Sample Category Title

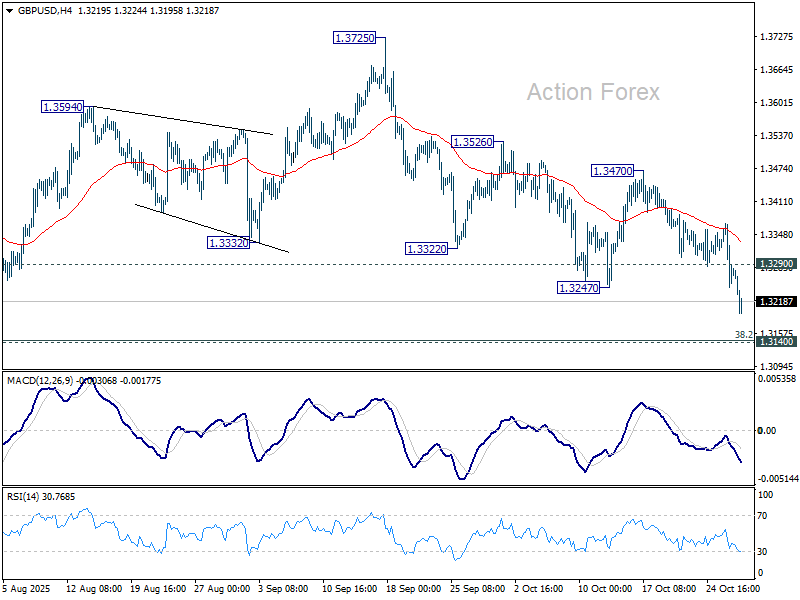

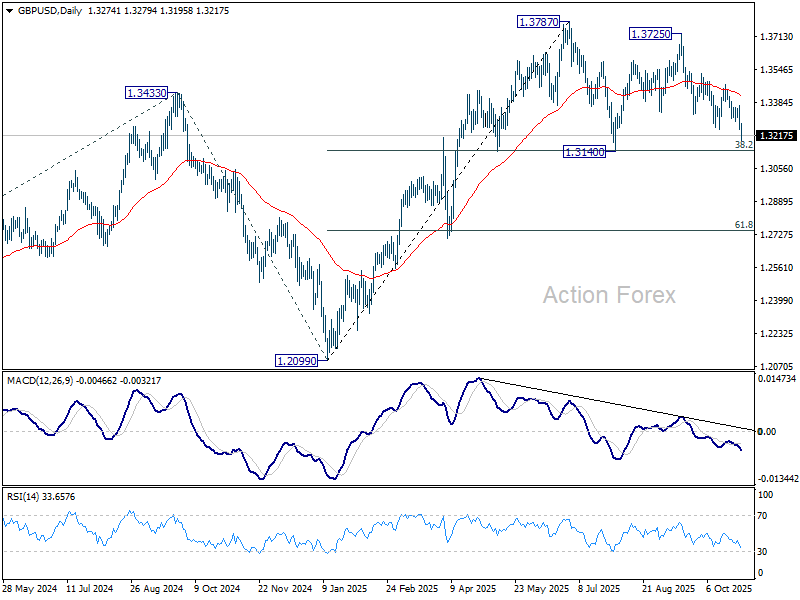

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3223; (P) 1.3297; (R1) 1.3345; More...

Intraday bias in GBP/USD stays on the downside for 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, above 1.3290 minor resistance will turn intraday bias neutral first. However, decisive break of 1.3140/2 will complete a double top pattern (1.3787/3725) and turn near term outlook bearish.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

