Dollar jumped in early US session after jobless claims came in much stronger than expected, reinforcing signs of labor market resilience. The data added fresh fuel to a rally that had already begun following yesterday’s more hawkish-than-expected FOMC minutes. The greenback’s strength is most visible against European majors with EUR/USD sliding through the near-term low set in early February.

Markets appear to be getting more comfortable with the idea that Fed may not need to cut rates again in first half of year. The combination of firm labor data and cautious Fed tone raises the bar for further easing. yesterday’s FOMC minutes already suggested that additional cuts are far from automatic. The mention by some participants that rate hikes could even be discussed under certain inflation scenarios shifted perceived risk asymmetry back in favor of Dollar. Today’s labor figures reinforce that narrative. With initial jobless claims falling sharply, evidence of labor market deterioration remains limited. That reduces urgency for policy accommodation.

Besides, some uncertainty centers on leadership at Fed. US President Donald Trump’s nomination of Kevin Warsh to replace Jerome Powell is facing potential delays amid political standoff in Senate. If confirmation is prolonged, Powell could remain in role slightly longer than anticipated. Alternatively, Vice Chair Philip Jefferson could serve as acting chair during transition.

Either scenario could slow policy adjustments, as institutional continuity tends to favor stability over rapid change. That, in turn, may delay next rate cut even further.

For week so far, Dollar leads performance table and momentum is building. Aussie follows, supported by firm employment data. Loonie benefits from rebound in oil. Yen is now weakest after renewed selling, followed by Sterling and Kiwi, while Euro and Swiss Franc trade in middle of pack.

In Europe, at the time of writing, FTSE is down -0.57%. DAX is down -0.91%. CAC is down -0.76%. UK 10-year yield is up 0.008 at 4.383. Germany 10-year yield is up 0.009 at 2.752. Earlier in Asia, Nikkei rose 0.57%. Hong Kong and China were on holiday. Singapore Strait Times rose 1.28%. Japan 10-year JGB yield rose 0.001 to 2.141.

US initial jobless claims fall to 206k vs exp 229k

US initial jobless claims fell -23k to 206k in the week ending February 14, well below expectation of 229k. Four-week moving average of initial claims fell -1k to 219k.

Continuing claims rose 17k to 1,869k in the week ending February 7. Four-week moving average of continuing claims rose 1k to 1,845k.

BoE’s Mann: Inflation improving, but jobless rise ‘very much of a concern’

BoE MPC member Catherine Mann described this week’s inflation data as “good numbers,” though she cautioned that underlying pressures had not improved as much as policymakers had hoped. While headline CPI continues to slow, Mann signaled that the central bank remains focused on whether the disinflation trend is sustainable rather than temporary.

She pointed to the rise in unemployment as “very much of a concern”, added that the MPC is approaching a point where policy must carefully balance inflation control with labor market risks. That framing suggests internal debate is shifting from solely combating inflation toward weighing growth considerations more seriously.

However, Mann stopped short of endorsing a March rate cut. She questioned whether the projected fall of inflation toward 2% in coming months truly reflects a durable return to target.

Mann voted with the majority to hold rates in the recent 5-4 decision and indicated the time for a cut is drawing nearer.

Australia unemployment rate unchanged at 4.1%, jobs solid enough to keep RBA May hike in play

Australia added 17.8k jobs in January, slightly below expectations of 20.3k, but the details were firm. Full-time employment rose a strong 50.5k, while part-time positions fell -32.7k. Unemployment rate held steady at 4.1%, undershooting forecasts for a rise to 4.2%, with participation unchanged at 66.7%. Monthly hours worked increased 0.6% mom, reinforcing signs of steady labor demand.

The composition matters. The shift toward full-time employment and higher hours worked suggests underlying strength rather than softening. Taken together, the data indicate the labor market remains relatively tight, with the economy still operating close to capacity.

From the RBA’s perspective, the failure of employment conditions to weaken keeps inflation risks front and center. A cooling labor market would have allowed policymakers to shift focus toward growth risks. Instead, today’s figures reinforce the view that wage pressures may remain sticky.

The base case remains for another 25bps rate hike in May, pending Q1 CPI confirmation. Whether further tightening is needed beyond that remains an open question. But for now, the labor market is not providing the RBA with any comfort that inflation pressures will fade on their own.

RBNZ’s Silk: Growth and disinflation can coexist amid spare capacity

Following the RBNZ’s decision to keep the OCR at 2.25% yesterday, Assistant Governor Karen Silk emphasized that the economy can grow even as inflation moderates.

