Sample Category Title

FI and FX Markets Zooming in on Fed Tonight.

Markets

US president Trump is considering to cut a punitive 20% tariff over Chinese fentanyl exports to 10%. The rumour reported yesterday and confirmed by the man himself this morning encouraged the bulls and supported US stocks towards new record highs (again). The Nasdaq outperformed by eking out a 0.8% gain. The fentanyl tariff will be one of the topics presidents Trump and Xi will discuss during their meeting tomorrow. Add to the list: Nvidia’s state-of-the-art “super-duper” Blackwell chips. Trump in overnight comments said he’s open to providing China with access to it as part of a trade deal in what would be a major U turn by POTUS. China in turn is said to have bought the first US soybean cargoes in months in return as a sweetener ahead of the meeting. Everything is set for another risk-on vibe across markets today. European futures pare losses. Wall Street (though early to tell) is set for a higher open. The US dollar snaps a 5-day losing streak against the euro (EUR/USD 1.163). AUD outperforms (see below). The pound remains in the defensive after an already disastrous day yesterday. Multiple technical support zones broke, pushing EUR/GBP currently to its highest level since May 2023 just shy of 0.88. The trigger was BRC October price data showing that food inflation dropped the most since December 2020, stripping the hawks at the Bank of England from key arguments not to lower rates. The market implied probability for a BoE rate cut next week rises to 35%.

Today’s a big day for all corners in the market. Several European countries including Spain and Belgium release Q3 GDP numbers. Equities are eyeballing day one of after-market earnings from big tech including Alphabet, Meta and Microsoft. They are followed by Amazon and Apple tomorrow and, carrying around a quarter of the S&P500’s weight, could be crucial in entertaining the current risk rally. FI and FX markets are zooming in on the Fed tonight. A 25 bps rate cut is all but certain. Investors are keen to spot hints for future moves but we’re not sure whether chair Powell is in a position to give them since there’s virtually no official data rolling in. That could temper the market reaction. We don’t expect him to actively push back against markets pricing an additional move in December though. The end to QT could steal the rate cut’s thunder instead. Powell announced it two weeks ago at the NABE conference amid commercial bank reserves at the central bank dwindling to below $3tn. That’s less than 10% of GDP Fed Waller suggested as a minimum some years ago. That ballpark figure was based on the liquidity squeeze in 2019 which saw a spike in the short-term SOFR interbank rate. The level of bank reserves back then had dropped below 8% of GDP. The SOFR in recent days climbed back above the Fed’s upper bound rate again, potentially signaling growing liquidity pressures. We expect the chair to be queried about it. The current roll-off cap for Treasuries stands at $5bn per month, a limited amount anyway. MBS’s are capped at $35bn but the monthly amount in practice is often lower.

News & Views

Australian inflation quickened more than expected in Q3, rising by 1.3% Q/Q (up from +0.7% in Q2 & vs +1.1% consensus). It was the fastest quarterly pace since Q1 2023. The main contributors to the quarterly rise were housing (+2.5%), recreation and culture (+1.9%) and transport (+1.2%). The rise in electricity costs (+9%) was a significant contributor to the growth in housing inflation. Annual inflation (compared with Q3 2024) hit its highest level since Q2 2024 at 3.2% (up from 2.1% vs 3% expected). A monthly CPI report moreover pointed at an accelerating intra-quarter dynamic with inflation rising from 3% Y/Y in August to 3.5%. Stripping out for the biggest quarterly price swings, the trimmed mean CPI measure accelerated more than thought as well, from 0.7% Q/Q to 1% Q/Q and from 2.7% Y/Y to 3% Y/Y. Other details showed annual food inflation rising by 3.1% Y/Y in Q3, annual goods inflation going from 1.1% Y/Y to 3% Y/Y and annual services inflation hitting 3.5% Y/Y (from 3.3%). Today’s inflation numbers help convince markets that more RBA rate cuts are no foregone option. RBA governor Bullock recently also pushed back against the idea. The market implied probability of a 25 bps rate cut before year-end dropped from 91% just a week ago to currently 21%. The positive trade vibe between the US and China is the other thing at play. The AUD swap rate curve bear flattens with yields rising by 4.3 bps (30-yr) to 11.2 bps (2-yr). The Aussie dollar benefits, extending this week’s rally to currently AUD/USD 0.66.

Japanese consumer confidence rose from 35.3 to 35.8 in October (vs 35.5 consensus), the highest level since December 2024. Details showed a broad-based improvement with metrics like the overall livelihood, expectations for income growth and employment and willingness to purchase durable goods all hitting multi-month best levels.

