performer, followed by Yen and Kiwi. Sterling sits at the bottom. Dollar and Loonie also trade soft, while Euro and Swiss Franc hold mid-range. The configuration underscores a market leaning toward risk neutrality — cautious on Sterling, patient on the RBA, and positioning ahead of key macro catalysts later in the week.

In Europe, at the time of writing, FTSE is up 0.20%. DAX is down -0.04%. CAC is down -0.07%. UK 10-year yield is down -0.011 at 4.394. Germany 10-year yield is flat at 2.620. Earlier in Asia, Nikkei fell -0.58%. Hong Kong HSI fell -0.33%. China Shanghai SSE fell -0.22%. Singapore Strait Times rose 0.23%. Japan 10-year JGB yield fell -0.035 to 1.640.

ECB survey shows inflation expectations edge lower to 2.7%

The ECB’s September Consumer Expectations Survey showed a modest easing in near-term inflation expectations, with the median outlook for the next 12 months slipping to 2.7% from 2.8%.

Expectations for three years ahead were unchanged at 2.5%, while five-year projections held steady at 2.2%, suggesting longer-term views remain well anchored. Uncertainty around the 12-month outlook also stayed unchanged, indicating little shift in household sentiment.

On the growth side, consumers’ expectations for economic performance over the next year remained negative but stable, holding at –1.2%. The data continue to reflect subdued confidence in the near-term recover.

Unemployment expectations were similarly steady at 10.7% for the 12-month horizon, signaling limited change in labor-market sentiment.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8729; (R1) 0.8738; More…

EUR/GBP's break of 0.8750 resistance confirms resumption of whole rally from 0.8221. Intraday bias is back on the upside for 0.8867 fibonacci level. On the downside, below 0.8718 minor support will turn intraday bias neutral again first. But near term outlook will now stay bullish as long as 0.8654 support holds, in case of retreat.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Considering bearish divergence condition in D MACD, firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).

GOLD (XAUUSD) Elliott Wave: Incomplete Sequences Suggest the Path

Hello fellow traders. In this technical article, we are going to present Elliott Wave charts of GOLD (XAUUSD). In the following sections, we’ll break down the Elliott Wave structure in detail and explain the forecast and present the target levels.

GOLD Elliott Wave 1 Hour Chart 10.28.2025

GOLD has broken the previous low at 4012.3, marked as A red on the chart. This break has made the swing sequences from the 4382.5 peak incomplete, confirming further downside extension. The commodity is potentially forming an Elliott Wave Zigzag pattern, due to the fact that the first leg shows a 5-wave structure. As long as the price holds below the 4163.8 peak, we can continue to expect lower prices within the C red leg, targeting the 3927–3865 area next

GOLD Elliott Wave 1 Hour Chart 10.28.2025

GOLD continued trading lower as expected. The first target area at 3927–3865 has been reached. The main target comes around the 3785 area, where we would like to be buyers again if it gets reached.

