Sample Category Title

EUR/GBP: Hits Highest in Over Two Years as Shift in BoE Policy Expectations

EUR/GBP hit new 2025 high and held at the highest levels since May 2023 on Wednesday.

Steep upleg from Oct 22 extends into sixth straight day, as sterling came under increased pressure from shift in monetary policy expectations which sees BoE rate cut as early as November (the MPC meets next week).

The latest economic data showed that inflation held steady last month, earnings grew at the slowest pace in almost three years, and unemployment ticked higher, setting stage for policy easing, against previous forecasts for no rate cuts this year.

Growing UK budget concerns also add to Pound’s recent weak performance.

Firmly bullish daily studies support the action, though overbought stochastic and RSI touching the borderline of overbought territory, warning that bulls might be losing traction that contributes to scenario of profit taking after strong rally.

Overall picture remains bullish and suggests that limited dips would be positioning for fresh push higher.

Former tops /trendline at 0.8750/40 and rising 10DMA / broken Fibo 61.8% (0.8700 zone) offer solid supports which should ideally contain dips.

Res: 0.8817; 0.8835; 0.8875; 0.8900.

Sup: 0.8750; 0.8700; 0.8650; 0.8631.

GBP/USD: Extends Steep Decline on Growing Expectations for BoE Rate Cut

Cable hit three-month low on Wednesday, extending the steep bear-leg which emerged after strong upside rejection at daily cloud, into second consecutive week.

Fresh bears broke through important support provided by 200DMA (1.3239) and cracked 1.3200 level that unmasks key short-term support at 1.3141 (Aug 1 low (Fibo 38.2% of 1.2999/1.3788).

Today’s break of former low of Oct 14 (1.3248) generated another bearish continuation signal (continuation of larger downtrend from Sep 17 peak (1.3725).

Bears need close below 200DMA to open way towards 1.3141 pivot, break of which to complete bearish failure swing pattern on weekly chart and signal potential deeper correction of 1.2999/1.3788 (January – June uptrend) and expose psychological 1.30 support.

The notion is supported by daily MA’s now in full bearish configuration and strong negative momentum, from the technical perspective, while shift in fundamentals (growing expectations for BoE rate cut this year against previous forecasts for staying on hold until the end of the year) also contributes bearish near- term stance.

Broken 200DMA reverted to initial resistance, followed by session high / falling 5DMA (1.3280/85), which should ideally cap potential upticks and guard 10DMA (1.3342).

Res: 1.3239; 1.3280; 1.3300; 1.3342.

Sup: 1.3162; 1.3141; 1.3100; 1.3000.

BoC Warns of Structural Economic Damage from Tariffs

The Bank of Canada delivered an expected 25 basis point rate cut today, lowering the overnight rate to 2.25%—the bottom of the neutral range that would not add to or subtract from inflation pressures over time.

Beyond the rate cut itself, two themes stood out from today's announcement. First, the Bank adopted a clear holding bias, stating that "Governing Council sees the current policy rate at about the right level" assuming future economic and inflation data evolve largely in line with current projections.

Second, the Bank emphasized concerns about structural economic damage from trade disruptions, reducing the effectiveness of monetary policy as a tool in addressing weakening demand while maintaining inflation control.

Overall, our base case assumes no further rate reductions, as we expect a ramp up in fiscal stimulus (with more details to come in the federal budget next week) will do the bulk of the heavy lifting in the policy response to address tariff-related, concentrated economic weakness.

The BoC’s latest baseline economy projections are in line with ours

The BoC’s guidance that the overnight rate is not expected to be reduced further is contingent on the economic outlook evolving in line with their base case projections that were the first since January. The Bank had resorted to scenario analysis in April and July due to volatile U.S. trade policy.

The Bank's overarching assumption behind the projections is that current tariff measures will remain in place. Key estimates regarding these measures—including a roughly 6% average effective tariff rate imposed by the U.S. on Canadian exports, with the majority of exports remaining exempt due to CUSMA compliance—align directly with our own analysis.

As a result, there is substantial alignment between our forecasts and the central bank's outlook. Both anticipate slow but positive growth in the Canadian economy through the second half of this year, followed by moderate acceleration in 2026 as trade related uncertainty starts to fade.

Headline inflation is expected to remain close to the 2% target over the forecast horizon. However, we see upside risks to this baseline projection primarily from robust domestic demand, given household spending that has broadly held on to resilience to-date and expectation that weakening in the labour market could be drawing to an end.