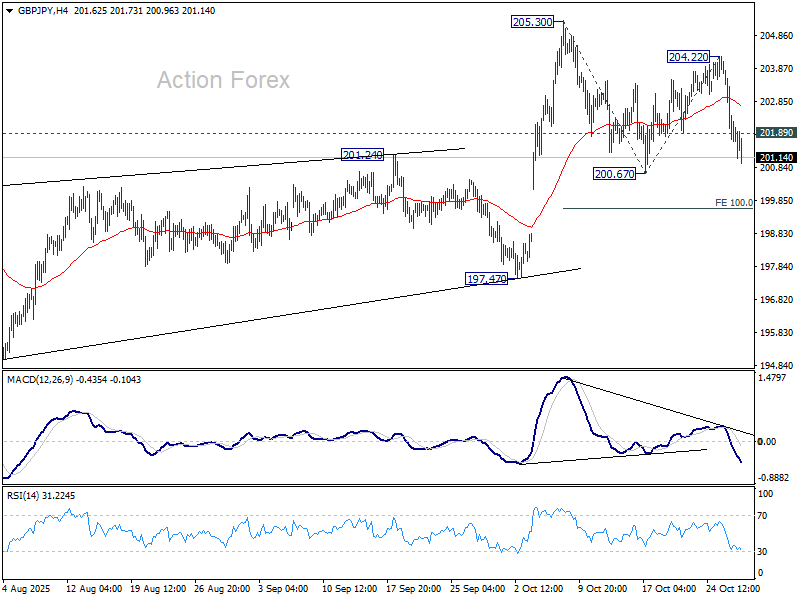

GBP/JPY Daily Outlook

Daily Pivots: (S1) 201.06; (P) 202.54; (R1) 203.41; More...

GBP/JPY's break of 201/89 minor support suggests that rebound from 200.67 has completed. Intraday bias is back on the downside for 200.67. Firm break there will resume whole fall from 205.30, and target 100% projection of 205.30 to 200.67 from 204.22 at 199.59. For now, risk will stay on the downside as long as 204.22 resistance holds, in case of recovery.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 197.47 support will dampen this view and extend the corrective pattern with another fall.

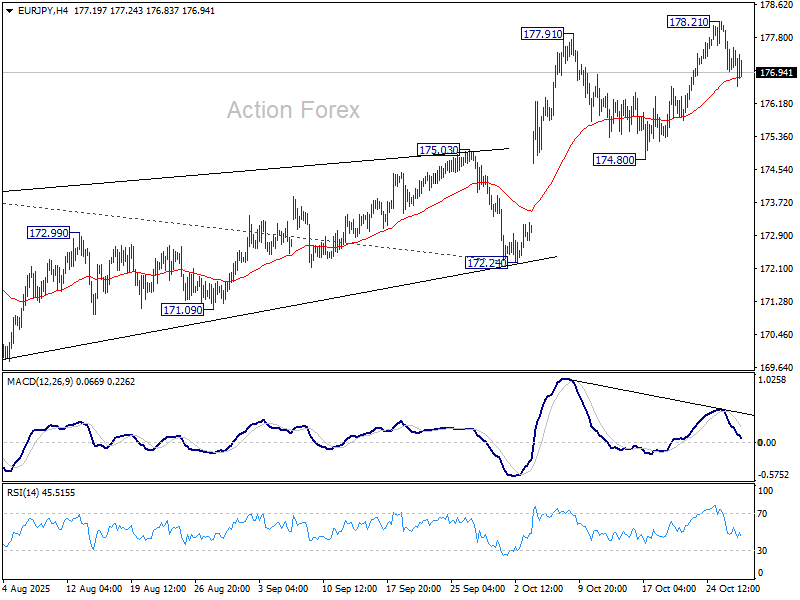

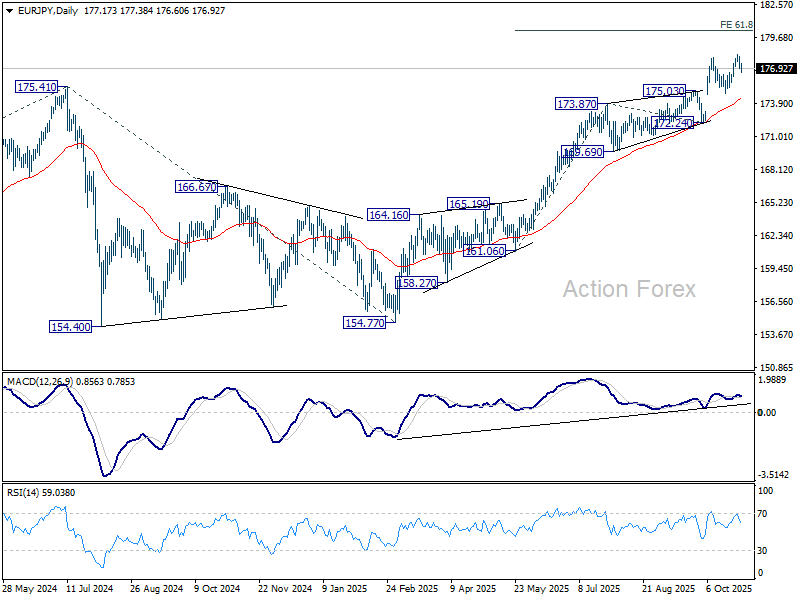

EUR/JPY Daily Outlook

Daily Pivots: (S1) 176.81; (P) 177.44; (R1) 177.89; More...

