Dollar stays broadly firm in Asian sessions after the recovery overnight. There were signs of bottoming in the greenback but the rally remains unconvincing with no follow through buying yet. Australian and New Zealand Dollars are currently the weaker ones. Better than expected job data is giving little support to the Aussie, as full coronavirus impact is not reflected in today’s release yet. Canadian Dollar recovers mildly but remain one of the worst performing for the week, on oil price and BoC’s QE extension.

Technically, some resistance levels are needed to be taken out to confirm Dollar’s strength. Those include 1.0768 support in EUR/USD, 0.9797 resistance in USD/CHF and 1.4349 resistance in USD/CAD. Developments in Aussie pairs would also be watch to confirm return of risk aversion. The levels include 0.5979 support in AUD/USD, 64.39 support in AUD/JPY and 1.8124 resistance in EUR/AUD, which are still far away.

In Asia, currently, Nikkei is down -1.39%. Hong Kong HSI dropped -0.81%. China Shanghai SSE is up 0.08%. Singapore Strait Times is up 0.37%. Japan 10-year JGB yield is down -0.0144 at 0.006. Overnight, DOW dropped -1.86%. S&P 500 dropped -2.20%. NASDAQ dropped -1.44%. 10-year yield dropped -0.114 to 0.638.

Australia employment grew in March, coronavirus impact to be evident in April

Australia employment unexpected grew 5.9k in March, versus expectation of -40.0k contraction. Full-time employment dropped just 400 to 8.88m. Part-time employment rose 6.4k to 4.14m. Unemployment rate rose just 1% from 5.1% to 5.2%, much better than expectation of 5.5%. Participation rate was steady at 66.0%.

Chief Economist at the ABS, Bruce Hockman, said: “Today’s data shows some small early impact from COVID-19 on the Australian labour market in early March, but any impact from the major COVID-19 related actions will be evident in the April data.”

RBNZ Orr not ruling out negative interest rates

RBNZ Governor Adrian Orr told the Epidemic Response Committee today that recovery from the coronavirus pandemic would be more challenging than that of the global financial crisis of 2008-9. He noted, “the most optimistic scenario is that we come out of this very very tight lockdown, and we remain out of this lockdown in varying levels of economic activity.”

He said RBNZ’s measures are just the beginning and even negative interest rates were not off the table. Though, it wouldn’t come for 12 months and the time frame would give retail banks some certainty to prepare for the possibilities. “We’re doing the best out of a bad situation,” he said.

Separately, Prime Minister Jacinda Ardern said a decision on whether to lower lockdown from level 4 would be made on April 20. But she emphasized that significant restrictions would remain in place even if that happens. “By design, Level 3 is a progression, not a rush to normality. It carries forward many of the restrictions in place at Level 4, including the requirement to mainly be at home in your bubble and to limit contact with others,” Ardern said.

Fed Beige Book: Activity contracted sharply and abruptly across all regions

Fed’s Beige Book report showed that economic activity “contracted sharply and abruptly across all regions” in the US as a result of the coronavirus pandemic. And, “all districts” reported highly uncertain outlooks among business contacts, with most expecting “conditions to worsen in the next several months.”

Regarding the job markets, contacts in several Districts noted they were cutting employment via “temporary layoff s and furloughs” that they hoped to reverse once business activity resumes. The near-term outlook was for “more job cuts in coming months.”

BoC stood pat, extended quantitative easing

BOC left the policy rate unchanged at 0.25% overnight. With the policy rate standing at the lower effective bound, the central bank added further monetary easing by extending the QE program. Unlike previous meetings, BOC did not provide the updated economic projections this time. Rather it used scenario analysis to estimate the level of real GDP and inflation outlook. The best scenario-a V-shaped recovery- requires removal of containment measures at the end of May. More in BOC Extends QE to Provincial and Corporate Bonds, while Leaving Rate at Lower Bound.

Looking ahead

Germany will release March CPI final in European session. Eurozone will release industrial production. Swiss will release PPI. Later in the day, US jobless claims will be a focus again. Housing starts and building permits will be featured with Philly Fed survey. Canada will release manufacturing sales.