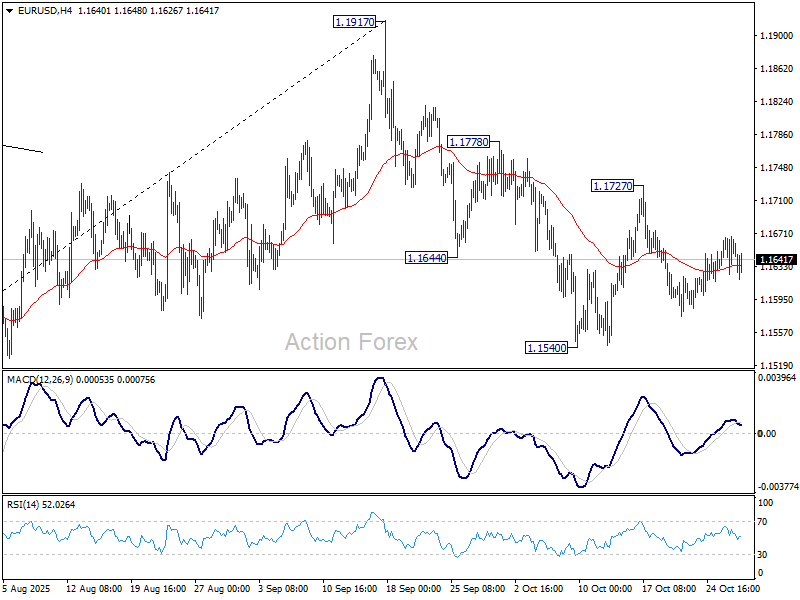

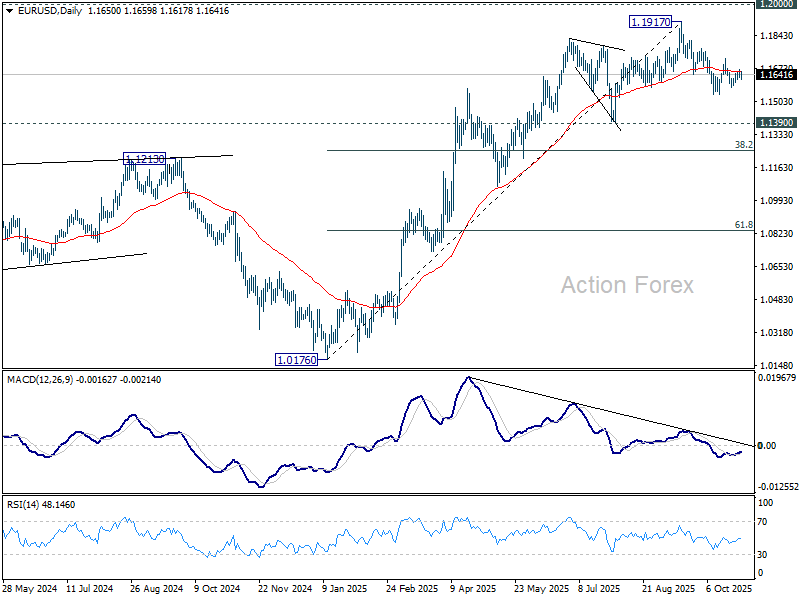

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1628; (P) 1.1648; (R1) 1.1672; More…

No change in EUR/USD's outlook as sideway trading continues. Intraday bias remains neutral for the moment. On the downside, below 1.1540 will resume the fall from 1.1917 and target 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1301) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

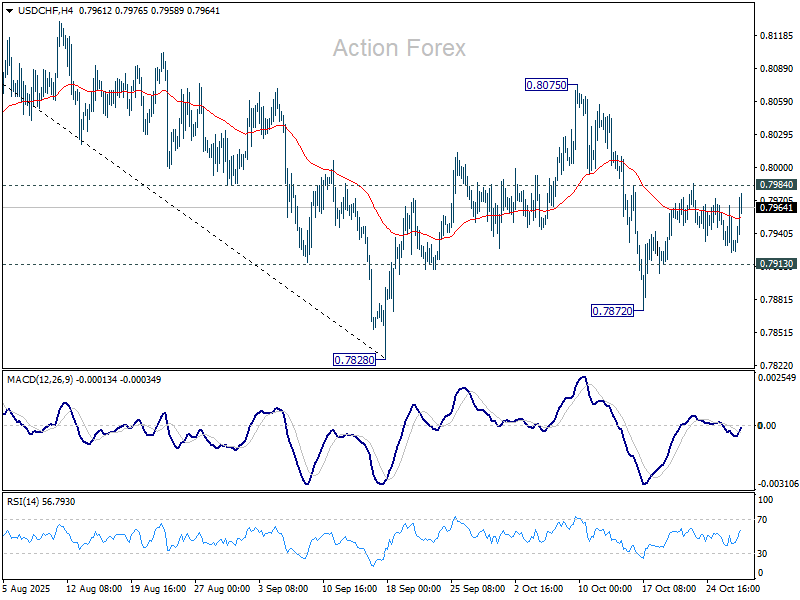

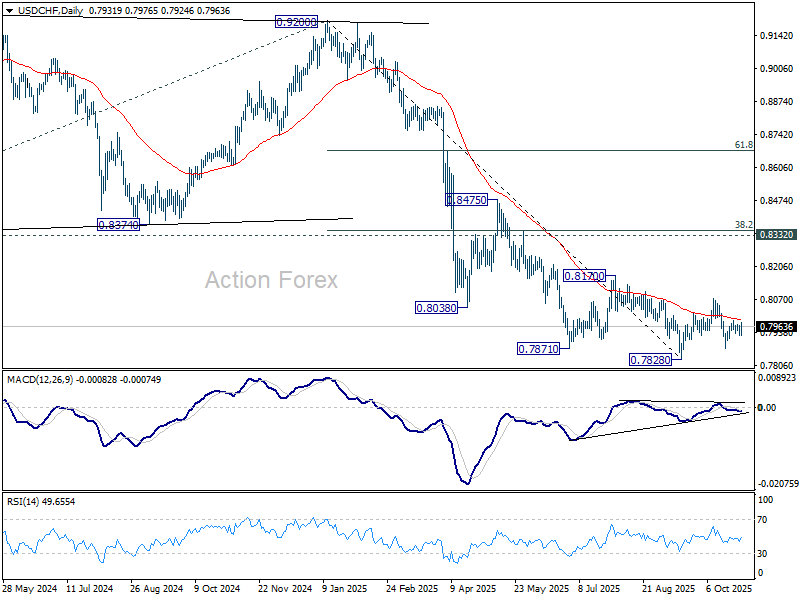

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7917; (P) 0.7942; (R1) 0.7959; More…

Intraday bias in USD/CHF stays neutral as sideway trading continues. On the downside, below 0.7913 will turn bias to the downside for 0.7872 support, and then 0.7828 low. However, firm break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