Intraday bias in EUR/JPY remains neutral and more consolidations could be seen below 178.21. Downside should be contained well above 174.80 to bring another rally. On the upside, break of 178.21 will resume larger up trend to 61.8% projection of 161.06 to 173.87 from 172.24 at 180.15 next.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Firm break of 172.24 support will suggests that it has turned into consolidations again. But still, outlook will continue to stay bullish as long as 55 W EMA (now at 167.87) holds, even in case of deep pullback.

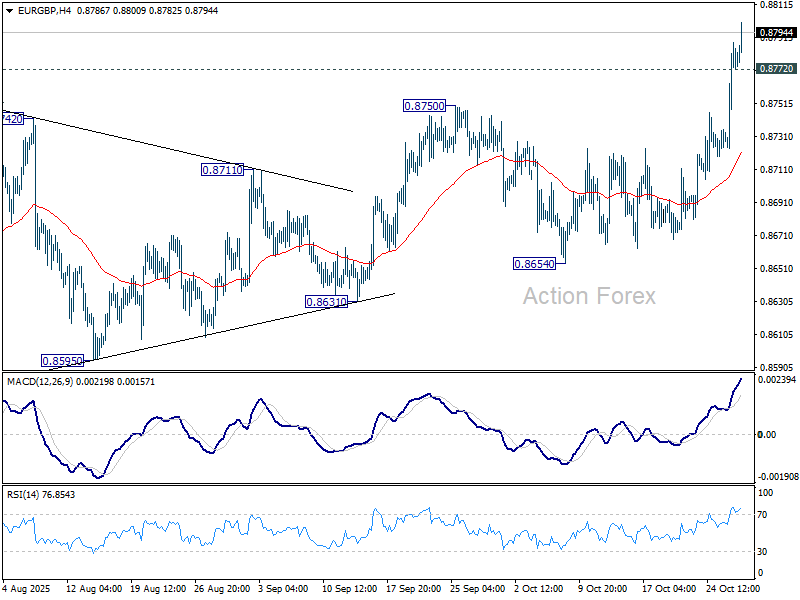

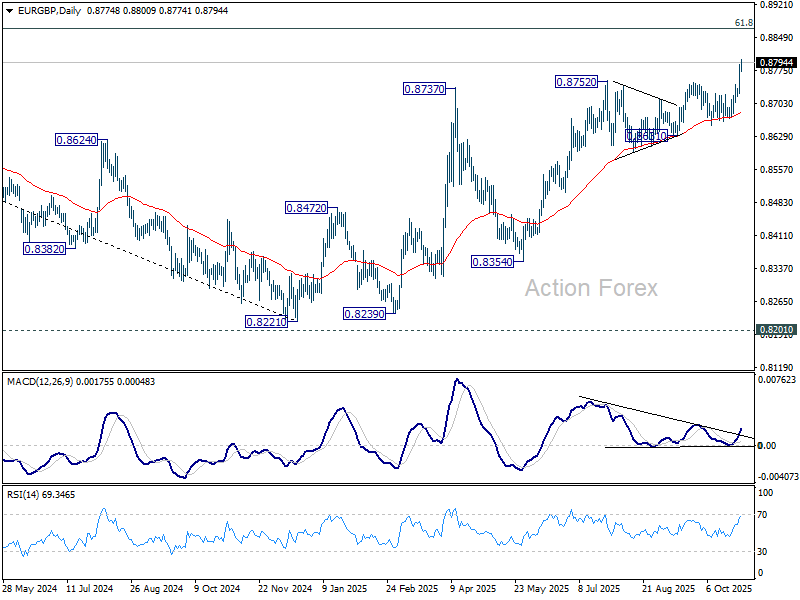

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8737; (P) 0.8764; (R1) 0.8804; More…

EUR/GBP's rally accelerates higher today and intraday bias stays on the upside for 0.8867 fibonacci level. On the downside, below 0.8718 minor support will turn intraday bias neutral again first. But near term outlook will now stay bullish as long as 0.8654 support holds, in case of retreat.