She acknowledged that the idea may appear counterintuitive but argued that the output gap provides room for above-trend growth without reigniting price pressures. But, according to Silk, the presence of spare capacity allows output to grow above potential temporarily without reigniting inflation.

Silk described risks around the projected cash-rate path as balanced. While some sectors are showing signs of recovery, consumption remains subdued. At the same time, she warned of upside inflation risks if firms facing squeezed margins begin raising prices more aggressively.

The RBNZ estimates the neutral cash rate at around 3%, suggesting policy is still accommodative. Current projections show only a gradual move toward that neutral level by late 2027. “That’s a reflection of that spare capacity that exists within the economy and the time it will take for that to be absorbed,” Silk said.

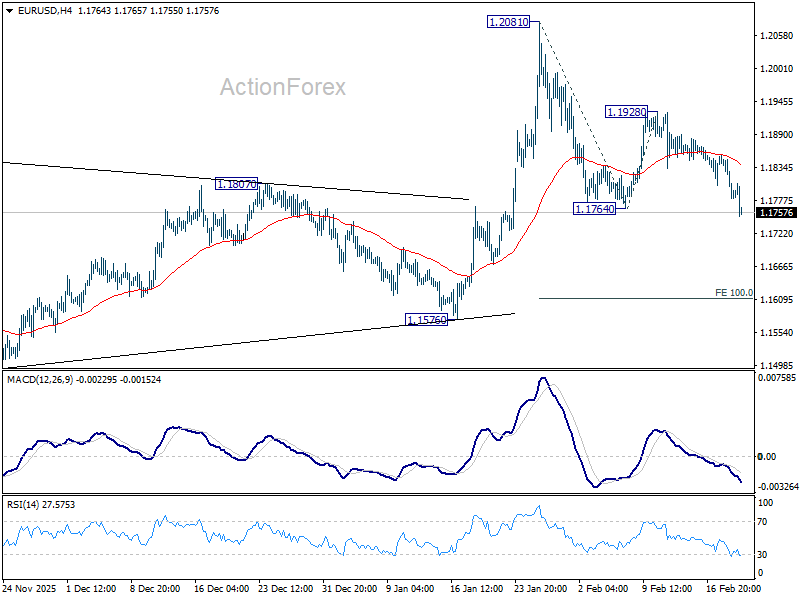

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1756; (P) 1.1808; (R1) 1.1833; More….

EUR/USD’s fall from 1.2081 resumed by breaking 11764 support and intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 1.1763) will raise the chance of reversal on rejection by 1.2, and target 1.1576 support for confirmation. For now, risk will stay mildly on the downside as long as 1.1928 resistance holds, in case of recovery.

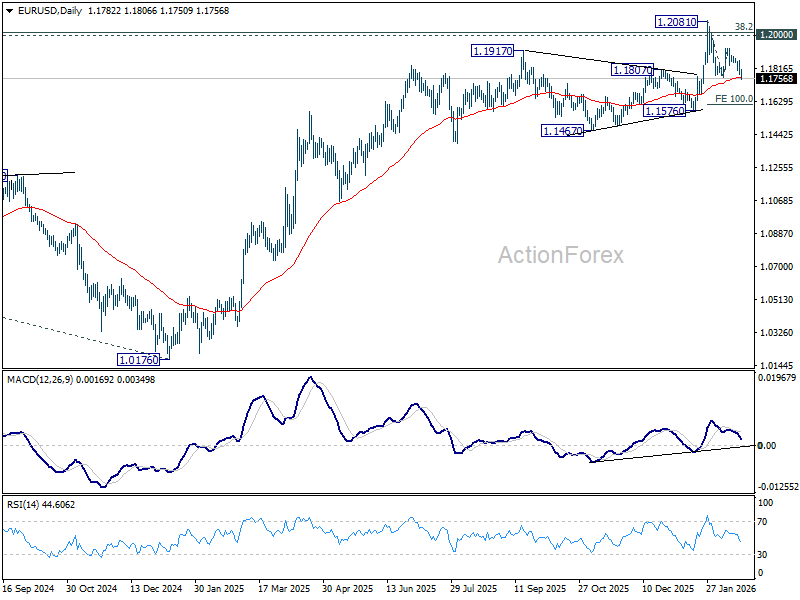

In the bigger picture, as long as 55 W EMA (now at 1.1485) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

{kind=link}