The Bank of Canada anticipates upside risks mainly from trade-related factors, such as larger-than-expected cost increases from tariffs or sudden reductions in sectoral tariffs.

It see downside risks to the inflation projections from softer than expected domestic demand, or a sudden tightening in global financial conditions sparked by a correction in AI related stock market valuations that have been tied to resilient growth in the U.S. economy this year.

BoC expects lasting structural damage to the economy from the trade shock

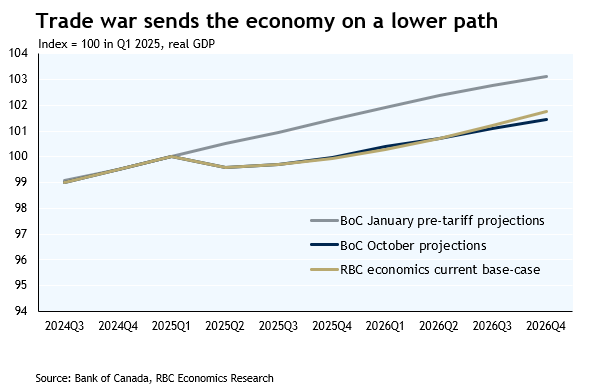

Beyond this cycle, the Bank of Canada expects structural damage from ongoing trade disruptions. Combined with slower population growth, Canada's potential output is expected to expand at a reduced rate of 1.6% in 2025 and 1.0% in 2026, before recovering slightly to 1.3% in 2027.

This structural damage will reduce the productive capacity of the Canadian economy and erode the effectiveness of monetary policy. In simple terms, as the economy's capacity shrinks, it will become increasingly difficult for the Bank of Canada to lower interest rates to stimulate demand without risking that demand will exceed what the economy can produce, thereby causing inflation.

This highlights the urgency for fiscal policy to step up by helping expand the economy's capacity limits—a priority we expect will account for the bulk of new spending to be announced at the fall budget update on November 4.

Sunset Market Commentary

Markets

The record rally on stock markets is once again name of the game today as US president Trump continues his Asian tour. He made a deal with South Korean president Lee where $150bn in shipbuilding investment and another $200bn earmarked for other investments amongst others are matched by the US capping tariff goods at 15%. Ahead of the European bell, more bilateral commitments between the US and China had already been announced including lower fentanyl-related tariffs and the first Chinese bulk buying of soybeans this season. We approach the big moment with the planned 3-hour meeting between presidents Trump and Xi Jinping at 3am CET (tonight) after which Trump takes the Air Force One back home following a busy Asian tour. Also in the US/China-mix: the export of Nvidia chips. The company rallies to a record-breaking $5tn valuation today and lifts AI spirits in the run-up to Q3 earnings releases starting tonight with Alphabet, Meta and Microsoft. The Nasdaq currently adds 0.66%, making it a weekly gain of more than 5%.

A second “risk management” 25 bps rate cut by the Fed is all but certain tonight. For now, the narrative stands that downside employment risks are building faster than upside inflation risks. Lack of US eco data might mean lack of Fed guidance for December and could temper the market reaction. We don’t expect Powell to actively push back against markets pricing an additional move in December though. The end to QT could steal the rate cut’s thunder instead. Powell announced it two weeks ago at the NABE conference amid commercial bank reserves at the central bank dwindling to below $3tn. That’s less than 10% of GDP Fed Waller suggested as a minimum some years ago. That ballpark figure was based on the liquidity squeeze in 2019 which saw a spike in the short-term SOFR interbank rate. The level of bank reserves back then had dropped below 8% of GDP. The SOFR (and other general collateral rates for that matter) in recent days climbed back above the Fed’s upper bound rate again. Apart from this week’s huge t-bill supply, it potentially suggests that we’re moving from a situation of abundant liquidity to an ample one. We expect the chair to be queried about it. The current roll-off cap for Treasuries stands at $5bn per month, a limited amount anyway. MBS’s are capped at $35bn but the monthly amount in practice is often lower.

Sterling suffers more losses after yesterday’s technical break beyond EUR/GBP 0.8768/69. Apart from rising BoE rate cut bets, there’s the approaching 2026 Budget deadline (one month away). Today, UK PM Starmer refused to rule out raising income tax, national insurance or VAT hinting at a break of the election manifesto promises which could significantly weigh on UK growth.