In the bigger picture, rise from 0.8221 medium term bottom is seen as a corrective move. While further rally cannot be ruled out, upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Firm break of 0.8654 support will be the first sign that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high).

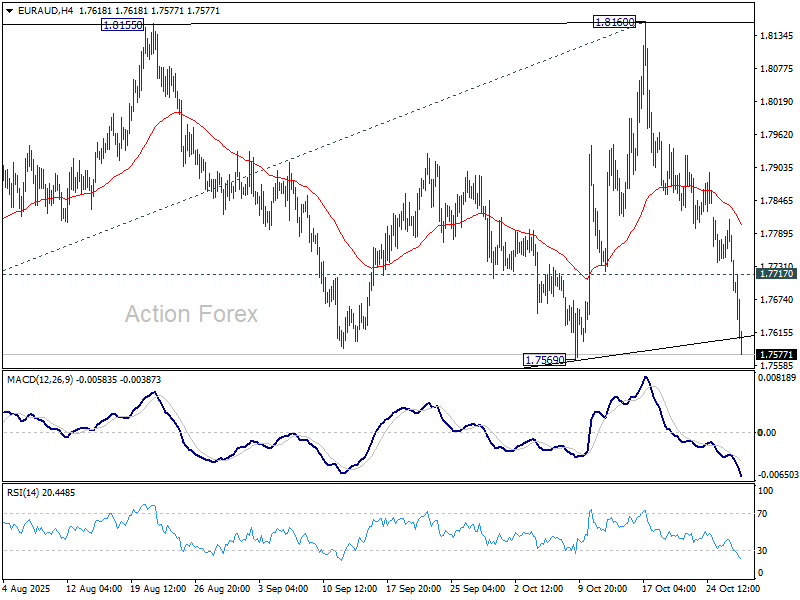

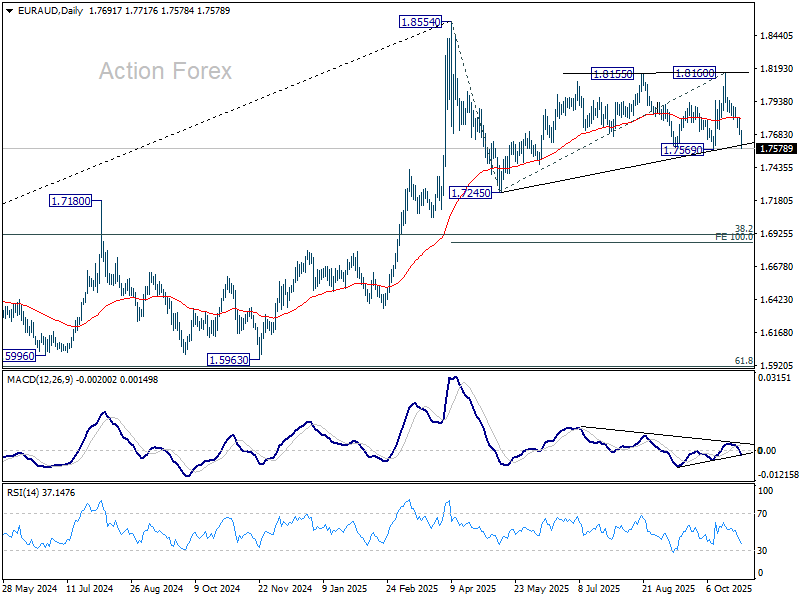

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7654; (P) 1.7734; (R1) 1.7777; More...

EUR/AUD's fall from 1.8160 accelerates lower today and intraday bias remains on the downside. Firm break of 1.7569 support will confirm that pattern from 1.8554 already in its third leg, and target 1.7245 next. On the upside, above 1.7717 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound form 55 W EMA will likely bring resumption of the up trend sooner.

