The brief reprieve for Dollar has already faded. As markets move into the US session, the greenback is once again under broad selling pressure, undoing the tentative stabilization seen earlier and returning to a defensive footing. There is little in the way of fresh fundamental catalysts today. Instead, the renewed pressure appears to reflect positioning fatigue, with traders increasingly unwilling to wait until tomorrow’s FOMC rate decision before re-engaging against the Dollar.

Nevertheless, a key question is whether Fed policymakers deliver any slightly hawkish twist in language alongside the widely expected rate hold, and whether such a signal would be sufficient to spark a durable Dollar recovery. Even if the Fed leans marginally firmer, expectations for a sustained rebound remain muted. With geopolitical uncertainty surrounding the US still elevated, markets may be reluctant to chase Dollar higher on nuance alone.

Also, the renewed strength in Swiss Franc, which is outperforming both Euro and Sterling, points to some underlying risk aversion rather than a purely Dollar-specific adjustment. Hence, while geopolitical noise has softened somewhat. Several developments continue to hover in the background, capable of unsettling sentiment if mishandled.

In Europe, UK Prime Minister Keir Starmer’s visit to China is one such event to pay attention to. The trip, the first by a British leader in eight years, signals London’s desire to diversify partnerships and ease reliance on the US at a time of growing unpredictability. That sensitivity stems from recent precedent. After Canadian Prime Minister Mark Carney’s China engagement, US President Donald Trump threatened 100% tariffs on Canadian goods should Ottawa proceed with a China trade deal. Similar rhetoric toward the UK cannot be ruled out.

A second focal point is Trump’s response to the India–EU free trade agreement. The “Mother of All Deal”, announced by Prime Minister Narendra Modi and set to be detailed alongside President Ursula von der Leyen, represents a major step in global trade integration outside US-led frameworks. That sense of fragmentation was echoed by German Economy Minister Katherina Reiche, who warned that trusted alliances are fraying, forcing nations to balance cooperation with the pursuit of new partners in a more uncertain world.

In FX markets, Dollar is currently the weakest performer on the day, followed by Loonie and Kiwi. Swiss Franc leads, with Yen and Aussie also firm. Euro and Sterling sit in the middle. Aussie stands out as a potential mover in the next session. With Australian CPI due shortly.

In Europe at the time of writing, FTSE is up 0.69%. DAX is down -0.11%. CAC is up 0.36%. UK 10-year yield is up 0.036 at 4.534. Germany 10-year yield is up 0.013 at 2.885. Earlier in Asia, Nikkei rose 0.85%. Hong Kong HSI rose 1.35%. China Shanghai SSE rose 0.18%. Singapore Strait Times rose 1.28%. Japan 10-year JGB yield rose 0.04 to 2.288.

Australia NAB business survey reinforces solid backdrop for RBA

Australia’s NAB business survey showed a modest but broad-based improvement in December, pointing to resilient momentum into year-end. Business Confidence edged up from 2 to 3, while Business Conditions rose from 7 to 9.

The details underline that improvement. Trading conditions climbed from 13 to 16, while profitability rose from 4 to 7. Employment conditions were unchanged at 4, suggesting hiring demand remains steady rather than accelerating. Capacity utilisation eased slightly to 83.2%, down from its recent peak but still well above its long-run average.

Cost pressures also edged higher, with purchase costs rising from 1.3% to 1.4% in quarterly equivalent terms, labour costs from 1.5% to 1.8%, and product prices from 0.6% to 0.9%, even as retail price growth slowed to 0.4% from 0.8% in November.

Overall, the survey suggests the economy ended the year on a firm footing, with most indicators sitting modestly above late-Q3 levels. Meanwhile, NAB noted that for the RBA, the small pullback in capacity utilisation is unlikely to materially ease concerns that the economy remains close to capacity.

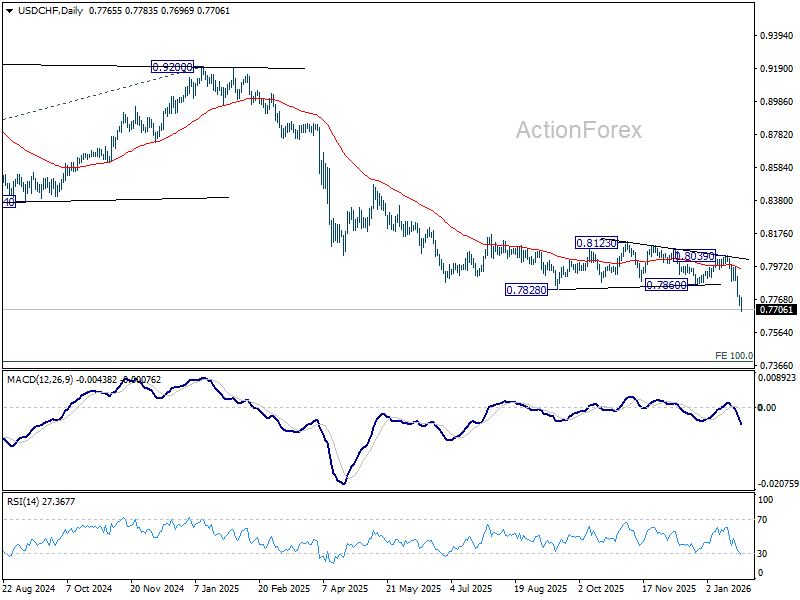

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7736; (P) 0.7765; (R1) 0.7799; More….

USD/CHF’s fall resumes after brief consolidations and intraday bias is back on the downside. Current fall is part of the long term down trend and should target 0.7382 projection level next. On the upside, above 0.7283 minor resistance will turn intraday bias neutral again first. But outlook will continue to stay bearish as long as 0.7860 support turned resistance holds, in case of another recovery.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

{kind=link}