News & Views

The Bank of Canada lowered its policy rate to 2.25% from 2.5%. Today’s decision comes with the resumption of baseline growth and inflation forecasts instead of a scenario analysis. GDP should grow by 1.2% this year, followed by 1.1% and 1.6% in 2026 and 2027. The BoC expects a weak 2025H2 to be followed by a recovery from next year on. Canada’s labour market is considered soft with job losses building in trade-sensitive sectors and weak hiring elsewhere. Inflation was 2.4% in September, slightly higher than the BoC had anticipated. Its preferred measures of core inflation had been sticky around 3% but alternative gauges suggested underlying inflation remains around 2.5%. Inflationary pressures should ease in the months ahead, allowing CPI to remain near 2% over the policy horizon. The current policy rate level is said to be “about the right level to keep inflation close to 2% while helping the economy”, suggesting a pause or perhaps the end to the easing cycle, provided the BoC’s forecasts more or less materialize. That’s supporting Canadian swap yields (+3.6-5 bps) and the Canadian dollar. USD/CAD drops to 1.39.

Swedish GDP grew a consensus-smashing 1.1% q/q in Q3 of this year. The accompanying monthly series showed the dynamic easing towards the end of the quarter with September GDP falling marginally by 0.1% m/m. But that comes after a huge boost in August (+1.2% m/m) and doesn’t change the notion of Sweden’s economic recovery finally taking hold. GDP since September 2022 never grew faster than 0.2% and even declined in five out of the 12 quarters. The annual print improved from 0.9% to 2.4%, the best outcome in three years. The numbers should comfort the Riksbank. The central bank last month cut the policy rate to 1.75%. It referred to growth being weak “for a long time” and had to push forward the timing of a recovery multiple times. It wasn’t planning on cutting rates much (if any) further though and today’s release adds to that conviction. The SEK strengthens to EUR/SEK 10.89.

Bank of Canada Cuts Rates, Maybe for the Last Time

The Bank of Canada (BoC) cut its policy rate to 2.25%, in line with market expectations.

The decision was accompanied by an updated forecast, the first since January as “the effects of US trade actions on economic growth and inflation” are “somewhat clearer”. The bank now expects the economy will grow by 1.2% in 2025, 1.1% in 2026 and 1.6% in 2027. These figures are very similar to our forecast.

The Bank expects that inflation will moderate in the coming months and that CPI inflation will “remain near 2% over the projection horizon.” Notably, the emphasis on underlying inflation remains and that it is holding “around 2.5%”.

Looking forward, should the economy and inflation evolve as expected “Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment”. Of course, they leave room to respond should circumstances change.

Key Implications

The outlook shows a gradual uptake of excess capacity and inflation stabilizing, a scenario that would suggest no more easing is required. However, despite the effects of the trade shock being better understood, the outlook is replete with uncertainty – not least because CUSMA negotiations are set to ramp up next year. Stabilization at 2.25% is our base case on where the policy rate will hold, but we acknowledge that risks abound.

The Bank is now at the bottom end of their estimated neutral range, and a pause is reasonable. While trade represents a downside risk to the outlook, the upcoming federal budget could well represent the upside risk. PM Carney is expected to chart out a vision for the economy to offset some of the structural change the Bank is unable to address. The structure and timing of potential outlays could materially affect the medium-term outlook for the economy, and the Bank’s decision making.

Canadian Dollar Jumps as BoC Declares Policy ‘About Right’ After Cut

Canadian Dollar climbed after the BoC lowered its overnight rate to 2.25% and signaled that policy is likely now at its terminal level. The bank’s statement that rates are “about the right level” if the outlook unfolds as expected was interpreted as a clear end-of-cycle message. The message was subtle but decisive: the bar for additional easing is now much higher.

That stance gave the Loonie a lift, even as the currency’s gains were eclipsed by Aussie, which remains the day's star performer. Stronger-than-expected CPI report earlier today led some analysts to abandon expectations of further RBA cuts, while some analysts now speculate that the next policy move could even be upward if price pressures persist. Kiwi also joined the rally, supported by robust risk appetite.

At the weaker end, Sterling extended its sell-off amid lingering fiscal concerns tied to next month’s budget and a deteriorating U.K. fiscal outlook. The Swiss Franc and Euro also traded lower. Dollar and Yen were positioned mid-range ahead of Fed decision.

Attention now turns to the Fed, which is widely expected to cut rates by 25 bps to 3.75–4.00%. Futures continue to price in about a 90% chance of another cut in December, meaning that unless Fed Chair Jerome Powell explicitly pushes back, markets are unlikely to adjust much. Opinions on the 2026 policy path remain highly divided, not least because of uncertainty surrounding Powell’s successor. Until a decision is made and fresh data are available, markets are unlikely to get a clear picture of where rates may stand in 2026.

