Global equity markets traded cautiously and remained stable on Tuesday, showing limited reaction to escalating US trade threats. Major European indexes moved in narrow ranges following modest gains in Asia, while US equity futures stayed flat. The restrained response suggests markets are neither complacent nor panicked as they assess the credibility and timing of new tariff risks.

Investor nerves were tested when US President Donald Trump confirmed that imports from 14 countries—including Japan, South Korea, Malaysia, and Indonesia—will face new tariffs ranging from 25% to 40%, starting August 1. However, the absence of immediate action and Trump’s ambiguous tone helped calm markets. “The deadline is firm, but not 100% firm,” he told reporters, suggested that the US remains open to renegotiation.

It’s also noted that pushing the implementation date to August—beyond the previously expected July 9 deadline—helped ease fears of an imminent cliff edge. This delay gives key US trade partners more time to negotiate or soften the impact, explaining why risk sentiment has remained broadly resilient so far.

In the currency markets today, Australian Dollar outperformed sharply, gaining across the board after RBA defied expectations and held the cash rate steady at 3.85%. Speaking after the decision, RBA Governor Michele Bullock stressed that the hold was a matter of timing rather than a change in direction. She said the board preferred to wait for the full Q2 CPI report before confirming that inflation is heading sustainably toward target. Bullock emphasized that monetary policy remains well-positioned to respond if global conditions deteriorate further.

Overall, Kiwi followed Aussie as the second-best performer, with Loonie also firming. Yen lagged alongside Sterling and Dollar, while Swiss Franc and Euro were mixed.

Focus now turns to RBNZ, which is expected to keep its official cash rate unchanged at 3.25%. Recent inflation data has been mixed, and policymakers are looking for clearer signals before moving again. Holding now gives the RBNZ space to reassess in August with updated projections.

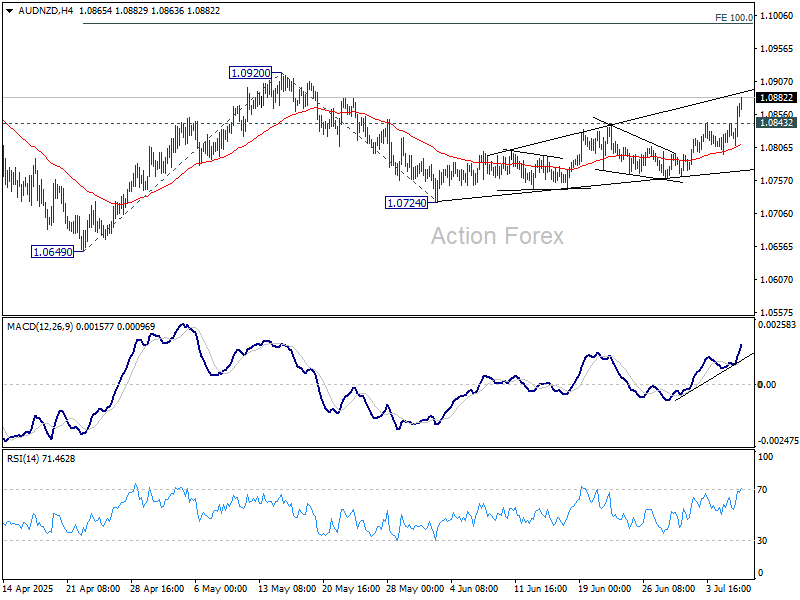

Technically, Aussie is currently outperforming Kiwi for the moment. AUD/NZD’s rise from 1.0724 accelerated higher today and remains on track to retest 1.0920. Firm break there will resume whole rally from 1.0649 and target 100% projection of 1.0649 to 1.0920 from 1.0724 at 1.0995. Nevertheless, break of 1.0843 minor support will mix up the outlook and turn bias neutral first.

In Europe, at the time of writing, FTSE is up 0.07%. DAX is up 0.07%. CAC is down -0.33%. UK 10-year yield is up 0.051 at 4.643. Germany 10-year yield is up 0.05 at 2.695. Earlier in Asia, Nikkei rose 0.26%. Hong Kong HSI rose 1.09%. China Shanghai SSE rose 0.70%. Singapore Strait Times rose 0.40%. Japan 10-year JGB yield rose 0.052 to 1.490.

RBA skips July cut, prefers to wait a little more for clarity

RBA held its cash rate target at 3.85%, opting not to deliver the widely expected 25bps cut. The decision, passed by a 6-3 majority, reflected cautious optimism as the central bank noted more balanced inflation risks and a still-resilient labor market. However, the Board stopped short of declaring victory on inflation and flagged considerable uncertainty in the domestic and global outlook.

In its statement, RBA said it could afford to “wait for a little more information” to ensure inflation is sustainably heading toward its 2.5% target. The Board remains concerned about both demand and supply-side uncertainty, particularly in light of volatile global trade policy. RBA stressed that monetary policy remains “well-positioned” to respond quickly if conditions deteriorate.

