Global markets appeared to stabilize somewhat today after the sharp U.S. selloff overnight, which saw the DOW suffer its worst one-day loss since October. That said, the underlying source of stress has not faded. Greenland-related tensions remain unresolved, with no visible path toward de-escalation. The current stabilization looks more like position-squaring, rather than renewed confidence.

For now, markets are simply catching their breath, awaiting the next catalyst. Attention has shifted to World Economic Forum, where US President Donald Trump is due to deliver a closely watched address later today. Trump’s speech comes amid soaring tensions between the U.S. and Europe over Danish territory Greenland, which Trump wants the U.S. to acquire. Markets are watching closely for any signal of escalation, moderation, or strategic ambiguity.

On Tuesday, Trump declined to specify how far he is prepared to go to achieve that objective, telling reporters bluntly, “You’ll find out.” He has previously refused to rule out military action and has threatened new tariffs on multiple European countries if they block the takeover bid.

Those threats have already left their mark on markets this week. The renewed risk of a transatlantic trade war pushed U.S. Treasuries sharply lower, while Gold surged to new record highs.

U.S. 10-year yield briefly breached 4.3% overnight, before settling around 4.295%. Speaking in Davos, Scott Bessent sought to play down concerns about the bond selloff. He said he was not worried about Treasuries, dismissing speculation that European investors were pulling back.

Asked specifically about Denmark, Bessent said its holdings were “irrelevant,” noting they amounted to less than USD 100 million, and added that Denmark has been selling Treasuries for years. He emphasized that the U.S. has seen record foreign investment in Treasuries overall.

Instead, Bessent pointed to Japan, arguing that the recent Japanese bond selloff following a snap election announcement had spilled over into global markets. He dismissed talk of European liquidation as originating from a single analyst at Deutsche Bank. Bessent added that Deutsche Bank’s CEO had personally contacted him to say the bank did not stand by the analyst report, accusing “fake news media” of amplifying unfounded fears.

Meanwhile, Gold climbed above 4,800, extending a powerful rally driven by tariff threats, geopolitical instability, falling real rates, and ongoing diversification away from the dollar. After a record 2025, Gold has entered 2026 with momentum firmly intact. According to analysts surveyed by the London Bullion Market Association, prices are increasingly expected to rise above 5,000 this year, citing lower U.S. real yields, continued Fed easing, and sustained central-bank diversification.

In FX performance terms this week so far, Dollar sits at the bottom, followed by Yen and Sterling, while Kiwi leads, followed by Swiss Franc and Aussie, with Euro and Loonie in the middle.

In Asia, Nikkei fell -0.41%. Hong Kong HSI rose 0.37%. China Shanghai SSE rose 0.08%. Singapore Strait Times is down -0.46%. Japan 10-year JGB yield stabilized and fell -0.056 to 2.288. Overnight, DOW fell -1.76%. S&P 500 fell -2.06%. NADSAQ fell -2.39%. 10-year yield rose 0.064 to 4.295.

ECB’s Lagarde: Tariffs manageable, Trump’s constant reversals more damaging

ECB President Christine Lagarde said she expects only a “minimal” inflationary impact from additional U.S. tariffs, arguing that Eurozone price pressures remain firmly under control. Speaking to RTL, Lagarde noted that inflation is currently around 1.9%, leaving little scope for tariffs to materially disrupt the ECB’s inflation outlook.

Though, she acknowledged that the impact would not be evenly distributed, with Germany likely more exposed than France given its export-heavy manufacturing base. However, Lagarde argued that Europe would be far more resilient if it focused on removing non-tariff trade barriers within the EU, strengthening internal trade and competitiveness rather than reacting defensively to external shocks.

Lagarde’s sharper warning was reserved for uncertainty, not tariffs themselves. Referring to renewed threats from US President Donald Trump, who has vowed to impose escalating tariffs on several European countries over Greenland, she said the “constant reversals” and unpredictability pose a more serious risk. Trump, she added, often takes a transactional approach, setting demands at “sometimes completely unrealistic” levels.