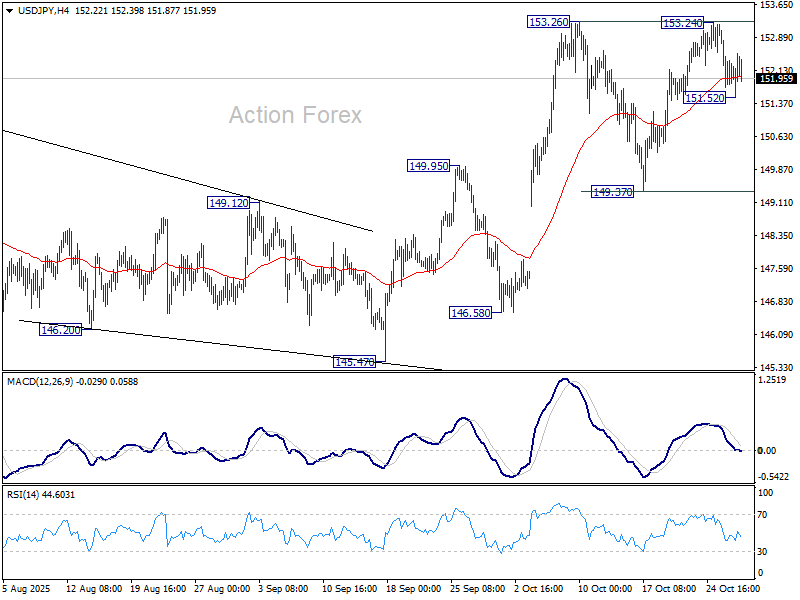

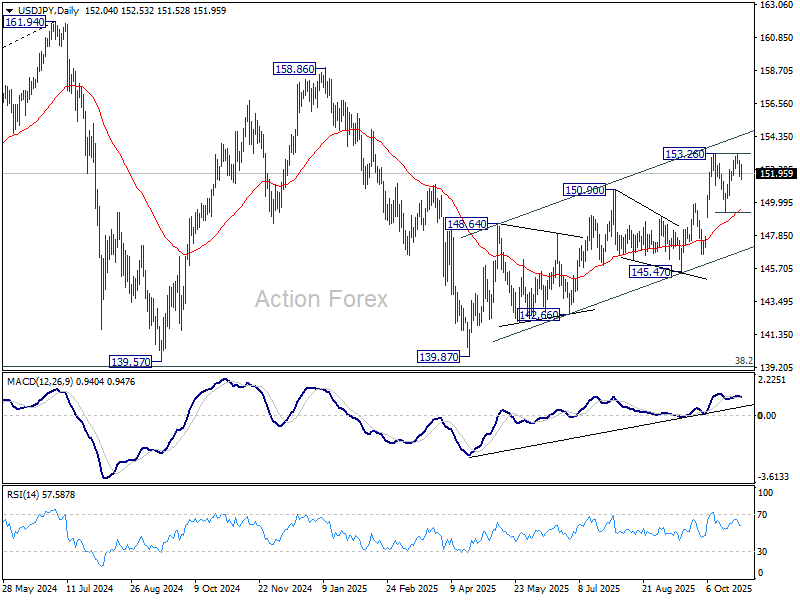

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.61; (P) 152.26; (R1) 152.75; More...

Intraday bias in USD/JPY remains neutral for the moment. On the upside, firm break of 153.24 will resume larger rally from 139.87. On the downside, break of 151.52 and sustained trading below 55 4H EMA (now at 151.99) will indicate that corrective pattern from 153.26 is extending with the third leg, and target 149.37 support next.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

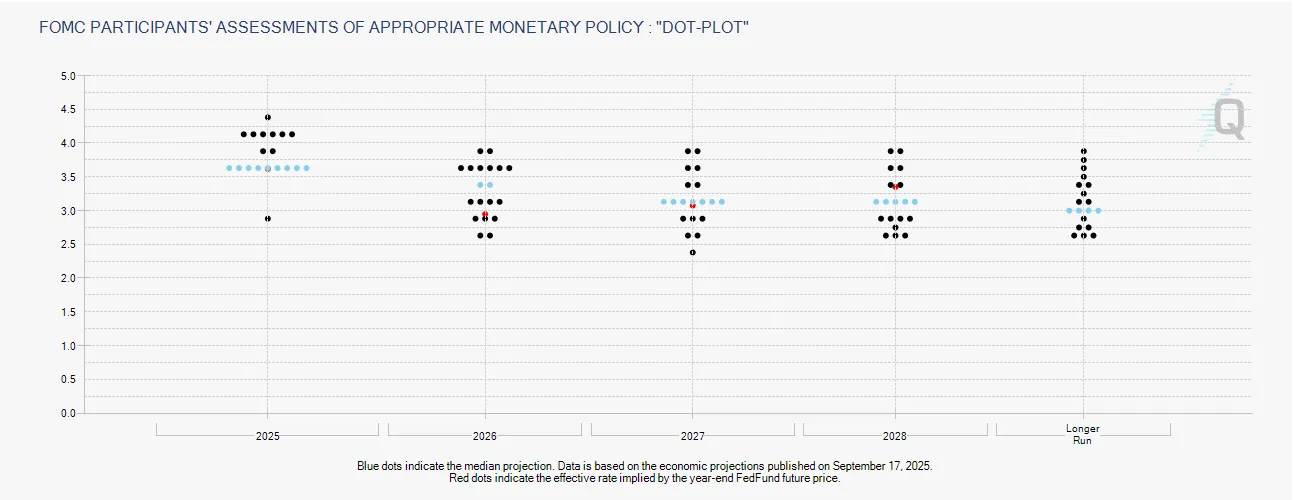

Fed (FOMC) Meeting Preview: 25 Bps Cut Incoming, Implications for US Dollar (DXY)

The Federal Reserve's meeting is wrapping up today, Wednesday, October 29, 2025. The biggest expected outcome is a change in monetary policy: the central bank is widely anticipated to lower its main interest rate (the federal funds rate) by 25 basis points (or a quarter of a percentage point).