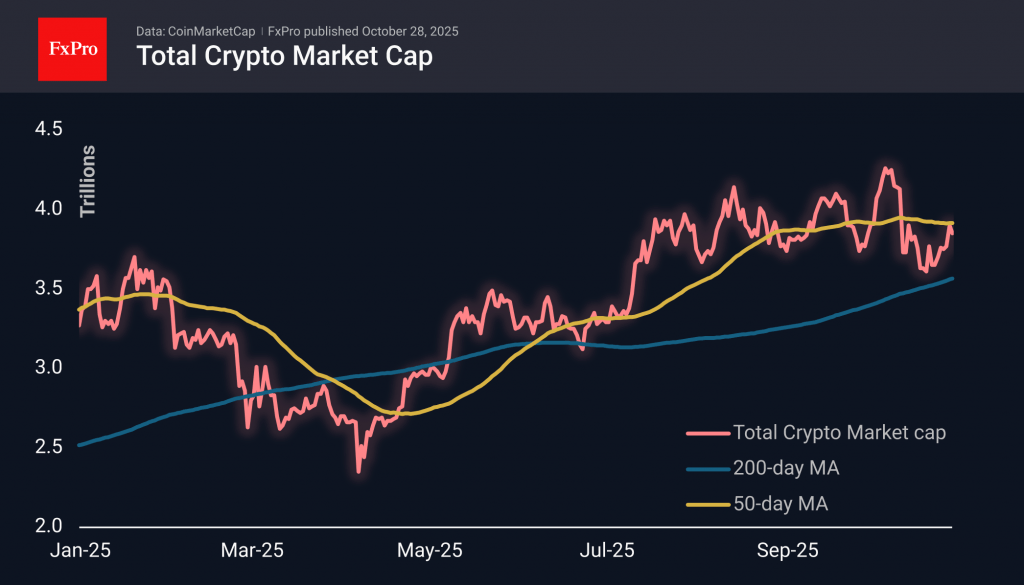

Crypto Market Confused About Who to Follow

Market Overview

The crypto market cap fell by 1.7% to $3.85 trillion in 24 hours. External conditions are a mixture of new highs in stock indices and a rapid sell-off of gold, confusing cryptocurrency investors. The Trump coin is up about 10% daily, likely fuelled by negotiations in Asia. Zcash, among the day’s outsiders, is down 9% but still showing 500% growth over 30 days.