UK CPI rises to 3.4%, core holds at cycle low of 3.2%

UK inflation firmed at the end of 2025, with headline pressure coming in slightly hotter than expected. CPI rose to 3.4% yoy in December, up from 3.2% and above expectations of 3.3%, while prices increased 0.4% mom, pointing to ongoing near-term inflation momentum.

The upside in headline inflation, however, masked relative stability in underlying pressures. Core CPI—excluding energy, food, alcohol and tobacco—was unchanged at 3.2% yoy, undershooting expectations of 3.3%, and marking the joint-lowest reading since December 2024. Core inflation was last lower in September 2021, reinforcing the view that underlying disinflation progress, while slow, remains intact.

By component, services inflation edged up to 4.5% yoy from 4.4%, keeping the sector firmly in focus for the BoE, while goods inflation rose to 2.2% from 2.1%.

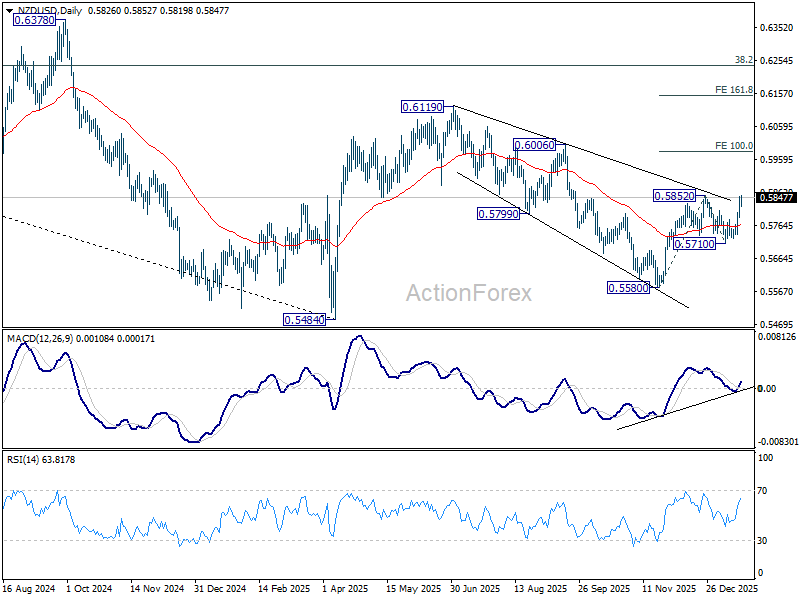

NZD/USD presses resistance Q4 CPI awaited on RBNZ hike guidance

NZD/USD has surged sharply this week and is now pressing key near-term resistance at 0.5852, as shifting global risk dynamics unexpectedly favor the Kiwi. With Dollar and Euro under pressure from Greenland-related geopolitical tensions, both New Zealand dollar and Australian Dollar have surprisingly emerged as relative safe havens, benefiting from stable domestic backdrops and distance from the dispute.

At the same, Yen remains under pressure, weighed down by an aggressive selloff in Japanese government bonds as markets price in post-election fiscal expansion. That divergence has left antipodean currencies unusually well-bid, along with Swiss Franc.

For Kiwi, attention now turns to New Zealand Q4 CPI, due Friday in Asia. The annual rate is expected to hold at 3.0%, right at the top of the RBNZ’s 2–3% target band. With the Official Cash Rate at 2.25%, markets broadly agree the RBNZ has completed its easing cycle. The open question is timing of the next hike, not whether one eventually comes. CPI overshoot would sharply pull forward expectations and offer fresh support to NZD.

That focus will intensify at the February 18 OCR review, the first major policy decision under new Governor Anna Breman. Markets will be listening closely to the tone of the post-meeting press conference for clues on whether Breman leans hawkish, dovish, or neither.

Technically, NZD/USD’s dip to 0.5710 earlier this month was a little deeper than expected. But that didn’t alter the overall structure. The corrective down trend from 0.6119 (2025 high) should have completed with three waves down to 0.5580.