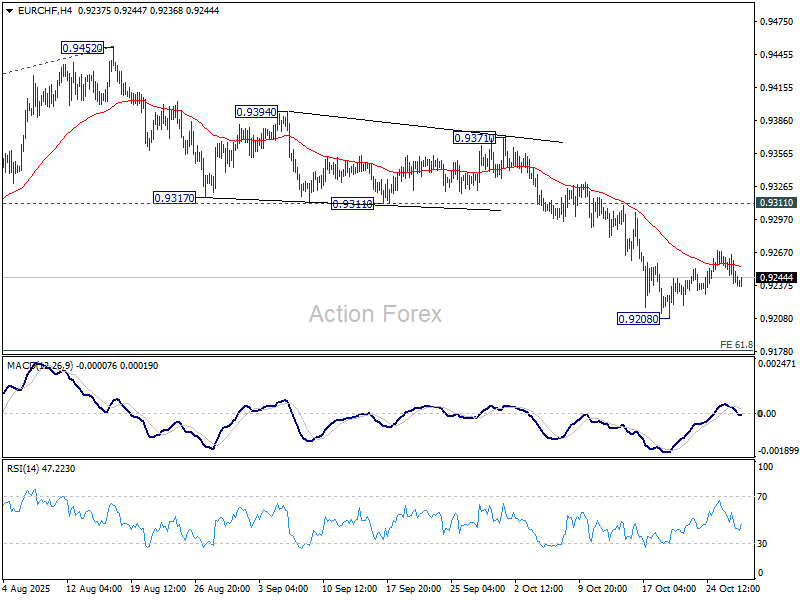

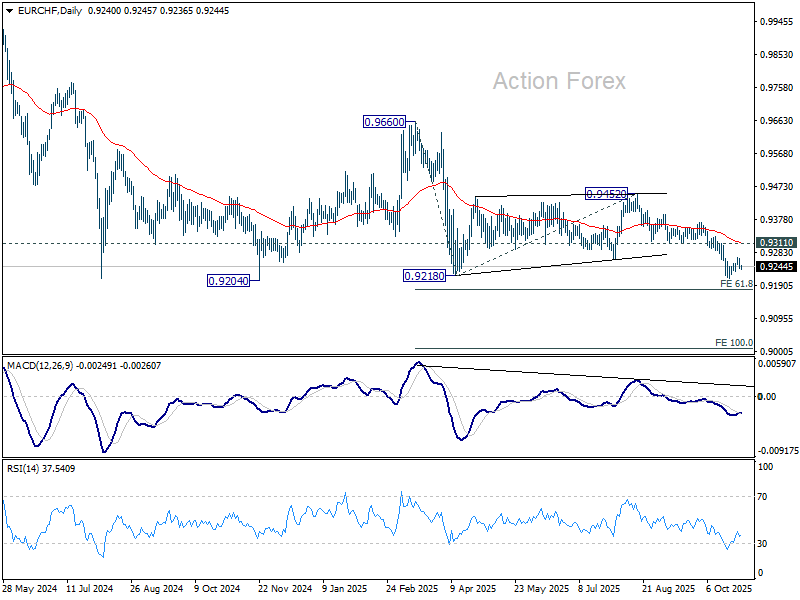

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9235; (P) 0.9252; (R1) 0.9263; More....

Intraday bias in EUR/CHF remains neutral and more consolidations could still be seen above 0.9208 support. Upside should be limited below 0.9311 support turned resistance. On the downside, break of 0.9204/8 will confirm larger down trend resumption. Next target is 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179. Firm break there will target 100% projection at 0.9010.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9385). Firm break of 0.9204 will resume the whole down trend from 1.2004 (2018 high). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming.

FOMC Meeting Takes Centre Stage

In focus today

The main event today will be the FOMC's rate decision, where we and the broad market consensus expect a 25bp cut. With no new projections, all eyes will be on Powell's forward guidance, which we expect to remain vague. While markets price in a high likelihood of another cut in December, we do not expect the Fed to pre-commit at this stage. We expect the Fed to end QT for US Treasury holdings but continue QT for MBS. Read more in Reading the Markets USD, 28 October. Note that in Europe, the rate decision comes one hour earlier than usual (19CET/20EET) due to the US daylight savings time.

In Norway, private consumption has seen a solid uplift this year, as expected given high real wage growth, low unemployment and some tailwind from lower mortgage rates. Fundamentals should continue to support private consumption, but current data suggests a moderate decline of around 0.3% in September.

In Sweden, the GDP-indicator for September and Q3 should, as usual, be interpreted with caution. Consensus expectations for Q3 stand at +0.7% q/q and +1.6% y/y. Following an improvement in Q2, the economy appears to be trending upward after a long period of sideways development.

Overnight, US President Trump and Chinese President Xi are set to meet on the sidelines of the APEC Summit in South Korea. The agenda is packed, given recent escalations including China's export controls on rare earths and Trump's tariff threats. We expect the two leaders to strike a deal to ease tensions, however, failure to reach an agreement could trigger a negative reaction in risk markets.

Overnight, the Bank of Japan (BoJ) meets to decide on the next steps in policy normalisation. With Abenomics loyalist Sanae Takaichi now leading the government and recent spending and wage data showing weakness, we expect the BoJ to take a cautious stance and leave the policy rate unchanged. However, we still see solid arguments for further tightening and anticipate a potential rate hike at the December meeting.

Economic and market news

What happened yesterday

In the euro area, the ECB's Bank Lending Survey showed a slight, unexpected tightening of credit standards for firms in Q3 due to higher risk perceptions. Firm loan demand remains weak, while household demand grew strongly. Overall, the survey supports the view that monetary easing policies are still feeding through to bank lending, but the pace of transmission appears slower, with broadly stable loan demand and a slight tightening of supply.