This move would set the new target rate range at 3.75% to 4.00%. Financial markets are nearly certain this will happen, with a 99% probability already factored into trading.

Rate Action and Dissent

A decision to cut interest rates is primarily focused on the weakening job market, even though the economy's growth (GDP) was still strong at 3.8% last quarter. Policymakers seem willing to ignore inflation because they think the recent price hikes, mainly caused by new tariffs, won't last.

However, the Fed is still deeply divided. At least one official, likely Governor Miran, is expected to formally disagree with the decision, arguing for a larger 50 basis point (half-percent) rate cut. This sharp disagreement highlights a major split: some policymakers want to lower rates faster to prevent job losses, while others are worried that cutting too much will cause inflation to rise again.

The push for a deeper cut suggests that if the next report on the job market (whenever it finally comes out after the government shutdown) is very weak, the majority of the Fed could quickly agree to lower rates more aggressively than they are planning right now.

Forward Guidance and the Critical Dot Plot Disparity

Regarding the future of interest rates, the Federal Reserve is expected to signal that it is ready to make another cut in December, a view largely shared by the market with a 94% chance priced in for another 25 basis point reduction.

However, the biggest source of risk for the financial markets lies in the major disagreement over 2026. The Fed's own long-term projections (known as the Dot Plot) suggest a cautious approach with only 50 basis points of total cuts planned for all of 2026.

Source: CME FedWatch Tool

In stark contrast, market traders are expecting a much more aggressive response, pricing in at least 75 basis points of cuts, with some even anticipating as much as 125 basis points of easing by the end of 2026, which would drop the main interest rate down to 3%. This large gap shows that the market believes the Fed is moving too slowly to prevent a major collapse in the job market.

If Fed Chair Powell confirms the cautious 50 basis point path, markets that are currently counting on aggressive support will likely experience an immediate sell-off due to disappointment with the policy outlook.

Key Focus Areas and Macroeconomic Vulnerabilities

The biggest problem facing the Fed right now is the government shutdown, which is now in its 24th day. Because of the shutdown, they are missing crucial economic information, like the important September jobs report. This lack of official data has created a "data blind spot," forcing the Fed to rely on bits of information from private companies instead.

As a result, the Fed is not likely to change its overall economic view much; it will probably just repeat its concern that the "risk of job losses has increased."

Fed Chair Powell is expected to give a careful warning, emphasizing that the current economic growth is dangerously dependent on only three narrow things: wealthy consumers, a big wave of investment in AI, and rising stock/housing prices. This shaky foundation makes the economy very vulnerable, increasing the potential for a rapid boom or a quick, painful collapse.

Separately, regarding money management, the Fed is expected to announce a change in how it reinvests money from its assets, shifting toward buying shorter-term government bonds. This is meant to formally end its previous balance sheet reduction program (Quantitative Tightening or QT), balance its investments better, and help stabilize the short-term lending markets.

Potential Implications for the US Dollar

The immediate movement of the US Dollar will depend entirely on the relative hawkishness of Chair Powell's commentary compared to the market's aggressive easing expectations. The balance of risks is slightly tilted toward short-term USD upside.

If Powell stresses the elevated uncertainty, acknowledges the "healthy divergence of opinions" within the Committee, or emphasizes caution regarding inflation and the “no risk-free path for policy,” the resulting perceived policy resistance relative to market pricing could temporarily strengthen the greenback.

However, any FOMC-day USD rally is not expected to be long-lasting. The fundamental driver, the necessity for easing due to underlying labor market weakness is confirmed. Once the delayed official US data schedule resumes and validates the economic slowdown, renewed dollar softness is anticipated, continuing the longer-term depreciation trend.

Consequently, market participants should view any sharp, immediate dollar strength as a short-term mispricing of expectations, creating a potential selling opportunity against major pairs.

US Dollar Index (DXY) Daily Chart, October 29, 2025

Source: TradingView.com (click to enlarge)

A Key Day for EUR/USD as the Fed Decision Looms

The EUR/USD pair declined to 1.1642 on Wednesday, with investor attention firmly fixed on the Federal Reserve's impending policy decision. The central bank is widely expected to cut interest rates by 25 basis points.

Market participants will scrutinise the subsequent commentary from Chair Jerome Powell for any signals regarding the path for further policy easing. A further rate cut in December is already partially priced into the market.

Additional attention is being drawn to the upcoming meeting between Donald Trump and Xi Jinping, at which the parties may approve a framework trade agreement. The document provides for the suspension of new US tariffs and Chinese restrictions on exports of rare earth metals.

Meanwhile, the US dollar continues to weaken against the Japanese yen. This follows discussions between Japanese Finance Minister Satsuki Katayama and US Treasury Secretary Scott Bessent, in which they addressed recent volatility in the currency markets. Bessent’s call for a "prudent monetary policy" was interpreted by investors as a veiled criticism of the slow pace of interest rate normalisation in Japan.

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, the EUR/USD pair formed a tight consolidation range around the 1.1600 level. After an upward breakout, the pair completed a correction to 1.1680. With that correction now over, a new decline has begun. The next target for this bearish wave is 1.1540, which is considered only the first leg of the downtrend. Following a minor correction back towards 1.1600, the decline is expected to extend to at least 1.1488. This scenario is technically confirmed by the MACD indicator. Its signal line is above zero but has diverged from the histogram and is pointing decisively downward, indicating sustained bearish momentum.