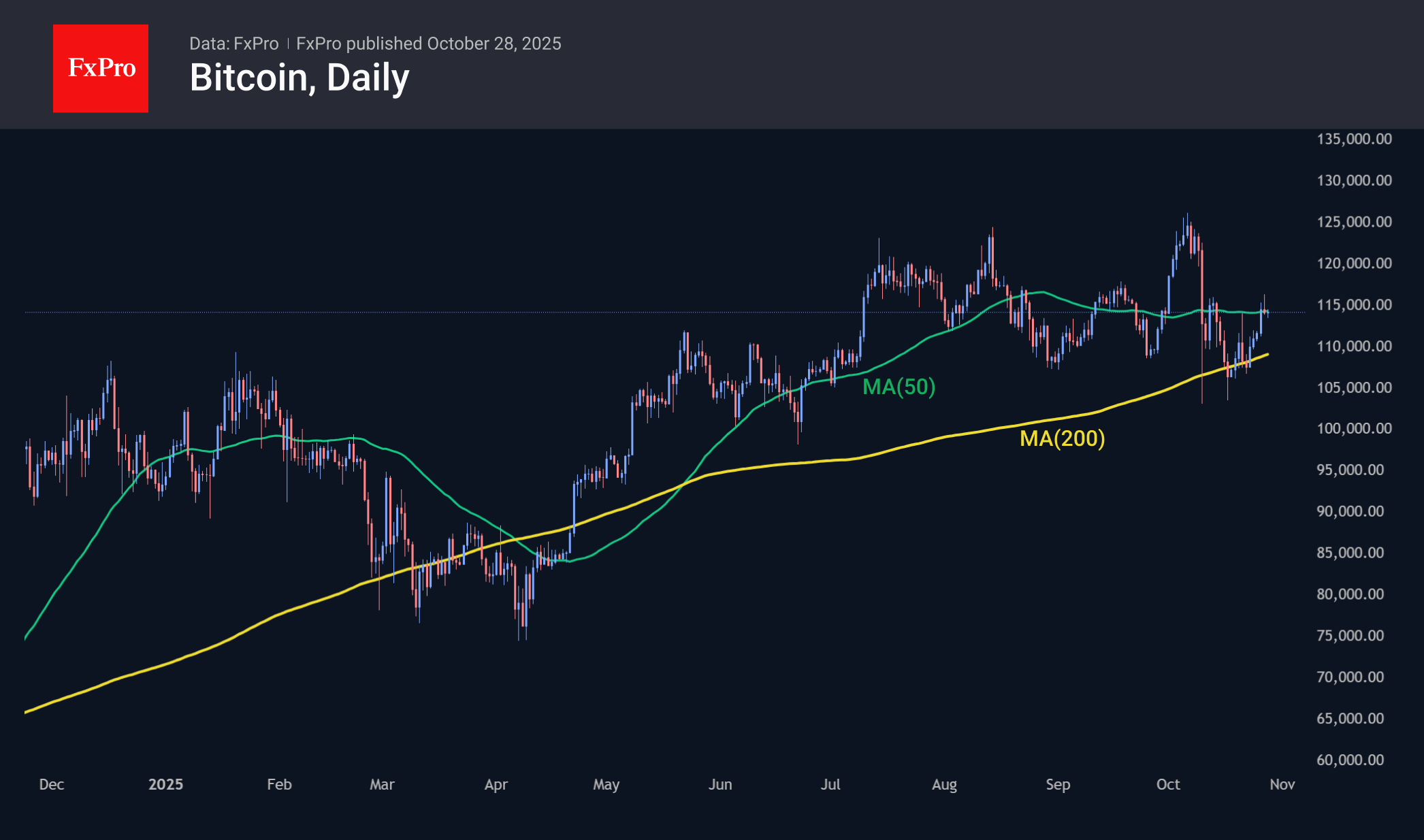

Bitcoin has fallen back to $114K, remaining stuck to the 50-day moving average. At the start of the week, there was an attempt to break out of the range defined by the 50- and 200-day moving averages. The price pullback at the end of Monday does not allow us to declare victory for the bulls. If Bitcoin is still digital gold, this is bad news for buyers.