In the US, consumer confidence improved modestly in October, rising to 94.6 (cons: 93.2). The report was mixed, with a slight improvement in the assessment of the current situation, though consumer confidence remains on a declining trend overall. Future expectations continued to weaken, reflecting persistent uncertainty.

In China's more detailed communiqué on its upcoming 2026-2030 Five-Year Plan, the focus is on boosting consumption and shifting to a domestic demand-driven economy. Compared to the initial communiqué, which used softer language, this update signals a stronger emphasis on consumption as a key driver of economic growth.

In Sweden, the Riksbank Business Survey showed a weaker-than-expected assessment of the current economic situation and outlook for Sweden. Pricing plans have dropped sharply, but the impact of the upcoming VAT cut on food remains unclear. Here, it will be interesting to see the NIER survey on Thursday, which is more granular on a sector level.

Equities: Equities were slightly higher yesterday on the surface, however beneath that we saw that the "only" reason for a green day was due to Mag7 (up about 1.3%). Otherwise, it was day with sour risk sentiment. Only 21% of the S&P500 ended with a positive return yesterday yet it ended 0.23% up. Thus, if we exclude the Mag7, the S&P493 was down -0.6%. Looking at the tech index, it was a semi-conductor driven rally, not least also due to Nvidia's Jensen Huang dismissing concerns over an AI bubble and also Nvidia broadening its scope with them taking a USD1bn equity stake in Nokia. Russel2000 was down 0.6%, with Dow Jones up 0.3% and Nasdaq 0.8%. Stoxx 600 down -0.2%. Overnight, the sentiment continued in Asia. The indices are up (Nikkei +1.9% and Shenzen +0.5%), but largely focused on tech.

FI and FX: EUR/USD continues to trade in the mid-1.16-1.17 range, moving towards 1.1630 overnight, as markets await today's FOMC meeting. A 25bp cut looks all but certain, with attention shifting to whether the Fed signals an end to QT and to Powell's tone at the press conference. Fixed income markets were in wait-and-see mode yesterday with European and US yields ending the day broadly unchanged. EUR/SEK continues to trade in the lower end of the long-held 10.90-11-10 range, but we continue to favour the upside tactically in EUR/SEK. Similarly, we maintain our bullish EUR/NOK view.

Who Needs Data When Nvidia is Out Announcing Deals?

At yesterday’s GTC conference, Nvidia CEO Jensen Huang unveiled a fresh round of partnerships with Nokia, Palantir, Uber, and the US Department of Energy.

Nvidia will team up with the DoE to build seven AI supercomputers — meaning a lot of chips heading to the government.

Nvidia also plans to invest $1 billion in Nokia to help transform the Finnish networking company into an AI-driven firm. Nokia, in turn, will use Nvidia chips to accelerate its 5G and 6G software development, while Nvidia will explore Nokia’s data-center strategy for its own AI infrastructure. There’s some circularity in the arrangement, but also tangible revenue potential for both companies — and investors liked what they heard: Nokia shares jumped 24%, hitting their highest level since 2010.

Nvidia also announced a collaboration with Palantir on government and industrial AI applications and customizable AI agents. According to reports, Nvidia has already booked around $500 billion worth of Blackwell and Rubin chip sales for 2025–26, and further deals with Samsung and Hyundai are expected later this week.

No surprise then that Jensen Huang insists there’s no bubble in sight. Nvidia shares soared 5%, passing the $200 mark for the first time. The S&P 500 edged to another all-time high, led by tech, while the Nasdaq 100 rose 0.74% — also supported by a 2% gain in Microsoft after it reportedly received a 27% ownership stake in OpenAI, positioning the AI startup to transition into a for-profit company.

So, you heard it — move on, there’s no bubble to see here!

Big Tech earnings remain in the center stage today with Microsoft, Meta and Alphabet reporting Q3 results after the bell. At current price levels and valuations, there’s little room for missteps — whether on earnings, spending plans or guidance. Skeptics have been calling for a broad sell-off for at least more than a year, arguing that AI revenues aren’t growing fast enough. That day may eventually come, but for three years running, Big Tech has consistently met and beaten expectations. And given the scale of deals and capex we’re seeing, it’s hard to swim against the tide — at least in Nvidia’s case. Whether AI investments generate revenue immediately or not, Big Tech has the cash to spend on Nvidia’s chips. And they are spending.

One minor setback came from ASM International, whose Q3 orders missed expectations due to weaker demand from major clients including TSMC, Intel, and Samsung. But will that discourage AI bulls from buying more? Hardly.