H1 Chart:

On the H1 chart, the market is forming a downward wave structure targeting 1.1616. The pair is effectively establishing the boundaries of a new consolidation range around this level. An upward breakout could trigger another correction towards 1.1640. However, the primary expectation is for a resumption of the downtrend to 1.1576, with the potential to extend the wave to 1.1540. This would represent only the first half of the third wave within the broader downward trend. The Stochastic oscillator supports this outlook. Its signal line is below 50 and is falling confidently towards 20, suggesting that short-term downward potential remains.

Conclusion

The fundamental focus is squarely on the Fed, with technicals pointing to a bearish resolution for the EUR/USD. The overall structure suggests any rallies are likely corrective within a broader downtrend, with key targets situated near 1.1540 and potentially 1.1488.

Disclaimer:

Any forecasts contained herein are based on the author’s particular opinion. This analysis may not be treated as trading advice. RoboForex bears no responsibility for trading results based on trading recommendations and reviews contained herein.

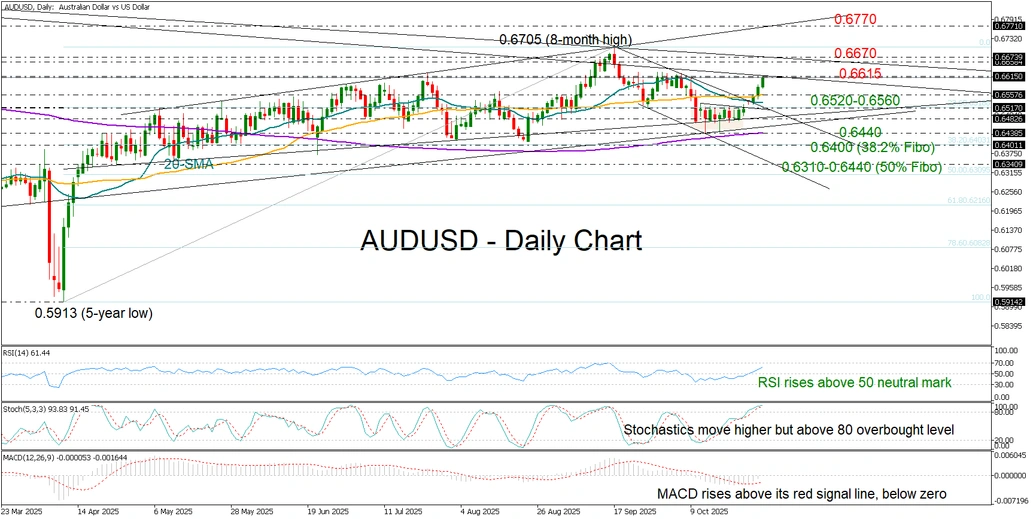

AUD/USD Poised for More Upside

- AUDUSD extends recovery phase toward October’s highs.

- Short-term bias remains positive, but key barriers still lie ahead.

AUDUSD continues its recovery, extending toward October’s highs near 0.6625 after the Reserve Bank of Australia (RBA) downplayed the chances of further rate cuts while inflation ticked higher. The shift in expectations helped lift the currency out of a brief consolidation phase.

In contrast, the U.S. Federal Reserve is expected to maintain its easing stance. While rate reductions are already priced in for this year, markets are watching for hints of additional cuts in early 2026. If confirmed, such expectations could fuel further gains in AUDUSD. However, the Fed will not update its rate or economic projections when its two-day policy meeting concludes today.

Technically, the pair’s break above the simple moving averages (SMAs) has improved the short-term picture. The positive trajectory in the RSI and the stochastic oscillator also support bullish momentum. Still, the pair remains capped below the long-term descending trendline connecting the 2021 and 2024 highs around 0.6615. The nearby 200-weekly SMA near 0.6670 is another critical resistance. A decisive move above these barriers could open the way toward 0.6770.

On the downside, the 0.6520–0.6560 region, containing the short-term SMAs and the 23.6% Fibonacci retracement of the April–September rally, may buffer downside movements. Further weakness below 0.6480 or 0.6400 could shift the outlook to bearish, shifting the spotlight to 0.6340.

Overall, the short-term bias for AUDUSD remains positive, with a close above 0.6615 likely to confirm renewed bullish momentum.

