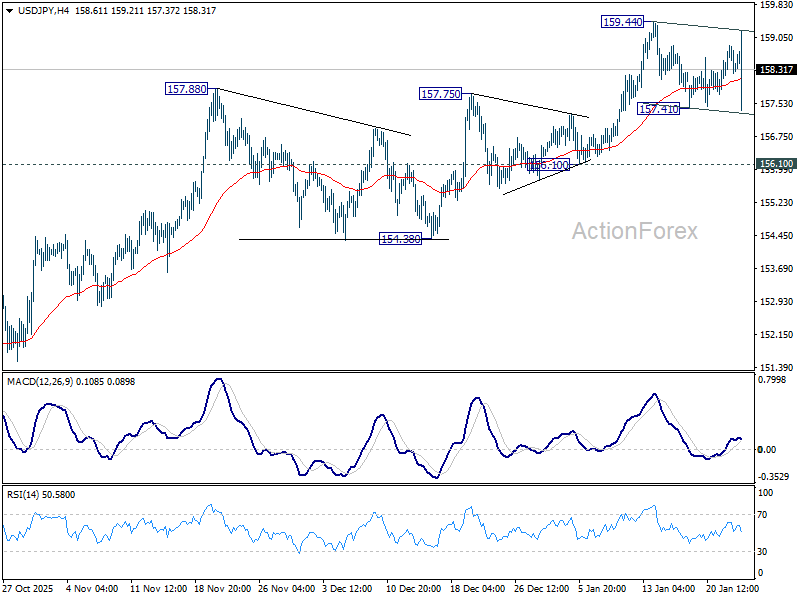

Yen staged a sharp rebound in early European session on suspected intervention, interrupting a renewed bout of selling that followed the Bank of Japan policy decision. The bounce came after markets judged the BoJ’s message insufficiently hawkish to arrest currency weakness.

Before the reversal, USD/JPY pushed beyond 159, extending gains after BoJ Governor Kazuo Ueda stopped short of signaling imminent tightening. The move was swiftly countered, with the pair knocked down to 157.30 in a sharp, one-way drop characteristic of official action. Yet the rebound quickly stalled. Demand re-emerged above 157, keeping USD/JPY trapped within a 157.40–159.40 range, indicating that intervention has stabilized, but not reversed, the broader trend.

The price action nevertheless highlights an important point: Japanese authorities appear unwilling to tolerate a sustained move above 160. That line in the sand may deter momentum traders in the near term, but history suggests it will be retested once volatility fades.

The underlying policy story remains a headwind for Yen. The BoJ failed to offer any sense of urgency around further hikes, with just one policymaker advocating a move toward 1%. That vote count reinforces the view that the board remains cautious. Although the BoJ raised growth forecasts, inflation projections were left broadly unchanged, weakening the case for front-loaded tightening. The message remains one of gradualism rather than acceleration.

Incoming data have also sent mixed signals. Core inflation slowed sharply, partly due to energy subsidies, while PMI readings were exceptionally strong, highlighting solid activity momentum but limited near-term inflation pressure. Taken together, there is no strong signal for an April hike. Market pricing has converged decisively on June as the earliest realistic timing for the next BoJ move.

Elsewhere in FX, Kiwi eased modestly, likely reflecting profit-taking after stronger-than-expected inflation data earlier. Even so, the broader trend remains supportive, with markets increasingly pulling forward expectations for the first RBNZ hike, now seen as “odds on” by December 2026, with upside risk toward even earlier action. Aussie also remains firm. Strong PMI data added to the momentum built earlier in the week by robust employment figures, reinforcing expectations of a sooner-than-expected RBA hike.

On a weekly basis, Yen remains the worst-performing currency, despite today’s bounce. Dollar follows closely, still weighed down by lingering transatlantic political strains, with Loonie next weakest. At the top, Kiwi leads, followed by Aussie and Swiss Franc, while Euro and Sterling sit in the middle of the pack.

In Asia, Nikkei rose 0.29%. Hong Kong HSI rose 0.45%. China Shanghai SSE rose 0.33%. Singapore Strait Times is up 1.20%. Japan 10-year JGB yuield rose 0.012 to 2.252. Overnight, DOW rose 0.63%. S&P 500 rose 0.55%. NASDAQ rose 0.91%. 10-year yield fell -0.004 to 4.249.