Of course, AI needs energy, and nuclear has re-emerged as the form of clean power best suited to meet those needs — since solar and wind can’t run the machines 24/7. Big Tech and the US government are now rolling out nuclear partnerships almost daily. The Global X Uranium ETF jumped another 8% yesterday, reaching its highest level since 2011 — a parabolic move that mirrors AI’s own hunger for energy.

And if anything, yesterday’s rally could still get a bit of sugar coating if the Federal Reserve (Fed) sounds sufficiently dovish later today. In the absence of fresh data, policymakers are effectively acting half-blind, but the market widely expects a 25-basis-point rate cut and possibly an end to quantitative tightening (QT), as much of the pandemic-era liquidity has now evaporated. Some even expect the Fed to announce an immediate end to QT today — which would certainly lift market sentiment: the more liquidity, the more fuel for assets. And with roughly $7.5 trillion parked in US money market funds, lower rates could push investors toward riskier corners of the market.

The US dollar remains under pressure. Although it was slightly better bid in Asia, a dovish Fed statement could renew selling. Still, the downside looks limited for the greenback, given how unappealing the major alternatives currently are:

- Japanese yen: Little appetite amid talk of a softer Bank of Japan (BoJ) stance, which could push the USDJPY toward the 155–160 range by year-end.

- Euro: Confidence remains shaky amid ongoing French political turmoil and fears of another government collapse.

- Sterling: Investors are cautious ahead of the Autumn Budget, and yesterday’s BRC inflation report showed the sharpest drop in food prices since the pandemic, largely due to falling sugar prices — a boost for Bank of England (BoE) doves.

So, the dollar’s stabilization — despite a looming US government shutdown — owes more to a lack of alternatives than genuine demand. A dovish Fed could change that today, though any rebound in major peers will likely be limited and may even present opportunities to fade rallies against the dollar, given how much Fed dovishness is already priced in.

As for gold, its recent slide could find support near $3’800 per ounce, just above the 23.6% Fibonacci retracement of its two-year rally.

So I’ll leave it here for today — and let Powell and the earnings do the talking for the rest of the day.

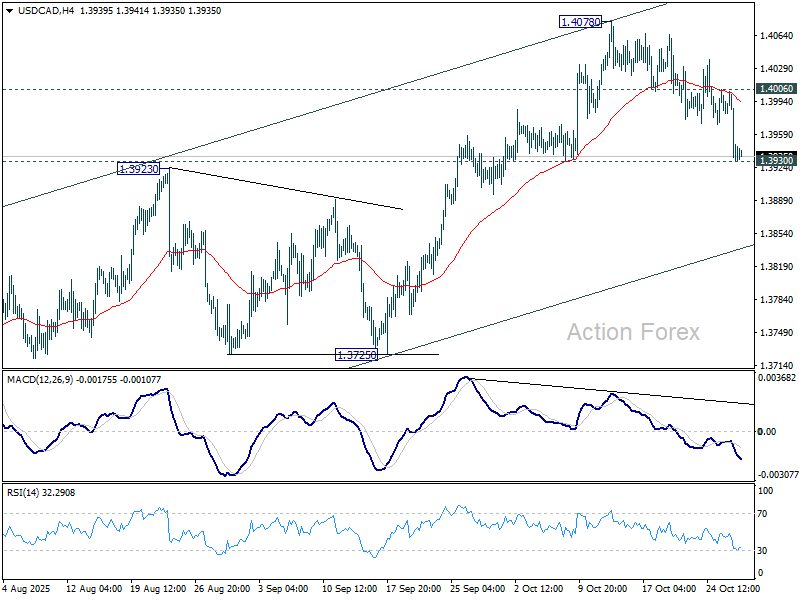

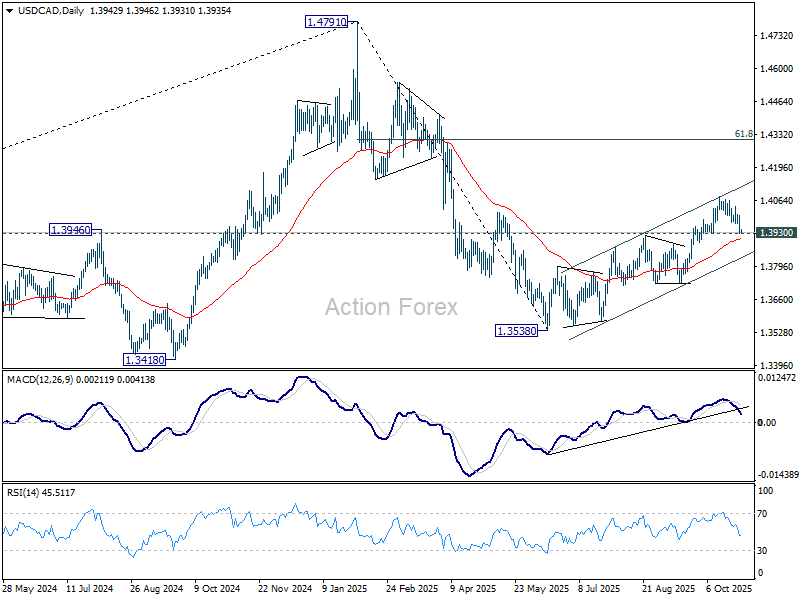

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3918; (P) 1.3962; (R1) 1.3989; More...