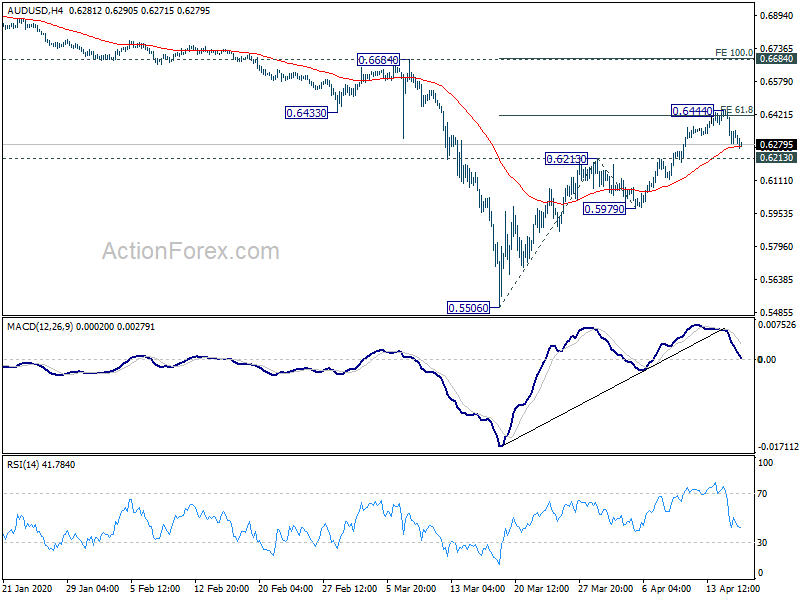

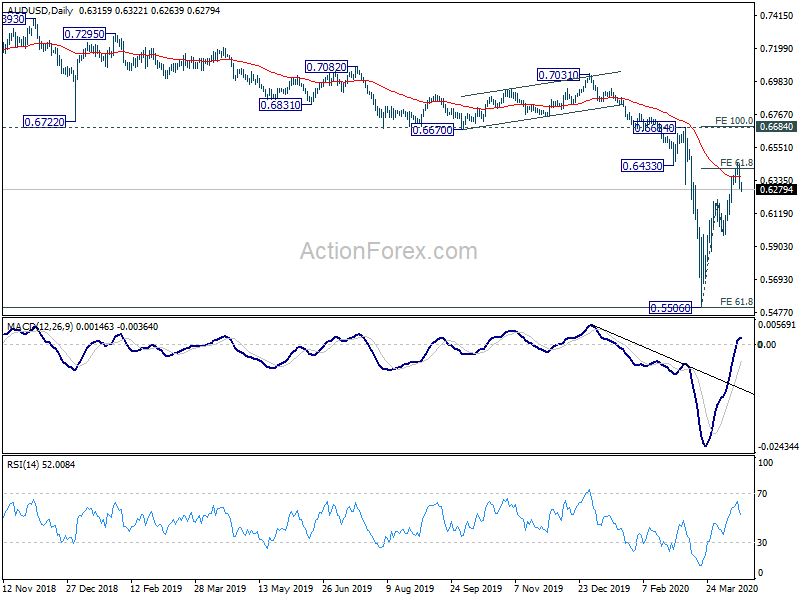

AUD/USD Daily Report

Daily Pivots: (S1) 0.6256; (P) 0.6350; (R1) 0.6415; More…

Intraday bias in AUD/USD remains neutral first. On the downside, break of 0.6213 resistance turned support will argue that rebound from 0.5506 has completed. Intraday bias will be turned back to the downside for 0.5979 support for confirmation. On the upside, break of 0.6444 will extend the rebound to 100% projection of 0.5506 to 0.6213 from 0.5979 at 0.6686, which is close to 0.6684 key resistance.

In the bigger picture, there is no clear sign of trend reversal yet. The larger down trend from 1.1079 (2011 high) is still in favor to extend. 61.8% projection of 1.1079 to 0.6826 from 0.8135 at 0.5507 is already met. Sustained break there will pave the way to 0.4773 (2001 low). On the upside, break of 0.6670 support turned resistance is needed to indicate medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Apr | 4.60% | 4.00% | ||

| 01:30 | AUD | Employment Change Mar | 5.9K | -40.0K | 26.7K | 25.6K |

| 01:30 | AUD | Unemployment Rate Mar | 5.20% | 5.50% | 5.10% | |

| 06:00 | EUR | Germany CPI M/M Mar F | 0.10% | 0.10% | ||

| 06:00 | EUR | Germany CPI Y/Y Mar F | 1.40% | 1.40% | ||

| 06:30 | CHF | Producer and Import Prices M/M Mar | -1.20% | -0.90% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Mar | -2.10% | |||

| 09:00 | EUR | Eurozone Industrial Production M/M Feb | -0.70% | 2.30% | ||

| 12:30 | CAD | Manufacturing Sales M/M Feb | -0.20% | |||

| 12:30 | USD | Housing Starts Mar | 1.31M | 1.60M | ||

| 12:30 | USD | Building Permits Mar | 1.30M | 1.45M | ||

| 12:30 | USD | Initial Jobless Claims (Apr 10) | 6606K | |||

| 12:30 | USD | Philadelphia Fed Manufacturing Apr | -30 | -12.7 | ||

| 14:30 | USD | Natural Gas Storage | 38B |

{kind=link}