On the trade front, US President Donald Trump told business leaders at the APEC Summit he was confident of striking a “good deal” with President Xi Jinping at their Thursday meeting—the first since Trump’s second-term tariff offensive began. Officials say the deal could include deferring China’s export controls on rare earth minerals and scrapping the planned 100% U.S. tariff on Chinese goods, as well as renewed agricultural purchases. That optimism has helped propel U.S. indexes to record highs this week, a rally that now depends on both leaders delivering on expectations.

In Europe, at the time of writing, FTSE is up 0.64%. DAX is down -0.27%. CAC is down -0.30%. UK 10-year yield is down -0.01 at 4.395. Earlier in Asia, Nikkei rose 2.17%. Hong Kong was on holiday. China Shanghai SSE rose 0.70%. Singapore Strait Times fell -0.23%. Japan 10-year JGB yield rose 0.015 to 1.654.

BoC cuts to 2.25%, signals end of easing Cycle

BoC delivered a widely expected 25bps rate cut, lowering its overnight rate to 2.25%, but signaled that this could mark the end of its current easing cycle. The central bank said that if inflation and economic activity evolve in line with its October projection, the current policy rate is “about the right level” to balance supporting growth with keeping inflation close to target. That phrasing was interpreted as indicating that 2.25% is the likely terminal rate, barring major economic shocks.

In its accompanying statement, the BoC acknowledged that U.S. trade actions and uncertainty are having “severe effects” on key export-oriented industries. As a result, the Bank expects GDP growth to remain weak in the second half of the year before recovering gradually through 2026. The economy is projected to expand 1.2% in 2025, 1.1% in 2026, and 1.6% in 2027, with excess capacity expected to be absorbed only slowly.

The BoC described the labour market as soft, with job declines concentrated in trade-sensitive sectors, while hiring across the broader economy remains subdued.

On inflation, the BoC noted that headline CPI stood at 2.4% in September, slightly above expectations, while its preferred core measures remain sticky around 3%. Broader alternative indicators suggest underlying inflation near 2.5%, but the BoC expects price pressures to ease gradually and headline CPI to remain close to 2% over the projection horizon.