USD/CAD's fall from 1.4078 accelerated lower, but it's still staying above 1.3930 support. Intraday bias remains neutral first. On the upside, break of 1.4006 will indicate that the pullback has completed. Intraday bias will be back on the upside for 1.4078 and above to resume the rally from 1.3538. However, decisive break of 1.3930 will be the first sign of bearish reversal, and bring deeper fall to channel support (now at 1.3835).

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds.

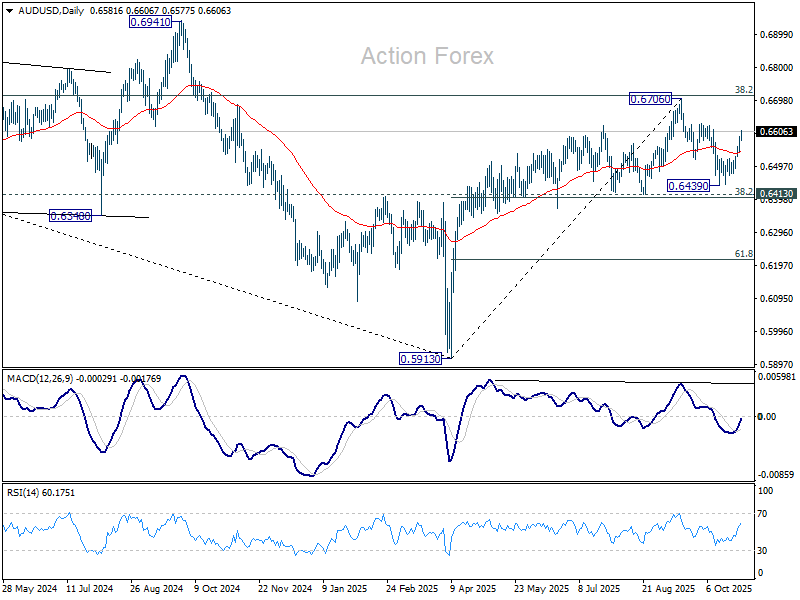

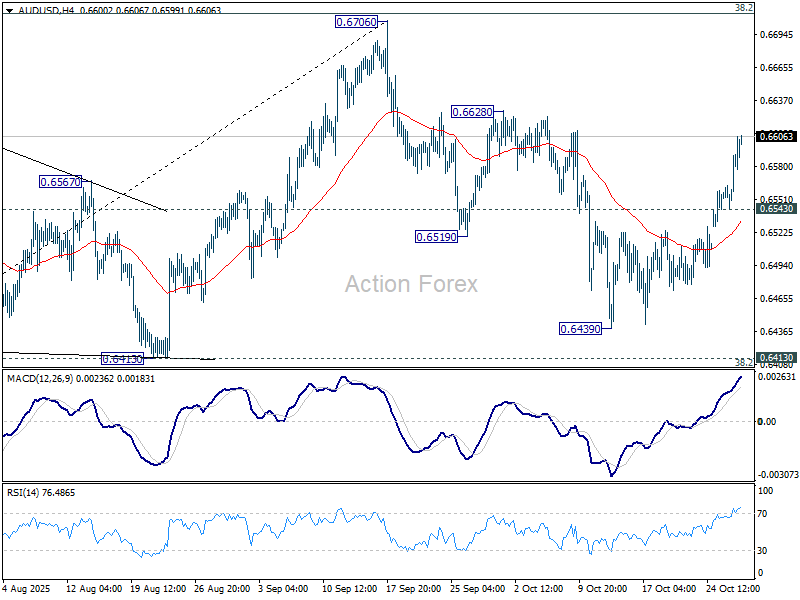

AUD/USD Daily Report

Daily Pivots: (S1) 0.6556; (P) 0.6574; (R1) 0.6602; More...

Intraday bias in AUD/USD remains on the upside at this point. As noted before, corrective fall from 0.6706 should have completed with three waves to 0.6439. Further rise should be seen to retest 0.6706 high next. On the downside, below 0.6543 minor support will turn intraday bias neutral first.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.