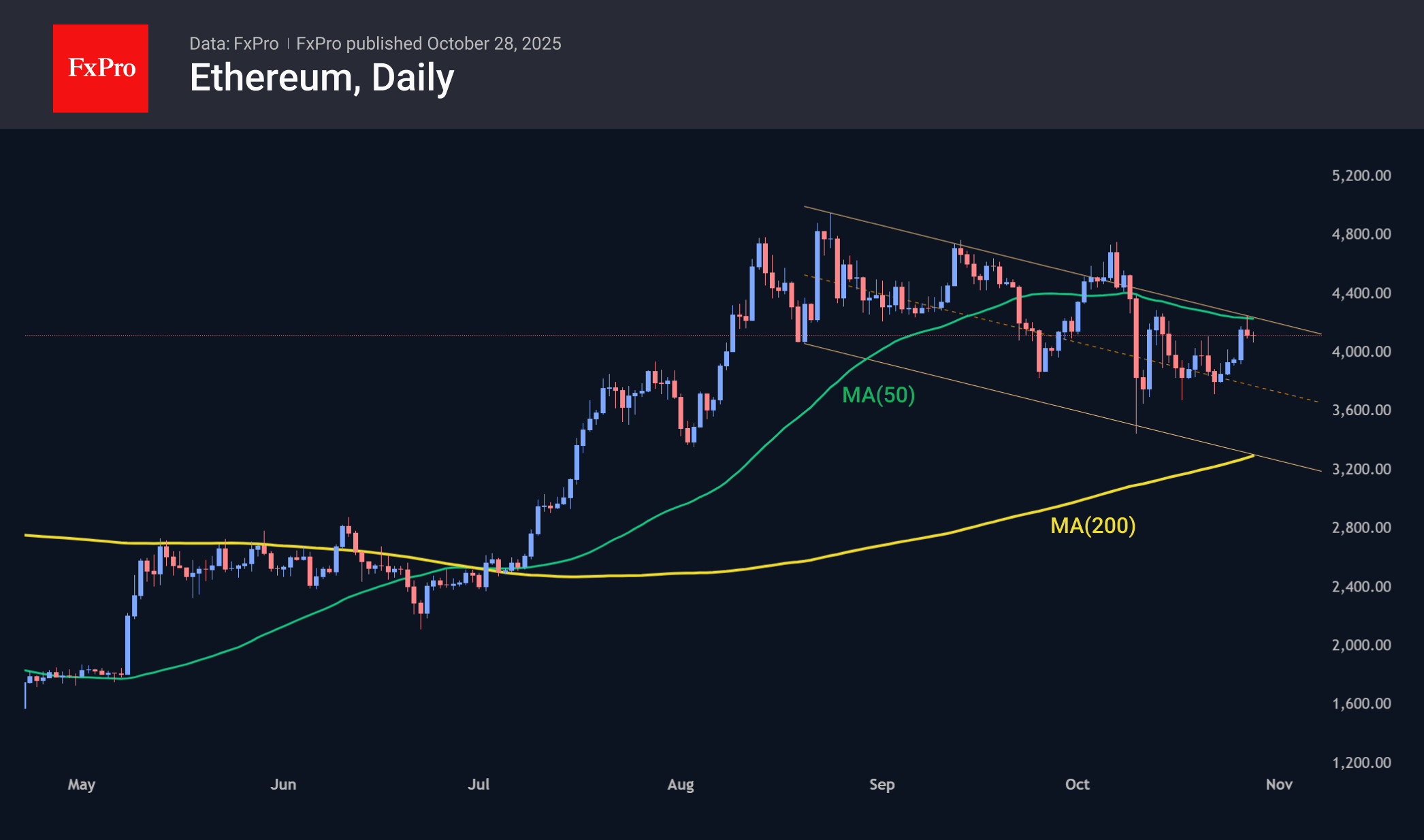

Ethereum is trading near $4,100. Attempts to break above $4,200 and overcome resistance in the form of the 50-day average on Monday were unsuccessful. Since August, ETHUSD has been on a downward trend with lower local lows and highs. We can only discuss a break in this trend after it consolidates above $4,300.

News Background

According to CoinShares, global investment in crypto funds rose by $921 million last week after an outflow the week before. Investments in Bitcoin increased by $931 million, XRP by $84 million, and Solana by $29 million. Investments in Ethereum decreased by $169 million, and Sui by $9 million.

Bitcoin has returned above the short-term holders’ cost basis (STH-Cost Basis), which is a constructive signal for a bull market, according to Checkonchain.

Since mid-October, long-term investors have withdrawn about 62,000 BTC from their wallets. The growth in market supply could hinder Bitcoin’s rally in the absence of intense demand, according to Glassnode.

BitMine increased its reserves to 3.3 million ETH, buying 77,055 ETH over the past week. BitMine’s total cryptocurrency reserves reached $14.2 billion.

Strategy bought 390 BTC over the past week. The company now has 640,808 BTC on its balance sheet, with a total value of $47.44 billion at an average purchase price of $74,032.

The bankrupt crypto exchange Mt.Gox has postponed the deadline for payments to creditors from 31 October 2025 to 31 October 2026. This is the third postponement of payments, which were initially planned to be completed by 31 October 2023.

Gold Extends Its Decline Below the $4,000 Level

As the chart shows, the XAU/USD quote has fallen below $3,945 today — its lowest level since 6 October. The downward momentum is being driven by traders’ caution ahead of two key events:

→ the U.S. Federal Reserve’s upcoming interest rate decision;

→ the meeting between U.S. and Chinese leaders, which could help ease tensions between the world’s two largest economies.

Technical Analysis of the XAU/USD Chart

The ascending channel (shown in blue) illustrates gold’s remarkable rally from the 20 August low (point A):

→ throughout September, the median line acted as strong support;

→ the peak at point B coincided with the upper boundary of the channel;

→ the QH line — dividing the upper half into quarters — alternated between resistance and support.

The black lines mark the consolidation zone observed between 21 and 27 October:

→ its lower boundary aligns with the median;

→ the shape resembles a Symmetrical Triangle pattern, which has since been broken to the downside.

The chart highlights the confidence of sellers — bears managed to push prices through the key support area defined by:

→ the psychological $4,000 level;

→ the 0.382 Fibonacci retracement (indicated by the orange arrow).

The next potential target for the ongoing decline lies near the QL line, which coincides with the round-number level of $3,900. However, this may only serve as a temporary barrier before bears attempt to drive the price lower — towards the bottom boundary of the primary channel.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Rebounds to 4,000 USD Mark

Gold prices returned to the 4,000 USD per troy ounce mark on Tuesday, partially recovering from the previous day's 3.2% decline. The initial sell-off was triggered by encouraging developments in US-China trade negotiations.

According to officials, the two sides reached a framework agreement on tariffs and several key issues during talks in Malaysia. This paves the way for a final approval by the US and Chinese leaders at their upcoming meeting in South Korea later this week.

The metal found renewed support as investor attention shifted to the impending US Federal Reserve meeting. Markets are now pricing in a 25 basis point rate cut following the release of softer-than-anticipated inflation data, making this one of the most significant events in a week packed with risk.