BoJ holds rates, upgrades growth outlook, hawkish dissent keeps hike risk alive

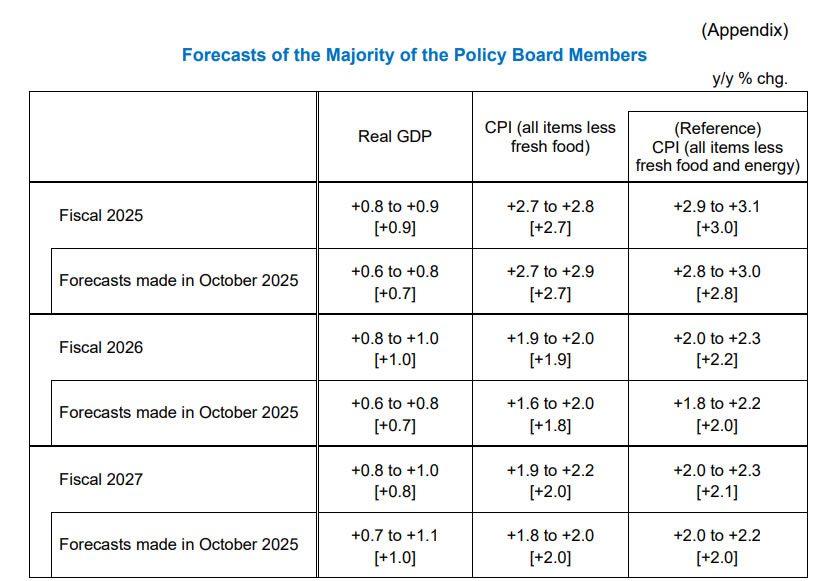

The BoJ left its benchmark interest rate unchanged at 0.75%, in line with expectations, but the decision revealed persistent internal debate. Hawkish board member Hajime Takata proposed a hike toward 1%, citing upside risks to inflation, though the motion was voted down by the majority.

The central bank maintained its assessment that the 2% inflation target will be achieved in the latter half of the three-year projection period through fiscal 2027, keeping its medium-term normalization narrative intact despite near-term caution.

At the post-meeting press conference, Governor Kazuo Ueda reiterated a data-dependent tightening bias. He said the BoJ would “continue to raise rates if economic and price forecasts materialize”, stressing that the pace and path of hikes would be determined meeting by meeting as conditions evolve.

In its quarterly outlook report, the BoJ upgraded growth forecasts, reflecting the impact of fiscal stimulus under Prime Minister Sanae Takaichi. The economy is now seen growing 0.9% in the current fiscal year and 1.0% next year, up from 0.7% previously. Inflation projections were largely unchanged, aside from a 0.1pp upward revision to 1.9% for fiscal 2026.

The BoJ highlighted risks from overseas growth and prices, adding “exchange rate developments are, compared to the past, more likely to affect prices.”

Japan’s CPI core falls to 2.4% with sharp energy drag, limited core-core cooling

Japan’s December CPI report showed sharp moderation in headline inflation, largely reflecting energy relief rather than broad-based disinflation. Headline CPI slowed to 2.1% yoy from 2.9%, the weakest pace since early 2022. Core CPI (ex-fresh food) fell from 3.0% to 2.4%, helped by government measures to stabilize gasoline prices.

However, the decline was far less pronounced beneath the surface. Core-core CPI (ex-fresh food and energy) edged down just 0.1pp to 2.9% yoy, highlighting the stickiness of domestic inflation. Food prices excluding fresh items remained elevated at 6.7% yoy, though the pace eased slightly from 7.0%. Rice prices were still up 34.4%, even as inflation in the staple continued to cool gradually from prior peaks.

Energy prices were the key drag, reversing into a -3.1% yoy decline as gasoline prices fell -7.1%, reflecting higher subsidies and preparation for a gasoline tax cut late in the month. While these policy measures are temporarily easing inflation readings, the modest pullback in core-core CPI suggests underlying price pressures remain too firm to ignore.

Japan PMI composite jumps to 52.8, manufacturing returns to growth

Japan’s January PMI readings delivered an upbeat signal, indicating a broadening recovery across the private sector, with PMI data pointing to the strongest expansion in 17 months. Manufacturing PMI rose from 50.0 to 51.1, returning to expansion. Services PMI jumped from 51.6 to 53.4. As a result, Composite PMI climbed from 51.1 to 52.8, signaling broad-based growth momentum.

According to Annabel Fiddes of S&P Global Market Intelligence, the data show a “solid start” to the year, supported primarily by accelerating services activity. Also, manufacturing output rose for the first time since June 2025, marking an important shift after a prolonged period of weakness.