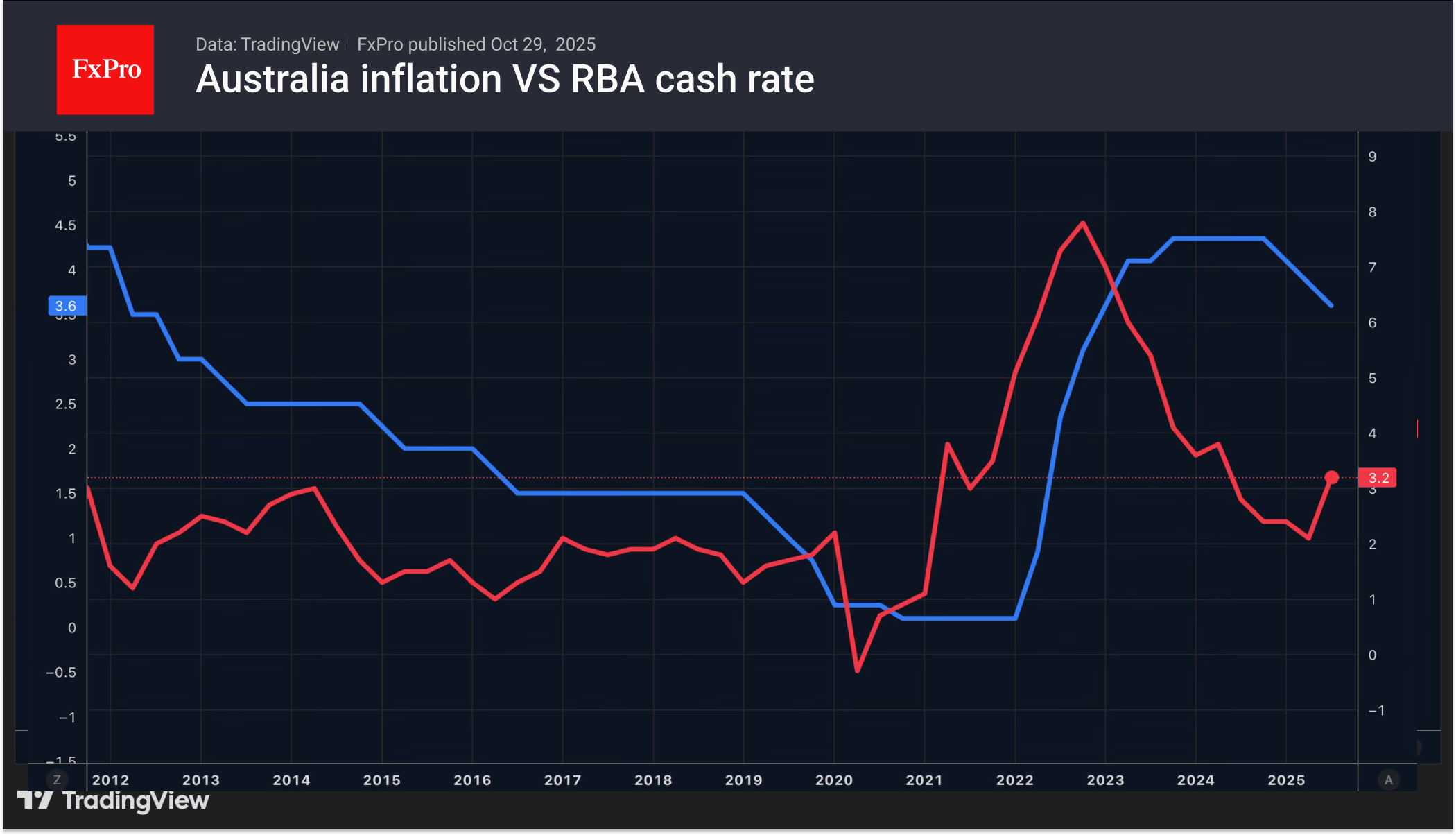

Australia inflation shock: CPI surges to 3.2%, core re-accelerates

Australia’s inflation surprised sharply to the upside in Q3, reigniting concerns that price pressures are proving stickier than expected. Headline CPI jumped 1.3% qoq, accelerating from 0.7% in Q2 and beating expectations of 1.1% — marking the strongest quarterly increase since Q1 2023. The Australian Bureau of Statistics said the largest contributor was a 9.0% rise in electricity costs, which alone drove much of the headline surge.

On an annual basis, CPI rose to 3.2% yoy, sharply higher than the previous 2.1% yoy and above forecasts of 3.0%. That marks the fastest pace of annual inflation since Q2 2024. Electricity costs were again the main driver, soaring 23.6% from a year earlier despite targeted government relief measures.

Core inflation was equally strong. Trimmed mean CPI — the RBA’s preferred measure — rose 1.0% qoq, up from 0.7% and above expectations of 0.8%. Annually, core inflation accelerated to 3.0% yoy from 2.7%, underlining persistent price pressures across utilities and essential services, exceeding the RBA’s 2–3% target range again. This marks the first uptick in the trimmed mean since Q4 2022, confirming that underlying price momentum remains firm.

The data strengthen the case for the RBA to delay or even reconsider rate-cut expectations for the near term.