Firm break of 0.5852 will resume the whole rally from 0.5580 and target 100% projection of 0.5580 to 0.5852 from 0.5710 at 0.6015. Decisive break of 0.6015 will solidify that NZD/USD is in an impulsive move that should be resuming whole rise from 0.5484 (2025 low) through 0.6119. In any case, outlook will now stay bullish as long as 0.5710 support holds.

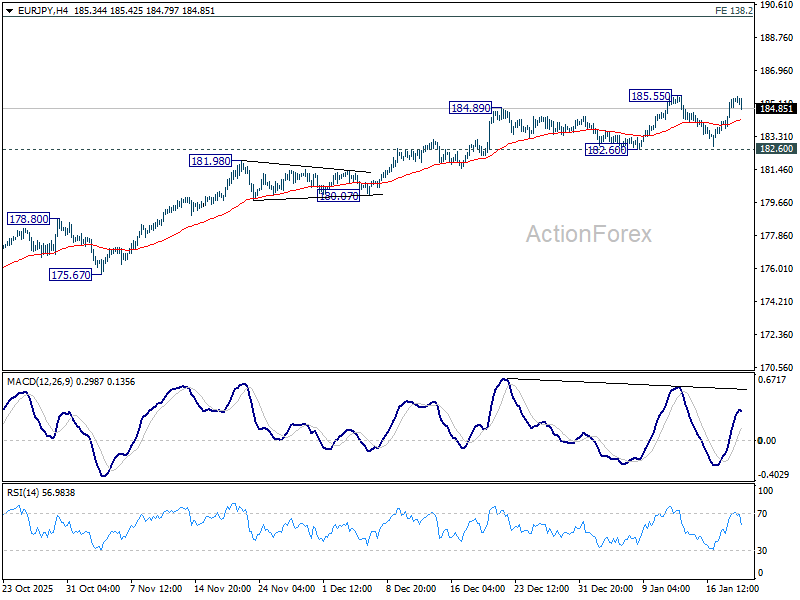

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.33; (P) 184.90; (R1) 186.02; More…

EUR/JPY retreated ahead of 185.55 resistance as range trading continues. Intraday bias remains neutral for the moment. With 182.60 support intact, further rally is expected. On the upside, break of 185.55 will resume larger up trend to 186.31 projection level. Firm break there will target 138.2% projection of 151.06 to 173.87 from 172.24 at 189.94. However, sustained break of 182.60 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 181.83) and below.

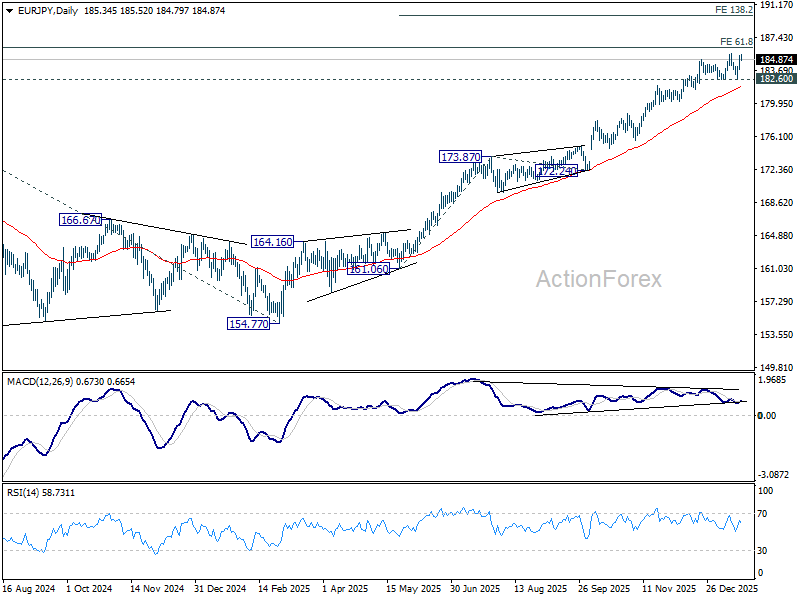

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 172.58) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 78.6% projection at 194.88 next.

{kind=link}