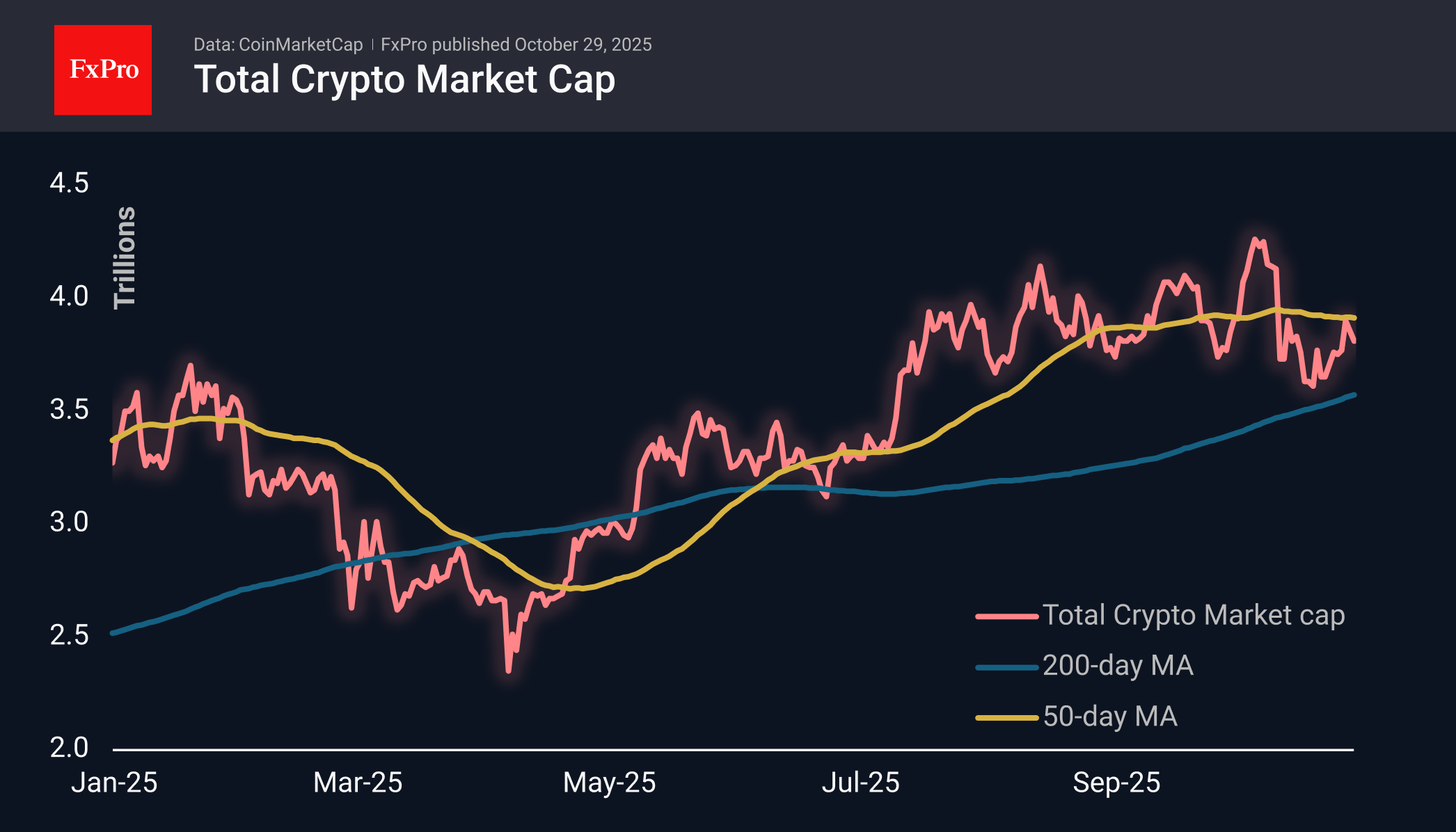

Crypto Market Continues to Retreat

Market Overview

The crypto market cap fell by another 1% to $3.81 trillion over the past 24 hours, continuing its retreat. On Monday, the 50-day moving average acted as resistance, stumbling the market’s recovery. The Trump coin is bucking the market trend, gaining more than 15% in 24 hours and 35% in 7 days.

