Sterling trades broadly lower today after weaker-than-expected UK labor data strengthened expectations for a March rate cut from BoE. Rising unemployment and moderating wage growth have shifted the tone around policy outlook, particularly among more centrist MPC members who may now lean more dovish.

Traders are now assigning more than 75% probability to a March cut, while two rate cuts are fully priced by November. The repricing marks a clear pivot from earlier caution. Still, Sterling selling remains relatively restrained. Investors appear reluctant to extend bearish positions ahead of tomorrow’s CPI release, which could either validate or challenge the dovish shift. A softer inflation print would cement expectations for March action, while sticky services inflation could temper aggressive bets.

Beyond UK data, focus quickly shifts to Asia, where RBNZ delivers its rate decision. A hold at 2.25% is widely expected tomorrow, with consensus that policy is in prolonged pause phase following earlier easing. However, debate centers on timing of next move. More aggressive forecasters anticipate two hikes beginning in Q3 this year, while conservative views push normalization into early 2027. The divergence reflects uncertainty around durability of domestic recovery.

A key element will be how RBNZ addresses Q4 CPI at 3.1%, which surprised to upside. Markets will also scrutinize updated projections for signals that inflation risks are tilting higher or that slack remains sufficient to justify patience. A clear hawkish tilt in language or forecasts could lift Kiwi. Conversely, a cautious tone emphasizing spare capacity may dampen tightening expectations.

So far today, Yen leads gains, followed by Dollar and Kiwi. Sterling is weakest, trailed by Aussie and Euro, while Swiss Franc and Loonie sit in middle.

In Europe, at the time of writing, FTSE is up 0.33%. DAX is up 0.01%. CAC is down -0.04%. UK 10-year yield is down -0.042 at 4.36. Germany 10-year yield is down -0.027 at 2.731. Earlier in Asia, Nikkei fell -0.42%. Japan 10-year JGB yield fell -0.088 to 2.126. Hong Kong, China, and Singapore were on Lunar New Year holiday.

Canada CPI slows to 2.3% in January as gasoline drives deceleration

Canada’s headline CPI eased from 2.4% yoy to 2.3% yoy in January, slightly below expectations of unchanged inflation. The moderation was largely driven by gasoline prices, which fell -16.7% yoy following a -13.8% decline in December. The sharper drop at the pump was the main contributor to the slowdown in headline inflation.

However, underlying price pressures remain more resilient. Excluding gasoline, CPI rose 3.0% yoy, unchanged from December. Excluding food and energy, inflation edged down modestly to 2.4% yoy from 2.5%.

Core measures were mixed but generally softer. CPI Median slipped to 2.5% yoy from 2.6%, while CPI Trim declined more sharply to 2.4% yoy from 2.7%. CPI Common eased to 2.7% yoy from 2.8%.

Germany ZEW falls to 58.3 as recovery remains fragile

Germany’s ZEW Economic Sentiment index edged down from 59.6 to 58.3 in February, missing expectations of 65.2 but still pointing to cautious optimism. Current Situation index improved from -72.7 to -65.9, roughly in line with forecasts. At the Eurozone level, ZEW Economic Sentiment index fell from 40.8 to 39.4, undershooting expectations of 45.2. However, the Current Situation measure improved by 4.5 points to -13.6.

ZEW President Achim Wambach described the recovery as “fragile,” noting that structural challenges continue to weigh on industry and private investment. He emphasized that upcoming reforms to Germany’s social insurance system should be used to strengthen the country’s competitiveness as a business location.

Sector breakdown showed moderate to strong improvement in export-oriented industries, including chemicals and pharmaceuticals, steel and metals, and mechanical engineering, likely reflecting stronger incoming orders late last year. Private consumption prospects also improved, while banks, insurers, and IT sectors reported weaker expectations.

UK unemployment hits five-year high at 5.2%, wage growth slows

UK labor market data pointed to further cooling at the start of the year. Payrolled employment fell by -11k in January and is down -134k over the past 12 months, a -0.4% yoy decline.

Meanwhile, the January claimant count rose by 28.6k, above expectations of 22.8k, signaling rising pressures in the job market. Early estimates for January showed median monthly pay growth ticking up to 4.6% yoy from 4.4%.

In the three months to December, the unemployment rate increased from 5.1% to 5.2% — the highest level since 2020. Wage growth showed signs of moderation. Average earnings including bonus slowed to 4.2% yoy from 4.6%, undershooting expectations of 4.6%. Earnings excluding bonus eased to 4.2% yoy from 4.4%, in line with forecasts.

RBA minutes sees risks tilting toward tighter policy

Minutes of RBA’s February 3 meeting revealed that while the case for holding rates was considered, members ultimately saw a stronger argument for raising the cash rate by 25 bps to 3.85%. The decision reflected growing concern that inflation pressures may prove more persistent than previously anticipated.