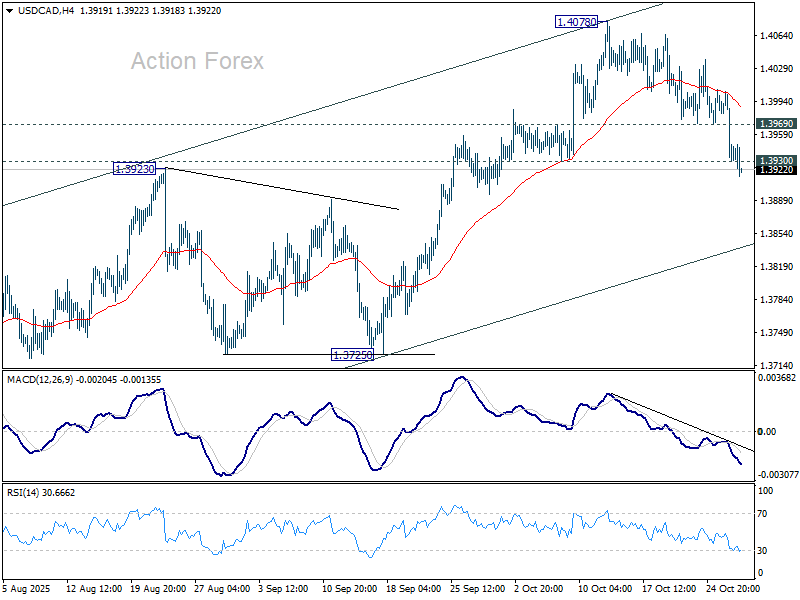

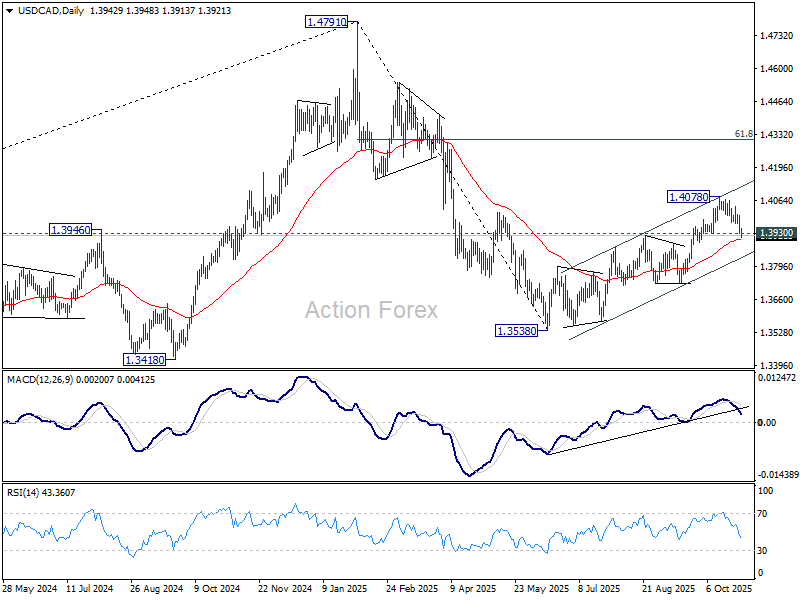

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3918; (P) 1.3962; (R1) 1.3989; More...

Intraday bias in USD/CAD is back now on the downside with break of 1.3930 support. Fall from 1.4078 should extend to rising channel support (now at 1.3835). Sustained break there will be a sign of bearish reversal. That is, rebound from has completed at 1.4078, and further fall would be seen to 1.3725 support for confirmation. On the upside, though, above 1.3969 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds. However, firm break of 1.3725 will revive the case that fall from 1.4791 is indeed a larger scale correction.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3918; (P) 1.3962; (R1) 1.3989; More...

Intraday bias in USD/CAD is back now on the downside with break of 1.3930 support. Fall from 1.4078 should extend to rising channel support (now at 1.3835). Sustained break there will be a sign of bearish reversal. That is, rebound from has completed at 1.4078, and further fall would be seen to 1.3725 support for confirmation. On the upside, though, above 1.3969 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3725 support holds. However, firm break of 1.3725 will revive the case that fall from 1.4791 is indeed a larger scale correction.

BoC cuts to 2.25%, signals end of easing Cycle

BoC delivered a widely expected 25bps rate cut, lowering its overnight rate to 2.25%, but signaled that this could mark the end of its current easing cycle. The central bank said that if inflation and economic activity evolve in line with its October projection, the current policy rate is “about the right level” to balance supporting growth with keeping inflation close to target. That phrasing was interpreted as indicating that 2.25% is the likely terminal rate, barring major economic shocks.

In its accompanying statement, the BoC acknowledged that U.S. trade actions and uncertainty are having “severe effects” on key export-oriented industries. As a result, the Bank expects GDP growth to remain weak in the second half of the year before recovering gradually through 2026. The economy is projected to expand 1.2% in 2025, 1.1% in 2026, and 1.6% in 2027, with excess capacity expected to be absorbed only slowly.

The BoC described the labour market as soft, with job declines concentrated in trade-sensitive sectors, while hiring across the broader economy remains subdued.

On inflation, the BoC noted that headline CPI stood at 2.4% in September, slightly above expectations, while its preferred core measures remain sticky around 3%. Broader alternative indicators suggest underlying inflation near 2.5%, but the BoC expects price pressures to ease gradually and headline CPI to remain close to 2% over the projection horizon.

Bank of Canada lowers policy rate to 2¼%

The Bank of Canada today reduced its target for the overnight rate by 25 basis points to 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%.

With the effects of US trade actions on economic growth and inflation somewhat clearer, the Bank has returned to its usual practice of providing a projection for the global and Canadian economies in this Monetary Policy Report (MPR). Because US trade policy remains unpredictable and uncertainty is still higher than normal, this projection is subject to a wider-than-usual range of risks.