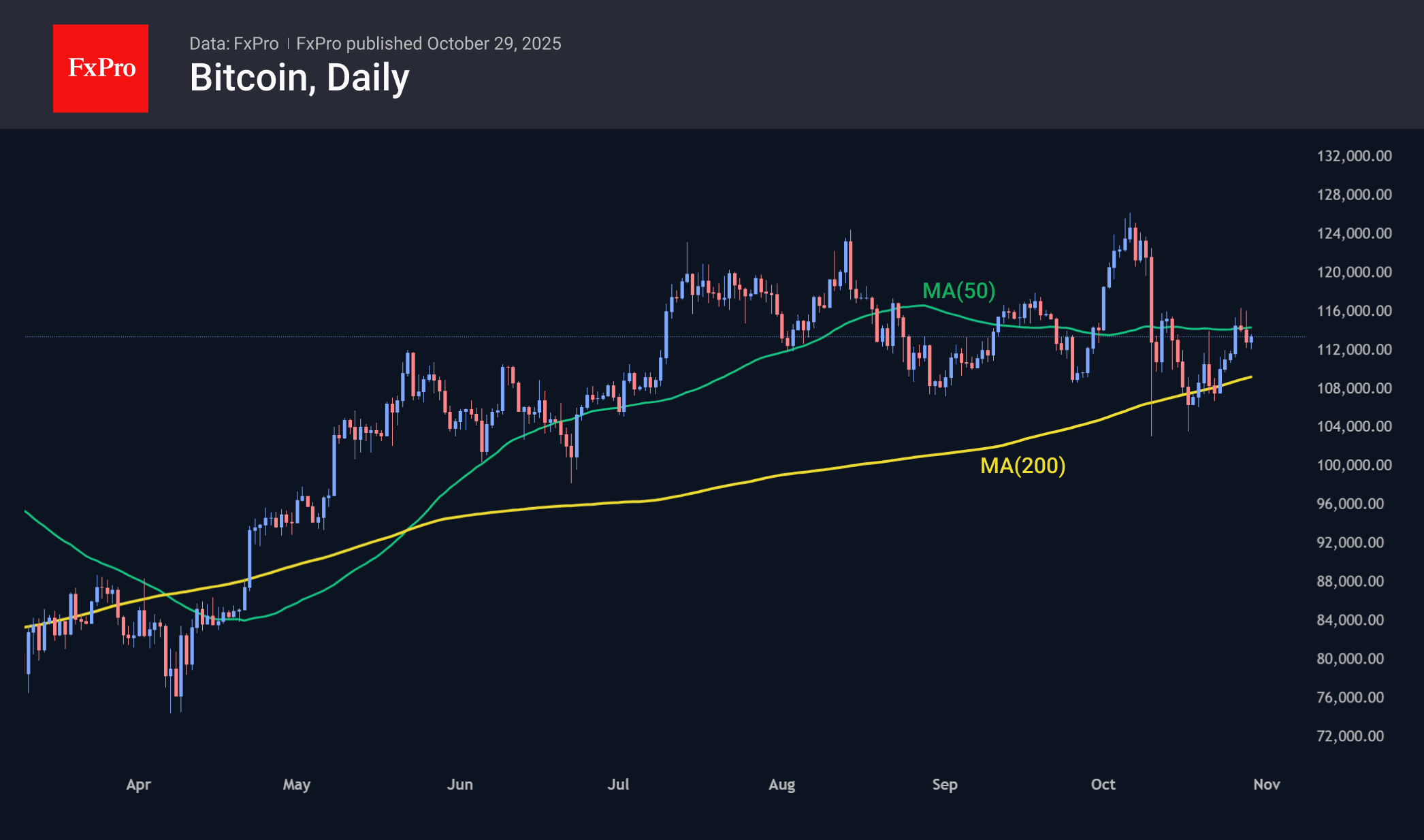

Bitcoin has gained slightly since the start of the day to $113.4K but is down 0.7% from the previous day’s level. The first cryptocurrency remains between two essential moving averages, the 50-day above and the 200-day below. So far this week, we have seen sales on the rise towards $115K. This performance contrasts with stock indices, which are constantly updating their all-time highs. We view this dynamic as an indicator of the fragility of global investor sentiment beneath the mask of general positivity.

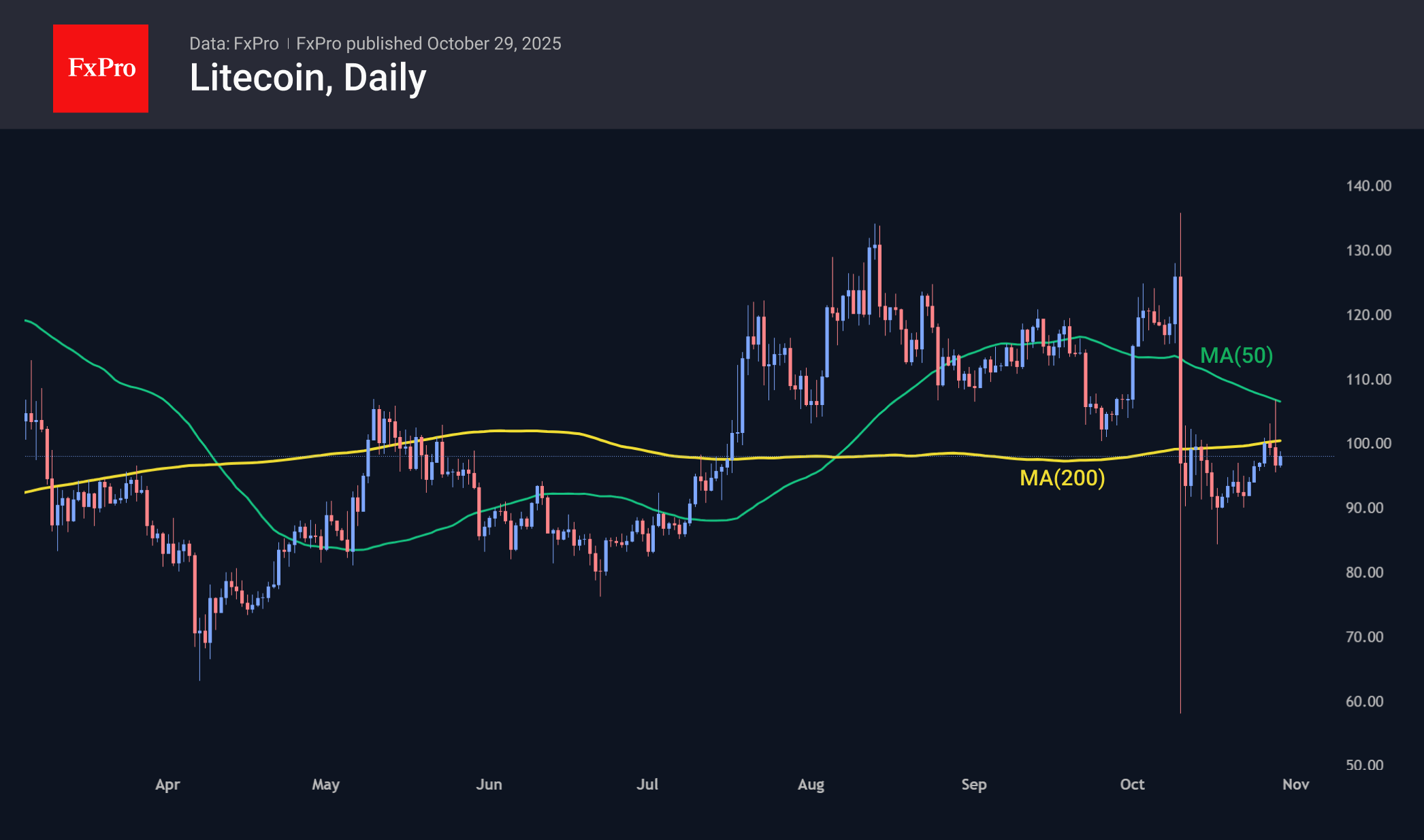

Litecoin has fallen more than 8% to $97 from Tuesday’s peak. As with the whole crypto market and Bitcoin, the coin failed to take the 50-day MA, which was tested later than in the first two cases. However, in this case, LTC immediately fell below the 200-day MA, and a death cross is brewing in the coin due to the downward 50-day MA.