The Board judged that part of the recent rise in inflation likely reflects sustained “capacity pressure”, and that financial conditions were “currently not restrictive enough ” to return inflation to target within a reasonable timeframe. Data received since the previous meeting strengthened the view that, “without a policy response, inflation could remain persistently above target for too long.”

Members also acknowledged that risks to both price stability and full employment objectives had “shifted materially”. Staff forecasts show inflation staying above the midpoint of the target range for at least two more years, based on a market-implied path that assumes two additional hikes in 2026. If realized, that would extend the already prolonged period during which underlying inflation has exceeded target. At the same time, downside risks to the labor market were seen as having diminished.

Still, policymakers stressed “prevailing uncertainties meant it was not possible to have a high degree of confidence in any particular path for the cash rate.” The minutes suggest the tightening bias remains intact, but future moves will hinge squarely on incoming data, particularly inflation and labor market developments.

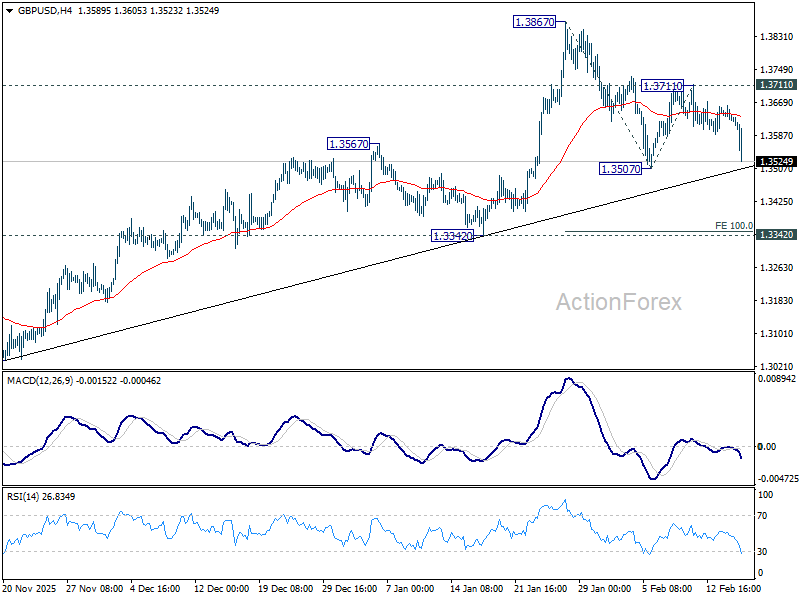

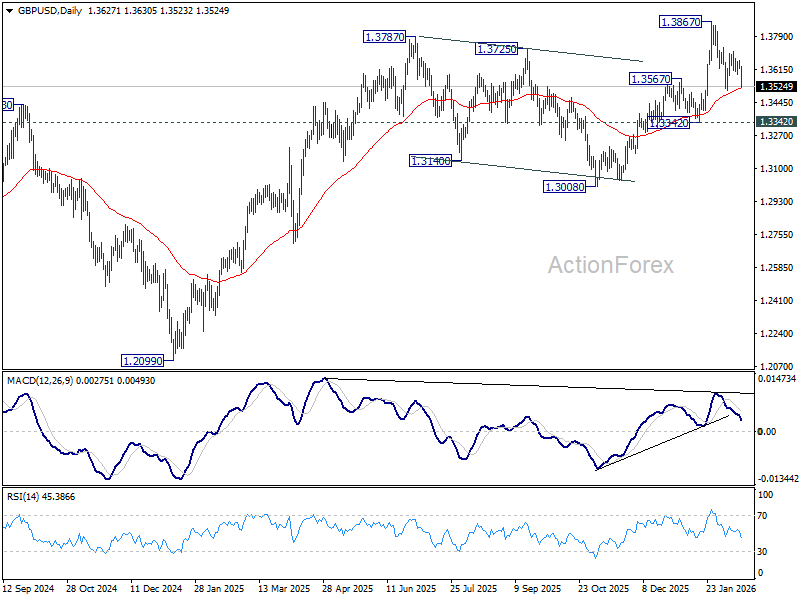

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3616; (P) 1.3639; (R1) 1.3653; More…

Immediate focus is now on 1.3507 support in GBP/USD with today’s downside acceleration. Firm break there and sustained trading below 55 D EMA (now at 1.3518) will raise the chance of larger scale correction. Deeper fall should then be seen to 1.3342 support for confirmation. On the upside, break of 1.3711 will bring retest of 1.3867 high.

In the bigger picture, rise from 1.0351 (2022 low) still in progress and should target 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

{kind=link}