The improvement was reinforced by the first increase in manufactured goods sales in more than three-and-a-half years, alongside rise in new export orders for the first time since early 2022.

However, business optimism weakened, reflecting concerns over rising costs, global uncertainty, labour shortages, and Japan’s ageing population, suggesting growth momentum may face headwinds later in the year.

Australia PMI composite surges to 55.0, manufacturing and services in solid expansion

Australia’s business activity accelerated sharply in January, pointing to a strong start to 2026. PMI Manufacturing rose from 51.6 to 52.4, while PMI Services surged from 51.1 to 56.0. As a result, PMI Composite jumped from 51.0 to 55.0, marking the joint-highest level since April 2022 and signaling a broad-based expansion.

According to Jingyi Pan of S&P Global Market Intelligence, the flash PMI data show that growth has become “more balanced”, with “solid expansions evident across both manufacturing and services”. The readings reflect resilient domestic demand and improving momentum entering the new year.

That said, forward-looking indicators were mixed. Faster new order growth contrasted with declining business confidence, particularly among service providers.

While output price inflation eased, driven by softer service-sector charges, rising manufacturing input costs remain a risk factor, suggesting inflation pressures could re-intensify later in the quarter.

NZ CPI pushes above target as RBNZ Breman’s tone shifts

New Zealand inflation accelerated again. Headline CPI rose 3.1% yoy, up from 3.0% and above expectations of 3.0%, pushing inflation back above the RBNZ’s 1–3% target band. It marked the highest annual rate since Q2 2024.

The composition of inflation showed renewed pressure from tradeable prices. Tradeable CPI jumped from 2.2% yoy to 2.6% yoy, while non-tradeable CPI held steady at 3.5% yoy.

On a quarterly basis, CPI rose 0.6% q/q, exceeding expectations of 0.5%, with both tradeable (0.7% qoq) and non-tradeable (0.6% qoq) components contributing.

Notably, RBNZ Governor Anna Breman struck a firmer in a Bloomberg interview, pledging that policymakers will ensure inflation returns to the midpoint of the target band. She declined to push back against market pricing for a rate hike, saying policy decisions would be based on a “holistic view” of incoming data at the February meeting—marking a clear shift from her more neutral comments earlier this month.

USD/JPY Daily Outlook

Daily Pivots: (S1) 158.10; (P) 158.50; (R1) 158.82; More…

USD/JPY drops sharply in early European session, but stays in range below 159.44. Intraday bias remains neutral at this point. Also, with 156.10 support as well as 55 D EMA (now at 156.03) intact, further rise is expected. On the upside, break of 159.44 will resume the rise from 139.87 towards 161.94 high. However, firm break of 156.10 will confirm short term topping, and turn bias back to the downside for deeper pullback.

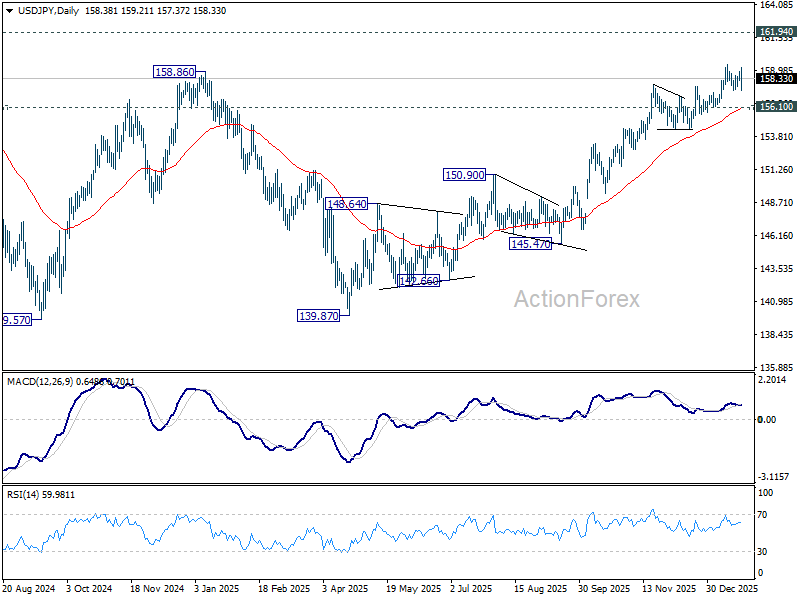

In the bigger picture, corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.86 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.

{kind=link}