News Background

To continue its rally to new highs, Bitcoin must hold the support level at $114K, where the 200-day moving average is located, Swissblock notes.

Bitcoin’s ability to overcome resistance at $116K is limited by the lack of significant inflows and low activity on the network, according to Glassnode. Continued growth requires an increase in spot trading volume and on-chain activity.

S&P Global Ratings has assigned Strategy a B- credit rating, classifying its securities as junk bonds. This is because of the company’s excessive concentration of assets in Bitcoin with debt obligations in US dollars.

In recent months, Strategy has sharply slowed the pace of BTC purchases due to difficulties in raising capital. TD Cowen remains optimistic about the company and its shares.

The Bitplanet crypto exchange will become the first public company in South Korea to create its own Bitcoin reserve. Bitplanet has already purchased its first 93 BTC and plans daily purchases to bring its reserves to 10,000 BTC.

EUR/USD Holds Weak, USD/CHF Retreats From Highs

EUR/USD started a downside correction from 1.1665. USD/CHF failed to clear 0.8000 and recently started a downside correction.

Important Takeaways for EUR/USD and USD/CHF Analysis Today

- The Euro seems to be facing strong resistance at 1.1665 against the US Dollar.

- There is a bullish trend line forming with support at 1.1635 on the hourly chart of EUR/USD at FXOpen.

- USD/CHF is correcting gains below 0.7960 and 0.7950.

- There is a declining channel or a bullish flag pattern forming with resistance at 0.7950 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair gained pace for a move above 1.1635. The Euro tested 1.1665 and recently corrected gains against the US Dollar.

The pair dipped below 1.1645, the 50-hour simple moving average, and the 23.6% Fib retracement level of the upward move from the 1.1576 swing low to the 1.1668 high. The pair is now testing a bullish trend line forming with support at 1.1635.

If the trend line holds, the pair could attempt a fresh increase. Immediate resistance on the upside is near 1.1645. The next key hurdle for the bulls could be near 1.1665.

An upside break above 1.1665 might send the pair toward 1.1700. Any more gains might open the doors for a move toward 1.1740. On the downside, immediate support on the EUR/USD chart is seen near the trend line.

The next major area of interest is 1.1620 and the 50% Fib retracement. A downside break below 1.1620 could send the pair toward the 1.1600 handle.

USD/CHF Technical Analysis

On the hourly chart of USD/CHF at FXOpen, the pair attempted a fresh increase above 0.7950. However, the US Dollar struggled near 0.7985 and recently started a fresh decline against the Swiss Franc.

The pair dipped below 0.7950 and the 50-hour simple moving average. The decline was such that the pair even spiked below the 50% Fib retracement level of the upward move from the 0.7872 swing low to the 0.7986 high.

On the other hand, there is a declining channel or a bullish flag pattern forming with resistance at 0.7950 and the 50-hour simple moving average. To start a fresh increase, the pair must settle above the channel.

The next major area of interest could be 0.7985. The main sell region could be near 0.8000. If there is a clear break above 0.8000 and the RSI remains above 60, the pair could start another increase. In the stated case, it could test 0.8050.

If there is another decline, the pair might test 0.7915 and the 61.8% Fib retracement. The first major support on the USD/CHF chart is near 0.7900.

A downside break below 0.7900 might spark bearish moves. The next key target for the bears might be 0.7870. Any more losses may possibly open the doors for a move toward 0.7820 in the near term.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Australian Dollar Rises Above $0.660

According to the AUD/USD chart today, the Australian dollar has climbed to its highest level in three weeks. The currency’s strength stems from the following factors:

→ Australia’s monthly consumer price index (CPI) came in stronger than expected. According to Forex Factory, annual inflation reached 3.5%, compared with analysts’ forecasts of 3.1%. This marks the highest reading since July 2024, pointing to renewed inflationary pressure.

→ As a result, traders have significantly reduced bets on further monetary easing. Data from Trading Economics shows that the probability of the Reserve Bank of Australia keeping its interest rate unchanged at 3.6% at its 4 November meeting is now close to 90%.

Technical Analysis of the AUD/USD Chart

Since mid-September, movements in the AUD/USD pair have formed a descending channel (shown in red), built on a series of lower highs and lows starting from point A.

However, note that in mid-October:

→ the price dipped below the lower boundary;

→ the RSI indicator entered oversold territory;

→ candles displayed large bodies;

→ an inverted head and shoulders reversal pattern emerged.

From a Smart Money Concept perspective, it is reasonable to assume that within the area marked by the purple rectangle, Smart Money was accumulating sellers’ liquidity to build long positions.

Following this, the Australian dollar showed strong momentum as the price broke through:

→ resistance at 0.6520 near the channel’s median (forming a bullish gap in the process);

→ the upper boundary of the red channel around 0.6565.

Building on this view → the price now appears to be moving towards a liquidity zone, where Smart Money could find sufficient buy-side liquidity. This area may lie above the 0.6630 level, which previously acted as resistance in early October.

It is also possible that today’s Federal Reserve decision (the Federal Funds Rate announcement scheduled for 21:00 GMT+3) will help this scenario play out.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.