While the global economy has been resilient to the historic rise in US tariffs, the impact is becoming more evident. Trade relationships are being reconfigured and ongoing trade tensions are dampening investment in many countries. In the MPR projection, the global economy slows from about 3¼% in 2025 to about 3% in 2026 and 2027.

In the United States, economic activity has been strong, supported by the boom in AI investment. At the same time, employment growth has slowed and tariffs have started to push up consumer prices. Growth in the euro area is decelerating due to weaker exports and slowing domestic demand. In China, lower exports to the United States have been offset by higher exports to other countries, but business investment has weakened. Global financial conditions have eased further since July and oil prices have been fairly stable. The Canadian dollar has depreciated slightly against the US dollar.

Canada’s economy contracted by 1.6% in the second quarter, reflecting a drop in exports and weak business investment amid heightened uncertainty. Meanwhile, household spending grew at a healthy pace. US trade actions and related uncertainty are having severe effects on targeted sectors including autos, steel, aluminum, and lumber. As a result, GDP growth is expected to be weak in the second half of the year. Growth will get some support from rising consumer and government spending and residential investment, and then pick up gradually as exports and business investment begin to recover.

Canada’s labour market remains soft. Employment gains in September followed two months of sizeable losses. Job losses continue to build in trade-sensitive sectors and hiring has been weak across the economy. The unemployment rate remained at 7.1% in September and wage growth has slowed. Slower population growth means fewer new jobs are needed to keep the employment rate steady.

The Bank projects GDP will grow by 1.2% in 2025, 1.1% in 2026 and 1.6% in 2027. On a quarterly basis, growth strengthens in 2026 after a weak second half of this year. Excess capacity in the economy is expected to persist and be taken up gradually.

CPI inflation was 2.4% in September, slightly higher than the Bank had anticipated. Inflation excluding taxes was 2.9%. The Bank’s preferred measures of core inflation have been sticky around 3%. Expanding the range of indicators to include alternative measures of core inflation and the distribution of price changes among CPI components suggests underlying inflation remains around 2½%. The Bank expects inflationary pressures to ease in the months ahead and CPI inflation to remain near 2% over the projection horizon.

With ongoing weakness in the economy and inflation expected to remain close to the 2% target, Governing Council decided to cut the policy rate by 25 basis points. If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment. If the outlook changes, we are prepared to respond. Governing Council will be assessing incoming data carefully relative to the Bank’s forecast.

The Canadian economy faces a difficult transition. The structural damage caused by the trade conflict reduces the capacity of the economy and adds costs. This limits the role that monetary policy can play to boost demand while maintaining low inflation. The Bank is focused on ensuring that Canadians continue to have confidence in price stability through this period of global upheaval.

Information note

The next scheduled date for announcing the overnight rate target is December 10, 2025. The Bank’s next MPR will be released on January 28, 2026.

Fed Will Make Things Clear

- Strong statistics are helping the dollar.

- The Fed may spring a surprise.

- The US asks the Bank of Japan to loosen its grip.

- The Aussie becomes the favourite.