RBA also issued a measured warning on the risks stemming from U.S. tariffs and global trade policy shifts, noting that while extreme outcomes may be avoided, the uncertainty itself could weigh on demand. Financial markets have rebounded on hopes of compromise, but the RBA highlighted the risk that firms and households could delay spending amid the policy fog.

Australia’s NAB business confidence rises to 5, conditions rebound to 9

Australia’s business sentiment improved sharply in June, with NAB Business Confidence rising from 2 to 5, its highest trend level in over a year. Business Conditions surged from 0 to 9 after weakening for five straight months. The rebound was broad-based, with trading conditions jumping from 5 to 15, profitability returning to positive territory from -5 at 4, and employment conditions edging up from to 3.

On the pricing side, signals were mixed. Labour cost growth eased slightly from 1.6% to 1.5% (quarterly equivalent), while purchase costs rose from 1.2% to 1.5%. Final product price growth ticked up from 0.5% to 0.6%, although retail price growth slowed to 0.6%, hinting at easing consumer price pressures despite supply-side stickiness.

NAB’s Gareth Spence said the data suggest momentum may be picking up into the second half of 2025. “While we know the monthly survey can be volatile, the hope is at least some of these trends will be sustained,” he noted, calling the jump in both confidence and conditions a positive surprise amid ongoing global uncertainty.

EUR/USD Mid-Day Outlook

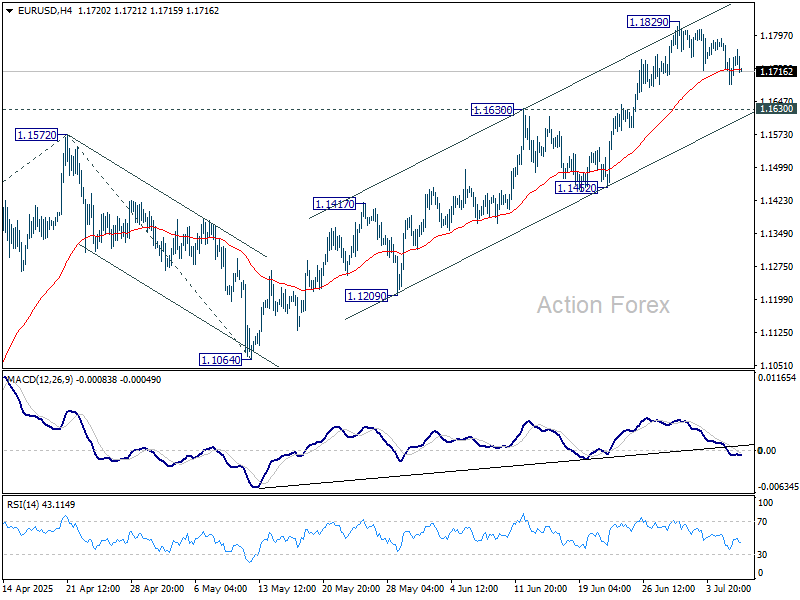

Daily Pivots: (S1) 1.1667; (P) 1.1729; (R1) 1.1770; More…

EUR/USD’s correction from 1.1829 continues today and intraday bias stays neutral. Downside should be contained by 1.1630 resistance turned support to bring rebound. Firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

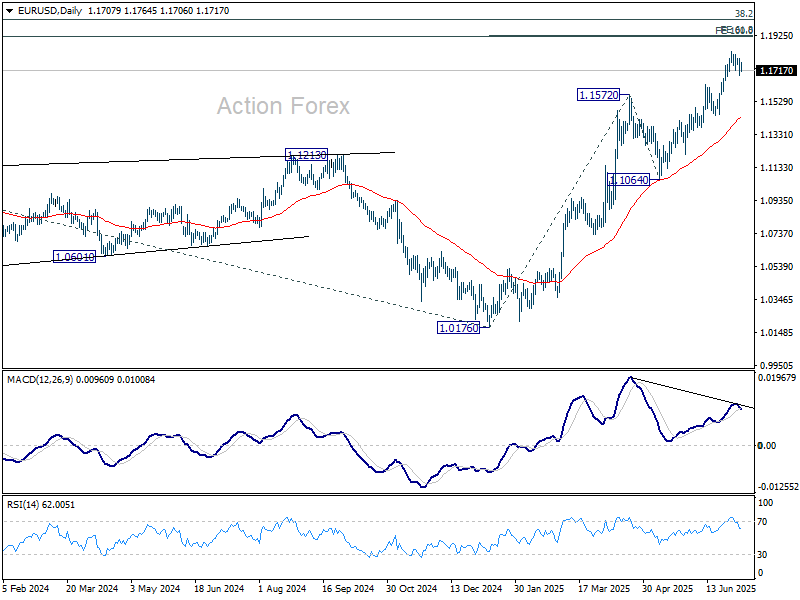

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

{kind=link}