Technical Analysis: XAU/USD

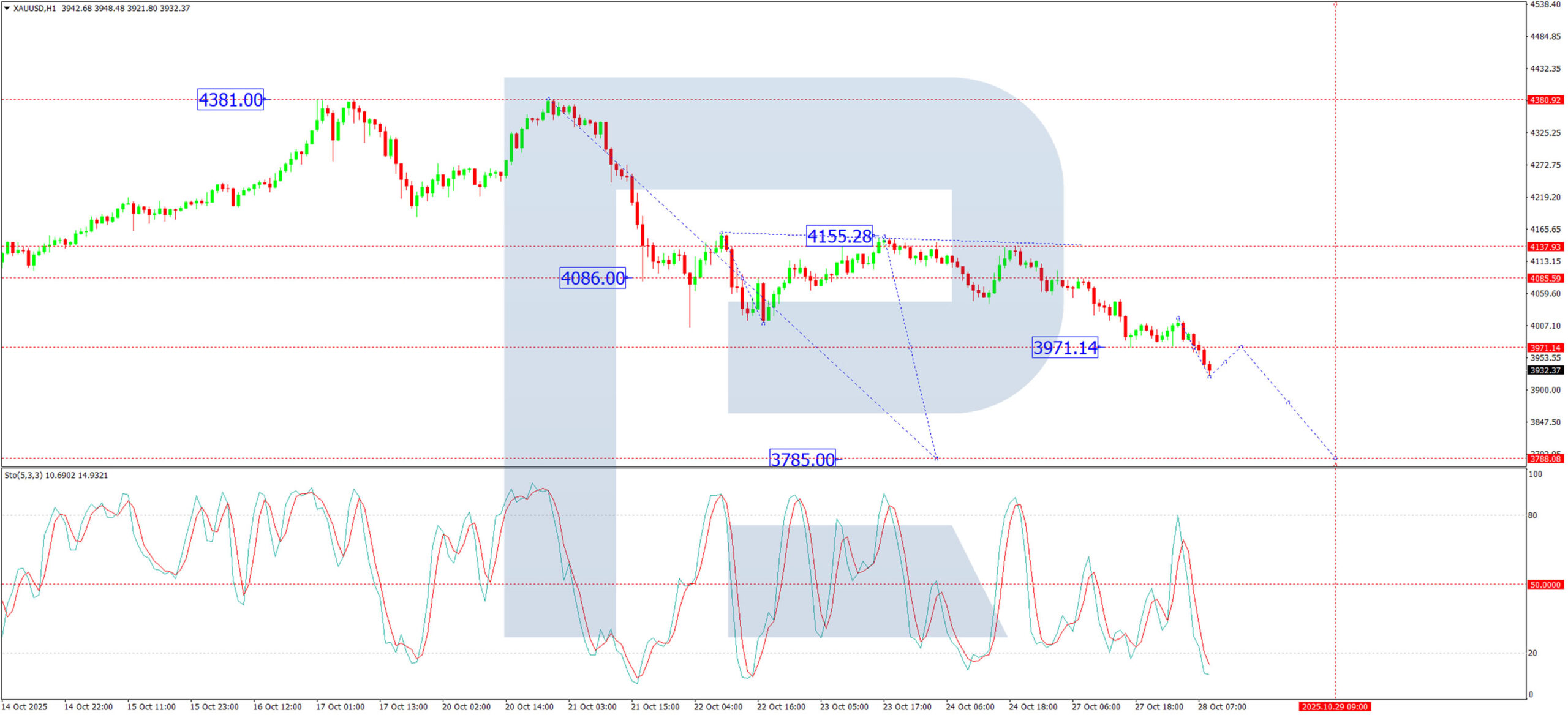

H4 Chart:

On the H4 chart, XAU/USD formed a consolidation range around 4,085 USD before breaking decisively to the downside. The market appears to be developing the second leg of this downward wave, with a subsequent target projected at 3,785 USD. This bearish near-term outlook is supported by the MACD indicator. Its signal line is pointing downward, and the histogram has moved into negative territory, suggesting the corrective phase is not yet complete.

H1 Chart:

On the H1 chart, the pair is developing a downward structure toward 3,785 USD. A consolidation range has formed around 3,971 USD; a break below this level would signal a continuation of the decline toward the stated target. The Stochastic oscillator confirms this momentum, with its signal line positioned below 50 and trending downward toward 20, reflecting strengthening selling pressure.

Conclusion

While gold has rebounded on shifting expectations for Fed policy, the technical structure points to further potential downside. The primary focus for traders will be the Fed's decision, which will determine whether this current correction extends toward 3,785 USD or if the longer-term bullish trend can reassert itself.