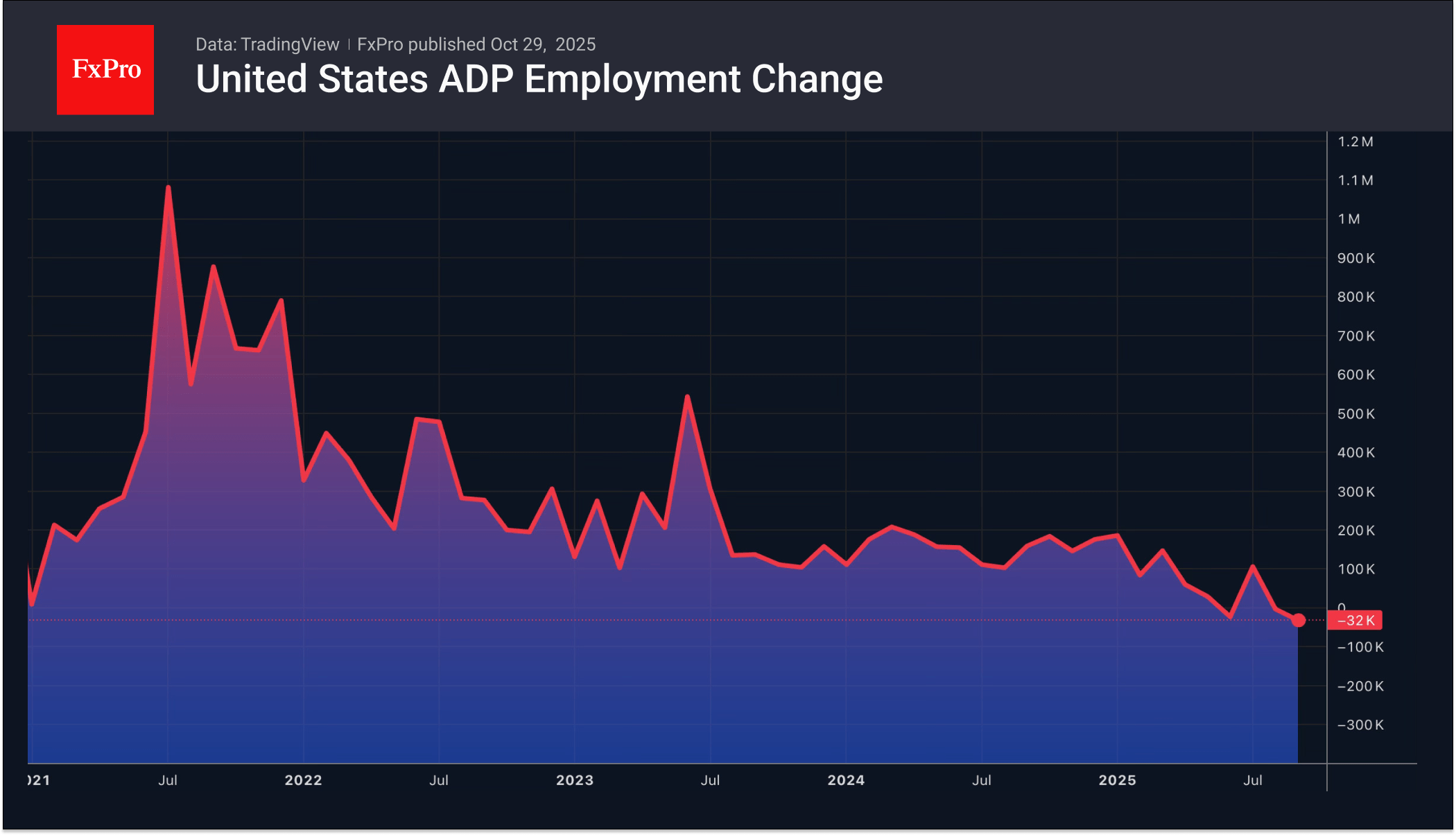

Strong US macroeconomic data and the closure of speculative positions on the US dollar ahead of the FOMC meeting announcement caused the EURUSD to retreat. ADP reported that private sector employment growth averaged 14,250 over the last four weeks to October 11. Compared to a decline of 32,000 over August, this indicates an improvement in the labour market. This pleases Fed hawks.

The doves received a dose of positivity after the September inflation statistics. Each group of opponents has its own trump cards. The divided Committee does not allow Jerome Powell to give a clear signal about the future of interest rates. The Fed chairman’s hawkish rhetoric is expected to positively impact the US dollar. The chances of monetary policy easing after December will fall, and EURUSD will drop even lower. On the contrary, a quiet and peaceful FOMC meeting will allow the world’s main currency pair to resume growth.

Meanwhile, the yen continues to strengthen. Scott Bessent called on the Japanese government to give its central bank room for manoeuvre. In his opinion, tightening monetary policy will help to anchor inflation expectations and prevent excessive exchange rate volatility. The White House is clearly unhappy with the previous USDJPY rallies. This is forcing the bulls to take profits, which leads to a pullback. While the chances of an overnight rate hike in October are slim, Kazuo Ueda’s hawkish rhetoric could breathe new life into the yen, boosting chances of a December hike.

Meanwhile, the Australian dollar has become a notable star in the Forex market recently. Accelerating inflation Down Under to a 2.5-year high has added fuel to the AUDUSD rally. The futures market has lowered the chances of the RBA easing monetary policy in early November from 40% to 8%. The probability of a sharp cash rate cut by December is only 25%.

The Aussie was supported by rumours that the US intends to reduce tariffs on Chinese imports related to fentanyl from 20% to 10% in exchange for Beijing tightening export controls on these goods. If this happens, the average tariff against China will fall from 55% to 45%. This is good news for the yuan and its proxy currencies, including the Australian dollar.